高盛投行估值财务模型

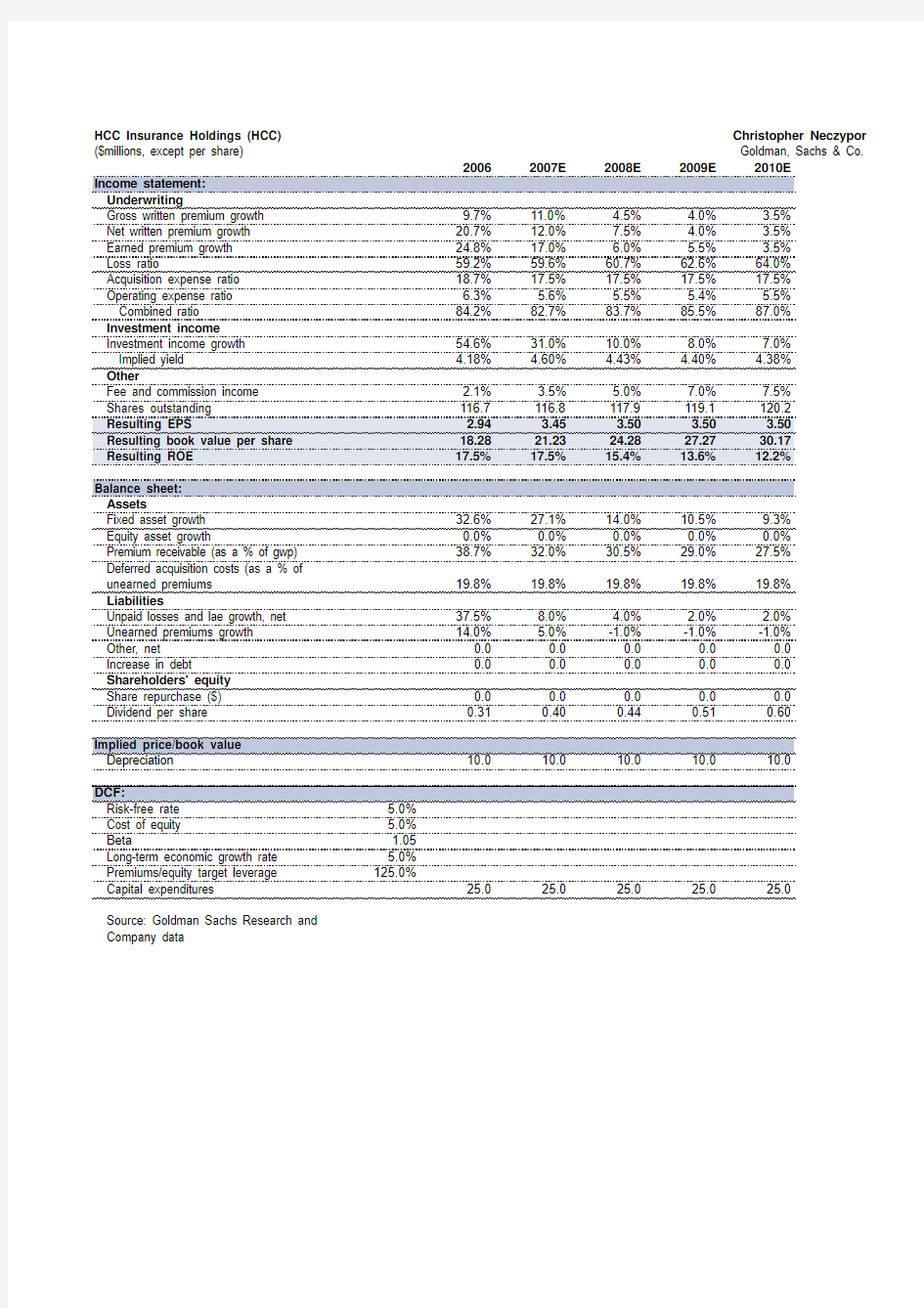

HCC Insurance Holdings (HCC)Christopher Neczypor ($millions, except per share)Goldman, Sachs & Co.

Gross written premium growth9.7%11.0% 4.5% 4.0% 3.5%

Net written premium growth20.7%12.0%7.5% 4.0% 3.5%

Earned premium growth24.8%17.0% 6.0% 5.5% 3.5%

Loss ratio59.2%59.6%60.7%62.6%64.0%

Acquisition expense ratio18.7%17.5%17.5%17.5%17.5%

Operating expense ratio 6.3% 5.6% 5.5% 5.4% 5.5%

Investment income

Investment income growth54.6%31.0%10.0%8.0%7.0%

Implied yield 4.18% 4.60% 4.43% 4.40% 4.38%

Other

Fee and commission income 2.1% 3.5% 5.0%7.0%7.5%

Fixed asset growth32.6%27.1%14.0%10.5%9.3%

Equity asset growth0.0%0.0%0.0%0.0%0.0%

Premium receivable (as a % of gwp)38.7%32.0%30.5%29.0%27.5%

Deferred acquisition costs (as a % of

unearned premiums19.8%19.8%19.8%19.8%19.8%

Liabilities

Unpaid losses and lae growth, net37.5%8.0% 4.0% 2.0% 2.0%

Other, net0.00.00.00.00.0

Increase in debt0.00.00.00.00.0 Shareholders' equity

Share repurchase ($)0.00.00.00.00.0

Dividend per share0.310.400.440.510.60

Cost of equity 5.0%

Beta 1.05

Long-term economic growth rate 5.0%

Premiums/equity target leverage125.0%

Capital expenditures25.025.025.025.025.0

Source: Goldman Sachs Research and

Company data

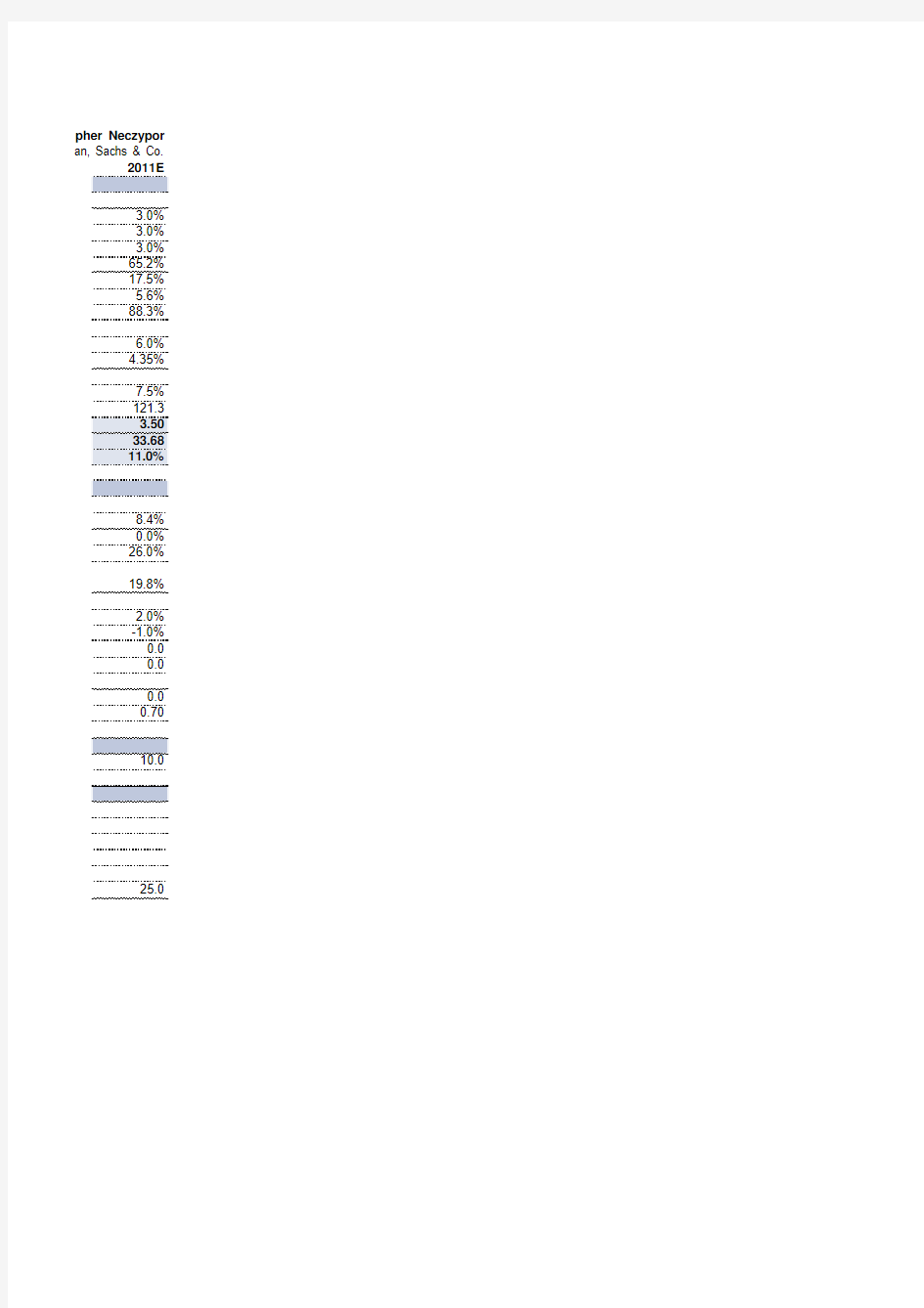

pher Neczypor an, Sachs & Co.

3.0%

3.0%

3.0%

65.2%

17.5%

5.6%

6.0%

4.35%

7.5%

8.4%

0.0%

26.0%

19.8%

2.0%

0.0

0.0

0.0

0.70

25.0