查尔斯亨格瑞_财务会计_课后练习答案01.

财务会计FA3_习题答案ch22

*This material is dealt with in an Appendix to the chapter.

22-1

School of Management,HUST

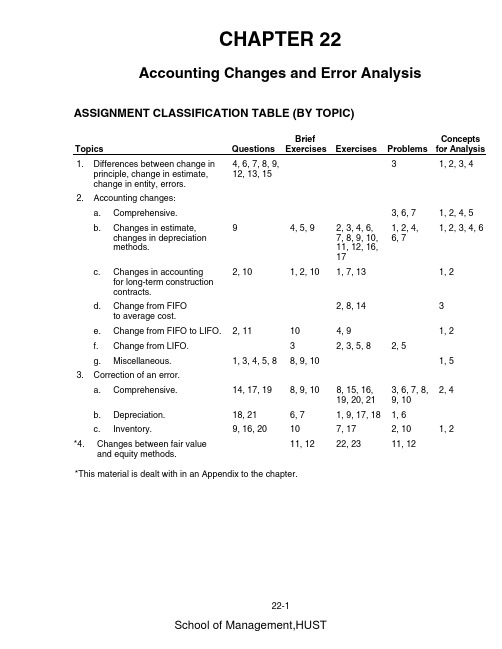

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives 1. Identify the types of accounting changes. 2. Describe the accounting for changes in accounting principles. 3. Understand how to account for retrospective accounting changes. 4. Understand how to account for impracticable changes. 5. Describe the accounting for changes of estimates. 6. Identify changes in a reporting entity. 7. Describe the accounting for correction of errors. 6, 7, 8, 9, 10 7, 8, 9, 10, 15, 16, 17, 18, 19, 20, 21 1, 2, 3, 6, 7, 8, 9, 10 4, 5, 9, 10 1, 2, 3, 9, 10 1, 2, 3, 4, 5, 8, 13, 14 2 6, 7, 8, 9, 10, 11, 12 1, 2, 3, 4, 6 1 2, 3, 5 Brief Exercises Exercises Problems

School of Management,HUST

亨格瑞管理会计英文第15版练习答案01

亨格瑞管理会计英文第15版练习答案01CHAPTER 1COVERAGE OF LEARNING OBJECTIVESLEARNING OBJECTIVE LO1: Describe the major users and uses of accounting information. LO2: Describe the cost-benefit and behavioral issues involved in designing an accounting system. LO3: Explain the role of budgets and performance reports in planning and control. LO4: Discuss the role accountants play in the company’s value chain functions. LO5: Explain why accounting is important in a variety of career paths. LO6: Identify current trends in management accounting. LO7: Explain why ethics and standards of ethical conduct are important to accountants. FUNDA- CRITICAL CASES, MENTAL THINKING EXCEL, ASSIGN-EXERCISES COLLAB., & MENT AND INTERNET MATERIAL EXERCISES PROBLEMS EXERCISES A1, B1 28, 29, 33 39, 40, 42 55 41, 43 A2, B2 32 45 53A1, B1 30, 31, 34, 35, 39, 42, 44 36 30, 31 52, 55 A3, B3 37, 38 47, 48, 49 54 51, 52, 55 1 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.CHAPTER 1Managerial Accounting, the Business Organization, and Professional Ethics1-A1 (10-15 min.)Information is often useful for more than one function, so the following classifications for each activity are not definitive but serve as a starting point for discussion: 1. Scorekeeping. A depreciation schedule is used in preparing financial statementsto report the results of activities. 2. Problem solving. Helps a manager assess the impact of a purchase decision. 3. Scorekeeping. Reports on the results of an operation. Could also be attentiondirecting if scrap is an area that might require management attention. 4. Attention directing. Focuses attention on areas that need attention. 5. Attention directing. Helps managers learn about the information contained in aperformance report. 6. Scorekeeping. The statement reports what has happened. Could also be attentiondirecting if the report highlights a problem or issue. 7. Problem solving. Assuming the cost comparison is to help the manager decidebetween two alternatives, this is problem solving. 8. Attention directing. Variances point out areas where results differ fromexpectations. Interpreting them directs attention to possible causes of the differences. 9. Problem solving. Aids a decision about where to make parts. 10. Attention directing and problem solving. Budgeting involves making decisionsabout planned activities -- hence, aiding problem solving. Budgets also direct attention to areas of opportunity or concern --hence, directing attention. Reporting against the budget also has a scorekeeping dimension.2 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-A2 1. 2.(15-20 min.)Room rental FoodEntertainment Decorations TotalBudgeted Amounts $ 140 700 600 220 $1,660 Actual Amounts $ 140865 600 260 $1,865 Deviations or Variances $ 0 165U 0 40U $205U Because of the management by exception rule, room rental and entertainment require no explanation. The actual expenditure for food exceeded the budgetby $165. Of this $165, $150 is explained by attendance of 15 persons morethan budgeted (at a budget of $10 per person for food) and $15 is explained by expenditures above $10 per person.Actual expenditures for decorations were $40 more than the budget. The decorations committee should be asked for an explanation of the excess expenditures.1-A3 (10 min.)All of the situations raise possibilities for violation of the integrity standard. In addition, the manager in each situation must address an additional ethical standard: 1. The General Mills manager must respect the confidentiality standard. He or sheshould not disclose any information about the new cereal. 2. Felix must address his level of competence for the assignment. If his supervisorknows his level of expertise and wants an analysis from a “layperson” point of view, he should do it. However, if the supervisor expects an expert analysis, Felix must disclose his lack of competence. 3. The credibility standard should cause Mary Sue to decline to omit the informationfrom the budget. It is relevant information, and its omission may mislead readers of the budget.3 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-B1 (15-20 min.)Information is often useful for more than one function, so the following classifications for each activity are not definitive but serve as a starting point for discussion: 1. Problem solving. Provides information for deciding between two alternativecourses of action. 2. Scorekeeping. Recording what has happened. If amounts are compared withexpectations, this could also serve an attention-directing function. 3. Problem solving. Helps a manager decide among alternatives. 4. Attention directing. Directs attention to the use of overtime labor. Alsoscorekeeping. 5. Problem solving. Provides information to managers for deciding whether to movecorporate headquarters. 6. Attention directing. Directs attention to why nursing costs increased. 7. Attention directing. Directs attention to areas where actual results differed fromthe budget. 8. Problem solving. Helps the vice-president decide which course of action is best. 9. Problem solving. Produces information to help the marketing department make adecision about a marketing campaign. 10. Scorekeeping. Records actual overtime costs. If results are compared withexpectations, also attention directing. 11. Attention directing. Directs attention to stores with either high or low ratios ofadvertising expenses to sales. 12. Attention directing. Directs attentionto causes of returns of the drug. 13. Attention directing or problem solving, depending on the use of the schedule. If itis to identify areas of high fuel usage it is attention directing. If itis to plan for purchases of fuel, it is problem solving. 14. Scorekeeping. Records items needed for financial statements.4 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.1-B2 (10-15 min.)1 & 2. Budget Actual Variance Sales $75,000 $74,600 $ 400U Costs: Fireworks $36,000 $35,500 $500F Labor 15,000 18,000 3,000U Other 8,000 7,910 90F Total cost 59,000 61,410 2,410U Profit $16,000 $13,190 $2,810U 3. The cost of fireworks was $500 ÷ $36,000 = 1.4%under budget while sales wasjust 400 ÷ $75,000 = .5% under budget. Did fireworks suppliers lowertheir prices? Were selling prices set higher than expected? There should be some explanation for the lower cost of fireworks. The labor cost was $3,000÷ $15,000 =20% over budget. Sales and other costswere close to budget in percentage terms. Why was labor cost much higherthan expected?1-B3 (15 - 20 min.) 1. A code of conduct is a document specifying theethical standards of anorganization. 2. Different companies include different elements intheir codes of conduct. Some ofthe items included in companies’ codes of condu ct include maintaining adress code, avoiding illegal drugs, following instructions of superiors, being reliable and prompt, maintaining confidentiality, not accepting personal gifts fromstakeholders as a result of company role, avoiding racial or sexual discrimination, avoiding conflict of interest, complying with laws and regulations, not using organization’s property for personal use, andreporting illegal or questionable activity. Some companies have a simple code with little detail, and others have long lists of rules and regulations regarding appropriate conduct. The key is that the code of conduct must fit with the corporate culture. 3. Simply having a code of conduct does not guarantee ethical behavior byemployees. Most important is top management’s ethical example and its support of the code of conduct. A company’s performance evaluation and reward system must be consistent with its code of conduct. If unethical actions are rewarded, they will be encouraged even if they violate the code of conduct.5 Copyright ?2021 Pearson Education, Inc., Publishing as Prentice Hall.感谢您的阅读,祝您生活愉快。

查尔斯亨格瑞_财务会计_课后练习答案01解析

CHAPTER 1COVERAGE OF LEARNING OBJECTIVESChapter 1 Accounting: The Language of Business1CHAPTER 11-1 Accounting is a process of identifying, recording, summarizing, and reporting economic information to decision makers.1-2 No. Accounting is about real information about real companies. In learning accounting it is helpful to see accounting reports from various companies. This helps put the rules and techniques of accounting into an understandable framework and provides familiarity with the diversity of practice.1-3 Examples of decisions that are likely to be influenced by financial statements include choosing where to expand or reduce operations, lending money, investing ownership capital, and rewarding mangers.1-4 Users of financial statements include managers, lenders, suppliers, owners, income tax authorities, and government regulators.1-5 The major distinction between financial accounting and management accounting is their use by two classes of decision makers. Management accounting is concerned mainly with how accounting can serve internal decision makers such as the chief executive officer and other executives. Financial accounting is concerned with supplying information to external users.1-6 The balance sheet equation is Assets = Liabilities + Owners’ equity. It is the fundamental framework of accounting. The left side lists the resources of the organization, and the right side lists the claims against those resources.1-7 No. Every transaction should leave the balance sheet equation in balance. Accounting is often called “double-entry” because accountants must enter at least two numbers for eac h transaction to keep the equation in balance.1-8 This is true. When a company buys inventory for cash, one asset is traded for another, and neither total assets nor total liabilities change. Thus, the balance sheet equation stays in balance. When a company buys inventory on credit, both inventory and accounts payable increase. Thus, both total assets and total liabilities increase by the same amount, again keeping the balance sheet equation in balance.1-9 The evidence for a note payable includes a promissory note, but the evidence for an account payable does not. A note payable is generally to a lender while an account payable is generally to a supplier.1-10 Ownership shares in most large corporations are easily traded in the stock markets, corporate owners have limited liability, and the owners of sole proprietorships or partnerships are usually also managers in the company while most corporations hire professional managers.101-11 Limited liability means that corporate owners are not personally liable for the debts of the corporation. Creditors’claims can be satisfied only by the assets of the particular corporation.1-12 The corporation is the most prominent type of entity and corporations do by far the largest volume of business.1-13 Yes. In the United Kingdom corporations frequently use the word limited (Ltd.) in their name. In many countries whose laws trace back to Spain, the initials S.A. refer to a “society anonymous,” meaning that multiple unidentified owners stand behind the company, which is essentially the same structure as a corporation.1-14 Almost all states forbid the issuance of stock at below par; thus, par values are customarily set at very low amounts and have no real importance in affecting economic behavior of the issuing entity.1-15 The board of directors is the elected link between stockholders and the actual managers.It is the board’s duty to ensure that managers act in the best interests of shareholders.1-16 In the U.S. GAAP is generally set by the Financial Accounting Standards Board. The SEC has formal authority for specifying accounting standards for companies with publicly held stock, as delegated by Congress, but it usually accepts the standards promulgated by the FASB. Internationally, a majority of countries accept IFRS as set by the International Accounting Standards Board as their GAAP.1-17 Until recently this was true. However, now the SEC allows companies headquartered outside the U. S. to report using IFRS.1-18 Audits have value because they add credibilit y to a company’s financial statements.Provided that auditors have the expertise to assess the accuracy of financial statements and the integrity to report any problems they discover, the investing public can put more faith in statements that are audited.1-19 A CPA is a certified public accountant. One becomes a CPA by a combination of education, qualifying experience, and the passing of a two-day national examination. A CA (chartered accountant) is the equivalent of a CPA in many parts of the world, including most former British Commonwealth countries.1-20 Public accountants must obey standards of independence and integrity. In addition, there are many more ethical standards that pertain to accountants. Some folks call accounting the moral guardian of companies. This reputation has been sullied recently by corporate scandals that went undetected (or, at least, unreported by accountants), but accountants are working to regain the high ethical regard they have traditionally maintained.Chapter 1 Accounting: The Language of Business11-21 No. The fundamental accounting principles apply equally to nonprofit (that is, not-for-profit) and profit-seeking organizations. Managers and accountants in hospitals, universities, government agencies, and other nonprofit organizations use financial statements. They need to raise and spend money, prepare budgets, and judge financial performance. Nonprofit organizations need to use their limited resources wisely, and financial statements are essential for judging their use of resources.1-22 Double-entry refers to the concept that every transaction involves two or more accounts with the effect being to retain the balance in the balance sheet equation. The double-entry concept is important because it emphasizes that there are assets and claims on assets. In the balance sheet, for example, borrowing money provides an asset, cash, and creates a liability. In addition to this conceptual benefit there is a clerical benefit. Maintaining a balanced relationship provides an indicator of errors. If the balance sheet equation does not balance, an error has been made.1-23 Historians are primarily concerned with events that have already occurred. In that sense,a company’s financial statements do report on history—transactions that are complete.The negative side of this is that many important things that affect the value of a firm are based on what will happen in the future. Thus, investors often worry about expectations and predictions. Of course, there is no way to agree on the accuracy of expectations and predictions. The positive side of historical financial statements is that they present a no-nonsense perspective on what actually happened, where the company was at a point in time, or what it accomplished over a period of time. It is easier to predict the future when you know where you are and how you got there. You might liken the importance of historical financial statements to the importance of navigation instruments. If you do not know where you are and where you are headed, it is very hard to get to where you want to go.Most people who refer to accountants as historians intend it as a criticism, although, as indicated above, a historical focus ensures that the data are measurable and verifiable.1-24 Such arguments are fun but can never be truly resolved. The notion behind the importance of the corporation is that for any substantial growth to occur there must be a system for organizing resources and using them over long periods of time. The corporate form of ownership helps companies raise large amounts of capital via stock issuance as well as borrowing. It allows us to separate ownership from management. It protects the personal assets of shareholders, and because their maximum losses can be limited, more risky undertakings can be financed. Finally, it has perpetual life so its activity is not disrupted by the death of any shareholder. Corporations operate under a set of established rules of behavior for entering into contracts and being sure that other parties can be relied upon to uphold their side of an agreement.Accounting helped corporations emerge as the dominant economic organization in the world. Without accounting it would be difficult to coordinate the activities of large corporations. It would be especially difficult to separate management from ownership if accounting did not provide information about the performance of managements.101-25 The auditor increases the value of financial statements by reassuring the reader of the statements that an “independent” and a “qualified” third party has reviewed management’s disclosures and believes they fairly present the company’s performance.The fact that you personally do not recognize the name of the audit firm should not be a problem, because only CPAs can perform public audits and sign audit opinions. Every state has strict procedures for licensing CPAs, so such people are qualified. Nevertheless, audit firms develop reputations, and ones with a positive public image may give some financial statement users more confidence in the financial statements they audit.1-26 (10 min.) Amounts are in millions.1. Assets = Liabilities + Owners’ Equity$7 = $3 + $42. Assets and liabilities would increase by $1 million. Owners’ equity would be unaffected.1-27 (15-20 min.)June 2 Owners invested $6,000 additional cash in Sok ol’s Furniture Company.3 Owners invested an additional $4,000 into the company by contributingadditional store fixtures valued at $4,000.4 Sok ol’s Furniture Company purchased additional furniture inventory for$3,000 cash.5 Sok ol’s Furniture Company purchased furniture inventory on account for$6,000.6 Sok ol’s Furniture Company sold store fixtures for $3,000 cash.7 Sok ol’s Furniture Company purchased $6,000 of store fixtures, paying$5,000 cash now and agreeing to pay $1,000 later.8 Sok ol’s Furniture Company paid $2,000 on accounts payable.9 Sok ol’s Furniture Company returned $400 of merchandise (furnitureinventory) for credit against accounts payable.10 Owners withdrew $2,000 cash from Sokol’s Furniture Company.Chapter 1 Accounting: The Language of Business1Sept. 2 Brisbane purchased $2,500 of store fixtures on account.3 Owner or owners withdrew $2,000 cash.4 Brisbane returned $5,000 of its inventory of computers for $5,000 creditagainst its accounts payable.5 Computers (inventory) valued at $7,000 were invested in the company byowners.8 Brisbane paid $500 on accounts payable.9 Brisbane purchased $3,500 of store fixtures, paying $1,000 now andagreeing to pay $2,500 later.10 Brisbane returned $300 of store fixtures for credit against accounts payable.1-29 (15-25 min.)ATLANTA CORPORATIONBalance SheetMarch 31, 20X1Liabilities andAssets Stockholders’ EquityCash $ 5,000 (a) Liabilities:Merchandise inventory 44,000 (b) Accounts payable $ 12,000 (f) Furniture and fixtures 2,000 (c) Notes payable 10,000 Machinery and equipment 27,000 (d) Long-term debt 27,000 (g) Land 39,000 (e) Total liabilities 49,000 Building 24,000 Stockholders’ equity:Total $141,000 Paid-in capital 92,000 (h)Total $141,000(a) Cash: 14,000 + 1,000 – 10,000 = 5,000(b) Merchandise inventory: 40,000 + 4,000 = 44,000(c) Furniture and fixtures: 3,000 – 1,000 = 2,000(d) Machinery and equipment: 15,000 + 12,000 = 27,000(e) Land: 14,000 + 25,000 = 39,000(f) Accounts payable: 8,000 + 4,000 = 12,000(g) Long-term debt: 12,000 + 15,000 = 27,000(h) Paid-in capital: 80,000 + 12,000 = 92,000Note: Event 5 requires no change in the balance sheet.10LIVERPOOL COMPANYBalance SheetNovember 30, 20X1Liabilities andAssets Stockholders’ EquityCash £ 18,000 (a) Liabilities:Merchandise inventory 29,000 Accounts payable £ 9,000 (d) Furniture and fixtures 8,000 Notes payable 31,000 (e) Machinery and equip. 33,000 (b) Long-term debt payable 101,000 (f) Land 35,000 (c) Total liabilities 141,000 Building 241,000 Stockholders’ equity:Total £364,000 Paid-in Capital 223,000 (g)Total £364,000(a) Cash: 22,000 – 3,000 – 7,000 + 6,000 = 18,000(b) Machinery and equipment: 20,000 + 13,000 = 33,000(c) Land: 41,000 – 6,000 = 35,000(d) Accounts payable: 16,000 – 7,000 = 9,000(e) Notes payable: 21,000 + (13,000 – 3,000) = 31,000(f) Long-term debt payable: 124,000 – 23,000 = 101,000(g) Paid-in capital: 200,000 + 23,000 = 223,000Note: Event 4 requires no change in the balance sheet.1-31 (5-10 min.)1. Total liabilities = Total assets -stockholders’ equity= $798,000,000,000 - $105,000,000,000= $693,000,000,0002. Common stock, par value = $.07 × 10,536,897,000 = $737,582,790.Like other items on General Electric’s balance sheet, the amount would be rounded off to millions:Common stock, par value $738Chapter 1 Accounting: The Language of Business11-32 (20-30 min.) See Exhibit 1-32. Equipment and furniture could be in two separate accounts rather than combined.1-33 (20-35 min.)1. See Exhibit 1-33.2. LMN CORPORATIONBalance SheetJanuary 31, 20X1(In Thousands of Dollars)Liabilities andAssets Stockholders’ EquityLiabilities:Cash $131 Note payable $ 30Accounts payable 106 Merchandise inventory 269 Total liabilities $136Stockholders’ equity:Equipment 36 Capital stock,$1 par, 30,000 sharesissued and outstanding $ 30Additional paid-in capitalin excess of par value 270 300 Total $436 Total $436 1-34 (20-35 min.)1. See Exhibit 1-34.2. AUTOPARTES MADRIDBalance SheetMarch 31, 20X1Assets Liabilities and Owners’ EquityCash €58,800 Liabilities:Inventory 16,600 Accounts payable € 4,500 Equipment 17,500 Note payable 9,000Total liabilities 13,500You, capital 79,400 Total €92,900 Total €92,900 10MCLEAN SERVICES, INC.Analysis of April 20X1 Transactions(In Thousands of Dollars)Assets Liabilities and Stockholders’ EquityEquipment Note Accounts Paid-in Description of Transactions Cash + and Furniture = Payable + Payable + Capital1. Issuance of stock +50 = +502. Issuance of stock +20 = +203. Borrowing +35 = +354. Acquisition for cash –33 +33 =5. Acquisition on account +10 = +106. Payments to creditors – 4 = – 47. Sale of equipment + 8 – 8 =8. No entry =+56 +55 = +35 + 6 + 70111 111MCLEAN SERVICES, INC.Balance SheetApril 30, 20X1Assets Liabilities and Stockholders’ EquityNote payable $ 35,000 Cash $ 56,000 Account payable 6,000Equipment and furniture 55,000 Paid-in Capital 70,000Total $111,000 Total $111,000Chapter 1 Accounting: The Language of Business1LMN CORPORATIONJanuary 20X1Analysis of Transactions(In Thousands of Dollars)Assets Liabilities + Owners’ EquityMerch- Capital Additionalandise Equip- Notes Accounts Stock Paid-in Description of Transactions Cash + Inventory + ment = Payable + Payable + (at par) + Capital1. Original incorporation +300 = + 30 + 2702. Inventory purchased –95 +95 =3. Inventory purchased +85 = + 854. Return of inventory tosupplier –11 = – 115. Purchase of equipment –10 +40 = +306. Sale of equipment + 4 – 4 =7. Payment to creditor –18 = – 188. Inventory purchased –50 +100 = + 509. No entry except ondetailed underlyingrecords ==Balance, January 31, 20X110EXHIBIT 1–34AUTOPARTES MADRIDAnalysis of TransactionsFor the Month Ended March 31, 20X1Assets Liabilities + Owner’s EquityEquip- Accounts Note You, Description of Transactions Cash + Inventory + ment = Payable + Payable + Capital1. Initial investment +75,000 = +75,0002. Inventory acquired for cash 10,000 +10,000 =3. Inventory acquired on credit + 8,000 = + 8,0004. Equipment acquired – 5,000 +15,000 = +10,0005. No entry =6. Tires for family – 600 = - 6007. Parts returned tosupplier for cash + 300 – 300 =8. No effect on total inventory =9. Parts returned tosupplier for credit – 500 = – 50010. Payment on note – 1,000 = –1,00011. Equipment acquired + 5,000 = +5,00012. Payment to creditors – 3,000 = –3,00013. No entry14. No entry15. Exchange of equipment + 2,500 – 4,000 =+ 1,500+ 58,800 +16,600 +17,500 = +4,500 + 9,000 +79,40092,900 92,900Chapter 1 Accounting: The Language of Business231-35 (25-40 min.) Note that transaction 9 is not covered directly in the text. However, it should be possible to figure out the accounting for it from similar items that are covered. However, some instructors may want to omit transaction 9.1. See Exhibit 1-35.2. FREIDA CRUZ, ATTORNEY-AT-LAWBalance SheetDecember 31, 20X0Liabilities andAssets Owner’s EquityLiabilities:Cash in bank $46,000 Note payable $ 3,000 Note receivable 2,000 Account payable 1,000 Rental damage deposit 1,000 Total liabilities $ 4,000 Legal supplies on hand 1,000 Owner’s equity:Computer 5,000 Freida Cruz, capital 55,000 Office furniture 4,000 Total liabilities andTotal assets $59,000 owner’s equity $59,000 1-36 (15-25 min.) See Exhibit 1-36.1-37 (20-35 min.)1. See Exhibit 1-37.2. NIKE, INC.Balance SheetJune 3, 2009(In Millions)Liabilities andAssets Owners’ EquityCash $ 2,424 Total liabilities $ 4,617 Inventories 2,400 Owners’ equity 8,783 Property, plant, and equipment 1,932Other assets 6,644Total $13,400 Total $13,40024EXHIBIT 1–35FREIDA CRUZ ATTORNEYAnalysis of Business Transactions(In Thousands of Dollars)Assets = Liabilities and Owner’s EquityOwner’s Cash Note Rental Legal Office Liabilities Equity Description in Receiv- Damage Supplies Furni- Note Account F. Cruz of Transactions Bank able Deposit on Hand Computer ture Payable Payable Capital 2. Openinginvestment +55 = +554. Rental deposit – 1 +1 =5. Purchased computer – 2 +5 = +36. Purchased supplies +1 = +17. Purchasedfurniture – 4 +4 =9. Note receivablefrom G. See – 2 +2 =Balance, December31, 20X0 +46 +2 +1 +1 +5 +4 = +3 +1 +5559 59General Comments:•Transactions 1 and 3 are personal rather than business transactions.•In transaction 4, no obligation (liability) is set up for the rent because it is not payable until January 2 and no rental services will occur until January.•Transaction 8 requires no entry because no services have been performed during December.Chapter 1 Accounting: The Language of Business23EXHIBIT 1–36WALGREEN COMPANYAnalysis of Transactions(In Millions of Dollars)Assets Liabilities and Stockholders’ EquityProperty Stock-Inven- and Other Notes Accounts Other holders’Description of Transactions Cash + tories + Assets = Payable + Payable + Liabilities + Equity Balance May 31 2,300 6,891 15,952 = 4,599 6,357 14,1871. Issuance of stock for cash +30 = + 302. Issuance of stock for equipment +42 = + 423. Borrowing +13 = +134. Acquisition of equipment for cash –18 +18 =5. Acquisition of inventory on account +94 = +946. Payments to creditors –35 = –357. Sale of equipment +2 - 2 =Balance June 2 2,292 6,985 16,010 = 13 4,658 6,357 14,25925,287 25,287WALGREEN COMPANYBalance SheetJune 2, 2009(In Millions of Dollars)Assets Liabilities and Stockholders’ EquityCash $ 2,292 Notes payable $ 13Inventories 6,985 Accounts payable 4,658Property and other assets 16,010 Other liabilities 6,357Stockholders’ equity 14,259 Total $25,287 Total $25,28724EXHIBIT 1–37NIKE, INC.Analysis of Transactions(In Millions of Dollars)AssetsLiabilities and Owners’ EquityDescription of Transactions Cash + Inven-tories +Property,Plant, andEquip. +Other Assets=TotalLiabil-ities +Owners’EquityBalance May 31 2,291 2,357 1,958 6,644 4,557 8,6931. Inventory purchased -28 +28 =2. Inventory purchased +19 = +193. Return of inventoryto supplier -4 = -44. Purchase of equipment -3 +14 = +115. Sale of equipment +40 -40 =6. No entry =7. Payment to creditor -16 = -168. Borrowed from bank +50 = +509. Issued common stock +90 = +9010. No entry except ondetailed underlyingrecords =Balance, June 3 2,424 2,400 1,932 6,644 =13,400 13,400Chapter 1 Accounting: The Language of Business231-38 (15-20 min.)REBECCA GURLEY, REALTORBalance SheetNovember 30, 20X1Liabilities andAssets Owners’ EquityCash $ 6,000 Liabilities:Undeveloped land 180,000 Accounts payable $ 6,000 Office furniture 16,000 (a) Mortgage payable 95,000 Franchise 18,000 (b) Total liabilities 101,000Owner’s equity:Rebecca Gurley, capital 119,000 (c) Total assets $220,000 Total liabilities andown er’s equity $220,000a.$17,000 – $1,000 = $16,000b. A franchise is an economic resource that has been purchased to benefit future operations.c.$220,000 – $101,000 = $119,000Note that Goldstein’s death may have considerable negative influence on future operations, but accounting does not formally measure its monetary impact. Moreover, transactions 3 and 4 are personal rather than business transactions.1-39 (10 min.)1. Cash would rise by $1,000 and the liability, Deposits, would rise by the same amount.2. Deposits are liabilities because Wells Fargo owes these amounts to depositors. They aredepositors’ claims on the assets of the bank.3. Loans Receivable would increase and Cash would decrease by $75,000.4. Deposits would decrease and Cash would decrease by $4,000.1-40 (10 min.) Amounts are in millions.1. a. Cash = Total assets - Noncash assets= €28,598 -€24,492= €4,106b. Stockholders’ equity= Total assets - Total liabilities= €28,598 -€22,495= €6,1032. Total liabilit ies and stockholders’ equity = total assets = €28,598.241-41 (20-30 min.)UNITED TECHNOLOGIES CORPORATIONBalance SheetJune 30, 2009(In Millions of Dollars)Liabilities andAssets Stockholders’ EquityCash $ 4,196 (1) Accounts payable $ 4,599 Inventories 8,539 Other liabilities 24,819 Fixed assets 6,179 Long term debt 8,721 Other assets 37,811 Total liabilities 38,139Common stock $11,369Other stockholders’equity 7,037 (3)Total stockholders’equity 18,406 (2)Total liabilities andTotal assets $56,545 stockholders’ equity $56,545 Notations (1), (2), and (3) designate the answers to the requirements. (1) The $4,016 cash was computed by taking total assets minus all assets except cash. To calculate (2) and (3), note that total assets must equal tota l liabilities plus stockholders’ equity, $56,545. Furthermore, total liabilities is $4,599 + $24,819 + $8,721 = $38,139. Therefore, total stockholders’equity is $56,545 – $38,139 = $18,406, denoted by (2) above. Other stockholders’equity is $18,406 –$11,369 = $7,037, denoted by (3) above.Chapter 1 Accounting: The Language of Business231-42 (20 min.)MACY’S, INC.Balance SheetAugust 1, 2009(In Millions of Dollars)Liabilities andAssets Share holders’ EquityCash $ 515 (a)Merchandise accountsInventories 4,634 payable $ 1,683 Property, plant, Long-term debt 8,632and equipment 10,046 Other liabilities 5,920Total liabilities $16,235 (b) Other assets 5,589 Shareholders’ equity 4,549 (c)Total liabilities andTotal assets $20,784 shareholders’ equity $20,784 Notations (a), (b), and (c) designate the answers to the requirements. Cash is calculated by subtracting the values given for the other assets from total assets: $20,784 - $4,634-$10,046 -$5,589 = $515. Cash is the smallest individual asset. Companies try to keep cash balances small because they do not earn large returns on cash accounts. To calculate (b), simply add the components $1,683 + $8,632 + $5,920. For (c), note that total liabilities and shareholde rs’ equity equals total assets, $20,784, so shareholders’ equity is $20,784 less total liabilities of $16,235, which equals $4,549.241-43 (10 min.)1.ABBOUD PARTNERSBalance SheetJune 15, 20X0Assets Liabilities and Owners’ EquityRental house $300,000 Mortgage loan $240,000Owners’ equityAdnan Abboud, Capital 30,000Gamal Abboud, Capital 30,000Total assets $300,000 Total liabilities and ow ners’equity $300,0002.ABBOUD CORPORATIONBalance SheetJune 15, 20X0Assets Liabilities & Stockholders’ EquityRental house $300,000 Mortgage loan $240,000Stockholders’ equityCommon stock, par value 2,000Additional paid-in capital 58,000Total assets $300,000 Total liabilities and sto ckholders’ equity $300,0001-44 (10 min.)1. The par value line would increase by 500,000,000 × $.01 = $5,000,000 and the number ofshares issued and outstanding would increase by 500 million. Additional paid-in capital would increase by 500,000,000 × ($6.00 – $.01) = $2,995,000,000.2. IBM shows all of its paid-in capital as a one-line item. Therefore, its common stock linewould increase by $120,000,000 and the number of issued and outstanding shares would increase by 1 million.Chapter 1 Accounting: The Language of Business231-45 (5-10 min.)The common stock line should show 2,442,676,580 × $.75 = $1,832 million. The average price per share paid by the original investors for the Chevron common stock was $14,359 million + $1,832 million = $16,191 million ÷ 2,442,676,580 = $6.63. Note that the par value is small, $.75, as compared to $6.63.The relatively large difference between the original issuance price ($6.63) and the current market price ($66 on June 30, 2009) is quite typical of many large successful companies. This is usually caused by increased investment attractiveness based on a record of profitable operations over many years.1-46 (5-10 min.)1. The par value of Honda’s shares is ¥86,067,000,000 ÷ 1,834,828,430 = ¥46.9.2. The average price per share paid by the original investors was ¥140.9: ¥86,067 million +¥172,529 million = ¥258,596 million; ¥258,596 million ÷ 1,834,828,430 = ¥140.9. Note that the ¥140.9 easily exceeds the par value of ¥46.9.3. The large difference between the original issuance price of ¥140.9 and the market price of¥2,150 at the end of fiscal 2009 is typical for many successful companies. This phenomenon is usually caused by increased investment attractiveness based on a record of profitable operations over many years.1-47 (10 min.)There are two popular sets of generally accepted accounting principles (GAAP) in the world—IFRS set by the International Accounting Standards Board, and U.S. GAAP set by the Financial Accounting Standards Board. In 2005 the European Union adopted IFRS to be used by all companies in its member nations. Thus, Carrefour, a French company, must issue financial statements that comply with IFRS. Its auditors will examine its financial statements to ensure compliance with IFRS and must confirm this in the audit opinion. Although not mentioned in the chapter, the phrase “as adopted by the European Union” is also significant. As in many cases, countries that adopt IFRS may not accept 100% of its standards, and the European Union makes a few adjustments to the standards.In contrast, companies based in the United States, such as Safeway, must use U.S. GAAP, not IFRS. Thus, Safeway’s audit opinion clearly states that its statements comply with U. S. GAAP.Both companies use Deloitte & Touche LLP as an auditor, but the auditor must apply different standards when auditing Carrefour than when auditing Safeway.24。

高级财务会计课后答案

高级财务会计课后答案第一章简介本章是高级财务会计的课后答案,将解答课后练习题,帮助学生更好地理解和掌握所学知识。

1.1 问题一问题描述:简要介绍财务会计的定义和目的。

解答:财务会计是一种记录、报告和分析经济活动的方法和过程。

它旨在提供有关企业财务状况和业务运营的信息,帮助利益相关者做出决策。

财务会计的目的是为了提供透明、准确、可靠的财务信息,以满足外部利益相关者的信息需求。

1.2 问题二问题描述:解释财务会计与管理会计之间的区别。

解答:财务会计和管理会计都是会计学的分支,但它们有着不同的目标和受众。

财务会计主要关注企业整体财务状况和业务运营情况,主要面向外部利益相关者,如股东、投资者、政府等。

它的报告对象是整个企业,其财务报表包括资产负债表、利润表、现金流量表等。

管理会计则是为企业内部的管理决策提供信息支持。

它关注企业内部各个部门和业务的成本、效益等信息,并通过各种报表和分析工具帮助管理层进行决策。

管理会计更加灵活和细致,可以根据不同的管理需求进行定制化报告。

第二章会计框架本章将解答与会计框架相关的课后练习题。

2.1 问题一问题描述:解释会计框架的作用。

解答:会计框架是一套规范和原则,用于指导财务会计的报告和分析。

它的主要作用有以下几个方面:•提供统一的准则和标准,使财务报表在不同企业和行业之间具有可比性。

•确保财务报表的准确性和可靠性,提高信息的可信度。

•帮助利益相关者理解和解读财务报表,做出准确的决策。

•为审计和监管提供依据,确保企业遵守财务规章和法律法规。

2.2 问题二问题描述:列举并解释会计框架的基本假设。

解答:会计框架的基本假设包括以下几个方面:•会计实体假设:假设企业是一个独立的实体,与其所有者和其他企业区分开来。

•持续经营假设:假设企业将长期经营下去,不会短期倒闭或停业。

•会计期间假设:假设企业的经营活动可以划分为一系列离散的会计期间,如月度、季度和年度。

•货币计量假设:假设企业的经济活动和财务信息可以用货币单位进行度量和记录。

查尔斯亨格瑞_财务会计_课后练习答案01

查尔斯亨格瑞_财务会计_课后练习答案01CHAPTER 1COVERAGE OF LEARNING OBJECTIVESChapter 1 Accounting: The Language of Business1CHAPTER 11-1 Accounting is a process of identifying, recording, summarizing, and reporting economic information to decision makers.1-2 No. Accounting is about real information about real companies. In learning accounting it is helpful to see accounting reports from various companies. This helps put the rules and techniques of accounting into an understandable framework and provides familiarity with the diversity of practice.1-3 Examples of decisions that are likely to be influenced by financial statements include choosing where to expand or reduce operations, lending money, investing ownership capital, and rewarding mangers.1-4 Users of financial statements include managers, lenders, suppliers, owners, income tax authorities, and government regulators.1-5 The major distinction between financial accounting and management accounting is their use by two classes of decision makers. Management accounting is concerned mainly with how accounting can serve internal decision makers such as the chief executive officer and other executives. Financial accounting is concerned with supplying information to external users. 1-6 The balance sheet equation is Assets = Liabilities + Owners’ equity. It is the fundamental framework of accounting. The left side lists the resources of the organization, and the right side lists the claims against those resources.1-7 No. Every transaction should leave the balance sheet equation in balance. Accounting is often called ―double-entry‖because accountants must enter at least two numbers for eac h transaction to keep the equation in balance.1-8 This is true. When a company buys inventory for cash, one asset is traded for another, and neither total assets nor total liabilities change. Thus, the balance sheet equation stays in balance. When a company buys inventory on credit, both inventory and accounts payable increase. Thus, both total assets and total liabilities increase by the same amount, again keeping the balance sheet equation in balance.1-9 The evidence for a note payable includes a promissory note, but the evidence for an account payable does not. A note payable is generally to a lender while an account payable is generally to a supplier.1-10 Ownership shares in most large corporations are easily traded in the stock markets, corporate owners have limited liability, and the owners of sole proprietorships or partnerships are usually also managers in the company while most corporations hire professional managers.21-11 Limited liability means that corporate owners are not personally liable for the debts of the corporation. Creditors’claims can be satisfied only by the assets of the particular corporation.1-12 The corporation is the most prominent type of entity and corporations do by far the largest volume of business.1-13 Yes. In the United Kingdom corporations frequently use the word limited (Ltd.) in their name. In many countries whose laws trace back to Spain, the initials S.A. refer to a ―society anonymous,‖ meaning that multiple unidentified owners stand behind the company, which is essentially the same structure as a corporation.1-14 Almost all states forbid the issuance of stock at below par; thus, par values are customarily set at very low amounts and have no real importance in affecting economic behavior of the issuing entity.1-15 The board of directors is the elected link between stockholders and the actual managers.It is the board’s duty to ensure that managers act in the best interests of shareholders.1-16 In the U.S. GAAP is generally set by the Financial Accounting Standards Board. The SEC has formal authority for specifying accounting standards for companies with publicly held stock, as delegated by Congress, but it usually accepts the standards promulgated by the FASB. Internationally, a majority of countries accept IFRS as set by the International Accounting Standards Board as their GAAP.1-17 Until recently this was true. However, now the SEC allows companies headquartered outside the U. S. to report using IFRS.1-18 Audits have value because they add credibilit y to a company’s financial statements.Provided that auditors have the expertise to assess the accuracy of financial statements and the integrity to report any problems they discover, the investing public can put more faith in statements that are audited.1-19 A CPA is a certified public accountant. One becomes a CPA by a combination of education, qualifying experience, and the passing of a two-day national examination. A CA (chartered accountant) is the equivalent of a CPA in many parts of the world, including most former British Commonwealth countries.1-20 Public accountants must obey standards of independence and integrity. In addition, there are many more ethical standards that pertain to accountants. Some folks call accounting the moral guardian of companies. This reputation has been sullied recently by corporate scandals that went undetected (or, at least, unreported by accountants), but accountants are working to regain the high ethical regard they have traditionally maintained.Chapter 1 Accounting: The Language of Business31-21 No. The fundamental accounting principles apply equally to nonprofit (that is, not-for-profit) and profit-seeking organizations. Managers and accountants in hospitals, universities, government agencies, and other nonprofit organizations use financial statements. They need to raise and spend money, prepare budgets, and judge financial performance. Nonprofit organizations need to use their limited resources wisely, and financial statements are essential for judging their use of resources.1-22 Double-entry refers to the concept that every transaction involves two or more accounts with the effect being to retain the balance in the balance sheet equation. The double-entry concept is important because it emphasizes that there are assets and claims on assets. In the balance sheet, for example, borrowing money provides an asset, cash, and creates a liability. Inaddition to this conceptual benefit there is a clerical benefit. Maintaining a balanced relationship provides an indicator of errors. If the balance sheet equation does not balance, an error has been made.1-23 Historians are primarily concerned with events that have already occurred. In that sense,a company’s financial statements do report on history—transactions that are complete.The negative side of this is that many important things that affect the value of a firm are based on what will happen in the future. Thus, investors often worry about expectations and predictions. Of course, there is no way to agree on the accuracy of expectations and predictions. The positive side of historical financial statements is that they present a no-nonsense perspective on what actually happened, where the company was at a point in time, or what it accomplished over a period of time. It is easier to predict the future when you know where you are and how you got there. You might liken the importance of historical financial statements to the importance of navigation instruments. If you do not know where you are and where you are headed, it is very hard to get to where you want to go.Most people who refer to accountants as historians intend it as a criticism, although, as indicated above, a historical focus ensures that the data are measurable and verifiable.1-24 Such arguments are fun but can never be truly resolved. The notion behind the importance of the corporation is that for any substantial growth to occur there must be a system for organizing resources and using them over long periods of time. The corporate form of ownership helps companies raise large amounts of capital via stock issuance as well as borrowing. It allows us to separate ownership from management. It protects the personal assets of shareholders, and because their maximum losses can be limited, more risky undertakings can be financed. Finally, it has perpetual life so its activity is not disrupted by the death of any shareholder. Corporations operate under a set of established rules of behavior for entering into contracts and being sure that other parties can be relied upon to uphold their side of an agreement.Accounting helped corporations emerge as the dominant economic organization in the world. Without accounting it would be difficult to coordinate the activities of large corporations. It would be especially difficult to separate management from ownership if accounting did not provide information about the performance of managements.41-25 The auditor increases the value of financial statements by reassuring the reader of the statements that an―independent‖ and a ―qualified‖ third party has reviewed management’s disclosures and believes they fairly present the company’s performance.The fact that you personally do not recognize the name of the audit firm should not be a problem, because only CPAs can perform public audits and sign audit opinions. Every state has strict procedures for licensing CPAs, so such people are qualified. Nevertheless, audit firms develop reputations, and ones with a positive public image may give some financial statement users more confidence in the financial statements they audit.1-26 (10 min.) Amounts are in millions.1. Assets = Liabilities + Owners’ Equity$7 = $3 + $42. Assets and liabilities would increase by $1 million. Owners’ equity would be unaffected.1-27 (15-20 min.)June 2 Owners invested $6,000 additional cash in Sok ol’s Furniture Company.3 Owners invested an additional $4,000 into the company by contributingadditional store fixtures valued at $4,000.4 Sok ol’s Furniture Company purchased additional furniture inventory for$3,000 cash.5 Sok ol’s Furniture Company purchased furniture inventory on account for$6,000.6 Sok ol’s Furniture Company sold store fixtures for $3,000 cash.7 Sok ol’s Furniture Company purchased $6,000 of store fixtures, paying$5,000 cash now and agreeing to pay $1,000 later.8 Sok ol’s Furniture Company paid $2,000 on accounts payable.9 Sok ol’s Furniture Company returned $400 of merchandise (furnitureinventory) for credit against accounts payable.10 Owners withdrew $2,000 cash from Sokol’s Furniture Company.Chapter 1 Accounting: The Language of Business51-28 (10-20 min.)Sept. 2 Brisbane purchased $2,500 of store fixtures on account.3 Owner or owners withdrew $2,000 cash.4 Brisbane returned $5,000 of its inventory of computers for $5,000 creditagainst its accounts payable.5 Computers (inventory) valued at $7,000 were invested in the company byowners.8 Brisbane paid $500 on accounts payable.9 Brisbane purchased $3,500 of store fixtures, paying $1,000 now andagreeing to pay $2,500 later.10 Brisbane returned $300 of store fixtures for credit against accounts payable.1-29 (15-25 min.)ATLANTA CORPORATIONBalance SheetMarch 31, 20X1Liabilities andAssets Stockholders’ EquityCash $ 5,000 (a) Liabilities:Merchandise inventory 44,000 (b) Accounts payable $ 12,000 (f) Furniture and fixtures 2,000 (c) Notes payable 10,000 Machinery and equipment 27,000 (d) Long-term debt 27,000 (g) Land 39,000 (e) Total liabilities 49,000 Building 24,000 Stockholders’ equity:Total $141,000 Paid-in capital 92,000 (h)Total $141,000(a) Cash: 14,000 + 1,000 – 10,000 = 5,000(b) Merchandise inventory: 40,000 + 4,000 = 44,000(c) Furniture and fixtures: 3,000 – 1,000 = 2,000(d) Machinery and equipment: 15,000 + 12,000 = 27,000(e) Land: 14,000 + 25,000 = 39,000(f) Accounts payable: 8,000 + 4,000 = 12,000(g) Long-term debt: 12,000 + 15,000 = 27,000(h) Paid-in capital: 80,000 + 12,000 = 92,000Note: Event 5 requires no change in the balance sheet.61-30 (25-35 min.)LIVERPOOL COMPANYBalance SheetNovember 30, 20X1Liabilities andAssets Stockholders’ EquityCash £ 18,000 (a) Liabilities:Merchandise inventory 29,000 Accounts payable £ 9,000 (d) Furniture and fixtures 8,000 Notes payable 31,000 (e) Machinery and equip. 33,000 (b) Long-term debt payable 101,000 (f) Land 35,000 (c) Total liabilities 141,000 Building 241,000 Stockholders’ equity:Total £364,000 Paid-in Capital 223,000 (g)Total £364,000(a) Cash: 22,000 – 3,000 – 7,000 + 6,000 = 18,000(b) Machinery and equipment: 20,000 + 13,000 = 33,000(c) Land: 41,000 – 6,000 = 35,000(d) Accounts payable: 16,000 – 7,000 = 9,000(e) Notes payable: 21,000 + (13,000 – 3,000) = 31,000(f) Long-term debt payable: 124,000 – 23,000 = 101,000(g) Paid-in capital: 200,000 + 23,000 = 223,000Note: Event 4 requires no change in the balance sheet.1-31 (5-10 min.)1. Total liabilities = Total assets -stockholders’ equity= $798,000,000,000 - $105,000,000,000= $693,000,000,0002. Common stock, par value = $.07 × 10,536,897,000 = $737,582,790.Like other items on General Electric’s balance sheet, the amount would be rounded off to millions:Common stock, par value $738Chapter 1 Accounting: The Language of Business71-32 (20-30 min.) See Exhibit 1-32. Equipment and furniture could be in two separate accounts rather than combined. 1-33 (20-35 min.)1. See Exhibit 1-33.2. LMN CORPORATIONBalance SheetJanuary 31, 20X1(In Thousands of Dollars)Liabilities andAssets Stockholders’ EquityLiabilities:Cash $131 Note payable $ 30Accounts payable 106 Merchandise inventory 269 Total liabilities $136Stockholders’ equity:Equipment 36 Capital stock,$1 par, 30,000 sharesissued and outstanding $ 30Additional paid-in capitalin excess of par value 270 300 Total $436 Total $436 1-34 (20-35 min.)1. See Exhibit 1-34.2. AUTOPARTES MADRIDBalance SheetMarch 31, 20X1Assets Liabilities and Owners’ EquityCash €58,800 Liabilities:Inventory 16,600 Accounts payable € 4,500 Equipment 17,500 Note payable 9,000Total liabilities 13,500You, capital 79,400 Total €92,900 Total €92,900 8EXHIBIT 1–32MCLEAN SERVICES, INC.Analysis of April 20X1 Transactions(In Thousands of Dollars)Assets Liabilities and Stockholders’ EquityEquipment Note Accounts Paid-in Description of Transactions Cash + and Furniture = Payable + Payable + Capital1. Issuance of stock +50 = +502. Issuance of stock +20 = +203. Borrowing +35 = +354. Acquisition for cash –33 +33 =5. Acquisition on account +10 = +106. Payments to creditors – 4 = – 47. Sale of equipment + 8 – 8 =8. No entry =+56 +55 = +35 + 6 + 70111 111MCLEAN SERVICES, INC.Balance SheetApril 30, 20X1Assets Liabilities and Stockholders’ EquityNote payable $ 35,000 Cash $ 56,000 Account payable 6,000Equipment and furniture 55,000 Paid-in Capital 70,000Total $111,000 Total $111,000Chapter 1 Accounting: The Language of Business9EXHIBIT 1–33LMN CORPORATIONJanuary 20X1Analysis of Transactions(In Thousands of Dollars)Assets Liabilities + Owners’ EquityMerch- Capital Additionalandise Equip- Notes Accounts Stock Paid-in Description of Transactions Cash + Inventory + ment = Payable + Payable + (at par) + Capital1. Original incorporation +300 = + 30 + 2702. Inventory purchased –95 +95 =3. Inventory purchased +85 = + 854. Return of inventory tosupplier –11 = – 115. Purchase of equipment –10 +40 = +306. Sale of equipment + 4 – 4 =7. Payment to creditor –18 = – 188. Inventory purchased –50 +100 = + 509. No entry except ondetailed underlyingrecords ==Balance, January 31, 20X110EXHIBIT 1–34AUTOPARTES MADRIDAnalysis of TransactionsFor the Month Ended March 31, 20X1Assets Liabilities + Owner’s EquityEquip- Accounts Note You, Description of Transactions Cash + Inventory + ment = Payable + Payable + Capital1. Initial investment +75,000 = +75,0002. Inventory acquired for cash 10,000 +10,000 =3. Inventory acquired on credit + 8,000 = + 8,0004. Equipment acquired – 5,000 +15,000 = +10,0005. No entry =6. Tires for family – 600 = - 6007. Parts returned tosupplier for cash + 300 – 300 =8. No effect on total inventory =9. Parts returned tosupplier for credit – 500 = – 50010. Payment on note – 1,000 = –1,00011. Equipment acquired + 5,000 = +5,00012. Payment to creditors – 3,000 = –3,00013. No entry14. No entry15. Exchange of equipment + 2,500 – 4,000 =+ 1,500+ 58,800 +16,600 +17,500 = +4,500 + 9,000 +79,40092,900 92,900Chapter 1 Accounting: The Language of Business111-35 (25-40 min.) Note that transaction 9 is not covered directly in the text. However, it should be possible to figure out the accounting for it from similar items that are covered. However, some instructors may want to omit transaction 9.1. See Exhibit 1-35.2. FREIDA CRUZ, ATTORNEY-AT-LAWBalance SheetDecember 31, 20X0Liabilities andAssets Owner’s EquityLiabilities:Cash in bank $46,000 Note payable $ 3,000 Note receivable 2,000 Account payable 1,000 Rental damage deposit 1,000 Total liabilities $ 4,000 Legal supplies on hand 1,000 Owner’s equity:Computer 5,000 Freida Cruz, capital 55,000 Office furniture 4,000 Total liabilities andTotal assets $59,000 owner’s equity $59,000 1-36 (15-25 min.) See Exhibit 1-36.1-37 (20-35 min.)1. See Exhibit 1-37.2. NIKE, INC.Balance SheetJune 3, 2009(In Millions)Liabilities andAssets Owners’ EquityCash $ 2,424 Total liabilities $ 4,617 Inventories 2,400 Owners’ equity 8,783 Property, plant, and equipment 1,932 Other assets 6,644Total $13,400 Total $13,40012FREIDA CRUZ ATTORNEYAnalysis of Business Transactions(In Thousands of Dollars)Assets = Liabilities and Owner’s EquityOwner’s Cash Note Rental Legal Office Liabilities Equity Description in Receiv- Damage Supplies Furni- Note Account F. Cruz of Transactions Bank able Deposit on Hand Computer ture Payable Payable Capital 2. Openinginvestment +55 = +554. Rental deposit – 1 +1 =5. Purchased computer – 2 +5 = +36. Purchased supplies +1 = +17. Purchasedfurniture – 4 +4 =9. Note receivablefrom G. See – 2 +2 =Balance, December31, 20X0 +46 +2 +1 +1 +5 +4 = +3 +1 +5559 59General Comments:Transactions 1 and 3 are personal rather than business transactions.In transaction 4, no obligation (liability) is set up for the rent because it is not payable until January 2 and no rental services will occur until January.Transaction 8 requires no entry because no services have been performed during December.Chapter 1 Accounting: The Language of Business13WALGREEN COMPANYAnalysis of Transactions(In Millions of Dollars)Assets Liabilities and Stockholders’ EquityProperty Stock-Inven- and Other Notes Accounts Other holders’Description of Transactions Cash + tories + Assets = Payable + Payable + Liabilities + Equity Balance May 31 2,300 6,891 15,952 = 4,599 6,357 14,1871. Issuance of stock for cash +30 = + 302. Issuance of stock for equipment +42 = + 423. Borrowing +13 = +134. Acquisition of equipment for cash –18 +18 =5. Acquisition of inventory on account +94 = +946. Payments to creditors –35 = –357. Sale of equipment +2 - 2 =Balance June 2 2,292 6,985 16,010 = 13 4,658 6,357 14,25925,287 25,287WALGREEN COMPANYBalance SheetJune 2, 2009(In Millions of Dollars)Assets Liabilities and Stockholders’ EquityCash $ 2,292 Notes payable $ 13Inventories 6,985 Accounts payable 4,658Property and other assets 16,010 Other liabilities 6,357Stockholders’ equity 14,259 Total $25,287 Total $25,28714NIKE, INC. Analysis of Transactions (In Millions of Dollars)AssetsLiabilities and Owners’ EquityDescription of Transactions Cash + Inven-tories +Property,Plant, andEquip. +Other Assets=TotalLiabil-ities +Owners’EquityBalance May 31 2,291 2,357 1,958 6,644 4,557 8,6931. Inventory purchased -28 +28 =2. Inventory purchased +19 = +193. Return of inventoryto supplier -4 = -44. Purchase of equipment -3 +14 = +115. Sale of equipment +40 -40 =6. No entry =7. Payment to creditor -16 = -168. Borrowed from bank +50 = +509. Issued common stock +90 = +9010. No entry except ondetailed underlyingrecords =Balance, June 3 2,424 2,400 1,932 6,644 =13,400 13,400Chapter 1 Accounting: The Language of Business15 REBECCA GURLEY, REALTORBalance SheetNovember 30, 20X1Liabilities andAssets Owners’ EquityCash $ 6,000 Liabilities:Undeveloped land 180,000 Accounts payable $ 6,000 Office furniture 16,000 (a) Mortgage payable 95,000 Franchise 18,000 (b) Total liabilities 101,000Owner’s equity:Rebecca Gurley, capital 119,000 (c) Total assets $220,000 Total liabilities andown er’s equity $220,000a.$17,000 – $1,000 = $16,000b. A franchise is an economic resource that has been purchased to benefit future operations.c.$220,000 – $101,000 = $119,000Note that Goldstein’s death may have considerable negative influence on future operations, but accounting does not formally measure its monetary impact. Moreover, transactions 3 and 4 are personal rather than business transactions.1-39 (10 min.)1. Cash would rise by $1,000 and the liability, Deposits, would rise by the same amount.2. Deposits are liabilities because Wells Fargo owes these amounts to depositors. They aredepositors’ claims on the assets of the bank.3. Loans Receivable would increase and Cash would decrease by $75,000.4. Deposits would decrease and Cash would decrease by $4,000.1-40 (10 min.) Amounts are in millions.1. a. Cash = Total assets - Noncash assets= €28,598 -€24,492= €4,106b. Stockholders’ equity= Total assets - Total liabilities= €28,598 -€22,495= €6,1032. Total liabilit ies and stockholders’ equity = total assets = €28,598.16UNITED TECHNOLOGIES CORPORATIONBalance SheetJune 30, 2009(In Millions of Dollars)Liabilities andAssets Stockholders’ EquityCash $ 4,196 (1) Accounts payable $ 4,599 Inventories 8,539 Other liabilities 24,819 Fixed assets 6,179 Long term debt 8,721 Other assets 37,811 Total liabilities 38,139Common stock $11,369Other stockholders’equity 7,037 (3)Total stockholders’equity 18,406 (2)Total liabilities andTotal assets $56,545 stockholders’ equity $56,545 Notations (1), (2), and (3) designate the answers to the requirements. (1) The $4,016 cash was computed by taking total assets minus all assets except cash. To calculate (2) and (3), note that total assets must equal tota l liabilities plus stockholders’ equity, $56,545. Furthermore, total liabilities is $4,599 + $24,819 + $8,721 = $38,139. Therefore, total stockholders’equity is $56,545 – $38,139 = $18,406, denoted by (2) above. Other stockholders’equity is $18,406 –$11,369 = $7,037, denoted by (3) above.Chapter 1 Accounting: The Language of Business17MACY’S, INC.Balance SheetAugust 1, 2009(In Millions of Dollars)Liabilities andAssets Share holders’ EquityCash $ 515 (a)Merchandise accountsInventories 4,634 payable $ 1,683 Property, plant, Long-term debt 8,632and equipment 10,046 Other liabilities 5,920Total liabilities $16,235 (b) Other assets 5,589 Shareholders’ equity 4,549 (c)Total liabilities andTotal assets $20,784 shareholders’ equity $20,784 Notations (a), (b), and (c) designate the answers to the requirements. Cash is calculated by subtracting the values given for the other assets from total assets: $20,784 - $4,634-$10,046 -$5,589 = $515. Cash is the smallest individual asset. Companies try to keep cash balances small because they do not earn large returns on cash accounts. To calculate (b), simply add the components $1,683 + $8,632 + $5,920. For (c), note that total liabilities and shareholde rs’ equity equals total assets, $20,784, so shareholders’ equity is $20,784 less total liabilities of $16,235, which equals $4,549.181.ABBOUD PARTNERSBalance SheetJune 15, 20X0Assets Liabilities and Owners’ EquityRental house $300,000 Mortgage loan $240,000Owners’ equityAdnan Abboud, Capital 30,000Gamal Abboud, Capital 30,000Total assets $300,000 Total liabilities and ow ners’equity $300,0002.ABBOUD CORPORATIONBalance SheetJune 15, 20X0Assets Liabilities & Stockholders’ EquityRental house $300,000 Mortgage loan $240,000Stockholders’ equityCommon stock, par value 2,000Additional paid-in capital 58,000Total assets $300,000 Total liabilities and sto ckholders’ equity $300,0001-44 (10 min.)1. The par value line would increase by 500,000,000 × $.01 = $5,000,000 and the number ofshares issued and outstanding would increase by 500 million. Additional paid-in capital would increase by 500,000,000 ×($6.00 – $.01) = $2,995,000,000.2. IBM shows all of its paid-in capital as a one-line item. Therefore, its common stock linewould increase by $120,000,000 and the number of issued and outstanding shares would increase by 1 million. Chapter 1 Accounting: The Language of Business19。

亨格瑞管理会计英文第15版答案11.docx

亨格瑞管理会计英文第15版答案11CHAPTERllCapitalBudgetin ; 1. ; Thepresentvalueis$480,00(a)$480,000=annualpaymen ; annualpayment=$480,0004- 1 annualpaymcnt=$480,000 4- 9 ; annualpayment=$480,000 4- 8 armualpaymcnt 二$480, 0004-8; anCHAPTER 11 Capital Budgeting1.The present value is $480, 000 and the annual payments are an annuity, requiring use of Table 2:(a)$480,000 = annual payment X 11.2578 annual payment 二 $480, 000 4- 11. 2578 二 $42, 637 (b) $480, 000 二 annual payment X 9.4269annual payment = $480, 000payment X 8.0552 annual payment二 $480,000payment X 8.5595 annual payment= $480, 000 payment X 7.6061 annual payment = $480, 000payment X 6.8109 annual payment= $480, 000 4- 6.8109 =$70,475 (a) Total payments=30 X $50,918 = $1,527,540Total interest paid= $1, 527, 540- $480, 000 = $1, 047, 540 2.3.(b) Total payments 二 15 X $63, 107= $946, 605 Total interest paid 二$946, 605 一 $480, 000 = $466, 6059. 4269 = $50,918 (c) $480, 000 = annual8. 0552 二$59, 589 (a)$480, 000 = annual 8. 5595 二 $56, 078 (b) $480, 000 = annual 7. 6061 = $63, 107 (c) $480, 000 二 annualmin.) Buy. The net present value is positive.Initial outlay *Present value of cash operating savings, from12-year, 12% column of Table 2, 6. 1944 X $5, 000 Net present value$ (21,000) * The trade-in allowance really consists of a $5,000 adjustme nt of the sei ling price and a bona fide $10,000 cash al Iowa neo for the old equipment ・ The relevant amo unt is the incremental cash outlay, $21,000. The book value is irrelevant・ min.)Copyright ?2011 Pearson Education11.NPV @ 10% = 10, 000 X 3. 7908 = $37, 908 - $36, 048 = $1, 860 NPV @ 12% =10, 000 X 3. 6048 = $36, 048 - $36, 048 = $0NPV @ 14% = 10, 000 X 3.4331 = $34, 331 - $36, 048 = $(1,717)The IRR is the interest rate at which NPV 二$0; therefore, from requirement 1 we know that IRR 二12%・The NPV at the company? s cost of capital, 10%, is positive, so the project should be accepted・The TRR (12%) is greater than the company' s cost of capital (10%), so the project should be accepted・ Note that the IRR and NPV models give the same decision.2.3.4.min.)Payback period is $36, 000 $10, 000 = 3.6 years・ It is not a good measure of profitabi1ity because it ignores returns beyond the payback period and it does not account for the time value of money.NPV = $5, 114. Accept the proposal because NPV is positive・ Computation: NPV 二($10, 000 X 4. 1114) - $36,000 =$41, 114 一$36, 000 = $ 5, 114 2.3. ARR 二(Increase in average cash f 1 ow - Increase in depreciation)4- Initial investmenl二($10, 000 - $6, 000) 一$36, 000 二11. 1%min.)Salaries $49, 920 (a) $41, 600(b) $ 8,320 Overtime 1, 728(c) — 1,728 Repairs and maintenanee 1,800 1,050 750Toner, supplies, etc. Total annual cash outflows(a) ($ 8 X 40 hrs.) X 52 weeks X 3 employees 二$320 X 52 X 3 =$49,920 (b) ($10 X 40 hrs.) X 52 weeks X 2 employees = $400 X 52 X 2 二$41, 600 (c) ($12 X 4 hrs.) X 12 months X 3 machines =$ 48 X 12 X 3 = $ 1,728Purchase of Cannon machines $ -- $50,000 $50,000Copyright ?2011 Pearson Education2 1.Sale of Xerox machines Training and remodeling Total 一一-3,000-3,000 Copyright ?2011 Pearson Education 3All numbers are expressed in Mexican pesos・ 2. 18% Total Sketch ofRelevant Cash Flows (in thousands) Cash operating savings:* ・847583,902 99,000 10& 900 119, 790 131,769 .4371 144,946 Income tax savings fromdepreciation not changed by inflation, see 1 3.1272 33,600 33, 600 33, 60033,600 33,600 Required outlay at time zero 1.0000 Net present value^Amounts are computed by multiplying (150,000 X .6) = 90, 000 by 1. 10, 1. 102, 1. 10 3, etc.Copyright ?2011 Pearson Education 461PV Present of $1.00 Value ofTOTAL PROJECT APPROACH: Cannon:Init. cash outflow 1.0000 $ (51,000) Oper. cash flows (45,950) (45, 950) (45,950) (45, 950) (45, 950) Total $(216, 641)Xerox:Oper. cash flows 3. 6048 (57, 048) (57, 048) (57, 048) (57, 048) (57, 048)Differenee in favor of retaining XeroxINCREMENTAL APPROACH: Initial investment 1.0000 $(51,000) Annual operatingcash savings 3. 6048 11, 098 11, 098 11, 098 11, 098 11, 098 Net present valueof purchase 2. The Xerox machines should not be replaced by the Cannonequipment. Net savings = (Present value of expenditures to retain Xeroxmachines) 1 ess (Present value of expenditures toconvert to Cannon machines)二$205, 647 - $216,641 二$ (10, 994) 3. a. How flexible is the new machinery? Will it be useful only for the presently intended functions, or can it beeasilyadapted for other tasks that may arise over the next 5 years?b. What psychological effects will it have on various interested parties? Copyright ?2011 Pearson Education。

财务会计英语版课后答案