财管专业——《管理会计(双语)》

《管理会计》课件全英文Acct_ch1_ManAcct_(Feb_25)

1. Externally focused 2. Must follow externally imposed rules 3. Objective financial information

1 -23

Types of Information

For management accounting, the The restrictions imposed on financial accounting tend to financial or nonfinancial produce objectivebe much more information may and verifiable financial information. subjective in nature.

Continued

1 -3

Objectives

5. Describe the role of management accountants in an organization. 6. Explain the importance of ethical behavior for managers and management accountants. 7. List three forms of certification available to management accountants.

1 -12

Management Process

The Management Process is defined by the following activities: Planning Controlling Decision Making

Decision making is the process of choosing among competing alternatives.

管理会计双语第5章

Sales level at which operating income is zero Sales above breakeven result in a profit Sales below breakeven result in a loss Two methods: Income statement approach Contribution margin approach

Units produced Direct materials cost per unit Total direct materials cost

100 200 300

$120 $60 $40

12,000 12,000 12,000

400

500

$30

$24

12,000

12,000

Committed fixed costs represent investments with a

Contribution margin is used first to cover fixed expenses.

Any remaining contribution margin contributes to net operating income.

Sales revenue per unit

Fixed costs Contribution margin ratio

Breakeven point in sales dollars

$20,000 $15,000

Dollars

$10,000 $5,000 $0 0 500

•

Revenues

1,000

1,500

Volume of Units

大学会计类专业阅读书籍推荐

大学会计类专业的学生推荐的阅读书籍•《会计原理》(Accounting Principles):作者是美国著名的会计学家韦伯,是会计领域的经典教材之一。

该书系统地阐述了会计的基本概念、原则和方法,适合作为入门读物。

•《会计基础》(Financial Accounting):作者是美国著名的会计学家韦尔斯,这本书被广泛用于大学本科的会计课程。

它详细介绍了财务会计的基本概念、原则和实务操作,对于理解财务报表的编制和分析非常有帮助。

•《管理会计》(Management Accounting):作者是美国著名的管理会计学家安东尼,本书对管理会计的概念、原则、方法、技巧等方面进行了全面深入的探讨。

它有助于理解企业在管理决策中如何运用会计信息。

•《会计研究方法》(Research Methods in Accounting):同样是安东尼所著,这本书详细介绍了会计研究的各种方法和技巧,对于进行会计研究或撰写相关论文的学生非常有用。

•《成本会计学》:作者是中国著名的成本会计学专家李冠英教授,本书介绍了成本会计的基本概念、原则、方法和技巧,涵盖了成本核算、成本控制、成本分析等方面的内容。

对于理解企业的成本管理和决策非常有帮助。

此外,还有以下一些值得一读的会计类书籍:•《公司理财》(Corporate Finance):作者是斯蒂芬A.罗斯等人,这本书是财务管理学的权威著作,涵盖了公司理财的所有核心问题,如资产定价、融资工具和筹资决策、资本结构和股利分配政策等。

它有助于理解企业的财务决策和资本运作。

•《让数字说话》(Numbers Rule Your World):这本书通过生动的案例和深入的分析,展示了数字在商业世界中的重要作用。

它有助于培养会计专业学生的数据分析和决策能力。

•《手把手教你读财报》(How to Read a Financial Report):作者唐朝详细介绍了如何阅读和理解企业的财务报表,包括资产负债表、利润表和现金流量表等。

《财务管理学》课程中英文简介

《财务管理学》课程中英文简介Corporate Finance课程代码:040013A/040013B Course Code:040025A/040015A/040012B 040025A/040015A /040012B 040025A/040015A课程名称:财务管理学Course Name:Corporate Finance学时:48/32/80 Periods:48/32/80学分:3/2/5 Credits:3/2/5考核方式:考查/考试Assessment:Inspection/Examination先修课程: Preparatory Courses:成本管理会计学(上)MA1 Management AccountingⅠ本课程就是国际会计专业方向的基础财务管理学课程,主要讲授的就是财务经理在进行投资、筹资与日常营运管理过程中如何进行财务决策,才能实现股东财富最大化这一企业理财目标。

先修课程为管理会计基础(MA1)。

该课程主要包括以下内容:(1)财务管理学简介; (2)财务环境与其组成要素分析。

(3)证券估价。

(4)利息率与汇率的确定:利息率的影响因素与确定步骤、利率期限结构、风险溢价、汇率的影响因素、购买力平价理论与利率平价理论。

(5)战略决策——资本预算:主要讲授项目现金流的确定、资本预算方法与决策标准、内部报酬率法的优缺点分析、资本限额决策、资本预算决策中的风险分析。

(6)战略决策——资本成本:主要讲授资本结构、个别资本成本(包括债券、优先股、普通股)与综合资本成本的确定。

(7)经营决策——营运资本管理:主要讲授营运资本筹资决策、存货、应收帐款的管理。

(8)财务计划:主要讲授财务计划(或资金需求计划)的编制与分析。

Corporate Finance Fundamentals [FN1] is a fundamental course in managerial finance with an emphasis on the major decisions to be made by the financial executive of an organization、Topics introduced in FN1 include the following parts:Part 1 Introduction to the corporate finance; Part 2 The financial environment,including the financial system, the major intermediaries and the specialized markets; Part 3 Security valuation: Risk-free assets, including the interest rate as an opportunity cost, varying compound intervals and annuities; Part 4 The determinants of interest rates, including the determinants of interest rates, term structure effects; Part 5 Security valuation: Risk-adjusted discount rates, including the determinants of equity prices, the relationship between the price and the expected return; Part 6 Strategic decisions: Capital budgeting and cash flow estimation, including the capital budgeting process, estimating cash flows; Part 7 Strategic decisions: Capital budgeting evaluation criteria, including the NPV rule measures shareholder wealth, alternative capital budgeting criteria; Part 8 Financial planning, including Important elements in financial planning and the benefits of financial planning、《财务管理学》课程中英文简介Financial Management课程代码:040015A Course Code:040015A课程名称:财务管理学Course Name:Financial Management学时:80 Periods:80学分:5 Credits:5考核方式:考试Assessment:Examination先修课程:会计学基础Preparatory Courses:Accounting 财务管理学就是会计学与注册会计师专业的学科基础课,开设本课程的主要任务就是加强学生对财务管理理论与实务的全面、深入了解,培养学生课堂讨论与课外阅读与写作的习惯,引导学生对有关现代企业财务管理问题进行思考,从而培养出适应市场经济需要的中级理财者。

管理会计双语版总结PPT

第四页,共七十三页。

Chapter 3 :Determining Costs of Products

Job order costing

Direct material : trace Direct labor : trace Manufacturing overhead : allocate

Cost pool and allocation base Actual cost system vs. normal cost system Over-apply vs. under-apply

Three formulas (page 136)

Sensitivity analysis

8 第九页,共七十三页。

CVP Equations

Sales – Variable Costs – Fixed Costs = target profit

(SP/unit * units) – (VC/unit * units) – FC = target profit

Chapter 1: Introduction

Why management accounting? Origin and evolution of management

accounting Contrasting financial and management

accounting Ethical standards for management

Accounting rate of return

17

第十八页,共七十三页。

Chapter 9 : The Operating Budget

Different approaches to budgeting

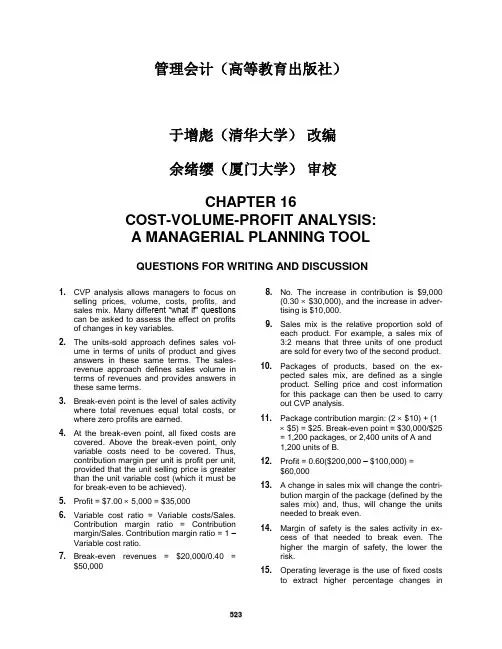

管理会计(英文版)课后习题答案(高等教育出版社)chapter 16

管理会计(高等教育出版社)于增彪(清华大学)改编余绪缨(厦门大学)审校CHAPTER 16COST-VOLUME-PROFIT ANALYSIS: A MANAGERIAL PLANNING TOOL QUESTIONS FOR WRITING AND DISCUSSION1.CVP analysis allows managers to focus onselling prices, volume, costs, profits, and sales mix. Many diffe rent “what if” questions can be asked to assess the effect on profits of changes in key variables.2.The units-sold approach defines sales vo-lume in terms of units of product and gives answers in these same terms. The sales-revenue approach defines sales volume in terms of revenues and provides answers in these same terms.3.Break-even point is the level of sales activitywhere total revenues equal total costs, or where zero profits are earned.4.At the break-even point, all fixed costs arecovered. Above the break-even point, only variable costs need to be covered. Thus, contribution margin per unit is profit per unit, provided that the unit selling price is greater than the unit variable cost (which it must be for break-even to be achieved).5.Profit = $7.00 ⨯ 5,000 = $35,0006.Variable cost ratio = Variable costs/Sales.Contribution margin ratio = Contribution margin/Sales. Contribution margin ratio = 1 –Variable cost ratio.7.Break-even revenues = $20,000/0.40 =$50,0008.No. The increase in contribution is $9,000(0.30 ⨯ $30,000), and the increase in adver-tising is $10,000.9.Sales mix is the relative proportion sold ofeach product. For example, a sales mix of3:2 means that three units of one productare sold for every two of the second product.10.Packages of products, based on the ex-pected sales mix, are defined as a singleproduct. Selling price and cost informationfor this package can then be used to carryout CVP analysis.11.Package contribution margin: (2 ⨯ $10) + (1⨯ $5) = $25. Break-even point = $30,000/$25= 1,200 packages, or 2,400 units of A and1,200 units of B.12.Profit = 0.60($200,000 – $100,000) =$60,00013. A change in sales mix will change the contri-bution margin of the package (defined by thesales mix) and, thus, will change the unitsneeded to break even.14.Margin of safety is the sales activity inexcess of that needed to break even. Thehigher the margin of safety, the lower therisk.15.Operating leverage is the use of fixed coststo extract higher percentage changes inprofits as sales activity changes. It isachieved by increasing fixed costs while lo-wering variable costs. Therefore, increasedleverage implies increased risk, and viceversa.16.Sensitivity analysis is a “what if” techniquethat examines the impact of changes in un-derlying assumptions on an answer. A com-pany can input data on selling prices, varia-ble costs, fixed costs, and sales mix and setup formulas to calculate break-even pointsand expected profits. Then, the data can bevaried as desired to see what impactchanges have on the expected profit.17.By specifically including the costs that varywith nonunit drivers, the impact of changesin the nonunit drivers can be examined. Intraditional CVP, all nonunit costs are lumpedtogether as “fixed costs.” While the costs arefixed with respect to units, they vary with re-spect to other drivers. ABC analysis remindsus of the importance of these nonunit driversand costs.18.JIT simplifies the firm’s cost equation sincemore costs are classified as fixed (e.g., di-rect labor). Additionally, the batch-level vari-able is gone (in JIT, the batch is one unit).Thus, the cost equation for JIT includes fixedcosts, unit variable cost times the number ofunits sold, and unit product-level cost timesthe number of products sold (or related cost driver). JIT means that CVP analysis ap-proaches the standard analysis with fixed and unit-level costs only.EXERCISES 16–11. e2. c3. d4. b5. a16–21. f2. d3. b4. a5. g6. e7. c16–31. Units = Fixed cost/Contribution margin= $10,350/($15 – $12)= 3,4502. Sales (3,450 ⨯ $15) $51,750Variable costs (3,450 ⨯ $12) 41,400Contribution margin $ 10,350Fixed costs 10,350Operating income $ 03. Units = (Target income + Fixed cost)/Contribution margin= ($9,900 + $10,350)/($15 – $12)= $20,250/$3= 6,7501. Contribution margin per unit = $15 – $12 = $3Contribution margin ratio = $3/$15 = 0.20, or 20%2. Variable cost ratio = $60,000/$75,000 = 0.80, or 80%3. Revenue = Fixed cost/Contribution margin ratio= $10,350/0.20= $51,7504. Revenue = (Target income + Fixed cost)/Contribution margin ratio= ($9,900 + $10,350)/0.20= $101,25016–51. 0.15($15)(Units) = $15(Units) – $12(Units) – $10,350$2.25(Units) = $3(Units) – $10,350$10,350 = $0.75(Units)Units = 13,8002. Sales (13,800 ⨯ $15) $ 207,000Variable costs (13,800 ⨯ $12) 165,600Contribution margin $ 41,400Fixed costs 10,350Operating income $ 31,050$31,050 does equal 15% of $207,000, so the answer of 13,800 units is correct.1. Before-tax income = (After-tax income)/(1 – Tax rate)= $6,000/(1 – 0.40)= $10,000Units = (Target income + Fixed cost)/Contribution margin= ($10,000 + $10,350)/($15 – $12)= 6,783**The answer is 6,783.3333, and so it must be rounded to a whole unit. You may prefer that students round up the answer to 6,784, instead, since it is better to be marginally above break-even than marginally below it.2. Before-tax income = (After-tax income)/(1 – Tax rate)= $6,000/(1 – 0.50)= $12,000Units = (Target income + Fixed cost)/Contribution margin= ($12,000 + $10,350)/($15 – $12)= 7,4503. Before-tax income = (After-tax income)/(1 – Tax rate)= $6,000/(1 – 0.30)= $8,571Units = (Target income + Fixed cost)/Contribution margin= ($8,571 + $10,350)/($15 – $12)= 6,30716–71. Break-even units = Fixed costs/(Price – Variable cost)= $150,000/($2.45 – $1.65)= $150,000/$0.80= 187,5002. Units = ($150,000 + $12,600)/($2.45 – $1.65)= $162,600/$0.80= 203,2503. Unit variable cost = $1.65Unit variable manufacturing cost = $1.65 – $0.17 = $1.48The unit variable cost is used in cost-volume-profit analysis, since it includes all of the variable costs of the firm.1. Before-tax income = $25,200/(1 – 0.40) = $42,000Units = ($150,000 + $42,000)/$0.80= $192,000/$0.80= 240,0002. Before-tax income = $25,200/(1 – 0.30) = $36,000Units = ($150,000 + $36,000)/$0.80= $186,000/$0.80= 232,5003. Before-tax income = $25,200/(1 – 0.50) = $50,400Units = ($150,000 + $50,400)/$0.80= $200,400/$0.80= 250,5004. 215,000 – 187,500 = 27,500 pansor$526,750 – $459,375 = $67,375A B C D Sales $ 5,000 $ 15,600* $ 16,250* $9,000 Variable costs 4,000 11,700 9,750 5,400* Contribution margin $ 1,000 $ 3,900 $ 6,500* $3,600* Fixed costs 500* 4,000 6,100* 750 Operating income (loss) $ 500 $ (100)* $ 400 $2,850 Units sold 1,000* 1,300 125 90 Price/unit $5 $12* $130 $100* Variable cost/unit $4* $9 $78* $60* Contribution margin/unit $1* $3 $52* $40* Contribution margin ratio 20%* 25%* 40% 40%* Break-even in units 500* 1,334* 118* 19* *Designates calculated amount.Note: When the calculated break-even in units includes a fractional amount, it has been rounded up to the next whole unit.16–101. Variable cost ratio = Variable costs/Sales= $399,900/$930,000= 0.43, or 43%Contribution margin ratio = (Sales – Variable costs)/Sales= ($930,000 – $399,900)/$930,000= 0.57, or 57%2. Break-even sales revenue = $307,800/0.57 = $540,0003. Margin of safety = Sales – Break-even sales= $930,000 – $540,000 = $390,0004. Contribution margin from increased sales = ($7,500)(0.57) = $4,275Cost of advertising = $5,000No, the advertising campaign is not a good idea, because the company’s o p-erating income will decrease by $725 ($4,275 – $5,000).1. Income = Revenue – Variable cost – Fixed cost0 = 1,500P – $300(1,500) – $120,0000 = 1,500P – $450,000 – $120,000$570,000 = 1,500PP = $3802. $160,000/($3.50 – Unit variable cost) = 128,000 unitsUnit variable cost = $2.2516–121. Contribution margin per unit = $5.60 – $4.20*= $1.40*Variable costs per unit:$0.70 + $0.35 + $1.85 + $0.34 + $0.76 + $0.20 = $4.20Contribution margin ratio = $1.40/$5.60 = 0.25 = 25%2. Break-even in units = ($32,300 + $12,500)/$1.40 = 32,000 boxesBreak-even in sales = 32,000 ⨯ $5.60 = $179,200or= ($32,300 + $12,500)/0.25 = $179,2003. Sales ($5.60 ⨯ 35,000) $ 196,000Variable costs ($4.20 ⨯ 35,000) 147,000Contribution margin $ 49,000Fixed costs 44,800Operating income $ 4,2004. Margin of safety = $196,000 – $179,200 = $16,8005. Break-even in units = 44,800/($6.20 – $4.20) = 22,400 boxesNew operating income = $6.20(31,500) – $4.20(31,500) – $44,800= $195,300 – $132,300 – $44,800 = $18,200 Yes, operating income will increase by $14,000 ($18,200 – $4,200).1. Variable cost ratio = $126,000/$315,000 = 0.40Contribution margin ratio = $189,000/$315,000 = 0.602. $46,000 ⨯ 0.60 = $27,6003. Break-even revenue = $63,000/0.60 = $105,000Margin of safety = $315,000 – $105,000 = $210,0004. Revenue = ($63,000 + $90,000)/0.60= $255,0005. Before-tax income = $56,000/(1 – 0.30) = $80,000Note: Tax rate = $37,800/$126,000 = 0.30Revenue = ($63,000 + $80,000)/0.60 = $238,333Sales ............................................................................... $ 238,333 Less: Variable expenses ($238,333 ⨯ 0.40) ................. 95,333 Contribution margin ...................................................... $ 143,000 Less: Fixed expenses ................................................... 63,000 Income before income taxes ........................................ $ 80,000 Income taxes ($80,000 ⨯ 0.30) ...................................... 24,000 Net income ................................................................ $ 56,0001. Operating income = Revenue(1 – Variable cost ratio) – Fixed cost(0.20)Revenue = Revenue(1 – 0.40) – $24,000(0.20)Revenue = (0.60)Revenue – $24,000(0.40)Revenue = $24,000Revenue = $60,000Sales ............................................................................... $ 60,000Variable expenses ($60,000 ⨯ 0.40) .............................. 24,000Contribution margin ...................................................... $ 36,000Fixed expenses .............................................................. 24,000 Operating income ..................................................... $ 12,000 $12,000 = $60,000 ⨯ 20%2. If revenue of $60,000 produces a profit equal to 20 percent of sales and if theprice per unit is $10, then 6,000 units must be sold. Let X equal number of units, then:Operating income = (Price – Variable cost) – Fixed cost0.20($10)X = ($10 – $4)X – $24,000$2X = $6X – $24,000$4X = $24,000X = 6,000 buckets0.25($10)X = $6X – $24,000$2.50X = $6X – $24,000$3.50X = $24,000X = 6,857 bucketsSales (6,857 ⨯ $10) ......................................................... $68,570Variable expenses (6,857 ⨯ $4) ..................................... 27,428Contribution margin ...................................................... $41,142Fixed expenses .............................................................. 24,000 Operating income ..................................................... $17,142 $17,142* = 0.25 ⨯ $68,570 as claimed*Rounded down.Note: Some may prefer to round up to 6,858 units. If this is done, the operat-ing income will be slightly different due to rounding.16–14 Concluded3. Net income = 0.20Revenue/(1 – 0.40)= 0.3333Revenue0.3333Revenue = Revenue(1 – 0.40) – $24,0000.3333Revenue = 0.60Revenue – $24,0000.2667Revenue = $24,000Revenue = $89,98916–151. Company A: $100,000/$50,000 = 2Company B: $300,000/$50,000 = 62. Company BX = $50,000/(1 – 0.80) X = $250,000/(1 – 0.40)X = $50,000/0.20 X = $250,000/0.60X = $250,000 X = $416,667Company B must sell more than Company A to break even because it must cover $200,000 more in fixed costs (it is more highly leveraged).3. Company A: 2 ⨯ 50% = 100%Company B: 6 ⨯ 50% = 300%The percentage increase in profits for Company B is much higher than Com-pany A’s increase because Company B has a higher degree of oper ating leve-rage (i.e., it has a larger amount of fixed costs in proportion to variable costs as compared to Company A). Once fixed costs are covered, additional reve-nue must cover only variable costs, and 60 percent of Company B’s revenue above break-even is profit, whereas only 20 perce nt of Company A’s revenue above break-even is profit.1. Variable Units in PackageProduct Price* –Cost = CM ⨯Mix = CM Scientific $25 $12 $13 1 $13 Business 20 9 11 5 55 Total $68 *$500,000/20,000 = $25$2,000,000/100,000 = $20X = ($1,080,000 + $145,000)/$68X = $1,225,000/$68X = 18,015 packages18,015 scientific calculators (1 ⨯ 18,015)90,075 business calculators (5 ⨯ 18,015)2. Revenue = $1,225,000/0.544* = $2,251,838*($1,360,000/$2,500,000) = 0.5441. Sales mix is 2:1 (Twice as many videos are sold as equipment sets.)2. Variable SalesP roduct Price –Cost = CM ⨯Mix = Total CM Videos $12 $4 $8 2 $16 Equipment sets 15 6 9 1 9 Total $25 Break-even packages = $70,000/$25 = 2,800Break-even videos = 2 ⨯ 2,800 = 5,600Break-even equipment sets = 1 ⨯ 2,800 = 2,8003. Switzer CompanyIncome StatementFor Last YearSales .......................................................................................... $ 195,000Less: Variable costs ................................................................. 70,000Contribution margin ................................................................. $ 125,000Less: Fixed costs ..................................................................... 70,000 Operating income ................................................................ $ 55,000 Contribution margin ratio = $125,000/$195,000 = 0.641, or 64.1%Break-even sales revenue = $70,000/0.641 = $109,2044. Margin of safety = $195,000 – $109,204 = $85,7961. Sales mix is 2:1:4 (Twice as many videos will be sold as equipment sets, andfour times as many yoga mats will be sold as equipment sets.)2. Variable SalesP roduct Price –Cost = CM ⨯Mix = Total CM Videos $12 $ 4 $8 2 $16 Equipment sets 15 6 9 1 9 Yoga mats 18 13 5 4 20 Total $45 Break-even packages = $118,350/$45 = 2,630Break-even videos = 2 ⨯ 2,630 = 5,260Break-even equipment sets = 1 ⨯ 2,630 = 2,630Break-even yoga mats = 4 ⨯ 2,630 = 10,5203. Switzer CompanyIncome StatementFor the Coming YearSales .......................................................................................... $555,000Less: Variable costs ................................................................. 330,000Contribution margin ................................................................. $225,000Less: Fixed costs ..................................................................... 118,350 Operating income ................................................................ $106,650 Contribution margin ratio = $225,000/$555,000 = 0.4054, or 40.54%Break-even revenue = $118,350/0.4054 = $291,9344. Margin of safety = $555,000 – $291,934 = $263,0661. Contribution margin/unit = $410,000/100,000 = $4.10Contribution margin ratio = $410,000/$650,000 = 0.6308Break-even units = $295,200/$4.10 = 72,000 unitsBreak-even revenue = 72,000 ⨯ $6.50 = $468,000or= $295,200/0.6308 = $467,977**Difference due to rounding error in calculating the contribution margin ratio.2. The break-even point decreases:X = $295,200/(P – V)X = $295,200/($7.15 – $2.40)X = $295,200/$4.75X = 62,147 unitsRevenue = 62,147 ⨯ $7.15 = $444,3513. The break-even point increases:X = $295,200/($6.50 – $2.75)X = $295,200/$3.75X = 78,720 unitsRevenue = 78,720 ⨯ $6.50 = $511,68016–19 Concluded4. Predictions of increases or decreases in the break-even point can be madewithout computation for price changes or for variable cost changes. If both change, then the unit contribution margin must be known before and after to predict the effect on the break-even point. Simply giving the direction of the change for each individual component is not sufficient. For our example, the unit contribution changes from $4.10 to $4.40, so the break-even point in units will decrease.Break-even units = $295,200/($7.15 – $2.75) = 67,091Now, let’s look at the break-even point in revenues. We might expect that it, too, will decrease. However, that is not the case in this particular example.Here, the contribution margin ratio decreased from about 63 percent to just over 61.5 percent. As a result, the break-even point in revenues has gone up.B reak-even revenue = 67,091 $7.15 = $479,7015. The break-even point will increase because more units will need to be sold tocover the additional fixed expenses.Break-even units = $345,200/$4.10 = 84,195 unitsRevenue = $547,26816–201.Break-even point = 2,500 units; + line is total revenue and x line is total costs.2. a. Fixed costs increase by $5,000:Break-even point = 3,750 unitsb. Unit variable cost increases to $7:Break-even point = 3,333 unitsc. Unit selling price increases to $12:Break-even point = 1,667 unitsd. Both fixed costs and unit variable cost increase:Break-even point = 5,000 units3. Original data:-$10,000$0$10,000Break-even point = 2,500 unitsa. Fixed costs increase by $5,000:-$15,000$0$15,000Break-even point = 3,750 unitsb. Unit variable cost increases to $7:-$10,000$0$10,000Break-even point = 3,333 unitsc.-$10,000$0$10,000Break-even point = 1,667 unitsd. Both fixed costs and unit variable cost increase:-$15,000$0$15,000Break-even point = 5,000 units4. The first set of graphs is more informative since these graphs reveal howcosts change as sales volume changes.1. Unit contribution margin = $1,060,000/50,000 = $21.20Break-even units = $816,412/$21.20 = 38,510 unitsOperating income = 30,000 ⨯ $21.20 = $636,0002. CM ratio = $1,060,000/$2,500,000 = 0.424 or 42.4%Break-even point = $816,412/0.424 = $1,925,500Operating income = ($200,000 ⨯ 0.424) + $243,588 = $328,3883. Margin of safety = $2,500,000 – $1,925,500 = $574,5004. $1,060,000/$243,588 = 4.352 (operating leverage)4.352 ⨯ 20% = 0.87040.8704 ⨯ $243,588 = $212,019New operating income level = $212,019 + $243,588 = $455,6075. Let X = Units0.10($50)X = $50.00X – $28.80X – $816,412$5X = $21.20X – $816,412$16.20X = $816,412X = 50,396 units6. Before-tax income = $180,000/(1 – 0.40) = $300,000X = ($816,412 + $300,000)/$21.20 = 52,661 units1. Variable Sales PackageP roduct Price –Cost = CM ⨯Mix = CM Vases $40 $30 $10 2 $20 Figurines 70 42 28 1 28 Total $48 Break-even packages = $30,000/$48 = 625Break-even vases = 2 ⨯ 625 = 1,250Break-even figurines = 6252. The new sales mix is 3 vases to 2 figurines.Variable Sales Package P roduct Price –Cost = CM ⨯Mix = CM Vases $40 $30 $10 3 $30 Figurines 70 42 28 2 56 Total $86 Break-even packages = $35,260/$86 = 410Break-even vases = 3 ⨯ 410 = 1,230Break-even figurines = 2 ⨯ 410 = 82016–231. d2. c3. a4. d5. e6. b7. cPROBLEMS16–241. Unit contribution margin = $825,000/110,000 = $7.50Break-even point = $495,000/$7.50 = 66,000 unitsCM ratio = $7.50/$25 = 0.30Break-even point = $495,000/0.30 = $1,650,000or= $25 ⨯ 66,000 = $1,650,0002. Increased CM ($400,000 ⨯ 0.30) $ 120,000Less: Increased advertising expense 40,000Increased operating income $ 80,0003. $315,000 ⨯ 0.30 = $94,5004. Before-tax income = $360,000/(1 – 0.40) = $600,000Units = ($495,000 + $600,000)/$7.50= 146,0005. Margin of safety = $2,750,000 – $1,650,000 = $1,100,000or= 110,000 units – 66,000 units = 44,000 units6. $825,000/$330,000 = 2.5 (operating leverage)20% ⨯ 2.5 = 50% (profit increase)16–251. Sales mix:Squares: $300,000/$30 = 10,000 unitsCircles: $2,500,000/$50 = 50,000 unitsSales Total Product P –V* = P – V ⨯ Mix = CM Squares $30 $10 $20 1 $ 20 Circles 50 10 40 5 200 Package $220 *$100,000/10,000 = $10$500,000/50,000 = $10Break-even packages = $1,628,000/$220 = 7,400 packagesBreak-even squares = 7,400 ⨯ 1 = 7,400Break-even circles = 7,400 ⨯ 5 = 37,0002. Contribution margin ratio = $2,200,000/$2,800,000 = 0.78570.10Revenue = 0.7857Revenue – $1,628,0000.6857Revenue = $1,628,000Revenue = $2,374,2163. New mix:Sales Total Product P –V = P – V ⨯ Mix = CM Squares $30 $10 $20 3 $ 60 Circles 50 10 40 5 200 Package $260 Break-even packages = $1,628,000/$260 = 6,262 packagesBreak-even squares = 6,262 ⨯ 3 = 18,786Break-even circles = 6,262 ⨯ 5 = 31,310CM ratio = $260/$340* = 0.7647*(3)($30) + (5)($50) = $340 revenue per package0.10Revenue = 0.7647Revenue – $1,628,0000.6647Revenue = $1,628,000Revenue = $2,449,2254. Increase in CM for squares (15,000 ⨯ $20) $ 300,000Decrease in CM for circles (5,000 ⨯ $40) (200,000)Net increase in total contribution margin $ 100,000Less: Additional fixed expenses 45,000Increase in operating income $ 55,000Gosnell would gain $55,000 by increasing advertising for the squares. This isa good strategy.16–261. Currently:Sales (830,000 ⨯ $0.36) $ 298,800Variable expenses 224,100Contribution margin $ 74,700Fixed expenses 54,000Operating income $ 20,700New contribution margin = 1.5 ⨯ $74,700 = $112,050$112,050 – promotional spending – $54,000 = 1.5 ⨯ $20,700Promotional spending = $27,0002. Here are two ways to calculate the answer to this question:a. The per-unit contribution margin needs to be the same:Let P* represent the new price and V* the new variable cost.(P – V) = (P* – V*)$0.36 – $0.27 = P* – $0.30$0.09 = P* – $0.30P* = $0.39b. Old break-even point = $54,000/($0.36 – $0.27) = 600,000New break-even point = $54,000/(P* – $0.30) = 600,000P* = $0.39The selling price should be increased by $0.03.3. Projected contribution margin (700,000 ⨯ $0.13) $91,000Present contribution margin 74,700Increase in operating income $16,300The decision was good because operating income increased by $16,300.(New quantity ⨯ $0.13) – $54,000 = $20,700New quantity = 574,615Selling 574,615 units at the new price will maintain profit at $20,700.16–271. P –V = P – V ⨯Mix = TotalResidential $540.00a$221.64c$318.36 2 $636.72 Commercial 160.00b124.52c35.48 1 35.48 Package $672.20 a$13.50 ⨯ 10 ⨯ 4b$40 ⨯ 4c Cost per acre for four applicationsCommercialChemicals $ 70.00 $ 70.00 [$40 + (3 ⨯ $10)] Labor* 80.00 18.00Operating expenses** 55.12 20.00Supplies** 16.52 16.52Total $ 221.64 $ 124.52*10/3 ⨯ $6.00 ⨯ 4; 3/4 ⨯ $6.00 ⨯ 4**The per-acre amount ⨯ 4 applicationsX = F/(P – V)= $39,708/$672.20 = 59* packagesResidential: 2 ⨯ 59 = 118 acresCommercial: 1 ⨯ 59 = 59 acresAverage number of residential customers = 118/0.10 = 1,180*Rounded2. Hours needed to service break-even volume (in packages):Residential: 10/3 ⨯ 4 ⨯ 2 = 26.67* hoursCommercial: 3/4 ⨯ 4 ⨯ 1 = 3.00 hours29.67 hours per packageTotal hours required = 29.67 ⨯ 59 = 1,751 hoursHours per employee = 8 ⨯ 140 = 1,120Employees needed = 1,751/1,120 = 1.6 laborersOne employee is not sufficient.Volume/Employee = 1,120/29.67 = 38 packages. Thus, if volume exceeds 38 composite units (76 residential and 38 commercial), a second laborer is needed (at least part time).*RoundedNote: Adding another employee could affect the costs used in the initial anal-ysis; for example: (1) another truck might be added (increasing fixed costs and the break-even point; (2) a two-man crew might be used (increasing variable costs); (3) the new employee might work evenings/weekends (no change in either fixed or variable costs). CVP used for planning is often an iterative process—the original solution may raise problems that may call for a recal-culation, altering plans further.3. The mix is redefined to be 1.2:0.8:1.0.P roduct P –V = P – V ⨯Mix = Total CM Res.-1 $135.00 $ 77.91* $ 57.09 1.2 $ 68.51 Res.-4 540.00 221.64 318.36 0.8 254.69 Comm. 160.00 124.52 35.48 1.0 35.48 Package $ 358.68 *Variable cost for one-time residential application:Chemicals $40.00Labor 20.00Operating expenses 13.78Supplies 4.13TotalX = F/(P – V) = $39,708/$358.68 = 111 packagesResidential (one application): 1.2 ⨯ 111 = 133 acresResidential (four applications): 0.8 ⨯ 111 = 89 acresCommercial: 1 ⨯ 111 = 111 acres1. Contribution margin ratio = $487,548/$840,600 = 0.582. Revenue = $250,000/0.58 = $431,0343. Operating income = CMR ⨯ Revenue – Total fixed cost0.08R/(1 – 0.34) = 0.58R – $250,0000.1212R = 0.58R – $250,0000.4588R = $250,000R = $544,9004. $840,600 ⨯ 110% = $924,660$353,052 ⨯ 110% = 388,357$536,303CMR = $536,303/$924,660 = 0.58The contribution margin ratio remains at 0.58.5. Additional variable expense = $840,600 ⨯ 0.03 = $25,218New contribution margin = $487,548 – $25,218 = $462,330New CM ratio = $462,330/$840,600 = 0.55Break-even point = $250,000/0.55 = $454,545The effect is to increase the break-even point.6. Present contribution margin $ 487,548Projected contribution margin ($920,600 ⨯ 0.55) 506,330Increase in contribution margin/profit $ 18,782Fitzgibbons should pay the commission because profit would increase by $18,782.1. Let X be a package of three Grade I cabinets and seven Grade II cabinets.Then:0.3X($3,400) + 0.7X($1,600) = $1,600,000X = 748 packagesGrade I: 0.3 ⨯ 748 = 224 unitsGrade II: 0.7 ⨯ 748 = 524 units2. P roduct P –V = P – V ⨯Mix = Total CMGrade I $3,400 $2,686 $714 3 $2,142 Grade II 1,600 1,328 272 7 1,904 Package $4,046 Direct fixed costs—Grade I $ 95,000Direct fixed costs—Grade II 95,000Common fixed costs 35,000Total fixed costs $ 225,000$225,000/$4,046 = 56 packagesGrade I: 3 ⨯ 56 = 168; Grade II: 7 ⨯ 56 = 3923. P roduct P –V = P – V ⨯Mix = Total CMGrade I $3,400 $2,444 $956 3 $2,868 Grade II 1,600 1,208 392 7 2,744 Package $5,612 P ackage CM = 3($3,400) + 7($1,600)P ackage CM = $21,400$21,400X = $1,600,000 – $600,000X = 47 packages remaining141 Grade I (3 ⨯ 47) and 329 Grade II (7 ⨯ 47)Additional contribution margin:141($956 – $714) + 329($392 – $272) $73,602Increase in fixed costs 44,000Increase in operating income $29,602Break-even: ($225,000 + $44,000)/$5,612 = 48 packages144 Grade I (3 ⨯ 48) and 336 Grade II (7 ⨯ 48)If the new break-even point is interpreted as a revised break-even for 2004, then total fixed costs must be reduced by the contribution margin already earned (through the first five months) to obtain the units that must be sold for the last seven months. These units would then be added to those sold during the first five months:CM earned = $600,000 – (83* ⨯ $2,686) – (195* ⨯ $1,328) = $118,102*224 – 141 = 83; 524 – 329 = 195X = ($225,000 + $44,000 – $118,102)/$5,612 = 27 packagesFrom the first five months, 28 packages were sold (83/3 or 195/7). Thus, the revised break-even point is 55 packages (27 + 28)—in units, 165 of Grade I and 385 of Grade II.。

《管理会计》(ManagementAccounting)课程教学大纲

《管理会计》(Management Accounting)课程教学大纲制定人:崔秀梅、殷俊明 审核人:杨 政第一部分 课程概述一、基本信息(一)课程代码:02110090(二)课程属性、学分、学时《管理会计》是会计学、财务管理学、审计学等专业(本科)的一门专业必修课,主要讲授管理会计的基本理论和基本方法,阐述以提高经济效益为最终目的的会计信息利用系统,是为培养学生基本理论知识和应用能力而设置的一门专业课。

它将现代化管理与会计有机融为一体,向企业管理当局提供所需的会计信息,以便其有效地经营管理企业,制定企业政策,计划和控制企业活动,评价、选择决策方案,为企业提高经济效益服务。

学分:3 学时:48(三)适用对象适用于会计学、财务管理、审计学等专业的本科生。

二、课程简介《管理会计》将现代管理与会计融为一体,作为内部报告会计,向企业管理当局提供会计信息支持,以便其有效地经营管理企业,制定企业政策,计划和控制企业活动,评价决策方案,帮助企业实现其价值。

《管理会计》课程的内容主要包括四大知识模块:第一模块为管理会计基础篇部分,主要包括管理会计概述、成本性态的分析与应用、本量关系解析、变动成本法;第二模块为预测和决策部分,主要包括分部报告和分权制、短期经营决策;第三为规划和控制部分,主要包括全面预算管理、标准成本控制、作业成本管理;第四模块为责任与评价部分,主要包括责任会计和业绩评价。

Management accounting, as accounting for internal reporting, integrates modern management and accounting, providing accounting information to managers of enterprises to facilitate their management, decision-making, enterprise activities planning and evaluation scheme, for the purpose of realizing enterprise value.This course is divided into four parts. The first part is the fundamental knowledge of management accounting, including overview of accounting management, analysis and application of cost behavior, cost-volume-profit analysis andvariable costing. The second part deals with forecasting and decision-making, mainly including the segment reporting, system of decentralization, and short-term business decision. The third part is concerned with planning and control, covering comprehensive budgeting management, control of standard cost, and activity-based costing management.The last part is about responsibility and evaluation, including the responsibility accounting and performance evaluation.三、教学目标通过本课程的教学,使学生系统掌握现代管理会计的基本理论和基本方法,掌握预测、决策、全面预算、成本控制、责任考核评价等内容的技术方法和相关知识,并能将所学知识和操作技能,在社会主义市场经济条件下和现代企业制度环境中,应用于企业经营管理活动中,提高分析和解决企业经营管理问题的能力,为走向社会,加强企业管理、提高企业经济效益等方面发挥积极作用。

管理会计 双语课件 Management accounting

03 作业

High-Tech

Globalization

Economic Transition

03 作业 Need for innovation and relevant produces: – Activity-based management • ABC Improves accuracy of assigning costs

– Customer orientation

• Strategic positioning to maintain competitive advantage

• Value chain framework to focus on customer value

– Total quality management emphasized continuous improvement

1950-1980 1980-

Most of the product-costing and internal accounting procedures used in the last century were developed.

Emphasis of accounting information for internal management . Management accounting practices developed, including: Flexible budgeting, Standard costs, Variance analysis, transfer prices et al.

03 管理会计的定义

1 、国外会计学界的定义 1 )狭义管理会计 管理会计知识为企业内部管理者提供规划和控制所需信息的内部会计。 • 为企业管理当局的管理目标服务。

《管理会计(双语)》课程 (5)

Time-Driven ABC

Use parameter estimates to assign indirect costs: Cost of using resource i by product j =

Capacity cost rate of resource i x Quantity of capacity of resource i used

Time-driven activity-based costing systems (TDABC or Time-Driven ABC) estimate two parameters and then assign indirect costs similar to the way direct costs are assigned

by product j

8

TDABC Profitability Report

Refer to Madison Dairy’s report, Exhibit 5-5 The results from the time-driven activity-based

costing system were quite different from the results based on the traditional cost system

Committed costs become variable via a two-st resources change either because of changes in the quantity of activities performed or because of changes in the efficiency of performing activities

金陵科技学院-管理会计(双语)管理会计复习提纲

PRACTICE QUESTIONS PART A, LECTURE 1QUESTION 3Answer the five questions below which relate to the following data: A firm had the following per unit costs for a period in which it expected to produce 1,000 units: DM $20, DL $30, Variable OH $20, Fixed OH $10, Variable selling costs $5 per unit. Answer the following costs related to the data:(a) Calculate the prime costs per unit.(b) Calculate the conversion costs per unit.(c) Calculate the product (inventoriable) cost per unit under absorption costing.(d) Calculate the variable product (inventoriable) cost per unit under absorption costing.(e) Calculate the period costs per unit.(f) Calculate the total expected costs if the firm produced and sold 1,100 units. Answer(a)Prime cost = DM + DL = $50 ($20 + $30)(b)Conversion cost = DL + OH = $60 ($30 + $20 + $10)(c)Product (inventoriable) cost under absorption costing = all manufacturing costs, i.e. $80 ($20 + $30 + $20 + $10)(d)V ariable product (inventoriable) cost under absorption costing = remove fixed OH of $10 per unit, therefore $70.(e)Period cost = all costs that are not manufacturing costs. Here, only selling costs, therefore $5.(f)Answer is $92,500, calculated as follows. Add total of expected manufacturing andnon-manufacturing costs. Note that the fixed and variable costs are treated differently: SOLUTIONS TO PRACTICE QUESTIONS, PART A LECTURE 2QUESTION 1Production budget for the month of AprilRequired for sales 1,000+ desired ending inventory 60 (5% x 1,200)1,060- opening inventory 52*Required production 1,008* If you did not know the actual inventory of products at the beginning of April (whether you do or not depends on how far in advance you are preparing the budgets), you would use the estimate for the beginning of April (which is the same as the end of March, i.e. 5% x 1,000 = 50).Direct Materials purchases budget for the month of April (in kgs)Required for production 2,016 (1,008 units x 2 kg)+ desired ending inventory 2002,216- opening inventory 125**Required purchases of material 2,091 kg** As before, if you did not know the actual inventory of materials at the beginning of April, you would use the estimate for the beginning of April (which is the same as the end of March, i.e. 250 kg)QUESTION 3Flexible budget formula is $100,000 + $40 per unit, therefore with no changes, budgeted costs would be: $100,000 + (20,000 x $40)= $900,000The effect of using overtime is that the variable cost will be greater than $40 per unit. Without further information, all we can conclude is that the budgeted amount will be some amount greater than $900,000.QUESTION 4A v. CM = (.1 x $4) + (.7 x $6) + (.2 x $2)= (.4 + 4.2 + .4) = $5BE point = 6,000 = 1,200 units in total, which is:5120 units of product 1 (10%)840 units of product 2 (70%)240 units of product 3 (20%)QUESTION 5(a)Cost A is not fixed, as it changes across activity levels. Not variable, because it is a different amount per unit at the different activity levels. Therefore it is mixed.Cost B is a fixed cost as in total it remains the same in total across different activity levels. Because Cost C is constant per unit across different activity levels, the total cost will vary in proportion to activity level, therefore it is a variable cost.(b)High cost – low costHigh activity – low activity$3,000-$2,0002,000-1,000= $1,000/1,000= $1 per unit.(c)Flexible budget formula for Cost A is $1,000 + $1 per unit.SOLUTIONS TO PRACTICE QUESTIONS, PART A, LECTURE 3QUESTION 2The following are summaries of the job cards for a particular period:Assume that only two jobs (#101 and #103) are finished, and job #103 is sold.(a) What is the balance of the WIP a/c and FG a/c at the end of the period, and the total expense for the period?(b) Is it possible to tell the total DM cost incurred for the period. If so, what is the amount?(c) Is it possible to tell the total DM cost EXPENSED during the period. If so, what is the amount?ANSWER(a) Identify which jobs are at different stages of the manufacturing and selling cycle, and therefore in each of the different accounts. Total the costs of those jobs. The total of the costs on the job cost sheets will be the balances of WIP and FG, and the total expense (amounta journal entry for all goods finished during the period.. However, at a particular point of time all jobs can be in one place only: either they are incomplete (WIP); finished and not sold (FG); or finished and sold (COGS).(b) Because the job cards indicate the opening balance for the period, all costs incurred in a previous period would be in the opening balance. Any costs itemised as DM, DL and OH on the job card are costs incurred this period. Therefore the cost of DM incurred for the periodis the total of the DM column, which is $96,000.(c)It would always be possible to find out the amount by going back through all the job cost sheets. In this example it is very easy to do because the opening balance is zero. Therefore, the amount of DM cost expensed during the period is the DM cost of any jobs sold. Job #103 was sold, and the DM cost of job #103 was $50,000.QUESTION 3Assume a firm started 5 jobs in a period. A summary of the costs on the job cost sheets∙Jobs 1, 2, 3 and 4 are finished in the period.∙Jobs 1 and 2 are sold in the period.∙Opening balances are zeroRequired:(a)Show the completed WIP, FG and COGS accounts.(b)What is the total amount of OH that has been applied during the period?(c)What is the amount of OH in the WIP account balance at the end of the period? ANSWER(a)WIPMaterials 150 FG 420 (jobs 1-4)Wages 200 Balance 180 (job 5)OH 250600 600FGWIP 420 COGS 150 (jobs 1-2)Balance 270 (jobs 3-4)420 420COGSFG 150(b) The total OH applied is found by adding OH on the job cost sheets for all jobs worked, i.e. $250.(c) The balance in any account consists of DM, DL and OH costs incurred on all jobs at that stage. There is only one job unfinished (job #5) therefore the balance in WIP of $180represents the costs incurred on job#5. We know from the job card that $70 of that cost is OH applied.QUESTION 4The following budgeted and actual results for a period relate to Dustin Pty Ltd, a firm which employs normal absorption job costing and applies OH using DL cost as the cost driver.Direct Manufacturing labour costs Manufacturing overhead costs Budget for 20071,000,0001,750,000Actual Results for 2007980,0001,862,000(a)Calculate the firm’s budgeted OH rate.(b)Calculate the cost of a particular job, job #323, which incurs $40,000 DM and $30,000 DL.(c)Calculate the amount of under/over applied overhead for the entire firm for the period, i.e. not just for job #323.ANSWER(a) 1,750,0001,000,000= 175% of DL cost or $1.75 for every dollar of DL.(b)Normal cost of job #323:DM $ 40,000DL $ 30,000OH $ 52,500 (175% of DL)$122,500(c)Total actual OH = $1,862,000Total applied OH = $1,715,000 (175% x $980,000)Under applied $ 147,000PRACTICE QUESTIONS, PART A, TOPIC 4QUESTION 2Calculate OH applied for the period given the following selected information:Budget information:Activity level 3,000 DL hoursV OH rate $3 per DL hourBudgeted total OH costs for actual activity level $15,900Actual data:Activity level 3,300 DL hoursANSWEROH applied will be actual hours worked x budgeted OH rates (both fixed and variable). What do we know?Actual hours worked = 3,300V ariable OH rate = $3 per DL hourWhat do we need to find?Fixed OH rate –this is not given. Recall that fixed OH rates can only be calculated at budgeted activity level. We know the budgeted activity level is 3,000, therefore the fixed OH rate will equal:Budgeted F OH (at budgeted activity)Budgeted activity level, i.e. 3,000Therefore, we need the budgeted F OH at budgeted activity level. But it is not given. All we are told is the total budgeted OH for actual activity, i.e. for 3,300 hours. We need to use this information to determine budgeted F OH, as follows:Total budgeted OH at 3,300 hours = $15,900V ariable budgeted OH at 3,300 hours = 3,300 x $3 = $9,900Therefore fixed budgeted OH at 3,300 hours = $15,900 - $9,900 = $6,000But if budgeted fixed OH at 3,300 hours is $6,000, budgeted fixed OH at 3,000 hours is also $6,000, so now we can work out the fixed OH rate, i.e.$6,000/3,000 = $2 per DL hour.We can now calculate OH applied, i.e. 3,300 x ($3+$2) = $16,500QUESTION 4A manufacturing firm has a direct labour cost of $25 per direct labour hour. Where jobs are worked in overtime hours, the cost is time-and-a-half, i.e. $37.50 per direct labour hour. A particular job was worked on for 8 hours, 4 hrs in normal time, and 4 hrs overtime.(a) What is the amount of overtime premium per DL hour?(b) What is the amount of overtime premium related to the job?(c) Show the journal entry for the labour cost assuming:(i) the overtime was necessary because of the particular nature of the job.(ii) the overtime was necessary because of poor scheduling by the firm.Answer(a)The premium is $12.50 per DL hour.(b)4 hours x $12.50 = $50.(c) (i)WIP DR 250Wages and Salaries Payable CR 250(in these circumstances the overtime premium is charged to the job, and therefore ends up in the WIP account, and eventually in FG account).(ii)WIP DR 200OH DR 50Wages and Salaries Payable CR 250(in these circumstances the overtime premium is not charged to the job. Only the ordinary costs per hour ($25) for the hours worked on the job are charged to WIP.)SOLUTIONS TO PRACTICE QUESTIONS, PART A, TOPIC 5(a) Calculate the labour rate variance and the labour efficiency variance, using either tables or formulae.(b) Show the journal entry required to record labour information for the period.(c) Calculate the material price variance and the material efficiency variance (using either tables or formulae) assuming the MPV is isolated on purchase.(d) Show the journal entries for materials purchased and used.(e) Repeat (c) and (d) assuming MPV is isolated on usage. This means you are to recalculate the MPV, and show the journal entries for purchase and use of material for this option.AnswerUsing formulae:LRV = 770 x ($32 - $30) = +$1,540 = $1,540 ULEV = $30 x (770 – 725) = -$1,350 = $1,350 UPart (c)Using formulae:MPV = 4,000 x ($10.50 - $10) = +$2,000 = $2,000 UMEV = $10 (3,100 – 2,900) = +$2,000 = $2,000 UPart (e)Using formulae:MPV = 3,100 x ($10.50 - $10) = +$1,550 = $1,550 UQUESTION 3“Fit to a T” designs and manufactures T-shirts, and sells them in one-dozen lots. A new type of material was purchased in the period, which led to faster cutting and sewing but the workers used more material than usual as they learned to work with it. The following are selected budget and actual results for the period:Static BudgetNumber of T-shirt lots (1 lot = 1 dozen) 500Per lot of T-shirts:Direct materials 12 metres at $1.50 per meter = $18.00Direct manufacturing labour 2 hours at $8.00 per hour = $16.00Actual resultsNumber of T-shirt lots sold 550Total direct inputs:Direct materials 7,260 metres at $1.75 per meter = $12,705 Direct manufacturing labour 1,045 hours at $8.10 per hour = $8,464.50(a) Calculate the direct material and direct labour variances for the period.(b) Identify possible reasons (suggested from the facts given only – not the general ones in the lecture notes) for the efficiency variances you have calculated.Answer(a) Direct MaterialsAQ used x AP AQ used x SP SQ x SP7,260 x 1.75 7,260 x 1.50 (550 x 12) x 1.5012,705 10,890 6,600 x 1.509,900MPV MEV$1,815 U $990 UFLEXIBLE BUDGET V ARIANCE$2,805 UDirect LabourAQ used x AP AQ used x SP SQ x SP1,045 x 8.10 1,045 x 8 (550 x 2) x 88,464.50 8,360 1,100 x 88,800LRV LEV$104.50 U $440 FFLEXIBLE BUDGET V ARIANCE$335.50 FTOTAL FLEXIBLE BUDGET V ARIANCE$2,469.50 U ($2,805 - $335.50)(b) Possible reasons for efficiency variances (using only facts given):Unfavourable MEV because the new type of material was di fferent to work with, therefore the workers wasted more material than usual while getting used to its different texture etc. Favourable LEV because we are told that the material resulted in “faster cutting and sewing”.AYB225 – PRACTICE QUESTIONS, LECTURE 7QUESTION 1Standard manufacturing costs per unit: (Unchanged from previous accounting period)DM $6; DL $4; V OH $3; F OH $2Physical quantities: (There were no WIP inventories.)Opening FG - 300Units produced - 6,000Closing FG - 200Other cost and price data:Selling price per unit - $25Actual F OH - $11,500Selling and admin costs - $5,000 Fixed, $3,000 V ariable.Variances for the period:Total variable (DM, DL, V OH) - 15,000 UTotal fixed – 500 FRequired:(a) Properly classified Absorption Costing Income Statement for the period.(b) Properly classified V ariable Costing Income Statement for the period.(c) Quantitatively reconcile the profits under the two systems.(d) Explain why the AC profit is less than DC profit.ANSWERAC product cost per unit is 6+4+3+2 = $15DC product cost per unit is 6+4+3 = $13(a) Absorption Costing Income StatementSales (6,100 x $25) 152,500Less Cost of Goods Sold:(6,100 x $15) 91,500Add net variances (unfavourable) 14,500 106,000GROSS MARGIN 46,500Less Selling and Administrative Expenses 8,000NET PROFIT $38,500(b) Direct Costing Income StatementSales (6,100 x $25) 152,500Less V ariable Costs;COGS (6,100 x $13) 79,300Add net variances (unfavourable) 15,000 94,300Selling and Administrative Expenses 3,000 97,300 CONTRIBUTION MARGIN 55,200Less Fixed Costs:Overhead 11,500Selling and Administrative 5,000 16,500NET PROFIT $38,700(c)Inventory decreased from 300 to 200, therefore:Change in inventory 100 x F OH per unit ($2) = $200 explains the difference in profit. Because the fixed OH per unit is unchanged from the previous period, it is possible to conclude that because inventory has decreased profit under AC will be $200 smaller than under DC.(d)The total fixed OH incurred and expensed under DC relates to the 6,000 units produced. Under AC the firm expenses the amount of F OH relating to units sold, which is 6,100. Therefore, because the firm produced less than it sold, under AC an additional amount of fixed OH is expensed which relates to the units in opening inventory. (The full explanationis actually more complicated than this explanation, but the above is all that you are required to know for this unit.AYB225 – SOLUTIONS, PRACTICE QUESTIONS LECTURE 8Note: If you are required to complete a cost of production report in the examination you will be provided with a pro-forma.QUESTION 1 (a)Calc. EUOpening WIP 50%Transferred InTo A/c forCompletedClosing WIP (75%)A/c forCalc. Unit CostsWIPCurrentCosts to Account ForEUUNIT COSTSAllocation of CostsGoods Completed8,000 x $10.2091 81,673Work in process3,000 x 2.9091 8,7273,000 x 2.9 8,7000 x .80 02,250 x 3.60 8,100 25,527107,200* In practice the journal entries would separate out these amounts, as the solution does. If you know the figures, you must show them separately.(c)Work in Process – 2 a/cBalance 44,800 To FG 81,673WIP-1 20,000 Close bal 25,527 (this agrees with the amount above)Material X 16,000Material Y 6,400Payroll 14,000OH 6,000107,200 107,200QUESTION 2(a) COST OF PRODUCTION REPORTCalc. EUOpening WIP 40%Transferred InTo A/c forCompletedClosing WIP(60%)A/c forCalc. Unit CostsWIPCurrentCosts to Account ForEUUNIT COSTSAllocation of CostsGoods Completed2,000 x 83.004 $166,008WIP 400 x 49.104 T/I 19,642240 X 25 CC 6,000 $ 25,642$191,650(b) Work in Process - Spinning Department $96,000Work in Process - Drawing Department $96,000Work in Process – Spinning $ 63,800Materials $ 17,800Payroll, Misc. Credits (if known list separately) $ 46,000Finished Goods $166,008Work in Process - Spinning Department $166,008AYB225 – PRACTICE QUESTIONS, LECTURE 9COST ALLOCATIONPART A – SERVICE DEPARTMENT ALLOCATIONQUESTION 1A firm has two production departments, Mixing and Finishing. These departments areserviced by two support departments, Administration and Payroll. The costs and % usage of the service departments follows:(b) Calculate the billing rates per work unit for administration and payroll under the directmethod, assuming that 1% = 1 work unit. Round to 2 decimal places.(c) Show the allocation using the step-down method, starting with Administration.(d) Show the allocation using the step-down method, starting with Payroll.(e) Calculate the billing rates per work unit for administration and payroll for the methodused in (d) assuming that 1% = 1 work unit. Round to 2 decimal places.FromAdministration From Payroll(b) Administration = 60,000/80 = $750 per unit of work Payroll = 80,000/70 = $1,142.86 per unit of work(c) - STEPFromAdministration From Payroll(d)From PayrollFromAdministration(e) Administration = 84,000/80 = $1,050 per work unit Payroll = 80,000/100 = $800 per work unitQUESTION 1Daniel Supply Company manufactures three products. The first process is a joint process, with joint costs of $127,500. Opening WIP and FG inventory are(a) Show three (3) different “physical measures method” allocations of joint costs using the above data.Note: Joint cost allocation must be based on units produced, NEVER units sold.(b) Show joint cost allocation for Daniel Supply Company assuming the net realisable value method.(c) Use the data for Daniel Supply Company above, except assume now that Bizmo is a by-product.Show the allocation of the joint costs assuming the net realisable value method, and:(i)the net realisable value of the by-product is treated as miscellaneous income.(ii)(ii) the net realisable value of the by-product reduces the costs of the principal products.ANSWER(a)One method would be to say there are three products, therefore each product will be allocatedAnother would be based on the number of physical units produced. The firm produced the following number of units through the joint process:A third would be based on the weighted units produced, i.e.Note that under the three different ways to interpret “physical method”, the amounts are different, and so is the direction in terms of which products are allocated the higher cost.(c)Note: Use the proportions of NRV calculated in part (b) above, i.e. Gizmo 630, Wizmo 280(i) Under this method the total joint costs are allocated to the products only (i.e. not to by-product Bizmo):NRV AllocationGizmo 630 630/910 $ 88,269Wizmo 280 $ 39,231$127,500(ii) Under this method the joint costs are reduced by the net realisable value of Bizmo, i.e. $127,500 less ($40,000 less $8,000) = $95,500. These costs are then allocated to the products only (i.e. not to by-product Bizmo):NRV AllocationGizmo 630 630/910 $66,115Wizmo 280 $29,385$95,500。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

《管理会计(双语)》课程教学大纲课程编码:12120204211课程性质:专业必修课学分:3课时:48开课学期:5适用专业:财务管理一、课程简介《管理会计(双语)是财务管理专业(本科)的一门必修课程。

是以现代企业所处的社会经济环境为背景,明确阐明以企业为主体,密切联系现代会计的预测、决策、规划、控制、考核评价等职能,系统地介绍了现代管理会计的基本理论、基本方法和实用操作技术。

课程分为三部分,第一部分主要交代了管理会计的基本原理和传统管理会计的基本方法;第二部分主要分别讨论管理会计各项职能在实践中的应用程序与具体操作方法。

第三部分集中介绍管理会计发展的新领域。

管理会计是一门理论性较强、计算内容较多的课程。

通过该门课程的学习,使学生领会管理会计的精髓,掌握管理会计的基本理论和基本方法,学会各种分析方法的应用技能和技巧,不断提高学生分析问题和解决问题的能力。

二、教学目标课程总体目标:通过本课程教学,掌握管理会计的基本理论和基本分析方法,结合相应的实践教学,培养学生能独立开展各项管理会计工作的能力。

(一)知识要求:1.了解管理会计的产生与发展,明确管理会计的特点、职能、内容和任务;2.掌握成本习性与变动成本法、本量利分析等管理会计基础分析方法,并了解方法的一般原理;3.掌握短期经营决策分析、长期投资决策分析、全面预算、标准成本控制、责任会计等内容的基本理论与方法。

(二)能力要求:1、具有热爱管理会计工作,爱岗敬业的道德观念;2、具有胜任管理会计工作的良好业务素质和身体素质;3、具有预测、决策、规划、控制的实务能力;4、具有管理会计工作的职业判断、分析和思维能力三、教学内容(一)Chapter 1 Managerial Accounting Concepts and PrinciplesThe main content: Chapter 1 introduces students to managerial accounting and the manufacturing process. Students will learn how managerial accounting is used in the management decision process. They will also be exposed to the terminology used to describe costs related to manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe managerial accounting and the role of managerial accounting in a business.2. Define and illustrate the following costs: 1. direct and indirect costs, 2. direct materials,direct labor, and factory overhead costs, 3. product and period costs.3. Describe and illustrate the following statements for a manufacturing business: 1.balance sheet, 2. statement of cost of goods manufactured, 3. income statement.4. Describe the uses of managerial accounting information.Some key points: direct and indirect costs, direct materials, direct labor, factory overhead costs, product and period costs; cost of goods manufactured.Teaching methods: use of multimedia tools. We ad opt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(二)Chapter 2Job Order CostingThe main content:Chapter 2 introduces students to managerial job order cost systems. Students will be exposed to the terminology used to describe costs related to manufacturing. The first of two basic manufacturing accounting systems, job order, is described in this chapter. Students learn how costs flow through a manufacturing system and the basis for determining product costs under job order costing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe cost accounting systems used by manufacturing businesses.2. Describe and illustrate a job order cost accounting system.3. Describe the use of job order cost information for decision making.4. Describe the flow of costs for a service business that uses a job order cost accountingsystem.Some key points: Job Order Cost System; Overapplied Factory Overhead; Underapplied Factory Overhead; predetermined overhead rate;Teaching methods: use of multimedia tools. We adopt Classroom-based teaching,which is suppl emented by the necessary classroom discussion. Besides,arrange stud ents to d o some appropriate exercises and self-extending reading after class.(三)Chapter 3Process Cost SystemsThe main content:Chapter 3 completes the coverage of manufacturing accounting by introducing process costing. The text demonstrates process costing under the FIFO method. The average cost method is presented in th e chapter’s appendix. Chapter 3 also discusses the impact of just-in-time systems on manufacturing.Learning Objectives:After studying the chapter, your students should be able to:1. Describe process cost systems.2. Prepare a cost of production report.3. Journalize entries for transactions using a process cost system.4. Describe and illustrate the use of cost of production reports for decision making.5. Compare just-in-time processing with traditional manufacturing processing.Some key points: Process Cost System; First-in, First-out (FIFO) Method; Cost of Production Report; Just-in-Time (JIT) Processing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(四)Chapter 4 Cost Behavior and Cost-Volume-Profit AnalysisThe main content: In Chapter 4, students learn how to conduct cost-volume-profit analysis. In preparation for this activity, the chapter discusses variable, fixed, and mixed costs.Learning Objectives:After studying the chapter, your students should be able to:1. Classify costs as variable costs, fixed costs, or mixed costs.2. Compute the contribution margin, the contribution margin ratio, and the unitcontribution margin.3. Determine the break-even point and sales necessary to achieve a target profit.4. Using a cost-volume-profit chart and a profit-volume chart, determine the break-evenpoint and sales necessary to achieve a target profit.5. Compute the break-even point for a company selling more than one product, theoperating leverage, and the margin of safety.Some key points:variable costs; fixed costs; mixed costs; High-Low Method; Contribution Margin; Cost-Volume-Profit Analysis; Contribution Margin Ratio; Unit Contribution Margin.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(五)Chapter 5 BudgetingThe main content: Chapter 5 emphasizes accounting activities that help managers plan, direct, and control the operations of a business. Budgeting is used to establish business goals in the planning function. Budgets help guide managers’ operational decisions. Budgets are also used to control operations as actual results are compared to the budgeted results.Learning Objectives:After studying the chapter, your students should be able to:1. Describe budgeting, its objectives, and its impact on human behavior.2. Describe the basic elements of the budget process, the two major types of budgeting,and the use of computers in budgeting.3. Describe the master budget for a manufacturing company.4. Prepare the basic income statement budgets for a manufacturing company.5. Prepare balance sheet budgets for a manufacturing company.Some key points: Goal Conflict;Budgetary Slack;Continuous Budgeting;Static Budget;Flexible Budget;Zero-Based Budgeting;Capital Expenditures Budget.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(六)Chapter 6 Performance Evaluation Using Variances from Standard Costs The main content: Standard cost systems set budgets for the materials, labor, and factory overhead used by a manufacturer to produce its product. Deviations from these standards are reported as variances.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the types of standards and how they are established.2. Describe and illustrate how standards are used in budgeting.3. Compute and interpret direct materials and direct labor variances.4. Compute and interpret factory overhead controllable and volume variances.5. Journalize the entries for recording standards in the accounts and prepare an incomestatement that includes variances from standard.6. Describe and provide examples of nonfinancial performance measures.Some key points: Direct Labor Rate Variance ;Direct Materials Price Variance;Direct Labor Time Variance;Direct Materials Quantity Variance;Budgeted Variable Factory Overhead;Factory Overhead Cost Variance Report;Controllable Variance;Volume Variance.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(七)Chapter 7 Performance Evaluation for Decentralized Operations The main content: Chapter 7 applies responsibility accounting to cost, profit, and investment centers. The chapter demonstrates the responsibility accounting reports that are used to evaluate department or division performance. This provides an excellent opportunity to remind your students that managers are judged, at least in part, using accounting data.Learning Objectives:After studying the chapter, your students should be able to:1. Describe the advantages and disadvantages of decentralized operations.2. Prepare a responsibility accounting report for a cost center.3. Prepare responsibility accounting reports for a profit center.4. Compute and interpret the rate of return on investment, the residual income, and thebalanced scorecard for an investment center.5. Describe and illustrate how the market price, negotiated price, and cost priceapproaches to transfer pricing may be used by decentralized segments of a business.Some key points:Responsibility Accounting;Balanced Scorecard;Profit Margin;DuPont Formula;Rate of Return on Investment (ROI);Investment Center ;Residual Income;Investment TurnoverTeaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(八)Chapter 8 Differential Analysis, Product Pricing, and Activity-Based CostingThe main content: This chapter covers (1) differential analysis, (2) methods of determining the selling price of a product using a cost-plus markup approach, (3) the effects of production bottlenecks, and (4) activity-based costing. The cost-plus approach of product cost is described in Objective 2; total cost and variable cost methods are presented in the chapter appendix. All topics in this chapter are able to stand alone. Therefore, the instructor is free to cover only one or two of the topics if class time is a limited resource as the term draws to a close.Learning Objectives:After studying the chapter, your students should be able to:1. Prepare differential analysis reports for a variety of managerial decisions.2. Determine the selling price of a product, using the product cost concept.3. Compute the relative profitability of products in bottleneck production processes.4. Allocate product costs using activity-based costing.Some key points:Product Cost Concept ; Target Costing; Production Bottleneck; Theory of Constraints (TOC); Activity-Based Costing (ABC).Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.(九)Chapter 9 Capital Investment AnalysisThe main content: Capital investment analysis is a topic that usually receives detailed coverage in introductory finance courses and/or intermediate accounting. The purpose of this chapter is to give students a brief introduction to the basics of capital investment analysis using the following methods: average rate of return, cash payback, net present value, and internal rate of return.Learning Objectives:After studying the chapter, your students should be able to:1. Explain the nature and importance of capital investment analysis.2. Evaluate capital investment proposals using the average rate of return and cashpayback methods.3. Evaluate capital investment proposals using the net present value and internal rate ofreturn methods.4. List and describe factors that complicate capital investment analysis.5. Diagram the capital rationing process.Some key points: Capital Investment Analysis;Time Value of Money Concept;Average Rate of Return;Cash Payback Period;Internal Rate of Return (IRR) Method;Capital Rationing.Teaching methods: use of multimedia tools. We adopt Classroom-based teaching, which is supplemented by the necessary classroom discussion. Besides,arrange students to do some appropriate exercises and self-extending reading after class.四、整体课时分配五、课程考核与成绩评定1.考核方式:考查;笔试;闭卷。