公司金融课后题答案CHAPTER-18

公司理财全书课后答案及人大金融考研

公司理财全书课后答案及人大金融考研操作指南:大家一般都是用的中文版本,所以题目和英文原书有些出入,我提供的是英文版的详细答案,除了概念题外,都没有原始题目对应,但是这并不防碍大家找到答案,因为中文和英文的题目在数字上全是一致的,所以大家拿着这份答案可以很容易的找到书中的题目.我今年已经确定被录取了,马上要去工作一段时间了然后准备上学去了.最后写点东西给08的DDMM 吧关于理财:建议大家提早看,因为复试的时候其他几门全是记忆的,而理财想在短期提高很不容易,所以大家如果有时间,建议大家在初试前看一看,熟悉一下,理财的重点是前18章+第22章关于其它三门复试课程:金融学要记忆的很多,而且很多地方都有出题的可能,商行的重点很集中就是第9章,证券和理财重叠的知识很多所以看好理财,证券也就基本拿下了,技术分析那章具体的如K线,波浪线,形态理论等看不懂就算了,考试基本不会涉及的.关于人大考研初试公共课:总的来说,你考试的成败就取决于数学上面,当然其它的你要保证上线,想靠英语政治提分很难,北京今年压分压的太厉害,唯一压不了的只有数学,数学的结果是确定的,对就是对,错就是错,但英语政治2卷就不然,你的作文觉得能拿15分,老师就是给你3分你能怎么样呢? 所以劝大家好好学好数学,其他2门中庸一下也不会影响大局,当然对于立志做人大金融第一又或者冲着公费去的DDMM,可以忽略我上面的那段话.推荐几本书吧:数学:基础还行的话直接看二李的复习全书吧不推荐老陈的二李的看3遍然后做660 11月开始做400+真题就足够了我考2次都是这么复习的题目要反复做特别是660 那书你做透了选择填空不会扣分 400最后做按时间严格做做3遍真题再好好看看简单的卷子140 难的这样的分数基本没问题的如果想150 基本要看发挥了政治:看红宝书看3遍不用背但要认真看选择都是那里面的(当然今年有2个题目确实不是,出题的人因此被狂骂)最后一定记得买20天20题那个一定要背每年大题基本都能压到的8月开始准备政治就行了到最后冲刺的时候多花点时间背 75左右没问题的英语: 我只看过真题,看了很多遍.初试专业课:3本指定教材足够了,好好看几遍,重点的东西记忆一下,至于西经计算,考的很EASY的,没时间的话不专门准备也可,IS-LM的计算几乎每年都考,不过很简单的最后祝大家好运,周2回京工作去了,感谢在这里陪我度过考研的每个人.........R,KEVIN,橙子,大K,小鱼...........9月人大见啦~ ~理财答案感谢橙子,这个答案是给我的,很不错,每个题目都有详细的过程,这样让我轻松的在英文中找到了中文原题)CONCEPT部分解决是是所有章节的概念题CONCEPT QUESTIONS - CHAPTER 11.1 · What are the three basic questions of corporate finance?a. Investment decision (capital budgeting): What long-term investment strategy should a firm adopt?b. Financing decision (capital structure): How much cash must be raised for therequired investments?c. Short-term finance decision (working capital): How much short-term cash flow does company need to pay its bills.· Describe capital structure.Capital structure is the mix of different securities used to finance a firm's investments.· List three reasons why value creation is difficult.Value creation is difficult because it is not easy to observe cash flows directly. The reasons are: a. Cash flows are sometimes difficult to identify.b. The timing of cash flows is difficult to determine.c. Cash flows are uncertain and therefore risky.1.2 · What is a contingent claim?A contingent claim is a claim whose payoffs are dependent on the value of the firm at the end ofthe year. In more general terms, contingent claims depend on the value of an underlng asset.· Describe equity and debt as contingent claims. Both debt and equity depend on the value of the firm. If the value of the firm is greater than the amount owed to debt holders, they will get what the firm owes them, while stockholders will get the difference. But if the value of the firm is less than equity, bondholders will get the value of the firm and equity holders nothing.1.3 · Define a proprietorship, a partnership anda corporation.A proprietorship is a business owned by a single individual with unlimited liability. A partnership is a business owned by two or more individuals with unlimited liability. A corporation is a business which is a "legal person" with many limited liability owners.· What are the advantages of the corporate form of business organization?Limited liability, east of ownership transfer and perpetual succession.1.4 · What are the two types of agency costs? Monitoring costs of the shareholders and the incentive fees paid to the managers.· How are managers bonded to shareholders? a. Shareholders determine the membership to the board of directors, which selects management.b. Management contracts and incentives are build into compensation arrangements.c. If a firm is taken over because the firm's price dropped, managers could lose their jobs.d. Competition in the managerial labor market makes managers perform in the best interest of stockholders.· Can you recall some managerial goals?Maximization of corporate wealth, growth and company size.· What is the set-of-contracts perspective? The view of the corporation as a set of contracting relationships among individuals who have conflicting objectives.1.5 · Distinguish between money markets and capital markets.Money markets are markets for debt securities that pay off in less than one year, while capital markets are markets for long-term debt and equity shares.· What is listing?Listing refers to the procedures by which a company applies and qualifies so that its stock can be traded on the New York Stock Exchange.· What is the difference between a primary market and a secondary market?The primary market is the market where issuers of securities sell them for the first time to investors, while a secondary market is a market for securities previously issued.CONCEPT QUESTIONS - CHAPTER 22.1 · What is the balance-sheet equation? Assets = Liabilities + Stockholders' equity· What three things should be kept in mind when looking at a balance sheet?Accounting liquidity, debt vs. equity, and value vs. cost.2.2 · What is the income statement equation? Revenue - expenses = Income· What are the three things to keep in mind when looking at an income statement?Generally Accepted Accounting Principles (GAAP), noncash items, and time and costs.· What are noncash e xpenses?Noncash expenses are items included as expenses but which do not directly affect cash flow. The most important one is depreciation.2.3 · What is net working capital?It is the difference between current assets and current liabilities.· What is the change in net working capital? To determine changes in net working capital you subtract uses of net working capital from sources of net working capital.2.4 · How is cash flow different from changes in net working capital?The difference between cash flow and changes in new working capital is that some transactions affect cash flow and not net working capital. Theacquisition of inventories with cash is a good example of a change in working capital requirements.· What is the difference between opera ting cash flow and total cash flow of the firm?The main difference between the two is capital spending and additions to working capital, that is, investment in fixed assets and "investment" in working capital.CONCEPT QUESTIONS - CHAPTER 33.1 · What i s an interest rate?It is the payment required by the lender of money for the use of it during a determined period of time. It is expressed in percentage.· What are institutions that match borrowers and lenders called?They are called financial institutions.· What do we mean when we say a market clears? What is an equilibrium rate of interest?A market clears if the amount of money borrowers want to borrow is equal to the amount lenders wish to lend. An equilibrium rate of interest is the interest rate at which markets clear.3.2 · How does an individual change his consumption across periods throughborrowing and lending.By borrowing and lending different amounts the person can achieve any of all consumption possibilities available.· How do interest r ate changes affect one's degree of impatience?A person's level of patience depends upon the interest rate he or she faces in the market. A person eager to borrow money at a low interest rate will become less eager if that interest rate is raised and may prefer to lend money to take advantage of higher interest rates.3.3 · What is the most important feature of a competitive financial market?No investor, individual or corporation can have a significant effect on total lending or on interest rates. Therefore, investors are price takers.· What conditions are likely to lead to this?a. Trading is costless.b. Information about borrowing and lending opportunities is availablec. There are many traders.3.4 · Describe the basic financial principle of investment decision-making?An investment project is worth undertaking only if it is mores desirable than what is available in the financial markets.3.5 · Describe how the financial markets can be used to evaluate investmentalternatives?The financial markets can be used as a benchmark. If the proposed investment provides a better alternative than the financial markets, it should be undertaken.· What is the separation theorem? Why is it important?The separation theorem says that the decision as to whether to undertake a project (compared to the financial markets) is independent of the consumption preferences of the individual. It is important because we can make investment decisions based on objective data, disregarding personal preferences.3.6 · Give the definitions of net present value, future value and present value?New present value is the difference in present value terms between cash inflows and cash outflows. Given the financial market, the future value is an amount equivalent to the amountcurrently held, and present value is the amount equivalent to an amount to be received or given in the future.· What information does a person need to compute an investment's net presentvalue?Cash inflows, cash outflows and an interest or discount rate.3.7 · In terms of the net-present-value rule, what is the essential differencebetween the individual and the corporation. The main difference is that firms have no consumption endowment.CONCEPT QUESTIONS - CHAPTER 44.1 · Define future value and present value. Future value is the value of a sum after investing over one or more periods. Present value is thevalue today of cash flows to be received in the future.· How does one use net present value when making an investment decision?One determines the present value of future cash flows and then subtracts the cost of the investment. If this value is positive, the investment should be undertaken. If the NPV is negative, then the investment should be rejected.4.2 · What is the difference between simple interest and compound interest?With simple interest, the interest on the original investment is not reinvested. With compound interest, each interest payment is reinvested and one earns interest on interest.· What is the formula for the net present value of a project?TNPV = -C0 + å Ct /(1+I)tt=14.3 · What is a stated annual interest rate? The stated annual interest rate is the annual interest rate without consideration of compounding.· What is an effective annual interest rate? An effective annual interest rate is a rate that takes compounding into account.· What is the relationship between the stated annual interest rate and the effective annual interest rate?Effective annual interest rate = (1 + (r/m) )m - 1.· Define continuous compoundin g.Continuous compounding compounds investments every instant.4.4 · What are the formulas for perpetuity, growing-perpetuity, annuity, andgrowing annuity?Perpetuity: PV = C/rGrowing Perpetuity: PV = C/(r-g)Annuity: PV = (C/r) [1-1/(1+r)T]Growing Annuity: PV = [C/(r-g)] [1-((1+g) / (1+r))T ]· What are three important points concerning the growing perpetuity formula?1. The numerator.2. The interest rate and the growth rate.3. The timing assumption.· What are four tricks concerning annuities?1. A delayed annuity.2. An annuity in advance3. An infrequent annuity4. The equating of present values of two annuities.CONCEPT QUESTIONS - CHAPTER 55.2 · Define pure discount bonds, level-coupon bonds, and consols.A pure discount bond is one that makes no intervening interest payments. One receives a single lump sum payment at maturity. A level-coupon bond is a combination of an annuity and a lump sum at maturity. A consol is a bond that makes interest payments forever.· Contrast the state interest rate and the effective annual interest rate for bonds pang semi-annual interest.Effective annual interest rate on a bond takes into account two periods of compounding per year received on the coupon payments. The state rate does not take this into account.5.3 · What is the relationship between interest rates and bond prices?There is an inverse relationship. When one goes up, the other goes down.· How does one calculate the eld to maturity on a bond?One finds the discount rate that equates the promised future cash flows with the price of the bond.5.8 · What are the three factors determining a firm's P/E ratio?1. Today's expectations of future growth opportunities.2. The discount rte.3. The accounting method.5.9 · What is the closing price of Gen eral Data? The closing price of General Data is 6 3/16.· What is the PE of General House?The PE of General House is 29.· What is the annual dividend of General Host? The annual dividend of General Host is zero.CONCEPT QUESTIONS - Appendix to Chapter 5· What is the difference between a spot interest rate and the eld to maturity?The eld to maturity is the geometric average of the spot rates during the life of the bond.· Define the forward rate.Given a one-year bond and a two-year bond, one knows the spot rates for both. The forward rate is the rate of return implicit on a one-year bond purchased in the second year that would equate the terminal wealth of purchasing the one-year bond today and another in one year with that of the two-year bond.·What is the relationship between the one-year spot rate, the two-year spot rate and the forward rate over the second year?The forward rate f2 = [(1+r2)2 /(1+r1 )] - 1· What is the expectation hypothesis?Investors set interest rates such that the forward rate over a given period equals the spot rate for that period.What is the liquidity-preference hypothesis? This hypothesis maintains that investors require a risk premium for holding longer-term bonds (i.e. they prefer to be liquid or short-term investors). This implies that the market sets the forward rate for a given period above the expected spot rate for that period.CONCEPT QUESTIONS - CHAPTER 66.2 · List the problems of the payback period rule.1. It does not take into account the time value of money.2. It ignores payments after the payback period.3. The cutoff period is arbitrary.· What are some advantages?1. It is simple to implement.2. It may help in controlling and evaluating managers.6.4 · What are the three steps in calculating AAR?1. Determine average net income.2. Determine average investment3. Divide average net income by average investment.· What are some flaws with the AAR approach?1. It uses accounting figures.2. It takes no account of timing.3. The cutoff period is arbitrary.6.5 · How does one calculate the IRR of a project? Using either trial-and-error or a financial calculator, one finds the discount rate that produces an NPV of zero.6.6 · What is the difference between independentprojects and mutually exclusiveprojects?An independent project is one whose acceptance does not affect the acceptance of another. A mutually exclusive project, on the other hand is one whose acceptance precludes the acceptance of another.· What are two problems with the IRR approach that apply to both independent and mutually exclusive projects?1. The decision rule depends on whether one is investing of financing.2. Multiple rates of return are possible.· What are two additional problems applng only to mutually exclusive projects?1. The IRR approach ignores issues of scale.2. The IRR approach does not accommodate the timing of the cash flows properly.6.7 · How does one calculate a project'sprofitability index?Divide the present value of the cash flows subsequent to the initial investment by the initial investment.· How is the profitability index applied to independent projects, mutually exclusive projects, and situations of capital rationing?1. With independent projects, accept the project if the PI is greater than 1.0 and reject if less than 1.0.2. With mutually exclusive projects, use incremental analysis, subtracting the cash flows of project 2 from project 1. Find the PI. If the PI is greater than 1.0, accept project 1. If less than 1.0, accept project 2.3. In capital rationing, the firm should simply rank the projects according to their respective PIs and accept the projects with the highest PIs, subject to the budget constrain.CONCEPT QUESTIONS - CHAPTER 77.1 · What are the three difficulties in determining incremental cash flows?1. Sunk costs.2. Opportunity costs3. Side effects.· Define sunk costs, opportunity costs, and side effects.1. Sunk costs are costs that have already been incurred and that will not be affected by the decision whether to undertake the investment.2. Opportunity costs are costs incurred by the firm because, if it decides to undertake a project, it will forego other opportunities for using the assets.3. Side effects appear when a project negatively affects cash flows from other parts of the firm.7.2 · What are the items leading to cash flow in any year?Cash flow from operations (revenue-operating costs-taxes) plus cash flow of investment (costof new machines + changes in net working capital + opportunity costs).· Why did we determi ne income when NPV Analysis discounts cash flows, not income?Because we need to determine how much is paid out in taxes.· Why is working capital viewed as a cash outflow?Because increases in working capital must be funded by cash generated elsewhere in the firm.7.3 · What is the difference between the nominal and the real interest rate?The nominal interest rate is the real interest rate with a premium for inflation.· What is the difference between nominal and real cash flows?Real cash flows are nominal cash flows adjusted for inflation.7.4 · What is the equivalent annual cost method of capital budgeting?The decision as to which of various mutually exclusive machines to buy is based on the equivalent annual cost. The EAC is determined by dividing the net present value of costs by an annuity factor that has the same life as the machines. The machine with the lowest EAC should be acquired.· Can you list the assumptions that we must to use EAC?1. All machines do the same job.2. They have different operating costs and lives3. The machine will be indefinitely replaced. CONCEPT QUESTIONS - CHAPTER 88.1 · What are the ways a firm can create positive NPV.1. Be first to introduce a new product.2. Further develop a core competency to product goods or services at lower costs than competitors.3. Create a barrier that makes it difficult for the other firms to compete effectively.4. Introduce variation on existing products to take advantage of unsatisfied demand5. Create product differentiation by aggressive advertising and marketing networks.6. Use innovation in organizational processes to do all of the above.· How can managers use the market to help them screen out negative NPV projects?8.2 · What is a decision tree?It is a method to help capital budgeting decision-makers evaluating projects involving sequential decisions. At every point in the tree, there are different alternatives that should be analyzed.· What are potential problems in using a decision tree?Potential problems 1) that a different discount rate should be used for different branches in the tree and 2) it is difficult for decision trees to capture managerial options.8.3 · What is a sensitivity analysis?It is a technique used to determine how the result of a decision changes when some of the parameters or assumptions change.· Why is it important to perform a sensitivity analysis?Because it provides an analysis of the consequences of possible prediction or assumption errors.· What is a break-even analysis?It is a technique used to determine the volume of production necessary to break even, that is, to cover not only variable costs but fixed costs aswell.· Describe how sensitivity analysis interacts with break-even analysis.Sensitivity analysis can determine how the financial break-even point changes when some factors (such as fixed costs, variable costs, or revenue) change.CONCEPT QUESTIONS - CHAPTER 99.1 · What are the two parts of total return? Dividend income and capital gain (or loss)· Why are unrealized capi tal gains or losses included in the calculation of returns? Because it is as much a part of returns as dividends, even if the investor decides to hold onto the stock and not to realize the capital gain.· What is the difference between a dollar returnand a percentage return?A dollar return is the amount of money the original investment provided, while percentage return is the percentage of the original investment represented by the total return.9.2 · What is the largest one-period return in the 63-year history of commonstocks we have displayed, and when did it occur? What is the smallest return, and when did it occur?Largest common stock return: 53.99% in 1933. Smallest common stock return: -43.34% in 1931.· In how many years did the common stock r eturn exceed 30 percent, and inhow many years was it below 20 percent?It exceeded 30% in 16 years. It was below 20% in 39 years.· For common stocks, what is the longest period of time without a single losingyear? What is the longest streak of losing years? There are 6 consecutive years of positive returns. The longest losing streak was 4 years.· What is the longest period of time such that if you have invested at thebeginning of the period, you would still not have had a positive return on your common-stock investment by the end?The longest period of time was 14 years (from 1929 to 1942).9.4 · What is the major observation about capital markets that we will seek toexplain?That the return on risky assets has been higher on average than the return on risk-free assets.· What does the observation tell us about investors for the period from 1926through 1994.An investor in this period was rewarded forinvestment in the stock market with an extra or excess return over what would have achieved by simply investing in T-bills.9.5 · What is the definition of sample estimates of variance and standarddeviation?Variance is given by Var (R) = (1 / (T-1) ) St (Rt - R)2 where T is the number of periods, Rt is the period return and R is the sample mean. Standard deviation is given by SD = Var 1/2. For large T, (T-1) may be approximated by T.· How does the normal distribution help us interpret standard deviation?For a normal distribution, the probability of having a return that is above or below the men by a certain amount only depends on the standard deviation.9.6 · How can financial managers use the history of capital markets to estimatethe required rate of return on nonfinancial investments with the same risk as the average common stock?They can determine the historical risk premium and add this amount to the current risk-free rate to determine the required return on investments of that risk.CONCEPT QUESTIONS - CHAPTER 1111.1· What are the two basic parts of a return?1. The expected part2. The surprise part· Under what conditions will some news have no effect on common stock prices?If there is no surprise in the news, there will not be any effect on prices. That is, the news was fully expected.11.2· Describe the difference between systematic risk and unsystematic risk.A systematic risk is any risk that affects a largenumber of assets, each to a greater or lesser degree. An unsystematic risk is a risk that specifically affects a single asset or a small group of assets.· Why is unsystematic risk sometimes referred to as idiosyncratic risk?Because information such as the announcement of a labor strike, may affect only some companies.11.3 · What is an inflation beta? A GNP beta? An interest-rate beta?An inflation beta is a measure of the sensitivity of a stock's return to changes in the expected inflation rate. A GNP beta measures the sensitivity of a stock's return to changes in the expected GNP. An interest rate beta reflects the sensitivity of a stock's return to changes in the market interest rate.· What is the difference between a k-factor model and the market model?The main difference is that the market model assumes that only one factor, usually a stock market aggregate, is enough to explain stock returns, while a k-factor model relies on k factors to explain returns.· Define the beta coefficient.The beta coefficient is a measure of the sensitivity of stock's return to unexpected changes in one factor.11.4· How can the return on a portfolio be expressed in terms of a factor model?It is the weighted average of expected returns plus the weighted average of each security's beta times a factor F plus the weighted average of the unsystematic risks of the individual securities.· What risk is diversified away in a large portfolio?The unsystematic risk.11.5· What is the relationship between the one-factor model and CAPM?Assuming the market portfolio is properly scaled, it can be shown that the one-factor model is identical to the CAPM.11.7 · Empirical models are sometimes called factor models. What is the difference between a factor as we have used it previously in this chapter and an attribute as we use it in this section?A factor is generally a market wide or industry wide factor proxng the systematic risk. An attribute is related with the returns of the stocks.· What is data mining and why might it overstate the relation between some stock attribute and returns?Choosing parameters because they have been shown to be related to returns is data mining. The relation found between some attribute and returnscan be accidental, thus overstated.· What is wrong with measuring the performance of a U.S. growth stock manager against a benchmark composed of English stocks?Using a benchmark composed of English stocks is wrong because the stocks included are not of the same style as those in a U.S. growth stock fund.CONCEPT QUESTIONS - CHAPTER 1212.1· What is the disadvantage of using too few observations when estimating beta?Small samples can lead to inaccurate estimations.· Wha t is the disadvantage of using too many observations when estimating beta?Firms may change their industries over time making observations from the distant past out-of-date.· What is the disadvantage of using the industry beta as the estimate of the beta of an individual firm?The operations of a particular firm may not be similar to the industry average.12.2· What are the determinants of equity betas?1. The responsiveness of a firm's revenues to economy wide movements.2. The degree of a firm's operating leverage.3. The degree of a firm's financial leverage.· What is the difference between an asset beta and an equity beta?Financial leverage.12.6h What is liquidity?Liquidity in this context means the cost of bung and selling stocks. Thosestocks that are expensive to trade are considered less liquid.。

国际公司金融习题答案--第十八章

国际公司金融课后习题答案--第十八章第十八章课后习题参考答案1. 谈谈税收在经济中的作用。

税收在市场经济中主要起资源配置作用,通过税收政策和税收制度,在不同部门之间对各种资源进行配置,并在这一过程中影响个人和公司的经济活动。

首先,税收的变动会直接或间接地影响商品价格,从而影响商品的供求状况。

其次,税收影响经济结构,不同的税收政策对不同产品、不同行业、不同地区、不同企业组织形式都会产生影响。

通过影响商品价格以及经济结构,税收政策使各种资源在不同部门、不同地区间流动,而这些流动带来的影响意味着国际公司将不得不就此做出相应的经营决策。

这表明税收在经济中的作用最终会通过不同的渠道影响国际公司的经营。

2. 国际税收体系中的税收中性是指什么?对于税收中性,当前流行的国际税收理论中大体有两种观点:一是资本输出中性,二是资本输入中性。

所谓资本输出中性,就是税收不应影响投资者在国内、国外投资地点的选择,也不应影响投资者在各不同国家之间的选择,从而能使资本在世界范围内得到有效配置。

资本输入中性则认为,不同国籍的纳税人在同一国家从事投资活动,应享受相同的税收待遇。

3. 重复征税对于国际公司经营有什么弊端?从法律角度看,国际重复征税导致从事跨国投资和其他各种经济活动的纳税人相对于从事国内投资和其他各种经济活动的纳税人承受更为沉重的税收负担,从而违背了税收中立和税负公平的税法原则。

从经济角度看,国际重复征税造成税负不公致使跨国纳税人处于不利的竞争地位,势必挫伤其从事跨国经济活动的积极性,从而阻碍国际间资金、技术和人员的正常流动和交往。

4. 出现国际重复征税的原因是什么?应如何解决?国际重复征税的出现,最根本的原因是税收管辖权出了问题。

甲国根据自己的税法,认为对一项收入应由自己征税;乙国则认为应由乙国征税,于是纳税管辖权出现了重合,两国都向同一项收入征收所得税,国际重复征税就出现了。

各国为了避免重复征税,会通过一定方式对国际公司已缴国外所得税进行抵免,从而消除或减轻这种不利影响。

最新《公司金融学》全本课后习题参考答案

最新《公司金融学》全本课后习题参考答案《公司金融》课后习题参考答案各大重点财经学府专业教材期末考试考研辅导资料第一章导论第二章财务报表分析与财务计划第三章货币时间价值与净现值第四章资本预算方法第五章投资组合理论第六章资本结构第七章负债企业的估值方法第八章权益融资第九章债务融资与租赁第十章股利与股利政策第十一章期权与公司金融第十二章营运资本管理与短期融资第一章导论1.治理即公司治理(corporate governance),它解决了企业与股东、债权人等利益相关者之间及其相互之间的利益关系。

融资(financing),是公司金融学三大研究问题的核心,它解决了公司如何选择不同的融资形式并形成一定的资本结构,实现企业股东价值最大化。

估值(valuation),即企业对投资项目的评估,也包括对企业价值的评估,它解决了企业的融资如何进行分配即投资的问题。

只有公司治理规范的公司,其投资、融资决策才是基于股东价值最大化的正确决策。

这三个问题是相互联系、紧密相关的,公司金融学的其他问题都可以归纳入这三者的范畴之中。

2.对于上市公司而言,股东价值最大化观点隐含着一个前提:即股票市场充分有效,股票价格总能迅速准确地反映公司的价值。

于是,公司的经营目标就可以直接量化为使股票的市场价格最大化。

若股票价格受到企业经营状况以外的多种因素影响,那么价值确认体系就存在偏差。

因此,以股东价值最大化为目标必须克服许多公司不可控的影响股价的因素。

第二章财务报表分析与财务计划1.资产负债表;利润表;所有者权益变动表;现金流量表。

资产= 负债+ 所有者权益2.我国的利润表采用“多步式”格式,分为营业收入、营业利润、利润总额、净利润、每股收益、其他综合收益和综合收益总额等七个盈利项目。

3.直接法是按现金收入和支出的主要类别直接反映企业经营活动产生的现金流量,一般以利润表中的营业收入为起算点,调整与经营活动有关项目的增减变化,然后计算出经营活动现金流量。

朱叶公司金融第二版【课后习题答案】

【复旦大学 431 金融学考研专业课重难点】

复旦大学 431 金融学专业课一共四门课程,即《投资学》, 《货币银行学》,《国际金融学》以及《公司金融学》。这四门课 的重要程度排序为:《国际金融学》,《投资学》,《公司金融》,《货

3

朱叶——《公司金融》——课后习题详解

点进行系统梳理,总结归纳就显得非常重要。

三、注重实际运用

我个人认为,对金融学把握不太好的表现之一就是不会实际 运用。例如,中国的广义货币(M2)当前存量大概为 80 万亿, 有同学会去根据中国的高能货币以及货币乘数算出来这个货币 存量吗?例如,同学们都学过国际金本位体系,布雷顿森林体系, 牙买加体系的知识。那么可否根据这些知识说明当前国际收支体 系的问题、汇率调节机制的问题或者未来国际收支体系的发展方 向?实际上,这些问题并不难以回答,仍然跳不出我们在书本上 学到的知识,只是很多同学从来没尝试过用书本上的知识来解释 现实。因此,学会实际运用,不仅可以使得同学们对知识理解得 更加深刻,更重要的是,它会使得同学们养成自己的经济学金融 学思维,而这正是复旦大学经济学院研究生所必须具备的素质!

(3)企业的投资决策问题。由于投资企业是创造和利用投资机会的最佳工具,从而成 为经济发展的根本驱动力。但在公司金融理论的研究中,一般都遵循费雪的分离原理,即公

7

朱叶——《公司金融》——课后习题详解

司的投资与融资决策是相分离的,莫迪格利安尼与米勒(1958)的开创性论文对此做了较为 严格的证明。然而,现实中的企业即使面临无限的投资机会,并不可能获得全部足够的资金 支持。因此,由于各种原因,企业可能面临着投资不足或者投资过度的两难处境。为了保证 企业能够有效把握投资机会,并能从可供选择的投资机会中筛选出最能实现其市场价值最大 化的投资项目,需要运用相应的金融技术与程序。随着金融理论与技术的发展,资本预算的 方法与程序,也处于不断的发展过程之中。

公司金融课后习题

公司具备哪些特征?大企业为何大多选择公司制?公司是以资本联合为基础,以营利为目的,依照法律规定的条件和法律规定的程序设立,具有法人资格的企业组织。

公司的基本特征在于是:1. 公司是资本的联合而形成的经济组织。

2.公司具有法人资格。

3.公司股东承担有限责任。

4.公司是以营利为目的的。

5.公司实行所有权与经营权分离。

6.公司依照法律设立和运行,是规范化程序较高的企业组织形式。

7.公司是永续存在的企业组织形式。

大企业选择公司制的原因:1、有利于形成一个产权明晰,权责明确,管理科学的现代公司制度,从而推动企业规模化、规范化、专业化的建设与发展。

2、可以实现所有权和经营权分离,实现企业发展决策的科学化、民主化,能避免由于组织的庞大,一个人知识、能力不足而导致决策的失误3、公司讲究的是团队精神,形成的是整体合力,发挥的是“拳头”优势。

只有部门齐全、分工细致的规模化的公司才能提供系统的服务,满足客户“一站式”、“一条龙”服务的需要。

4、可以使管理职业化、专业化,提高了管理的层次与水平,有利于树立服务品牌,使企业高效率运转和扩张。

同时,这种机制不仅有利于调节内部责权利关系,而且能够组织协调企业的整体行动,参与市场竞争。

5、公司制有利于形成投资主体多元化,有利于资本的积累,可以吸纳国家、组织和个人出资,任何所有制性质的主体均能够成为企业的出资者或股东。

6、公司制企业的产权结构决定了股东不能够直接对企业的运行施加影响,从而可以较大幅度地降低服务成本7、公司制企业的责任有限化成为降低企业经营风险的最佳手段。

公司制企业由于采取有限责任和股权可转让的形式,因而除破产等极少数特殊原因外,一般不会发生因股东更迭而导致企业解体的情况,这就使得企业能够步入可持续发展之路。

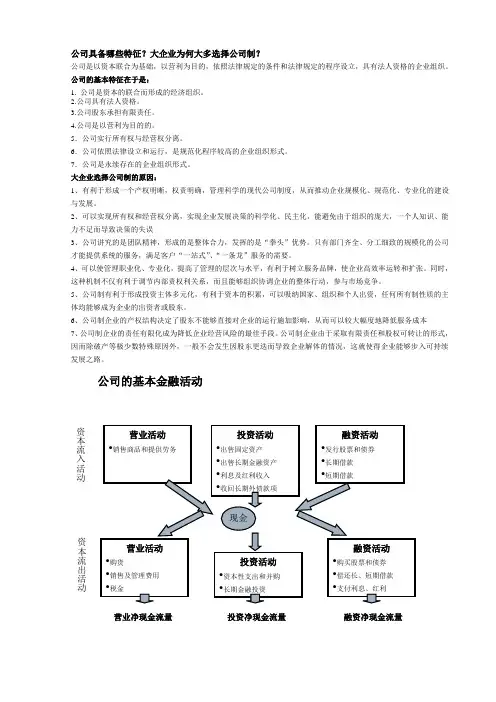

公司的基本金融活动营业净现金流量 投资净现金流量 融资净现金流量 资本流入活动资本流出活动如何理解公司价值最大化作为公司金融目标的合理性?企业价值不等于账面资产的总价值,它取决于企业潜在或预期获利能力。

最新《公司金融学》全本课后习题参考答案

《公司金融》课后习题参考答案各大重点财经学府专业教材期末考试考研辅导资料第一章导论第二章财务报表分析与财务计划第三章货币时间价值与净现值第四章资本预算方法第五章投资组合理论第六章资本结构第七章负债企业的估值方法第八章权益融资第九章债务融资与租赁第十章股利与股利政策第十一章期权与公司金融第十二章营运资本管理与短期融资第一章导论1.治理即公司治理(corporate governance),它解决了企业与股东、债权人等利益相关者之间及其相互之间的利益关系。

融资(financing),是公司金融学三大研究问题的核心,它解决了公司如何选择不同的融资形式并形成一定的资本结构,实现企业股东价值最大化。

估值(valuation),即企业对投资项目的评估,也包括对企业价值的评估,它解决了企业的融资如何进行分配即投资的问题。

只有公司治理规范的公司,其投资、融资决策才是基于股东价值最大化的正确决策。

这三个问题是相互联系、紧密相关的,公司金融学的其他问题都可以归纳入这三者的范畴之中。

2.对于上市公司而言,股东价值最大化观点隐含着一个前提:即股票市场充分有效,股票价格总能迅速准确地反映公司的价值。

于是,公司的经营目标就可以直接量化为使股票的市场价格最大化。

若股票价格受到企业经营状况以外的多种因素影响,那么价值确认体系就存在偏差。

因此,以股东价值最大化为目标必须克服许多公司不可控的影响股价的因素。

第二章财务报表分析与财务计划1.资产负债表;利润表;所有者权益变动表;现金流量表。

资产= 负债+ 所有者权益2.我国的利润表采用“多步式”格式,分为营业收入、营业利润、利润总额、净利润、每股收益、其他综合收益和综合收益总额等七个盈利项目。

3.直接法是按现金收入和支出的主要类别直接反映企业经营活动产生的现金流量,一般以利润表中的营业收入为起算点,调整与经营活动有关项目的增减变化,然后计算出经营活动现金流量。

间接法是以净利润为起算点,调整不涉及现金的收入、费用、营业外收支以及应收应付等项目的增减变动,据此计算并列示经营活动现金流量。

《公司理财》(第8版)第9-18章课后习题答案

《公司理财》(第8版)第9-18章课后习题答案第九章1. 因为公司的表现具有不可预见性。

2. 投资者很容易看到最坏的投资结果,但是确很难预测到。

3. 不是,股票具有更高的风险,一些投资者属于风险规避者,他们认为这点额外的报酬率还不至于吸引他们付出更高风险的代价。

4. 股票市场与赌博是不同的,它实际是个零和市场,所有人都可能赢。

而且投机者带给市场更高的流动性,有利于市场效率。

5. 在80年代初是最高的,因为伴随着高通胀和费雪效应。

6. 有可能,当投资风险资产报酬非常低,而无风险资产报酬非常高,或者同时出现这两种现象时就会发生这样的情况。

7. 相同,假设两公司2年前股票价格都为P0,则两年后G公司股票价格为1.1*0.9* P0,而S公司股票价格为0.9*1.1 P0,所以两个公司两年后的股价是一样的。

8. 不相同,Lake Minerals 2年后股票价格= 100(1.10)(1.10) = $121.00 而Small Tow n Furniture 2年后股票价格= 100(1.25)(.95) = $118.759. 算数平均收益率仅仅是对所有收益率简单加总平均,它没有考虑到所有收益率组合的效果,而几何平均收益率考虑到了收益率组合的效果,所以后者比较重要。

10. 不管是否考虑通货膨胀因素,其风险溢价没有变化,因为风险溢价是风险资产收益率与无风险资产收益率的差额,若这两者都考虑到通货膨胀的因素,其差额仍然是相互抵消的。

而在考虑税收后收益率就会降低,因为税后收益会降低。

11. R = [(91 –83) + 1.40] / 83 = 11.33%12. 股利收益率= 1.40/83=1.69% 资本利得收益率= (91–83)/83= 9.64%13. R = [(76–83) +1.40] /83=–6.75% 股利收益率= 1.40/83=1.69% 资本利得收益率=(76–83)/83=–8.43%14. (1)总收益= $1,074 –1,120 + 90= $44(2)R = [($1,074 –1,120) + 90] / $1,120=3.93%(3)运用费雪方程式:(1 + R) = (1 + r)(1 + h)r = (1.0393 / 1.030) –1= 0.90%15. (1)名义收益率=12.40%(2)运用费雪方程式:(1 + R) = (1 + r)(1 + h)r =9.02%16. 运用费雪方程式:(1 + R) = (1 + r)(1 + h)r G = 2.62%r C = 3.01%17. X,Y的平均收益率为:X,Y的方差为:将数据带入公式分别可以得到所以X,Y的标准差各为:18. (1)根据表格数据可求得:大公司算数平均收益率=19.41%/6=3.24%国库券算数平均收益率=39.31%/6=6.55%(2)将数据带入公式,可得到大公司股票组合标准差=0.2411,国库券标准差=0.0124(3)平均风险溢价= -19.90%/6= -3.32% 其标准差为0.249219. (1)算术平均收益率= (2.16 +0.21 + 0.04 +0 .16 +0 .19)/5=55.2%(2)将数据带入公式,可得其方差=0.081237,所以标准差=0.901320. (1)运用费雪方程式:(1 + R) = (1 + r)(1 + h)r = (1.5520/ 1.042) –1= 48.94%(2)21. (1)运用费雪方程式:(1 + R) = (1 + r)(1 + h)r = (1.051/ 1.042) –1= 0.86%(2)22. 持有期收益率=[(1 – .0491)(1 +0.2167)(1 +0.2257)(1 +0.0619)(1 +0.3185)] –1 =98.55%23. 20年期零息债券的现值美元所以,收益率R = (163.51–152.37)/152.37=7.31%24. 收益率R = (80.27–84.12 +5.00)/84.12=1.37%25. 三个月的收益率R =(42.02–38.65)/38.65=8.72%,所以,年度平均收益率APR=4(8.72%)=34.88%年度实际年利率EAR=(1+0.0872)4–1=39.71%26. 运用费雪方程式:(1 + R) = (1 + r)(1 + h)则平均实际收益率= (0.0447+0.0554+0.0527+0.0387+0.0926+0.1155+0.1243)/ 7=7.48%27. 根据前面的表格9-2可知,长期公司债券的平均收益率为6.2%,标准差为8.6%,所以,其收益率为68%的可能会落在平均收益率加上或者减去1个标准差的范围内:,同理可得收益率为95%的可能范围为:28. 同理27题大公司股票收益率为68%的可能范围为:,收益率为95%的可能范围为:29.运用Blume公式可得:30. 估计一年的收益率最好运用算数平均收益率,即为12.4%运用Blume公式可得:31 0.55 =0.08–0.13–0.07+0.29+RR=38%32. 算数平均收益率=(0.21+0.14+0.23-0.08+0.09-0.14)/6=7.5%几何平均收益率:=33. 根据题意可以先求出各年的收益率:R1 =(49.07–43.12+0.55)/43.12=15.07%R2 =(51.19–49.07+0.60)/49.07=5.54%R3 =(47.24–51.19+0.63)/51.19=–6.49%R4 =(56.09–47.24+0.72)/47.24=20.26%R5 =(67.21–56.09+0.81)/56.09=21.27%算数平均收益率R A =(0.1507 +0.0554–0.0649+0.2026+0.2127)/5=11.13%几何平均收益率:R G=[(1+0.1507)(1+0.0554)(1–0.0649)(1+0.2026)(1+0.2127)]1/5–1=10. 62%34. (1)根据表9-1数据可以计算出国库券在此期间平均收益率=0.619/8=7.75%,平均通胀率=0.7438/8=9.30%(2)将数据带入公式,可得其方差=0.000971 标准差=0.0312(3)平均实际收益率= -0.1122/8= -1.4%(4)有人认为国库券没有风险,是指政府违约的几率非常小,因此很少有违约风险。

米什金货币金融学英文版习题答案chapter18英文习题

米什金货币金融学英文版习题答案chapter18英文习题Economics of Money, Banking, and Financial Markets, 11e, Global Edition (Mishkin) Chapter 18 The Foreign Exchange Market18.1 Foreign Exchange Market1) The exchange rate isA) the price of one currency relative to gold.B) the value of a currency relative to inflation.C) the change in the value of money over time.D) the price of one currency relative to another.Answer: DAACSB: Reflective Thinking2) Exchange rates are determined inA) the money market.B) the foreign exchange market.C) the stock market.D) the capital market.Answer: BAACSB: Reflective Thinking3) Although foreign exchange market trades are said to involve the buying and selling of currencies, most trades involve the buying and selling ofA) bank deposits denominated in different currencies.B) SDRs.C) gold.D) ECUs.Answer: AAACSB: Reflective Thinking4) The immediate (two-day) exchange of one currency foranother is aA) forward transaction.B) spot transaction.C) money transaction.D) exchange transaction.Answer: BAACSB: Reflective Thinking5) An agreement to exchange dollar bank deposits for euro bank deposits in one month is aA) spot transaction.B) future transaction.C) forward transaction.D) deposit transaction.Answer: CAACSB: Reflective Thinking6) Today 1 euro can be purchased for $1.10. This is theA) spot exchange rate.B) forward exchange rate.C) fixed exchange rate.D) financial exchange rate.Answer: AAACSB: Reflective Thinking7) In an agreement to exchange dollars for euros in three months at a price of $0.90 per euro, the price is theA) spot exchange rate.B) money exchange rate.C) forward exchange rate.D) fixed exchange rate.Answer: CAACSB: Reflective Thinking8) When the value of the British pound changes from $1.25 to $1.50, the pound has ________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: CAACSB: Reflective Thinking9) When the value of the British pound changes from $1.50 to $1.25, then the pound has________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: BAACSB: Reflective Thinking10) When the value of the dollar changes from £0.5 to £0.75, then the British pound has________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: BAACSB: Reflective Thinking11) When the value of the dollar changes from £0.75 to £0.5, then the British pound has________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: CAACSB: Reflective Thinking12) When the exchange rate for the Mexican peso changes from 9 pesos to the U.S. dollar to 10 pesos to the U.S. dollar, then the Mexican peso has ________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: BAACSB: Reflective Thinking13) When the exchange rate for the Mexican peso changes from 10 pesos to the U.S dollar to 9 pesos to the U.S. dollar, then the Mexican peso has ________ and the U.S. dollar has ________.A) appreciated; appreciatedB) depreciated; appreciatedC) appreciated; depreciatedD) depreciated; depreciatedAnswer: CAACSB: Reflective Thinking14) On January 25, 2009, one U.S. dollar traded on the foreign exchange market for about 0.75 euros. Therefore, one euro would have purchased about ________ U.S. dollars.A) 0.75B) 1.00C) 1.33D) 1.75Answer: CAACSB: Analytical Thinking15) On January 25, 2009, one U.S. dollar traded on the foreign exchange market for about 49.0 Indian rupees. Thus, one Indian rupee would have purchased about ________ U.S. dollars.A) 0.02B) 1.20C) 7.00D) 49.0Answer: AAACSB: Analytical Thinking16) On January 25, 2009, one U.S. dollar traded on the foreign exchange market for about 1.15 Swiss francs. Therefore, one Swiss franc would have purchased about ________ U.S. dollars.A) 0.30B) 0.87C) 1.15D) 3.10Answer: BAACSB: Analytical Thinking17) On January 25, 2009, one U.S. dollar traded on the foreign exchange market for about 3.33 Romanian new lei. Therefore, one Romanian new lei would have purchased about ________ U.S. dollars.A) 0.30B) 1.86C) 2.86D) 3.33Answer: AAACSB: Analytical Thinking18) If the U.S. dollar appreciates from 1.25 Swiss franc per U.S. dollar to 1.5 francs per dollar, then the franc depreciates from ________ U.S. dollars per franc to ________ U.S. dollars per franc.A) 0.80; 0.67B) 0.67; 0.80C) 0.50; 0.33D) 0.33; 0.50Answer: AAACSB: Analytical Thinking19) If the British pound appreciates from $0.50 per pound to $0.75 per pound, the U.S. dollar depreciates from ________ per dollar to ________ per dollar.A) £2; £2.5B) £2; £1.33C) £2; £1.5D) £2; £1.25Answer: BAACSB: Analytical Thinking20) If the Japanese yen appreciates from $0.01 per yen to $0.02 per yen, the U.S. dollar depreciates from ________ per dollar to ________ per dollar.A) 100¥; 50¥B) 10¥; 5¥C) 5¥; 10¥D) 50¥; 100¥Answer: AAACSB: Analytical Thinking21) If the dollar appreciates from 1.5 Brazilian reals per dollar to 2.0 reals per dollar, the real depreciates from ________ per real to ________ per real.A) $0.67; $0.50B) $0.33; $0.50C) $0.75; $0.50D) $0.50; $0.67E) $0.50; $0.75Answer: AAACSB: Analytical Thinking22) When the exchange rate for the British pound changes from $1.80 per pound to $1.60 per pound, then, holding everything else constant, the pound has ________ and ________ expensive.A) appreciated; British cars sold in the United States become moreB) appreciated; British cars sold in the United States become lessC) depreciated; American wheat sold in Britain becomes moreD) depreciated; American wheat sold in Britain becomes lessAnswer: CAACSB: Analytical Thinking23) If the dollar depreciates relative to the Swiss francA) Swiss chocolate will become cheaper in the United States.B) American computers will become more expensive in Switzerland.C) Swiss chocolate will become more expensive in the United States.D) Swiss computers will become cheaper in the United States.Answer: CAACSB: Analytical Thinking24) Everything else held constant, when a country's currencyappreciates, the country's goods abroad become ________ expensive and foreign goods in that country become ________ expensive.A) more; lessB) more; moreC) less; lessD) less; moreAnswer: AAACSB: Analytical Thinking25) Everything else held constant, when a country's currency depreciates, its goods abroad become ________ expensive while foreign goods in that country become ________ expensive.A) more; lessB) more; moreC) less; lessD) less; moreAnswer: DAACSB: Analytical Thinking。

公司金融第八版中文课后习题答案

第一章 1.在所有权形式的公司中,股东是公司的所有者。

股东选举公司的董事会,董事会任命该公司的管理层。

企业的所有权和控制权分离的组织形式是导致的代理关系存在的主要原因。

管理者可能追求自身或别人的利益最大化,而不是股东的利益最大化。

在这种环境下,他们可能因为目标不一致而存在代理问题。

2.非营利公司经常追求社会或政治任务等各种目标。

非营利公司财务管理的目标是获取并有效使用资金以最大限度地实现组织的社会使命。

3.这句话是不正确的。

管理者实施财务管理的目标就是最大化现有股票的每股价值,当前的股票价值反映了短期和长期的风险、时间以及未来现金流量。

4.有两种结论。

一种极端,在市场经济中所有的东西都被定价。

因此所有目标都有一个最优水平,包括避免不道德或非法的行为,股票价值最大化。

另一种极端,我们可以认为这是非经济现象,最好的处理方式是通过政治手段。

一个经典的思考问题给出了这种争论的答案:公司估计提高某种产品安全性的成本是30美元万。

然而,该公司认为提高产品的安全性只会节省20美元万。

请问公司应该怎么做呢?” 5.财务管理的目标都是相同的,但实现目标的最好方式可能是不同的,因为不同的国家有不同的社会、政治环境和经济制度。

6.管理层的目标是最大化股东现有股票的每股价值。

如果管理层认为能提高公司利润,使股价超过35美元,那么他们应该展开对恶意收购的斗争。

如果管理层认为该投标人或其它未知的投标人将支付超过每股35美元的价格收购公司,那么他们也应该展开斗争。

然而,如果管理层不能增加企业的价值,并且没有其他更高的投标价格,那么管理层不是在为股东的最大化权益行事。

现在的管理层经常在公司面临这些恶意收购的情况时迷失自己的方向。

7.其他国家的代理问题并不严重,主要取决于其他国家的私人投资者占比重较小。

较少的私人投资者能减少不同的企业目标。

高比重的机构所有权导致高学历的股东和管理层讨论决策风险项目。

此外,机构投资者比私人投资者可以根据自己的资源和经验更好地对管理层实施有效的监督机制。

公司金融第四版参考答案

公司金融第四版参考答案公司金融是一门研究企业财务管理和金融决策的学科,它涉及到公司的资金筹集、投资决策、资本结构和分红政策等方面。

对于学习者来说,参考答案是一个重要的学习工具,可以帮助他们更好地理解和应用所学的知识。

本文将为大家提供公司金融第四版的参考答案,帮助读者更好地掌握这门学科。

第一章:公司金融概述在公司金融的概述部分,主要介绍了公司金融的定义、目标和作用。

参考答案中提到,公司金融是指企业通过资金的筹集和运用,以实现企业目标并最大化股东财富的一门学科。

它对企业的经营决策和财务管理起着重要的指导作用。

第二章:公司金融环境在公司金融环境的部分,参考答案中涉及到了宏观经济环境、市场环境和法律环境对公司金融决策的影响。

它强调了宏观经济环境对企业经营和金融决策的重要性,以及市场环境和法律环境对企业的影响。

第三章:企业投资决策在企业投资决策的部分,参考答案中详细介绍了投资决策的基本原理和方法。

它强调了企业在进行投资决策时需要考虑的因素,如现金流量、风险和回报等,以及投资评价指标的应用。

第四章:资本预算在资本预算的部分,参考答案中提到了资本预算的概念和方法。

它介绍了资本预算的基本步骤,包括项目评估、项目选择和项目实施等,以及资本预算的风险分析和灵敏度分析。

第五章:资本结构与成本在资本结构与成本的部分,参考答案中涉及到了企业的资本结构和成本的决策。

它介绍了资本结构的理论和影响因素,以及资本成本的计算和决策。

第六章:分红政策在分红政策的部分,参考答案中提到了企业的分红政策和决策。

它介绍了不同的分红政策和方法,如现金分红和股票分红,以及分红决策的影响因素。

第七章:公司估值在公司估值的部分,参考答案中详细介绍了公司估值的方法和应用。

它强调了不同的估值方法,如贴现现金流量模型和市场多元回归模型,以及估值的实际应用。

第八章:公司并购与重组在公司并购与重组的部分,参考答案中涉及到了企业的并购与重组决策。

它介绍了并购与重组的类型和目的,以及并购与重组的过程和影响。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

CHAPTER 18VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRMAnswers to Concepts Review and Critical Thinking Questions1.APV is equal to the NPV of the project (i.e. the value of the projectfor an unlevered firm) plus the NPV of financing side effects.2. The WACC is based on a target debt level while the APV is based on theamount of debt.3.FTE uses levered cash flow and other methods use unlevered cash flow.4.The WACC method does not explicitly include the interest cash flows, butit does implicitly include the interest cost in the WACC. If he insists that the interest payments are explicitly shown, you should use the FTE method.5. You can estimate the unlevered beta from a levered beta. The unleveredbeta is the beta of the assets of the firm; as such, it is a measure of the business risk. Note that the unlevered beta will always be lower than the levered beta (assuming the betas are positive). The difference is due to the leverage of the company. Thus, the second risk factor measured by a levered beta is the financial risk of the company.Solutions to Questions and ProblemsNOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple steps. Due to space and readability constraints, when these intermediate steps are included in this solutions manual, rounding may appear to have occurred. However, the final answer for each problem is found without rounding during any step in the problem.Basic1. a.The maximum price that the company should be willing to pay for thefleet of cars with all-equity funding is the price that makes theNPV of the transaction equal to zero. The NPV equation for the projectis:NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(DepreciationTax Shield)If we let P equal the purchase price of the fleet, then the NPV is: NPV = –P + (1 – .35)($140,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5Setting the NPV equal to zero and solving for the purchase price, we find:0 = –P + (1 – .35)($140,000)PVIFA13%,5 + (.35)(P/5)PVIFA13%,5P = $320,068.04 + (P)(0.35/5)PVIFA13%,5P = $320,068.04 + .2462P.7538P = $320,068.04P = $424,609.54b.The adjusted present value (APV) of a project equals the net presentvalue of the project if it were funded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation Tax Shield)The company paid $395,000 for the fleet of cars. Because this fleet will be fully depreciated over five years using the straight-line method, annual depreciation expense equals:Depreciation = $395,000/5Depreciation = $79,000So, the NPV of an all-equity project is:NPV = –$395,000 + (1 – 0.35)($140,000)PVIFA13%,5 +(0.35)($79,000)PVIFA13%,5NPV = $22,319.49NPV(Financing Side Effects)The net present value of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt,so:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(PrincipalPayments)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt R B. So, the NPV of the financing side effects are:NPV = $260,000 – (1 – 0.35)(0.08)($260,000)PVIFA8%,5–[$260,000/(1.08)5]NPV = $29,066.93So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = $22,319.49 + 29,066.93APV = $51,386.422.The adjusted present value (APV) of a project equals the net presentvalue of the project if it were funded completely by equity plus the net present value of any financing side effects. In this case, the NPV of financing side effects equals the after-tax present value of the cash flows resulting from the firm’s debt, so:APV = NPV(All-Equity) + NPV(Financing Side Effects)So, the NPV of each part of the APV equation is:NPV(All-Equity)NPV = –Purchase Price + PV[(1 – t C )(EBTD)] + PV(Depreciation TaxShield)Since the initial investment of $1.9 million will be fully depreciated over four years using the straight-line method, annual depreciationexpense is:Depreciation = $1,900,000/4Depreciation = $475,000NPV = –$1,900,000 + (1 – 0.30)($685,000)PVIFA9.5%,4 +(0.30)($475,000)PVIFA13%,4NPV (All-equity) = – $49,878.84NPV(Financing Side Effects)The net present value of financing side effects equals the aftertaxpresent value of cash flows resulting from the firm’s debt. So, the NPV of the financing side effects are:NPV = Proceeds(Net of flotation) – Aftertax PV(Interest Payments) –PV(Principal Payments)+ PV(Flotation Cost Tax Shield)Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, R B. Since the flotation costs will beamortized over the life of the loan, the annual flotation costs that will be expensed each year are:Annual flotation expense = $28,000/4Annual flotation expense = $7,000NPV = ($1,900,000 – 28,000) – (1 – 0.30)(0.095)($1,900,000)PVIFA9.5%,4– $1,900,000/(1.095)4+ 0.30($7,000) PVIFA9.5%,4NPV = $152,252.06So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$49,878.84 + 152,252.06APV = $102,373.233. a.In order to value a firm’s equity us ing the flow-to-equity approach,discount the cash flows available to equity holders at the cost ofthe firm’s levered equity. The cash flows to equity holders will bethe firm’s net income. Remembering that the company has three stores,we find:Sales $3,600,000COGS 1,530,000G & A costs 1,020,000Interest 102,000EBT $948,000Taxes 379,200NI $568,800Since this cash flow will remain the same forever, the presentvalue of cash flows available to the firm’s equity holders is aperpetuity. We can discount at the levered cost of equity, so, thevalue of the company’s equity is:PV(Flow-to-equity) = $568,800 / 0.19PV(Flow-to-equity) = $2,993,684.21b.The value of a firm is equal to the sum of the market values of its debt and equity, or:V L = B + SWe calculated the value of the company’s equity in part a, so nowwe need to calculate the value of debt. The company has a debt-to-equity ratio of 0.40, which can be written algebraically as:B / S = 0.40We can substitute the value of equity and solve for the value ofdebt, doing so, we find:B / $2,993,684.21 = 0.40B = $1,197,473.68So, the value of the company is:V = $2,993,684.21 + 1,197,473.68V = $4,191,157.894. a.In order to determine the cost of the firm’s debt, we need to findthe yield to maturity on its current bonds. With semiannual couponpayments, the yield to maturity in the company’s bonds is:$975 = $40(PVIFA R%,40) + $1,000(PVIF R%,40)R = .0413 or 4.13%Since the coupon payments are semiannual, the YTM on the bonds is:YTM = 4.13%× 2YTM = 8.26%b.We can use the Capital Asset Pricing Model to find the return onunlevered equity. According to the Capital Asset Pricing Model:R0 = R F+ βUnlevered(R M– R F)R0 = 5% + 1.1(12% – 5%)R0 = 12.70%Now we can find the cost of levered equity. According toModigliani-Miller Proposition II with corporate taxesR S = R0 + (B/S)(R0– R B)(1 – t C)R S = .1270 + (.40)(.1270 – .0826)(1 – .34)R S = .1387 or 13.87%c.In a world with corporate taxes, a firm’s weighted average cost ofcapital is equal to:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SThe problem does not provide either the debt-value ratio or equity-value ratio. However, the firm’s debt-equity ratio of is:B/S = 0.40Solving for B:B = 0.4SSubstituting this in the debt-value ratio, we get:B/V = .4S / (.4S + S)B/V = .4 / 1.4B/V = .29And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .29S/V = .71So, the WACC for the company is:R WACC = .29(1 – .34)(.0826) + .71(.1387) R WACC = .1147 or 11.47%5. a.The equity beta of a firm financed entirely by equity is equal toits unlevered beta. Since each firm has an unlevered beta of 1.25,we can find the equity beta for each. Doing so, we find:North PoleβEquity = [1 + (1 – t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($2,900,000/$3,800,000](1.25)βEquity = 1.87South PoleβEquity = [1 + (1 – t C)(B/S)]βUnleveredβEquity = [1 + (1 – .35)($3,800,000/$2,900,000](1.25)βEquity = 2.31b.We can use the Capital Asset Pricing Model to find the requiredreturn on each firm’s equity. Doing so, we find:North Pole:R S = R F+ βEquity(R M– R F)R S = 5.30% + 1.87(12.40% – 5.30%)R S = 18.58%South Pole:R S = R F+ βEquity(R M– R F)R S = 5.30% + 2.31(12.40% – 5.30%)R S = 21.73%6. a.If flotation costs are not taken into account, the net presentvalue of a loan equals:NPV Loan = Gross Proceeds – Aftertax present value of interest andprincipal paymentsNPV Loan = $5,350,000 – .08($5,350,000)(1 – .40)PVIFA8%,10–$5,350,000/1.0810NPV Loan = $1,148,765.94b.The flotation costs of the loan will be:Flotation costs = $5,350,000(.0125)Flotation costs = $66,875So, the annual flotation expense will be:Annual flotation expense = $66,875 / 10 Annual flotation expense = $6,687.50If flotation costs are taken into account, the net present value ofa loan equals:NPV Loan = Proceeds net of flotation costs – Aftertax present valueof interest and principalpayments + Present value of the flotation cost tax shield NPV Loan = ($5,350,000 – 66,875) – .08($5,350,000)(1– .40)(PVIFA8%,10)– $5,350,000/1.0810 + $6,687.50(.40)(PVIFA8%,10)NPV Loan = $1,099,840.407.First we need to find the aftertax value of the revenues minus expenses.The aftertax value is:Aftertax revenue = $3,800,000(1 – .40)Aftertax revenue = $2,280,000Next, we need to find the depreciation tax shield. The depreciation tax shield each year is:Depreciation tax shield = Depreciation(t C)Depreciation tax shield = ($11,400,000 / 6)(.40)Depreciation tax shield = $760,000Now we can find the NPV of the project, which is:NPV = Initial cost + PV of depreciation tax shield + PV of aftertax revenueTo find the present value of the depreciation tax shield, we should discount at the risk-free rate, and we need to discount the aftertax revenues at the cost of equity, so:NPV = –$11,400,000 + $760,000(PVIFA6%,6) + $2,280,000(PVIFA14%,6)NPV = $1,203,328.438.Whether the company issues stock or issues equity to finance the projectis irrelevant. The company’s optimal capital structure determines the WACC. In a world with corpor ate taxes, a firm’s weighted average cost of capital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .80(1 – .34)(.072) + .20(.1140)R WACC = .0608 or 6.08%Now we can use the weighted average cost of capital to discount NEC’s unlevered cash flows. Doing so, we find the NPV of the project is:NPV = –$40,000,000 + $2,600,000 / 0.0608NPV = $2,751,907.399. a.The company has a capital structure with three parts: long-term debt,short-term debt, and equity. Since interest payments on both long-term and short-term debt are tax-deductible, multiply the pretaxcosts by (1 – t C) to determine the aftertax costs to be used in theweighted average cost of capital calculation. The WACC using the bookvalue weights is:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = ($3 / $19)(.035)(1 – .35) + ($10 / $19)(.068)(1 – .35) +($6 / $19)(.145)R WACC = 0.0726 or 7.26%ing the market value weights, the company’s WACC is:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = ($3 / $40)(.035)(1 – .35) + ($11 / $40)(.068)(1 – .35) +($26 / $40)(.145)R WACC = 0.1081 or 10.81%ing the target debt-equity ratio, the target debt-value ratio forthe company is:B/S = 0.60B = 0.6SSubstituting this in the debt-value ratio, we get:B/V = .6S / (.6S + S)B/V = .6 / 1.6B/V = .375And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .375S/V = .625We can use the ratio of short-term debt to long-term debt in a similar manner to find the short-term debt to total debt and long-term debt to total debt. Using the short-term debt to long-term debt ratio, we get:STD/LTD = 0.20STD = 0.2LTDSubstituting this in the short-term debt to total debt ratio, weget:STD/B = .2LTD / (.2LTD + LTD)STD/B = .2 / 1.2STD/B = .167And the long-term debt to total debt ratio is one minus the short-term debt to total debt ratio, or:LTD/B = 1 – .167LTD/B = .833Now we can find the short-term debt to value ratio and long-term debt to value ratio by multiplying the respective ratio by the debt-value ratio. So:STD/V = (STD/B)(B/V)STD/V = .167(.375)STD/V = .063And the long-term debt to value ratio is:LTD/V = (LTD/B)(B/V)LTD/V = .833(.375)LTD/V = .313So, using the target capital structure weights, the company’s WACCis:R WACC = (w STD)(R STD)(1 – t C) + (w LTD)(R LTD)(1 – t C) + (w Equity)(R Equity)R WACC = (.06)(.035)(1 – .35) + (.31)(.068)(1 – .35) + (.625)(.145)R WACC = 0.1059 or 10.59%d.The differences in the WACCs are due to the different weightingschemes. The company’s WACC will most closely resemble the WACCcalculated using target weights since future projects will befinanced at the target ratio. Therefore, the WACC computed withtarget weights should be used for project evaluation.Intermediate10. The adjusted present value of a project equals the net present value ofthe project under all-equity financing plus the net present value of any financing side effects. In the joint v enture’s case, the NPV of financing side effects equals the aftertax present value of cash flows resulting from the firms’ debt. So, the APV is:APV = NPV(All-Equity) + NPV(Financing Side Effects)The NPV for an all-equity firm is:NPV(All-Equity)NPV = –Initial Investment + PV[(1 – t C)(EBITD)] + PV(Depreciation Tax Shield)Since the initial investment will be fully depreciated over five years using the straight-line method, annual depreciation expense is:Annual depreciation = $30,000,000/5Annual depreciation = $6,000,000NPV = –$30,000,000 + (1 – 0.35)($3,800,000)PVIFA5.13%,20 +(0.35)($6,000,000)PVIFA5,13%,20NPV = –$5,262,677.95NPV(Financing Side Effects)The NPV of financing side effects equals the after-tax present value of cash flows resulting from the firm’s debt. The coupon rate on the debt is relevant to determine the interest payments, but the resulting cash flows should still be discounted at the pretax cost of debt. So, the NPV of the financing effects is:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Repayments)NPV = $18,000,000 – (1 – 0.35)(0.05)($18,000,000)PVIFA8.5%,15–$18,000,000/1.08515NPV = $7,847,503.56So, the APV of the project is:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,262,677.95 + $7,847,503.56APV = $2,584,825.6111.I f the company had to issue debt under the terms it would normally receive,the interest rate on the debt would increase to the company’s normal cost of debt. The NPV of an all-equity project would remain unchanged, but the NPV of the financing side effects would change. The NPV of the financing side effects would be:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(PrincipalRepayments)NPV = $18,000,000 – (1 – 0.35)(0.085)($18,000,000)PVIFA8.5%,15–$18,000,000/((1.085)15NPV = $4,446,918.69Using the NPV of an all-equity project from the previous problem, the new APV of the project would be:APV = NPV(All-Equity) + NPV(Financing Side Effects)APV = –$5,262,677.95 + $4,446,918.69APV = –$815,759.27The gain to the company from issuing subsidized debt is the difference between the two APVs, so:Gain from subsidized debt = $2,584,825.61 – (–815,759.27)Gain from subsidized debt = $3,400,584.88Most of the value of the project is in the form of the subsidized interest rate on the debt issue.12. The adjusted present value of a project equals the net present value ofthe project under all-equity financing plus the net present value of any financing side effects. First, we need to calculate the unlevered cost of equity. According to Modigliani-Miller Proposition II with corporate taxes:R S = R0 + (B/S)(R0– R B)(1 – t C).16 = R0 + (0.50)(R0– 0.09)(1 – 0.40)R0 = 0.1438 or 14.38%Now we can find the NPV of an all-equity project, which is:NPV = PV(Unlevered Cash Flows)NPV = –$21,000,000 + $6,900,000/1.1438 + $11,000,000/(1.1438)2 +$9,500,000/(1.1438)3NPV = –$212,638.89Next, we need to find the net present value of financing side effects. This is equal the aftertax present value of cash flows resulting from the firm’s debt. So:NPV = Proceeds – Aftertax PV(Interest Payments) – PV(Principal Payments)Each year, an equal principal payment will be made, which will reduce the interest accrued during the year. Given a known level of debt, debt cash flows should be discounted at the pre-tax cost of debt, so the NPV of the financing effects are:NPV = $7,000,000 – (1 – .40)(.09)($7,000,000) / (1.09) –$2,333,333.33/(1.09)– (1 – .40)(.09)($4,666,666.67)/(1.09)2–$2,333,333.33/(1.09)2– (1 – .40)(.09)($2,333,333.33)/(1.09)3–$2,333,333.33/(1.09)3NPV = $437,458.31So, the APV of project is:APV = NPV(All-equity) + NPV(Financing side effects)APV = –$212,638.89 + 437,458.31APV = $224,819.4213.a.To calculate the NPV of the project, we first need to find thecompany’s WACC. In a world with corporate taxes, a firm’s weightedaverage cost of capital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SThe market value of the company’s equity is:Market value of equity = 6,000,000($20)Market value of equity = $120,000,000So, the debt-value ratio and equity-value ratio are:Debt-value = $35,000,000 / ($35,000,000 + 120,000,000)Debt-value = .2258Equity-value = $120,000,000 / ($35,000,000 + 120,000,000)Equity-value = .7742Since the CEO believes its current capital structure is optimal,these values can be used as the target weights in the firm’s weightedaverage cost of capital calculation. The yield to maturity of thecompany’s debt is its pretax cost of debt. To find the company’scost of equity, we need to calculate the stock beta. The stock betacan be calculated as:β = σS,M / σ2Mβ = .036 / .202β = 0.90Now we can use the Capital Asset Pricing Model to determine the cost of equity. The Capital Asset Pricing Model is:R S = R F+ β(R M– R F)R S = 6% + 0.90(7.50%)R S = 12.75%Now, we can calculate the company’s WACC, which is:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .2258(1 – .35)(.08) + .7742(.1275)R WACC = .1105 or 11.05%Finally, we can use the WACC to discount the unlevered cash flows,which gives us an NPV of:NPV = –$45,000,000 + $13,500,000(PVIFA11.05%,5)NPV = $4,837,978.59b.The weighted average cost of capital used in part a will not changeif the firm chooses to fund the project entirely with debt. Theweighted average cost of capital is based on optimal capitalstructure weights. Since the current capital structure is optimal,all-debt funding for the project simply implies that the firm willhave to use more equity in the future to bring the capital structureback towards the target.Challenge14.a.The company is currently an all-equity firm, so the value as an all-equity firm equals the present value of aftertax cash flows,discounted at the cost of the firm’s unlevered cost of equity. So,the current value of the company is:V U = [(Pretax earnings)(1 – t C)] / R0V U = [($28,000,000)(1 – .35)] / .20V U = $91,000,000The price per share is the total value of the company divided by theshares outstanding, or:Price per share = $91,000,000 / 1,500,000Price per share = $60.67b.The adjusted present value of a firm equals its value under all-equity financing plus the net present value of any financing sideeffects. In this case, the NPV of financing side effects equals theaftertax present value of cash flows resulting from the firm’s debt.Given a known level of debt, debt cash flows can be discounted atthe pretax cost of debt, so the NPV of the financing effects are:NPV = Proceeds – Aftertax PV(Interest Payments)NPV = $35,000,000 – (1 – .35)(.09)($35,000,000) / .09NPV = $12,250,000So, the value of the company after the recapitalization using the APV approach is:V = $91,000,000 + 12,250,000V = $103,250,000Since the company has not yet issued the debt, this is also the value of equity after the announcement. So, the new price per share will be:New share price = $103,250,000 / 1,500,000New share price = $68.83c.The company will use the entire proceeds to repurchase equity. Usingthe share price we calculated in part b, the number of shares repurchased will be:Shares repurchased = $35,000,000 / $68.83Shares repurchased = 508,475And the new number of shares outstanding will be:New shares outstanding = 1,500,000 – 508,475New shares outstanding = 991,525The value of the company increased, but part of that increase will be funded by the new debt. The value of equity afterrecapitalization is the total value of the company minus the value of debt, or:New value of equity = $103,250,000 – 35,000,000New value of equity = $68,250,000So, the price per share of the company after recapitalization will be:New share price = $68,250,000 / 991,525New share price = $68.83The price per share is unchanged.d.In order to value a firm’s equity using the flow-to-equity approach,we must discount the cash flows available to equity holders at the cost of the firm’s levered equity. According to Modigliani-Miller Proposition II with corporate taxes, the required return of levered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .20 + ($35,000,000 / $68,250,000)(.20 – .09)(1 – .35)R S = .2367 or 23.67%After the recapitalization, the net income of the company will be:EBIT $28,000,000Interest 3,150,000EBT $24,850,000Taxes 8,697,500Net income $16,152,500The firm pays all of its earnings as dividends, so the entire netincome is available to shareholders. Using the flow-to-equityapproach, the value of the equity is:S = Cash flows available to equity holders / R SS = $16,152,500 / .2367S = $68,250,00015.a.If the company were financed entirely by equity, the value of thefirm would be equal to the present value of its unlevered after-taxearnings, discounted at its unlevered cost of capital. First, we needto find the company’s unlevered cash flows, which are:Sales $28,900,000Variablecosts 17,340,000EBT $11,560,000Tax 4,624,000Net incomeSo, the value of the unlevered company is:V U = $6,936,000 / .17V U = $40,800,000b.According to Modigliani-Miller Proposition II with corporate taxes,the value of levered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .17 + (.35)(.17 – .09)(1 – .40)R S = .1868 or 18.68%c.In a world with corporate taxes, a firm’s weighted average cost ofcapital equals:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SSo we need the debt-value and equity-value ratios for the company.The debt-equity ratio for the company is:B/S = 0.35B = 0.35SSubstituting this in the debt-value ratio, we get:B/V = .35S / (.35S + S) B/V = .35 / 1.35B/V = .26And the equity-value ratio is one minus the debt-value ratio, or:S/V = 1 – .26S/V = .74So, using the capital structure weights, the company’s WACC is:R WACC = [B / (B + S)](1 – t C)R B + [S / (B + S)]R SR WACC = .26(1 – .40)(.09) + .74(.1868)R WACC = .1524 or 15.24%We can use the weighted average cost of capital to discount the firm’s unlevered aftertax earnings to value the company. Doing so, we find:V L = $6,936,000 / .1524V L = $45,520,661.16Now we can use the debt-value ratio and equity-value ratio to find the value of debt and equity, which are:B = V L(Debt-value)B = $45,520,661.16(.26)B = $11,801,652.89S = V L(Equity-value)S = $45,520,661.16(.74)S = $33,719,008.26d.In order to v alue a firm’s equity using the flow-to-equity approach,we can discount the cash flows available to equity holders at the cost of the firm’s levered equity. First, we need to calculate the levered cash flows available to shareholders, which are:Sales $28,900,000Variablecosts 17,340,000EBIT $11,560,000Interest 1,062,149EBT $10,497,851Tax 4,199,140Net incomeSo, the value of equity with the flow-to-equity method is:S = Cash flows available to equity holders / R S S = $6,298,711 / .1868S = $33,719,008.2616.a.Since the company is currently an all-equity firm, its value equalsthe present value of its unlevered after-tax earnings, discounted atits unlevered cost of capital. The cash flows to shareholders forthe unlevered firm are:EBIT $83,000Tax 33,200Net income $49,800So, the value of the company is:V U = $49,800 / .15V U = $332,000b.The adjusted present value of a firm equals its value under all-equityfinancing plus the net present value of any financing side effects.In this case, the NPV of financing side effects equals the after-taxpresent value of cash flows resulting from debt. Given a known levelof debt, debt cash flows should be discounted at the pre-tax cost ofdebt, so:NPV = Proceeds – Aftertax PV(Interest payments)NPV = $195,000 – (1 – .40)(.09)($195,000) / 0.09NPV = $78,000So, using the APV method, the value of the company is:APV = V U + NPV(Financing side effects)APV = $332,000 + 78,000APV = $410,000The value of the debt is given, so the value of equity is the valueof the company minus the value of the debt, or:S = V – BS = $410,000 – 195,000S = $215,000c.According to Modigliani-Miller Proposition II with corporate taxes,the required return of levered equity is:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .15 + ($195,000 / $215,000)(.15 – .09)(1 – .40)R S = .1827 or 18.27%d.In order to value a firm’s equity using the flow-to-equity approach,we can discount the cash flows available to equity holders at thecost of the firm’s levered equity. First, we need to calculate thelevered cash flows available to shareholders, which are:EBIT $83,000Interest 17,550EBT $65,450Tax 26,180Net incomeSo, the value of equity with the flow-to-equity method is:S = Cash flows available to equity holders / R SS = $39,270 / .1827S = $215,00017. Since the company is not publicly traded, we need to use the industrynumbers to calculate the industry levered return on equity. We can then find the industry unlevered return on equity, and re-lever the industry return on equity to account for the different use of leverage. So, using the CAPM to calculate the industry levered return on equity, we find:R S = R F+ β(MRP)R S = 5% + 1.2(7%)R S = 13.40%Next, to find the average cost of unlevered equity in the holiday gift industry we can use Modigliani-Miller Proposition II with corporate taxes, so:R S = R0 + (B/S)(R0– R B)(1 – t C).1340 = R0 + (.35)(R0– .05)(1 – .40)R0 = .1194 or 11.94%Now, we can use the Modigliani-Miller Proposition II with corporate taxes to re-lever the return on equity to account for this company’s debt-equity ratio. Doing so, we find:R S = R0 + (B/S)(R0– R B)(1 – t C)R S = .1194 + (.40)(.1194 – .05)(1 – .40)R S = .1361 or 13.61%。