Chapter 8 Capital Budgeting Decision Criteria:8章资本预算决策标准

资本预算

Accounting Rate of Return Criterion

What is the straight-line method annual depreciation? ($70,000 – $10,000) ÷5 = $12,000 What is the increased annual income? $20,000 – $12,000 = $8,000 What is the average investment? ($70,000 + $10,000) ÷2 = $40,000

Long-Term (Capital) Assets

Organizations have developed specific tools to control the acquisition and use of longterm assets for three reasons: 1 Organizations commit to long-term assets for extended periods of time. 2 The amount of capital committed is usually very large. 3 The long-term nature of capital assets creates technological risk for organizations.

Year 4: $1.2155 Year 3: $1.1576 Year 2: $1.1025 Year 1: $1.05 Year 0: $1.00

Present Value

What is the present value of money? It is the current monetary worth of an amount to be paid in the future under stated conditions of interest and compounding. Analysts call a future cash flow’s value at time zero its present value. The process of computing present value is called disconey

预算编制-资本预算1 精品002

investment, return, future value, present value, annuities, and required rate

of return.

Investment and Return

Present Value

What is the present value of $127.63 to be received 5 years from now when the rate of return is 5% per year? $100.00

PV = FV ÷(1 + r)n

Time Value of Money

The future value of money is the value that an amount invested today will be after a stated number of periods at a given rate of return. How much would an initial amount of $100 accumulate over five years when the rate of return is 5% per year?

Time Value of Money

A central concept in capital budgeting is the time value of money. Because money can earn a return, its value depends on the time period in which it is received. Amounts of money received at different periods of time must be converted to their value on a common date to be compared.

国际财务管理(原书第8版)教学课件Eun8e_Ch_018_PPT

-$1,000

$125

$250

$375

$500

0

1

2

3

4

The APV of the project under leverage is:

ST

APV

T t 1

StOCFt (1 τ) (1 Kud )t

T t 1

St τDt (1 id )t

T t 1

St τIt (1 id )t

STTVT (1 Kud )T

S0C0 S0RF0

S0CL0

T t 1

St LPt (1 id )t

Copyright © 2018 by the McGraw-Hill Companies, Inc. All rights reserved. 18-13

International Capital Budgeting

Chapter Eighteen

Copyright © 2018 by the McGraw-Hill Companies, Inc. All rights reserved.

Chapter Outline

• Review of Domestic Capital Budgeting • The Adjusted Present Value Model • Capital Budgeting from the Parent Firm’s

It is incremental interest

expense is the marginal tax rate

CapitalBudgeting(ppt47).pptx

of return.

2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kappter 8

2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

8- 1

Learning Objective 1

u Organizations commit to long-term assets for extended periods of time.

u The amount of capital committed is usually very large.

u The long-term nature of capital assets creates technological risk for organizations.

2001 Prentice Hall Business Publishing Management Accounting, 3/E, Atkinson, Banker, Kaplan, and Young

8- 3

Long-Term (Capital) Assets

Organizations have developed specific tools to control the acquisition and use of longterm assets for three reasons:

管理会计双语版总结

Static budget Flexible budget Static budget variance

Sales volume variance Flexible budget variance

Favorable variance and unfavorable variance Management by exception

16

Types of Problems

A. Equipment Replacement

Sunk Costs & Depreciation

B. Special Order

Fixed Cost & Opportunity Costs

C. Outsourcing: Make or Buy Decision

Comparison of traditional and ABC overhead allocation

6

Major Points of Cost Allocation

1 2 3

4

Why allocate? How much to allocate?

Allocate to whom? How to allocate?

7

Chapter 5 : Cost Behavior

Common cost behavior patterns

Fixed costs : think as total Variable costs : think on a per-unit basis Relevant range

Mixed costs and its separation

2

Chapter 2 :Classifying Costs

managerial accounting

Step 2: Compute the payback period. Using the annual net cash inflow from above, the payback period can be determined as follows: Cost of the new equipment . . . . . . . . . . . . . . $80,000 Less salvage value of old equipment . . . . . . 5,000 Investment required . . . . . . . . . . . . . . . . . . . . . $75,000 Payback period = = Investment required Annual net cash inflow $75,000 = 2.5 years $30,000

Evaluation of the Payback Method

To illustrate, refer back to Example A on the previous page. Machine B has a shorter payback period than machine A, but it has a useful life of only 5 years rather than 10 years for machine A. Machine B would have to be purchased twice—once immediately and then again after the fifth year—to provide the same service as just one machine A.

罗斯公司理财原书第七版全套Excel Solutions (38)

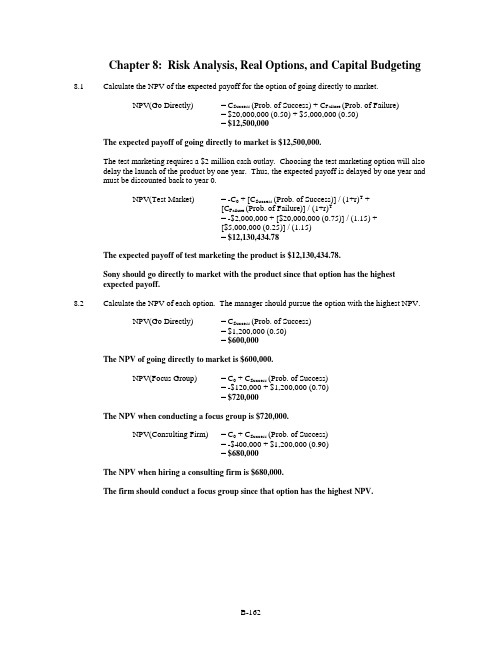

Chapter 8: Risk Analysis, Real Options, and Capital Budgeting 8.1Calculate the NPV of the expected payoff for the option of going directly to market.NPV(Go Directly) = C Success (Prob. of Success) + C Failure (Prob. of Failure)= $20,000,000 (0.50) + $5,000,000 (0.50)= $12,500,000The expected payoff of going directly to market is $12,500,000.The test marketing requires a $2 million cash outlay. Choosing the test marketing option will also delay the launch of the product by one year. Thus, the expected payoff is delayed by one year and must be discounted back to year 0.NPV(Test Market) = -C0 + [C Success (Prob. of Success)] / (1+r)T +[C Failure (Prob. of Failure)] / (1+r)T= -$2,000,000 + [$20,000,000 (0.75)] / (1.15) +[$5,000,000 (0.25)] / (1.15)= $12,130,434.78The expected payoff of test marketing the product is $12,130,434.78.Sony should go directly to market with the product since that option has the highestexpected payoff.8.2Calculate the NPV of each option. The manager should pursue the option with the highest NPV.NPV(Go Directly) = C Success (Prob. of Success)= $1,200,000 (0.50)= $600,000The NPV of going directly to market is $600,000.NPV(Focus Group) = C0 + C Success (Prob. of Success)= -$120,000 + $1,200,000 (0.70)= $720,000The NPV when conducting a focus group is $720,000.NPV(Consulting Firm) = C0 + C Success (Prob. of Success)= -$400,000 + $1,200,000 (0.90)= $680,000The NPV when hiring a consulting firm is $680,000.The firm should conduct a focus group since that option has the highest NPV.8.3Recommend the strategy that has the highest NPV.NPV(Lower Prices) = C Success (Prob. of Success) + C Failure (Prob. of Failure)= -$1,300,000 (0.55) - $1,850,000 (0.45)= -$1,547,500NPV(Lobbyist) = C0 + C Success (Prob. of Success) + C Failure (Prob. of Failure)= -$800,000 - $0 (0.75) - $2,000,000 (0.25)= -$1,300,000The CFO should hire the lobbyist since that option has the highest NPV.8.4Since the NPV of Research is greater than that of no research, based on expected outcomes, B&Bshould go directly to market.$3 million at t = 0Note: Research = –1 million investment + 0.7 * (26.087) if successful + 0.3 * (2.6087) if unsuccessful No Research = 0.55 * (30) if successful + 0.45 * (3) if unsuccessful8.5Carl should have taken the $5,000.Expected return for 1% of movie profits is $3,000. Since only good scripts are made into movies and only a good movie would make a profit: (10% x 30% x $10 mil x 1%)Movie studio decision tree:B-1648.6 Apply the accounting profit break-even point (BEP) formula and solve for the sales price, x, thatallows the firm to break even when producing 20,000 calculators. In order for the firm to breakeven, the revenues from the calculator sales (number of calculators sold sales price per unit)must equal the total annual cost of producing the calculators. Remember to include taxes in theanalysis.Variable costs = $15 per calculatorFixed costs = $900,000 per yearDepreciation = (Initial Investment / Economic Life)= ($600,000 / 5)= $120,000 per yearDivide the after-tax sum of the depreciation expense and the fixed costs by the calculator’s after-tax contribution margin (selling price, x, minus variable cost). The after-tax contribution margin is the amount that each additional calculator contributes to the firm’s profit. Before the firm canrealize a positive profit, it must have earned enough to cover its fixed costs and depreciationexpense. Solve for x.[(Fixed Costs + Depr.) (1–T c)] / [(Sales Price - Variable Cost) (1-T c)] = BEP[($900,000 + $120,000) (1 – 0.30)] / [(x - $150) (1 – 0.30)] = 20,000x= $66 The break-even sales price of the calculator is $66.8.7 Apply the accounting profit break-even point formula. Divide the after-tax sum of the annualdepreciation expense and the annual fixed costs by the television’s after-tax contribution margin(selling price minus variable cost).[(Fixed Costs + Depr.) (1–T c)] / [(Sales Price - Variable Cost) (1-T c)] = BEP[($120,000 + $20,000) (1 -0.35)] / [($1,500 - $1,100) (1 - 0.35)] = 350 The distributor must sell 350 televisions per year to break even.8.8 a. Apply the accounting profit break-even point formula. Divide the after-tax sum of thefixed costs and depreciation charge by the abalone’s after-tax contribution margin(selling price minus variable cost). The number of abalones that the proprietor must sellin order for you to receive any profit is the break-even point (BEP).[(Fixed Costs + Depr.) (1–T c)] / [(Sales Price – Variable Cost) (1-T c)] = BEP[($340,000 + $20,000) (1 – 0.35)] / [($2.00 - $0.72) (1 – 0.35)]= 281,250The proprietor must sell at least 281,250 abalones per year in order for you toreceive any profit.b. To calculate the amount of profit you will receive if the proprietor sells 300,000 abalones,subtract the total cost incurred from the total revenue received. Remember to includetaxes.Total Revenue Per Year = (Sales Price) (Number Sold) (1 – T c)= ($2.00) (300,000) (1 – 0.35)= $390,000Total Cost Per Year = [Fixed Cost + Deprc. + (Variable Cost) (Number Sold)] (1-T c)= [$340,000 + $20,000 +($0.72) (300,000)] (1 – 0.35)= $374,400Total Profit = Total Revenue – Total Cost= $390,000 - $374,400= $15,600You will receive $15,600 if the proprietor sells 300,000 abalones.8.9 Played 2187.5 = CEILING ((1000 + 50)/(0.5-0.02),1)8.10 a) ()()()()()()()()shirts-T10003.18103.1000,2Tc-1costVariable-priceSalesTc-1onDepreciatiCostFixed=-⨯--⨯+=⨯⨯+b) ()()()()()()()()shirts-T29743.18104018.2/000,10Tc-1costVariable-priceSalesTconDepreciatiTc1costFixedEAC=-⨯-++=⨯⨯+-⨯+8.11 When calculating the present value break-even point, express the initial investment of $140,000 asan equivalent annual cost (EAC). Divide the initial investment by the seven-year annuity factor,discounted at 15 percent. The EAC incorporates the opportunity cost of the investment.EAC = Initial Investment / A T r= $140,000 / A70.15= $33,650.45Calculate the annual depreciation expense.Depreciation = $140,000 / 7= $20,000Calculate the present-value break-even point. The fixed costs are $340,000. Remember toincorporate taxes into the calculation. Remember to include the depreciation tax shield, whichlowers the firm’s tax bill.[EAC+(Annual Fixed Costs) (1 - T c) – (Annual Depr.) (T c)] / [(Sales Price – Variable Cost) (1 – T c)]= BEP[$33,650.45 + $340,000 (0.65) - $20,000 (0.35)] / [($2 - $0.72) (0.65)] =297,656.79≅ 297,657 units The present value break-even point is 297,657 abalones.8.12 When calculating the present value break-even point, express the initial investment of $200,000 asan equivalent annual cost (EAC). Divide the initial investment by the five-year annuity factor,discounted at 12 percent.EAC = Initial Investment / A T r= $200,000 / A50.12= $55,481.95Calculate the annual depreciation expense.Depreciation = $200,000 / 5= $40,000Calculate the present-value break-even point.[EAC+(Fixed Costs) (1 - T c) – (Depr.) (T c)] / [(Sales Price – Variable Cost) (1 – T c)]= BEP[$55,481.95 + ($350,000) (0.75) – ($40,000) (0.25)] / [($25 - $5) (0.75)] = 20,532.13 The present value break-even point is 20,532 units.8.13 The following represents a different approach to solving present-value break-even problems,unlike the EAC method used in problems 8.8 and 8.7.Both the EAC approach and this approach will yield the same answer.First, determine the cash flow from selling the old harvester. When calculating the salvage value, remember that tax liabilities or credits are generated on the difference between the resale value and the book value of the asset.Use the original purchase price of the old harvester to determine annual depreciation.Depreciation Per Period = $45,000 / 15= $3,000Since the machine is five years old, the firm has accumulated five annual depreciation charges,reducing the book value of the machine. The current book value of the machine is equal to theinitial purchase price minus the accumulated depreciation.Book Value = Initial Purchase Price – Accumulated Depreciation= $45,000 – ($3,000 ⨯ 5 years)= $30,000Since the firm is able to resell the old harvester for $20,000, which is less than the $30,000 bookvalue of the machine, the firm will generate a tax credit on the sale.PV(Resale Value) = C - T C (Resale Value – Book Value)= $20,000 – 0.34 ($20,000 - $30,000)= $23,400Calculate the incremental depreciation. Calculate the depreciation tax shield generated by the new harvester less the forgone depreciation tax shield from the old harvester. Let P be the break-even purchase price.Depreciation Tax Shield, New Harvester = (Initial Investment / Economic Life) ⨯ T c= (P / 10) (0.34)Depreciation Tax Shield, Old Harvester = ($45,000 / 15) (0.34)= ($3,000) (0.34)Incremental Depreciation Tax Shield = (P / 10 - $3,000) (0.34)Apply the 10-year annuity formula, discounted at 15 percent, to calculate the PV of theincremental depreciation tax shield.PV(Depreciation Tax Shield) = (P / 10 - $3,000) (0.34) A100.15 The new harvester will generate year-end pre-tax cash flow savings of $10,000 per year for 10years. Apply the 10-year annuity formula, discounted at 15 percent, to find the PV of thosesavings. Remember to include taxes.PV(Savings) = (1 – T c) C1 A T r= (1 - 0.34) $10,000 A100.15= $33,123.87The break-even purchase price of the new harvester is the price, P, which makes the NPV of themachine equal to zero.NPV = -P + PV(Resale Value) + PV(Depreciation Tax Shield) + PV(Savings)$0 = -P + $23,400 + (P / 10 - $3,000) (0.34) A100.15 + $33,123.87P= $61,981.06The break-even purchase price is $61,981.06.8.14 A 5,0.08 3.993EAC 75,136,936Depreciation 60,000PVBreak-Even 3,5188.15 a. Pessimistic:Calculate the NPV of the pessimistic scenario. First, determine the yearly cash flow.Cash Flow = [Revenue - Variable Costs – Fixed Costs] (1 – T c) + Depr. Tax Shield= [($38 ⨯ 23,000) – ($21 ⨯ 23,000) - $320,000] (1- 0.35) +($420,000 / 7) (0.35)= $67,150Apply the seven-year annuity formula to calculate the NPV of the machine. Subtract theinitial investment.NPV = C0 + C1 A T r= -$420,000 + $67,150 A70.13= -$123,021.71The NPV of the pessimistic scenario is -$123,021.71.Expected:Calculate the NPV of the expected scenario. First, determine the yearly cash flow.Cash Flow = [Revenue - Variable Costs – Fixed Costs] (1 – T c) + Depr. Tax Shield= [($40 ⨯ 25,000) – ($20 ⨯ 25,000) - $300,000] (1- 0.35)+ ($420,000 / 7) (0.35)= $151,000Apply the seven-year annuity formula to calculate the NPV of the machine. Subtract theinitial investment.NPV = C0 + C1 A T r= -$420,000 + $151,000 A70.13= $247,814.18The NPV of the expected scenario is $247,814.18.Optimistic:Calculate the NPV of the optimistic scenario. First, determine the yearly cash flow.Cash Flow = [Revenue – Variable Costs – Fixed Costs] (1 – T c)+ Depreciation Tax Shield= [($42 ⨯ 27,000) – ($19 ⨯ 27,000) - $280,000] (1- 0.35)+ ($420,000 / 7) (0.35)= $242,650Apply the seven-year annuity formula to calculate the NPV of the machine. Subtract theinitial investment.NPV = C0 + C1 A T r= -$420,000 + $242,650 A70.13= $653,146.42The NPV of the optimistic scenario is $653,146.42.b. Calculate the expected NPV of the project to form your conclusion about the project.Remember that, since each scenario is equally likely, the expected NPV is the average ofthe three scenarios.NPV = [NPV(Pessimistic) + NPV(Expected) + NPV(Optimistic)] / (3)= [-$123,021.71 + $247,814.18 + $653,146.42] / 3= $259,312.96The expected NPV of the project is $259,312.96. You should conclude that theproject is worthwhile.8.16 Pessimistic:Calculate the NPV of the pessimistic scenario. First, determine the yearly cash flow. Todetermine the number of rackets sold, multiply the market size by the market share.Number of Rackets = Market Size ⨯ Market Share= 110,000 ⨯ 0.22= 24,200Cash Flow = [Revenue – Variable Costs – Fixed Costs] (1 – T c)+ Depreciation Tax Shield= [$115 ⨯ 24,200 - $72 ⨯ 24,200 - $850,000] (1 – 0.4)+ ($1,500,000 / 5) (0.4)= $234,360Apply the five-year annuity formula to calculate the NPV of the racket project. Subtract the initial investment.NPV = C0 + C1 A T r= -$1,500,000 + $234,360 A50.13= -$675,701.68Expected:Calculate the NPV of the expected scenario. First, determine the yearly cash flow. To determine the number of rackets sold, multiply the market size by the market share.Number of Rackets = Market Size ⨯ Market Share= 120,000 ⨯ 0.25= 30,000Cash Flow = [Revenue – Variable Costs – Fixed Costs] (1 – T c)+ Depreciation Tax Shield= [$120 ⨯ 30,000 - $70 ⨯ 30,000 - $800,000] (1 – 0.4)+ ($1,500,000 / 5) (0.4)= $540,000Apply the five-year annuity formula to calculate the NPV of the racket project. Subtract the initial investment.NPV = C0 + C1 A T r= -$1,500,000 + $540,000 A50.13= $399,304.88Optimistic:Calculate the NPV of the optimistic scenario. First, determine the yearly cash flow. To determine the number of rackets sold, multiply the market size by the market share.Number of Rackets = Market Size ⨯ Market Share= 130,000 ⨯ 0.27= 35,100Cash Flow = [Revenue – Variable Costs – Fixed Costs] (1 – T c)+ Depreciation Tax Shield= [$125 ⨯ 35,100 - $68 ⨯ 35,100 - $750,000] (1 – 0.4)+ ($1,500,000 / 5) (0.4)= $870,420Apply the five-year annuity formula to calculate the NPV of the racket project. Subtract the initial investment.NPV = C0 + C1 A T r= -$1,500,000 + $870,420 A50.13= $1,561,468.43Calculate the expected NPV of the project. Since each scenario is equally likely, the expectedNPV is the average of the three scenarios.NPV = [NPV(Pessimistic) + NPV(Expected) + NPV(Optimistic)] / (3)= [-$675,701.68 + $399,304.88 + $1,561,468.43] / (3)= $428,357.21The expected NPV of the project is $428,357.21. You should accept the project.8.17 Holding all variables as expected, except a single sensitivity analysis variable that is held atpessimistic or optimistic.Since under all scenarios NPVs come out positive, the project should be taken.8.18B-172Optimistic8.19 a. Apply the 10-year annuity formula, discounted at 10 percent, to calculate the NPV of thevideo game.NPV = C0 + C1 A T r= -$4,000,000 + $750,000 A100.1= $608,425.33The NPV of the video game is $608,425.33.b.Calculate the revised NPV of the project. The firm expects to receive net cash flow of$750,000 at the end of the first year of operations. Discount that value back one period toyear 0.PV(Year 1 Cash Flow) = C1 / (1+r)T= $750,000 / (1.1)= $681,818.18For the next nine years, the firm has a 50 percent chance of receiving annual cash flowsof $1,500,000 and a 50 percent chance of receiving annual cash flows of $0. Should thefirm receive cash flows of $0, the firm should exercise the option of abandonment andreceive the $200,000 cash flow. The probability of exercising that option is 50 percent.Calculate the expected PV of the revised cash flows by applying the nine-year annuityformula. To calculate the expected PV as of year 0, discount that value back one periodto year 0. The option is exercised in year 1 and must also be discounted back one periodto year 0.PV(Revised) = (Prob. ⨯ C2⨯ A T r + Prob. ⨯ Salvage) / (1+r)T= (0.5 ⨯ $1,500,000 ⨯ A90.1 + 0.5 ⨯ $200,000) / (1.1)= $4,017,516.23After including the initial investment, the revised NPV of the project is equal to the sumof the first year’s cash flow, the PV of the expected cash flows for the next nine years,and the expected value of abandoning the project.Revised NPV = C0 + C1 / (1+r)T +[(Prob. ⨯ C2⨯ A T r) + (Prob. ⨯ C2)] / (1+r)T= -$4,000,000 + $750,000 / (1.1) +(0.5 ⨯ $1,500,000 ⨯ A90.1 + 0.5 ⨯ $200,000) / (1.1)= $699,334.42The revised NPV is $699,334.42.c. The market value of the project, M, is the NPV of the project without an option toabandon plus the value of the option, Opt. The NPV of the project without the option toabandon was calculated in part (a). The difference between the NPV as calculated in part(a) and the revised NPV is equal to the option value of abandonment, Opt.M= NPV + Opt$699,334.42 = $608,425.33+ Opt$90,909.09 = OptThe option value of abandonment is $90,909.09.8.20 a. Apply the 10-year annuity formula, discounted at 20 percent to calculate the NPV of theproject. Total annual net cash flow is $200,000,000.NPV = C0 + C1 A T r= -$100,000,000 + $200,000,000 A100.2= $738,494,417.11The NPV of the project is $738,494,417.11.b.Allied Products should abandon the project if the PV of the revised cash flows for thenext nine years is less than the project’s scrap value. Since the option to abandon theproject occurs in year 1, discount the revised cash flows to year 1 as well. To determinethe level of expected cash flows below which Allied should abandon the project,calculate the equivalent annual cash flows the project must earn to equal the scrap value,$50 million. Set the scrap value equal to a nine-year annuity, discounted at 20 percent.Solve for C1.Scrap Value = C1 A T r$50,000,000 = C1 A90.2$50,000,000 / A90.2= C1$12,403,973.08 = C1The firm should abandon the project after the first year if the revised expectedannual cash flows are below $12,403,973.08. Below that level, the firm is better offabandoning the project and receiving the $50 million scrap value of the project.8.21 a. NPV (1.932) = –10 + 10*0.3*(1/0.25-1/0.25*(1/1.25)5)b. Option Value 2.000 = 0.5*9/1.25New NPV 0.068 = –10 + 10*0.3/1.25 + 0.5*15*0.3*(1/0.25 –1/0.25*(1/1.25)4)/(1.25) + 0.5*9/1.25B-175。

公司理财第七版Chap008

Cash Flows Project Project 1 Project 2 Project 3 C0 - $1,000 - $1,000 - $1,000 C1 $700 $500 $500 C2 $500 $700 $700 $700 C3

Payback Period 1.6 years 1.7 years 1.7 years

8-2

Net Present Value

Opportunity Cost of Capital - Expected rate of

return given up by investing in a project

Net Present Value - Present value of cash flows

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Chapter 11: The Basics of Capital BudgetingI. What is Capital Budgeting?The process of determining what capital projects to acceptProject Classification is the starting point for determining the appropriate discount rate Replacement to maintain current operationsReplacement to reduce costsExpansion of existing products or marketsExpansion into new products or marketsPure research & development (example: pharmaceutical firms)Exploration (example: energy firms)Safety and /or environmental (government mandated) projectsII. Decision CriteriaWhat are the major investment decision criteria?Net Present Value - NPVInternal Rate of Return - IRRModified Internal Rate of Return - MIRRPayback Period - PaybackDiscounted Payback Period – Discounted PaybackProfitability Index - PIWhat are they used for?To evaluate the cash flows from capital investment projectsTo make the accept or reject decisionA. The NPV Rule:1. Why Is Net Present Value the Best Decision Criteria?- It considers the time value of money(TVM)… a dollar today is worth more than a dollar in the future- It considers all cash flows during the project’s entire life- NPV lets you know exactly how much value is being added by the project- You can set the appropriate require rate of return (discount rate or hurdle rate) depending on a project’s risk2. Calculating Net Present Value (NPV:NPV =CF0+ CF1 + CF2 + ... + CF tt3. The NPV decision (accept/reject) rule:- Accept the project (investment) if NPV > zero- Reject the project if NPV < zero4. What does a positive NPV mean?- The PV of cash inflows > PV of cash outflows- The value of the company is being increased by the amount of NPV- The project meets the required rate of return…and then someA friend asks you to invest $20,000 and promises to pay you $26,000 at the end of 2 years. Your required rate of return is 15%. Do you take the offer?NPV =CF0+ CF2NPV = -20,000 + 26,000 => -20,000 + 19,6601.15 2NPV = $-340 You should reject your friend’s offer!* If this were a capital investment project, acceptance would reduce the value of the company by $340!* Acceptance of the project would not increase the value of the company by $6,000! The key variable here is the required rate of return (or discount rate).The required rate of return (RRR) is:* The hurdle rate* The cost of capital (funds)* The best rate of return the company could expect on other projects of similar risk Note:In a competitive market, positive NPV projects are considered rare and require diligent effort to uncoverTwo projects with identical cash outflows (investment =$1,000) but different timing of cash inflows. Discount rate = 10%NPV for project S: (Large cash inflows come sooner)0 1 2 3 4|---------------|---------------|---------------|--------------|Net CF -1,000 500 400 300 100NPV(S) = $78.82NPV for project L: (Large cash inflows come later)0 1 2 3 4|---------------|---------------|---------------|--------------|Net CF -1,000 100 300 400 500NPV(L) = -$19.12B. The Payback Rule:Time period required for a project to generate enough cash inflows to recover the initial cost.The Payback decision (accept/reject) rule:- Accept if payback period < maximum acceptable payback period.- Reject if payback period > maximum acceptable payback period.Advantages- Easy to understand: the shorter the payback period, the better- Quick indicator of the liquidity risk of the project (how long funds will be tied up) Disadvantages- Ignores time value of money- Ignores cash flows beyond acceptable payback date- Acceptable payback date is usually an arbitrary cutoff point. Risk is not quantified in a required rate of return. The liquid ity risk is simply a “rule ofthumb”Project S:0 1 2 3 4|---------------|---------------|---------------|---------------|Net CF -1,000 500 400 300 100 Cumulative -1,000 -500 -100 200 300NCFPayback = years before + uncovered cost at end of yearfull recovery NCF during following year= 2 + 100/300= 2.33 yearsIf acceptable payback period is 2.33 or more years, you accept project SC. The Discounted Payback Rule:Time period required for a project to generate enough discounted cash inflows to recover the initial cost.The Discounted Payback decision (accept/reject) rule:- Accept if discounted payback period < maximum acceptable payback period.- Reject if discounted payback period > maximum acceptable payback period. Advantages- Easy to understand: the shorter the payback period, the better- Quick indicator of the liquidity risk of the project (how long funds will be tied up) - Does consider the time value of moneyDisadvantages- Ignores cash flows beyond acceptable payback date- Acceptable payback date is usually an arbitrary cutoff point.Project S: Assume a 10 percent discount rate0 1 2 3 4|---------------|---------------|---------------|---------------|Net CF -1,000 500 400 300 100PVNCF -1,000 454 331 225 68Cumulative -1,000 -546 -215 10PVNCFPayback = years before + uncovered cost at end of yearfull recovery NCF during following year= 2 + 215/225= 2.96 yearsIf acceptable payback period is 2.96 or more years, you accept project SD. Internal Rate of ReturnThe IRR is similar to a bond’s yield to maturity. It is the rate that makes the present value of cash inflows (CIF) equal to the present value of cash outflows (COF). Thus, it is the rate of return that results in a zero NPV when it is used as the discount rate.NPV = CF0+ CF1 + CF2 + ... + CF t(1 + r)1 (1 + r)2 (1 + r)t0 = CF0+ CF1 + CF2 + ... + CF t(1 + IRR) 1(1 + IRR) 2(1 + IRR)tIRR Decision Rule- Accept the project if IRR > req’d rate of return (discount rate)- Reject the project if IRR < req’d rate of return (discount r ate)Advantages- Considers TVM- Considers all cash flows- Easy to understandDisadvantages- May use unreasonable discount rate- Can conflict with NPV if projects are mutually exclusiveIRR Examples:IRR for Project S0 1 2 3 4Project S|---------------|---------------|---------------|---------------|-1,000 500 400 300 1000 = -1000 + 500 + 400 + 300 + 100(1+Irr) 1 (1+Irr) 2 (1+Irr) 3 (1+Irr)4Solve for the IRR. That is the discount rate that solves this equation and makes the answer (NPV) equal to zero.IRR for Project S = 14.49%IRR for Project L0 1 2 3 4Project L|---------------|---------------|---------------|----------------|-1,000 100 300 400 5000 = -1000 + 100 + 300 + 400 + 500(1+Irr) 1 (1+Irr) 2 (1+Irr) 3 (1+Irr)4IRR for Project L =9.27%The IRR is the most popular method, after NPV, for evaluating cash flows and is almost as good.Problems with IRR:There are problems with using IRR rather than NPV with you are choosing between mutually exclusive projects:- Independent projects: When evaluating multiple projects and any, none, or all of them can be accepted. Acceptance of any project has no bearing on the acceptance or rejection of another.- Mutually exclusive projects: When evaluating multiple projects and only one can be accepted. Acceptance of one project means rejection of the other(s).There is never a conflict between IRR and NPV criterion when evaluating independent projects. But when choosing between mutually exclusive projects, the IRR choice may conflict with the NPV choice under certain conditions.The Scale Problem: A potential conflict exists when there are significant differences in the size of the cash flows. An example would be if comparing a project with a $100,000 initial investment (COF) with another project with a $1,000,000 initial investment.The Timing Problem: A potential conflict exists when the timing of the cash flows for two projects are radically different. This can result in a conflict between the NPV choice and the IRR choice at low discount rates.Multiple IRRs: Projects with non-normal (non-conventional) cash flows may have multiple IRRs. A normal (or conventional) cash flow is a cash outflow at the beginning of a project, followed by cash inflows thereafter.The NPV Profile: NPV graphed against the discount rateRecall the NPV & IRR acceptance rules:NPV: Accept the project if NPV > zeroIRR: Accept the project if IRR > RRRNPVCash Flows-1000$300 500400300100IRR0 r.1449Any project with a positive NPV will also have an IRR that exceeds the discount rate (required rate of return).NPV Profiles for Mutually Exclusive Projects:NPV Cash FlowsExample: IRR vs NPV for Mutual Exclusive ProjectsCash FlowsA B-10,000 -10,00010,000 1,0001,000 1,0001,000 12,000IRR for A _____________ IRR for B is ___________ NPV at 0% ____________ NPV at 0% ____________ NPV at 10% ___________ NPV at 10% ___________ NPV at 15% ___________ NPV at 15% ___________ Which project is acceptable if they are independent? Why?Which project is acceptable if they are mutually exclusive? Why? E. Modified Internal Rate of Return- Accept the project if M IRR > req’d rate of return (discount rate) - Reject the project if M IRR < req’d rate of return (discount rate) Advantage: Let’s you decide the reinvestment rate!Cost = Terminal Value TGiven: Cost, TVSolve: MIRRF. Profitability Index (PI)PI = (PV of Cash Inflows)/(PV of Cash Outflows)The PI is the ratio of the PV of the project’s cash inflows to the PV of the project’s cash outflows.PI for Project SPVCIF S= 500 + 400 + 300 + 100 = 1,078.82(1+.10)1 (1+.10)2 (1+.10)3 (1+.10)4PVCOF S= 1,000PI S= 1,078.82/1,000 = 1.07882PI Decision Rule- Accept if PI > 1.00- Reject if PI < 1.00Advantages- Considers TVM- Considers all cash flows- Uses reasonable discount rate- Useful when faced with capital rationing.Disadvantages- Cannot distinguish projects of vastly different scale- May conflict with NPV when evaluating mutually exclusive projectsProfitability Index vs NPV for Mutually Exclusive Projects0 1|---------------------|Cash FlowsProject A -$10 $15Project B -$1,000 $1,250A BNPV at .10 $ 3.64 $136.36PI at .10 1.364 1.136According to NPV, you choose B.According to PI, you choose A.。