From risk society to audit society

保险公司风险管理指引【释义提纲】

第四章风险控制第二十二条风险控制包括明确风险管理总体策略、制定风险解决方案和方案的组织实施等内容。

【释义】本条是关于风险控制内容的规定。

1、风险控制体系总论2、风险控制的重要意义3、风险控制的内容和流程1.风险控制体系风险控制体系可分为两个部分:-风险控制政策-风险控制程序所以风险控制活动是使保险公司高层管理当局的指示得以贯彻执行的政策和程序2.风险控制的重要意义3.风险控制的内容和流程风险处理内部控制方案应包括以下内容:1.明确控制风险的相关职责与权限2.控制的策略,方法,资源需求和时限要求3.重大,突发事项应急预案,明确责任人,处理流程和措施风险控制活动并非孤立存在.而是根据其对应的风险和作用,体现在保险公司不同的流程中.第二十三条制定风险管理总体策略是指保险公司根据自身发展战略和条件,明确风险管理重点,确定风险限额,选择风险管理工具以及配置风险管理资源等的总体安排。

【释义】本条是关于风险管理总体策略的规定。

1、风险管理总体策略包含的内容2、制定风险管理总体策略的方法和步骤3、制定风险管理总体策略的重要意义及目的1.风险管理总体策略包含的内容寿险公司的风险管理总体策略应包括以下内容:a.保险公司发展战略和条件b.明确风险管理重点因为每家保险公司的资源都是有c.d.e.f.保险公司所拟定的风险管理总体策略,D e f i n e a n d d o c u m e n t了该公司对风险管理的A P P R O A C H.有了明确的风险管理总体策略,保险公司才1.制定风险管理总体策略的方法和步骤2.制定风险管理总体策略的重要意义及目的第二十四条保险公司应当根据风险发生的可能性和对经营目标的影响程度,对各项风险进行分析比较,确定风险管理的重点。

【释义】本条是关于确定风险管理重点的规定。

1.风险衡量的两个纬度(发生可能性×影响程度)2.对风险进行比较的方法3.风险重点的确定1.风险衡量的两个纬度(发生可能性×影响程度)要将不定量的风险做比较,以便能够让保险公司能根据风险的重要性来做出相应的对策和解决方案,保险公司必须先用风险发生可能性和风险发生后对公司的影响程度做评估.发生可能性在评估风险发生可能性,保险公可以参考历史数据来做参考,保险公可以根据该风险的发生频率来定下以下的评估发生可能性表:影响程度风险发生后对公司的影响程度可分为以下范围:1)对公司财务的直接影响2)对公司名誉的影响3)对公司人员的影响4)对公司正常运做的影响其他的影响范围包括:1)Risk analysis may concentrate on impacts in one area only or on severalpossible areas of impact.Areas of impact include the following:a) Asset and resource baseOf the organization, including personnel.b) Revenue and entitlementsc) CostsOf activities, both direct and indirect.d) Peoplee) Communityf) Performanceg) Timing and schedule of activitiesh) The environmenti) IntangiblesSuch as reputation, goodwill, quality of life.j) Organizational behaviour2.对风险进行比较的方法保险公司在评估了发生可能性和对公司影响程度后,可以用以下的方式来决定每个风险的相对重要性:3.风险重点的确定第二十五条确定风险限额是指保险公司根据自身财务状况、经营需要和各类保险业务的特点,在平衡风险与收益的基础上,确定愿意承担哪些风险及所能承受的最高风险水平,并据此确定风险的预警线。

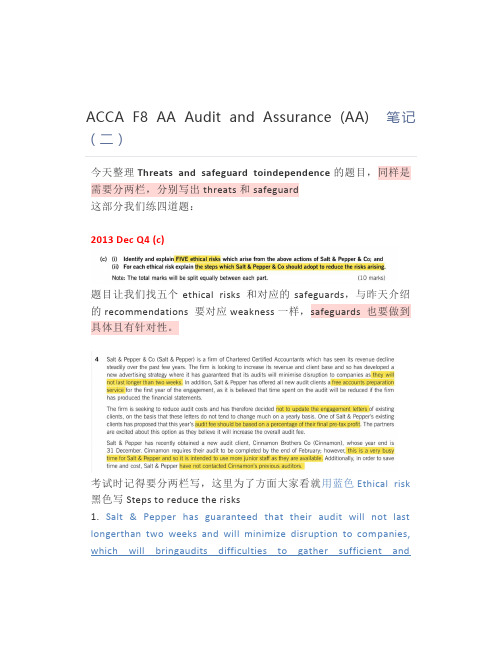

ACCA F8 AA Audit and Assurance (AA) 笔记(二)

ACCA F8 AA Audit and Assurance (AA) 笔记(二)今天整理Threats and safeguard toindependence的题目,同样是需要分两栏,分别写出threats和safeguard这部分我们练四道题:2013 Dec Q4 (c)题目让我们找五个ethical risks 和对应的safeguards,与昨天介绍的recommendations 要对应weakness一样,safeguards 也要做到具体且有针对性。

考试时记得要分两栏写,这里为了方面大家看就用蓝色Ethical risk 黑色写 Steps to reduce the risks1. Salt & Pepper has guaranteed that their audit will not last longerthan two weeks and will minimize disruption to companies, which will bringaudits difficulties to gather sufficient andrisk类型写上)Salt & Pepper should cease thisadvertising campaign immediately as it is not in compliance with ACCA’s Code ofEthics and Conduct. The firm should inform the clients that the audit durationwill be based on the level of audit risk present2. Salt & Pepper has offered all new audit clients a free accountspreparation service for the first year of the engagement, which willincrease the risk of self-reviewSalt & Pepper must ensure that thiswork is undertaken by a team separate to the audit team.3. The firm is not updating engagement letters for existing clients, sothe engagement letters will not be reviewed to ensure that they are stillrelevant and up to date.Salt & Pepper should comply fully withISA 210 and annually review the need for revising the engagement letters.4. An existing client of Salt & Pepper has proposed an audit feebased on a percentage of the client’s final pre-tax profit. This is acontingent fee arrangement and is prohibited as it creates a self-interestthreat.Salt & Pepper should politely declinethe proposed contingent fee arrangement and inform the client that the feeswill be based on the level of work required to obtain sufficient andappropriate audit evidence.5. Salt & Pepper intends to use junior staff for the audit of their newclient as the timing of the audit is when the firm is very busy. Junior staffmay not be competent enough and the risk of giving an incorrect audit opinionis increased.Salt & Pepper should try to increasethe amount of experienced team members. If this is not possible, they shoulddiscuss with thedirectors of Cinnamon to see whether the timing of the auditcould be changed.6. Salt & Pepper has n ot contacted Cinnamon’s previous auditors. Inthis way Salt & Pepper cannot know the reasons why Cinnamon changed their auditors.They may have been acting unethically and their previous auditors thereforerefused to continue.Salt & Pepper should contact theprevious auditors to identify if there are any ethical issues which wouldprevent them from acting as auditors of Cinnamon.2014 Specimen Q1 (a)没有说明找几点的,一般是一分一点。

如何解决人工智能带来的问题英语作文

如何解决人工智能带来的问题英语作文The rapid development of artificial intelligence (AI) technology has brought about numerous benefits to our society, such as improving efficiency, reducing costs, and enhancing the quality of life. However, along with these benefits, AI has also raised certain concerns and challenges that need to be addressed to ensure a safe and sustainable future for humanity. In this essay, I will discuss some of the problems that AI can potentially bring and propose some solutions to mitigate these issues.One of the most concerning issues surrounding AI is job displacement. As AI technology becomes more advanced, there is a growing fear that many jobs currently performed by humans will be replaced by machines, leading to unemployment and economic instability. To address this issue, it is essential for governments and industries to invest in retraining programs for workers who are at risk of losing their jobs to automation. By providing opportunities for workers to acquire new skills and transition to new roles in the workforce, we can help mitigate the negative impact of AI on employment.Another significant challenge posed by AI is the ethical implications of using autonomous systems that have the powerto make decisions without human intervention. As AI technology becomes more sophisticated, there is a need to establish clear guidelines and regulations to ensure that AI systems are used in a responsible and ethical manner. It is essential for policymakers to work with experts in the field to develop a framework for AI ethics that prioritizes transparency, accountability, and human oversight in the design and deployment of AI systems.Furthermore, there are concerns about the potential for AI to perpetuate bias and discrimination, particularly in algorithms used for decision-making in areas such as hiring, lending, and criminal justice. To address this issue, it is crucial for developers to prioritize fairness and inclusivity in the design of AI systems and to regularly audit and test algorithms for bias. Additionally, policymakers should consider implementing regulations that require transparency and accountability in the use of AI to prevent discrimination and uphold human rights.In addition to these challenges, there are also concerns about the potential for AI to be used for malicious purposes, such as cyberattacks, surveillance, and misinformation. To address these security risks, it is vital for governments and industries to invest in cybersecurity measures to protect AI systems from external threats and develop protocols fordetecting and preventing the misuse of AI technology. Collaboration between stakeholders, including policymakers, researchers, and industry leaders, is essential to establish best practices for securing AI systems and preventing malicious actors from exploiting their capabilities.Overall, while AI technology has the potential to bring significant benefits to our society, it is essential to address the challenges and risks associated with its development and deployment. By investing in education and retraining programs, establishing ethical guidelines for AI usage, addressing bias and discrimination in algorithms, and enhancing cybersecurity measures, we can ensure that AI technology is used responsibly and ethically to promote the well-being and prosperity of humanity. With a collaborative and proactive approach, we can harness the power of AI to create a more equitable and sustainable future for all.。

审计的重要性英文作文

审计的重要性英文作文1. Auditing is crucial in ensuring the accuracy of financial information. It helps to detect errors, fraud, and other irregularities that could affect the financial health of an organization. Without auditing, there would be no way to verify the validity of financial reports, which could lead to serious consequences for both the organization and its stakeholders.2. Auditing also plays a critical role in maintaining compliance with laws and regulations. Many industries are subject to strict regulatory requirements, and failure to comply with these regulations can result in hefty fines, legal action, and damage to the organization's reputation. Auditing helps to ensure that the organization is following all applicable laws and regulations, reducing the risk of noncompliance.3. In addition to providing assurance to stakeholders and ensuring compliance, auditing can also helporganizations improve their operations. By identifying areas of weakness or inefficiency, auditors can make recommendations for improvement that can lead to cost savings, increased productivity, and better overall performance.4. Another important aspect of auditing is risk management. Auditors can help organizations identify and assess potential risks, such as cybersecurity threats, supply chain disruptions, or natural disasters. By understanding these risks, organizations can develop strategies to mitigate them and minimize their impact.5. Finally, auditing helps to promote transparency and accountability. By conducting regular audits and making the results available to stakeholders, organizations demonstrate their commitment to responsible financial management and ethical business practices. This can help to build trust and confidence among stakeholders, which is essential for long-term success.。

审计五要素 英语作文

审计五要素英语作文Audit Five Elements。

Audit is an important process for companies to ensure that their financial statements are accurate and reliable. There are five key elements of an audit that must be considered in order to ensure that the audit is effective and efficient. These five elements are: risk assessment, internal control, substantive testing, audit evidence, and reporting.Risk Assessment。

Risk assessment is the first step in the audit process. The auditor must identify and assess the risks that may affect the accuracy and reliability of the financial statements. This includes identifying the risks of material misstatement, such as fraud or error, and determining the likelihood and potential impact of these risks.Internal Control。

Internal control is the second element of the audit process. The auditor must evaluate the company's internal control system to determine whether it is effective in preventing and detecting material misstatements. This includes assessing the design and implementation ofinternal controls, as well as testing their effectiveness.Substantive Testing。

企业ESG_表现对审计意见的影响研究

Operations Research and Fuzziology 运筹与模糊学, 2023, 13(4), 4014-4024 Published Online August 2023 in Hans. https:///journal/orf https:///10.12677/orf.2023.134402企业ESG 表现对审计意见的影响研究徐紫琼上海工程技术大学管理学院,上海收稿日期:2023年7月5日;录用日期:2023年8月13日;发布日期:2023年8月21日摘要近些年,随着建设美丽中国的进程大力推进,可持续发展和高质量发展观念逐渐在社会各个领域流行。

企业ESG 表现的相关研究也势如破竹,然而,大部分的研究都集中在ESG 表现对企业本身的影响上,很少有研究探讨ESG 表现对公司外部审计的影响。

在这一背景下,本文以沪深两市2011~2020年间的有关数据为基础,对我国上市公司ESG 表现与审计意见之间的关系进行了实证分析。

研究发现,在其它条件相同的情况下,具有良好ESG 表现的企业能够增加审计师提出标准审计报告的可能性。

实证分析了企业ESG 表现与审计意见之间的相关性。

研究结果表明:在其他条件相同时,ESG 表现较好的企业可以提高审计师出具标准审计意见的概率。

机制检验发现,经营风险在企业ESG 表现影响审计意见过程中发挥中介作用。

异质性研究发现,ESG 表现对审计意见的正面效应在分析师关注较高和机构投资者持股比例较高的公司中尤其显著。

ESG 表现对审计意见的正向影响在分析师关注度较高、以及机构投资者持股比例较高的公司中尤为明显。

在通过一系列的稳健性检验后,上述结论依然成立。

本文得出的结论有助于扩展审计意见影响因素以及企业ESG 表现经济后果的相关研究,为企业重视ESG 表现提供参考和依据。

关键词ESG 表现,审计意见,经营风险Research on the Impact of Enterprise ESG Performance on Audit OpinionZiqiong XuSchool of Management, Shanghai University of Engineering Science, ShanghaiReceived: Jul. 5th , 2023; accepted: Aug. 13th , 2023; published: Aug. 21st , 2023AbstractIn recent years, with the vigorous promotion of the process of building a beautiful China, the con-徐紫琼cept of sustainable development and high-quality development has gradually become popular in all fields of society. The relevant research on ESG performance of enterprises is also overwhelm-ing, but most of the research focuses on the impact of ESG performance on enterprises themselves, and few studies focus on the impact of ESG performance on external audit. In light of the above, this paper empirically analyses the correlation between ESG performance and audit opinion based on relevant data for A-share listed companies in Shanghai and Shenzhen from 2011 to 2020. The results show that companies with higher ESG performance are more likely to have auditors issue a standard audit opinion. In testing the mechanism, we found that operational risk plays a mediat-ing role in a company’s ESG performance affecting the audit opinion. Operational risk plays a me-diating role in the process of corporate ESG performance affecting audit opinion. The heterogene-ity study finds that the positive impact of ESG performance on audit opinion is particularly ob-vious in companies with higher analyst attention and higher shareholding ratio of institutional investors. After a series of robustness tests, the above conclusions remain valid. The results of this study help to expand relevant research on factors influencing auditor judgment and the financial impact of a company’s ESG performance, and provide a helpful framework for companies that con-sider ESG performance to be important.KeywordsESG Performance, Audit Opinions, Risk of OperationThis work is licensed under the Creative Commons Attribution International License (CC BY 4.0)./licenses/by/4.0/1. 引言改革开放以来、我国综合实力不断增强,经济发展的进程势不可挡。

CCAA《审计学》测试题及解答英文版

CCAA《审计学》测试题及解答英文版CCAA "Auditing" Test Questions and Answers1. What is the purpose of an audit?The purpose of an audit is to provide an independent assessment of an organization's financial statements to ensure they are free from material misstatement.2. What are the main types of audit evidence?The main types of audit evidence include physical examination, confirmation, documentation, observation, analytical procedures, and inquiries.3. What are the key components of the audit process?The key components of the audit process include planning, risk assessment, testing of controls, substantive procedures, and reporting.4. Explain the concept of materiality in auditing.Materiality in auditing refers to the significance of an item or an error in the financial statements that could influence the decisions of users. Auditors consider materiality when planning and performing an audit.5. What is the role of internal controls in an audit?Internal controls are processes implemented by management to provide reasonable assurance regarding the reliability of financial reporting and the effectiveness and efficiency of operations. Auditors assess the effectiveness of internal controls to determine the nature, timing, and extent of audit procedures.6. Describe the difference between a compliance audit and a financial statement audit.A compliance audit focuses on verifying whether an organization is following specific laws, regulations, or policies, while a financial statement audit examines the accuracy and completeness of an organization's financial statements.7. How do auditors assess audit risk?Auditors assess audit risk by considering inherent risk, control risk, and detection risk. The combination of these risks determines the overall risk of material misstatement in the financial statements.8. Explain the concept of independence in auditing.Independence in auditing refers to the auditor's ability to perform an audit without being influenced by relationships or conflicts of interest. It is essential for auditors to maintain independence to ensure the integrity and credibility of the audit process.9. What are the different types of audit reports?The different types of audit reports include unmodified (clean), qualified, adverse, and disclaimer of opinion. The type of report issued by auditors depends on their findings during the audit.10. How do auditors communicate audit findings to stakeholders?Auditors communicate audit findings through the audit report, which includes the auditor's opinion on the financial statements, key audit matters, and any significant issues identified during the audit.Stakeholders use this information to make informed decisions about the organization.These are some of the key concepts and topics related to auditing that are often covered in the CCAA "Auditing" test. Understanding these concepts can help prepare you for the exam and enhance your knowledge of auditing principles and practices.。

阿伦斯 审计学:一种整合方法 课后习题答案

Chapter 1The Demand for Audit and Other Assurance Services Review Questions1-1The relationship among audit services, attestation services, and assurance services is reflected in Figure 1-3 on page 13 of the text. An assurance service is an independent professional service to improve the quality of information for decision makers. An attestation service is a form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. Audit services are a form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria.The most common form of audit service is an audit of historical financial statements, in which the auditor expresses a conclusion as to whether the financial statements are presented in conformity with generally accepted accounting principles. An example of an attestation service is a report on the effe ctiveness of an entity’s internal control over financial reporting. There are many possible forms of assurance services, including services related to business performance measurement, health care performance, and information system reliability.1-2 An independent audit is a means of satisfying the need for reliable information on the part of decision makers. Factors of a complex society which contribute to this need are:1.Remoteness of informationa.Owners (stockholders) divorced from managementb.Directors not involved in day-to-day operations ordecisionsc.Dispersion of the business among numerous geographiclocations and complex corporate structures2.Biases and motives of providerrmation will be biased in favor of the providerwhen his or her goals are inconsistent with thedecision maker's goals.3.Voluminous dataa.Possibly millions of transactions processed daily viasophisticated computerized systemsb.Multiple product linesc.Multiple transaction locationsplex exchange transactionsa.New and changing business relationships lead toinnovative accounting and reporting problemsb.Potential impact of transactions not quantifiable,leading to increased disclosures1-3 1. Risk-free interest rate This is approximately the rate the bank could earn by investing in U.S. treasury notes for thesame length of time as the business loan.2.Business risk for the customer This risk reflects thepossibility that the business will not be able to repay itsloan because of economic or business conditions such as arecession, poor management decisions, or unexpectedcompetition in the industry.rmation risk This risk reflects the possibility thatthe information upon which the business risk decision wasmade was inaccurate. A likely cause of the information riskis the possibility of inaccurate financial statements.Auditing has no effect on either the risk-free interest rate or business risk. However, auditing can significantly reduce information risk.1-4The four primary causes of information risk are remoteness of information, biases and motives of the provider, voluminous data, and the existence of complex exchange transactions.The three main ways to reduce information risk are:er verifies the information.er shares the information risk with management.3.Audited financial statements are provided.The advantages and disadvantages of each are as follows:1-5 To do an audit, there must be information in a verifiable form and some standards (criteria) by which the auditor can evaluate the information. Examples of established criteria include generally accepted accounting principles and the Internal Revenue Code. Determining the degree of correspondence between information and established criteria is determining whether a given set of information is in accordance with the established criteria. The information for Jones Company's tax return is the federal tax returns filed by the company. The established criteria are found in the Internal Revenue Code and all interpretations. For the audit of Jones Company's financial statements the information is the financial statements being audited and the established criteria are generally accepted accounting principles.1-6The primary evidence the internal revenue agent will use in the audit of the Jones Company's tax return include all available documentation and other information available in Jones' office or from other sources. For example, when the internal revenue agent audits taxable income, a major source of information will be bank statements, the cash receipts journal and deposit slips. The internal revenue agent is likely to emphasize unrecorded receipts and revenues. For expenses, major sources of evidence are likely to be cancelled checks, vendors' invoices and other supporting documentation.1-7This apparent paradox arises from the distinction between the function of auditing and the function of accounting. The accounting function is the recording, classifying and summarizing of economic events to provide relevant information to decision makers. The rules of accounting are the criteria used by the auditor for evaluating the presentation of economic events for financial statements and he or she must therefore have an understanding of generally accepted accounting principles (GAAP), as well as auditing standards. The accountant need not, and frequently does not, understand what auditors do, unless he or she is involved in doing audits, or has been trained as an auditor.1-81-9Five examples of specific operational audits that could be conducted by an internal auditor in a manufacturing company are:1.Examine employee time cards and personnel records todetermine if sufficient information is available to maximizethe effective use of personnel.2.Review the processing of sales invoices to determine if itcould be done more efficiently.3.Review the acquisitions of goods, including costs, todetermine if they are being purchased at the lowest possiblecost considering the quality needed.4.Review and evaluate the efficiency of the manufacturingprocess.5.Review the processing of cash receipts to determine if theyare deposited as quickly as possible.1-10 When using a strategic systems auditing approach in an audit of historical financial statements, an auditor must have a thorough understanding of the client and its environment. This knowledge should include the client’s regulatory and operating environment, business strategies and processes, and measurement indicators. The strategic systems approach is also useful in other assurance or consulting engagements. For example, an auditor who is performing an assurance service on information technology would need to understand the client’s business strategies and processes related to information technology, including such things as purchases and sales via the Internet. Similarly, a practitioner performing a consulting engagement to evaluate the efficiency and effectiveness of a cli ent’s manufacturing process would likely start with an analysis of various measurement indicators, including ratio analysis and benchmarking against key competitors.1-11 The major differences in the scope of audit responsibilities are:1.CPAs perform audits in accordance with auditing standards ofpublished financial statements prepared in accordance withgenerally accepted accounting principles.2.GAO auditors perform compliance or operational audits inorder to assure the Congress of the expenditure of publicfunds in accordance with its directives and the law.3.IRS agents perform compliance audits to enforce the federaltax laws as defined by Congress, interpreted by the courts,and regulated by the IRS.4.Internal auditors perform compliance or operational auditsin order to assure management or the board of directors thatcontrols and policies are properly and consistentlydeveloped, applied and evaluated.1-12 The four parts of the Uniform CPA Examination are: Auditing and Attestation, Financial Accounting and Reporting, Regulation, and Business Environment and Concepts.1-13 It is important for CPAs to be knowledgeable about e-commerce technologies because more of their clients are rapidly expanding their use of e-commerce. Examples of commonly used e-commerce technologiesinclude purchases and sales of goods through the Internet, automatic inventory reordering via direct connection to inventory suppliers, and online banking. CPAs who perform audits or provide other assurance services about information generated with these technologies need a basic knowledge and understanding of information technology and e-commerce in order to identify and respond to risks in the financial and other information generated by these technologies.Multiple Choice Questions From CPA Examinations1-14 a. (3) b. (2) c. (2) d. (3)1-15 a. (2) b. (3) c. (4) d. (3)Discussion Questions And Problems1-16 a. The relationship among audit services, attestation services and assurance services is reflected in Figure 1-3 on page 13of the text. Audit services are a form of attestationservice, and attestation services are a form of assuranceservice. In a diagram, audit services are located within theattestation service area, and attestation services arelocated within the assurance service area.b. 1. (1) Audit of historical financial statements2.(2) An attestation service other than an auditservice; or(3) An assurance service that is not an attestationservice (WebTrust developed from the AICPASpecial Committee on Assurance Services, but theservice meets the criteria for an attestationservice.)3.(2) An attestation service other than an auditservice4.(2) An attestation service other than an auditservice5.(2) An attestation service other than an auditservice6.(2) An attestation service that is not an auditservice (Review services are a form ofattestation, but are performed according toStatements on Standards for Accounting andReview Services.)7.(2) An attestation service other than an auditservice8.(2) An attestation service other than an auditservice9.(3) An assurance service that is not an attestationservice1-17 a. The interest rate for the loan that requires a review report is lower than the loan that did not require a review becauseof lower information risk. A review report provides moderateassurance to financial statement users, which lowersinformation risk. An audit report provides further assuranceand lower information risk. As a result of reducedinformation risk, the interest rate is lowest for the loanwith the audit report.b.Given these circumstances, Vial-tek should select the loanfrom City First Bank that requires an annual audit. In thissituation, the additional cost of the audit is less than thereduction in interest due to lower information risk. Thefollowing is the calculation of total costs for each loan:1-17 (continued)c. Vial-tek may desire to have an audit because of the manyother positive benefits that an audit provides. The auditwill provide Vial-tek’s management with assurance aboutannual financial information used for decision-makingpurposes. The audit may detect errors or fraud, and providemanagement with information about the effectiveness ofcontrols. In addition, the audit may result inrecommendations to management that will improve efficiencyor effectiveness.d. Under a strategic systems audit approach, the auditor musthave a thorough understanding of the client and itsenvironment, including the client’s e-commerce technologies,industry, regulatory and operating environment, suppliers,customers, creditors, and business strategies and processes.This thorough analysis helps the auditor identify risksassociated with the client’s strategies that may affectwhether the financial statements are fairly stated. Whenapplying the strategic systems audit approach, the auditoroften discovers ways to help the client improve businessoperations, thereby providing added value to the auditfunction.1-18 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The servicesprovided by Consumers Union and assurance services providedby CPA firms are designed to improve the quality ofinformation for decision makers. CPAs are valued for theirindependence, and the reports provided by Consumers Unionare valued because Consumers Union is independent of theproducts tested.b.The concepts of information risk for the buyer of anautomobile and for the user of financial statements areessentially the same. They are both concerned with theproblem of unreliable information being provided. In thecase of the auditor, the user is concerned about unreliableinformation being provided in the financial statements. Thebuyer of an automobile is likely to be concerned about themanufacturer or dealer providing unreliable information.c.The four causes of information risk are essentially the samefor a buyer of an automobile and a user of financialstatements:(1)Remoteness of information It is difficult for a userto obtain much information about either an automobilemanufacturer or the automobile itself withoutincurring considerable cost. The automobile buyer doeshave the advantage of possibly knowing other users who are satisfied or dissatisfied with a similar automobile.(2)Biases and motives of provider There is a conflictbetween the automobile buyer and the manufacturer. The buyer wants to buy a high quality product at minimum cost whereas the seller wants to maximize the selling price and quantity sold.(3)Voluminous data There is a large amount of availableinformation about automobiles that users might like to have in order to evaluate an automobile. Either that information is not available or too costly to obtain.1-18 (continued)(4)Complex exchange transactions The acquisition of anautomobile is expensive and certainly a complexdecision because of all the components that go intomaking a good automobile and choosing between a largenumber of alternatives.d.The three ways users of financial statements and buyers ofautomobiles reduce information risk are also similar:(1)User verifies information him or herself That can beobtained by driving different automobiles, examiningthe specifications of the automobiles, talking toother users and doing research in various magazines.(2)User shares information risk with management Themanufacturer of a product has a responsibility to meetits warranties and to provide a reasonable product.The buyer of an automobile can return the automobilefor correction of defects. In some cases a refund maybe obtained.(3)Examine the information prepared by Consumer ReportsThis is similar to an audit in the sense thatindependent information is provided by an independentparty. The information provided by Consumer Reports iscomparable to that provided by a CPA firm that auditedfinancial statements.1-19 a. The following parts of the definition of auditing are related to the narrative:(1)Virms is being asked to issue a report aboutqualitative and quantitative information for trucks.The trucks are therefore the information with whichthe auditor is concerned.(2)There are four established criteria which must beevaluated and reported by Virms: existence of thetrucks on the night of June 30, 2005, ownership ofeach truck by Regional Delivery Service, physicalcondition of each truck and fair market value of eachtruck.(3)Susan Virms will accumulate and evaluate four types ofevidence:(a)Count the trucks to determine their existence.(b)Use registrations documents held by Oatley forcomparison to the serial number on each truck todetermine ownership.(c)Examine the trucks to determine each truck'sphysical condition.(d)Examine the blue book to determine the fairmarket value of each truck.(4)Susan Virms, CPA, appears qualified, as a competent,independent person. She is a CPA, and she spends most of her time auditing used automobile and truck dealerships and has extensive specialized knowledge about used trucks that is consistent with the nature of the engagement.1-19(continued)(5)The report results are to include:(a)which of the 35 trucks are parked in Regional'sparking lot the night of June 30.(b)whether all of the trucks are owned by RegionalDelivery Service.(c)the condition of each truck, using establishedguidelines.(d)fair market value of each truck using thecurrent blue book for trucks.b.The only parts of the audit that will be difficult for Virmsare:(1)Evaluating the condition, using the guidelines of poor,good, and excellent. It is highly subjective to do so.If she uses a different criterion than the "bluebook," the fair market value will not be meaningful.Her experience will be essential in using thisguideline.(2)Determining the fair market value, unless it isclearly defined in the blue book for each condition.1-20 a. The major advantages and disadvantages of a career as an IRS agent, CPA, GAO auditor, or an internal auditor are:1-20 (continued)EMPLOYMENT ADVANTAGES DISADVANTAGESINTERNAL AUDITOR 1.Extensive exposure to allsegments of theenterprise with whichemployed.2.Constant exposure to oneindustry presentingopportunity for expertisein that industry.3.Likely to have exposureto compliance, financialand operational auditing.1.Little exposure totaxation and the auditthereof.2.Experience is limited toone enterprise, usuallywithin one or a limitednumber of industries.(b)Other auditing careers that are available are:Auditors within many of the branches of the federalgovernment ., Atomic Energy Commission)Auditors for many state and local government units .,state insurance or bank auditors)1-21 The most likely type of auditor and the type of audit for each of the examples are:EXAMPLE TYPE OF AUDITOR TYPE OF AUDIT1.2.3.4.5.6.7.8.9.10.11.12.IRSGAOInternal auditor or CPACPA or Internal auditorGAOCPAGAOIRSCPAInternal auditor or CPAInternal auditor or CPAGAOComplianceOperationalOperationalFinancial statementsOperationalFinancial statementsFinancial statementsComplianceFinancial statementsComplianceFinancial statementsCompliance1-22 a. The conglomerate should either engage the management advisory services division of a CPA firm or its own internalauditors to conduct the operational audit.b.The auditors will encounter problems in establishingcriteria for evaluating the actual quantitative events andin setting the scope to include all operations in whichsignificant inefficiencies might exist. In writing thereport, the auditors must choose proper wording to statethat no financial audit was performed, that the procedureswere limited in scope and that the results reported do notnecessarily include all the inefficiencies that might exist.1-23 a. The CPA firm for the Internet company described in this problem could address these customer concerns by performinga WebTrust attestation engagement. The WebTrust assuranceservice was created by the profession to respond to thegrowing need for assurance resulting from the growth ofbusiness transacted over the Internet.b.The appropriate WebTrust principle for each of the customerconcerns noted in the problem is as follows:1.Accuracy of product descriptions and adherence tostated return policies: (3) Processing Integrity.2.Credit card and other personal information: (1) OnlinePrivacy and (2) Security.3.Selling information to other companies: (1) OnlinePrivacy and (2) Security.4.System failure: (4) Availability.Internet Problem Solution: Assurance Services1-1 This problem requires students to work with the AICPA assurance services Web site.1.Considering the assurance needs of customers and thecapabilities of CPAs, the Special Committee on AssuranceServices developed business plans for six assurance services.Chapter 1 of the textbook discussed several of theseservices. Go to the service description for the assuranceservice that most interests you (any one of the six). Whatare the major aspects or sections of the associated businessplan ., does the plan address market potential, competition,etc.?)Answer: Each business plan provides background information,describes the service, assesses market potential, discussesissues such as competition and why CPAs should offer theservice, identifies practice tools available and steps thatCPAs must take to begin offering the services.2.The Special Committee's report on Assurance Servicesdiscusses competencies needed by assurance providers todayand in the coming decade. Briefly describe the 5 generalcompetencies needed in the next decade (Hint: See the“About Assurance Services” link. Then follow the“Assurance Services and Academia” link.)Answer:The Committee identified the following five majorimperatives regarding future competencies, each of whichimplies increasing emphasis on the competencies noted:1-1 (continued)Customer focus.Assurance service providers need tounderstand user decision processes and how informationshould enter into those processes. Increased emphasis isneeded on: understanding user needs, communication skills,relationship management, responsiveness and timeliness.Migration to higher value-added information activities. Toprovide more value to client/decision makers and others,assurance service providers need to focus less on activitiesinvolved in the conversion of business events intoinformation ., collecting, classifying, and summarizingactivities) and more on activities involved in thetransformation of information into knowledge ., analyzing,interpreting, and evaluating activities) that effectivelydrives decision processes. This will require: analyticalskills, business advisory skills, business knowledge, modelbuilding (including sensitivity analysis), understanding theclient’s business processes, measurement theory(development of operational definitions of concepts, designof appropriate measurement techniques, etc.).Information technology (IT).Assurance services deal ininformation. Hence, the profound changes occurring ininformation technology will shape virtually all aspects ofassurance services. As information specialists, assuranceservice providers need to embrace information technology inall of its complex dimensions. Embracing IT meansunderstanding how it is transforming all aspects of business.It also means learning how to effectively use newdevelopments in hardware, software, communications, memory,encryption, etc., in everything assurance service providersdo as information specialists, not only in dealing withclients, but also in dealing with each other as individuals,teams, firms, state societies, and national professionalorganizations.Pace of change and complexity. Assurance services will takeplace in an environment of rapid change and increasingcomplexity. Assurance service providers need to investheavily in life-long learning in order to maintain up-to-date knowledge and skills. They will require: intellectualcapability, learning and rejuvenation.Competition.Growth in new assurance services will dependless on franchise/regulation and more on market forces.Assurance service providers need to develop their marketingskills —the ability to see clients’ latent informationand assurance needs and rapidly design and deploy cost-effective services to meet those needs —in order toeffectively compete for market-driven assurance services.Required skills include: marketing and selling,understanding customer needs, designing and deployingeffective solutions.1-1 (continued)(Note: Internet problems address current issues using Internet sources. Because Internet sites are subject to change, Internet problems and solutions are subject to change. Current information on Internet problems is available at。

有关审计报告的审计准则英文版

有关审计报告的审计准则英文版Auditing standards, also known as Generally Accepted Auditing Standards (GAAS) in the United States, are a set of systematic guidelines used by auditors when conducting audits of a company's financial information. 审计准则,也被称为美国的一般受理审计准则(GAAS),是审计师在对公司财务信息进行审计时所使用的一套系统性指导方针。

These standards are used to ensure that auditors perform their duties with integrity, objectivity, and professional competence. 这些标准用于确保审计师在履行职责时具有诚信、客观性和专业能力。

The auditing standards serve as a framework for auditors to follow in order to provide a reasonable assurance that the financial statements of a company are free from material misstatement. 审计准则作为审计师所要遵循的框架,旨在提供合理保证,即公司的财务报表不存在重大错误陈述。

By adhering to these standards, auditors are able to maintain consistency and reliability in their audit work across different companies and industries. 通过遵守这些标准,审计师能够在不同公司和行业的审计工作中保持一致性和可靠性。

大数据演讲稿

大数据演讲稿篇一:大数据演讲稿大數據演講稿第二頁:人類從十三世紀以來,透過測量世界、進而征服世界,為了減少資料錯誤,確保資料品質,我們不斷改善工具,好讓測量更精準。

然而現在有愈來愈多的資料,我們必須要知道資料量越多,就愈不可能精確,因此我們必須換個心態,來接受這個事實。

第三頁:在大數據的概念裏頭,我們必須以新觀念來面對新局面,我們必須跳脫「越多越好」的概念,讓愈多會比品質愈好更重要。

因此我們要開始認識在這些越多的東西裏頭,無可避免會產生的雜亂問題,而也就是這個問題,我們必須了解有哪些雜亂!雜亂基本上分成三種,第一種是資料量多而產生的雜亂,越多的資料出錯率越高。

第二種是資料型態不同而產生相容性問題,例如:消防員用語音辨識系統和人做受災資料蒐集,機器和人收集資料型態不同,比對時無可避面會產生雜亂,但往往更能掌握當下的實際情況。

第三種是不同格式的資料型態產生的雜亂,此雜亂往往發生在提取或處理資料時,因為接收端與輸出端,資料格式不一,而產生的雜亂問題。

但我們不用擔心,舉個例子-用十隻很貴的溫度計量和一百隻便宜的溫度計量,雖然便宜不準,但蒐集越多的數據,也可以越看清全貌,因此更多的資料點,帶來的巨大價值,使得雜亂變得微不足道。

總之,我們可以犧牲一點精確度,取用所有的資料點,我們更能看出整體的大趨勢。

第四頁:西洋棋規則完善,行之有年,其主要歸功於他的演算法和殘局處理能力,而殘局處理能力往往源自於它內建的殘局應對資料,而這個殘局應對分析主要是在只剩下六顆棋子的情況下,每一步都經過完整的分析,做成巨量的表供程式做運算處理,那我們發現,如果我們讓其殘局應對資料增加越多,甚至高達1TB,我們越能讓程式變得完成無暇,無人能敵。

在語料庫的例子,這個例子來自微軟在做word 的文法檢查所得到的發現。

他們一開始在增進文法檢查這個功能上,考慮到,是否要改良演算法、用更複雜的功能去實現,or使用更多的資料去餵給現有的演算系統,結果發現,改良演算法,準確率提升8%,但用後者方法,準確率提升足足20%以上,由此兩個例子可知資料數量子資料品質更重要。