《商业银行管理》word版

商业银行合规风险管理指引

商业银行合规风险管理指引第一章总则第一条为加强商业银行合规风险管理,维护商业银行安全稳健运行,根据《中华人民共和国银行业监督管理法》和《中华人民共和国商业银行法》,制定本指引。

第二条在中华人民共和国境内设立的中资商业银行、外资独资银行、中外合资银行和外国银行分行适用本指引。

在中华人民共和国境内设立的政策性银行、金融资产管理公司、城市信用合作社、农村信用合作社、信托投资公司、企业集团财务公司、金融租赁公司、汽车金融公司、货币经纪公司、邮政储蓄机构以及经银监会批准设立的其他金融机构参照本指引执行。

第三条本指引所称法律、规则和准则,是指适用于银行业经营活动的法律、行政法规、部门规章及其他规范性文件、经营规则、自律性组织的行业准则、行为守则和职业操守。

本指引所称合规,是指使商业银行的经营活动与法律、规则和准则相一致。

本指引所称合规风险,是指商业银行因没有遵循法律、规则和准则可能遭受法律制裁、监管处罚、重大财务损失和声誉损失的风险。

本指引所称合规管理部门,是指商业银行内部设立的专门负责合规管理职能的部门、团队或岗位。

第四条合规管理是商业银行一项核心的风险管理活动。

商业银行应综合考虑合规风险与信用风险、市场风险、操作风险和其他风险的关联性,确保各项风险管理政策和程序的一致性。

第五条商业银行合规风险管理的目标是通过建立健全合规风险管理框架,实现对合规风险的有效识别和管理,促进全面风险管理体系建设,确保依法合规经营。

第六条商业银行应加强合规文化建设,并将合规文化建设融入企业文化建设全过程。

合规是商业银行所有员工的共同责任,并应从商业银行高层做起。

董事会和高级管理层应确定合规的基调,确立全员主动合规、合规创造价值等合规理念,在全行推行诚信与正直的职业操守和价值观念,提高全体员工的合规意识,促进商业银行自身合规与外部监管的有效互动。

第七条银监会依法对商业银行合规风险管理实施监管,检查和评价商业银行合规风险管理的有效性。

商业银行理财业务档案管理办法

商业银行理财业务档案管理办法第一章总则第一条为规范本行理财业务档案管理,保证理财业务档案安全、完整,确保理财业务资产安全,促进理财业务健康发展,根据有关政策法规、监管政策和本行有关规定,制订本办法。

第二条本办法所称理财业务是指本行根据监管规定,接受客户委托和授权,按照与客户事先约定的方式进行投资和资产管理,并收取一定管理费用的行为。

理财业务涉及的产品类型包括银行理财产品以及银行理财管理计划等,具体包括:(一)面向本行金融市场、企业金融、零售金融(含私人银行)等各条线客户发售的本行创设的理财产品;(二)通过银银平台理财门户(钱大掌柜)、直销银行等各类渠道等向行内外客户发售的本行创设的理财产品;(三)中国银监会规定的其他属于银行理财的产品。

各类代销类产品、代理收付类产品、本银行集团各子公司资产管理业务等均不在本办法规范范围内。

第三条本办法所称理财业务档案是指经营机构(包括分行和总行业务部门,以下简称“经营机构”)在理财业务开展过程中形成的用以记录和反映理财业务全过程的重要文件、凭据和图表、声像等档案。

第四条理财业务档案管理严格按照监管政策和总行规定,遵循以下原则:(一)本级机构集中统一管理原则。

经营机构应指定单一部门(或处室)统一对本机构的理财业务档案进行管理。

(二)及时完整、真实有效原则。

经营机构的产品创设和发行部门(或处室)应在规定的时间内将业务档案移交于档案管理部门(或处室),并对移交前业务档案的真实性、有效性及完整性负责。

(三)保密性原则。

业务档案涉及到国家、全行和客户秘密,档案管理人员、调阅人员和其他相关人员必须严格遵守保密原则。

第五条本办法属于“管理办法”,适用于本行各级机构。

第二章理财业务档案管理职责分工第六条总行资产管理部负责制定全行理财业务档案管理规范及制度,督促经营机构做好理财业务档案保管。

总行资产管理部负责对已移交的业务档案定期检查,发现问题时督促经营机构及时纠正;定期检查经营机构业务档案管理工作,并根据业务需要组织档案管理培训交流工作。

银监发201919商业银行信息科技风险管理指引word精品文档23页

商业银行信息科技风险管理指引第一章总则第一条为加强商业银行信息科技风险管理,根据《中华人民共和国银行业监督管理法》、《中华人民共和国商业银行法》、《中华人民共和国外资银行管理条例》,以及国家信息安全相关要求和有关法律法规,制定本指引。

第二条本指引适用于在中华人民共和国境内依法设立的法人商业银行。

政策性银行、农村合作银行、城市信用社、农村信用社、村镇银行、贷款公司、金融资产管理公司、信托公司、财务公司、金融租赁公司、汽车金融公司、货币经纪公司等其他银行业金融机构参照执行。

第三条本指引所称信息科技是指计算机、通信、微电子和软件工程等现代信息技术,在商业银行业务交易处理、经营管理和内部控制等方面的应用,并包括进行信息科技治理,建立完整的管理组织架构,制订完善的管理制度和流程。

第四条本指引所称信息科技风险,是指信息科技在商业银行运用过程中,由于自然因素、人为因素、技术漏洞和管理缺陷产生的操作、法律和声誉等风险。

第五条信息科技风险管理的目标是通过建立有效的机制,实现对商业银行信息科技风险的识别、计量、监测和控制,促进商业银行安全、持续、稳健运行,推动业务创新,提高信息技术使用水平,增强核心竞争力和可持续发展能力。

第二章信息科技治理第六条商业银行法定代表人是本机构信息科技风险管理的第一责任人,负责组织本指引的贯彻落实。

第七条商业银行的董事会应履行以下信息科技管理职责:(一)遵守并贯彻执行国家有关信息科技管理的法律、法规和技术标准,落实中国银行业监督管理委员会(以下简称银监会)相关监管要求。

(二)审查批准信息科技战略,确保其与银行的总体业务战略和重大策略相一致。

评估信息科技及其风险管理工作的总体效果和效率。

(三)掌握主要的信息科技风险,确定可接受的风险级别,确保相关风险能够被识别、计量、监测和控制。

(四)规范职业道德行为和廉洁标准,增强内部文化建设,提高全体人员对信息科技风险管理重要性的认识。

(五)设立一个由来自高级管理层、信息科技部门和主要业务部门的代表组成的专门信息科技管理委员会,负责监督各项职责的落实,定期向董事会和高级管理层汇报信息科技战略规划的执行、信息科技预算和实际支出、信息科技的整体状况。

(完整word版)农商行从业人员行为规范

某某农村商业银行股份有限公司从业人员行为规范第一章总则第一条为了加强某某农村商业银行股份有限公司(以下简称“本行”) 从业人员管理,提高在岗人员素质,规范从业行为,塑造本行形象,根据国家有关法律法规、中国银监会印发的《银行业金融机构从业人员职业操守指引》和社会道德规范,结合本行实际,制定本规范。

第二条本行从业人员必须认真履行公民义务和工作职责,切实维护行业利益和信誉,自觉做到思想先进、道德高尚、业务优良、纪律严明、服务规范。

第三条本规范适用于本行全体从业人员,是全体从业人员必须自觉遵守的基本行为准则,是本行对员工日常行为进行管理的依据。

第二章职业道德第四条热爱祖国,热爱人民,热爱金融事业。

(一)拥护党的基本路线,贯彻执行党和国家的金融方针政策,自觉与党中央和上级保持高度一致。

(二)有强烈的社会责任感,自觉维护国家利益和集体利益。

(三)有强烈的主人翁责任感,关心本行改革发展,积极建言献策,提出合理化建议。

(四)有高度的职业荣誉感,努力为本行发展贡献智慧和力量。

第五条学法知法守法,严格依法办事。

(一)遵守国家法律,履行法定义务,保守国家秘密和商业秘密,维护金融安全。

(二)敢于抵制不正之风,敢于同各种违规、违纪和违法犯罪行为作坚决的斗争。

(三)坚决抵制非法集资及商业贿赂,拒绝黄、赌、毒等不法行为。

第六条遵守社会公德,维护公平正义。

(一)以“八荣八耻”作为个人的道德准则和行为指南,努力做到热心公益、奉献爱心、勤俭自强、明礼诚信、见义勇为,大力弘扬中华民族传统美德。

(二)恪守“客户自愿”的公平竞争原则,自觉抵制贬低同业、虚假宣传等不正当竞争行为。

第三章职业素养第七条坚持“理论联系实际、学以致用、讲求实效”的原则,自觉地持之以恒地搞好学习,努力提高个人素质,适应事业发展。

第八条加强政治思想修养,不断提高政策理论水平。

(一)认真学习时事政治,关注社会焦点问题,积极参加单位组织的政治学习活动,提高政治敏锐性和是非鉴别力。

(完整word版)我国商业银行的利润结构分析

我国商业银行的利润结构分析引言商业银行作为追求利润的金融机构,其获取利润的能力,利润的数量和结构都关系着其生存和发展,在遵循安全性,流动性,盈利性“三性”经营原则的前提下,银行的利润结构在某种程度上可以反映出该行的利润结构,经营理念以及运行机制中存在的问题和缺陷。

在西方商业银行经过数百年的发展,其经营理念已发生深刻变化,伴随的表现即利润结构的不断调整和经营效益的提高。

从短期资产负债业务为主到全面的资产负债业务管理,再到服务性中间业务的崛起和投资业务的不断发展,西方商业银行的利润结构趋于稳健合理,这使得其进入一个成熟高效的全面发展阶段。

与此相比,我国商业银行利润结构所暴露出的问题还很多。

当前银行业改革正大刀阔斧的进行,股份制改革,实施有效的内部治理,建立健全的风险管理机制等,这一系列相互关联的改革涉及到银行当前经营的方方面面,而对于利润结构的分析恰恰是一个切入点,通过对其特点及成因的分析,我们可以发现并研究一些深层次的问题,从而有效地改善我国商业银行的运营和经营管理。

一我国商业银行利润结构现状与成因商业银行利润来源包括很多项目,主要有:利差净收入,手续费收入(中间业务收入),投资收益,营业外收入等,由于各行损益表结构存在差异,对各项目的划分也有所不同,我们很难得到各个利润来源的准确数据并进行比较分析。

结合我国商业银行利润结构特点,我选取了其中主要几项进行分析,我们可以通过以下几张表格发现我国商业银行利润结构的最主要特点。

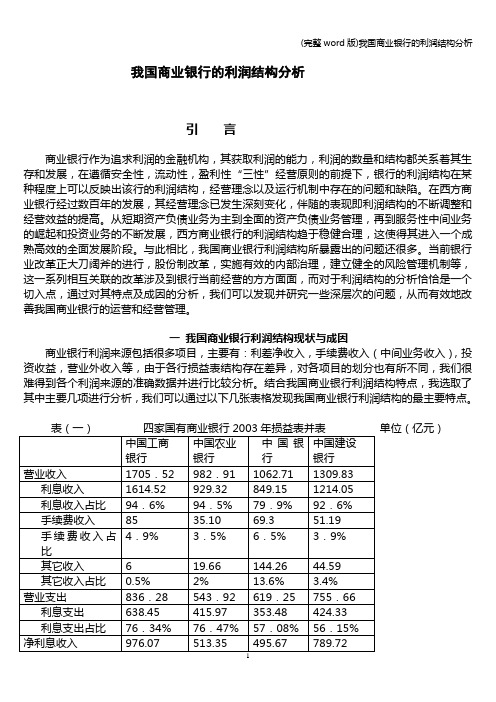

单位(亿元)表中数据取自2004年《中国金融年鉴》表(二)十一家股份制银行2003年损益表并表(亿元)注:表中数据取自2004年《中国金融年鉴》34从表(一)表(二)中可以看出,利息收入一直是我国商业银行利润的最主要来源,2003年,国有商业银行利息收入占营业收入之比平均为90.4%,股份制商业银行平均为72.18%。

国有商业银行中由于中国银行传统上在国际资金清算,出口服务等方面的优势,具有中间业务性质的业务开展较多,利差收入占比相对较少。

(完整word版)商业银行声誉风险管理指引

商业银行声誉风险管理指引第一条为引导商业银行有效管理声誉风险,完善全面风险管理体系,维护市场信心和金融稳定,根据《中华人民共和国银行业监督管理法》、《中华人民共和国商业银行法》以及其他有关法律法规,制定本指引。

第二条本指引所称声誉风险是指由商业银行经营、管理及其他行为或外部事件导致利益相关方对商业银行负面评价的风险。

声誉事件是指引发商业银行声誉风险的相关行为或事件。

重大声誉事件是指造成银行业重大损失、市场大幅波动、引发系统性风险或影响社会经济秩序稳定的声誉事件。

第三条商业银行应将声誉风险管理纳入公司治理及全面风险管理体系,建立和制定声誉风险管理机制、办法、相关制度和要求,主动、有效地防范声誉风险和应对声誉事件,最大程度地减少对社会公众造成的损失和负面影响。

第四条商业银行董事会应制定与本行战略目标一致且适用于全行的声誉风险管理政策,建立全行声誉风险管理体系,监控全行声誉风险管理的总体状况和有效性,承担声誉风险管理的最终责任。

其主要职责包括:(一)审批及检查高级管理层有关声誉风险管理的职责、权限和报告路径,确保其采取必要措施,持续、有效监测、控制和报告声誉风险,及时应对声誉事件。

(二)授权专门部门或团队负责全行声誉风险管理,配备与本行业务性质、规模和复杂程度相适应的声誉风险管理资源。

(三)明确本行各部门在声誉风险管理中的职责,确保其执行声誉风险管理制度和措施。

(四)确保本行制定相应培训计划,使全行员工接受相关领域知识培训,知悉声誉风险管理的重要性,主动维护银行的良好声誉。

(五)培育全行声誉风险管理文化,树立员工声誉风险意识。

第五条商业银行应建立和制定适用于全行的声誉风险管理机制、办法、相关制度和要求,其内容至少包括:(一)声誉风险排查,定期分析声誉风险和声誉事件的发生因素和传导途径。

(二)声誉事件分类分级管理,明确管理权限、职责和报告路径。

(三)声誉事件应急处置,对可能发生的各类声誉事件进行情景分析,制定预案,开展演练。

商业银行管理彼得S.罗斯英文原书第8版-英语试题库Chap007

Chapter 7Risk Management for Changing Interest Rates: Asset-Liability Management and Duration TechniquesFill in the Blank Questions1. The ___________________ view of assets and liabilities held that the amount and types ofdeposits was primarily determined by customers and hence the key decision a bank needed to make was with the assets.Answer: asset management2. Recent decades have ushered in dramatic changes in banking. The goal of__________________ was simply to gain control of the bank's sources of funds.Answer: liability management3. The__________________________ is the interest rate that equalizes the current market price ofa bond with the present value of the future cash flows.Answer: yield to maturity (YTM)4. The __________________ risk premium on a bond allows the investor to be compensated fortheir projected loss in purchasing power from the increase in the prices of goods and services in the future.Answer: inflation5. The __________________ shows the relationship between the time to maturity and the yield tomaturity of a bond. It is usually constructed using treasury securities since they are assumed to have no default risk.Answer: yield curve6. The __________________ risk premium on a bond reflects the differences in the ease and abilityto sell the bond in the secondary market at a favorable price.Answer: liquidityplanning period.Answer: Interest-sensitive assets8. __________________________ is the difference between interest-sensitive assets andinterest-sensitive liabilities.Answer: Dollar interest-sensitive gap9. A(n)__________________________ means that the bank has more interest-sensitive liabilitiesthan interest-sensitive assets.Answer: negative interest-sensitive gap (liability sensitive)10. The bank's__________________________ takes into account the idea that the speed (sensitivity)of interest rate changes will differ for different types of assets and liabilities.Answer: weighted interest-sensitive gap11. __________________________ is the coordinated management of both the bank's assets and itsliabilities.Answer: Funds management12. __________________________ is the risk due to changes in market interest rates which canadversely affect the bank's net interest margin, assets and equity.Answer: Interest rate risk13. The__________________________ is the rate of return on a financial instrument using a 360day year relative to the instrument's face value.Answer: bank discount rate14. The __________________________ component of interest rates is the risk premium due to theprobability that the borrower will miss some payments or will not repay the loan.Answer: default risk premium15. __________________ is the weighted average maturity for a stream of future cash flows. It is adirect measure of price risk.Answer: Duration16. __________________________ is the difference between the dollar-weighted duration of theasset portfolio and the dollar-weighted duration of the liability portfolio.Answer: Duration gap17. A(n)__________________________ duration gap means that for a parallel increase in all interestrates the market value of net worth will tend to decline.Answer: positive18. A(n)__________________________ duration gap means that for a parallel increase in allinterest rates the market value of net worth will tend to increase.Answer: negative19. The __________________ refers to the periodic fluctuations in the scale of economic activity.Answer: business cycle20. The__________________________ is equal to the duration of each individual type of assetweighted by the dollar amount of each type of asset out of the total dollar amount of assets.Answer: duration of the asset portfolio21. The__________________________ is equal to the duration of each individual type of liabilityweighted by the dollar amount of each type of asset out of the total dollar amount of assets.Answer: duration of the liability portfolio22. A bank is __________________ against changes in its net worth if its duration gap is equal tozero.Answer: immunized (insulated or protected)23. The relationship between a change in an asset's price and an asset’s change in the yield or interestrate is captured by __________________________.Answer: convexity24. The change in a financial institution's __________________ is equal to difference in the durationof the assets and liabilities times the change in the interest rate divided by the starting interest rate times the dollar amount of the assets and liabilities.Answer: net worth25. When a bank has a positive duration gap a parallel increase in the interest rates on the assets andliabilities of the bank will lead to a(n) __________________ in the bank's net worth.Answer: decrease26. When a bank has a negative duration gap a parallel decrease in the interest rates on the assets andliabilities of the bank will lead to a(n)_________________________ in the bank's net worth.Answer: decrease27. U.S. banks tend to do better when the yield curve is upward-sloping because they tend to have____________ maturity gap positions.Answer: positive28.One government-created giant mortgage banking firms which have subsequently been privatizedis the .Answer: FNMA or Fannie Mae (or FHLMC or Freddie Mac)29.One part of interest rate risk is .This part of interest rate risk reflects that as interest rates rise, prices of securities tend to fall.Answer: price risk30.One part of interest rate riskis . This part of interest rate risk reflects that as interest rates fall, any cash flows that are received before maturity areinvested at a lower interest rate.Answer: reinvestment risk31.When a borrower has the right to pay off a loan early which reduced the lender’s expected rate ofreturn it is called .Answer: call risk32.In recent decades, banks have aggressively sought to insulate their assets and liability portfoliosand profits from the ravages if interest rate changes. Many banks now conduct theirasset-liability management strategy with the help of anwhich often meets daily.Answer: asset-liability committee33.is interest income from loans and investmentsless interest expenses on deposits and borrowed funds divided by total earning assets.Answer: Net interest margin (NIM)34.are those liabilities that whichmature or must be repriced within the planning period.Answer: Interest-sensitive liabilities35.Variable rate loans and securities are included as part offor banks.Answer: repriceable assetsfor banks.Answer: repriceable liabilities37.Interest sensitive assets less interest sensitive liabilities divided by total assets of the bank isknown as .Answer: relative interest sensitive gap38.Interest sensitive assets divided by interest sensitive liabilities is knownas .Answer: Interest sensitivity ratio39.is a measure of interest rate exposurewhich is the total difference in dollars between those assets and liabilities that can be repricedover a designated time period.Answer: Cumulative gap40.is the phenomenon that interest ratesattached to various assets often change by different amounts and at different speeds than interest rates attached to various liabilities,Answer: basis riskTrue/False QuestionsT F 41. Usually the principal goal of asset-liability management is to maximize or at least stabilize a bank's margin or spread.Answer: TrueT F 42. Asset management strategy in banking assumes that the amount and kinds of deposits and other borrowed funds a bank attracts are determined largely by its management.Answer: FalseT F 43. The ultimate goal of liability management is to gain control over a financial institution's sources of funds.Answer: Truewill rise.Answer: FalseT F 45. A liability-sensitive bank will experience an increase in its net interest margin if interest rates rise.Answer: FalseT F 46. Under the so-called liability management view in banking the key control lever banks possess over the volume and mix of their liabilities is price.Answer: TrueT F 47. Under the so-called funds management view bank management's control over assets must be coordinated with its control over liabilities so that asset and liability management areinternally consistent.Answer: TrueT F 48. Bankers cannot determine the level or trend of market interest rates; instead, they can only react to the level and trend of rates.Answer: TrueT F 49. Short-term interest rates tend to rise more slowly than long-term interest rates and to fall more slowly when all interest rates in the market are headed down.Answer: FalseT F 50. A financial institution is liability sensitive if its interest-sensitive liabilities are less than its interest-sensitive assets.Answer: FalseT F 51. If a bank's interest-sensitive assets and liabilities are equal than its interest revenues from assets and funding costs from liabilities will change at the same rate.Answer: TrueT F 52. Banks with a positive cumulative interest-sensitive gap will benefit if interest rates rise, but lose income if interest rates decline.Answer: TrueT F 53. Banks with a negative cumulative interest-sensitive gap will benefit if interest rates rise, but lose income if interest rates decline.Answer: FalseT F 54. For most banks interest rates paid on liabilities tend to move more slowly than interest rates earned on assets.Answer: FalseT F 55. Interest-sensitive gap techniques do not consider the impact of changing interest rates on stockholders equity.Answer: TrueT F 56. Interest-sensitive gap, relative interest-sensitive gap and the interest-sensitivity ratio will often reach different conclusions as to whether the bank is asset or liability sensitive.Answer: FalseT F 57. The yield curve is constructed using corporate bonds with different default risks so the bank can determine the risk/return tradeoff for default risk.Answer: FalseT F 58. Financial securities that are the same in all other ways may have differences in interest rates that reflect the differences in the ease of selling the security in the secondary marketat a favorable price.Answer: TrueT F 59. Financial institutions face two major kinds of interest rate risk. These risks include price risk and reinvestment risk.Answer: TrueT F 60. Interest-sensitive gap and weighted interest-sensitive gap will always reach the same conclusion as to whether a bank is asset sensitive or liability sensitive.Answer: FalseT F 61. Weighted interest-sensitive gap is less accurate than interest-sensitive gap in determining the affect of changes in interest rates on net interest margin.Answer: FalseT F 62. A bank with a positive duration gap experiencing a rise in interest rates will experience an increase in its net worth.Answer: FalseT F 63. A bank with a negative duration gap experiencing a rise in interest rates will experience an increase in its net worth.Answer: TrueT F 64. Duration is a direct measure of the reinvestment risk of a bond.Answer: FalseT F 65. A bank with a positive duration gap experiencing a decrease in interest rates will experience an increase in its net worth.Answer: TrueT F 66. A bank with a negative duration gap experiencing a decrease in interest rates will experience an increase in its net worth.Answer: FalseT F 67. Duration is the weighted average maturity of a promised stream of future cash flows.Answer: TrueT F 68. Duration is a direct measure of the price risk of a bond.Answer: TrueT F 69. A bond with a greater duration will have a smaller price change in percentage terms when interest rates change.Answer: FalseT F 70. Long-term interest rates tend to change very little with the cycle of economic activity.Answer: TrueT F 71. A bank with a duration gap of zero is immunized against changes in the value of net worth due to changes in interest rates in the market.Answer: TrueT F 72. Convexity is the idea that the rate of change of an asset's price varies with the level of interest rates.Answer: TrueT F 73. The change in the market price of an asset's price from a change in market interest rates is roughly equal to the asset's duration times the change the interest rate divided by theoriginal interest rate.Answer: TrueT F 74. U.S. banks tend to do better when the yield curve is upward-sloping.Answer: TrueT F 75. Net interest margin tends to rise for U.S. banks when the yield curve is upward-sloping.Answer: TrueT F 76. Financial institutions laden with home mortgages tend be immune to interest-rate risk.Answer: FalseT F 77. If a Financial Institution's net interest margin is immune to interest-rate risk then so is its net worth.Answer: FalseMultiple Choice Questions78.When is interest rate risk for a bank greatest?A)When interest rates are volatile.B)When interest rates are stable.C)When inflation is high.D)When inflation is low.E)When loan defaults are high.Answer: A79. A bank’s IS GAP is defined as:A)The dollar amount of rate-sensitive assets divided by the dollar amount of rate-sensitiveliabilities.B)The dollar amount of earning assets divided by the dollar amount of total liabilities.C)The dollar amount of rate-sensitive assets minus the dollar amount of rate-sensitiveliabilities.D)The dollar amount of rate-sensitive liabilities minus the dollar amount of rate-sensitiveassets.E)The dollar amount of earning assets times the average liability interest rate.Answer: C80.According to the textbook, the maturing of the liability management techniques, coupled withmore volatile interest rates, gave birth to the __________________ approach which dominates banking today. The term that correctly fills in the blank in the preceding sentence is:A) Liability managementB) Asset managementC) Risk managementD) Funds managementE) None of the above.Answer: D81.The principal goal of interest-rate hedging strategy is to hold fixed a bank's:A) Net interest marginB) Net income before taxesC) Value of loans and securitiesD) Noninterest spreadE) None of the above.Answer: A82. A bank is asset sensitive if its:A) Loans and securities are affected by changes in interest rates.B) Interest-sensitive assets exceed its interest-sensitive liabilities.C) Interest-sensitive liabilities exceed its interest-sensitive assets.D) Deposits and borrowings are affected by changes in interest rates.E) None of the above.Answer: B83.The change in a bank's net income that occurs due to changes in interest rates equals the overallchange in market interest rates (in percentage points) times _____________. The choice belowthat correctly fills in the blank in the preceding sentence is:A) V olume of interest-sensitive assetsB) Price risk of the bank's assetsC) Price risk of the bank's liabilitiesD) Size of the bank's cumulative gapE) None of the above.Answer: D84. A bank with a negative interest-sensitive GAP:A) Has a greater dollar volume of interest-sensitive liabilities than interest-sensitive assets.B) Will generate a higher interest margin if interest rates rise.C) Will generate a higher interest margin if interest rates fall.D) A and B.E) A and C.Answer: E85.The net interest margin of a bank is influenced by:A) Changes in the level of interest rates.B) Changes in the volume of interest-bearing assets and interest-bearing liabilities.C) Changes in the mix of assets and liabilities in the bank's portfolio.D) All of the above.E) A and B only.Answer: D86.The discount rate that equalizes the current market value of a loan or security with the expectedstream of future income payments from that loan or security is known as the:A) Bank discount rateB) Yield to maturityC) Annual percentage rate (APR)D) Add-on interest rateE) None of the above.Answer: B87.The interest-rate measure often quoted on short-term loans and money market securities such asU.S. Treasury bills is the:A) Bank discount rateB) Yield to maturityC) Annual percentage rate (APR)D) Add-on interest rateE) None of the aboveAnswer: A88. A bank whose interest-sensitive assets total $350 million and its interest-sensitive liabilitiesamount to $175 million has:A) An asset-sensitive gap of 525 millionB) A liability-sensitive gap of $175 millionC) An asset-sensitive gap of $175 millionD) A liability-sensitive gap of $350 millionE) None of the above.Answer: C89. A bank has a 1-year $1,000,000 loan outstanding, payable in four equal quarterly installments.What dollar amount of the loan would be considered rate sensitive in the 0 – 90 day bucket?A)$0B)$250,000C)$500,000D)$750,000E)$1,000,000Answer: B90. A bank has Federal funds totaling $25 million with an interest rate sensitivity weight of 1.0.This bank also has loans of $105 million and investments of $65 million with interest ratesensitivity weights of 1.40 and 1.15 respectively. This bank also has $135 million ininterest-bearing deposits with an interest rate sensitivity weight of .90 and other money market borrowings of $75 million with an interest rate sensitivity weight of 1.0. What is the weighted interest-sensitive gap for this bank?A) $50.25B) $-15C) -$50.25D) $34.25E) None of the aboveAnswer: A91. A bond has a face value of $1000 and five years to maturity. This bond has a coupon rate of 13percent and is selling in the market today for $902. Coupon payments are made annually on this bond. What is the yield to maturity (YTM) for this bond?A) 13%B) 12.75%C) 16%D) 11.45%E) Cannot be calculated from the information givenAnswer: C92. A treasury bill currently sells for $9,845, has a face value of $10,000 and has 46 days to maturity.What is the bank discount rate on this security?A) 12.49%B) 12.13%C) 12.30%D) 2%E) None of the aboveAnswer: B93.The _______________ is determined by the demand and supply for loanable funds in themarket. The term that correctly fills in the blank in the preceding sentence is:A) The yield to maturityB) The banker's discount rateC) The holding period returnD) The risk-free real rate of interestE) The market rate of interest on a risky loanAnswer: D94. A bank with a positive interest-sensitive gap will have a decrease in net interest income wheninterest rates in the market:A) RiseB) FallC) Stay the sameD) A bank with a positive interest-sensitive gap will never have a decrease in net interest incomeAnswer: B95.The fact that a consumer who purchases a particular basket of goods for $100 today has to pay$105 next year for the same basket of goods is an example of which of the following risks:A) Inflation riskB) Default riskC) Liquidity riskD) Price riskE) Maturity riskAnswer: A96. A bank has Federal Funds totaling $25 million with an interest rate sensitivity weight of 1.0.This bank also has loans of $105 million and investments of $65 million with interest ratesensitivity weights of 1.40 and 1.15 respectively. This bank also has $135 million ininterest-bearing deposits with an interest rate sensitivity weight of .90 and other money marketborrowings of $75 million with an interest rate sensitivity weight of 1.0. What is the dollar interest-sensitive gap for this bank?A) $50.25B) $-15C) -$50.25D) $34.25E) None of the aboveAnswer: B97.If a bank has a positive GAP, an increase in interest rates will cause interest income to__________, interest expense to__________, and net interest income to __________.A)Increase, increase, increaseB)Increase, decrease, increaseC)Increase, increase, decreaseD)Decrease, decrease, decreaseE)Decrease, increase, increaseAnswer: A98.If a bank has a negative GAP, a decrease in interest rates will cause interest income to__________, interest expense to__________, and net interest income to __________.A)Increase, increase, increaseB)Increase, decrease, increaseC)Increase, increase, decreaseD)Decrease, decrease, decreaseE)Decrease, decrease, increaseAnswer: E99. A treasury bill currently sells for $9,845, has a face value of $10,000 and has 46 days to maturity.What is the yield to maturity on this security?A) 12.49%B) 12.13%C) 12.30%D) 2%E) None of the aboveAnswer: A100.The Third National Bank of Edmond reports a net interest margin of 5.83%. It has total interest revenues of $275 million and total interest expenses of $210 million. What does this bank's earnings assets have to be?A) $4717 millionB) $3602 millionC) $1115 millionD) $3.790 millionE) None of the aboveAnswer: C101.The Third National Bank of Edmond reports a net interest margin of 5.83%. It has total interest revenues of $275 million and total interest expenses of $210 million. This bank has earnings assets of $1115. Suppose this bank's interest revenues rise by 8 percent and its interest expenses and earnings assets rise by 10 percent next year. What is this bank's new net interest margin?A) 5.83%B) 7.09%C) 3.59%D) 5.38%E) 7.80%Answer: D102.Which of the following is part of funds management?A) The goal of funds management is simply to gain control over the bank's funds sources.B) Since the amount of deposits a bank holds is determined largely by its customers, the focusof the bank should be on managing the assets of the bank.C) Management of the bank's assets must be coordinated with management of the bank'sliabilities.D) The spread between interest revenues and interest expenses is unimportant.E) None of the aboveAnswer: C103.If Fifth National Bank's asset duration exceeds its liability duration and interest rates rise, this will tend to __________________ the market value of the bank's net worth.A) LowerB) RaiseC) StabilizeD) Not affectE) None of the aboveAnswer: A104.If Main Street Bank has $100 million in commercial loans with an average duration of 0.40 years;$40 million in consumer loans with an average duration of 1.75 years; and $30 million in U.S.Treasury bonds with an average duration of 6 years, what is Main Street's asset portfolioduration?A) 0.4 yearsB) 1.7 yearsC) 2.7 yearsD) 4.1 yearsE) None of the aboveAnswer: B105. A bank has an average asset duration of 4.7 years and an average liability duration of 3.3 years.This bank has $750 million in total assets and $500 million in total liabilities. This bank has:A) A positive duration gap of 8.0 years.B) A negative duration gap of 2.5 years.C) A positive duration gap of 1.4 years.D) A positive duration gap of 2.5 years.E) None of the above.Answer: D106. A bank has an average asset duration of 1.15 years and an average liability duration of 2.70 years.This bank has $250 million in total assets and $225 million in total liabilities. This bank has:A) A negative duration gap of 1.55 years.B) A positive duration gap of 1.28 years.C) A negative duration gap of 3.85 years.D) A negative duration gap of 1.28 years.E) None of the above.Answer: D107.The duration of a bond is the weighted average maturity of the future cash flows expected to be received on a bond. Which of the following is a true statement concerning duration?A) The longer the time to maturity, the greater the durationB) The higher the coupon rate, the higher the durationC) The shorter the duration, the greater the price volatilityD) All of the above are trueE) None of the above are trueAnswer: A108. A bond has a duration of 7.5 years. Its current market price is $1125. Interest rates in the market are 7% today. It has been forecasted that interest rates will rise to 9% over the nextcouple of weeks. How will this bank's price change in percentage terms?A) This bond's price will rise by 2 percent.B) This bond's price will fall by 2 percent.C) This bond's price will fall by 14 .02 percentD) This bond's price will rise by 14.02 percentE) This bond's price will not changeAnswer: C109. A bank has an average asset duration of 5 years and an average liability duration of 3 years.This bank has total assets of $500 million and total liabilities of $250 million. Currently, market interest rates are 10 percent. If interest rates fall by 2 percent (to 8 percent), what is this bank's change in net worth?A) Net worth will decrease by $31.81 millionB) Net worth will increase by $31.81 millionC) Net worth will increase by $27.27 millionD) Net worth will decrease by $27.27 millionE) Net worth will not change at allAnswer: B110. A bank has an average asset duration of 5 years and an average liability duration of 3 years.This bank has total assets of $500 million and total liabilities of $250 million. Currently, market interest rates are 10 percent. If interest rates fall by 2 percent (to 8 percent), what is this bank's duration gap?A) 2 yearsB) –2 yearsC) 3.5 yearsD) –3.5 yearsE) None of the aboveAnswer: C111. A bank has an average asset duration of 5 years and an average liability duration of 9 years.This bank has total assets of $1000 million and total liabilities of $850 million. Currently,market interest rates are 5 percent. If interest rates rise by 2 percent (to 7 percent), what is this bank's change in net worth?A) Net worth will decrease by $50.47 millionB) Net worth will increase by $50.47 millionC) Net worth will decrease by $240.95 millionD) Net worth will increase by $240.95 millionE) Net worth will not change at allAnswer: B112. A bank has an average asset duration of 5 years and an average liability duration of 9 years.This bank has total assets of $1000 million and total liabilities of $850 million. Currently,market interest rates are 5 percent. If interest rates rise by 2 percent (to 7 percent), what is this bank's duration gap?A) –4 yearsB) 4 yearsC) 2.65 yearsD) –2.65 yearsE) 12.65 yearsAnswer: D113. A bank has $100 million of investment grade bonds with a duration of 9.0 years. This bank also has $500 million of commercial loans with a duration of 5.0 years. This bank has $300 million of consumer loans with a duration of 2.0 years. This bank has deposits of $600 million with a duration of 1.0 years and nondeposit borrowings of $100 million with an average duration of .25 years. What is this bank's duration gap? These are all of the assets and liabilities this bank has.A) This bank has a duration gap of 14.75 yearsB) This bank has a duration gap of 15.03 yearsC) This bank has a duration gap of 3.55 yearsD) This bank has a duration gap of 3.75 yearsE) This bank has a duration gap of 5.15 yearsAnswer: D114.Which of the following statements is true concerning a bank's duration gap?A) If a bank has a positive duration gap and interest rates rise, the bank's net worth will declineB) A bank with a positive duration gap has a longer average duration for its assets than for itsliabilitiesC) If a bank has a zero duration gap and interest rates rise, the bank's net worth will not changeD) If a bank has a negative duration gap and interest rates rise, the bank's net worth will increaseE) All of the above are true statementsAnswer: E115. A bank has an average duration for its asset portfolio of 5.5 years. This bank has total assets of $1000 million and total liabilities of $750 million. If this bank has a zero duration gap, what must the duration of its liabilities portfolio be?A) 7.33 yearsB) 4.125 yearsC) 7.5 yearsD) 5.5 yearsE) None of the aboveAnswer: A116. A bond has a face value of $1000 and coupon payments of $80 annually. This bond matures in three years and is selling for $1000 in the market. Market interest rates are 8%. What is this。

商业银行经营管理期末模拟考试题一

《商业银行经营管理》综合测试一一、单选题(在每小题的四个备选答案中选出一个正确的答案,并将正确答案的号码填在题干的括号内。

每小题1分,共10分)( )1、银行业务营运的起点和前提条件是:A.自有资本 B.负债业务 C.资产业务 D.贷款业务( ) 2、________ 的成立,标志着资本主义商业银行的诞生。

A.英格兰银行 B.威尼斯银行 C.圣乔治银行 D.阿姆斯特丹银行( ) 3、在下列几种通过外部融资扩充银行资本的方法中,对普通股每股收益影响最小的是:A.发行普通股 B.发行优先股 C.发行资本性长期债券 D.发行可转换债券( ) 4、商业银行最主要的盈利性资金运用是:A.同业存款 B.短期国库券 C.贷款 D.长期证券( ) 5、借款人的还款能力出现了明显的问题,依靠其正常经营收入已无法保证足额偿还本息的贷款是:A.损失类贷款 B.可疑类贷款 C.次级类贷款 D.关注类贷款( ) 6、定活两便存款利率一般参照整存整取存款利率打 ________折计息。

A. 4 B. 5 C. 6 D. 7( ) 7、决定商业银行资产规模的基础是:A.比例规模 B.资产结构 C.银行资本 D.负债业务( ) 8、中国人民银行全面推行资产负债比例管理和风险管理始于:A. 1996 年 B. 1997 年 C. 1998 年 D. 1999 年( ) 9、通常把商业银行库存现金与在中央银行的超额准备金之和称为:A.可用头寸 B.基础头寸 C.可贷头寸 D.超额头寸( ) 10、一家银行的资产是 100 万元,资产收益率是 1%,其杠杆比率是 4,该银行的资本收益率为:A. 1% B. 4% C. 5% D. 10%二、多选题(在每小题的备选答案中选出二个或二个以上正确的答案,并将正确答案的号码填在题干的括号内。

正确答案未选全或有选错的,该小题无分。

每小题2分,共16分) ( ) 1、下列业务活动中引起银行现金流入增加的有:A.利息支付 B.同业拆入资金 C.兑付大额可转让存单 D.发行债券( ) 2、下列属商业银行非存款性的资金来源主要有:A.拆出资金 B.再贷款 C.再贴现 D.发行债券( ) 3、商业银行现金资产管理应坚持的基本原则有:A.成本最低原则 B.安全性原则 C.适时流量调节原则 D.适时存量控制原则( ) 4、下列________项目属于商业银行的附属资本。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第一章1.商业银行:是指依照《中华人民共和国商业银行法》和《中华人民共和国公司法》设立的吸收公众存款、发放贷款、办理结算等业务的企业法人。

2. 商业银行的功能为信用中介、支付中介、信用创造和金融服务。

(其中,信用中介功能是指商业银行通过负债业务,把社会上的各种闲散资金集中起来,再通过资产业务,把资金运用出去,从而在资金盈余者与资金短缺者之间架起一座桥梁,在资金所有权不发生转移的前提下,使闲置的资金资源得到最大限度的利用。

支付中介功能,是指商业银行利用活期存款账户为客户办理各种货币结算、货币收付、货币兑换和转移存款等业务活动的功能。

信用创造功能是指商业银行利用其可以吸收活期存款的有利条件,通过发放贷款而派生出更多的存款,从而扩大社会货币供应量的功能。

金融服务功能是指商业银行除了发挥前面三种功能以外,还向社会提供种类繁多的服务的功能。

)3. 欧洲大陆银行的前身:货币兑换商;英国银行的前身:金匠。

4. 影响商业银行发展变化的环境因素包括社会制度、宏观经济、信息技术、金融环境、银行监管、金融基础设施、人文社会环境。

5. 非银行金融机构的有利方面:(1)非银行金融机构可以通过其专业化服务促进商业银行的发展。

(2)非银行金融机构本身是商业银行的重要客户。

(3)非银行金融机构的发展,能够丰富我国的金融体系和金融服务,促进整个金融业甚至整个社会经济的发展,从而能为商业银行的经营提供一个良好的外部环境。

(4)非银行金融机构的规范和发展,使得商业银行本身也可以参与非银行机构,比如,商业银行设立基金管理公司,从而大大拓展了商业银行的业务空间。

6. 银行监管主要包括市场准入监管、审慎经营监管、信息披露监管和市场退出监管。

7. 银行监管的手段包括现场检查和非现场监管两大类。

8. 金融基础设施是指金融运行的硬件设施和制度安排,主要包括支付体系、法律法规、公司治理、会计标准、征信体系、反洗钱体系,以及由审慎金融监管、中央银行最后贷款人职能、投资者保护制度构成的金融安全网等。

第二章1. 商业银行的经营目标是银行在满足监管当局、存款人、借款人、经营管理者和职员的要求(所施加的约束)的前提下,最大化股东价值。

2. 商业银行以安全性、流动性、效益性为经营原则。

3. 安全性原则是指银行在经营活动中,必须保持足够的清偿能力,能经得起一定的风险和损失,保持客户对银行的坚定信心。

流动性原则是指银行能够随时满足客户提取存款、借入贷款、对外支付的需要,保证资金的正常流动。

效益性原则包括两个方面的内容:一是经济效益,即商业银行在经营中必须获得利润,即通常所说的盈利性;二是社会效益,即商业银行在经营中还必须承担相应的社会责任。

5. “三性”原则的矛盾性与一致性在商业银行经营管理的过程中,盈利性、流动性、安全性之间既有矛盾的一面,也有一致的一面。

“三性”之间的矛盾主要体现在盈利性与流动性、盈利性与安全性之间。

我们可以通过商业银行的资产负债结构来说明这期间的矛盾。

(下面两点归纳一下背吧)(1)资产结构。

在商业银行的所有资产中,现金资产的流动性最高,但盈利性最低。

为了保证银行的流动性,银行必须持有足够的现金资产,但这又会减少银行收益性资产(如贷款、国债)的比例,从而影响银行的盈利能力。

在商业银行的收益性资产中,贷款的收益率一般要高于国债,但贷款的流动性和安全性一般又要低于国债;一项资产的期限越长,其收益率一般越高,而其流动性和安全性则越低。

(2)负债结构。

存款的成本一般要比借入款的成本低,但由于存款可以随时提取,而借入款只需在到期时偿还。

因此,存款的稳定性要低一些,这会提高对银行流动性的要求(必须保持一定比例的现金一应付存款提取的需要),降低银行运用这部分资金的盈利能力。

从根本上说,银行的经营管理过程中的“三性”是一致的。

商业银行只有保持必要的流动性和安全性,才能从根本上保证盈利性原则的顺利实现,流动性和安全性是盈利性的基础和必要条件。

同时,盈利性是安全性和流动性的最终目标和重要保证。

5. 商业银行的财务报表一般包括资产负债表、利润表、现金流量表、所有者权益变动表和附注五个部分。

6. 分析企业资本利润率的主要模型是杜邦模型,其核心是通过分解资本利润率来分析影响企业盈利水平的各种因素。

7. 银行的资本利润率第一步分解为资产利润率与股权乘数之积,ROE = ROA * EM;第二步分解为收入利润率和资产利用率的乘积:ROA=PM*AU(PM=净利润/总收入;AU=总收入/总资产)。

(重点掌握第一步。

)8. 提高银行经营绩效的三大类方法和手段:(1)增加收入,包括增加利息收入和非利息收入,而增加利息收入又可以从提高利率、扩大规模、提高高利率资产所占比重三个方面着手;增加非利息收入则可以采取扩大收入项目、提高收费价格等手段。

(2)减少支出,包括四个基本方面:一是通过利率、规模、结构等方面等降低利息支出;二是通过降低工资(包括裁员)、压缩管理费用等降低非利息支出;三是通过提高资产质量来减少资产损失准备金;四是尽可能降低税负。

(3)提高股权乘数,即在尽可能的情况下,减少资本,增加负债,从而获得杠杆收益。

9. 在全球范围内应用最为广泛的监管评级体系,是源自美国的骆驼评级体系。

骆驼评级体系,是通过考察商业银行的资本充足性、资产质量、管理、盈利性、流动性和市场风险敏感度六大要素,系统评价银行机构整体财务实力和经营管理状况。

10. 信用评级,是由独立、中立的专业评级机构对个人、经济体与金融工具履行各种经济承诺的能力及可信任程度的综合评价。

第三章1. 按照资金来源划分,商业银行的负债主要包括存款负债、借款负债、结算性负债(包括汇出汇款和应解汇款)和应付款项(应付利息、应付工资、应付福利费、应付代理证券款项、应付税金、应付固定资产融资租赁费、应付股息等)。

其中,银行需要对前两项来源支付利息,称为计息负债;而对后两项来源一般不需要支付利息,称为非计息负债。

2. 银行负债管理的基本原则:(1)依法筹资原则;(2)成本控制原则;(3)量力而行原则;(4)结构合理原则。

3. 存款可以随时支取之所以能够导致银行的脆弱性,主要是由存款的部分准备、存款支取的“先来后到”原则及存款支取的低成本所决定的。

(1)存款的部分准备,是指商业银行对吸收来的存款,只将很少的一部分作为准备金,而将其余绝大部分以贷款等流动性较差的资产形式运用了出去。

(2)存款支取的“先来后到”原则,是指到银行支取存款的人,将会按照“先来后到”的原则得到服务,如果在银行失去支付能力之前到银行支取存款的人,就能够全额收回其存款的本金和利息,而在此之后去支取存款的人,就有可能遭受本金和利息的全部或部分损失。

(3)存款支取的低成本,是指存款人支取存款时所发生的成本,相对于银行倒闭后本金的损失来说,是极低的。

存款的这三个特征,使存款人极容易挤提存款,同时支取存款的部分极容易超过银行的支付能力,从而银行陷入流动性危机。

4. 保证金存款,是商业银行为保证客户在银行为客户对外出具具有结算功能的信用工具,或提供资金融通后,按约履行相关义务,而与其约定将一定数量的资金存入特定账户所形成的存款类别。

(在客户违约后,商业银行有权直接扣划该账户中的存款,以最大限度地减少银行损坏。

保证金存款包括银行承兑汇票保证金、信用证保证金、黄金交易保证金、个人购汇保证金、远期结售汇保证金等。

)5.同业存放:也称同业存款,是指因支付清算和业务合作等的需要,由其他金融机构存放于商业银行的款项。

(属于商业银行的负债业务)6. 结构性存款,属于收益增值产品之一,是指最终收益与一个或多个金融产品的价格表现挂钩、以提高收益率为目标的存款。

7. 存款保险是指为了保护中小存款人的利益,维护金融体系的安全与稳定,吸收存款的机构定期按照一定的比例向存款保险机构交纳保险费,以便在存款机构出现信用危机时,由存款保险机构向金融机构提供财务救援,或由存款保险机构直接向存款者支付部分或全部存款,以维护正常金融秩序的制度。

(起源于20世纪30年代以单一银行制为基本特征的美国。

)8. 建立存款保险体系的原因:一是从宏观上促进银行业的稳定,防范银行危机,减弱在银行危机实际发生时对政府财政、经济增长和社会稳定的冲击;二是在微观上为商业银行提供一个安全网,创造一个公平竞争的银行环境,并促进银行改善经营管理,从而保证银行的稳健经营。

“资产决定负债”的经营模式,具有一定的弊端和风险,表现在如下三个方面:(1)需要以发达的金融市场为基础。

(2)利息成本高。

(借款的利率一般高于存款的利率,这对银行资产的盈利能力提出了跟高的要求)(3)波动性大。

9. 同业拆借是商业银行从其他金融机构借入短期资金的行为,主要用于支持资金的临时周转。

10. 债券回购包括质押式回购和买断式回购。

质押式回购是交易双方进行的以债券为权利质押的一种短期资金融通业务。

买断式回购是指债券持有人将债券卖给债券购买方的同时,交易双方约定在未来某一时期,正回购方再以约定价格从逆回购方买回相等数量同种债券的交易行为。

买断式回购与质押式回购的主要区别在于标的券种的所有权归属不同。

(在质押式回购中,融券方(逆回购方)不拥有标的券种的所有权,在回购期内,融券方无权对标的债券进行处置;在买断式回购中,可以对标的债券进行处置,只要到期时有足够的同种债券反售给正回购方即可。

)11. 金融债券是商业银行在金融市场上发行的按约定还本付息的有价证券。

12. 商业银行通过发行金融债券的方式借入长期资金,具有很多优势:(1)利用率比较高。

(2)银行可以长期稳定使用。

(3)发行债券可起到广告宣传作用。

(4)债券发行时及其在二级市场上的交易价格,都会充分反映银行的经营状况和风险,从而能够有效地促使银行改善经营管理。

13. 次级债券:是指商业银行发行的、本金和利息的清偿顺序列于商业银行其他负债之后、先于商业银行股权的资本债券。

14. 次级债券的意义:(1)次级债券的期限比较长,一般为10年,最短不短于5年,属于银行可以长期使用的稳定资金来源;(2)次级债券可以计入银行附属资本,可以有效地提高银行的资本充足率,相对于发行股票补充资本的方式来说,发行次级债券程序相对简单、周期短,发行成本比较低;(3)具有与发行普通金融债券同样的广告宣传效应和市场约束作用。

15. 银行总体资金需求的预测:(1)发展性资金需求;(2)利率敏感组合资金需求;(3)流动性资金需求;(4)再筹资资金需求。

16. 借款成本包括利息成本和营业成本两大类:利息成本是商业银行按照约定的利率,以货币的形式向债权人支付的报酬;营业成本是指在筹资过程中发生的除了利息以外的所有开支。

17. 阅读本章小结p81.第四章1. 贷款是商业银行出借给贷款对象并按约定利率和期限还本付息的货币资金。