Carroll - 1979 - Three-Dimensional Conceptual Model of Corporate Performance

1978-More-The Levenberg-Marquardt algorithm-implementation and theory

but if D is diagonal, then E has axes along the coordinate directions and the length of the ith semi-axis is A/d..

i

We now consider the solution of (2.1) in some generality, and thus the problem (2.3) min{IIf+Jpll : IIDpll~ A} The basis for the Levenberg-Marquardt = p(l) for some

THE LEVE_~BERG-MARQUARDT IMPLEMENTATION

ALGORITHM:

AND THEORY

Jorge J. Mor~

i.

Introduction Let F: R n ÷ R m be continuously differentiable, of and consider the nonlinear least

4

ilI] I

where D~ = x½~TD~ is still a diagonal matrix and R is a (possibly singular) upper triangular matrix of order n.

108

In the second stage, compute the QR decomposition (3.4).

squares problem of finding a local minimizer

(1.1)

Levenberg numerical

I ~(x) = 7

专业投机原理(维可多.斯波朗迪)

专业投机原理维可多.斯波朗迪(著)出版者的话《专业投机原理》一书最初是由John Wiley&Sons出版公司出版的,在英语世界多年来一直畅销不衰,并被翻译成多国文字出版。

科文(香港)出版有限公司和宇航出版社于1999年引进该书的中文简体字版版权并在大陆出版,反响很好,几年来一再加印,因为最初翻译此书时参考的是台湾译本,故书中有些词汇的译法与现在大陆的通行译法有些出入。

故特在此说明,以供读者参考:1.Dow Jones书中译为“道琼”,通行泽法为“道琼斯”;2.Option书中译为“选择权”。

通行译法为“期权”;3. Real rate书中译为“实质利率”,通行译法为“实际利率”;4.Over the conter书中译为“店头市场”通行泽法为“柜台交易市场”;5.rediscount书中译为“重贴现”,通行译法为“再贴现”;6. Federal Reserve Board of Govermors书中泽为“联邦准备理事会”,通行译法为“联邦储备局”,其他如“联邦准备银行”(通行译法为“联邦储备银行”)、“联邦准备体系”(通行译法为“联邦储备体系”)也请读者注意;7. acknowledge书中译为“体认”,通行译法为“承认”。

另外,因英文原书为Ⅰ、Ⅱ两册,现合并为一本出版,故改称为上卷、下卷,正文中提及原书Ⅰ、Ⅱ处即为现译本的上、下卷,请读者注意。

本书将献给历史上最伟大的领袖,由一位女上与一位男士代表:伊丽莎白一世(Eliznbethl)英国女王(在位期间1555——1603)。

伊丽莎白继承王位时,国家背负庞大的债务。

她的才华表现在以独到的税收政策清偿债务:她使缴税成为一种自愿的行为!她曾经说过:“课税而被爱戴,并非男人所专有。

我将有始有终地受到子民的爱戴。

”在15年之内,她将国库转亏为盈,并为人民所热爱。

托马斯杰斐逊(Thomas Jeffersons)“独立宣言”的起草人与美国第三任总统.杰斐逊的领导哲学反映在“独立宣言”的前言中:“我们认为这是自明之理,人类生而平等,拥有天赋不可侵犯的权利,其中三者为生命、自由与追求快乐的权利。

钟耀祖 - 中国科学院深圳先进技术研究院

6.Chung YC, Duerk JL. Signal formation in echo shifted sequences, Magn Reson Med, 42(5): p.864-875, 1999.

7.Chung YC, Merkle EM, Lewin JS, et al. Fast T2-weighted imaging by PSIF at 0.2T for interventional MRI, Magn Reson Med, 42(2): p.335-344, 1999.

Direction

Fast MR imaging techniques, cardiovascular MR, vessel wall imaging and temperature imaging.

Achievements

Article

1.Ding Y,Chung YC, Simonetti OP, A Method to Assess Spatially-variant Noise in Dynamic MR Image Series, Magn Reson Med, vol.63(3), p.782-789, 2010.

Positions

Professor

照片

人社部2020—2021年每年培训农民工700万人次以上

山西农经//2020年11期会责任的过程是实现经济功能和社会功能的过程,也就是“双塔模型”互动的过程。

只有金字塔模型具备稳固的基底(经济责任和法律责任的履行),才能支撑起倒金字塔模型的高度(伦理责任和慈善责任的践行);只有倒金字塔模型呈现恰当的高度(适度的慈善责任),才能夯实金字塔模型的基础。

因此,农业企业在履行企业社会责任的过程中,应平衡二者之间的关系,确保双塔模型无论怎么变动和调整,始终保持平行、稳定的状态。

简言之,农业企业社会责任是指农业企业为实现经济功能和社会功能,以满足消费者、农村社区、农民以及政府等主要利益相关者的诉求,而对各主要利益相关者有选择地履行经济、法律、伦理和慈善责任的总和。

具体而言,农业企业社会责任有以下3层含义。

一是传统的价值链都强调经济功能,经济责任同样是农业企业社会责任的基础,其中提供质量安全的农产品是关键,具有基础性。

二是农业企业的“三农”本质决定其内嵌于农村社区,在维系、强化与农村社区互动、互融关系的过程中,践行着社会功能,其中伦理和慈善责任是农业企业实现社会功能的重点,具有自发性和持续性。

三是农业企业作为基础性、战略性产业的有效载体,在乡村振兴战略实施的背景下始终肩负着推动农业科技创新发展、带动农户增收、促进农业增产、推动农村增效的使命。

这是农业企业社会责任区别与一般企业社会责任的核心内容。

4结论与讨论自企业社会责任的概念提出以来,有关企业社会责任概念的界定一直争议不断,没有达成共识。

这是由企业社会责任本身的复杂性和内容的丰富性所决定的。

不同企业在盈利能力和资源、对社会和利益相关者的影响等方面都有所不同,因此企业社会责任的内容也不同。

要想厘清企业社会责任的内涵和范畴,就要抛开企业“同质性”的基本前提,根据企业的类型,从企业的产业特性入手,克服企业社会责任定义上的模糊性,使得研究具有可行性与可操作性。

鉴于此,基于乡村振兴战略视角,以农业企业的产业特性为逻辑起点,在分析讨论农业企业产业特性和新时代使命的基础上,构建农业企业社会责任模型,并对农业企业社会责任的内涵和外延进行界定。

IEC-61854架空线.隔离层的要求和检验

NORMEINTERNATIONALECEI IEC INTERNATIONALSTANDARD 61854Première éditionFirst edition1998-09Lignes aériennes –Exigences et essais applicables aux entretoisesOverhead lines –Requirements and tests for spacersCommission Electrotechnique InternationaleInternational Electrotechnical Commission Pour prix, voir catalogue en vigueurFor price, see current catalogue© IEC 1998 Droits de reproduction réservés Copyright - all rights reservedAucune partie de cette publication ne peut être reproduite niutilisée sous quelque forme que ce soit et par aucunprocédé, électronique ou mécanique, y compris la photo-copie et les microfilms, sans l'accord écrit de l'éditeur.No part of this publication may be reproduced or utilized in any form or by any means, electronic or mechanical,including photocopying and microfilm, without permission in writing from the publisher.International Electrotechnical Commission 3, rue de Varembé Geneva, SwitzerlandTelefax: +41 22 919 0300e-mail: inmail@iec.ch IEC web site http: //www.iec.chCODE PRIX PRICE CODE X– 2 –61854 © CEI:1998SOMMAIREPages AVANT-PROPOS (6)Articles1Domaine d'application (8)2Références normatives (8)3Définitions (12)4Exigences générales (12)4.1Conception (12)4.2Matériaux (14)4.2.1Généralités (14)4.2.2Matériaux non métalliques (14)4.3Masse, dimensions et tolérances (14)4.4Protection contre la corrosion (14)4.5Aspect et finition de fabrication (14)4.6Marquage (14)4.7Consignes d'installation (14)5Assurance de la qualité (16)6Classification des essais (16)6.1Essais de type (16)6.1.1Généralités (16)6.1.2Application (16)6.2Essais sur échantillon (16)6.2.1Généralités (16)6.2.2Application (16)6.2.3Echantillonnage et critères de réception (18)6.3Essais individuels de série (18)6.3.1Généralités (18)6.3.2Application et critères de réception (18)6.4Tableau des essais à effectuer (18)7Méthodes d'essai (22)7.1Contrôle visuel (22)7.2Vérification des dimensions, des matériaux et de la masse (22)7.3Essai de protection contre la corrosion (22)7.3.1Composants revêtus par galvanisation à chaud (autres queles fils d'acier galvanisés toronnés) (22)7.3.2Produits en fer protégés contre la corrosion par des méthodes autresque la galvanisation à chaud (24)7.3.3Fils d'acier galvanisé toronnés (24)7.3.4Corrosion causée par des composants non métalliques (24)7.4Essais non destructifs (24)61854 © IEC:1998– 3 –CONTENTSPage FOREWORD (7)Clause1Scope (9)2Normative references (9)3Definitions (13)4General requirements (13)4.1Design (13)4.2Materials (15)4.2.1General (15)4.2.2Non-metallic materials (15)4.3Mass, dimensions and tolerances (15)4.4Protection against corrosion (15)4.5Manufacturing appearance and finish (15)4.6Marking (15)4.7Installation instructions (15)5Quality assurance (17)6Classification of tests (17)6.1Type tests (17)6.1.1General (17)6.1.2Application (17)6.2Sample tests (17)6.2.1General (17)6.2.2Application (17)6.2.3Sampling and acceptance criteria (19)6.3Routine tests (19)6.3.1General (19)6.3.2Application and acceptance criteria (19)6.4Table of tests to be applied (19)7Test methods (23)7.1Visual examination (23)7.2Verification of dimensions, materials and mass (23)7.3Corrosion protection test (23)7.3.1Hot dip galvanized components (other than stranded galvanizedsteel wires) (23)7.3.2Ferrous components protected from corrosion by methods other thanhot dip galvanizing (25)7.3.3Stranded galvanized steel wires (25)7.3.4Corrosion caused by non-metallic components (25)7.4Non-destructive tests (25)– 4 –61854 © CEI:1998 Articles Pages7.5Essais mécaniques (26)7.5.1Essais de glissement des pinces (26)7.5.1.1Essai de glissement longitudinal (26)7.5.1.2Essai de glissement en torsion (28)7.5.2Essai de boulon fusible (28)7.5.3Essai de serrage des boulons de pince (30)7.5.4Essais de courant de court-circuit simulé et essais de compressionet de traction (30)7.5.4.1Essai de courant de court-circuit simulé (30)7.5.4.2Essai de compression et de traction (32)7.5.5Caractérisation des propriétés élastiques et d'amortissement (32)7.5.6Essais de flexibilité (38)7.5.7Essais de fatigue (38)7.5.7.1Généralités (38)7.5.7.2Oscillation de sous-portée (40)7.5.7.3Vibrations éoliennes (40)7.6Essais de caractérisation des élastomères (42)7.6.1Généralités (42)7.6.2Essais (42)7.6.3Essai de résistance à l'ozone (46)7.7Essais électriques (46)7.7.1Essais d'effet couronne et de tension de perturbations radioélectriques..467.7.2Essai de résistance électrique (46)7.8Vérification du comportement vibratoire du système faisceau/entretoise (48)Annexe A (normative) Informations techniques minimales à convenirentre acheteur et fournisseur (64)Annexe B (informative) Forces de compression dans l'essai de courantde court-circuit simulé (66)Annexe C (informative) Caractérisation des propriétés élastiques et d'amortissementMéthode de détermination de la rigidité et de l'amortissement (70)Annexe D (informative) Contrôle du comportement vibratoire du systèmefaisceau/entretoise (74)Bibliographie (80)Figures (50)Tableau 1 – Essais sur les entretoises (20)Tableau 2 – Essais sur les élastomères (44)61854 © IEC:1998– 5 –Clause Page7.5Mechanical tests (27)7.5.1Clamp slip tests (27)7.5.1.1Longitudinal slip test (27)7.5.1.2Torsional slip test (29)7.5.2Breakaway bolt test (29)7.5.3Clamp bolt tightening test (31)7.5.4Simulated short-circuit current test and compression and tension tests (31)7.5.4.1Simulated short-circuit current test (31)7.5.4.2Compression and tension test (33)7.5.5Characterisation of the elastic and damping properties (33)7.5.6Flexibility tests (39)7.5.7Fatigue tests (39)7.5.7.1General (39)7.5.7.2Subspan oscillation (41)7.5.7.3Aeolian vibration (41)7.6Tests to characterise elastomers (43)7.6.1General (43)7.6.2Tests (43)7.6.3Ozone resistance test (47)7.7Electrical tests (47)7.7.1Corona and radio interference voltage (RIV) tests (47)7.7.2Electrical resistance test (47)7.8Verification of vibration behaviour of the bundle-spacer system (49)Annex A (normative) Minimum technical details to be agreed betweenpurchaser and supplier (65)Annex B (informative) Compressive forces in the simulated short-circuit current test (67)Annex C (informative) Characterisation of the elastic and damping propertiesStiffness-Damping Method (71)Annex D (informative) Verification of vibration behaviour of the bundle/spacer system (75)Bibliography (81)Figures (51)Table 1 – Tests on spacers (21)Table 2 – Tests on elastomers (45)– 6 –61854 © CEI:1998 COMMISSION ÉLECTROTECHNIQUE INTERNATIONALE––––––––––LIGNES AÉRIENNES –EXIGENCES ET ESSAIS APPLICABLES AUX ENTRETOISESAVANT-PROPOS1)La CEI (Commission Electrotechnique Internationale) est une organisation mondiale de normalisation composéede l'ensemble des comités électrotechniques nationaux (Comités nationaux de la CEI). La CEI a pour objet de favoriser la coopération internationale pour toutes les questions de normalisation dans les domaines de l'électricité et de l'électronique. A cet effet, la CEI, entre autres activités, publie des Normes internationales.Leur élaboration est confiée à des comités d'études, aux travaux desquels tout Comité national intéressé par le sujet traité peut participer. Les organisations internationales, gouvernementales et non gouvernementales, en liaison avec la CEI, participent également aux travaux. La CEI collabore étroitement avec l'Organisation Internationale de Normalisation (ISO), selon des conditions fixées par accord entre les deux organisations.2)Les décisions ou accords officiels de la CEI concernant les questions techniques représentent, dans la mesuredu possible un accord international sur les sujets étudiés, étant donné que les Comités nationaux intéressés sont représentés dans chaque comité d’études.3)Les documents produits se présentent sous la forme de recommandations internationales. Ils sont publiéscomme normes, rapports techniques ou guides et agréés comme tels par les Comités nationaux.4)Dans le but d'encourager l'unification internationale, les Comités nationaux de la CEI s'engagent à appliquer defaçon transparente, dans toute la mesure possible, les Normes internationales de la CEI dans leurs normes nationales et régionales. Toute divergence entre la norme de la CEI et la norme nationale ou régionale correspondante doit être indiquée en termes clairs dans cette dernière.5)La CEI n’a fixé aucune procédure concernant le marquage comme indication d’approbation et sa responsabilitén’est pas engagée quand un matériel est déclaré conforme à l’une de ses normes.6) L’attention est attirée sur le fait que certains des éléments de la présente Norme internationale peuvent fairel’objet de droits de propriété intellectuelle ou de droits analogues. La CEI ne saurait être tenue pour responsable de ne pas avoir identifié de tels droits de propriété et de ne pas avoir signalé leur existence.La Norme internationale CEI 61854 a été établie par le comité d'études 11 de la CEI: Lignes aériennes.Le texte de cette norme est issu des documents suivants:FDIS Rapport de vote11/141/FDIS11/143/RVDLe rapport de vote indiqué dans le tableau ci-dessus donne toute information sur le vote ayant abouti à l'approbation de cette norme.L’annexe A fait partie intégrante de cette norme.Les annexes B, C et D sont données uniquement à titre d’information.61854 © IEC:1998– 7 –INTERNATIONAL ELECTROTECHNICAL COMMISSION––––––––––OVERHEAD LINES –REQUIREMENTS AND TESTS FOR SPACERSFOREWORD1)The IEC (International Electrotechnical Commission) is a worldwide organization for standardization comprisingall national electrotechnical committees (IEC National Committees). The object of the IEC is to promote international co-operation on all questions concerning standardization in the electrical and electronic fields. To this end and in addition to other activities, the IEC publishes International Standards. Their preparation is entrusted to technical committees; any IEC National Committee interested in the subject dealt with may participate in this preparatory work. International, governmental and non-governmental organizations liaising with the IEC also participate in this preparation. The IEC collaborates closely with the International Organization for Standardization (ISO) in accordance with conditions determined by agreement between the two organizations.2)The formal decisions or agreements of the IEC on technical matters express, as nearly as possible, aninternational consensus of opinion on the relevant subjects since each technical committee has representation from all interested National Committees.3)The documents produced have the form of recommendations for international use and are published in the formof standards, technical reports or guides and they are accepted by the National Committees in that sense.4)In order to promote international unification, IEC National Committees undertake to apply IEC InternationalStandards transparently to the maximum extent possible in their national and regional standards. Any divergence between the IEC Standard and the corresponding national or regional standard shall be clearly indicated in the latter.5)The IEC provides no marking procedure to indicate its approval and cannot be rendered responsible for anyequipment declared to be in conformity with one of its standards.6) Attention is drawn to the possibility that some of the elements of this International Standard may be the subjectof patent rights. The IEC shall not be held responsible for identifying any or all such patent rights. International Standard IEC 61854 has been prepared by IEC technical committee 11: Overhead lines.The text of this standard is based on the following documents:FDIS Report on voting11/141/FDIS11/143/RVDFull information on the voting for the approval of this standard can be found in the report on voting indicated in the above table.Annex A forms an integral part of this standard.Annexes B, C and D are for information only.– 8 –61854 © CEI:1998LIGNES AÉRIENNES –EXIGENCES ET ESSAIS APPLICABLES AUX ENTRETOISES1 Domaine d'applicationLa présente Norme internationale s'applique aux entretoises destinées aux faisceaux de conducteurs de lignes aériennes. Elle recouvre les entretoises rigides, les entretoises flexibles et les entretoises amortissantes.Elle ne s'applique pas aux espaceurs, aux écarteurs à anneaux et aux entretoises de mise à la terre.NOTE – La présente norme est applicable aux pratiques de conception de lignes et aux entretoises les plus couramment utilisées au moment de sa rédaction. Il peut exister d'autres entretoises auxquelles les essais spécifiques décrits dans la présente norme ne s'appliquent pas.Dans de nombreux cas, les procédures d'essai et les valeurs d'essai sont convenues entre l'acheteur et le fournisseur et sont énoncées dans le contrat d'approvisionnement. L'acheteur est le mieux à même d'évaluer les conditions de service prévues, qu'il convient d'utiliser comme base à la définition de la sévérité des essais.La liste des informations techniques minimales à convenir entre acheteur et fournisseur est fournie en annexe A.2 Références normativesLes documents normatifs suivants contiennent des dispositions qui, par suite de la référence qui y est faite, constituent des dispositions valables pour la présente Norme internationale. Au moment de la publication, les éditions indiquées étaient en vigueur. Tout document normatif est sujet à révision et les parties prenantes aux accords fondés sur la présente Norme internationale sont invitées à rechercher la possibilité d'appliquer les éditions les plus récentes des documents normatifs indiqués ci-après. Les membres de la CEI et de l'ISO possèdent le registre des Normes internationales en vigueur.CEI 60050(466):1990, Vocabulaire Electrotechnique International (VEI) – Chapitre 466: Lignes aériennesCEI 61284:1997, Lignes aériennes – Exigences et essais pour le matériel d'équipementCEI 60888:1987, Fils en acier zingué pour conducteurs câblésISO 34-1:1994, Caoutchouc vulcanisé ou thermoplastique – Détermination de la résistance au déchirement – Partie 1: Eprouvettes pantalon, angulaire et croissantISO 34-2:1996, Caoutchouc vulcanisé ou thermoplastique – Détermination de la résistance au déchirement – Partie 2: Petites éprouvettes (éprouvettes de Delft)ISO 37:1994, Caoutchouc vulcanisé ou thermoplastique – Détermination des caractéristiques de contrainte-déformation en traction61854 © IEC:1998– 9 –OVERHEAD LINES –REQUIREMENTS AND TESTS FOR SPACERS1 ScopeThis International Standard applies to spacers for conductor bundles of overhead lines. It covers rigid spacers, flexible spacers and spacer dampers.It does not apply to interphase spacers, hoop spacers and bonding spacers.NOTE – This standard is written to cover the line design practices and spacers most commonly used at the time of writing. There may be other spacers available for which the specific tests reported in this standard may not be applicable.In many cases, test procedures and test values are left to agreement between purchaser and supplier and are stated in the procurement contract. The purchaser is best able to evaluate the intended service conditions, which should be the basis for establishing the test severity.In annex A, the minimum technical details to be agreed between purchaser and supplier are listed.2 Normative referencesThe following normative documents contain provisions which, through reference in this text, constitute provisions of this International Standard. At the time of publication of this standard, the editions indicated were valid. All normative documents are subject to revision, and parties to agreements based on this International Standard are encouraged to investigate the possibility of applying the most recent editions of the normative documents indicated below. Members of IEC and ISO maintain registers of currently valid International Standards.IEC 60050(466):1990, International Electrotechnical vocabulary (IEV) – Chapter 466: Overhead linesIEC 61284:1997, Overhead lines – Requirements and tests for fittingsIEC 60888:1987, Zinc-coated steel wires for stranded conductorsISO 34-1:1994, Rubber, vulcanized or thermoplastic – Determination of tear strength – Part 1: Trouser, angle and crescent test piecesISO 34-2:1996, Rubber, vulcanized or thermoplastic – Determination of tear strength – Part 2: Small (Delft) test piecesISO 37:1994, Rubber, vulcanized or thermoplastic – Determination of tensile stress-strain properties– 10 –61854 © CEI:1998 ISO 188:1982, Caoutchouc vulcanisé – Essais de résistance au vieillissement accéléré ou à la chaleurISO 812:1991, Caoutchouc vulcanisé – Détermination de la fragilité à basse températureISO 815:1991, Caoutchouc vulcanisé ou thermoplastique – Détermination de la déformation rémanente après compression aux températures ambiantes, élevées ou bassesISO 868:1985, Plastiques et ébonite – Détermination de la dureté par pénétration au moyen d'un duromètre (dureté Shore)ISO 1183:1987, Plastiques – Méthodes pour déterminer la masse volumique et la densitérelative des plastiques non alvéolairesISO 1431-1:1989, Caoutchouc vulcanisé ou thermoplastique – Résistance au craquelage par l'ozone – Partie 1: Essai sous allongement statiqueISO 1461,— Revêtements de galvanisation à chaud sur produits finis ferreux – Spécifications1) ISO 1817:1985, Caoutchouc vulcanisé – Détermination de l'action des liquidesISO 2781:1988, Caoutchouc vulcanisé – Détermination de la masse volumiqueISO 2859-1:1989, Règles d'échantillonnage pour les contrôles par attributs – Partie 1: Plans d'échantillonnage pour les contrôles lot par lot, indexés d'après le niveau de qualité acceptable (NQA)ISO 2859-2:1985, Règles d'échantillonnage pour les contrôles par attributs – Partie 2: Plans d'échantillonnage pour les contrôles de lots isolés, indexés d'après la qualité limite (QL)ISO 2921:1982, Caoutchouc vulcanisé – Détermination des caractéristiques à basse température – Méthode température-retrait (essai TR)ISO 3417:1991, Caoutchouc – Détermination des caractéristiques de vulcanisation à l'aide du rhéomètre à disque oscillantISO 3951:1989, Règles et tables d'échantillonnage pour les contrôles par mesures des pourcentages de non conformesISO 4649:1985, Caoutchouc – Détermination de la résistance à l'abrasion à l'aide d'un dispositif à tambour tournantISO 4662:1986, Caoutchouc – Détermination de la résilience de rebondissement des vulcanisats––––––––––1) A publierThis is a preview - click here to buy the full publication61854 © IEC:1998– 11 –ISO 188:1982, Rubber, vulcanized – Accelerated ageing or heat-resistance testsISO 812:1991, Rubber, vulcanized – Determination of low temperature brittlenessISO 815:1991, Rubber, vulcanized or thermoplastic – Determination of compression set at ambient, elevated or low temperaturesISO 868:1985, Plastics and ebonite – Determination of indentation hardness by means of a durometer (Shore hardness)ISO 1183:1987, Plastics – Methods for determining the density and relative density of non-cellular plasticsISO 1431-1:1989, Rubber, vulcanized or thermoplastic – Resistance to ozone cracking –Part 1: static strain testISO 1461, — Hot dip galvanized coatings on fabricated ferrous products – Specifications1)ISO 1817:1985, Rubber, vulcanized – Determination of the effect of liquidsISO 2781:1988, Rubber, vulcanized – Determination of densityISO 2859-1:1989, Sampling procedures for inspection by attributes – Part 1: Sampling plans indexed by acceptable quality level (AQL) for lot-by-lot inspectionISO 2859-2:1985, Sampling procedures for inspection by attributes – Part 2: Sampling plans indexed by limiting quality level (LQ) for isolated lot inspectionISO 2921:1982, Rubber, vulcanized – Determination of low temperature characteristics –Temperature-retraction procedure (TR test)ISO 3417:1991, Rubber – Measurement of vulcanization characteristics with the oscillating disc curemeterISO 3951:1989, Sampling procedures and charts for inspection by variables for percent nonconformingISO 4649:1985, Rubber – Determination of abrasion resistance using a rotating cylindrical drum deviceISO 4662:1986, Rubber – Determination of rebound resilience of vulcanizates–––––––––1) To be published.。

Literature Review on Corporate Social Responsibili

Huixi RENGuangdong Polytechnic of Science and TechnologyAbstract: Corporate social responsibility has recently been a topic of concern indomestic and foreign academic circles. The author sorted out the relevant literatureon corporate social responsibility from the world, through sorting out early interna-tional research on social responsibility theory, other corporate social responsibilitytheoretical systems with characteristics of different periods, foreign interpretationsof corporate social responsibility in developing countries, and domestic scholarsThe construction of domestic corporate social responsibility theory system andother documents have studied the current situation of corporate social responsibilityresearch, and summarized the domestic impact of corporate social responsibility All Rights Reserved.research on enterprises and society, and finally proposed the future research direc-tion of corporate social responsibility.Keywords: Corporate Social Responsibility; Corporate Management; Social Con-tributionDOI: 10.47297/wspiedWSP2516-250001.20200408In the early 20th century, with the increasing number of enterprises, more and more related learning about enterprise management, the academic circles recog-nized the origin of corporate social responsibility theory is the United States. Inhundreds of years, the theory of corporate social responsibility has been developingand maturing.About the author: Huixi REN. Guangdong Polytechnic of Science and Technology.510640. Lecturer. Master Degree.Fund Project: 2019 school-level education and teaching reform research and practiceproject, construction and implementation of vocational college manager trainer model forprofessional groups and enterprise groups based on High-level vocational schools con-struction plans (JG201928);2019 high-level vocational schools construction plans (school-level), Golden Course (HighQuality Course) of Category Management (J61101002013).Journal of International Education and Development Vol.4 No.8 20201.Theoretical Research in the 20th Century(1) Early Research on Corporate Social Responsibility TheoryC lark first proposed the need for corporate social responsibility in the TheChanging Basis of Economic Responsibility in 1916. He believed that the econom-ic development of society should be supported by corporate social responsibility.However, the Clark does not give a clear definition of what corporate social re-sponsibility is, and only the voluntary charitable behavior of the enterprise is men-tioned in the article as the source of social responsibility. Bowen book Social Re-sponsibility of the Businessman in 1953 proposed the definition of social responsi-bility of businessmen. He believed that businessmen should consider the socialgoals and social values of enterprises when making decisions or taking actions. Theearliest theory of social responsibility only vaguely mentioned what enterprisesshould do to give back to society so that enterprises can survive and develop better.(2) A Study on Corporate Social Responsibility in the Period of CharityDavis put forward the basic theory of responsibility in 1960, that enterprises can not only enjoy the right to earn profits, but avoid fulfilling their responsibilitiesAll Rights Reserved.to society, otherwise enterprises will gradually lose their rights. Economists MiltonFriedman in 1970 that the very foundations of a free society would be destroyed ifthe managers of companies were to make money. If enterprises want to ensure theirsurvival in society and maximize profits, they need to abide by some social rules.The theory of social responsibility in this period mainly holds that enterprisesthemselves need to do more charity in addition to earning profits and play the roleof beautifying society.2. Research on Corporate Social Responsibility by Chinese ScholarsIn the early 21st century, The dimensions of Chinese scholars’research on corporate social responsibility have gradually increased, Wang Yan (2001) studiedcorporate social responsibility from the perspective of jurisprudence. In China,Corporate social responsibility should be based on ethics, protected and regulatedby law, This is also the responsibility of the enterprise for interest-related organiza-tions. 2004, Hu Xiaoquan proposed, Enterprises can follow the government’s “sus-tainable development” theory, Protecting the environment from a range of activities,including production, manufacturing, marketing, Fulfil your responsibilities. 2007,Yang believes, Corporate social responsibility can help enterprises to tap externaland internal new competitive advantages. Li Youhuan (2007) conducted a literatureLiterature Review on Corporate Social Responsibility review and analysis of key factors in the study of corporate society in China at thattime, Considering that most of the domestic research on corporate social responsi-bility directly cited the foreign research results, In the enterprise practice, there isno improvement and innovation according to the enterprise characteristics of ourcountry. Based on Carroll pyramid model, According to the characteristics of Chi-nese companies, Further proposed and refined corporate social responsibility. WangYing (2008) in analyzing the stakeholders of the enterprise, It is pointed out that thedisclosure of corporate social responsibility information in China is relatively de-layed. 2011, Through empirical research, It is found that most of the research oncorporate social responsibility in China pays more attention to resource utilizationor industrial competition. Xiao Red Army, Li Weiyang (2013) believes that Chineseenterprises should keep up with the times, Corporate responsibility shifted from asingle dimension to a comprehensive level, From the corporate perspective to themacro perspective, From forced charity to active social value creation. 2020, YuXinyu’s literature review lists studies on female managers and corporate social re-sponsibility, It is believed that female senior managers can promote the implemen-tation of corporate social responsibility.In general, the research of Chinese corporate social responsibility is still in theAll Rights Reserved.primary stage. It is necessary to carry out more localization research combined withChinese characteristics, perfect the theory of local corporate social responsibility,and apply it to Chinese enterprises.Works Cited[1] Clark, J M. (1916).The Changing Basis of Economic Responsibility. Journal ofPolitical Economy,1916,24, 209-29.[2] Bowen, H. R. (1953). Social Responsibility of the Businessman. NewYork: Har-per,1953, 31.[3] Davis, K. (1960). Can Business Afford to Ignore Corporate Social Responsibilities?California Management Review,1960,2(3), 70-76.[4] Friedman, M. (1970). The Social Responsibility of Business Is to Increase Its Prof-its Material. The New York Times Magazine, 1970(9).[5] Carroll, A. (1979). A Three-Dimensional Conceptual Model of Corporate Per-formance. Academy of Management Review,1979,4 (4), 497-505.[6] Carroll, A. (1999.) Corporate Social Responsibility -Evolution of a DefinitionalConstruction. Business and Society,1999 (3), 268- 95.[7] Freeman, R. E. and Evan, W. M. (1990). Corporate governance: A stakeholderinterpretation. Journal of Behavioral Economics,1990,19(4), 337-59.[8] Hill, C. and Jones. T. M. (1992). STAKEHOLDER-AGENCY THEORY. Jour-nal of Management Studies,1992,29(2), 131-54.Journal of International Education and Development Vol.4 No.8 2020[9] Yang, C. (1982). Xin Shi Qi Shang Ye Gong Zuo De She Hui Di Wei He She HuiZe Ren (Commercial work in the new period of social status and social responsibil-ity), Business Research, 1982 (2), 2-5.[10] Wang, Q. (1987). Shang Ye Qi Ye De She Hui Ze Ren (Social responsibility ofcommercial enterprises), Journal of Jiangsu Institute of Commercial Management,1987 (2), 21-23.[11] Wang, Yan. (2001). Qi Ye She Hui Ze Ren Ji Qi Fa Li Xue Yan Jiu (CorporateSocial Responsibility and Its Jurisprudence Research), J ournal of Harbin Instituteof Technology (Social Science Edition), 2001 (3), 104-09.[12] Hu, X. (2004). Qi Ye Ke Chi Xu Fa Zhan Yu Qi Ye She Hui Ze Ren (CorporateSustainable Development and Corporate Social Responsibility), Journal ofChongqing University of Posts and Telecommunications (Social Science Edition),2004 (2), 123-25.[13] Yang, J. (2007). Zi Yuan Ji Chu Li Lun Shi Jiao Xia De Qi Ye She Hui Ze Ren(Corporate Social Responsibility from the Perspective of Resource-based Theory).Theory Guide, 2007 (9), 91-94.[14] Wang, Ying. (2008). Qi Ye She Hui Ze Ren Kuai Ji Xin Xi Pi Lu Yan Jiu (Re-search on Corporate Social Responsibility Accounting Information Disclosure).Capital University of Economics, 2008.[15] Li, Y. (2007). Qi Ye She Hui Ze Ren Yan Jiu (Corporate Social ResponsibilityResearch). Northwestern University Doctoral Thesis. 2007 (16).[16] Xu, E and Xi, Y. (2011). Guo Nei Qi Ye She Hui Ze Ren Yan Jiu De Xian All Rights Reserved.Zhuang Yu Fa Zhan Qu Shi (The status quo and development trend of domesticcorporate social responsibility research). Management Scientist (Academic Edi-tion), 2011 (1), 48-68.[17] Xiao. H and Li, W. (2013). Guo Wai Qi Ye She Hui Ze Ren Yan Jiu Xin Jin Zhan(New progress in the study of corporate social responsibility abroad). EconomicManagement, 2013 (9), 179-88.[18] Wang, T. (2016). Gong Xiang Jia Zhi Shi Jiao Xia Qi Ye She Hui Ze Ren DeZhuan Xing Yu Ji Yu – Yi Ying Te Er (Zhong Guo) You Xian Gong Si Wei Li(The Transformation and Opportunities of Corporate Social Responsibility fromthe Perspective of Shared Value——Taking Intel (China) Co., Ltd. as an exam-ple). Yunnan University of Finance and Economics, 2016.[19] Yu, X. (2020). Nv Xing Gao Guan Dui Qi Ye She Hui Ze Ren De Ying XiangWen Xian Zong Shu (A Literature Review of the Impact of Female Executives onCorporate Social Responsibility). China Management Informationization, 2020(13), 70-72.。

基于CSR模型的我国国有企业社会责任分析

2008年9月伊始,知名乳制品企业三鹿含有三聚氰胺的婴幼儿“毒”奶粉事件爆发,震惊中国,引发了国家对国内奶制品行业的大规模检查,令人吃惊的是,不少知名品牌均添加有不同分量的三聚氰胺,国内奶制品企业社会责任的集体缺失让广大消费者对国产奶制品失去信心。

由此,企业社会责任问题又引起了社会广泛的高度关注。

本文在阐述企业社会责任(Corporate Social Responsibility ,缩写为CSR )的基本理论基础上,运用模型分析企业社会责任,并进行扩展,探讨我国国有企业所要承担的社会责任。

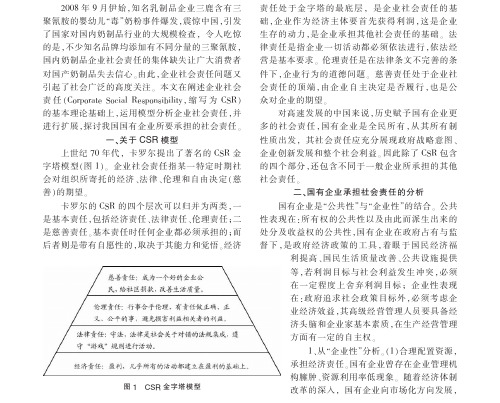

一、关于CSR 模型上世纪70年代,卡罗尔提出了著名的CSR 金字塔模型(图1)。

企业社会责任指某一特定时期社会对组织所寄托的经济、法律、伦理和自由决定(慈善)的期望。

卡罗尔的CSR 的四个层次可以归并为两类,一是基本责任,包括经济责任、法律责任、伦理责任;二是慈善责任。

基本责任时任何企业都必须承担的;而后者则是带有自愿性的,取决于其能力和觉悟。

经济责任处于金字塔的最底层,是企业社会责任的基础,企业作为经济主体要首先获得利润,这是企业生存的动力,是企业承担其他社会责任的基础。

法律责任是指企业一切活动都必须依法进行,依法经营是基本要求。

伦理责任是在法律条文不完善的条件下,企业行为的道德问题。

慈善责任处于企业社会责任的顶端,由企业自主决定是否履行,也是公众对企业的期望。

对高速发展的中国来说,历史赋予国有企业更多的社会责任,国有企业是全民所有,从其所有制性质出发,其社会责任应充分展现政府战略意图、企业创新发展和整个社会利益。

因此除了CSR 包含的四个部分,还包含不同于一般企业所承担的其他社会责任。

二、国有企业承担社会责任的分析国有企业是“公共性”与“企业性”的结合。

公共性表现在:所有权的公共性以及由此而派生出来的处分及收益权的公共性,国有企业在政府占有与监督下,是政府经济政策的工具,着眼于国民经济福利提高、国民生活质量改善、公共设施提供等,若利润目标与社会利益发生冲突,必须在一定程度上舍弃利润目标;企业性表现在:政府追求社会政策目标外,必须考虑企业经济效益,其高级经营管理人员要具备经济头脑和企业家基本素质,在生产经营管理方面有一定的自主权。

基于战略视角的企业社会责任问题思考

基于战略视角的企业社会责任问题思考摘要:现代社会中,企业社会责任日益重要,受到越来越多的关注。

企业应从战略的高度来认识企业社会责任问题,将履行社会责任视为与产品、价格、人力资源同等重要的新型战略。

塑造良好的企业文化和品牌形象,更加有效地整合各种资源,创造优良的内外部环境,谋求长远、持续的战略利益,从而打造企业的社会责任竞争力,才能获取竞争优势,保证企业的可持续发展。

关键词:企业社会责任战略管理可持续发展一、企业社会责任的起源与涵义企业社会责任(corporate social responsibility,简称csr)研究始于股东利益与其他社会主体利益之间的冲突。

在过去的近一百年中,企业社会责任已由一个狭隘的边缘概念逐渐发展成为一个复杂的多维概念,成为现代企业决策理论中的重要组成部分。

1924年,英国学者oliver sheldon在其著作《the philosophy of management》中正式提出了企业社会责任的概念,他指出企业应该为其影响到的其他实体、社会和环境的所有行为负责。

howardr.bowen在《social responsibility of the business》一书中,认为“企业的社会责任是指商人按照社会的目标和价值,向有关政府靠拢、做出相应的决策、采取理想的具体行动的义务。

”bowen 使企业社会责任正式走进人们的视野,被认为是开创了现代企业社会责任概念研究的创始者,因此被尊称为“企业社会责任之父”。

对企业社会责任研究做出重大贡献的学者是carroll,在《athree-dimensional conceptual model of corporate performance》一文中carroll把企业社会责任定义为4个方面的责任,即生产、盈利及满足消费者需求的经济责任,在法律范围内履行其经济责任的法律责任,遵守社会准则、规范和价值观的伦理责任,以及具有坚定意志和慈爱心怀的自愿责任。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

497

This content downloaded from 129.234.252.67 on Wed, 30 Sep 2015 13:21:17 UTC All use subject to JSTOR Terms and Conditions

to the objectives or motives that should be given weight by business in additionto [emphasis added]

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at /page/ info/about/policies/terms.jsp JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact support@.

A Three-Dimensional Conceptual Model of Corporate Performance Author(s): Archie B. Carroll Source: The Academy of Management Review, Vol. 4, No. 4 (Oct., 1979), pp. 497-505 Published by: Academy of Management Stable URL: /stable/257850 Accessed: 30-09-2015 13:21 UTC

Academy of Management is collaborating with JSTOR to digitize, preserve and extend access to The Academy of Management Review.

ห้องสมุดไป่ตู้

This content downloaded from 129.234.252.67 on Wed, 30 Sep 2015 13:21:17 UTC All use subject to JSTOR Terms and Conditions

conceptualizing social responsibility as something a firm considers over and above economic and legal criteria. Representative of this view is Henry Manne, who has argued "Another aspect of any workable definition of corporate social responsibility is that the behavior of the firms must be voluntary" [Manne & Wallich, 1972, p. 5, emphasis added]. Another approach to the question of what social responsibility means involves a definition simply listing the areas in which business is viewed as having a responsibility. For example, Hay, Gray, and Gates suggest that one aspect of social responsibility requires the firm to "make decisions and actually commit resources of various kinds in some of the following areas: pollution problems... poverty and racial discrimination problems.. . consumerism ... and other social problem areas" [1976, pp. 15-16]. One of the first approaches to encompass the spectrum of economic and non-economic concerns in defining social responsibility was the "three concentric circles" approach espoused by the Committee for Economic Development (CED) in 1971. The inner circle "includes the clear-cut basic responsibilities for the efficient execution of the economic function - products, jobs, and economic growth." The intermediate circle "encompasses a responsibility to exercise this economic function with a sensitive awareness of changing social values and priorities: for example, with respect to environmental conservation, hiring, and relations with emThe outer circle "outlines newly ployees.... emerging and still amorphous responsibilities that business should assume to become more broadly involved in actively improving the social environment" [Committee for Economic Development, 1971, p. 15]. The outer circle would refer to business helping with major social problems in society such as poverty and urban blight. This "widening circle" approach has also been adopted by Davis

Offeredhere is a conceptual model that comprehensivelydescribes essential aspects of corporatesocial performance.Thethree aspects of the model address majorquestions of concern to academics and managers alike: (1) Whatis included in corporatesocial responsibility?(2) Whatare the social issues the organization must address? and (3) What is the organization'sphilosophyor mode of social responsiveness?

those dealing with economic performance (e.g., profits)" [1975, p. 2]. Though McGuire and Backman see social responsibility as not only including but also moving beyond economic and legal considerations, others

Academy of Management Review 1979, Vol. 4, No. 4, 497-505

A

Three-Dimensional Conceptual Model of Corporate Performance

ARCHIE B. CARROLL University of Georgia

Joseph McGuire, in 1963, acknowledged the

[1954].

The idea of social responsibilities supposes thatthe corporationhas not only economic and legal oblito society gations, but also certainresponsibilities which extend beyondthese obligations[p. 144]. Arguing in a similar vein, Jules Backman has suggested that "social responsibility usually refers