会计专业英语考试总结版

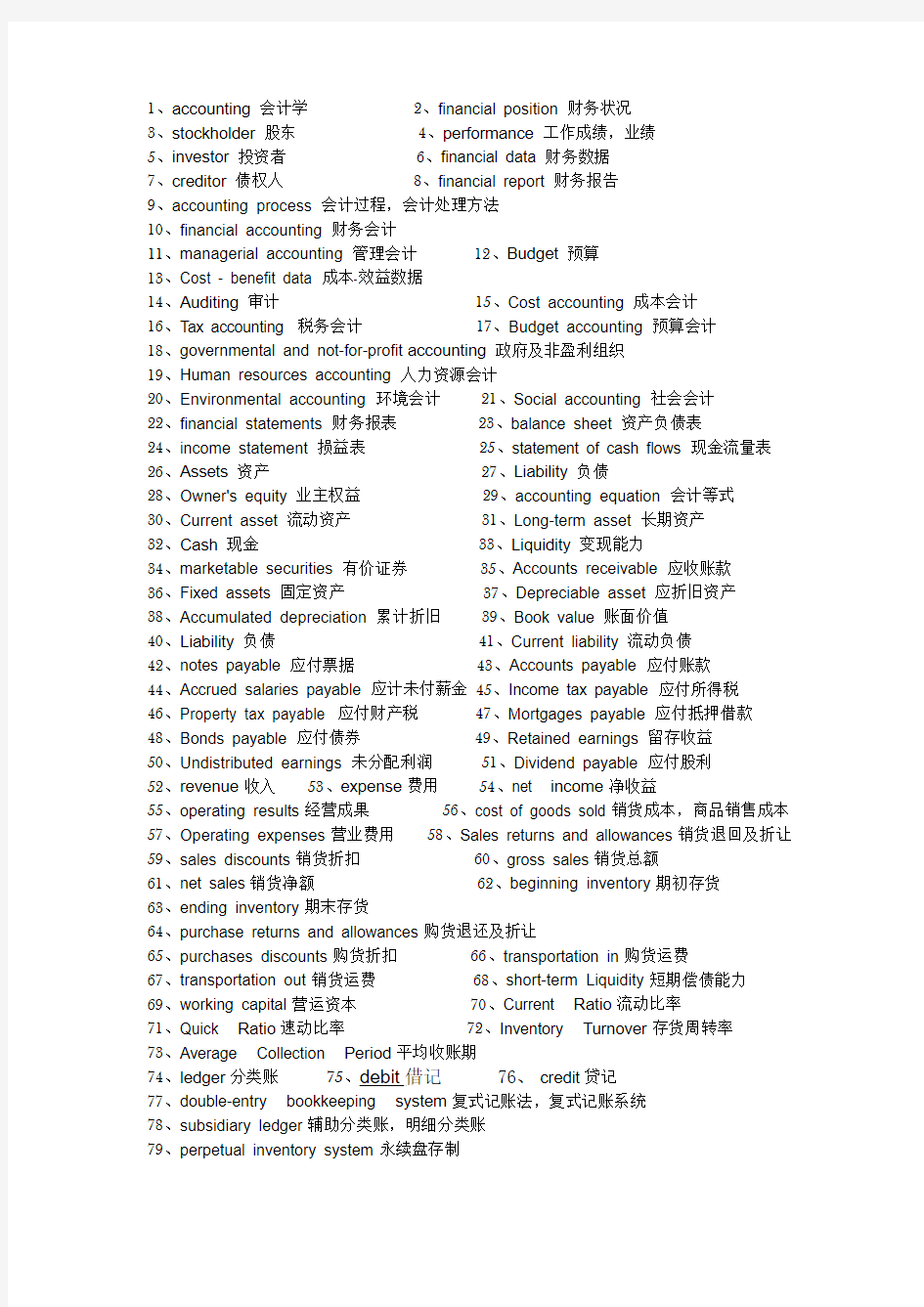

1、accounting会计学

2、financial position财务状况

3、stockholder股东

4、performance工作成绩,业绩

5、investor投资者

6、financial data财务数据

7、creditor债权人8、financial report财务报告

9、accounting process会计过程,会计处理方法

10、financial accounting财务会计

11、managerial accounting管理会计12、Budget预算

13、Cost - benefit data成本-效益数据

14、Auditing审计15、Cost accounting成本会计

16、Tax accounting 税务会计17、Budget accounting预算会计

18、governmental and not-for-profit accounting政府及非盈利组织

19、Human resources accounting人力资源会计

20、Environmental accounting环境会计21、Social accounting社会会计

22、financial statements财务报表23、balance sheet资产负债表

24、income statement损益表25、statement of cash flows现金流量表26、Assets资产27、Liability负债

28、Owner's equity业主权益29、accounting equation会计等式

30、Current asset流动资产31、Long-term asset长期资产

32、Cash现金33、Liquidity变现能力

34、marketable securities有价证券35、Accounts receivable应收账款

36、Fixed assets固定资产37、Depreciable asset应折旧资产

38、Accumulated depreciation累计折旧39、Book value账面价值

40、Liability负债41、Current liability流动负债

42、notes payable应付票据43、Accounts payable应付账款

44、Accrued salaries payable应计未付薪金45、Income tax payable应付所得税

46、Property tax payable 应付财产税47、Mortgages payable应付抵押借款48、Bonds payable应付债券49、Retained earnings留存收益

50、Undistributed earnings未分配利润51、Dividend payable应付股利

52、revenue收入53、expense费用54、net income净收益

55、operating results经营成果56、cost of goods sold销货成本,商品销售成本57、Operating expenses营业费用58、Sales returns and allowances销货退回及折让59、sales discounts销货折扣60、gross sales销货总额

61、net sales销货净额62、beginning inventory期初存货

63、ending inventory期末存货

64、purchase returns and allowances购货退还及折让

65、purchases discounts购货折扣66、transportation in购货运费

67、transportation out销货运费68、short-term Liquidity短期偿债能力

69、working capital营运资本70、Current Ratio流动比率

71、Quick Ratio速动比率72、Inventory Turnover存货周转率

73、Average Collection Period平均收账期

74、ledger分类账75、debit借记76、credit贷记

77、double-entry bookkeeping system复式记账法,复式记账系统

78、subsidiary ledger辅助分类账,明细分类账

79、perpetual inventory system永续盘存制

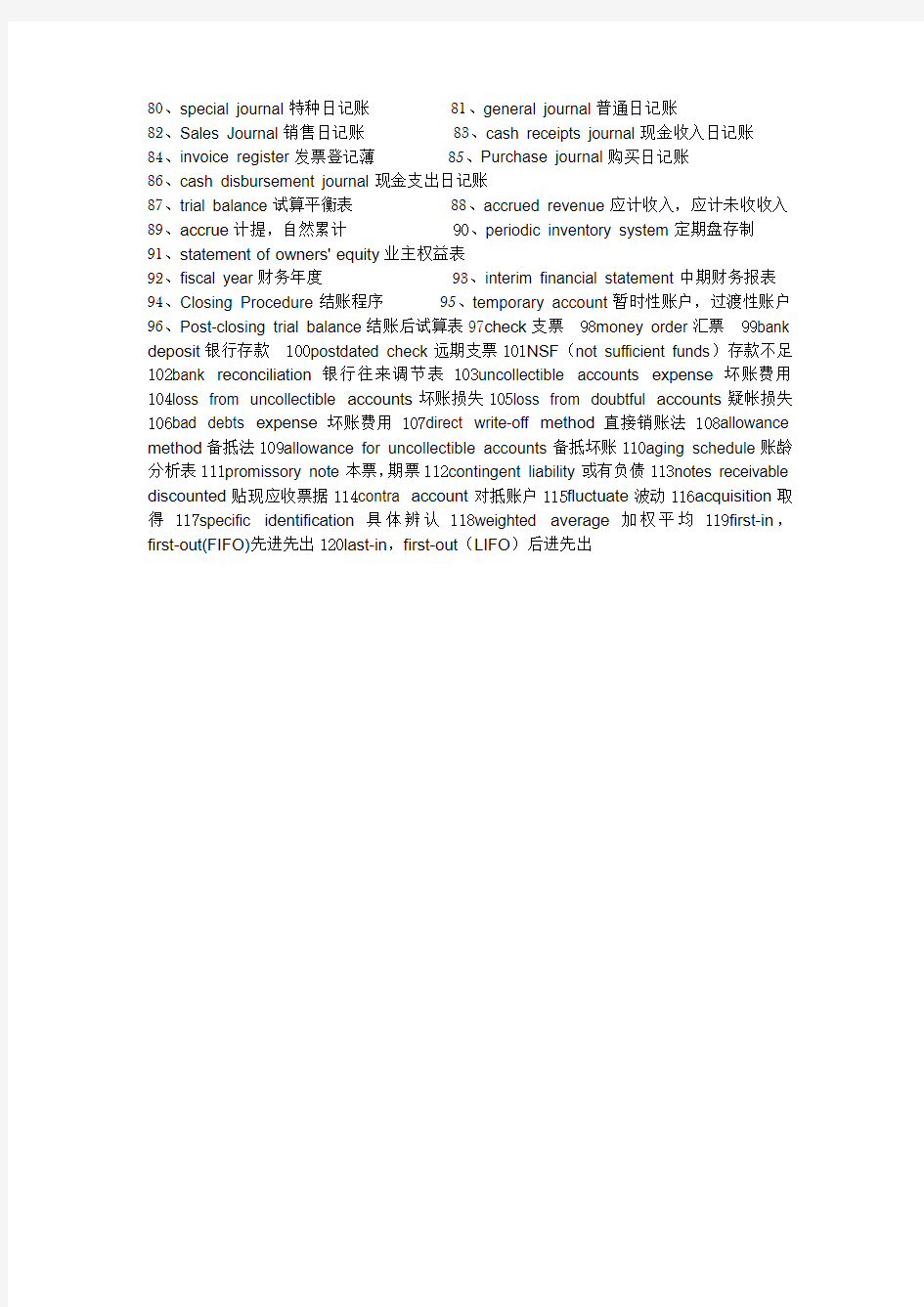

80、special journal特种日记账81、general journal普通日记账

82、Sales Journal销售日记账83、cash receipts journal现金收入日记账

84、invoice register发票登记薄85、Purchase journal购买日记账

86、cash disbursement journal现金支出日记账

87、trial balance试算平衡表88、accrued revenue应计收入,应计未收收入89、accrue计提,自然累计90、periodic inventory system定期盘存制

91、statement of owners'equity业主权益表

92、fiscal year财务年度93、interim financial statement中期财务报表94、Closing Procedure结账程序95、temporary account暂时性账户,过渡性账户96、Post-closing trial balance结账后试算表97check支票 98money order汇票 99bank deposit银行存款 100postdated check远期支票101NSF(not sufficient funds)存款不足102bank reconciliation银行往来调节表103uncollectible accounts expense坏账费用104loss from uncollectible accounts坏账损失105loss from doubtful accounts疑帐损失106bad debts expense坏账费用107direct write-off method直接销账法108allowance method备抵法109allowance for uncollectible accounts备抵坏账110aging schedule账龄分析表111promissory note本票,期票112contingent liability或有负债113notes receivable discounted贴现应收票据114contra account对抵账户115fluctuate波动116acquisition取得117specific identification具体辨认118weighted average加权平均119first-in,first-out(FIFO)先进先出120last-in,first-out(LIFO)后进先出

会计专业英语期末试题)

期期末测试题 Ⅰ、Translate The Following Terms Into Chinese . 1. entity concept 主题概念 2.depreciation折旧 3. double entry system 4.inventories 5. stable monetary unit 6.opening balance 7.current asset 8.financial report 9.prepaid expense 10.internal control 11.cash flow statement 12.cash basis 13.tangible fixed asset 14.managerial accounting 15. current liability 16.internal control 17.sales return and allowance 18.financial position 19.balance sheet 20.direct write-off method Ⅱ、Translate The Following Sentences Into Chinese . 1. Accounting is often described as an information system. It is the system that measures business activities, processes into reports and communicates these findings to decision makers. 2. The primary users of financial information are investors and creditors. Secondary users include the public, government regulatory agencies, employees, customers, suppliers, industry groups, labor unions, other companies, and academic researchers. 3. There are two sources of assets. One is liabilities and the other is owner’s equity. Liabilities are obligations of an entity arising from past transactions or events, the settlement of which may result in the transfer or use of assets or services in the future. 资产有两个来源,一个是负债,另一个是所有者权益。负债是由过去的交易或事件产生的实体的义务,其结算可能导致未来资产或服务的转让或使用。 4. Accounting elements are basic classification of accounting practices. They are essential units to present the financial position and operating result of an entity. In China, we have six groups of accounting elements. They are assets, liabilities, 可复制、编制,期待你的好评与关注!

会计专业英语翻译题知识分享

Account 、Accounting 和Accountant Account 有很多意思,常见的主要是“说明、解释;计算、帐单;银行帐户”。例如: 1、He gave me a full account of his plan。 他把计划给我做了完整的说明。 2、Charge it to my account。 把它记在我的帐上。 3、Cashier:Good afternoon。Can I help you ? 银行出纳:下午好,能为您做什么? Man :I’d like to open a bank account . 男人:我想开一个银行存款帐户。 还有account title(帐户名称、会计科目)、income account(收益帐户)、account book(帐簿)等。在account 后面加上词缀ing 就成为accounting ,其意义也相应变为会计、会计学。例如: 1、Accounting is a process of recording, classifying,summarizing and interpreting of those business activities that can be expressed in monetary terms. 会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程。 2、It has been said that Accounting is the language of business. 据说会计是“商业语言” 3、Accounting is one of the fastest growing profession in the modern business world. 会计是当今经济社会中发展最快的职业之一。 4、Financial Accounting and Managerial Accounting are two major specialized fields in Accounting. 财务会计和管理会计是会计的两个主要的专门领域。 其他还有accounting profession(会计职业)、accounting elements(会计要素)等。 Accountant 比Account只多ant三个字母,其意思是会计师、会计人员。例如: 1、A certified public accountant or CP A, as the term is usually abbreviated, must pass a series of examinations, after which he or she receives a certificate. 注册会计师(或,注册会计师的缩写),必须通过一系列考试方可取得证书。 2、Private accountant , also called executive or administrative accountant, handle the financial records of a business. 私人会计师,也叫做主管或行政会计师,负责处理公司的财务帐目。总之,这三个词,有很深的渊源关系。

会计专业英语重点1

Unit 1 Financial information about a business is needed by many outsiders .These outsiders include owners, bankers, other creditors, potential investors, labor unions, government agencies ,and the public ,because all these groups have supplied money to the business or have some other interest in the business that will be served by information about its financial position and operating results. 许多企业外部的人士需要有关企业的财务信息,这些外部人员包括所有者、银行家、其他债权人、潜在投资者、工会、政府机构和公众,因为这些群体对企业投入了资金,或享有某些利益,所以必须得到企业财务状况和经营成果信息。 Unit 2 Each proprietorship, partnership, and corporation is a separate entity. 每一独资企业、合伙企业和股份公司都是一个单独的主体。 In accrual accounting, the impact of events on assets and equities is recognized on the accounting records in the time periods when services are rendered or utilized instead of when cash is received or disbursed. That is revenue is recognized as it is earned, and expenses are recognized as they are incurred –not when cash changes hands .if the cash basis accounting were used instead of the accrual basis, revenue and expense recognition would depend solely on the timing of various cash receipts and disbursements. 在权责发生制下,视服务的提供而非现金的收付在本期对资产和权益的影响作出会计记录。即,收入是在赚取时确认,费用是在发生时确认——而不是在现金转手时。如果现金收付制替代权责发生制,那么收入和费用仅仅依靠各种现金收付活动的时间确定来确认。 Unit 3 During each accounting year ,a sequence of accounting procedures called the accounting cycle is completed. 在每一会计年度内,要依次完成被称为会计循环的会计程序。 Transactions are analyzed on the basis of the business documents known as source documents and are recorded in either the general journal or the special journal, i. e . the sales journal ,the purchases journal (invoice register ) ,cash receipts journal and cash disbursements journal . 根据业务凭证即原始凭证分析各项交易,并记入普通日记账或特种日记账,也就是销货日记账,购货日记账(发票登记簿),现金收入日记账和现金支出日记账。 A trial balance is prepared from the account balance in the ledger to prove the equality of debits and credits. 根据分类账户的余额编制试算平衡表,借以验证借项和贷项是否相等。 A T-account has a left-hand side and a right-hand side, called respectively the debit side and credit side. 一个T 型账户有左方和右方,分别称做借方和贷方。 After transactions are entered ,account balance (the difference between the sum of its debits and the sum of its credits ) can be computed.

会计专业英语模拟试题及答案

《会计专业英语》模拟试题及答案 一、单选题(每题1分,共20分) 1. Which of the following statements about accounting concepts or assumptions are correct? 1)The money measurement assumption is that items in accounts are initially measured at their historical cost. 2)In order to achieve comparability it may sometimes be necessary to override the prudence concept. 3)To facilitate comparisons between different entities it is helpful if accounting policies and changes in them are disclosed. 4)To comply with the law, the legal form of a transaction must always be reflected in financial statements. A 1 and 3 B 1 and 4 C 3 only D 2 and 3 Johnny had receivables of $5 500 at the start of 2010. During the year to 31 Dec 2010 he makes credit sales of $55 000 and receives cash of $46 500 from credit customers. What is the balance on the accounts receivables at 31 Dec 2010? $8 500 Dr $8 500 Cr $14 000 Dr $14 000 Cr Should dividends paid appear on the face of a company’s cash flow statement? Yes No Not sure Either Which of the following inventory valuation methods is likely to lead to the highest figure for closing inventory at a time when prices are dropping? Weighted Average cost First in first out (FIFO) Last in first out (LIFO) Unit cost 5. Which of following items may appear as non-current assets in a company’s the statement of financial position? (1) plant, equipment, and property (2) company car (3) €4000 cash (4) €1000 cheque A. (1), (3) B. (1), (2) C. (2), (3)

会计专业词汇英语翻译

会计专业词汇英语翻译 今天是2011年8月5日星期五2011年8月4日星期四| 首页| 财经英语| 视听| 课堂| 资源| 互动| 动态| 在线电影| 英语论坛| 英语角| 8 您现在的位置:西财英语>>财经英语学习>>会计英语>>文章正文 专题栏目 财经词汇 文献专题 财经词汇 文献专题 最新热门 母亲节专题 会计英语词汇漫谈(六) 会计英语词汇漫谈(五) 金融专业名词翻译(八) 金融专业名词翻译(七) 商务英语口语(十四) 商务英语口语(十三) 席慕容《一棵开花的树》(… 放松,微笑,创造 [图文]跳舞学数学函数图象… 最新推荐 体育英语——水上运动英语 外贸常用词语和术语(五) 外贸常用词语和术语(四) 商务英语email高手如何询… 外贸常用词语和术语(三) 外贸常用词语和术语(二) 外贸常用词语和术语(一) 外国经典名著导读《完》附… 外国经典名著导读31-40 外国经典名著导读21-30

相关文章 会计英语词汇漫谈(六) 会计英语词汇漫谈(五) 会计英语词汇漫谈(四) 会计专业词汇英语翻译 政治风险political risk 再开票中心re-invoicing center 现代管理会计专门方法special methods of modern management accounting 现代管理会计modern management accounting 提前与延期支付Leads and Lags 特许权使用管理费fees and royalties 跨国资本成本的计算the cost of capital for foreign investments 跨国运转资本会计multinational working capital management 跨国经营企业业绩评价multinational performance evaluation 经济风险管理managing economic exposure 交易风险管理managing transaction exposure 换算风险管理managing translation exposure 国际投资决策会计foreign project appraisal 国际存货管理international inventory management 股利转移dividend remittances 公司内部贷款inter-company loans 冻结资金转移repatriating blocked funds 冻结资金保值maintaining the value of blocked funds 调整后的净现值adjusted net present value 配比原则matching 旅游、饮食服务企业会计accounting of tourism and service 施工企业会计accounting of construction enterprises 民航运输企业会计accounting of civil aviation transportation enterprises 企业会计business accounting 商品流通企业会计accounting of commercial enterprises 权责发生制原则accrual basis 农业会计accounting of agricultural enterprises 实现原则realization principle 历史成本原则principle of historical cost 外商投资企业会计accounting of enterprises with foreign investment 通用报表all-purpose financial statements 铁路运输企业会计accounting of rail way transportation enterprises

会计专业英语翻译

. 1. Accounting first is an economic calculation. Economic calculation includes both static phenomenon on the economy's stock of the situation, including the situation of the period of dynamic flow, including both pre-calculated plan, but also after the actual calculation. Accounting is a typical example of economic calculation, calculation of economic calculation in addition to accounting, which includes statistical computing and business computing. 2. Accounting is an economic information systems. It would be a company dispersed into the business activities of a group of objective data, providing the company's performance, problems, and enterprise funds, labor, ownership, income, costs, profits, debt, and other information. Clearly, the accounting is to provide financial information-based economy information systems, business is the licensing of a points, thus accounting has been called "corporate language." 3. Accounting is an economic management.The accounting is social production develops to a certain stage of the product development and production is to meet the needs of the management, especially with the development of the commodity economy and the emergence of competition in the market through demand management on the economy activities strict control and supervision. At the same time, the content and form of accounting constantly improve and change, from a purely accounting, scores, mainly for accounting operations, external submit accounting statements, as in prior operating forecasts, decision-making, on the matter of economic activities control and supervision, in hindsight, check. Clearly, accounting whether past, present or future, it is people's economic management activities.

《财会专业英语》期末试卷及答案

《财会专业英语》期终试卷 I.Put the following into corresponding groups. (15 points) 1.Cash on hand 2.Notes receivable 3.Advances to suppliers 4. Other receivables 5.Short-term loans 6.Intangible assets 7.Cost of production 8.Current year profit 9. Capital reserve 10.Long-term loans 11.Other payables 12. Con-operating expenses 13.Financial expenses 14.Cost of sale 15. Accrued payroll II.Please find the best answers to the following questions. (25 Points) 1. Aftin Co. performs services on account when Aftin collects the account receivable A.assets increase B.assets do not change C.owner’s equity d ecreases D.liabilities decrease 2. A balance sheet report . A. the assets, liabilities, and owner’s equity on a particular date B. the change in the owner’s capital during the period C. the cash receipt and cash payment during the period D. the difference between revenues and expenses during the period 3. The following information about the assets and liabilities at the end of 20 x 1 and 20 x 2 is given below: 20 x 1 20 x 2 Assets $ 75,000 $ 90,000 Liabilities 36,000 45,000 how much the owner’sequity at the end of 20 x 2 ? A.$ 4,500 B.$ 6,000 C.$ 45,000 D.$ 43,000

会计英语试题及复习资料

会计英语试题及答案 会计专业英语是会计专业人员职业发展的必要工具。学习会计专业英语就是学习如何借助英语解决与完成会计实务中涉外的专业性问题和任务。以下为你收集了会计英语练习题及答案,希望给你带来一些参考的作用。 一、单选题 1. ? 1) . 2) . 3) . 4) , a . A 1 3 B 1 4 C 3 D 2 3 2. $5 500 2010. 31 2010 $55 000 $46 500 . 31 2010? A. $8 500 B. $8 500 C. $14 000 D. $14 000 3. a ’s ? A. B. C. D. 4. a ? A. B. () C. () D. 5. a ’s ? (1) , , (2) (3) 4000 (4) 1000 A. (1), (3) B. (1), (2) C. (2), (3) D. (2), (4)

6. a ’s ? (1) (2) . (3) . (4) A (1), (2) (3) B (1), (2) (4) C (1), (3) (4) D (2), (3) (4) 7. 30 2010 : $992,640 $1,026,480 , , ? 1. $6,160 . 2. $27,680 a . 3. $6,160 a . 4. $21,520 . A 1 2 B 2 3 C 2 4 D 3 4 8. . (1) (2) (3) (4) ? A (1), (3) (4) B (1), (2) (4) C (1), (2) (3) D (2), (3) (4) ( = [])({ : "u3054369" }); 9. ? (1) , (2) a (3) , A. 2 3 B. C. 1 2 D. 3 10. ? (1)

(完整版)会计专业英语重点词汇大全

?accounting 会计、会计学 ?account 账户 ?account for / as 核算 ?certified public accountant / CPA 注册会计师?chief financial officer 财务总监?budgeting 预算 ?auditing 审计 ?agency 机构 ?fair value 公允价值 ?historical cost 历史成本?replacement cost 重置成本?reimbursement 偿还、补偿?executive 行政部门、行政人员?measure 计量 ?tax returns 纳税申报表 ?tax exempt 免税 ?director 懂事长 ?board of director 董事会 ?ethics of accounting 会计职业道德?integrity 诚信 ?competence 能力 ?business transaction 经济交易?account payee 转账支票?accounting data 会计数据、信息?accounting equation 会计等式?account title 会计科目 ?assets 资产 ?liabilities 负债 ?owners’ equity 所有者权益 ?revenue 收入 ?income 收益

?gains 利得 ?abnormal loss 非常损失 ?bookkeeping 账簿、簿记 ?double-entry system 复式记账法 ?tax bearer 纳税人 ?custom duties 关税 ?consumption tax 消费税 ?service fees earned 服务性收入 ?value added tax / VAT 增值税?enterprise income tax 企业所得税?individual income tax 个人所得税?withdrawal / withdrew 提款、撤资?balance 余额 ?mortgage 抵押 ?incur 产生、招致 ?apportion 分配、分摊 ?accounting cycle会计循环、会计周期?entry分录、记录 ?trial balance试算平衡?worksheet 工作草表、工作底稿?post reference / post .ref过账依据、过账参考?debit 借、借方 ?credit 贷、贷方、信用 ?summary/ explanation 摘要?insurance 保险 ?premium policy 保险单 ?current assets 流动资产 ?long-term assets 长期资产 ?property 财产、物资 ?cash / currency 货币资金、现金

会计英语试题及答案

精品文档 会计英语试题及答案 会计专业英语是会计专业人员职业发展的必要工具。学 习会计专业英语就是学习如何借助英语解决与完成会计实务中涉外的专业性问题和任务。以下为你收集了会计英语练习题及答案,希望给你带来一些参考的作用。 一、单选题 1. Which of the following statements about accounting concepts or assumptions are correct? 1) The money measurement assumption is that items in accounts are initially measured at their historical cost. 2) In order to achieve comparability it may sometimes be necessary to override the prudence concept. 3) To facilitate comparisons between different entities it is helpful if accounting policies and changes in them are disclosed. 4) To comply with the law, the legal form of a transaction must always be reflected in financial statements. A 1 and 3 B 1 and 4 C 3 only D 2 and 3 2. Johnny had receivables of $5 500 at the start of 2010. During the year to 31 Dec 2010 he makes credit sales of $55 000 and receives cash of $46 500 from credit 2016 全新精品资料-全新公文范文-全程指导写作–独家

会计专业英语-模拟题

《会计专业英语》模拟题 一.单选题 1.The Realization Principle indicates that revenue usually should be recognized and recorded in the accounting record(). A.when goods are sole or services are rendered to customers B.when cash is collected from customers C.at the end of the accounting period D.only when the revenue can be matched by an equal dollar amount of expenses [答案]:A 2.The Matching Principle:(). A.applies only to situations in which a cash payment occurs before an expense is recognized B.applies only to situations in which a cash receipt occurs before revenue is recognized C.is used in accrual accounting to determine the proper period for recognition of expenses D.is used in accrual accounting to determine the proper period in which to recognize revenue [答案]:C 3.Xxx company paid $2850 on account. The effect of this transaction on the accounting equation is to (). A.decrease assets and decrease owner’s equity B.increase liabilities and decrease owner’s equity C.have no effect on total assets D.decrease assets and decrease liabilities [答案]:D 4.Which of the following concepts belongs to accounting assumption?(). A.Conservation B.Money measurement C.Materiality D.Consistency [答案]:B 5.Which of these is/are an example of an asset account?___ A.service revenue B.withdrawals C.supplies D.all of the above [答案]:C 6.Which of these statements is false?(). A.increase in assets and increase in revenues are recorded with a debit B.increase in liabilities and increase in owner’s equity are recorded with a c redit

财务管理专业英语期末复习

财务管理专业英语期末重点 一、单词 Topic1 财务管理financial management 资本预算capital budgeting 资本结构capital structure 股利政策dividend policy 存货inventory 风险规避risk aversion 股东权益stockholder s’ equity 流动负债current liability Topic2 财务风险financial risk 合伙制企业partnership 私人业主制企业sole proprietorship 收入revenue 主计长controller 财务困境financial distress 股票期权stock option 首次公开发行股票(IPO) initial public offering Topic 3 盈利能力profitability 偿付能力solvency 利润表income statement 有价证券marketable securities 提款withdrawal 应收账款accounts receivable 递延税款deferred tax Topic4 流动性比率liquidity ratio 权益乘数equity multiplier 资产收益率(ROA) return on assets 毛利gross profit margin 权益报酬率return on equity 市盈率P/E ratio 杠杆比率leverage ratio 息税前盈余(EBIT) earnings before interest and taxes Topic5 货币时间价值time value of money 年金annuity 折现率discount rate 机会成本opportunity cost

会计学专业会计英语试题

一、words and phrases 1.残值 scrip value 2.分期付款 installment 3.concern 企业 4.reversing entry 转回分录 5.找零 change 6.报销 turn over 7.past due 过期 8.inflation 通货膨胀 9.on account 赊账 10.miscellaneous expense 其他费用 11.charge 收费 12.汇票 draft 13.权益 equity 14.accrual basis 应计制15.retained earnings 留存收益 16.trad-in 易新,以旧换新 17.in transit 在途 18.collection 托收款项 19.资产 asset 20.proceeds 现值 21.报销 turn over 22.dishonor 拒付 23.utility expenses 水电费 24.outlay 花费 25.IOU 欠条 26.Going-concern concept 持续经营 27.运费 freight 二、Multiple-choice question 1.Which of the following does not describe accounting? ( C ) A. Language of business B. Useful ofr decision making C. Is an end rathe than a means to an end. https://www.360docs.net/doc/761092859.html,ed by business, government, nonprofit organizations, and individuals. 2.An objective of financial reporting is to ( B ) A. Assess the adequacy of internal control. B.Provide information useful for investor decisions. C.Evaluate management results compared with standards. D.Provide information on compliance with established procedures. 3.Which of the following statements is(are) correct?( B ) A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets. B.A company may use different depreciation methods in its financial statements and its income tax return. C.The cost of a machine includes the cost of repairing damage to the machine during the installation process. D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method. 4. Which of the following is(are) correct about a company’s balance sheet? ( B ) A.It displays sources and uses of cash for the period. B.It is an expansion of the basic accounting equation C.It is not sometimes referred to as a statement of financial position. D.It is unnecessary if both an income statement and statement of cash flows are availabe. 5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A ) https://www.360docs.net/doc/761092859.html,rmation used to determine which products to poduce https://www.360docs.net/doc/761092859.html,rmation about economic resources, claims to those resources, and changes in both resources and claims. https://www.360docs.net/doc/761092859.html,rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows. https://www.360docs.net/doc/761092859.html,rmation that is useful in making ivestment and credit decisions. 6.Each of the following measures strengthens internal control over cash receipts except. ( C ) A.The use of a petty cash fund. B.Preparation of a daily listing of all checks received through the mail. C.The use of cash registers. D.The deposit of cash receipts in the bank on a daily basis. 7.The primary purpose for using an inventory flow assumption is to. ( A )