FRM一级练习题(2)

frm一级题库 2023

frm一级题库2023

一、单项选择题

1.在2023年FRM考试中,一级考试的合格分数线是多少?

2. A. 400

3. B. 500

4. C. 600

5. D. 700

6.FRM一级考试中,风险管理基础占比多少?

7. A. 15%

8. B. 25%

9. C. 35%

10. D. 45%

11.FRM一级考试中,数量分析占比多少?

12. A. 10%

13. B. 15%

14. C. 20%

15. D. 25%

16.FRM一级考试中,金融市场与产品占比多少?

17. A. 20%

18. B. 25%

19. C. 30%

20. D. 35%

21.FRM一级考试中,估值与风险建模占比多少?

22. A. 15%

23. B. 20%

24. C. 25%

25. D. 30%

二、多项选择题

1.下列哪些科目是FRM一级考试的重要内容?

2. A. 风险管理基础

3. B. 数量分析

4. C. 公司金融

5. D. 金融市场与产品

6. E. 估值与风险建模

7.在FRM一级考试中,下列哪些知识点是考生需要掌握的?

8. A. 市场风险的管理方法

9. B. 信用风险的计算方式

10. C. 操作风险的识别与评估

11. D. 企业价值的评估方法

12. E. 对冲策略的有效性分析

三、简答题

1.请简述FRM一级考试的主要目的。

2.在FRM一级考试中,考生应具备哪些基本能力?。

FRM一级Financialdisaster

FRM一级Financialdisaster序号当事人涉案公司涉案金额1—Drysdale&ChaseManhattan bank300million2Joseph Jett Kidder Peabody350million 3Nick Leeson Barings Bank起因1. Drysdale borrowed 300M by exploiting a flaw in the US government bond without collateral2. Drysdale took the wrong position and lost all 300M3. Chase manhattan absorbed all the losses cause inexperienced managers in Chase believed they were just a middleman1. The head of the government bond trading desk at Kidder Peabody, Joseph Jett, reported substantial artificial profits. After the false profits were detected, $350 million in previously reported gains had to be reversed, The loss was not actual.2. The system failed to realize that this profit would disappear once financing costs for the cash bond were taken into account.1. Hidden trading losses at Barings induced Nick Leeson to abandon hedging strategies in favor of speculative strategies. A lack of operational oversight and his dual roles as trader and settlement officer allowed him to conceal his activities and losses.2. Speculative strategies:Selling straddle on the Nikkei 225.Long-long futures on Nikkei 225 in both Tokyo and Singapore3. Dual roles经验教训1. Need for more precise methods for computing the value of collateral.2. Need for better process control.The need for a process that forced areas contemplating new product offerings to receive prior approval from representatives of the principal risk control functions within the firm.1. Always investigate a stream of large unexpected profits thoroughly and make sure you completely understand the source.2. Periodically review models and systems to see if changes in the way they are being used require changes in simplifying assumptions.。

FRM一级练习题(2)答案

FRM一级练习题(2)答案1. If the daily, 95% confidence level value at risk (VaR) of a portfolio is correctly estimated to be USD 10,000, one would expect that 95% of the time (19 out of 20), the portfolio will lose l ess than USD 10,000; equivalently, 5% of the time (1 out of 20) the portfolio will lose USD 10,000 or more.(A) Incorrect. Portfolio value will decline by USD 10,000 or more.(B) Incorrect. In 1 out of 20 days, portfolio value will decline by USD 10,000 or more.(C) Incorrect. 1 out of 95 days woul d provide a 98.9% confidence level.(D) Correct.2. In imperfect markets, deadweight costs of financial distress or bankruptcy caused by debt financing cannot be hedged by the firm's sharehol ders in the capital markets. Hence it pays for the firm to hedge its cash flow uncertainty via the use of d erivatives contracts. The present value of its more stable cash fl ows in the presence of hedging is greater than the present value of its uncertain expected cash fl ows in the absence of hedging. Transaction costs for capital markets bearing this risk are sufficiently l ow in forward markets. Answers (A), (C), and (D) are incorrect because they contradict the correct answer, (B).3. According to CAPM, the expected return of the portfolio = 0.045 + 1.5(0.11) = 21%, and the expected return of the market portfolio is the risk premium plus the risk-free rate, or 11% +4.5% = 15.5%. Therefore, portfolio A is expected to outperform the market.From the preceding, (B) and (D) are clearly incorrect. (C) is incorrect since beta greater than 1.0 implies portfolio A is riskier than the market portfolio.4. Jensen's measure of a portfolio = ap = E (Rp) – RF –βx [E (RM) – RF] = 8% – 5% – 0.5 x (10% – 5%) = 0.5%(A) is incorrect. This is βP *σmaP = 0.5 * 0.20 = 10%.(B) is incorrect. This is the Black-Treynor ratio: αP /βP = 0.005 / 0.5 = 1%.(D) is incorrect. This is the Sharpe ratio: (E (Rp) – RF) / smaP = 0.03 / 0.2 = 15%.5. The answer is (B), since statement (B) is incorrect. An oil market move from a state of normal backwardation to contango and margin calls created a major cash crunch for Metallgesellschaft.6. Existing risk models generally fail to capture the distribution of large l osses over extended horizons. Theother statements are correct.7. As we know, cov(X, Y1 + Y2) = cov(X, Y1) + cov(X, Y2). So cov(z, x + y) = cov(z, x) + cov(z, y). That means cov(z, x) + cov(z, y) = 0. So if cov(z, x) = 1,cov(z, y) = –1, (A) and (B) are incorrect; if cov(z, x) = cov(z, y) = 0, (C) is incorrect.8. From the given information, there is a 77% chance that stock X increases and a 61% chance that stock Y increases. Since we have no additional information about the distributions, we know the maximum possible probability that both increases cannot be greater than 61%, since stock Y decreases 39% of the time. Suppose whenever Y increases, X increases as well, which is possibl e because X increases 77% of the time, in which case the probability both increase is 61%. This is the maximum possible probability that both increase.(B) is 0.61 * 0.77 = 0.4697.(C) is the maximum probability that both decrease.(D) is the probability that X increases.9. Use Bayes' Theorem:P (Neutral | Constant) = P (Constant | Neutral) * P (Neutral) / P(Constant) = 0.2 * 0.3 / (0.1 * 0.2 + 0.2 * 0.3 + 0.15 * 0.5) = 0.38710. Age and experience are highly correlated and woul d lead to multicollinearity. In fact, l ow t-statistics but a high R2 do suggest this problem also.Answers (A), (B), and (C) are not likely causes and are therefore incorrect.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。

FRM一级_风险管理基础&定量分析答案(★★)

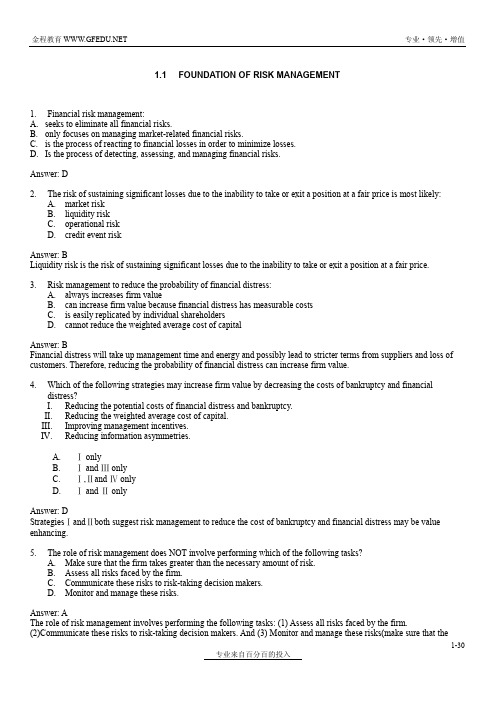

Answer: D StrategiesⅠandⅡboth suggest risk management to reduce the cost of bankruptcy and financial distress may be value enhancing. 5. The role of risk management does NOT involve performing which of the following tasks? A. Make sure that the firm takes greater than the necessary amount of risk. B. Assess all risks faced by the firm. C. Communicate these risks to risk-taking decision makers. D. Monitor and manage these risks.

Answer: D The CAPM assumes that investors all have the same horizon (as well as expectations). This means that the distribution of the horizons is not normal because normality implies a bell-shaped curve distribution, which would have a positive variance and, hence, dispersion. 10. Markowitz Portfolio Theory is not accurately described as including an assumption that: A. risk is measured by the range of expected returns B. for a given risk level, investor prefer higher returns to lower returns C. investors base all their decisions on expected return and risk D. investors focus on utility maximization

FRM一级模拟题(2)

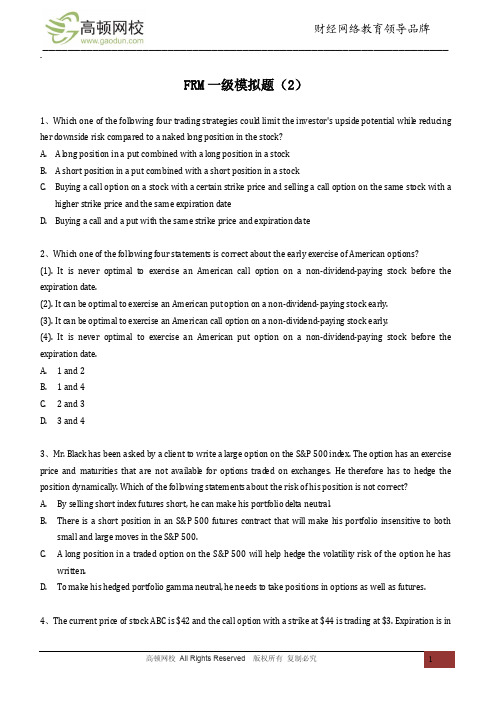

FRM一级模拟题(2)1、Which one of the foll owing four trading strategies coul d limit the investor's upside potential while reducing her d ownsid e risk compared to a naked long position in the stock?A. A long position in a put combined with a long position in a stockB. A short position in a put combined with a short position in a stockC.Buying a call option on a stock with a certain strike price and selling a call option on the same stock with ahigher strike price and the same expiration dateD.Buying a call and a put with the same strike price and expiration date2、Which one of the foll owing four statements is correct about the early exercise of American options? (1). It is never optimal to exercise an American call option on a non-divid end-paying stock before the expiration date.(2). It can be optimal to exercise an American put option on a non-dividend-paying stock early.(3). It can be optimal to exercise an American call option on a non-dividend-paying stock early.(4). It is never optimal to exercise an American put option on a non-dividend-paying stock before the expiration date.A. 1 and 2B. 1 and 4C. 2 and 3D. 3 and 43、Mr. Black has been asked by a client to write a large option on the S&P 500 ind ex. The option has an exercise price and maturities that are not availabl e for options traded on exchanges. He therefore has to hedge the position dynamically. Which of the foll owing statements about the risk of his position is not correct?A.By selling short index futures short, he can make his portfolio delta neutral.B.There is a short position in an S&P 500 futures contract that will make his portfolio insensitive to bothsmall and large moves in the S&P 500.C. A long position in a traded option on the S&P 500 will help hedge the volatility risk of the option he haswritten.D.To make his hedged portfolio gamma neutral, he needs to take positions in options as well as futures.4、The current price of stock ABC is $42 and the call option with a strike at $44 is trading at $3. Expiration is inone year. The corresponding put is priced at $2. Which of the foll owing trading strategies will result in arbitrage profits? Assume that the annual risk-free rate is 10%, and that there is a risk-free bond paying the risk-free rate that can be shorted costl essly. There are no transaction costs.A.Long position in both the call option and the stock, and short position in the put option and risk-free bondB.Long position in both the call option and the put option, and short position in the stock and risk-free bondC.Long position in both the call option and risk-free bond, and short position in the stock and the put optionD.Long position in both the put option and the risk-free bond, and short position in the stock and the putoption5、The foll owing table gives the prices of two out of three U.S. Treasury notes for settlement on August 30, 2008. All three notes will mature exactly one year later on August 30, 2009.Coupon Price2$98.404?6$101.30Approximately, what woul d the price of the 41/2 U.S. Treasury note?A.$99.20B.$99.40C.$99.80D.$100.206、The observed zero yiel d curve is given by the foll owing data:1-year spot rate = 3.65%2-year spot rate = 3.99%3-year spot rate = 4.11%Using the data for the spot curve, the forward rate on a one-year contract maturing in two years is closest to:A. 3.20%B. 3.79%C. 4.33%D. 4.15%7、The spot price of gold is US200/oz and the price of a one-year gold futures contract is US205/oz. Assuming that the annual risk-free rate remains 5% and there are no arbitrage opportunities, which of the foll owing situations would cause backwardation1. Future value of the net cost for carrying physical gol d per oz increases.2. Future value of the net cost for carrying physical gol d per oz decreases.3. There is a net positive benefit from carrying physical gold.4. There is a net negative cost from carrying physical gold.A. 1 and 4 onlyB. 3 onlyC. 2 and 4D. 1 and 38、The foll owing table gives the cl osing prices and yiel ds of a particular liquid bond over the past few days. Day Price YieldMonday $106.3 4.25%Tuesday $105.8 4.20%Wednesday $106.1 4.23%What is the approximate duration of the bond?A.18.8B.9.4C. 4.7D. 1.99、John Flag, the manager of a USD 150 million distressed bond portfolio, conducts stress tests on the portfolio. The portfolio's annualized return is 12%, with an annualized return volatility of 25%. In the past two years, the portfolio encountered several days when the daily value change of the portfolio was more than 3 standard deviations. If the portfolio woul d suffer a 4-sigma daily event, estimate the change in the value of this portfolio.A.$9.48 millionB.$23.70 millionC.$37.50 millionD.$150 million10、A single stock has a price of $10 and a current daily volatility of 2%. Using the delta-normal approximation, the VaR on a l ong at-the-money call on this stock over a one-day holding period is:A.$0.1645B.$0.329C.$1.645D.$16.45Answer and Explanation:1. Long position in a put combined with long position in a stock could limit only the d ownside risk; (A) is incorrect.Short position in a put combined with short position in a stock coul d limit only the upside risk; (B) is incorrect. Buying a call option on a stock with a certain strike price and selling a call option on the same stock with a higher strike price and the same expiration date could limit both the upside and d ownside risk; (C) is correct. Buying a call and a put with the same strike price and expiration date could limit only the d ownsid e risk; (D) is incorrect.2. There are no advantages to exercising early if the investor plans to keep the stock for the remaining life of the call option, because the early exercise woul d sacrifice the interest that woul d be earned. If the strike price is paid out later on expiration date after the early exercise, the investor may suffer the risk that the stock price will fall bel ow the strike price. As the stock pays no dividend, the early exercise will earn no income from the stock. So it is never optimal to exercise an American call option on a non-divid end-paying stock before the expiration date.At any given time during its life, a put option shoul d always be exercised early if it is sufficiently deep in-the-money. So it can be optimal to exercise an American put option on a non-dividend-paying stock early. As a result, answer (A) is correct.3. The short ind ex futures contract makes the portfolio delta neutral. It does not help with large moves.4. (A) is incorrect as this would not yield arbitrage profit.(B) is incorrect as this woul d not yield arbitrage profit.(C) is correct.The put-call parity relation is: stock + put = pv(strike) + callTherefore, for no arbitrage opportunity the foll owing relation should hold:42 + 2 = (44/1.10) + 3But 44 > 43Therefore, there is an arbitrage opportunity. The arbitrage profit is 49 – 42 = 7 by taking a long position in a call and buying the risk-free bond and going short on the stock and the put.(D) is incorrect as this woul d not yield arbitrage profit.5. 2.875% * X +6.25% * (1 – X) = 4.5%X = 52%The portfolio that has cash fl ows identical to the 41/2 bond consists of 52% of the 27/8 and 48% of the 61/4 bonds. As this portfolio has cash fl ows identical to the 41/2 bond, precluding arbitrage, the price of the portfolio should equal to 52% * 97.4 + 48% * 101.30, or $99.806. (A) is incorrect because the rate cannot be bel ow the spot rates as the zero curve has an upward sl ope.(B) is incorrect because the zero curve is upward-sloping and the rate must be higher than 3.99%.(C) is the correct answer:Rf = [(1 + r2) ^ t2/(1 + r1) ^ t1] – 1Rf = (r2t2 – r1t1)/(t2 – t1)[((1 + 3.99%) ^ 2)/(1 + 3.65%)] – 1 = 4.33%(D) is impossibl e because if we invest for a year at 3.65% and the next year at 4.15%, it is not the same as investing during two years at 3.99%.7. The expected spot price 1 year later is US210/oz. So, if no arbitrage opportunity exists, the future value of the net cost for carrying the physical gol d is US5/oz.If the future value of the net cost for carrying the gold per oz increases and exceeds US10/oz, the spot price one year later will be less than the current spot price. Thus backwardation occurs.Also, if the net benefit for carrying the gol d exists and the future value of such benefit exceeds US5/oz (with holding future value of net cost being constant), backwardation occurs too.Also, if the net negative from carrying the gol d exists and the future value of such benefit exceeds US5/oz (with holding future value of net cost being constant), backwardation d oes not occur.Therefore, both statement 1 and statement 3 are correct.(A) is incorrect because statement 3 is correct too.(B) is incorrect because statement 1 is correct too.(C) is incorrect because statement 2 is incorrect.(D) is correct because both statement 1 and statement 3 are correct.Remark: The tricky part of the question is that the candidate may feel confused since the no-arbitrage future price should be US210/oz (if net cost of storage d oes not exist), rather than the price US205/oz given in the question (where the net cost of storage exists).8. The duration can be approximated from the price changes.(106.3 – 105.8)/106.3/.0005 = 9.4(106.3 – 106.1)/106.3/.0002 = 9.4etc.9. Daily volatility is equal to 0.25 * sqrt (1/250) = 0.0158. A 4-sigma event therefore implies a l oss equal to 4*0.0158*150 = 9,486,832The correct answer is (A).(B) calculates the daily volatility and multiplies the volatility by the value of the portfolio.(C) multiplies the portfolio value by its annual volatility, or divides the portfolio value by 4.(D) attempts the shortcut of reducing the portfolio value by 4 times 25%, which is 100% (i.e., the value of the portfolio).10. This question requires candidates to know the formula for the delta-normal VaR approximation, and also to know that the delta of an at-the-money call is 0.5.The correct answer is (A).(B) uses a delta of 1.(C) confuses the decimal point.(D) uses 2 instead of 2% for the volatility.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。

FRM一级模考

FRM一级模拟题1 .If the daily returns of two assets are positively correlated, then:A. the covariance of their daily returns must be positiveB. the covariance of their daily returns must be zeroC. the covariance of their daily returns must be negativeD. nothing can be said about the covariance of their daily returnsAnswer: AIf variables are positively correlated, the covariance between the Variables will also be positive.2 .You are given that X and Y are random variables, and each of which follows a standard normal distribution with Covariance (X, Y) = 0.4. What is the variance of (5X+2Y)?A. 11.0B. 29.0C. 29.4D. 37.0Answer: DSince each variable is standardized, its variance is one. Therefore, Var(5X+2Y) = 25 x Var(X)+4xVar(Y)+2 x 5x2x Cov(X,Y) =25+4+8 = 373 . What is the covariance between populations A and B?If the variance ofA is 12, what is the variance of B?A. 10.00B. 2.89C. 8.33D. 14.40Answer:C5 . Which one of the following statements about the correlation coefficient is FALSE?A. It always ranges from -1 to +1B. A correlation coefficient of zero means that two random variables are independentC. It is a measure of linear relationship between two random variablesD. It can be calculated by scaling the covariance between two random variables Answer:BCorrelation describes the linear relationship between two variables. While we would expect to find a correlation of zero for independent .variables, finding a correlation of zero does not mean that two variables are independent.。

frm考试培训训练FRM一级模拟题

frm考试培训训练FRM一级模拟题高顿FRM考试培训训练FRM一级模拟题:If there are restrictions on short selling and borrowing at the risk-free rate,we would expect to see that:A.all investors hold the same market portfolio as predicted by the CAPM.B.highly risk-averse individuals tend to hold heavily diversified portfolios,while those with less risk aversion tend to concentrate their portfolios.C.less risk-averse individuals tend to hold heavily diversified portfolios,while those with more risk aversion tend to concentrate their portfolios.D.both highly risk-averse individuals and those with less risk aversion tend to concentrate their portfolios.Answer:BRestrictions on short selling or borrowing at the risk-free rate make investors construct portfolios with considerably different compositions.Highly risk-averse individuals tend to hold heavily diversified portfolios,while those with less risk aversion tend to concentrate their portfolios.FRM的一级考试四科目复习方法:风险管理基础(Foundations of Risk Management)考试比重:20%和定量分析(Quantitative Analysis)考试比重:20%我的数学底子并不好,理科废柴生。

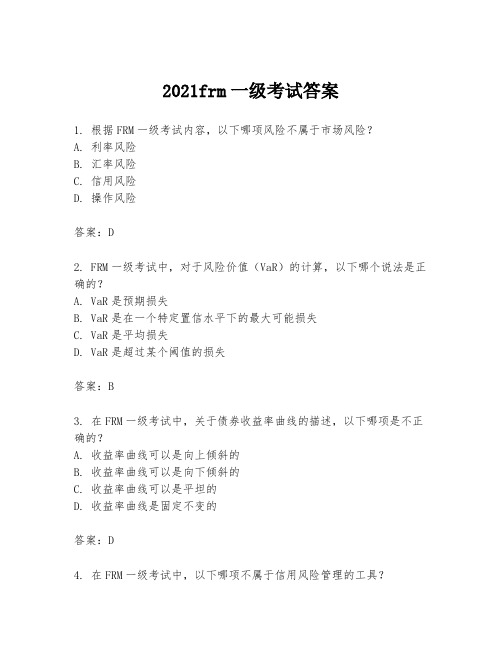

2021frm一级考试答案

2021frm一级考试答案1. 根据FRM一级考试内容,以下哪项风险不属于市场风险?A. 利率风险B. 汇率风险C. 信用风险D. 操作风险答案:D2. FRM一级考试中,对于风险价值(VaR)的计算,以下哪个说法是正确的?A. VaR是预期损失B. VaR是在一个特定置信水平下的最大可能损失C. VaR是平均损失D. VaR是超过某个阈值的损失答案:B3. 在FRM一级考试中,关于债券收益率曲线的描述,以下哪项是不正确的?A. 收益率曲线可以是向上倾斜的B. 收益率曲线可以是向下倾斜的C. 收益率曲线可以是平坦的D. 收益率曲线是固定不变的答案:D4. 在FRM一级考试中,以下哪项不属于信用风险管理的工具?A. 信用衍生品B. 信用评级C. 资产证券化D. 利率互换答案:D5. 根据FRM一级考试内容,以下哪项是操作风险的主要来源?A. 市场波动B. 法律诉讼C. 欺诈行为D. 自然灾害答案:C6. 在FRM一级考试中,以下哪项是流动性风险管理的关键要素?A. 资产负债管理B. 资本充足率C. 利率风险管理D. 信用评级答案:A7. 根据FRM一级考试内容,以下哪项不是风险管理的主要目标?A. 减少损失B. 增加收益C. 遵守法规D. 保护公司声誉答案:B8. 在FRM一级考试中,以下哪项是压力测试的目的?A. 评估在极端市场条件下的表现B. 预测未来的市场趋势C. 评估日常风险管理的有效性D. 计算风险价值(VaR)答案:A9. 根据FRM一级考试内容,以下哪项是风险限额设置的主要依据?A. 历史数据B. 市场预测C. 管理层的风险偏好D. 竞争对手的风险限额答案:C10. 在FRM一级考试中,以下哪项是风险管理框架的核心组成部分?A. 风险识别B. 风险评估C. 风险监控D. 所有选项答案:D结束语:以上是2021年FRM一级考试的部分答案,希望能够帮助考生更好地复习和准备考试。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

FRM一级练习题(2)1、If the daily, 95% confid ence l evel value at risk (VaR) of a portfolio is correctly estimated to be USD 10,000, one would expect that:A. In 1 out of 20 days, the portfolio value will decline by USD 10,000 or l ess.B. In 1 out of 95 days, the portfolio value will decline by USD 10,000 or l ess.C. In 1 out of 95 days, the portfolio value will decline by USD 10,000 or more.D. In 1 out of 20 days, the portfolio value will decline by USD 10,000 or more.2、By reducing the risk of financial distress and bankruptcy, a firm's use of derivatives contracts to hedge its cash fl ow uncertainty will:A. Lower its value due to the transaction costs of derivatives trading.B. Enhance its value since investors cannot hedge such risks by themselves.C. Have no impact on its value as investors can costl essly diversify this risk.D. Have no impact as only systematic risks can be hedged with derivatives.3、An analyst at CAPM Research Inc. is projecting a return of 21% on portfolio A. The market risk premium is 11%, the volatility of the market portfolio is 14%, and the risk-free rate is 4.5%. Portfolio A has a beta of 1.5. According to the Capital Asset Pricing Model (CAPM), which of the foll owing statements is true?A. The expected return of portfolio A is greater than the expected return of the market portfolio.B. The expected return of portfolio A is less than the expected return of the market portfolio.C. The expected return of portfolio A has l ower volatility than the market portfolio.D. The expected return of portfolio A is equal to the expected return of the market portfolio.4、Suppose portfolio A has an expected return of 8% and volatility of 20%, and its beta is 0.5. Suppose the market has an expected return of 10% and volatility of 25%. Finally, suppose the risk-free rate is 5%. What is Jensen's alpha for portfolio A?A. 10%B. 1%C. 0.5%D. 15%5、Which of the foll owing statements regarding Metallgesellschaft's failure is incorrect?A. The futures and swap positions Metallgesellschaft entered into introduced significant credit risk for the company.B. An oil market move from a state of contango to normal backwardation and margin calls created a major cash crunch for Metallgesellschaft.C. Metallgesellschaft engaged in a stack-and-roll hedge, and as spot prices began to decrease more than futures prices, roll over losses could not be recovered.D. Because of the size of its position in heating and gasoline oil futures, Metallgesellschaft was exposed to market liquidity risk and had difficulty liquidating its position.6、Which of the foll owing statements is incorrect?A. Existing risk models often rely on historical data and are most precise for short horizons, like days.B. Market crises often involve a dramatic withdrawal of liquidity from the market.C. During crisis periods, firms will often make multipl e losses that exceed daily VaRs, and these losses can be large enough to substantially weaken them.D. When evaluating risks associated with a potential crisis period, existing risk models generally fail to effectively incorporate the risk of a decrease in liquidity but do effectively capture the distribution of large losses over an extended horizon beyond one day.7、If cov(z, x + y) = 0 , which of the foll owing must be true?A. cov(z, x) = 0, cov(z, y) = 0B. cov(z, x) * cov(z, y) = 0C. cov(z, x) ! 0, cov(z, y) ! 0D. None of the above8、Angela Santori buys two stocks, stock X and stock Y. Suppose that the only information she has about the return distributions is that the probability of a stock price decrease in one year for stock X is 23% and for stock Y is 39%. What is the highest possibl e probability that both stock prices increase in one year?A. 61%B. 46.97%C. 23%D. 77%9、John is forecasting a stock's performance in 2010 conditional on the state of the economy of the country in which the firm is based. He divides the economy's performance into three categories of "good," "neutral," and"poor" and the stock's performance into three categories of " increase," "constant," and "d ecrease."He estimates:1、The probability that the state of the economy is good is 20%. If the state of the economy is good, theprobability that the stock price increases is 80% and the probability that the stock price decreases is 10%.2. The probability that the state of the economy is neutral is 30%. If the state of the economy is neutral, theprobability that the stock price increases is 50% and the probability that the stock price decreases is 30%.3. If the state of the economy is poor, the probability that the stock price increases is 15% and theprobability that the stock price decreases 70%.Billy, his supervisor, asks him to estimate the probability that the state of the economy is neutral given that the stock performance is constant. John's best assessment of that probability is closest to:A. 20%B. 15.5%C. 19.6%D. 38.7%10、You built a linear regression model to analyze annual salaries for a developed country. You incorporated two independent variables, age and experience, into your model. Upon reading the regression results, you noticed that the coefficient of "experience" is negative, which appears to be counterintuitive. In addition, you have discovered that the coefficients have l ow t-statistics but the regression mod el has a high R2. What is the most likely cause of these results?A. Incorrect standard errorsB. HeteroskedasticityC. Serial correlationD. Multicollinearity参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。