The Volatility Smile and Its Implied Tree

蒙娜丽莎是否微笑由看官你的情绪决定英语美文

蒙娜丽莎是否微笑由看官你的情绪决定英语美文Scientists have discovered why the Mona Lisa’s expression looks so different to different people and at different times.不同的人在不同的时间观察蒙娜丽莎的表情会得到完全不同的印象,对于这一点,科学家们已经找到原因。

For centuries, art lovers and critics have been perplexed by and debated the Leonardo Da Vinci paintings gaze and slight smile - or is it a grimace?几百年来,艺术爱好者和评论家一直对莱奥纳多.达芬奇这幅画中人物的目光和她的微笑(或是苦相)感到困惑,并对此进展争论。

But new research from the University of California, San Francisco has shed new light on the luminous and seemingly changing face of the Mona Lisa.不过,美国旧金山加利福尼亚大学的一项新研究让人们对蒙娜丽莎明亮且似乎在不断变化的表情有了新的理解。

Through experiments on visual perception and neurology, they discovered that our emotions really do alter how we see a neutral face.通过视觉和神经学实验,科学家们发现,我们的情绪确实可以改变我们看待一个中性的脸部表情的方式。

Dr Erika Siegel and her colleagues study how our emotions change our perceptions of the world around us - even when we aren’t aware that something has changed our feelings.该大学的埃丽卡.西格尔博士及其同事研究了情绪如何改变我们对周围世界的理解,即使我们不知道某些事情已经改变了自己的情绪。

纪伯伦泪与笑英语诗

纪伯伦泪与笑英语诗The Tears and Laughter of Kahlil Gibran's PoetryKahlil Gibran was a Lebanese-American artist philosopher and writer who is widely regarded as one of the most influential and inspirational literary figures of the 20th century His poetry and prose have captivated readers around the world with their profound insights into the human condition and their poetic exploration of the deepest emotions of the soul Gibran's work is characterized by a unique blend of Eastern mysticism and Western modernism a fusion that has given rise to a timeless and universal appealAt the heart of Gibran's literary legacy is his ability to capture the full range of human experience from the depths of sorrow and despair to the heights of joy and ecstasy His poems and stories are infused with a rare sensitivity and an unwavering commitment to the truth of the human spirit revealing the profound complexities and contradictions that lie at the core of the human experienceOne of the most striking features of Gibran's writing is his ability to evoke powerful emotional responses in his readers Through his masterful use of language and his keen insight into the humanpsyche Gibran is able to transport his audience to the very depths of their own souls stirring up feelings of profound longing nostalgia and even anguish His poems often explore the themes of love loss and the search for meaning in a world that can be both beautiful and brutalIn his most famous work The Prophet Gibran presents a series of profound meditations on the nature of life death love and the human condition Through the voice of the prophet Almustafa Gibran weaves a tapestry of exquisite poetry that speaks to the universal yearnings of the human heart In one particularly poignant passage Gibran writesYour joy is your sorrow unmaskedAnd the selfsame well from which your laughter rises was oftentimes filled with your tearsAnd how else can it beThe deeper that sorrow carves into your being the more joy you can containHere Gibran eloquently captures the essential interconnectedness of joy and sorrow revealing how the two are inextricably bound together as part of the human experience He suggests that it is only through embracing the fullness of our emotional lives that we can truly open ourselves up to the profound joys and blessings that lifehas to offerThroughout his work Gibran returns again and again to the theme of the human soul and its eternal search for meaning and fulfillment In poems like "On Children" and "On Marriage" he offers profound insights into the nature of love and the challenges of human relationships exploring the delicate balance between the need for individual expression and the desire for connection and intimacyIn "On Children" for example Gibran writesYour children are not your childrenThey are the sons and daughters of Life's longing for itselfThey come through you but not from youAnd though they are with you yet they belong not to youHere Gibran reminds us that our children are not mere extensions of ourselves but rather unique individuals with their own inherent worth and dignity He suggests that as parents our role is not to mold or control our children but rather to nurture and support them as they embark on their own unique journeys of self-discovery and fulfillmentSimilarly in "On Marriage" Gibran explores the complexities of romantic love offering a vision of marriage that transcends thenarrow confines of possessiveness and dependency He writesLet there be spaces in your togethernessAnd let the winds of the heavens dance between youLove one another but make not a bond of loveLet it rather be a moving sea between the shores of your soulsThrough these poetic meditations Gibran invites us to embrace the paradoxes and contradictions of the human experience to celebrate the beauty and mystery of the human soul and to find solace and inspiration in the timeless truths that lie at the heart of the human conditionUltimately what sets Gibran's writing apart is its ability to speak to the universal longings and aspirations of the human spirit His poems and stories resonate with readers across cultures and generations because they tap into the deepest wells of human emotion and experience offering a profound and transformative vision of what it means to be fully aliveWhether he is exploring the depths of sorrow or the heights of joy Gibran's writing is characterized by a rare sensitivity and a profound respect for the inherent dignity and worth of the human person His work invites us to embrace the fullness of our emotional lives to confront our fears and anxieties and to find solace and inspiration inthe eternal truths that lie at the heart of the human conditionIn a world that is often dominated by cynicism and despair Gibran's poetry stands as a shining beacon of hope and inspiration reminding us of the enduring power of the human spirit and the boundless potential of the human soul Through his timeless words and images Gibran continues to inspire and uplift readers around the world offering a vision of a more just compassionate and fulfilling world。

volatility surface

1

risk when these options are priced. Traders also use the volatility surface in an ad hoc way for hedging. They attempt to hedge against potential changes in the volatility surface as well as against changes in the asset price. As described in Derman (1999) one popular approach to hedging against asset price movements is the “volatility-by-strike” or “sticky strike” rule. This assumes that the implied volatility for an option with a given strike price and maturity will be unaffected by changes in the underlying asset price. Another popular approach is the “volatility-bymoneyness” or “sticky delta” rule. This assumes that the volatility for a particular maturity depends only on the moneyness (that is, the ratio of the price of an asset to the strike price). The first attempts to model the volatility surface were by Rubinstein (1994), Derman and Kani (1994), and Dupire (1994). These authors show how a one-factor model for an asset price, known as the implied volatility function (IVF) model, can be developed so that it is exactly consistent with the current volatility surface. Unfortunately, the evolution of the volatility surface under the IVF model can be unrealistic. The volatility surface given by the model at a future time is liable to be quite different from the initial volatility surface. For example, in the case of a foreign currency the initial U-shaped relationship between implied volatility and strike price is liable to evolve to one where the volatility is a monotonic increasing or decreasing function of strike price. Dumas, Fleming, and Whaley (1997) have shown that the IVF model does not capture the dynamics of market prices well. Hull and Suo (2002) have shown that it can be dangerous to use the model for the relative pricing of barrier options and plain vanilla options. In the first part of this paper we develop a general diffusion model for the evolution of a volatility surface and derive a restriction on the specification of the model necessary for it to be a no-arbitrage model. Other researchers that have independently followed a similar approach are Ledoit and Santa Clara (1998), Sch¨ onbucher (1999), and Brace et al (2001). In addition, Britten–Jones and Neuberger (2000) produce some interesting results characterizing the set of all continuous price processes that are consistent with a given set of option prices. Our work is different from that of other researchers in that we a) investigate the implications of the no-arbitrage condition for the shapes of the volatility surfaces likely to be observed in different situations and b) examine whether the various rules of thumb that have been put forward by traders are consistent with the no-arbitrage condition. We also extend the work of Derman (1999) to examine whether the rules of thumb are supported 2

关于雨果名言英文

关于雨果名言英文第1条He is fair in love and acting as she is a piece of infatuation.第2条使人变渺小的感情可耻,使人变孩子的感情可贵。

第3条我的风度是贵族的,但我的行为却是民主的。

第4条My presence is noble, but my behavior is democracy.第5条精神象乳汁一样可以养育人,智慧便是一只乳房。

第6条花朵预兆着果实,少女梦想着爱情。

第7条生活中最大的幸福是坚信有人爱我们。

第8条Books are friends,although there is no passion,but very loyal.第9条所有的植物都是一盏灯,而香味,就是它的光。

第10条有许多可爱的女性,但没有完美无缺的女性。

第11条We the people have their own idol.第12条The day belongs to all people, why only darkness for me?第13条The supreme happiness of life is the conviction that we are loved.第14条树干总是一成不变,树叶却时落时生。

第15条慈悲也不过是一种比较高级的法律而已。

第16条if you want to call the public wait patiently statement immediately begun to them.第17条A beggar, I d on’t know where to beg for love.第18条真正的强者,是那种具有自制力的人。

第19条谨慎比大胆要有力量得多。

第20条这世上只有生物,既无所谓善,也无所谓恶。

第21条做好人容易,做正直的人却难。

第22条谁虚度年华,青春就要褪色,生命就要抛弃他。

第23条Music expresses something beyond narration but have to say.第24条任何卓越的胜利总多少是大胆的成果。

紫藤萝瀑布这篇课文的读后感

紫藤萝瀑布这篇课文的读后感英文回答:"Wisteria Waterfall" is a lyrical and evocative prose poem that captures the breathtaking beauty of a cascading wisteria vine. The poet's vivid imagery and sensory details create a rich and immersive experience that transports the reader into the heart of nature's splendor.The poem begins with the speaker marveling at the sheer abundance of wisteria blossoms, hanging like a shimmering curtain from the eaves of a temple. The poet's use of the word "cascade" suggests a dynamic and fluid movement, as if the delicate flowers were flowing over the temple roof in a continuous stream. The image of the blossoms as a "waterfall" further emphasizes their sheer quantity and the sense of overflowing abundance.The poet then draws our attention to the individual blossoms, describing their "rich purple" hues and theirsoft, velvety texture. The use of the word "purple" evokes a sense of regal elegance, while the reference to "velvet" suggests a luxurious and tactile quality. These sensory details create a vivid impression of the flowers' beauty and allure.The poem's most striking feature is its use of metaphors and similes to compare the wisteria to various other natural phenomena. The blossoms are likened to "amethyst grapes," "emeralds," and "turquoise," evoking their beauty and preciousness. The poet also compares the vine to a "serpent" and a "fairy's ladder," suggesting its sinuous and ethereal qualities. These comparisons add depth and complexity to the poem's imagery, inviting the reader to see the wisteria in new and unexpected ways.The poem concludes with the speaker reflecting on the transformative power of the wisteria's beauty. They describe how the sight of the vine fills them with a sense of wonder and tranquility, and how it inspires them to appreciate the interconnectedness of all living things. The poem ends with the speaker expressing their hope that thewisteria will continue to bloom "year after year," a symbol of the enduring beauty and resilience of nature.Overall, "Wisteria Waterfall" is a celebration of the beauty and wonder of the natural world. The poet's skillful use of imagery and metaphor creates a rich and immersive experience that transports the reader into the heart of nature's splendor. The poem's message of interconnectedness and the transformative power of beauty is one that resonates deeply with readers and serves as a reminder to appreciate the wonders that surround us.中文回答:“紫藤萝瀑布”是一首优美抒情的散文诗,它捕捉到了紫藤花瀑布般的动人美。

07FRM真题答案3

94.The joint probability distribution of random variables X and Y is given by f (x, y)=k*x*y forx=1,2,3, y=1,2,3, and k is a positive constant. What is the probability that X+Y will exceed 5?a.1/9b.1/4c.1/36d.Cannot be determined95.Which of the following is not an approach for detecting style drift of hedge funds?a.Performance attributionb.Peer group comparisonc.Cash flow analysismunication with fund manager96.To hedge against future, unanticipated, and significant increases in borrowing rates, which ofthe following alternatives offers the greatest flexibility for the borrower?a.Interest rate collarb.Fixed for floating swapc.Call swaptiond.Interest rate floor97.Assume the true distribution of returns is leptokurtotic. If we assume normality when wecalculate the VaR, then which of the following statements is true:a.The 95% VaR is overstated.b.The 95% VaR is understated.c.The 95% VaR is appropriate.d.We cannot state the relationship between the true VaR and the calculated VaR.The next three questions use the following data:98. A portfolio consists of two bonds. The credit-VaR is defined as the maximum loss due todefaults at a confidence level of 98% over a one-year horizon. The probability of joint default of the two bonds is 1.27%, and the default correlation is 30%.Bond Value one year forward One year cumulative default probability Recovery rate B1=USD 1,000,000 3% 60%B2=USD 600,000 5% 40%What is the expected credit loss of the portfolio?D 0D 9,652D 20,348D 30,00098.What is your best estimate of the credit-VaR for this portfolio of bonds based on thedistribution of losses due to defaults?D 570,000D 400,000D 360,000D 370,00099.In the previous question, you estimated a VaR that corresponds to the VaR obtained fromCreditRisk+. Suppose that instead you wanted to estimate the VaR using the CreditMetrics approach. If you were given all additional data listed below, which data would you not need to estimate the CreditMetrics-Style credit-VaR?a.Volatility of firm value for each issuerb.Transition matrix for downgrades and upgrades in addition to default probabilitiesc.Tern structure of credit spreads and interest ratesd.Promised coupon payments and maturity101. Given the information provided in the table below, what is the risk budget, at the 99% confidence level of the following CHF million equally weighted investment portfolio?Asset Expected Return V olatility CorrelationStocks Bonds Stocks 24.00% 18% 1 0.1Bonds 15.00% 6% 0.1 1a. CHF 20.97 millionb. CHF 13.98 millionc. CHF 27.96 milliond. CHF 22.77 million102. The Chief Risk Officer (CRO) of an exporting firm is attempting to estimate the firm’s one-year cash flow at risk. Which of the following issues describes an approach that is irrelevant to the task to the CRO?a. Because cash flow at risk is generally estimated over a quarter or over a year, it isnecessary to forecast the future values of risk factors.b. To the extent that the firm’s income from exports is best approximated by a real optionbecause the firm does not have to export when the price of the foreign currency isunexpectedly low, the CRO can use option analysis and does not have to worry aboutforecasting exchange rates.c. A parametric approach can be used if exposures to foreign exchange risk factors arelinear, if there are no other risk factors, and if exchange rate changes are normallydistributed.d. Using a Monte Carlo approach will help the CRO if the firm’s foreign currency incomeis a nonlinear function of exchange rates.103. A single stock has a price of USD 10 and a current daily volatility of 2%. Using the delta-normal method, the VaR at the 95% confidence level of a long at-the-money call on this stock over a one-day holding period is approximatelyD 1.645D 0.16D 0.33D 0.23104. Your bank is using the internal models approach to estimate its general market risk charge.The multiplication factor ‘k’, set by the regulator, is 3 and banks are allowed to use the square root rule to scale daily VaR. The previous day’s one-day VaR estimate is EUR 3 million, and the average of the daily VaR over the last 60 days is EUR 2 million. Given the above information, what will be the market risk charge for your bank?a.EUR 9.49 millionb.EUR 28.46 millionc.EUR 6.32 milliond.EUR 18.97 million105. A portfolio manager has a bond position worth USD 100 million. The position has a modified duration of eight years and a convexity of 150 years. Assume that the term structure is flat.By how much does the value of the position change if interest rates increase by 25 basis points?D -2,046,875D -2,187,500D -1,953,125D -1,906,250106. Suppose you are holding 100 Wheelbarrow Company shares with a current price of USD 50.The daily historical mean and volatility of the return of the stock is 1% and 2%, respectively.The bid-ask spread of the stock varies over time. The daily historical mean and volatility of the spread is 0.5% and 1%, respectively. Calculate the daily liquidity-adjusted VaR (LVaR) at 99% confidence level (both the return and spread of the stock are normally distributed):D 254D 229D 325D 275107. Consider the following potential operational risks. Due to a rogue trader, we estimate that over one-year period there is a 10% chance we could lose anywhere between EUR 0 and EUR 100 million (equal probability for all points within that range and 0 probability of any losses outside that range). Due to model risk, we estimate that over a one-year period there isa 20% chance that we will lose EUR 25 million normally distributed with a standarddeviation of EUR 5 million. Which of the following statements is true?a.The expected loss from a rogue trader is less than the expected loss from model risk.b.The expected loss from a rogue trader is greater than the expected loss from model risk.c.The maximum unexpected loss from a rogue trader at the 95% confidence level is lessthan the maximum unexpected loss at the 95% confidence level from model risk.d.The maximum unexpected loss at the 95% level from a rogue trader is greater than themaximum unexpected loss at the 95% level from model risk.108. The risk-free rate is 5% per year and a corporate bond yields 6% per year. Assuming a recovery rate of 75% on the corporate bond, what is the approximate market implied one-year probability of default of the corporate bond?a. 1.33%b. 4.00%c.8.00%d. 1.60%109. A mutual fund investing in common stocks has adopted a liquidity risk measure limiting each of its holdings to a maximum of 30% of its 30-day average value traded. If the fund size is USD 3 billion, what is the maximum weight that the fund can hold in a stock with a 30-day average value traded of USD 2.4 million?a.24.00%b.0.08%c.0.024%d.80.0%110. Bank A makes a USD 10 million five-year loan and wants to offset the credit exposure to the obligor. A five-year credit default swap (CDS) with the loan as the reference asset trades on the market at a swap premium of 50 basis points paid quarterly. In order to hedge its credit exposure, Bank Aa.sells the five-year CDS and receives a quarterly payment of USD 50,000.b.buys the five-year CDS and makes a quarterly payment of USD 12,500.c.buys the five-year CDS and receives a quarterly payment of USD 12,500.d.sells the five-year CDS and makes a quarterly payment of USD 50,000.111. You don’t have access to KMV’s data. Your boss wants you to estimate the probability of default of a credit. To do so, you use the Merton model because the credit you are considering has no systematic risk. In Merton’s model, the distance to default and expected default frequency are:a.negatively and linearly related.b.positively and linearly related.c.negatively and nonlinearly related.d.positively and nonlinearly related.112. An investor is investigating three hedge funds as potential investments. Hedge fund A is an equity market neutral fund, B is a global macro fund with emphasis on equity markets, and C is a convertible arbitrage fund. Which answer correctly specifies the funds with the highest exposure to a worldwide, value-weighted equity index and to a credit default swaps index?Highest Equity Index Exposure Highest Credit Default Swap Index Exposurea. A Cb. B Cc. B Ad. A B113. Your bank is an active player in the commodity market. The view of the economist of the bank is that inflation is expected to rise moderately in the near term and market volatility is expected to remain low. The traders are advised to undertake deals on the metals exchange to align your book to conform with the expectations of the economist of the bank. As risk manager, you are asked to monitor the positions of the traders to make sure that they have the exposures to inflation and market volatility sought by the bank. Which trader has taken an appropriate position among the traders you are monitoring?a.Trader A bought a call and a put, both with 90 days to expiration and with strike priceequal to the existing spot level.b.Trader B bought a put option with a down-and-in knock in feature.c.Trader C bought a call option at the existing spot levels and sold a call at a higher strikeprice, both with 90 days to expiration.d.Trader D sold a call option and bought a put at the existing levels, both with 90 days toexpiration.114. It has been found that the correlations across indices increase during adverse market events(e.g., severe volatility, market crash). You are assessing the risks of a long-only global equityportfolio and are asked to describe for your boss the implications adverse market events might have in a VaR context. Which of the following statements is correct about the impact on future estimates of VaR for a long-only global equity portfolio?a.Following the onset of adverse market events, future VaR estimates will increase if VaRis estimated using the historical method compared to what would have happened had there been no adverse events.b.The effect of increased correlation on future VaR estimates cannot be estimated because,by definition, a crisis is a unique event with no comparable period.c.The performance of future VaR estimates will remain unaffected since by definition acrisis has a probability that is much lower than the probability level typically used to estimate VaR.d.Following the onset of adverse market events, future VaR estimates will decrease if VaRis estimated using a GARCH (1,1) model compared to what would have happened had there no adverse events.115. You have been asked to evaluate the performance of two hedge funds: Global Asset Management I and International Momentum II. Both are benchmarked to MSCI EAFE. The volatility of EAFE is 17.5% and the annualized performance is 10.6%. The risk-free rate is3.5%.Fund Volatility PerformanceGlobal Asset Management I 24.5% 12.5%International Momentum II 27.3% 13.6%Which of the two funds had a higher relative risk-adjusted performance (RAP) last year, and what is the RAP?a.International Momentum II, 5.42%b.International Momentum II, 1.18%c.Global Asset Management I, 4.85%d.Global Asset Management I, 6.16%116. Suppose that A and B are random variables, each follows a standard normal distribution, and the covariance between A and B is 0.35. What is the variance of (3A+2B)?a.14.47b.17.20c.9.20d.15.10117. The surplus of a pension fund is most important fora. a defined benefit fund.b. a defined contribution fund.c. a sponsoring company with strong financial status that operates in different industries.d. a young work force.118. Which of the following statements about liquidity risk elasticity (LRE) is incorrect?a.LRE is primarily useful for examining marginal changes in funding costs on a netasset/liability positionb.In calculating the sensitivity of a firm’s net assets to a change in its funding liquiditypremium, LRE assumes a parallel shift in funding costs across all maturities.c.The LRE is only reliable for small changes in interest costs.d.The LRE is a cash flow liquidity risk measure, not a present value liquidity risk measure.119. Your bank is using the Black-Scholes model for valuation and pricing of exchange rate options with implied volatility of the at-the money options imputed from the market quotes.However, the research staff is now suggesting that exchange rate markets are exhibiting a volatility smile and the existing valuations are incorrect. As a risk manager, you will be more concerned in which of the following situations?a.When the portfolio mainly consists of at-the-money long calls and puts.b.When the portfolio mainly consists of short put positions in deep out-of money options.c.When the portfolio mainly consists of short positions in at-the-money calls and puts.d.When the portfolio mainly consists of long call positions in deep out-of-money options.120. What does a hypothesis test at the 5% significance level mean?a.P (not reject H0 | H0 is true)=0.05b.P (not reject H0 | H0 is false)=0.05c.P (reject H0 | H0 is true)=0.05d.P (reject H0 | H0 is false)=0.05121. Bank A has exposure to USD 100 million of debt issued by Company R. Bank A enters into a credit default swap transaction with Bank B to hedge its debt exposure to Company R. BankB would fully compensate Bank A if Company R defaults in exchange for premium. Assumethat the defaults of Bank A, Bank B, and Company R are independent and that their default probabilities are 0.3%, 0.5%, and 3.6%, respectively. What is the probability that Bank A will suffer a credit loss in its exposure to Company R?a. 4.1%b. 3.6%c.0.0108%d.0.0180%122. A fund manager recently received a report on the performance of his portfolio over the last year. According to the report, the portfolio return is 9.3%, with a standard deviation of 13.5%, and beta of 0.83. The risk-free rate is 3.2%, the semi-standard deviation of portfolio is 8.4%, and the tracking error of the portfolio to the benchmark index is 2.8%. What is the difference between the value of the fund’s Sortino ratio (computed relative to the risk-free rate) and its Sharpe ratio?a. 1.727b.0.274c.-0.378d.0.653123. Your company is expecting a major export order from a London-based client. The receivables under the contract are to be billed in GBP, while your reporting currency is USD. Since the order is a large sum, your company does not want to bear the exchange risk and wishes to hedge it using derivatives. To minimize the cost of hedging, which of the following is the most suitable contract?a. A chooser option for GBP/USD pairb. A cross-currency swap where you pay fixed in USD and receive floating in GBPc. A barrier put option to sell GBP against USDd.An Asian call option on GBP against USD124. A bond trader has bought a position in Treasury bonds with a 4% annual coupon rate on February 15, 2015. The DV01 of the position is USD 80,000. The trader decides to hedge his interest rate risk with the 4.5% coupon rate Treasury bonds maturing on May 15, 2017, which has a DV01 of 0.076 per USD 100 face value. To implement this hedge, approximately what face amount of the 4.5% Treasury bonds maturing on May 15, 2017, should the trader sell?D 10,500,000D 80,000D 105,000,000D 80,000,000125. The bank you work for has a RAROC model. The RAROC model, computed for each specific activity, measures the ratio of the expected yearly net income to the yearly VaR risk estimate. You are asked to estimate the RAROC of its USD 500 million loan business. The average interest rate is 10%. All loans have the same probability of default of 2% with a loss given default of 50%. Operating costs are USD 10 million. The funding cost of the business is USD 30 million. RAROC is estimated using a credit-VaR for loan businesses. In this case, the appropriate credit-VaR for the loans is 7.5%. The economic capital is invested and earns 6%. The RAROC is:a.19.33%b.46.00%c.32.67%d.13.33%126. A firm is going to buy 10,000 barrels of West Texas Intermediate Crude Oil. It plans to hedge the purchase using the Brent Crude Oil futures contracts. The correlation between the spot and futures prices is 0.72. The volatility of the spot price is 0.35% per year. The volatility of the Brent Crude Oil futures price is 0.27 per year. What is the hedge ratio for the firm?a.0.9333b.0.5554c.0.8198d. 1.2099127. An investor sells a June 2008 call of ABC Limited with a strike price of USD 45 for USD 3and buys a June 2008 call of ABC Limited with a strike price of USD 40 for USD 5. What is the name of this strategy and the maximum profit and loss the investor could incur?a. Bear Spread, Maximum Loss USD 2, Maximum Profit USD 3b. Bull Spread, Maximum Loss Unlimited, Maximum Profit USD 3c. Bear Spread, Maximum Loss USD 2, Maximum Profit Unlimitedd. Bull Spread, Maximum Loss USD 2, Maximum Profit USD 3128. In pricing a derivative using the Monte Carlo method, we need to stimulate a reasonablenumber of paths for the price of the underlying asset. Suppose we use a simple model for the return of the underlying asset:()()t y t drift vol e t =*∆+,and e (t) is distributed ~ N (0,1)Where drift and vol are known parameters and ∆t is a step size. The generation of each pathrequires a number of steps. Which of the following describes the correct procedure?a. Generate a random number from a normal distribution N (0,1), use the cumulativenormal function to get e (t), which will be fed into the model to get y(t). Repeat the same procedure until you get the full desired path.b. Generate a random number from a normal distribution N (0,1), use the inverse normalfunction to get e (t), which will be fed into the model to get y (t). Repeat the same procedure until you get the full desired path.c. Generate a random number from a uniform distribution defined in [0,1], use thecumulative normal function to get e (t), which will be fed into the model to get y(t). Repeat the same procedure until you get the full desired path.d. Generate a random number from a uniform distribution defined in [0,1], use the inversecumulative normal function to get e (t), which will be fed into the model to get y(t). Repeat the same procedure until you get the full desired path.129. What type of operational risk caused substantial losses to Barings Bank?a.Inability to reconcile a new settlement systemb.Unauthorized tradingc.Political turmoild.Massive technology failure130. Which one of the following statements does not apply to the Basel II Advanced Measurement Approach (AMA) for operational risk?a.In contrast to the credit risk Internal Ratings Based Approaches, banks using the AMAmay estimate the correlation between different types of operational risks if their models satisfy regulatory requirements.b.In contrast to credit risk regulatory capital for corporate loans, banks using the AMAmay have to set aside capital for both expected and unexpected operational risk losses.c.Reporting of operational risk exposure to senior management is a necessary condition fora bank’s ability to use the AMA.d.To evaluate exposure to high-severity operational risk events, banks using the AMA mayuse either scenario analysis of expert opinion or VaR model estimates based on internal data using extreme value theory.131. The current value of the S&P 500 index is 1457, and each S&P futures contract is for delivery of 250 times the index. A long-only equity portfolio with market value of USD 300,100,000 has beta of 1.1. To reduce the portfolio beta to 0.75, how many S&P futures contract should you sell?a.288 contractsb.618 contractsc.906 contractsd.574 contracts132. A bank assigns capital to its traders using component-VaR, which is based on the trading portfolio’s VaR estimated at the 99% confidence level. The market value of the bank’s trading portfolio is HKD 1 billion with a daily volatility of 2%. Of this portfolio, 1% is invested in a trading book with a beta of 0.6 relative to the trading portfolio. The closest estimate of the capital assigned to this trading book isa.HKD 279,600b.HKD 167,760c.HKD 1,977,070d.HKD 197,400133. On January 1, 2006, a pension fund has assets of EUR 100 billion and is fully invested in the equity market. It has EUR 85 billion in liabilities. During 2006, the equity market declined by 15%, and yields increased by 1.2%. If the modified duration of the liabilities is 12.5, what is the pension fund’s surplus on December 31, 2006?a.EUR 15.00 billionb.EUR 12.93 billionc.EUR 12.75 billiond.EUR 12.57 billion134. Considering options generally (i.e., not only plain vanilla calls and puts), which of the following statements about vega is correct?a. A deep in-the-money up and out call option has a negative vega.b.An option holder can never be vega negative.c. A deep out-of-money digital option has a negative vega.d. A deep out-of-money up and out call option has a negative vega.135. Which of the following underlying macroeconomic conditions would leave an emerging market most vulnerable to the contagion effects of a currency crisis?rge current account surplus, low foreign exchange reserves, nonconvertible currencyrge current account deficit, low foreign exchange reserves, fully convertible currencyc.Small current account deficit, high foreign exchange reserves, nonconvertible currencyrge current account surplus, low foreign exchange reserves, fully convertible currency136. A three-year, credit-linked note (CLN) with underlying Company Z has a LIBOR+60 bps semi-annual coupon. The face value of the CLN is USD 100. LIBOR is 5% for all maturities.The current three-year credit default swap spread for Company Z is 90 bps. The fair value of the CLN is closest toD 100.00D 111.05D 101.65D 99.19137. A fund manager currently has a delta-neutral portfolio with a gamma of –11,000. He is interested in reducing the portfolio gamma to provide protection against large movements in prices. A particular traded call option has a delta of 0.87 and gamma of 3.5. To make the portfolio gamma neutral, how many call options must be bought or sold?a.Buy 3,143 call optionsb.Sell 3,143 call optionsc.Buy 2,734 call optionsd.Sell 2,734 call options138. The severity distribution of operational losses usually has the following shape:a.Symmetrical with short tailsb.Long tailed to the rightc.Uniformd.Symmetrical with long tails139. The risk of the occurrence of a significant difference between the mark-to-model value of a complex and/or illiquid instrument and the price at which the same instrument is revealed to have traded in the market is referred to asa.liquidity riskb.dynamic riskc.model riskd.mark-to-market risk140. In a collateralized debt obligation (CDO), the Special Purpose Vehicle (SPV) is typicallya.A-rated.b.AAA-rated.c.not rated.d.BBB-rated.。

狄更斯的名言英文

狄更斯的名言英文导读:本文是关于狄更斯的名言英文,如果觉得很不错,欢迎点评和分享!1、一只眼睛里闪烁着爱的光芒,而另一只眼睛却燃烧着自私的慾火。

One eye twinkled with love, while the other was burning selfish desire.2、说实话是我恪守的金科玉律,不管便宜还是吃亏,我都要这样做,可惜的是我常常吃了亏。

To tell the truth is the golden rule I abide by. Whether it is cheap or not, I will do it. Unfortunately, I often suffer losses.3、无论做什么事,请记住:千万不要小气,千万不要虚假,千万不要残酷!Whatever you do, please remember: never be mean, never be false, and never be cruel!4、知足的茅草屋要胜过冰冷华丽的宫殿。

有了爱,就有了一切!A thatched cottage is better than a cold, splendid palace. With love, everything is possible.5、感化在效果方面,自古以来都比由偏见、愚昧和残酷而发明的腰衣、手铐、脚镣不止大一百倍。

In terms of effect, the influence has been more than 100times greater since ancient times than the waistcoat, handcuffs and shackles invented by prejudice, ignorance and cruelty.6、父亲造了孽,往往会报到孩子身上,而母亲积了德,也会报在孩子身上。

When a father makes a sin, he often reports to the child, and his mother gains virtue and reports to the child.7、如果我的世界不能成为你的世界,那么我愿将你的世界变成我的世界。

金融衍生工具测试题-(26)

1. A box spread is a combination of a bull spread composed of two call options with strikeprices 1X and 2X and a bear spread composed of two put options with the same twostrike prices.a) Describe the payoff from a box spread on the expiration date of the options.b) What would be a fair price for the box spread today? Define variables asnecessary.c) Under what circumstances might an investor choose to construct a box spread? d) What sort of investor do you think is most likely to invest in such an optioncombination, i.e. a hedger, speculator or arbitrageur? Explain your answer.2. Form a long butterfly spread using the three call options in the table below.a) What does it cost to establish the butterfly spread? b) Calculate each of the Greek measures for this butterfly spread position and explain how each can be interpreted. c) How would you make this option portfolio delta neutral? What would be achieved by doing so? d) Suppose that tomorrow the price of C1 falls to $12.18 while the prices of C2 and C3 remain the same. Does this create an arbitrage opportunity? Explain.3. Consider a six month American put option on index futures where the current futures price is 450, the exercise price is 450, the risk-free rate of interest is 7 percent per annum, the continuous dividend yield of the index is 3 percent, and the volatility of the index is 30 percent per annum. The futures contract underlying the option matures in seven months. Using a three-step binomial tree, calculate a) the price of the American put option now, b) the delta of the option with respect to the futures price, c) the delta of the option with respect to the index level, and d) the price of the corresponding European put option on index futures. e) Apply the control variate technique to improve your estimate of the American option price and of the delta of the option with respect to the futures price. Note that the Black-Scholes price of the European put option is $36.704 and the delta with respect to the futures price given by Black-Scholes is –0.442.4.A financial institution trades swaps where 12 month LIBOR is exchanged for a fixed rate of interest. Payments are made once a year. The one-year s (i.e., the rate that would be exchanged for 12 month LIBOR in a new one-year swap) is 6 percent. Similarly the two-year s is 6.5 percent.a)Use this s to calculate the one and two year LIBOR zero rates, expressing the rateswith continuous compounding.b)What is the value of an existing s a notional principal of $10 million that has twoyears to go and is such that financial institution pays 7 percent and receives 12month LIBOR? Payments are made once a year.c)What is the value of a forward rate agreement where a rate of 8 percent will bereceived on a principal of $1 million for the period between one year and two years?Note: All rates given in this question are expressed with annual compounding.5.The term structure is flat at 5% per annum with continuous compounding. Sometime ago a financial institution entered into a 5-year s a principal of $100 million in which every year it pays 12-month LIBOR and receives 6%. The s has twoyears eight months to run. Four months ago 12-month LIBOR was 4% (withannual compounding). What is the value of the s? What is the financialinstitution’s credit exposure on the swap?6.An American put option to sell a Swiss franc for USD has a strike price of0.80 and a time to maturity of 1 year. The volatility of the Swiss franc is 10%,the USD interest rate is 6%, and the Swiss franc interest rate is 3% (both interest rates continuously compounded). The current exchange rate is 0.81. Use a threetime step tree to value the option.7. A European call option on a certain stock has a strike price of $30, a time tomaturity of one year and an implied volatility of 30%. A put option on the samestock has a strike price of $30, a time to maturity of one year and an impliedvolatility of 33%. What is the arbitrage opportunity open to a trader. Does theopportunity work only when the lognormal assumption underlying Black-Scholes holds. Explain the reasons for your answer carefully.8. A put option on the S&P 500 has an exercise price of 500 and a time to maturityof one year. The risk free rate is 7% and the dividend yield on the index is 3%.The volatility of the index is 20% per annum and the current level of the index is 500. A financial institution has a short position in the option.a) Calculate the delta, gamma, and vega of the position. Explain how they can beinterpreted.b) How can the position be made delta neutral?c) Suppose that one week later the index has increased to 515. How can deltaneutrality be preserved?9.An interest rate s a principal of $100 million involves the exchange of 5% perannum (semiannually compounded) for 6-month LIBOR. The remaining life is 14months. Interest is exchanged every six months. The 2 month, 8 month and 14 month rates are 4.5%, 5%, and 5.4% with continuous compounding. Six-monthLIBOR was 5.5% four months ago. What is the value of the swap?10.The Deutschemark-Canadian dollar exchange rate is currently 1.0000. At theend of 6 months it will be either 1.1000 or 0.9000. What is the value of a 6 month option to sell one million Canadian dollars for 1.05 million deutschemarks. Verify that the answer given by risk neutral valuation is the same as that given by no-arbitrage arguments. Is the option the same as one to buy 1.05 milliondeutschemarks for 1 million Canadian dollars? Assume that risk-free interest rates in Canada and Germany are 8% and 6% per annum respectively.11.An American put futures option has a strike price of 0.55 and a time to maturityof 1 year. The current futures price is 0.60. The volatility of the futures price is25% and the interest rate(continuously compounded) is 6% per annum. Usea four time step tree to value the option.12.Is it ever optimal to exercise early an American call option on a) the spot price ofgold, b) the spot price of copper, c) the futures price of gold, and d) the averageprice of gold measured between time zero and the current time. Explain youranswers.13.The future probability distribution of a stock price has a fatter right tail andthinner left tail than the lognormal distribution. Describe the effect of this on the prices of in-the-money and out-of-the-money calls and puts. What is the volatility smile that would be observed?14. A bank has just sold a call option on 500,000 shares of a stock. The strike price is40; the stock price is 40; the risk-free rate is 5%; the volatility is 30%; and thetime to maturity is 3 months.a) What position should the company take in the stock for delta neutrality?b) Suppose that the bank does set up a delta neutral position as soon as the optionhas been sold and the stock price jumps to 42 within the first hour of trading.What trade is necessary to maintain delta neutrality? Explain whether the bank has gained or lost money in this situation. (You do not need to calculate the exactamount gained or lost.)c) Repeat part b) on the assumption that the stock jumps to 38 instead of 4215.A bank has sold a product that offers investors the total return (excluding dividends)on the Toronto 300 index over a one year period. The return is capped at 20%.If the index goes down the original investment of the investor is returned.a) What option position is equivalent to the productb) Write down the formulas you would use to value the product and explain indetail how you would decide whether it is a good deal to the investore a three step tree to value a three month American put option on wheat futures.The current futures price is is 380 cents, the strike price is 370 cents, the risk-free rate is 5% per annum, and the volatility is 25% per annum. Explain carefully what happens if the investor exercises the option after two months. Suppose that thefutures price at the time of exercise is 362 and the most recent settlement price is 360.17.a) A bank’s assets and liabilities both have a duration of 5 years. Is the bankhedged against interest rate movements? Explain carefully any limitations of the hedging scheme it has chosen.b) Explain what is meant by basis risk in the situation where a company knows itwill be purchasing a certain asset in two months and uses a three-month futurescontract to hedge its risk.18.a) Give an example of how a s be used by a portfolio manager.b) Explain the nature of the credit risks to a financial institution in a sANSWERS1.(a) The box spread pays off X2-X1 in all circumstances (b) It should be worth thepresent value of X2-X1 today, c) and d) An arbitrageur might invest in a boxspread if it is mispriced in the market today.2.(a) 1.79 b) Greek letters are -0.0077, -0.0037, etc c) For delta neutrality we buy0.0077 of the underlying asset. Small changes in the price of the underlying assetthen have very little effect on the value of the whole portfolio d) Yes. We have a positive cash flow when we set up the butterfly spread today and a zero or positive cash in 180 days3.a) 40.13, b) -0.449, c) F0=S0e0.04*7/12 or S0=0.9769F0 so that delta with respect tothe index level is =0.439, d) 39.81, e) American option price becomes40.13+36.704-39.81=37.02. Delta becomes -0.449 +0.444-0.442=-0.4474.a) One year rate is5.827%, two-year rate is6.313%, b) -$91,239, c) $8,5045. 3.50. This is also the credit exposure.6.0.0217.Put is priced too high relative to call. Sell put and buy call. This works regardlessof whether the assumptions underlying Black-Scholes hold8.a) 0.371, -0.0038, -1.85, b) Sell 0.371 of index for each option sold, c) Deltachanges to 0.317 so 0.054 of index must be bought back9.$841,000 assuming floating is received.10.Assume that the exchange rate is DM per $. p is then 0.450 and the value of theoption is about 80,000 DM. Yes the two options are the same.11.0.03612.a) no b)yes c)yes d)yes13.This will lead to a smile where volatility increases with strike price. this is theopposite of what is usually observed.14.a) Delta of long position in one option is 0.563. Bank should buy 281,500 sharesb) Delta changes to 0.686. Bank should buy a further 61,500 shares. The bank hasa negative gamma and so is likely to have lost money from the big move, c) Deltachanges to 0.427. The bank should sell 68,000 shares. It will have lost money in this situation as well15.Suppose that S0 is invested in the product where S0 is the index level today. Thevalue of the investment in one year is S0 plus the payoff from a bull spread. The bull spread is created from a long call option with strike price S0 and a short call option with strike price 1.2S0. the interest earned can be calculated by valuing the options. This can be compared with other market opportunities.16.Value is 15.14 cents. Total gain from exercise after 2 months is 8 cents. therewould be a 10 cent cash pay off and a short futures position worth -2 cents.17.a) Limitations relate to possibility of non-parallel shifts in the term structure andthe possibility of large movements b) basis risk arises from the difference between spot and futures price in 2 months18.a) A s be used to change an asset earning a fixed rate of interest to one earning afloating rate. b) credit risks arise from the possibility of a default when the s a positive value and the counterparty defaults.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

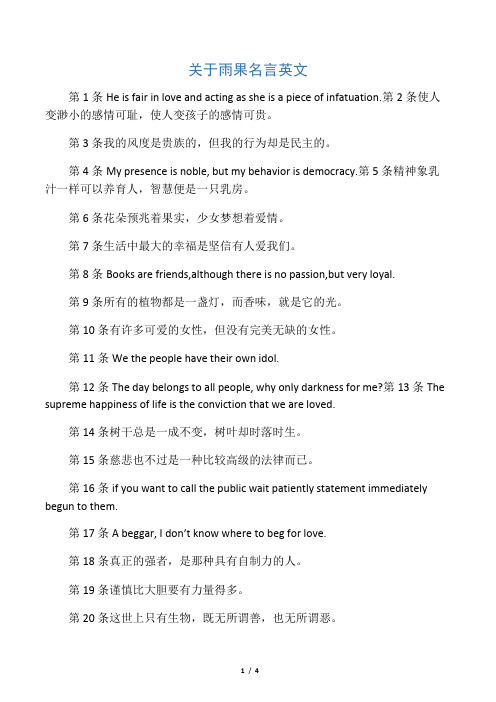

The Black-Scholes model assumes that the index level executes a random walk with a constant volatility. If the Black-Scholes model is correct, then the index distribution at any options expiration is lognormal, and all options on the index must have the same implied volatility. But, ever since the ‘87 crash, the market’s implied BlackScholes volatilities for index options have shown a negative relationship between implied volatilities and strike prices – out-of-the-money puts trade at higher implied volatilities than out-of-the-money calls. The graph above illustrates this behavior for 47-day European-style March options on the S&P 500, as of January 31, 1994. The data for strikes above (below) spot comes from call (put) prices. By empirically varying the Black-Scholes volatility with strike level, traders are implicitly attributing a unique non-lognormal distribution to the index. You can think of this non-lognormal distribution as a consequence of the index level executing a modified random walk – modified in the sense that the index has a variable volatility that depends on both stock price and time. To value European-style options consistently by calculating the expected values of their payoffs, you then need to know the exact form of the non-lognormal distribution. To value American-style or more exotic options, you must know the exact nature of the modified random walk – that is, how the volatility varies with stock price and time.

The Smile: Implied Volatilities of S&P 500 Options on Jan 31, 1994.

option implied volatility (%)

O

18

16

O

14

O

12

O O

10

O O

8

O O

90

95

100

105

option strike (% of spot)

Goldman Sachs

Quantitative Strategies Research Notes

January 1994

The Volatility Smile and It Iraj Kani

Goldman Sachs

QUANTITATIVE STRATEGIES RESEARCH NOTES

Goldman Sachs

QUANTITATIVE STRATEGIES RESEARCH NOTES

SUMMARY The market implied volatilities of stock index options often have a skewed structure, commonly called “the volatility smile.” One of the long-standing problems in options pricing has been how to reconcile this structure with the Black-Scholes model usually used by options traders. In this paper we show how to extend the Black-Scholes model so as to make it consistent with the smile.

Copyright 1994 Goldman, Sachs & Co. All rights reserved. This material is for your private information, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. Certain transactions, including those involving futures, options and high yield securities, give rise to substantial risk and are not suitable for all investors. Opinions expressed are our present opinions only. The material is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. We, our affiliates, or persons involved in the preparation or issuance of this material, may from time to time have long or short positions and buy or sell securities, futures or options identical with or related to those mentioned herein. This material has been issued by Goldman, Sachs & Co. and/or one of its affiliates and has been approved by Goldman Sachs International, regulated by The Securities and Futures Authority, in connection with its distribution in the United Kingdom and by Goldman Sachs Canada in connection with its distribution in Canada. This material is distributed in Hong Kong by Goldman Sachs (Asia) L.L.C., and in Japan by Goldman Sachs (Japan) Ltd. This material is not for distribution to private customers, as defined by the rules of The Securities and Futures Authority in the United Kingdom, and any investments including any convertible bonds or derivatives mentioned in this material will not be made available by us to any such private customer. Neither Goldman, Sachs & Co. nor its representative in Seoul, Korea is licensed to engage in securities business in the Republic of Korea. Goldman Sachs International or its affiliates may have acted upon or used this research prior to or immediately following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of or income derived from the investment. Further information on any of the securities mentioned in this material may be obtained upon request and for this purpose persons in Italy should contact Goldman Sachs S.I.M. S.p.A. in Milan, or at its London branch office at 133 Fleet Street, and persons in Hong Kong should contact Goldman Sachs Asia L.L.C. at 3 Garden Road. Unless governing law permits otherwise, you must contact a Goldman Sachs entity in your home jurisdiction if you want to use our services in effecting a transaction in the securities mentioned in this material. Note: Options are not suitable for all investors. Please ensure that you have read and understood the current options disclosure document before entering into any options transactions.