罗斯公司理财第九版第五章课后答案对应版

第五章:净现值和投资评价的其他方法

1.如果项目会带来常规的现金流,回收期短于项目的生命周期意味着,在折现率为0 的情况下,NPV 为正值。折现率大于0 时,回收期依旧会短于项目的生命周期,但根据折现率小于、等于、大于IRR 的情况,NPV 可能为正、为零、为负。折现回收期包含了相关折现率的影响。如果一个项目的折现回收期短于该项目的生命周期,NPV 一定为正值。

2.如果某项目有常规的现金流,而且NPV 为正,该项目回收期一定短于其生命周期。因为折现回收期是用与NPV 相同的折现值计算出来的,如果NPV为正,折现回收期也会短于该项目的生命周期。NPV 为正表明未来流入现金流大于初始投资成本,盈利指数必然大于1。如果NPV 以特定的折现率R 计算出来为正值时,必然存在一个大于R 的折现率R’使得NPV 为0,因此,IRR 必定大于必要报酬率。

3.(1)回收期法就是简单地计算出一系列现金流的盈亏平衡点。其缺陷是忽略了货币的时间价值,另外,也忽略了回收期以后的现金流量。当某项目的回收期小于该项目的生命周期,则可以接受;反之,则拒绝。回收期法决策作出的选择比较武断。

(2)平均会计收益率为扣除所得税和折旧之后的项目平均收益除以整个项目期限内的平均账面投资额。其最大的缺陷在于没有使用正确的原始材料,其次也没有考虑到时间序列这个因素。一般某项目的平均会计收益率大于公司的目标会计收益率,则可以接受;反之,则拒绝。

(3)内部收益率就是令项目净现值为0 的贴现率。其缺陷在于没有办法对某些项目进行判断,例如有多重内部收益率的项目,而且对于融资型的项目以及投资型的项目判断标准截然相反。对于投资型项目,若IRR 大于贴现率,项目可以接受;反之,则拒绝。对于融资型项目,若IRR 小于贴现率,项目可以接受;反之,则拒绝。

(4)盈利指数是初始以后所有预期未来现金流量的现值和初始投资的比值。必须注意的是,倘若初始投资期之后,在资金使用上还有限制,那盈利指数就会失效。对于独立项目,若PI 大于1,项目可以接受;反之,则拒绝。

(5)净现值就是项目现金流量(包括了最初的投入)的现值,其具有三个特点:①使用现金流量;②包含了项目全部现金流量;③对现金流量进行了合理的折现。某项目NPV 大于0 时,项目可接受;反之,则拒绝。

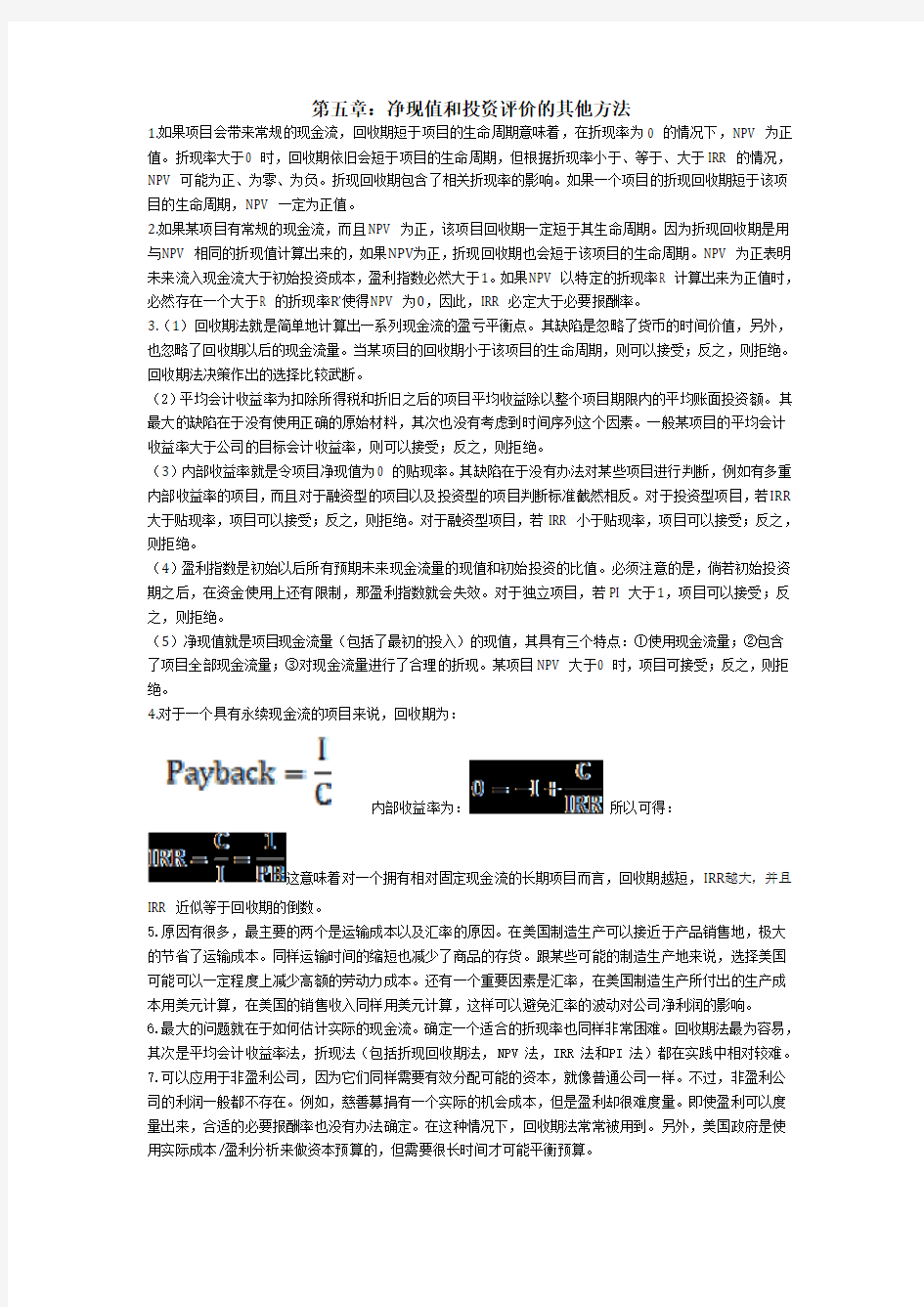

4.对于一个具有永续现金流的项目来说,回收期为:

内部收益率为:所以可得:

这意味着对一个拥有相对固定现金流的长期项目而言,回收期越短,IRR越大,并且IRR 近似等于回收期的倒数。

5.原因有很多,最主要的两个是运输成本以及汇率的原因。在美国制造生产可以接近于产品销售地,极大的节省了运输成本。同样运输时间的缩短也减少了商品的存货。跟某些可能的制造生产地来说,选择美国可能可以一定程度上减少高额的劳动力成本。还有一个重要因素是汇率,在美国制造生产所付出的生产成本用美元计算,在美国的销售收入同样用美元计算,这样可以避免汇率的波动对公司净利润的影响。

6.最大的问题就在于如何估计实际的现金流。确定一个适合的折现率也同样非常困难。回收期法最为容易,其次是平均会计收益率法,折现法(包括折现回收期法,NPV 法,IRR 法和PI 法)都在实践中相对较难。

7.可以应用于非盈利公司,因为它们同样需要有效分配可能的资本,就像普通公司一样。不过,非盈利公司的利润一般都不存在。例如,慈善募捐有一个实际的机会成本,但是盈利却很难度量。即使盈利可以度量出来,合适的必要报酬率也没有办法确定。在这种情况下,回收期法常常被用到。另外,美国政府是使用实际成本/盈利分析来做资本预算的,但需要很长时间才可能平衡预算。

8.这种说法是错误的,如果项目B 的现金流流入的更早,而项目A 的现金流流入较晚,在一个较低的折现率下,A 项目的NPV 将超过B 项目。不过,在项目风险相等的情况下,这种说法是正确的。如果两个项目的生命周期相等,项目B 的现金流在每一期都是项目A 的两倍,则B 项目的NPV 为A项目的两倍。

9.尽管 A 项目的盈利指数低于B 项目,但A 项目具有较高的NPV,所以应该选A 项目。盈利指数判断失误的原因在于B 项目比A 项目需要更少的投资额。只有在资金额受限的情况下,公司的决策才会有误。

10. (1)如果两个项目的现金流均相同,A 项目将有更高的IRR,因为A 项目的初期投资低于项目B。(2)相同,因为项目B 的初始投资额与现金流量都为项目A 的两倍。

11. B 项目将更加敏感。原因在于货币的时间价值。有较长期的未来现金流会对利率的变动更加敏感,这种敏感度类似于债券的利率风险。

12. MIRR 的计算方法是找到所有现金流出的现值以及项目结束后现金流入的未来值,然后计算出两笔现金流的IRR。因此,两笔现金流用同一利率(必要报酬率)折现,因此,MIRR 不是真正的利率。相反,考虑IRR。如果你用初始投资的未来值计算出IRR,就可以复制出项目未来的现金流量。

13. 这种说法是错误的。如果你将项目期末的内部现金流以必要报酬率计算NPV 和初始投资,你将会得到相同的NPV。但是,NPV 并不涉及内部的现金流再投资的问题。

14. 这种说法是不正确的。的确,如果你计算中间的所有现金的未来价值到项目结束流量的回报率,然后计算这个未来的价值和回报率的初步投资,你会得到相同的回报率。然而,正如先前的问题,影响现金流的因素一旦产生不会影响IRR。

15.1. a. The payback period is the time that it takes for the cumulative undiscounted cash inflows to equal the initial investment.

Project A:

Cumulative cash flows Year 1 = $6,500 = $6,500

Cumulative cash flows Year 2 = $6,500 + 4,000 = $10,500

Companies can calculate a more precise value using fractional years. To calculate the fractional payback period, find the fraction of year 2‘s cash flows that is needed for the company to have cumulative undiscounted cash flows of $10,000. Divide the difference between the initial investment and the cumulative undiscounted cash flows as of year 1 by the undiscounted cash flow of year 2. Payback period = 1 + ($10,000 – $6,500) / $4,000 = 1.875 years

Project B:

Cumulative cash flows Year 1 = $7,000 = $7,000

Cumulative cash flows Year 2 = $7,000 + 4,000 = $11,000

Cumulative cash flows Year 3 = $7,000 + 4,000 + 5,000 = $16,000

To calculate the fractional payback period, find the fraction of year 3‘s cash flows that is needed for the company to have cumulative undiscounted cash flows of $12,000. Divide the difference between the initial investment and the cumulative undiscounted cash flows as of year 2 by the undiscounted cash flow of year 3.

Payback period = 2 + ($12,000 – 7,000 – 4,000) / $5,000

Payback period = 2.20 years

Since project A has a shorter payback period than project B has, the company should choose

project A.

b. Discount each project‘s cash flows at 15 percent. Choose the project with the highest NPV. Project A:

NPV = –$10,000 + $6,500 / 1.15 + $4,000 / 1.152 + $1,800 / 1.153= –$139.72

Project B:

NPV = –$12,000 + $7,000 / 1.15 + $4,000 / 1.152 + $5,000 / 1.153= $399.11

The firm should choose Project B since it has a higher NPV than Project A has.

16. When we use discounted payback, we need to find the value of all cash flows today. The value today of the project cash flows for the first four years is:

Value today of Year 1 cash flow = $6,000/1.14 = $5,263.16

Value today of Year 2 cash flow = $6,500/1.142 = $5,001.54

Value today of Year 3 cash flow = $7,000/1.143 = $4,724.80

Value today of Year 4 cash flow = $8,000/1.144 = $4,736.64

To find the discounted payback, we use these values to find the payback period. The discounted first year cash flow is $5,263.16, so the discounted payback for an $8,000 initial cost is: Discounted payback = 1 + ($8,000 – 5,263.16)/$5,001.54 = 1.55 years

For an initial cost of $13,000, the discounted payback is:

Discounted payback = 2 + ($13,000 – 5,263.16 – 5,001.54)/$4,724.80 = 2.58 years

Notice the calculation of discounted payback. We know the payback period is between two and three years, so we subtract the discounted values of the Year 1 and Year 2 cash flows from the initial cost. This is the numerator, which is the discounted amount we still need to make to recover our initial investment. We divide this amount by the discounted amount we will earn in Year 3 to get the fractional portion of the discounted payback.

If the initial cost is $18,000, the discounted payback is:

Discounted payback = 3 + ($18,000 – 5,263.16 – 5,001.54 – 4,724.80) / $4,736.64 = 3.64 years 17. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the equation that defines the IRR for this project is:

0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = –$11,000 + $5,500/(1 + IRR) + $4,000/(1 + IRR)2 + $3,000/(1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 7.46%

Since the IRR is less than the required return we would reject the project.

18. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the equation that defines the IRR for this Project A is:

0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = – $3,500 + $1,800/(1 + IRR) + $2,400/(1 + IRR)2 + $1,900/(1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

IRR = 33.37%

And the IRR for Project B is:

0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = – $2,300 + $900/(1 + IRR) + $1,600/(1 + IRR)2 + $1,400/(1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 29.32%

19.The profitability index is defined as the PV of the cash inflows divided by the PV of the cash outflows. The cash flows from this project are an annuity, so the equation for the profitability index is:

PI = C(PVIFAR,t) / C0 PI = $65,000(PVIFA15%,7) / $190,000 PI = 1.423

20. a. The profitability index is the present value of the future cash flows divided by the initial cost. So, for Project Alpha, the profitability index is:

PIAlpha = [$800 / 1.10 + $900 / 1.102 + $700 / 1.103] / $1,500 = 1.331

And for Project Beta the profitability index is:

PIBeta = [$500 / 1.10 + $1,900 / 1.102 + $2,100 / 1.103] / $2,500 = 1.441

b. According to the profitability index, you would accept Project Beta. However, remember the profitability index rule can lead to an incorrect decision when ranking mutually exclusive projects.

Intermediate

21. a. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the IRR for each project is: Deepwater Fishing IRR:

0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = –$750,000 + $310,000 / (1 + IRR) + $430,000 / (1 + IRR)2 + $330,000 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 19.83%

Submarine Ride IRR:

0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = –$2,100,000 + $1,200,000 / (1 + IRR) + $760,000 / (1 + IRR)2 + $850,000 / (1 + IRR)3 Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 17.36%

Based on the IRR rule, the deepwater fishing project should be chosen because it has the higher IRR.

b. To calculate the incremental IRR, we subtract the smaller project‘s cash flows from the larger project‘s cash flows. In this case, we subtract the deepwater fishing cash flows from the submarine ride cash flows. The incremental IRR is the IRR of these incremental cash flows. So, the incremental cash flows of the submarine ride are:

Year 0 Year 1 Year 2 Year 3

Submarine

–$2,100,000 $1,200,000 $760,000 $850,000

Ride

Deepwater

–750,000 310,000 430,000 330,000

Fishing

–$1,350,000 $890,000 $330,000 $520,000

Submarine –

Fishing

Setting the present value of these incremental cash flows equal to zero, we find the incremental IRR is: 0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = –$1,350,000 + $890,000 / (1 + IRR) + $330,000 / (1 + IRR)2 + $520,000 / (1 + IRR)3 Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: Incremental IRR = 15.78%

For investing-type projects, accept the larger project when the incremental IRR is greater than the discount rate. Since the incremental IRR, 15.78%, is greater than the required rate of return of 14 percent, choose the submarine ride project. Note that this is not the choice when evaluating only the IRR of each project. The IRR decision rule is flawed because there is a scale problem. That is, the submarine ride has a greater initial investment than does the deepwater fishing project. This problem is corrected by calculating the IRR of the incremental cash flows, or by evaluating the NPV of each project.

c. The NPV is the sum of the present value of the cash flows from the project, so the NPV of each

project will be: Deepwater fishing:

NPV = –$750,000 + $310,000 / 1.14 + $430,000 / 1.142 + $330,000 / 1.143 NPV = $75,541.46 Submarine ride:

NPV = –$2,100,000 + $1,200,000 / 1.14 + $760,000 / 1.142 + $850,000 / 1.143 NPV = $111,152.69 Since the NPV of the submarine ride project is greater than the NPV of the deepwater fishing project, choose the submarine ride project. The incremental IRR rule is always consistent with the NPV rule.

22.a. The payback period is the time that it takes for the cumulative undiscounted cash inflows to equal the initial investment.

Board game: Cumulative cash flows Year 1 = $700 = $700

Payback period = $600 / $700 = .86 years

CD-ROM:

Cumulative cash flows Year 1 = $1,400 = $1,400

Cumulative cash flows Year 2 = $1,400 + 900 = $2,300

Payback period = 1 + ($1,900 – 1,400) / $900

Payback period = 1.56 years

Since the board game has a shorter payback period than the CD-ROM project, the company should choose the board game.

b. The NPV is the sum of the present value of the cash flows from the project, so the NPV of each project will be:

Board game: NPV = –$600 + $700 / 1.10 + $150 / 1.102 + $100 / 1.103 NPV = $235.46

CD-ROM: NPV = –$1,900 + $1,400 / 1.10 + $900 / 1.102 + $400 / 1.103 NPV = $417.05

Since the NPV of the CD-ROM is greater than the NPV of the board game, choose the CD-ROM.

c. The IRR is the interest rate that makes the NPV of a project equal to zero. So, the IRR of each project is:

Board game: 0 = –$600 + $700 / (1 + IRR) + $150 / (1 + IRR)2 + $100 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 42.43%

CD-ROM: 0 = –$1,900 + $1,400 / (1 + IRR) + $900 / (1 + IRR)2 + $400 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 25.03%

Since the IRR of the board game is greater than the IRR of the CD-ROM, IRR implies we choose the board game. Note that this is the choice when evaluating only the IRR of each project. The IRR decision rule is flawed because there is a scale problem. That is, the CD-ROM has a greater initial investment than does the board game. This problem is corrected by calculating the IRR of the incremental cash flows, or by evaluating the NPV of each project.

d. To calculate the incremental IRR, we subtract the smaller project‘s cash flows from the larger project‘s cash flows. In this case, we subtract the board game cash flows from the CD-ROM cash flows. The incremental IRR is the IRR of these incremental cash flows. So, the incremental cash flows of the CD-ROM are:

Year 0 Year 1 Year 2 year3

CD-ROM –$1,900 $1,400 $900 $400

Board game –600 700 150 100

CD-ROM – Board –$1,300 $700 $750 $300

game

Setting the present value of these incremental cash flows equal to zero, we find the incremental IRR is: 0 = C0 + C1 / (1 + IRR) + C2 / (1 + IRR)2 + C3 / (1 + IRR)3

0 = –$1,300 + $700 / (1 + IRR) + $750 / (1 + IRR)2 + $300 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: Incremental IRR = 18.78%

23. a. The payback period is the time that it takes for the cumulative undiscounted cash inflows to equal the initial investment.

AZM Mini-SUV: Cumulative cash flows Year 1 = $270,000 = $270,000

Cumulative cash flows Year 2 = $270,000 + 180,000 = $450,000

Payback period = 1+ $30,000 / $180,000 = 1.17 years AZF Full-SUV:

Cumulative cash flows Year 1 = $250,000 = $250,000

Cumulative cash flows Year 2 = $250,000 + 400,000 = $650,000

Payback period = 1+ $350,000 / $400,000 = 1.88 years

Since the AZM has a shorter payback period than the AZF, the company should choose the AZM. Remember the payback period does not necessarily rank projects correctly.

b. The NPV of each project is:

NPVAZM = –$300,000 + $270,000 / 1.10 + $180,000 / 1.102 + $150,000 / 1.103

NPVAZM = $206,912.10

NPVAZF = –$600,000 + $250,000 / 1.10 + $400,000 / 1.102 + $300,000 / 1.103

NPVAZF = $183,245.68

The NPV criteria implies we accept the AZM because it has the highest NPV.

c. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the IRR of the AZM is:

0 = –$300,000 + $270,000 / (1 + IRR) + $180,000 / (1 + IRR)2 + $150,000 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

IRRAZM = 51.43%

And the IRR of the AZF is:

0 = –$600,000 + $250,000 / (1 + IRR) + $400,000 / (1 + IRR)2 + $300,000 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:IRRAZF = 26.04%

The IRR criteria implies we accept the AZM because it has the highest IRR. Remember the IRR does not necessarily rank projects correctly

d. Incremental IRR analysis is not necessary. The AZM has the smallest initial investment, and the largest NPV, so it should be accepted.

24.a. The profitability index is the PV of the future cash flows divided by the initial investment. The profitability index for each project is:

PIA = [$140,000 / 1.12 + $140,000 / 1.122] / $200,000 = 1.18

PIB = [$260,000 / 1.12 + $260,000 / 1.122] / $400,000 = 1.10

PIC = [$150,000 / 1.12 + $120,000 / 1.122] / $200,000 = 1.15

b. The NPV of each project is:

NPVA = –$200,000 + $140,000 / 1.12 + $140,000 / 1.122 NPVA = $36,607.14

NPVB = –$400,000 + $260,000 / 1.12 + $260,000 / 1.122 NPVB = $39,413.27

NPVC = –$200,000 + $150,000 / 1.12 + $120,000 / 1.122 NPVC = $29,591.84

c. Accept projects A, B, and C. Since the projects are independent, accept all three projects because the respective profitability index of each is greater than one.

d. Accept Project B. Since the Projects are mutually exclusive, choose the Project with the highest PI, while taking into account the scale of the Project. Because Projects A and C have the same initial investment, the problem of scale does not arise when comparing the profitability indices. Based on the profitability index rule, Project C can be eliminated because its PI is less than the PI of Project A. Because of the problem of scale, we cannot compare the PIs of Projects A and B. However, we can calculate the PI of the incremental cash flows of the two projects, which are:

Project C0 C1 C2

B – A –$200,000 $120,000 $120,000

When calculating incremental cash flows, remember to subtract the cash flows of the project with the smaller initial cash outflow from those of the project with the larger initial cash outflow. This procedure insures that the incremental initial cash outflow will be negative. The incremental PI calculation is:

PI(B – A) = [$120,000 / 1.12 + $120,000 / 1.12⌒2] / $200,000 = 1.014

The company should accept Project B since the PI of the incremental cash flows is greater than one.

e. Remember that the NPV is additive across projects. Since we can spend $600,000, we could take two of the projects. In this case, we should take the two projects with the highest NPVs, which are Project B and Project A.

25. a. The payback period is the time that it takes for the cumulative undiscounted cash inflows to equal the initial investment.

Project A:

Cumulative cash flows Year 1 = $190,000 = $190,000

Cumulative cash flows Year 2 = $190,000 + 170,000 = $360,000

Payback period = 1 + ($90,000/$170,000) = 1.53 years

Project B:

Cumulative cash flows Year 1 = $270,000 = $270,000

Cumulative cash flows Year 2 = $270,000 + 240,000 = $510,000

Payback period = 1 + ($120,000/$240,000) = 1.50 years

Project C:

Cumulative cash flows Year 1 = $160,000 = $160,000

Cumulative cash flows Year 2 = $160,000 + 190,000 = $350,000

Payback period = 1 + ($70,000/$190,000) = 1.37 years

Project C has the shortest payback period, so payback implies accepting Project C. However, the payback period does not necessarily rank projects correctly.

b. The IRR is the interest rate that makes the NPV of the project equal to zero, so the IRR of each project is:

Project A: 0 = –$280,000 + $190,000 / (1 + IRR) + $170,000 / (1 + IRR)⌒2

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRRA = 18.91%

And the IRR of the Project B is:

0 = –$390,000 + $270,000 / (1 + IRR) + $240,000 / (1 + IRR)2

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRRB = 20.36%

And the IRR of the Project C is:

0 = –$230,000 + $160,000 / (1 + IRR) + $190,000 / (1 + IRR)2

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRRC = 32.10%

The IRR criteria implies accepting Project C.

c. The profitability index is the present value of all subsequent cash flows, divided by the initial investment. We need to discount the cash flows of each project by the required return of each project. The profitability index of each project is:

PIA = [$190,000 / 1.10 + $170,000 / 1.10⌒2] / $280,000 PIA = 1.12

PIB = [$270,000 / 1.20 + $240,000 / 1.20⌒2] / $390,000 PIB = 1.00

PIC = [$160,000 / 1.15 + $190,000 / 1.15⌒2] / $230,000 PIC = 1.23

The PI criteria implies accepting Project C.

d. We need to discount the cash flows of each project by the required return of each project. The NPV of each project is:

NPVA = –$280,000 + $190,000 / 1.10 + $170,000 / 1.10⌒2 NPVA = $33,223.14

NPVB = –$390,000 + $270,000 / 1.20 + $240,000 / 1.20⌒2 NPVB = $1,666.67

NPVC = –$230,000 + $160,000 / 1.15 + $190,000 / 1.15⌒2 NPVC = $52,797.73

The NPV criteria implies accepting Project C. In the final analysis, since we can accept only one of these projects. We should accept Project C since it has the greatest NPV.

26. The equation for the IRR of the project is:

0 =–$504 + $2,862/(1 + IRR) – $6,070/(1 + IRR)⌒2 + $5,700/(1 + IRR)⌒3 – $2,000/(1 + IRR)⌒4 Using Descartes rule of signs, from looking at the cash flows we know there are four IRRs for this project. Even with most computer spreadsheets, we have to do some trial and error. From trial and error, IRRs of 25%, 33.33%, 42.86%, and 66.67% are found.

We would accept the project when the NPV is greater than zero. See for yourself that the NPV is greater than zero for required returns between 25% and 33.33% or between 42.86% and 66.67%. 27. a. The project involves three cash flows: the initial investment, the annual cash inflows, and the abandonment costs. The mine will generate cash inflows over its 11-year economic life. To express the PV of the annual cash inflows, apply the growing annuity formula, discounted at the IRR and growing at eight percent.

PV(Cash Inflows) = C {[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]⌒t}

PV(Cash Inflows) = $175,000{[1/(IRR – .08)] – [1/(IRR – .08)] × [(1 + .08)/(1 + IRR)]⌒11} At the end of 11 years, the Utah Mining Corporate will abandon the mine, incurring a $125,000 charge. Discounting the abandonment costs back 11 years at the IRR to express its present value, we get: PV(Abandonment) = C11 / (1 + IRR)⌒11

PV(Abandonment) = –$125,000 / (1+ IRR)⌒11

So, the IRR equation for this project is:

0 = –$900,000 + $175,000{[1/(IRR – .08)] – [1/(IRR – .08)] × [(1 + .08)/(1 + IRR)]⌒11}

–$125,000 / (1+ IRR)⌒11

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that: IRR = 22.26%

b. Yes. Since the mine‘s IRR exceeds the required return of 10 percent, the mine should be opened. The correct decision rule for an investment-type project is to accept the project if the discount rate is above the IRR. Although it appears there is a sign change at the end of the project because of the abandonment costs, the last cash flow is actually positive because of the operating cash in the last year.

28.To answer this question, we need to examine the incremental cash flows. To make the projects equally attractive, Project Billion must have a larger initial investment. We know this because the subsequent cash flows from Project Billion are larger than the subsequent cash flows from Project Million. So, subtracting the Project Million cash flows from the Project Billion cash flows, we find the incremental cash flows are:

Incremental

Year cash flows

0 –Io + $1,200

1 240

2 240

3 400

Now we can find the present value of the subsequent incremental cash flows at the discount rate, 12 percent. The present value of the incremental cash flows is:

PV = $1,200 + $240 / 1.12 + $240 / 1.122 + $400 / 1.123

PV = $1,890.32

So, if I0 is greater than $1,890.32, the incremental cash flows will be negative. Since we are subtracting Project Million from Project Billion, this implies that for any value over $1,890.32 the NPV of Project Billion will be less than that of Project Million, so I0 must be less than $1,890.32.

公司理财罗斯第九版课后习题答案

罗斯《公司理财》第9版精要版英文原书课后部分章节答案详细? 1 / 17 CH5 11,13,18,19,20 11. To find the PV of a lump sum, we use: PV = FV / (1 + r) t PV = $1,000,000 / (1.10) 80 = $488.19 13. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for r, we get: r = (FV / PV) 1 / t –1 r = ($1,260,000 / $150) 1/11 2 – 1 = .0840 or 8.40% To find the FV of the first prize, we use: FV = PV(1 + r) t FV = $1,260,000(1.0840) 3 3 = $18,056,409.9 4 18. To find the FV of a lump sum, we use: FV = PV(1 + r) t FV = $4,000(1.11) 4 5 = $438,120.97 FV = $4,000(1.11) 35 = $154,299.40 Better start early! 19. We need to find the FV of a lump sum. However, the money will only be invested for six years, so the number of periods is six. FV = PV(1 + r) t FV = $20,000(1.084) 6 = $32,449.33 20. To answer this question, we can use either the FV or the PV formula. Both will give the same answer since they are the inverse of each other. We will use the FV formula, that is: FV = PV(1 + r) t Solving for t, we get: t = ln(FV / PV) / ln(1 + r) t = ln($75,000 / $10,000) / ln(1.11) = 19.31 So, the money must be invested for 19.31 years. However, you will not receive the money for another two years. From now, you’ll wait: 2 years + 19.31 years = 21.31 years CH6 16,24,27,42,58 16. For this problem, we simply need to find the FV of a lump sum using the equation: FV = PV(1 + r) t 2 / 1 7 It is important to note that compounding occurs semiannually. To account for this, we will divide the interest rate by two (the number of compounding periods in a year), and multiply the number of periods by two. Doing so, we get: FV = $2,100[1 + (.084/2)] 34 = $8,505.93 24. This problem requires us to find the FVA. The equation to find the FVA is: FV A = C{[(1 + r) t – 1] / r} FV A = $300[{[1 + (.10/12) ] 360 – 1} / (.10/12)] = $678,146.3 8 27. The cash flows are annual and the compounding period is quarterly, so we need to calculate the EAR to make the interest rate comparable with the timing of the cash flows. Using the equation for the EAR, we get: EAR = [1 + (APR / m)] m – 1 EAR = [1 + (.11/4)] 4 – 1 = .1146 or 11.46% And now we use the EAR to find the PV of each cash flow as a lump sum and add them together: PV = $725 / 1.1146 + $980 / 1.1146 2 + $1,360 / 1.1146 4 = $2,320.36 42. The amount of principal paid on the loan is the PV of the monthly payments you make. So, the present value of the $1,150 monthly payments is: PVA = $1,150[(1 – {1 / [1 + (.0635/12)]} 360 ) / (.0635/12)] = $184,817.42 The monthly payments of $1,150 will amount to a principal payment of $184,817.42. The amount of principal you will still owe is: $240,000 – 184,817.42 = $55,182.58 This remaining principal amount will increase at the interest rate on the loan until the end of the loan period. So the balloon payment in 30 years, which is the FV of the remaining principal will be: Balloon payment = $55,182.58[1 + (.0635/12)] 360 = $368,936.54 58. To answer this question, we should find the PV of both options, and compare them. Since we are purchasing the car, the lowest PV is the best option. The PV of the leasing is simply the PV of the lease payments, plus the $99. The interest rate we would use for the leasing option is the same as the interest rate of the loan. The PV of leasing is: PV = $9 9 + $450{1 –[1 / (1 + .07/12) 12(3) ]} / (.07/12) = $14,672.91 The PV of purchasing the car is the current price of the car minus the PV of the resale price. The PV of the resale price is : PV = $23,000 / [1 + (.07/12)] 12(3) = $18,654.82 The PV of the decision to purchase is: $32,000 – 18,654.82 = $13,345.18 3 / 17 In this case, it is cheaper to buy the car than leasing it since the PV of the purchase cash flows is lower. To find the breakeven resale price, we need to find the resale price that makes the PV of the two options the same. In other words, the PV of the decision to buy should be: $32,000 – PV of resale price = $14,672.91 PV of resale price = $17,327.09 The resale price that would make the PV of the lease versus buy decision is the FV of

Cha04 罗斯公司理财第九版原版书课后习题

The present value of the four new outlets is only $954,316.78. The outlets are worth less than they cost. The Trojan Pizza Company should not make the investment because the NPV is –$45,683.22. If the Trojan Pizza Company requires a 15 percent rate of return, the new outlets are not a good investment. SPREADSHEET APPLICATIONS How to Calculate Present Values with Multiple Future Cash Flows Using a Spreadsheet We can set up a basic spreadsheet to calculate the present values of the individual cash flows as follows. Notice that we have simply calculated the present values one at a time and added them up: Summary and Conclusions 1. Two basic concepts, future value and present value, were introduced in the beginning of this chapter. With a 10 percent interest rate, an investor with $1 today can generate a future value of $1.10 in a year, $1.21 [=$1 × (1.10)2] in two years, and so on. Conversely, present value analysis places a current value on a future cash flow. With the same 10 percent interest rate, a dollar to be received in one year has a present value of $.909 (=$1/1.10) in year 0. A dollar to be received in two years has a present value of $.826 [=$1/(1.10)2]. 2. We commonly express an interest rate as, say, 12 percent per year. However, we can speak of the interest rate as 3 percent per quarter. Although the stated annual interest rate remains 12 percent (=3 percent × 4), the effective annual interest rate is 12.55 percent [=(1.03)4 – 1]. In other words, the compounding process increases the future value of an investment. The limiting case is continuous compounding, where funds are assumed to be reinvested every infinitesimal instant.

罗斯公司理财第九版第十章课后答案对应版

第十章:风险与收益:市场历史的启示 1. 因为公司的表现具有不可预见性。 2. 投资者很容易看到最坏的投资结果,但是确很难预测到。 3. 不是,股票具有更高的风险,一些投资者属于风险规避者,他们认为这点额外的报酬率还不至于吸引他们付出更高风险的代价。 4. 股票市场与赌博是不同的,它实际是个零和市场,所有人都可能赢。而且投机者带给市场更高的流动性,有利于市场效率。 5. 在80 年代初是最高的,因为伴随着高通胀和费雪效应。 6. 有可能,当投资风险资产报酬非常低,而无风险资产报酬非常高,或者同时出现这两种现象时就会发生这样的情况。 7. 相同,假设两公司2 年前股票价格都为P0,则两年后G 公司股票价格为 1.1*0.9* P0,而S 公司股票价格为0.9*1.1 P0,所以两个公司两年后的股价是一样的。 8. 不相同,Lake Minerals 2年后股票价格= 100(1.10)(1.10) = $121.00 而SmallTown Furniture 2年后股票价格= 100(1.25)(.95) = $118.75 9. 算数平均收益率仅仅是对所有收益率简单加总平均,它没有考虑到所有收益率组合的效果,而几何平均收益率考虑到了收益率组合的效果,所以后者比较重要。 10. 不管是否考虑通货膨胀因素,其风险溢价没有变化,因为风险溢价是风险资产收益率与无风险资产收益率的差额,若这两者都考虑到通货膨胀的因素,其差额仍然是相互抵消的。而在考虑税收后收益率就会降低,因为税后收益会降低。 11. R = [($104 – 92) + 1.45] / $92 = .1462 or 14.62% 12. Dividend yield = $1.45 / $92 = .0158 or 1.58% Capital gains yield = ($104 – 92) / $92 = .1304 or 13.04% 13. R = [($81 – 92) + 1.45] / $92 = –.1038 or –10.38% Dividend yield = $1.45 / $92 = .0158 or 1.58% Capital gains yield = ($81 – 92) / $92 = –.1196 or –11.96% 14.

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解](风险、资本成本和资本预算)【圣才

罗斯《公司理财》第9版笔记和课后习题(含考研真题)详解[视频详解] 第13章风险、资本成本和资本预算[视频讲解] 13.1复习笔记 运用净现值法,按无风险利率对现金流量折现,可以准确评价无风险现金流量。然而,现实中的绝大多数未来现金流是有风险的,这就要求有一种能对有风险现金流进行折现的方法。确定风险项目净现值所用的折现率可根据资本资产定价模型CAPM(或套利模型APT)来计算。如果某无负债企业要评价一个有风险项目,可以运用证券市场线SML来确定项目所要求的收益率r s,r s也称为权益资本成本。 当企业既有债务融资又有权益融资时,所用的折现率应是项目的综合资本成本,即债务资本成本和权益资本成本的加权平均。 联系企业的风险贴现率与资本市场要求的收益率的原理在于如下一个简单资本预算原则:企业多余的现金,可以立即派发股利,投资者收到股利自己进行投资,也可以用于投资项目产生未来的现金流发放股利。从股东利益出发,股东会在自己投资和企业投资中选择期望收益率较高的一个。只有当项目的期望收益率大于风险水平相当的金融资产的期望收益率时,项目才可行。因此项目的折现率应该等于同样风险水平的金融资产的期望收益率。这也说明了资本市场价格信号作用。 1.权益资本成本 从企业的角度来看,权益资本成本就是其期望收益率,若用CAPM模型,股票的期望收益率为:

其中,R F是无风险利率,是市场组合的期望收益率与无风险利率之差,也称为期望超额市场收益率或市场风险溢价。 要估计企业权益资本成本,需要知道以下三个变量:①无风险利率;②市场风险溢价; ③公司的贝塔系数。 根据权益资本成本计算企业项目的贴现率需要有两个重要假设:①新项目的贝塔风险与企业风险相同;②企业无债务融资。 2.贝塔的估计 估算公司贝塔值的基本方法是利用T个观测值按照如下公式估计: 估算贝塔值可能存在以下问题:①贝塔可能随时间的推移而发生变化;②样本容量可能太小;③贝塔受财务杠杆和经营风险变化的影响。 可以通过如下途径解决上述问题:①第1个和第2个问题可通过采用更加复杂的统计技术加以解决;②根据财务风险和经营风险的变化对贝塔作相应的调整,有助于解决第3个问题;③注意同行业类似企业的平均β估计值。 根据企业自身历史数据来估算企业贝塔系数是一种常用方法,也有人认为运用整个行业的贝塔系数可以更好地估算企业的贝塔系数。有时两者计算的结果差异很大。总的来说,可以遵循下列原则:如果认为企业的经营与所在行业其他企业的经营十分类似,用行业贝塔降低估计误差。如果认为企业的经营与行业内其他企业的经营有着根本性差别,则应选择企业的贝塔。 3.贝塔的确定 前面介绍的回归分析方法估算贝塔并未阐明贝塔是由哪些因素决定的。主要存在以下三个因素:收入的周期性、经营杠杆和财务杠杆。

公司理财课后习题答案

《公司理财》考试范围:第3~7章,第13章,第16~19章,其中第16章和18章为较重点章节。书上例题比较重要,大家记得多多动手练练。PS:书中课后例题不出,大家可以当习题练练~ 考试题型:1.单选题10分 2.判断题10分 3.证明题10分 4.计算分析题60分 5.论述题10分 注:第13章没有答案 第一章 1.在所有权形式的公司中,股东是公司的所有者。股东选举公司的董事会,董事会任命该公司的管理层。企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。在这种环境下,他们可能因为目标不一致而存在代理问题。 2.非营利公司经常追求社会或政治任务等各种目标。非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。 3.这句话是不正确的。管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。 4.有两种结论。一种极端,在市场经济中所有的东西都被定价。因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。然而,该公司认为提高产品的安全性只会节省20美元万。请问公司应该怎么做呢?” 5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。 6.管理层的目标是最大化股东现有股票的每股价值。如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。 7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。较少的私人投资者能减少不同的企业目标。高比重的机构所有权导致高学历的股东和管理层讨论

第九版 公司理财 罗斯 中文答案 第四章

1、FV=PV*(1+R)^T,PV= FV/(1+R)^T,所以时间长度增加时,终值会 增加,现值会减少。 2、FV=PV*(1+R)^T,PV= FV/(1+R)^T,利率增加时,年金的终值会增 加,现值会减少。 3、第一种情况:PV=C*{[1-1/(1+r)^T]/r}=1000*{[1-1/(1+r)^10]/r} 第二种情况:PV=C*{[1-(1+g)^T/(1+r)^T]/(r-g)}= 1000*{[1-(1+5%)^10/(1+r)^10]/(r-5%)} 1000*{[1-1/(1+r)^10]/r}>1000*{[1-(1+5%)^10/(1+r)^10]/(r-5%)} 所以第一种情况分十次等分支付更好。 4、是,因为名义利率通常不提供相关利率。唯一的优势就是方便 计算,但是随着现在计算机设备的发展,这种优势已经不明显。 5、新生将收到更多的津贴。因为新生到偿还贷款的时间较长。 6、因为货币具有时间价值。GMAC当期获得五百美元的使用权, 如果投资得当,三十年后的收益将会高于一千美元。 7、除非出现通货紧缩,资金成本成为负值,否则GMAC有权利在 任意时候以10000美元的价格赎回该债券,都会增加投资者的持有该债券的意愿。 8、我不愿意今天支付五百美元来换取三十年后的一万美元。关键 因素:一是同类投资相比的回报率是否较高,二是投资的回报率和风险是否相匹配。回答取决于承诺偿还人,因为必须评估其三十年后存续的风险。 9、财政部的债券价格应该更高,因为财政部发行债券是以国家信

用为担保,违约风险最小,基本可视为无风险债券。 10、应该超过。因为货币具有时间价值,债券的价格会随着时间的 发展逐渐上升,最终达到一万美元。所以2010年,债券的价格 应该会更高。但是这具有很大的不确定性,因为宏观经济环境 和公司微观环境会发生变化,都有可能造成债券价格发生变化。 11、 a 1000*(1+6%)^10=1791美元 b 1000*(1+9%)^10=1967美元 c 1000*(1+6%)^20=3207美元 d 因为在按照复利计算时,不仅本金会产生利息,本金的利息 也会产生利息。 12、PV=FV/(1+r)^t=7.5/(1+8.2%)^20=1.55亿美元 13、PV=C/r=120/5.7%=2105美元 14、FV=C*e^(rT) a FV=1900*e^(12%*5)=1900*1.8221=3462美元 b FV=1900*e^(10%*3)=1900*1.3499=2565美元 c FV=1900*e^(5%*10)=1900*1.6487=3133美元 d FV=1900*e^(7%*8)=1900*1.7507=3326美元 15、有限年限支付下PV= C*{[1-1/(1+r)^T]/r} 当T=15时, PV=4300*{[1-1/(1+9%)^15]/9%}=4300*8.0607=34661美元 当T=40时, PV=4300*{[1-1/(1+9%)^40]/9%}=4300*10.7574=46257美元

公司理财部分课后答案演示教学

Chapter 1 Goal OF Firm N0.2, 3, 4, 5, 10. 2. Not-for-Profit Firm Goals Suppose you were the financial manager of a not-for-profit business (a not-for-profit hospital, perhaps). What kinds of goals do you think would be appropriate? 答:所有者权益的市场价值的最大化。 3.Goal of the Firm Evaluate the following statement: Managers should not focus on the current stock value because doing so will lead to an overemphasis on short-term profits at the expense of long-term profits. 答:错误;因为现在的股票价值已经反应了短期和长期的的风险、时间以及未来现金流量。 4. Ethics and Firm Goals Can the goal of maximizing the value of the stock conflict with other goals, such as avoiding unethical or illegal behavior? In particular, do you think subjects like customer and employee safety, the environment, and the general good of society fit in this framework, or are they essentially ignored? Think of some specific scenarios to illustrate your answer. 答:有两种极端。一种极端,所有的东西都被定价。因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。 一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30万美元。然而,该公司认为提高产品的安全性只会节省20万美元。请问公司应该怎么做呢?” 5.International Firm Goal Would the goal of maximizing the value of the stock differ for financial management in a foreign country? Why or why not? 答:财务管理的目标都是相同的,但实现目标的最好方式可能是不同的(因为不同的国家有不同的社会、政治环境和经济制度) 10. Goal of Financial Management Why is the goal of financial management to maximize the current value of the company’s stock? In other words, why isn’t the goal to maximize the future value? 答:最大化现在公司股票的价格和最大化未来股票价格是一样的。股票的价值取决于公司未来所有的现金流量。从另一方面来看,支付大量的现金股利给股东,股票的预期价格将会上升。 Chapter 2 1. Building a Balance Sheet Sankey, Inc., has current assets of $4,900, net fixed assets of $25,000, current liabilities of $4,100, and long-term debt of $10,300. What is the value of the shareholders’ equity account for this firm? How much is net working capital?

Cha07 罗斯公司理财第九版原版书课后习题

to abandon, and timing options. 4. Decision trees represent an approach for valuing projects with these hidden, or real, options. Concept Questions 1. Forecasting Risk What is forecasting risk? In general, would the degree of forecasting risk be greater for a new product or a cost-cutting proposal? Why? 2. Sensitivity Analysis and Scenario Analysis What is the essential difference between sensitivity analysis and scenario analysis? 3. Marginal Cash Flows A coworker claims that looking at all this marginal this and incremental that is just a bunch of nonsense, and states, “Listen, if our average revenue doesn’t exceed our average cost, then we will have a negative cash flow, and we will go broke!” How do you respond? 4. Break-Even Point As a shareholder of a firm that is contemplating a new project, would you be more concerned with the accounting break-even point, the cash break-even point (the point at which operating cash flow is zero), or the financial break-even point? Why? 5. Break-Even Point Assume a firm is considering a new project that requires an initial investment and has equal sales and costs over its life. Will the project reach the accounting, cash, or financial break-even point first? Which will it reach next? Last? Will this order always apply? 6. Real Options Why does traditional NPV analysis tend to underestimate the true value of a capital budgeting project? 7. Real Options The Mango Republic has just liberalized its markets and is now permitting foreign investors. Tesla Manufacturing has analyzed starting a project in the country and has determined that the project has a negative NPV. Why might the company go ahead with the project? What type of option is most likely to add value to this project? 8. Sensitivity Analysis and Breakeven How does sensitivity analysis interact with break-even analysis? 9. Option to Wait An option can often have more than one source of value. Consider a logging company. The company can log the timber today or wait another year (or more) to log the timber. What advantages would waiting one year potentially have? 10. Project Analysis You are discussing a project analysis with a coworker. The project involves real options, such as expanding the project if successful, or abandoning the project if it fails. Your coworker makes the following statement: “This analysis is ridiculous. We looked at expanding or abandoning the project in two years, but there are many other options we should consider. For example, we could expand in one year, and expand further in two years. Or we could expand in one year, and abandon the project in two years. There are too many options for us to examine. Because of this, anything this analysis would give us is worthless.” How would you evaluate this statement? Considering that with any capital budgeting project there are an infinite number of real options, when do you stop the option analysis on an individual project? Questions and Problems: connect? BASIC (Questions 1–10) 1. Sensitivity Analysis and Break-Even Point We are evaluating a project that costs $724,000, has an eight-year life, and has no salvage value. Assume that depreciation is straight-line to zero over the life of the project. Sales are projected at 75,000 units per year. Price per unit is $39, variable cost per unit is $23, and fixed costs are $850,000 per year. The tax rate is 35 percent, and we require a 15 percent return on this project. 1. Calculate the accounting break-even point.

罗斯公司理财第九版第六章课后答案对应版

第六章:投资决策 1.机会成本是指进行一项投资时放弃另一项投资所承担的成本。选择投资和放弃投资之间的收益差是可能获取收益的成本。 2. (1)新的投资项目所来的公司其他产品的销售下滑属于副效应中的侵蚀效应,应被归为增量现金流。 (2)投入建造的机器和厂房属于新生产线的成本,应被归为增量现金流。(3)过去3 年发生的和新项目相关的研发费用属于沉没成本,不应被归为增量现金流。 (4)尽管折旧不是现金支出,对现金流量产生直接影响,但它会减少公司的净收入,并且减低公司的税收,因此应被归为增量现金流。 (5)公司发不发放股利与投不投资某一项目的决定无关,因此不应被归为增量现金流。 (6)厂房和机器设备的销售收入是一笔现金流入,因此应被归为增量现金流。(7)需要支付的员工薪水与医疗保险费用应被包括在项目成本里,因此应被归为增量现金流。 3. 第一项因为会产生机会成本,所以会产生增量现金流;第二项因为会产生副效应中的侵蚀效应,所以会会产生增量现金流;第三项属于沉没成本,不会 产生增量现金流。 4. 为了避免税收,公司可能会选择MACRS,因为该折旧法在早期有更大的折旧额,这样可以减免赋税,并且没有任何现金流方面的影响。但需要注意的是直线折旧法与MACRS 的选择只是时间价值的问题,两者的折旧是相等的,只是时间不同。 5. 这只是一个简单的假设。因为流动负债可以全部付清,流动资产却不可能全部以现金支付,存货也不可能全部售完。 6. 这个说法是可以接受的。因为某一个项目可以用权益来融资,另一个项目可以用债务来融资,而公司的总资本结构不会发生变化。根据MM 定理,融资成本与项目的增量现金流量分析无关。 7. ECA 方法在分析具有不同生命周期的互斥项目的情况下比较适应,这是因为ECA 方法可以使得互斥项目具有相同的生命周期,这样就可以进行比较。ECA 方法在假设项目现金流相同这一点与现实生活不符,它忽略了通货膨胀率以及不断变更的经济环境。 8. 折旧是非付现费用,但它可以在收入项目中减免赋税,这样折旧将使得实际现金流出的赋税减少一定额度,并以此影响项目现金流,因此,折旧减免赋税的效应应该被归为总的增量税后现金流。 9. 应考虑两个方面:第一个是侵蚀效应,新书是否会使得现有的教材销售额下降?第二个是竞争,是否其他出版商会进入市场并出版类似书籍?如果是的话,侵蚀效应将会降低。出版商的主要需要考虑出版新书带来的协同效应是否大于侵蚀效应,如果大于,则应该出版新书,反之,则放弃。 10. 当然应该考虑,是否会对保时捷的品牌效应产生破坏是公司应该考虑到的。如果品牌效应被破坏,汽车销量将受到一定影响。 11. 保时捷可能有更低的边际成本或是好的市场营销。当然,也有可能是一个决策失误。 12. 保时捷将会意识到随着越来越多产品投入市场,竞争越来越激烈,过高的利润会减少。

(完整版)公司理财习题及答案

习题一 1.5.1单项选择题 1 .不能偿还到期债务是威胁企业生存的()。 A .外在原因 B .内在原因 C .直接原因 D .间接原因 2.下列属于有关竞争环境的原则的是()。 A .净增效益原则 B .比较优势原则 C .期权原则 D .自利行为原则3.属于信号传递原则进一步运用的原则是指() A .自利行为原则 B .比较优势原则 C . 引导原则 D .期权原则 4 .从公司当局可控因素来看,影响报酬率和风险的财务活动是()。 A .筹资活动 B .投资活动 C .营运活动 D .分配活动 5 .自利行为原则的依据是()。 A .理性的经济人假设 B .商业交易至少有两方、交易是“零和博弈”,以及各方都是自利的 C .分工理论 D .投资组合理论 6 .下列关于“有价值创意原则”的表述中,错误的是()。 A .任何一项创新的优势都是暂时的 B .新的创意可能会减少现有项目的价值或者使它变得毫无意义 C .金融资产投资活动是“有价值创意原则”的主要应用领域 D .成功的筹资很少能使企业取得非凡的获利能力 7 .通货膨胀时期,企业应优先考虑的资金来源是() A .长期负债 B .流动负债 C .发行新股 D .留存收益 8.股东和经营者发生冲突的根本原因在于()。 A .具体行为目标不一致 B .掌握的信息不一致 C .利益动机不同 D ,在企业中的地位不同 9 .双方交易原则没有提到的是()。 A .每一笔交易都至少存在两方,双方都会遵循自利行为原则 B .在财务决策时要正确预见对方的反映 C .在财务交易时要考虑税收的影响 D .在财务交易时要以“自我为中心” 10.企业价值最大化目标强调的是企业的()。 A .预计获利能力 B .现有生产能力 C .潜在销售能力 D .实际获利能力11.债权人为了防止其利益受伤害,通常采取的措施不包括()。 A .寻求立法保护 B .规定资金的用途 C .提前收回借款 D .不允许发行新股12.理性的投资者应以公司的行为作为判断未来收益状况的依据是基于()的要求。 A .资本市场有效原则 B .比较优势原则 C .信号传递原则 D .引导原则13.以每股收益最大化作为财务管理目标,存在的缺陷是()。 A .不能反映资本的获利水平 B .不能用于不同资本规模的企业间比较 C .不能用于同一企业的不同期间比较 D .没有考虑风险因素和时间价值 14 .以下不属于创造价值原则的是()。 A .净增效益原则 B .比较优势原则 C .期权原则 D .风险—报酬权衡原则 15. 利率=()+通货膨胀附加率+变现力附加率+违约风险附加率+到期风险附加率。 A .物价指数附加率 B .纯粹利率 C .风险附加率 D .政策变动风险 1.5.2多项选择题

Cha02 罗斯公司理财第九版原版书课后习题

reported in the financing activity section of the accounting statement of cash flows. When Tyco received payments from customers, the cash inflows were reported as operating cash flows. Another method used by Tyco was to have acquired companies prepay operating expenses. In other words, the company acquired by Tyco would pay vendors for items not yet received. In one case, the payments totaled more than $50 million. When the acquired company was consolidated with Tyco, the prepayments reduced Tyco’s cash outflows, thus increasing the operating cash flows. Dynegy, the energy giant, was accused of engaging in a number of complex “round-trip trades.” The round-trip trades essentially involved the sale of natural resources to a counterparty, with the repurchase of the resources from the same party at the same price. In essence, Dynegy would sell an asset for $100, and immediately repurchase it from the buyer for $100. The problem arose with the treatment of the cash flows from the sale. Dynegy treated the cash from the sale of the asset as an operating cash flow, but classified the repurchase as an investing cash outflow. The total cash flows of the contracts traded by Dynegy in these round-trip trades totaled $300 million. Adelphia Communications was another company that apparently manipulated cash flows. In Adelphia’s case, the company capitalized the labor required to install cable. In other words, the company classified this labor expense as a fixed asset. While this practice is fairly common in the telecommunications industry, Adelphia capitalized a higher percentage of labor than is common. The effect of this classification was that the labor was treated as an investment cash flow, which increased the operating cash flow. In each of these examples, the companies were trying to boost operating cash flows by shifting cash flows to a different heading. The important thing to notice is that these movements don’t affect the total cash flow of the firm, which is why we recommend focusing on this number, not just operating cash flow. Summary and Conclusions Besides introducing you to corporate accounting, the purpose of this chapter has been to teach you how to determine cash flow from the accounting statements of a typical company. 1. Cash flow is generated by the firm and paid to creditors and shareholders. It can be classified as: 1. Cash flow from operations. 2. Cash flow from changes in fixed assets. 3. Cash flow from changes in working capital. 2. Calculations of cash flow are not difficult, but they require care and particular attention to detail in properly accounting for noncash expenses such as depreciation and deferred taxes. It is especially important that you do not confuse cash flow with changes in net working capital and net income. Concept Questions 1. Liquidity True or false: All assets are liquid at some price. Explain. 2. Accounting and Cash Flows Why might the revenue and cost figures shown on a standard income statement not represent the actual cash inflows and outflows that occurred during a period? 3. Accounting Statement of Cash Flows Looking at the accounting statement of cash flows, what does the bottom line number mean? How useful is this number for analyzing a company? 4. Cash Flows How do financial cash flows and the accounting statement of cash flows differ? Which is more useful for analyzing a company? 5. Book Values versus Market Values Under standard accounting rules, it is possible for a