Cost15EChapter09_Solutions

APQP某汽车

访问 APQP 指南

Both the Guideline and the forms are available.指南和表格均可由此获得。

1-4

Module Introduction

FPDS Timing Relationship and ResponsibilitiesFPDS 时间进度关系和职责

APQP Benefits

APQP aids the program team by:APQP帮助项目小组:Adding discipline 增加纪律 Facilitating early identification of required changes 早期确定可能的更改Avoiding late changes 避免晚期更改 Providing a quality product on time, at acceptable cost, to satisfy customers 用可接受的价格,准时提供优质的产品,满足客户Facilitating continuous improvement 使持续改进更方便

APQP 23个要素

1 选点决定 2 顾客输入要求 3 精致工艺技术 4 设计失效模式后果分析 5 设计评审 6 设计验证计划 7 分承包方 APQP 状态 8 设施、工具和量具 9 样件制造计划 10 样件制造 11 图纸和规范

12 小组可行性承诺 13 制造过程流程图 14 过程失效模式后果分析 15 测量系统评价 16 试生产控制计划 17 操作工过程指导书 18 包装规范 19 产品试生产 20 生产控制计划 21 初始过程能力研究 22 生产确认试验 23 生产件批准 (PSW)

Course Goals

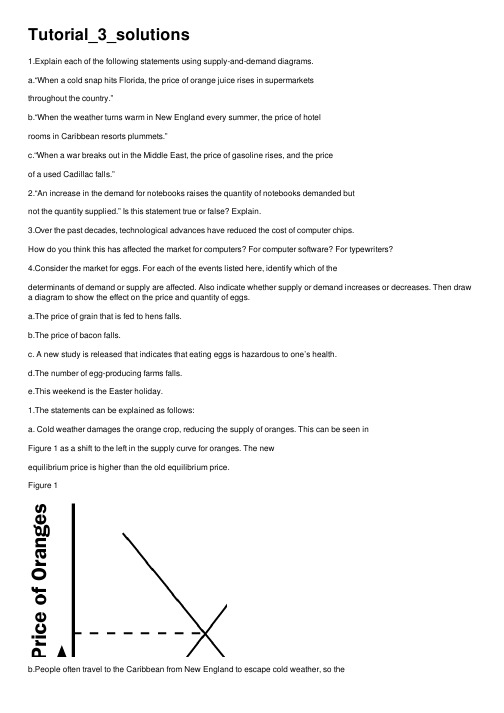

Tutorial_3_solutions

Tutorial_3_solutions1.Explain each of the following statements using supply-and-demand diagrams.a.“When a cold snap hits Florida, the price of orange juice rises in supermarketsthroughout the country.”b.“When the weather turns warm in New England every summer, the price of hotelrooms in Caribbean resorts plummets.”c.“When a war breaks out in the Middle East, the price of gasoline rises, and the priceof a used Cadillac falls.”2.“An increase in the demand for notebooks raises the quantity of notebooks demanded butnot the quantity supplied.” Is this statement true or false? Explain.3.Over the past decades, technological advances have reduced the cost of computer chips.How do you think this has affected the market for computers? For computer software? For typewriters?4.Consider the market for eggs. For each of the events listed here, identify which of thedeterminants of demand or supply are affected. Also indicate whether supply or demand increases or decreases. Then draw a diagram to show the effect on the price and quantity of eggs.a.The price of grain that is fed to hens falls.b.The price of bacon falls.c. A new study is released that indicates that eating eggs is hazardous to one’s health.d.The number of egg-producing farms falls.e.This weekend is the Easter holiday.1.The statements can be explained as follows:a. Cold weather damages the orange crop, reducing the supply of oranges. This can be seen inFigure 1 as a shift to the left in the supply curve for oranges. The newequilibrium price is higher than the old equilibrium price.Figure 1b.People often travel to the Caribbean from New England to escape cold weather, so thedemand for Caribbean hotel rooms is high in the winter. In the summer, fewer people travel to the Caribbean, because northern climes are more pleasant. The result, as shown in Figure 2, is a shift to the left in the demand curve. The equilibrium price of Caribbean hotel rooms is thus lower in the summer than in the winter, as the figure shows.Figure 2c.When a war breaks out in the Middle East, many markets are affected. Because a largeproportion of oil production takes place there, the war disrupts oil supplies, shifting the supply curve for gasoline to the left, as shown in Figure 3. The result is a rise in the equilibrium priceof gasoline. With a higher price for gasoline, the cost of operating a gas-guzzling automobile like a Cadillac will increase. As a result, the demand for used Cadillacs will decline, as people in the market for cars will not find Cadillacs as attractive. In addition, some people who already own Cadillacs will try to sell them. The result is that the demand curve for used Cadillacs shifts to the left, while the supply curve shifts to the right, as shown in Figure 4. The result is a decline in the equilibrium price of used Cadillacs.Figure 3 Figure 42. The statement that "an increase in the demand for notebooks raises the quantity of notebooksdemanded, but not the quantity supplied," in general, is false. As Figure 5 shows, the increasein demand for notebooks results in an increased quantity supplied. The only way the statement would be true is if the supply curve was a vertical line, as shown in Figure 6.Figure 5 Figure 63.Technological advances that reduce the cost of producing computer chips represent a decline in an input price for producing a computer. The result is a shift to the right in the supply of computers, as shown in Figure 7. The equilibrium price falls and the equilibrium quantity rises, as the figure shows.Figure 7Because computer software is a complement to computers, the lower equilibrium price of computers increases the demand for software. As Figure 8 shows, the result is a rise in both the equilibrium price and quantity of software.Figure 8Because typewriters are substitutes for computers, the lower equilibrium price of computers reduces the demand for typewriters. As Figure 9 shows, the result is a decline in both the equilibrium price and quantity of typewriters.Figure 94.The answers are as follows:a.If the price of grain used to feed hens falls, the supply of eggs will rise. Demand will not be affected. The result is a fall in the price and an increase in the quantity sold, as Figure 10 shows.Figure 10b.If the price of bacon falls, the demand for eggs will rise because eggs and bacon are complements. Supply will not be affected. The result is an increase in both the price of eggs and the quantity sold, as Figure 11 shows.Figure 11c. A new study that indicates that eat ing eggs is hazardous to one’s health will cause a decline in the demand for eggs. Supply is not affected. The result is a decline in the price of eggs and a decrease in the quantity sold, as Figure 12 shows.Figure 12d.If the number of egg-producing farms falls, the supply of eggs will decline. Demand isnot affected. The equilibrium price of eggs will fall and quantity of eggs sold rises as Figure13 shows.Figure 13equilibrium price and the equilibrium quantity rise, as Figure 11 shows.。

审计学:一种整合方法阿伦斯英文版第12版课后答案Chapter15SolutionsManual

审计学:⼀种整合⽅法阿伦斯英⽂版第12版课后答案Chapter15SolutionsManualChapter 15Audit Sampling for Tests of Controls andSubstantive Tests of TransactionsReview Questions15-1 A representative sample is one in which the characteristics of interest for the sample are approximately the same as for the population (that is, the sample accurately represents the total population). If the population contains significant misstatements, but the sample is practically free of misstatements, the sample is nonrepresentative, which is likely to result in an improper audit decision. The auditor can never know for sure whether he or she has a representative sample because the entire population is ordinarily not tested, but certain things, such as the use of random selection, can increase the likelihood of a representative sample.15-2Statistical sampling is the use of mathematical measurement techniques to calculate formal statistical results. The auditor therefore quantifies sampling risk when statistical sampling is used. In nonstatistical sampling, the auditor does not quantify sampling risk. Instead, conclusions are reached about populations on a more judgmental basis.For both statistical and nonstatistical methods, the three main parts are:1. Plan the sample2. Select the sample and perform the tests3. Evaluate the results15-3In replacement sampling, an element in the population can be included in the sample more than once if the random number corresponding to that element is selected more than once. In nonreplacement sampling, an element can be included only once. If the random number corresponding to an element is selected more than once, it is simply treated as a discard the second time. Although both selection approaches are consistent with sound statistical theory, auditors rarely use replacement sampling; it seems more intuitively satisfying to auditors to include an item only once.15-4 A simple random sample is one in which every possible combination of elements in the population has an equal chance of selection. Two methods of simple random selection are use of a random number table, and use of the computer to generate random numbers. Auditors most often use the computer to generate random numbers because it saves time, reduces the likelihood of error, and provides automatic documentation of the sample selected.15-5In systematic sampling, the auditor calculates an interval and then methodically selects the items for the sample based on the size of the interval. The interval is set by dividing the population size by the number of sample items desired.To select 35 numbers from a population of 1,750, the auditor divides 35 into 1,750 and gets an interval of 50. He or she then selects a random number between 0 and 49. Assume the auditor chooses 17. The first item is the number 17. The next is 67, then 117, 167, and so on.The advantage of systematic sampling is its ease of use. In most populations a systematic sample can be drawn quickly, the approach automatically puts the numbers in sequential order and documentation is easy.A major problem with the use of systematic sampling is the possibility of bias. Because of the way systematic samples are selected, once the first item in the sample is selected, other items are chosen automatically. This causes no problems if the characteristics of interest, such as control deviations, are distributed randomly throughout the population; however, in many cases they are not. If all items of a certain type are processed at certain times of the month or with the use of certain document numbers, a systematically drawn sample has a higher likelihood of failing to obtain a representative sample. This shortcoming is sufficiently serious that some CPA firms prohibit the use of systematic sampling. 15-6The purpose of using nonstatistical sampling for tests of controls and substantive tests of transactions is to estimate the proportion of items in a population containing a characteristic or attribute of interest. The auditor is ordinarily interested in determining internal control deviations or monetary misstatements for tests of controls and substantive tests of transactions.15-7 A block sample is the selection of several items in sequence. Once the first item in the block is selected, the remainder of the block is chosen automatically. Thus, to select 5 blocks of 20 sales invoices, one would select one invoice and the block would be that invoice plus the next 19 entries. This procedure would be repeated 4 other times.15-8 The terms below are defined as follows:15-8 (continued)15-9The sampling unit is the population item from which the auditor selects sample items. The major consideration in defining the sampling unit is making it consistent with the objectives of the audit tests. Thus, the definition of the population and the planned audit procedures usually dictate the appropriate sampling unit.The sampling unit for verifying the occurrence of recorded sales would be the entries in the sales journal since this is the document the auditor wishes to validate. The sampling unit for testing the possibility of omitted sales is the shipping document from which sales are recorded because the failure to bill a shipment is the exception condition of interest to the auditor.15-10 The tolerable exception rate (TER) represents the exception rate that the auditor will permit in the population and still be willing to use the assessed control risk and/or the amount of monetary misstatements in the transactions established during planning. TER is determined by choice of the auditor on the basis of his or her professional judgment.The computed upper exception rate (CUER) is the highest estimated exception rate in the population, at a given ARACR. For nonstatistical sampling, CUER is determined by adding an estimate of sampling error to the SER (sample exception rate). For statistical sampling, CUER is determined by using a statistical sampling table after the auditor has completed the audit testing and therefore knows the number of exceptions in the sample.15-11 Sampling error is an inherent part of sampling that results from testing less than the entire population. Sampling error simply means that the sample is not perfectly representative of the entire population.Nonsampling error occurs when audit tests do not uncover errors that exist in the sample. Nonsampling error can result from:1. The auditor's failure to recognize exceptions, or2. Inappropriate or ineffective audit procedures.There are two ways to reduce sampling risk:1. Increase sample size.2. Use an appropriate method of selecting sample items from thepopulation.Careful design of audit procedures and proper supervision and review are ways to reduce nonsampling risk.15-12 An attribute is the definition of the characteristic being tested and the exception conditions whenever audit sampling is used. The attributes of interest are determined directly from the audit program.15-13 An attribute is the characteristic being tested for in a population. An exception occurs when the attribute being tested for is absent. The exception for the audit procedure, the duplicate sales invoice has been initialed indicating the performance of internal verification, is the lack of initials on duplicate sales invoices.15-14 Tolerable exception rate is the result of an auditor's judgment. The suitable TER is a question of materiality and is therefore affected by both the definition and the importance of the attribute in the audit plan.The sample size for a TER of 6% would be smaller than that for a TER of 3%, all other factors being equal.15-15 The appropriate ARACR is a decision the auditor must make using professional judgment. The degree to which the auditor wishes to reduce assessed control risk below the maximum is the major factor determining the auditor's ARACR.The auditor will choose a smaller sample size for an ARACR of 10% than would be used if the risk were 5%, all other factors being equal.15-16 The relationship between sample size and the four factors determining sample size are as follows:a. As the ARACR increases, the required sample size decreases.b. As the population size increases, the required sample size isnormally unchanged, or may increase slightly.c. As the TER increases, the sample size decreases.d. As the EPER increases, the required sample size increases.15-17 In this situation, the SER is 3%, the sample size is 100 and the ARACR is 5%. From the 5% ARACR table (Table 15-9) then, the CUER is 7.6%. This means that the auditor can state with a 5% risk of being wrong that the true population exception rate does not exceed 7.6%.15-18 Analysis of exceptions is the investigation of individual exceptions to determine the cause of the breakdown in internal control. Such analysis is important because by discovering the nature and causes of individual exceptions, the auditor can more effectively evaluate the effectiveness of internal control. The analysis attempts to tell the "why" and "how" of the exceptions after the auditor already knows how many and what types of exceptions have occurred.15-19 When the CUER exceeds the TER, the auditor may do one or more of the following:1. Revise the TER or the ARACR. This alternative should be followed onlywhen the auditor has concluded that the original specifications weretoo conservative, and when he or she is willing to accept the riskassociated with the higher specifications.2. Expand the sample size. This alternative should be followed whenthe auditor expects the additional benefits to exceed the additionalcosts, that is, the auditor believes that the sample tested was notrepresentative of the population.3. Revise assessed control risk upward. This is likely to increasesubstantive procedures. Revising assessed control risk may bedone if 1 or 2 is not practical and additional substantive proceduresare possible.4. Write a letter to management. This action should be done inconjunction with each of the three alternatives above. Managementshould always be informed when its internal controls are notoperating effectively. If a deficiency in internal control is consideredto be a significant deficiency in the design or operation of internalcontrol, professional standards require the auditor to communicatethe significant deficiency to the audit committee or its equivalent inwriting. If the client is a publicly traded company, the auditor mustevaluate the deficiency to determine the impact on the auditor’sreport on internal control over financial reporting. If the deficiency isdeemed to be a material weakness, the auditor’s report on internalcontrol would contain an adverse opinion.15-20 Random (probabilistic) selection is a part of statistical sampling, but it is not, by itself, statistical measurement. To have statistical measurement, it is necessary to mathematically generalize from the sample to the population.Probabilistic selection must be used if the sample is to be evaluated statistically, although it is also acceptable to use probabilistic selection with a nonstatistical evaluation. If nonprobabilistic selection is used, nonstatistical evaluation must be used.15-21 The decisions the auditor must make in using attributes sampling are: What are the objectives of the audit test? Does audit sampling apply?What attributes are to be tested and what exception conditions are identified?What is the population?What is the sampling unit?What should the TER be?What should the ARACR be?What is the EPER?What generalizations can be made from the sample to thepopulation?What are the causes of the individual exceptions?Is the population acceptable?15-21 (continued)In making the above decisions, the following should be considered: The individual situation.Time and budget constraints.The availability of additional substantive procedures.The professional judgment of the auditor.Multiple Choice Questions From CPA Examinations15-22 a. (1) b. (3) c. (2) d. (4)15-23 a. (1) b. (3) c. (4) d. (4)15-24 a. (4) b. (3) c. (1) d. (2)Discussion Questions and Problems15-25a.An example random sampling plan prepared in Excel (P1525.xls) is available on the Companion Website and on the Instructor’s Resource CD-ROM, which is available upon request. The command for selecting the random number can be entered directly onto the spreadsheet, or can be selected from the function menu (math & trig) functions. It may be necessary to add the analysis tool pack to access the RANDBETWEEN function. Once the formula is entered, it can be copied down to select additional random numbers. When a pair of random numbers is required, the formula for the first random number can be entered in the first column, and the formula for the second random number can be entered in the second column.a. First five numbers using systematic selection:Using systematic selection, the definition of the sampling unit for determining the selection interval for population 3 is the total number of lines in the population. The length of the interval is rounded down to ensure that all line numbers selected are within the defined population.15-26a. To test whether shipments have been billed, a sample of warehouse removal slips should be selected and examined to see ifthey have the proper sales invoice attached. The sampling unit willtherefore be the warehouse removal slip.b. Attributes sampling method: Assuming the auditor is willing to accept a TER of 3% at a 10% ARACR, expecting no exceptions in the sample, the appropriate sample size would be 76, determined from Table 15-8.Nonstatistical sampling method: There is no one right answer to this question because the sample size is determined using professional judgment. Due to the relatively small TER (3%), the sample size should not be small. It will most likely be similar in size to the sample chosen by the statistical method.c. Systematic sample selection:22839 = Population size of warehouse removal slips(37521-14682).76 = Sample size using statistical sampling (students’answers will vary if nonstatistical sampling wasused in part b.300 = Interval (22839/76) if statistical sampling is used (students’ answers will vary if nonstatisticalsampling was used in part b).14825 = Random starting point.Select warehouse removal slip 14825 and every 300th warehouse removal slip after (15125, 15425, etc.)Computer generation of random numbers using Excel (P1526.xls): =RANDBETWEEN(14682,37521)The command for selecting the random number can be entered directly onto the spreadsheet, or can be selected from the function menu (math & trig) functions. It may be necessary to add the analysis tool pack to access the RANDBETWEEN function. Once the formula is entered, it can be copied down to select additional random numbers.d. Other audit procedures that could be performed are:1. Test extensions on attached sales invoices for clerical accuracy. (Accuracy)2. Test time delay between warehouse removal slip date and billing date for timeliness of billing. (Timing)3. Trace entries into perpetual inventory records to determinethat inventory is properly relieved for shipments. (Postingand summarization)15-26 (continued)e. The test performed in part c cannot be used to test for occurrenceof sales because the auditor already knows that inventory wasshipped for these sales. To test for occurrence of sales, the salesinvoice entry in the sales journal is the sampling unit. Since thesales invoice numbers are not identical to the warehouse removalslips it would be improper to use the same sample.15-27a. It would be appropriate to use attributes sampling for all audit procedures except audit procedure 1. Procedure 1 is an analyticalprocedure for which the auditor is doing a 100% review of the entirecash receipts journal.b. The appropriate sampling unit for audit procedures 2-5 is a line item,or the date the prelisting of cash receipts is prepared. The primaryemphasis in the test is the completeness objective and auditprocedure 2 indicates there is a prelisting of cash receipts. All otherprocedures can be performed efficiently and effectively by using theprelisting.c. The attributes for testing are as follows:d. The sample sizes for each attribute are as follows:15-28a. Because the sample sizes under nonstatistical sampling are determined using auditor judgment, students’ answers to thisquestion will vary. They will most likely be similar to the samplesizes chosen using attributes sampling in part b. The importantpoint to remember is that the sample sizes chosen should reflectthe changes in the four factors (ARACR, TER, EPER, andpopulation size). The sample sizes should have fairly predictablerelationships, given the changes in the four factors. The followingreflects some of the relationships that should exist in student’ssample size decisions:SAMPLE SIZE EXPLANATION1. 90 Given2. > Column 1 Decrease in ARACR3. > Column 2 Decrease in TER4. > Column 1 Decrease in ARACR (column 4 is thesame as column 2, with a smallerpopulation size)5. < Column 1 Increase in TER-EPER6. < Column 5 Decrease in EPER7. > Columns 3 & 4 Decrease in TER-EPERb. Using the attributes sampling table in Table 15-8, the sample sizesfor columns 1-7 are:1. 882. 1273. 1814. 1275. 256. 187. 149c.d. The difference in the sample size for columns 3 and 6 result from the larger ARACR and larger TER in column 6. The extremely large TER is the major factor causing the difference.e. The greatest effect on the sample size is the difference between TER and EPER. For columns 3 and 7, the differences between the TER and EPER were 3% and 2% respectively. Those two also had the highest sample size. Where the difference between TER and EPER was great, such as columns 5 and 6, the required sample size was extremely small.Population size had a relatively small effect on sample size.The difference in population size in columns 2 and 4 was 99,000 items, but the increase in sample size for the larger population was marginal (actually the sample sizes were the same using the attributes sampling table).f. The sample size is referred to as the initial sample size because it is based on an estimate of the SER. The actual sample must be evaluated before it is possible to know whether the sample is sufficiently large to achieve the objectives of the test.15-29 a.* Students’ answers as to whether the allowance for sampling error risk is sufficient will vary, depending on their judgment. However, they should recognize the effect that lower sample sizes have on the allowance for sampling risk in situations 3, 5 and 8.b. Using the attributes sampling table in Table 15-9, the CUERs forcolumns 1-8 are:1. 4.0%2. 4.6%3. 9.2%4. 4.6%5. 6.2%6. 16.4%7. 3.0%8. 11.3%c.d. The factor that appears to have the greatest effect is the number ofexceptions found in the sample compared to sample size. For example, in columns 5 and 6, the increase from 2% to 10% SER dramatically increased the CUER. Population size appears to have the least effect. For example, in columns 2 and 4, the CUER was the same using the attributes sampling table even though the population in column 4 was 10 times larger.e. The CUER represents the results of the actual sample whereas theTER represents what the auditor will allow. They must be compared to determine whether or not the population is acceptable.15-30a. and b. The sample sizes and CUERs are shown in the following table:a. The auditor selected a sample size smaller than that determinedfrom the tables in populations 1 and 3. The effect of selecting asmaller sample size than the initial sample size required from thetable is the increased likelihood of having the CUER exceed theTER. If a larger sample size is selected, the result may be a samplesize larger than needed to satisfy TER. That results in excess auditcost. Ultimately, however, the comparison of CUER to TERdetermines whether the sample size was too large or too small.b. The SER and CUER are shown in columns 4 and 5 in thepreceding table.c. The population results are unacceptable for populations 1, 4, and 6.In each of those cases, the CUER exceeds TER.The auditor's options are to change TER or ARACR, increase the sample size, or perform other substantive tests to determine whether there are actually material misstatements in thepopulation. An increase in sample size may be worthwhile inpopulation 1 because the CUER exceeds TER by only a smallamount. Increasing sample size would not likely result in improvedresults for either population 4 or 6 because the CUER exceedsTER by a large amount.d. Analysis of exceptions is necessary even when the population isacceptable because the auditor wants to determine the nature andcause of all exceptions. If, for example, the auditor determines thata misstatement was intentional, additional action would be requiredeven if the CUER were less than TER.15-30 (Continued)e.15-31 a. The actual allowance for sampling risk is shown in the following table:b. The CUER is higher for attribute 1 than attribute 2 because the sample sizeis smaller for attribute 1, resulting in a larger allowance for sampling risk.c. The CUER is higher for attribute 3 than attribute 1 because the auditorselected a lower ARACR. This resulted in a larger allowance for sampling risk to achieve the lower ARACR.d. If the auditor increases the sample size for attribute 4 by 50 items and findsno additional exceptions, the CUER is 5.1% (sample size of 150 and three exceptions). If the auditor finds one exception in the additional items, the CUER is 6.0% (sample size of 150, four exceptions). With a TER of 6%, the sample results will be acceptable if one or no exceptions are found in the additional 50 items. This would require a lower SER in the additional sample than the SER in the original sample of 3.0 percent. Whether a lower rate of exception is likely in the additional sample depends on the rate of exception the auditor expected in designing the sample, and whether the auditor believe the original sample to be representative.15-32a. The following shows which are exceptions and why:b. It is inappropriate to set a single acceptable tolerable exception rate and estimated population exception rate for the combined exceptions because each attribute has a different significance tothe auditor and should be considered separately in analyzing the results of the test.c. The CUER assuming a 5% ARACR for each attribute and a sample size of 150 is as follows:15-32 (continued)d.*Students’ answers will most likely vary for this attribute.e. For each exception, the auditor should check with the controller todetermine an explanation for the cause. In addition, the appropriateanalysis for each type of exception is as follows:15-33a. Attributes sampling approach: The test of control attribute had a 6% SER and a CUER of 12.9%. The substantive test of transactionsattribute has SER of 0% and a CUER of 4.6%.Nonstatistical sampling approach: As in the attributes samplingapproach, the SERs for the test of control and the substantive testof transactions are 6% and 0%, respectively. Students’ estimates ofthe CUERs for the two tests will vary, but will probably be similar tothe CUERs calculated under the attributes sampling approach.b. Attributes sampling approach: TER is 5%. CUERs are 12.9% and4.6%. Therefore, only the substantive test of transactions resultsare satisfactory.Nonstatistical sampling approach: Because the SER for the test ofcontrol is greater than the TER of 5%, the results are clearly notacceptable. Students’ estimates for CUER for the test of controlshould be greater than the SER of 6%. For the substantive test oftransactions, the SER is 0%. It is unlikely that students will estimateCUER for this test greater than 5%, so the results are acceptablefor the substantive test of transactions.c. If the CUER exceeds the TER, the auditor may:1. Revise the TER if he or she thinks the original specificationswere too conservative.2. Expand the sample size if cost permits.3. Alter the substantive procedures if possible.4. Write a letter to management in conjunction with each of theabove to inform management of a deficiency in their internalcontrols. If the client is a publicly traded company, theauditor must evaluate the deficiency to determine the impacton the auditor’s report on internal control over financialreporting. If the deficiency is deemed to be a materialweakness, the auditor’s report on internal control wouldcontain an adverse opinion.In this case, the auditor has evidence that the test of control procedures are not effective, but no exceptions in the sample resulted because of the breakdown. An expansion of the attributestest does not seem advisable and therefore, the auditor shouldprobably expand confirmation of accounts receivable tests. Inaddition, he or she should write a letter to management to informthem of the control breakdown.d. Although misstatements are more likely when controls are noteffective, control deviations do not necessarily result in actualmisstatements. These control deviations involved a lack ofindication of internal verification of pricing, extensions and footingsof invoices. The deviations will not result in actual errors if pricing,extensions and footings were initially correctly calculated, or if theindividual responsible for internal verification performed theprocedure but did not document that it was performed.e. In this case, we want to find out why some invoices are notinternally verified. Possible reasons are incompetence,carelessness, regular clerk on vacation, etc. It is desirable to isolatethe exceptions to certain clerks, time periods or types of invoices.Case15-34a. Audit sampling could be conveniently used for procedures 3 and 4 since each is to be performed on a sample of the population.b. The most appropriate sampling unit for conducting most of the auditsampling tests is the shipping document because most of the testsare related to procedure 4. Following the instructions of the auditprogram, however, the auditor would use sales journal entries asthe sampling unit for step 3 and shipping document numbers forstep 4. Using shipping document numbers, rather than thedocuments themselves, allows the auditor to test the numericalcontrol over shipping documents, as well as to test for unrecordedsales. The selection of numbers will lead to a sample of actualshipping documents upon which tests will be performed.。

ACCA P5 Summary

1Introduction to strategic management accounting1.1I ntroduction to planning, control and decision making☞Strategic planning is the process of deciding on objectives of the organization, on changes in these objectives, on the resource to attain these objectives, and on the policies that are to govern the acquisition, use and disposition of these resources.☞Characteristics of strategic information⏹Long term and wide scope⏹Generally formulated in writing⏹Widely circulated广泛流传⏹Doesn’t trigger direct action, but series of lesser plans⏹Includes selection of products, purchase of non-current assets, required levels ofcompany profit☞Management control: the process by which management ensure that resources are obtained and used effectively and efficiently in the accomplishment of the organisation’s objectives. It is sometimes called tactics ad tactical planning.☞Characteristics of management accounting information⏹Short-term and non-strategic⏹Management control planning activities include preparing annual sales budget⏹Management control activities include ensuring budget targets are reached⏹Carried out in a series of routine and regular planning and comparison procedures⏹Management control information covers the whole organisation, is routinely collected,is often quantitative and commonly expressed in money terms (cash flow forecasts, variance analysis reports, staffing levels⏹Source of information likely to be endogenous内生的☞Characteristics of operational control⏹Short-term and non-strategic⏹Occurs in all aspects of an organisations activities and need for day to dayimplementation of plans⏹Often carried out at short notice⏹Information likely to have an endogenous source, to be detailed transaction data,quantitative and expressed in terms of units/hours⏹Includes customer orders and cash receipts.1.2Management accounting information for strategic planning and control☞Strategic management accounting is a form of management accounting in which emphasis is placed on information about factors which are external to the organisation, as well as non-financial and internally-generated information.⏹External orientation: competitive advantage is relative; customer determination⏹Future orientation: forward- and outward looking; concern with values.⏹Goal congruence: translates the consequences of different strategies into a commonaccounting language for comparison; relates business operations to financial performance.1.3Planning and control at strategic and operational levels☞Linking strategy and operations, if not: unrealistic plans, inconsistent goals, poor communication, inadequate performance measurement.1.3.1Strategic control systems☞Formal systems of strategic control:⏹strategy review;⏹identify milestones of performance( outline critical success factors, short-term stepstowards long-term goals, enables managers to monitor actions)⏹Set target achievement levels (targets must be reasonably precise, suggest strategiesand tactics, relative to competition)⏹Formal monitoring of the strategic process⏹Reward.☞Desired features of strategic performance measures⏹Focus on what matters in the long term⏹Identify and communicate drivers of success⏹Support organisational learning⏹Provide a basis for reward⏹Measurable; meaningful; acceptable;⏹Described by strategy and relevant to it⏹Consistently measured⏹Re-evaluated regularly1.4Benchmarking1.4.1Types of benchmarking☞Internal benchmarking: easy; no innovative or best-practice.☞Industry benchmarking:⏹Competitor benchmarking: difficult to obtain information⏹Non-competitor benchmarking: motivate☞Functional benchmarking: find new, innovative ways to create competitive advantage1.4.2Stages of benchmarking☞Set objectives and determine the area to benchmark☞Establish key performance measures.☞Select organizations to study☞Measure own and others performance☞Compare performance☞Design and implement improvement prgoramme☞Monitor improvements1.4.3Reasons for benchmarking☞Assess current strategic position☞Assess generic competitive strategy☞Spur to innovation☞Setting objectives and targets☞Cross comparisons☞Implementing change☞Identifies the process to improve☞Helps with cost reduction, or identifying areas where improvement is required☞Improves the effectiveness of operations☞Delivers services to a defined standard☞Provide early warning of competitive disadvantage1.4.4Disadvantages of benchmarking☞Implies there is one best way of doing business☞Yesterday’s solution to tomorrow’s problem☞Catching-up exercise rather than the development of anything distinctive☞Depends on accurate information about comparator companies☞Potential negative side effects of ‘what gets measured gets done’.2Performance management and control of the organization2.1Strengths and weaknesses of alternative budget models2.1.1Incremental budgeting☞Is the traditional approach to setting a budget and involves basing next year’s budget on the current year’s results plus an extra amount for estimated growth of inflation next year. ☞Strengths: easy to prepare; can be flexed to actual levels to provide more meaningful control information☞Weaknesses: does not take account of alternative options; does not look for ways of improving performance; only works if current operations are as effective, efficient and economical as they can be; encourage slack in the budget setting process.2.1.2Zero based budgeting☞Preparing a budget for each cost centre from scratch.☞Strengths:⏹Provides a budgeting and planning tool for management that responds to changes inthe business environment.⏹Requires the organization to look very closely at its cost behavior patterns, andimproves understanding of cost-behaviour patterns.⏹Should help identify inefficient or obsolete processes, and thereby also help reducecosts.⏹Results in a more efficient allocation of resources⏹Be particularly useful in not-for-profit organizations which have a focus on achievingvalue for money.☞Weaknesses:⏹Requires a lot of management time and effort⏹Requires training in the use of ZBB techniques so that these are applied properly⏹Questioning current practices and processes can be seen as threatening2.1.3Rolling budgets☞Continuously updated by adding a further period when the earliest period has expired.☞Strengths:⏹Reduce the uncertainty of budgeting for business operating in an unstableenvironment. It is easier to predict what will happen in the short-term.⏹Most suitable form of budgeting for organizations in uncertain environments, wherefuture activity levels, costs or revenues cannot be accurately foreseen.⏹Planning and control is based on a more recent plan which is likely to be morerealistic an more relevant than a fixed annual budget drawn up several months ago.⏹The process of updating the budget means that managers identify current changes( and so can respond to these changes more quickly)⏹More realistic targets provide a better basis on which to appraise managers’performance⏹Realistic budgets are likely to have a better motivational effect on managers.☞Weaknesses:⏹Require time, effort and money to prepare and keep updating. If managers spend toolong preparing/revising budgets, they will have less time to control and manage actual results⏹Managers may not see the value in the continuous updating of budgets⏹May be demotivating if targets are constantly changing⏹It may not be necessary to update budgets so regularly in a stable operatingenvironment.2.1.4Flexible budgets☞Recognizing the potential uncertainty, budgets designed to adjust costs levels according to changes in the actual levels of activity and output.☞Strengths:⏹Finding out well in advance the costs of idle time and so on if the output falls belowbudget.⏹Being able to plan for the alternative use of spare capacity if output falls short ofbudget☞Weaknesses:⏹As many errors in modern industry are fixed costs, the value of flexible budgets as aplanning tool are limited.⏹Where there is a high degree of stability, the administrative effort in flexiblebudgeting produces little extra benefit. Fixed budgets can be perfectly adequate in these circumstances.2.1.5Activity based budgeting☞Involves defining the activities that underlie the financial figures in each function and usingthe level of activity to decide how much resources should be allocated, how well it is being managed and to explain variance from budget.☞Strengths:⏹Ensures that the organisation’s overall strategy and any changes to that strategy willbe taken into account.⏹Identifies critical success factors which are activities that a business must perform wellif it is to succeed⏹Recognizes that activities drive costs; so encourages a focus on controlling andmanaging cost drivers rather than just the costs⏹Concentrate on the whole activities so that there is more likelihood of getting it rightfirst time.☞Weaknesses:⏹Requires time and effort to prepare so suited to a more complex organization withmultiple cost drivers.⏹May be difficult to identify clear individual responsibilities for activities⏹Only suitable for organization which have adopted an activity-based costing system⏹ABBs are not suitable for all organization, especially with significant proportions offixed overheads.2.1.6The future of budgeting☞Criticisms of traditional budgeting⏹Time consuming and costly⏹Major barrier to responsiveness, flexibility and change⏹Adds little value given the amount of management time required⏹Rarely strategically focused⏹Makes people feel undervalued⏹Reinforces department barriers rather than encouraging knowledge sharing⏹Based on unsupported assumptions and guesswork as opposed to sound,well-constructed performance data⏹Development and updated infrequently2.2Budgeting in not-for-profit organizations☞Special issues: the budget process inevitably has considerable influence on organizational processes, and represents the financial expression of policies resulting from politically motivated goals and objectives. The reality of life for many public sector managers is an subjected to(受---支配) growing competition.⏹Be prevented from borrowing funds⏹Prevent the transfer of funds from one budget head to another without compliancewith various rules and regulations⏹Plan one financial year.⏹Incremental budgeting and the bid system are widely used.2.3Evaluating the organisation’s move beyond budgeting2.3.1Conventional budgeting in a changing environment☞Weaknesses of traditional budgets:⏹Adds little value, requires far too much valuable management time⏹Too heavy a reliance on the ‘agreed’ budget has an adverse impact on managementbehavior, which can become dysfunctional(功能失调的) with regard to(关于) the objectives of the organization as a whole⏹The use of budgeting as a base for communicating corporate goals, is contrary to theoriginal purpose of budgeting as a financial control mechanism⏹Most budgets are not based on a rational, causal(因果关系的) model of resourceconsumption, but are often the result of protracted internal bargaining processes.⏹Conformance to budget is not seen as compatible with a drive towards continuousimprovement⏹Traditional budgeting processes have insufficient external focus.2.3.2The beyond budgeting model☞Rolling budgets focus management attention on current and likely future realities within the organizational context, it is seen as an attempt to keep ahead of change, or strictly speaking to be more in control of the response to the challenges facing the organization. ☞Benefits:⏹Creates and fosters a performance climate based on competitive success. Managerialfocus shifts from beating other managers for a slice(部分) of resources to beating the competition.⏹It motivates properly by giving them challenges, responsibilities and clear values asguidelines. Rewards are team-based⏹It empowers operational managers to act by removing resource constraints. Speedingup the response to environmental threats and enabling quick exploitation of new opportunities.⏹It devolves performance responsibilities to operational management who are closer tothe action.⏹It establishes customer-orientated teams that are accountable for profitable customeroutcomes.⏹Creates transparent and open information systems throughout the organization,provides fast, open and distributed information to facilitate control at all levels.3Business structure, IT development and other environmental and ethical issues3.1Business structure and information needs3.1.1Functional departmentation☞Information characteristics and needs: information flows vertically; functions tend to be isolated☞Implications for performance management⏹Structure is based on work specialism⏹Economies of scale⏹Does not reflect the actual business processes by which values is created⏹Hard to identify where profits and losses are made on individual products or inindividual markets⏹People do not have an understanding of how the whole business works⏹Problems of co-ordinating the work of different specialisms.3.1.2The divisional form☞Information characteristics and needs⏹Divisionalisation is the division of a business into autonomous regions⏹Communication between divisions and head office is restricted, formal and related toperformance standards⏹Headquarters management influence prices and therefore profitability when it setstransfer prices between divisions.⏹Divisionalisation is a function of organisation size, in numbers and in product-marketactivities.☞Implications for performance management⏹Divisional management should be free to use their authority to do what they think isright, but must be held accountable to head office⏹ A division must be large enough to support the quantity and quality of managementit needs⏹Each division must have a potential for growth in its own area of operations⏹There should be scope and challenge in the job for the management of the division☞Advantages:⏹Focuses the attention of subordinate(下级) management on business performanceand results⏹Management by objectives can be applied more easily⏹Gives more authority to junior managers, more senior positions⏹Tests junior managers in independent command early in their careers and at areasonably low level in the management hierarchy.⏹Provides an organisation structure which reduces the number of levels ofmanagement.☞Problems:⏹Partly insulated from shareholders and capital markets⏹The economic advantages it offers over independent organisations ‘reflectfundamental inefficiencies in capital markets’⏹The divisions are more bureaucratic than they would be as independent corporation⏹Headquarters management usurp divisional profits by management charges,cross-subsidies, unfair transfer pricing systems.⏹Sometime, it is impossible to identify completely independent products or markets⏹Divisionalisation is only possible at a fairly senior management level⏹Halfway house(中途地点)⏹Divisional performance is not directly assessed by the market⏹Conglomerate diversification3.1.3Network organisations☞Information characteristics and needs: achieve innovative response in a changingcircumstances; communication tends to be lateral(侧面的), information and advice are given rather than instructions(指令) and decisions.☞Virtual teams: share information and tasks; make joint decision; fulfil the collaborative function of a team)☞Implications for performance management⏹Staffing: shamrock organisation⏹Leasing of facilities such as IT, machinery and accommodation(住房)⏹Production itself might be outsourced⏹Interdependence of organisations☞Benefits: cost reduction; increased market penetration; experience curve effects.3.2Business process re-engineering3.2.1Business processes and the technological interdependence betweendepartments☞Pooled interdependence(联营式相互依赖): each department works independently to the others, subjects to achieve the overall goals☞Sequential interdependence(序列式相互依存): a sequence with a start and end point.Management effort is required to ensure than the transfer of resources between departments is smooth.☞Reciprocal interdependence(互惠式相互依存): a number of departments acquire inputs from and offer outputs to each other.3.2.2Key characteristics of organisations which have adopted BPR☞Work units change from functional departments to process teams, which replace the old functional structure☞Jobs change. Job enlargement and job enrichment☞People’s roles change. Make decisions relevant to the process☞Performance measures concentrate on results rather than activities.☞Organisation structures change from hierarchical to flat3.3Business integration3.3.1Mckinsey 7S model☞Hard elements of business behaviour⏹Structure: formal division of tasks; hierarchy of authority⏹Strategy: plans to outperform胜过its competitors.⏹Systems: technical systems of accounting, personnel, management information☞‘soft’ elements⏹Style: shared assumptions, ways of working, attitudes and beliefs⏹Shared values: guiding beliefs of people in the organisation as to why it exists⏹Staff: people⏹Skills: those things the organisation does well3.3.2Teamwork and empowerment☞Aspects of teams:⏹Work organisation: combine the skills of different individuals and avoid complexcommunication⏹Control: control the behaviour and performance of individuals, resolve conflict⏹Knowledge generation: generate ideas⏹Decision making: investigate new developments, evaluate new decisions☞Multi-disciplinary teams:⏹Increases workers‘ awareness of their overall objectives and targets⏹Aids co-ordination⏹Helps to generate solutions to problems, suggestions for improvements☞Changes to management accounting systems⏹Source of input information: sources of data, methods used to record data⏹Processing involved: cost/benefit calculation⏹Output required: level of detail and accuracy of output, timescales involved⏹Response required:⏹When the output is required:3.4Information needs of manufacturing and service businesses3.4.1Information needs of manufacturing businesses☞Cost behaviour:⏹Planning: standard costs, actual costs compared with⏹Decision making: estimates of future costs to assess the likely profitability of a product⏹Control: monitor total cost information☞Quality: the customer satisfaction is built into the manufacturing system and its outputs☞Time: production bottlenecks, delivery times, deadlines, machine speed☞Innovation: product development, speed to market, new process. Experience curve, economies of scale, technological improvements.☞Valuation:☞Strategic, tactical and operational information⏹Strategic: future demand estimates, new product development plans, competitoranalysis⏹Tactical: variance analysis, departmental accounts, inventory turnover⏹Operational: production reject rates, materials and labour used, inventory levels3.4.2Service businesses☞Characteristics distinguish from manufacturing:⏹Intangibility: no substance⏹Inseparability/simultaneity: created at the same time as they are consumed⏹Variability/heterogeneity异质性: problem of maintaining consistency in the standardof output⏹Perishability非持久性:⏹No transfer of ownership:☞Strategic, tactical and operational information⏹Strategic: forecast sales growth and market share, profitability, capital structure⏹Tactical: resource utilisation, customer satisfaction rating⏹Operational: staff timesheets, customer waiting time, individual customer feedback3.5Developing management accounting systems3.5.1Setting up a management accounting system☞The output required: identify the information needs of managers☞When the output is required:☞The sources of input information: the output required dictate the input made3.6Stakeholders’ goals and objectives3.6.1The stakeholder view☞Organisations are rarely controlled effectively by shareholders☞Large corporations can manipulate markets. Social responsibility☞Business receive a lot of government support☞Strategic decisions by businesses always have wider social consequences.3.6.2Stakeholder theory☞Strong stakeholder view: each stakeholder in the business has a legitimate claim on management attention. Management’s job is to balance stakeholder demands:⏹Managers who are accountable to everyone are accountable to none⏹Danger of the managers favour their own interests⏹Confuses a stakeholder’s interest in a firm with a person citizenship of a state⏹People have interest, but this does not give them rights.3.7Ethics and organisation3.7.1Short-term shareholder interest(laissez-faire自由主义stance)☞Accept a duty of obedience to the demands of the law, but would not undertake to comply with any less substantial rules of conduct.3.7.2Long-term shareholder interest (enlightened self-interest开明自利)☞The organisation’s corporate image may be enhanced by an assumption of wider responsibilities.☞The responsible exercise of corporate power may prevent a built-up of social and political pressure for legal regulation.3.7.3Multiple stakeholder obligations☞Accept the legitimacy of the expectations of stakeholders other than shareholders. It is important to take account of the views of stakeholders with interests relating to social and environmental matters.☞Shape of society: society is more important than financial and other stakeholder interests.3.7.4Ethical dilemmas☞Extortion: foreign officials have been known to threaten companies with the complete closure of their local operations unless suitable payments are made☞Bribery: payments for service to which a company is not legally entitled☞Grease money: cash payments to the right people to oil the machinery of bureaucracy.☞Gifts: are regard as an essential part of civilised negotiation.4Changing business environment and external factors4.1The changing business environment4.1.1The changing competitive environment☞Manufacturing organisations:⏹Before 1970s, domestic markets because of barriers of communication andgeographical distance, few efforts to maximise efficiency and improve management practices.⏹After 1970s, overseas competitors, global networks for acquiring raw materials anddistributing high-quality, low-priced goods.☞Service organisations:⏹Prior to the 1980s: service organisations were government-owned monopolies, wereprotected by a highly-regulated, non-competitive environment.⏹After 1980s: privatisation of government-owned monopolies and deregulation, intensecompetition, led to the requirement of cost management and management accounting information systems.☞Changing product life cycles: competitive environment, technological innovation, increasingly discriminating and sophisticated customer demands.☞Changing customer requirements: Cost efficiency, quality (TQM), time (speedier response to customer requests), innovation☞New management approaches: continuous improvement, employee empowerment; total value-chain analysis☞Advanced manufacturing technology(AMT): encompasses automatic production technology, computer-aided design and manufacturing, flexible manufacturing systems and a wide array of innovative computer equipment.4.1.2The limitation of traditional management accounting techniques in achanging environment☞Cost reporting: costs are generally on a functional basis, the things that businesses do are “process es’ that cut across functional boundaries☞Absorption costing(归纳成本计算法)☞Standard costing: ignores the impact of changing cost structures; doesn’t provide any incentive to try to reduce costs further, is inconsistent with the philosophy of continuous improvement.☞Short-term financial measures: narrowly focused☞Cost accounting methods: trace raw materials to various production stages via WIP. With JIT systems, near-zero inventories, very low batch sizes, cost accounting and recording systems are greatly simplified.☞Performance measures: product the wrong type of response☞Timing: cost of a product is substantially determined when it is being designed, however, management accountants continue to direct their efforts to the production stage.☞Controllability: only a small proportion of ‘direct costs’are genuinely controllable in the short term.☞Customers: many costs are driven by customers, but conventional cost accounting does not recognise this.☞The solution: changes are taking place in management accounting in order to meet the challenge of modern developments.4.2Risk and uncertainty4.2.1Types of risk and uncertainty☞Physical: earthquake, fire, blooding, and equipment breakdown. Climatic changes: global warming, drought;☞Economic: economic environment turn out to be wrong☞Business: lowering of entry barriers; changes in customer/supplier industries; new competitors and factors internal to the firm; management misunderstanding of core competences; volatile cash flows; uncertain returns☞Product life cycle:☞Political: nationalisation, sanctions, civil war, political instability☞Financial:4.2.2Accounting for risk☞Quantify the risk:⏹Rule of thumb methods: express a range of values from worst possible result to bestpossible result with a best estimate lying between these two extremes.⏹Basic probability theory: expresses the likelihood of a forecast result occurring⏹Dispersion or spread values with different possible outcomes: standard deviation.4.2.3Basic probability theory and expected valuesEV=ΣpxP=the probability of an outcome occurringX=the value(profit or loss) of that outcome4.2.4Risk preference☞Risk seeker: is a decision maker who is interested trying to secure the best outcomes no matter how small the chance they may occur☞Risk neutral: a decision maker is concerned with what will be the most likely outcome☞Risk averse: a decision maker acts on the assumption that the worst outcome might occur ☞Risk appetite is the amount of risk an organisation is willing to take on or is prepared to accept in pursuing its strategic objectives.4.2.5Decision rules☞Maximin decision rule: select the alternative that offers the least unattractive worst outcome. Maximise the minimum achievable profit.⏹Problems: risk-averse approach, lead to defensive and conservative, without takinginto account opportunities for maximising profits⏹Ignores the probability of each different outcome taking place☞Maximax: looking for the best outcome. Maximise the maximum achievable profit⏹It ignores probabilities;⏹It is over-optimistic☞Minimax regret rule: minimise the regret from making the wrong decision. Regret is the opportunity lost through making the wrong decision⏹Regret for any combination of action and circumstances=profit for best action in shoescircumstances – profit for the action actually chosen in those circumstances4.3Factors to consider when assessing performance4.3.1Political factors☞Government policy; government plans for divestment(剥夺)/rationalisation; quotas, tariffs, restricting investment or competition; regulate on new products.☞Government policy affecting competition: purchasing decisions; regulations and control;policies to prevent the concentration of too much market share in the hands of one or two producers4.3.2Economic environment☞Gross domestic product: grown or fallen? Affection on the demand of goods/services☞Local economic trends: businesses rationalising or expanding? Rents increasing/falling?The direction of house prices moving? Labour rates☞Inflation: too high to making a plan, uncertain of future financial returns; too low to depressing consumer demand; encouraging investment in domestic industries; high rate leading employees to demand higher money wages to compensate for a fall in the value of their wages☞Interest rates: affect consumer confidence and liquidity, demand; cost of borrowing increasing, reducing profitability;☞Exchange rates: impact on the cost of overseas imports; prices affect overseas customers ☞Government fiscal policy: increasing/decreasing demands; corporate tax policy affecting on the organisation; sales tax(VAT) affecting demand.☞Government spending:☞Business cycle: economic booming or in recession; counter-cyclical industry; the forecast state of the economic4.3.3Funding☞Reasons for being reluctant to obtain further debt finance:⏹Fear the company can’t service the debt, make the required capital and interestpayments on time⏹Can’t use the tax shield, to obtain any tax benefit from interest payments⏹Lacks the asset base to generate additional cash if needed or provide sufficientsecurity⏹Maintain access to the capital markets on good terms.4.3.4Socio-cultural factors☞Class: different social classes have different values。

亨格瑞管理会计英文第15版练习答案解析