审计文献翻译

同样地,表二显示在其他竞争变量(COMP2和COMP3)和企业做出隐瞒销售信息之间有这正向单调相关性,并且在每一个案例中我们都驳回了在1%程度上没有联系这种无效假设。

4.3

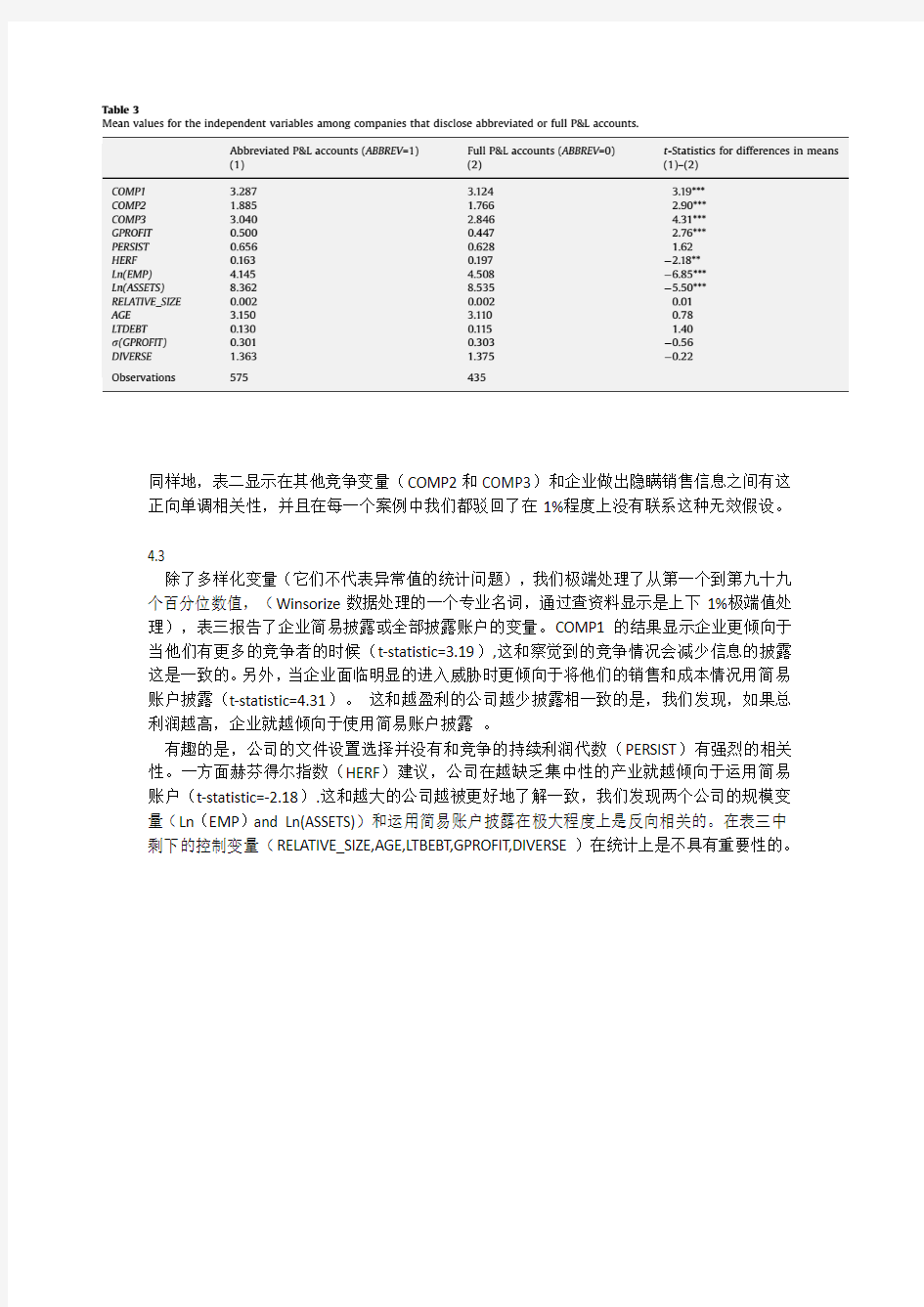

除了多样化变量(它们不代表异常值的统计问题),我们极端处理了从第一个到第九十九个百分位数值,(Winsorize数据处理的一个专业名词,通过查资料显示是上下1%极端值处理),表三报告了企业简易披露或全部披露账户的变量。COMP1的结果显示企业更倾向于当他们有更多的竞争者的时候(t-statistic=3.19),这和察觉到的竞争情况会减少信息的披露这是一致的。另外,当企业面临明显的进入威胁时更倾向于将他们的销售和成本情况用简易账户披露(t-statistic=4.31)。这和越盈利的公司越少披露相一致的是,我们发现,如果总利润越高,企业就越倾向于使用简易账户披露。

有趣的是,公司的文件设置选择并没有和竞争的持续利润代数(PERSIST)有强烈的相关性。一方面赫芬得尔指数(HERF)建议,公司在越缺乏集中性的产业就越倾向于运用简易账户(t-statistic=-2.18).这和越大的公司越被更好地了解一致,我们发现两个公司的规模变量(Ln(EMP)and Ln(ASSETS))和运用简易账户披露在极大程度上是反向相关的。在表三中

剩下的控制变量(RELATIVE_SIZE,AGE,LTBEBT,GPROFIT,DIVERSE)在统计上是不具有重要性的。

4.4

一个相关模型(表四)显示调查变量(COMP,COMP2和COMP3)在极大程度上是正向相关的,即使相关性这个数据不是非常高(0.26,0.23,0.16)。这些变量似乎捕捉到了不同但是相关的关于竞争的特点,这是被管理者所理解的。盈利性和进入威胁的测量之间的联系是正相关的,并具有统计重要性(p-value=0.01),这和可竞争市场理论是相一致的,根据高利润增加了外来竞争者进入企业所在市场的威胁。

盈利性(GPROFIT)和经营者报告的需求价格弹性(COMP)之间的相关性是负数(-0.06)并且具有重要性(p-value=0.04),这支持了当一个公司的需求更具有价格弹性时它盈利越少这样一个理论。在我们的样本里,更高的利润会增加新竞争者进入市场带来的竞争威胁,这和可竞争市场理论是相一致的。相应地,调查者需要明白高利润不是就一定指示着低竞争产品市场。

当在检查调查变量的有效性时我们调查了是否一个公司对调查问题的回答与和它在同一行业的公司的回答是相互应证的。对于每个公司i,我们计算了这个three-digit行业所有其他公司的平均答复,我们分别标注了AV_COMP1,AV_COMP2,和AV_COMP3,我们发现COMP 和AVCOMP变量之间有很大程度上的正向相关性。比如说,COMP1和AV_COMP1之间的相关性是+0.16,小于重要性值1%,表明公司i更倾向于认为竞争者的数量很多,如果这个行业里的其他公司都认为竞争者数量很多。这种在给定公司的调查回复和其他同行业公司的回复之间的具有重要性的正向相关性表明了经营者关于竞争的自我报告的看法会相互应证。在表四中,产业集中度变量(HERF)和现存报告竞争者数(COMP1)以及价格弹性的需求量(COMP3)是反向相关的.这种反向相关性表明,在集中市场中经营的管理者相信他们有更少的竞争者并且相信他们的需求曲线具有更少的价格弹性。同时,这些发现暗示出更集

中的产业和更少的竞争是相互联系的。此外,产业集中度和认为的新进入者的威胁(COMP2)是没有多大的联系的。更进一步,盈利性变量(GPROFIT)和赫德尔非产业集中度变量(HERF)也是没有多大联系的。这和产业组织结构理论是相一致的。同时,我们也发现PERSIST和经营者对竞争情况的看法是正交的。

5.主要的结果

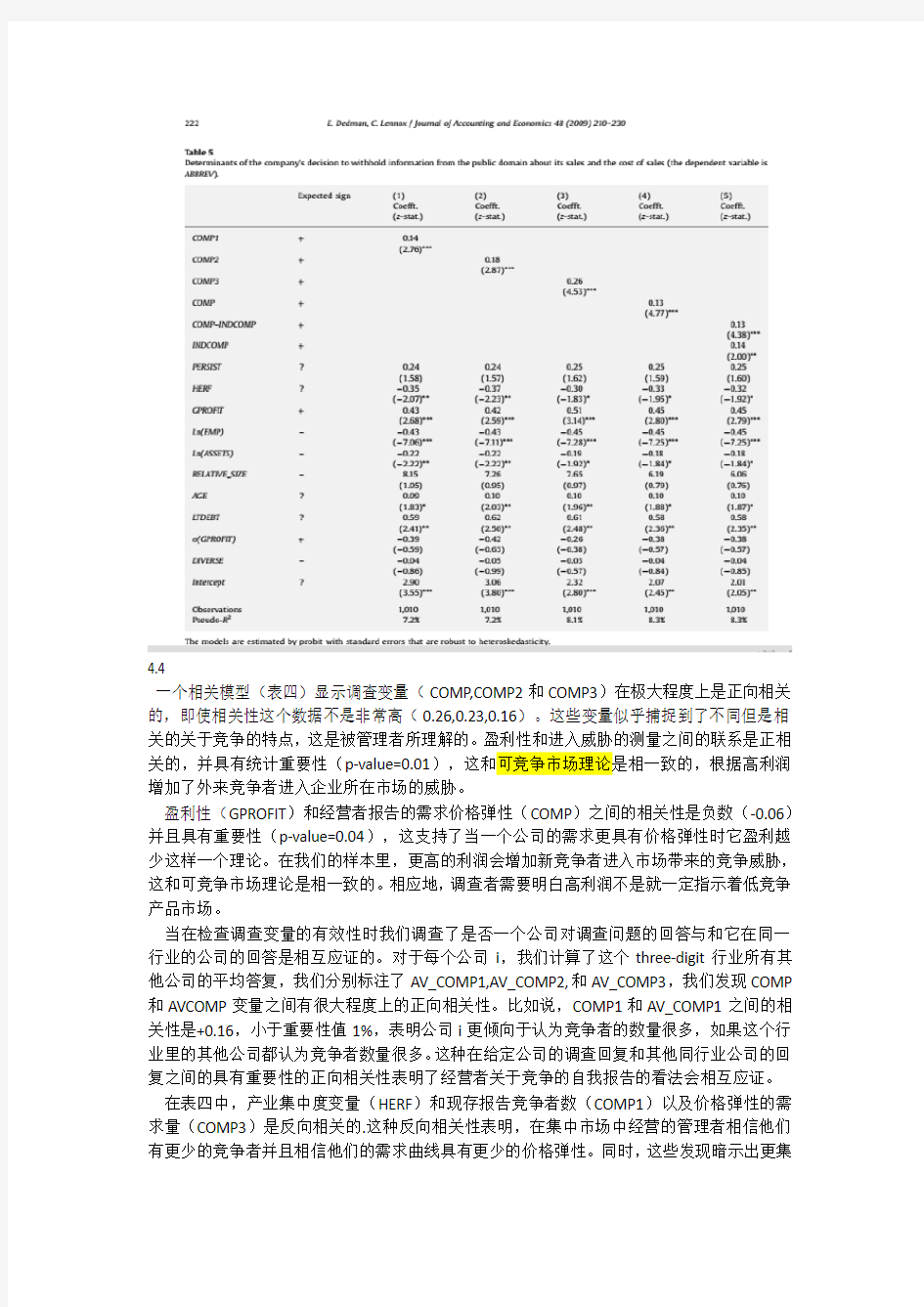

5.1 竞争和隐瞒销售信息的决定

表五报告了用回归分析法来检查企业对选择使用简易账户而不是全部账户的决定。纵列1-3显示,有三种对竞争的研究方法(COMP1-3)和选择使用简易账户之间的关系是正向且具有重要性的,(z-statistics=2.76,2.87,4.53),这和如果经营者认为市场的竞争太多就会选择隐瞒销售信息是相一致的。

为了分析这些结果的经济重要性,我们估计了一个选择运用简易账户的盈利值的其他的价值来作为调查变量。最后发现,披露和认为的竞争程度之间的经济性是十分大的。

表五中的持续盈利的竞争方法(PERSIST)和竞争的调查的调查方法相比就显得不那么具有重要性了。赫德尔非(HERF)系数是负数并且重要性在10%或者5%,这和Verrecchia and Weber关于越不集中的产业越倾向于隐瞒信息的理论是相一致的。

一个非常重要的在调查和关于档案的变量之间的差异是,前者在站在评估公司的角度,而后者站在产业的角度。

产业组织理论(Industrial Organization), 研究市场在不完全竞争条件下的企业行为和市场构造

Abbreviated Accounts

If you are a small limited company you may be entitled to file abbreviated accounts to Companies House. The current criteria (from 6th April 2008) for a small company is that you must meet at least two of the following conditions:

?Annual turnover must be no more than £6.5 million

?Balance sheet total must be no more than £3.26 million

?Average number of employees must be no more than 50

The advantage of this is that abbreviated accounts require much less information than full accounts, therefore competitors and the general public will not see detailed information regarding your accounts. Also, most small companies do not require a full audit.

Abbreviated accounts contain a basic balance sheet, which show the assets and liabilities of the company. Assets include things such as bank balances, equipment, vehicles, trade debtors (money customers owe you). Liabilities may include loans, overdrafts, trade creditors (money you owe suppliers. By adding up assets and taking away liabilities it gives a snapshot of your company’s net value. This of course doesn’t provide the full picture, as doesn’t take into account your order book, goodwill, brand, reputation etc.

世界贸易和国际贸易【外文翻译】

外文翻译 原文 World Trade and International Trade Material Source:https://www.360docs.net/doc/b33783605.html, Author: Ted Alax In today’s complex economic world, neither individuals nor nations are self-sufficient. Nations have utilized different economic resources; people have developed different skills. This is the foundation of world trade and economic activity. As a result of this trade and activity, international finance and banking have evolved. For example, the United States is a major consumer of coffee, yet it does not have the climate to grow any or its own. Consequently, the United States must import coffee from countries (such as Brazil, Colombia and Guatemala) that grow coffee efficiently. On the other hand, the United States has large industrial plants capable of producing a variety of goods, such as chemicals and airplanes, which can be sold to nations that need them. If nations traded item for item, such as one automobile for 10,000 bags of coffee, foreign trade would be extremely cumbersome and restrictive. So instead of batter, which is trade of goods without an exchange of money, the United State receives money in payment for what it sells. It pays for Brazilian coffee with dollars, which Brazil can then use to buy wool from Australia, which in turn can buy textiles Great Britain, which can then buy tobacco from the United State. Foreign trade, the exchange of goods between nations, takes place for many reasons. The first, as mentioned above is that no nation has all of the commodities that it needs. Raw materials are scattered around the world. Large deposits of copper are mined in Peru and Zaire, diamonds are mined in South Africa and petroleum is recovered in the Middle East. Countries that do not have these resources within their own boundaries must buy from countries that export them. Foreign trade also occurs because a country often does not have enough of a particular item to meet its needs. Although the United States is a major producer of sugar, it consumes more than it can produce internally and thus must import sugar.

关于力的外文文献翻译、中英文翻译、外文翻译

五、外文资料翻译 Stress and Strain 1.Introduction to Mechanics of Materials Mechanics of materials is a branch of applied mechanics that deals with the behavior of solid bodies subjected to various types of loading. It is a field of study that i s known by a variety of names, including “strength of materials” and “mechanics of deformable bodies”. The solid bodies considered in this book include axially-loaded bars, shafts, beams, and columns, as well as structures that are assemblies of these components. Usually the objective of our analysis will be the determination of the stresses, strains, and deformations produced by the loads; if these quantities can be found for all values of load up to the failure load, then we will have obtained a complete picture of the mechanics behavior of the body. Theoretical analyses and experimental results have equally important roles in the study of mechanics of materials . On many occasion we will make logical derivations to obtain formulas and equations for predicting mechanics behavior, but at the same time we must recognize that these formulas cannot be used in a realistic way unless certain properties of the been made in the laboratory. Also , many problems of importance in engineering cannot be handled efficiently by theoretical means, and experimental measurements become a practical necessity. The historical development of mechanics of materials is a fascinating blend of both theory and experiment, with experiments pointing the way to useful results in some instances and with theory doing so in others①. Such famous men as Leonardo da Vinci(1452-1519) and Galileo Galilei (1564-1642) made experiments to adequate to determine the strength of wires , bars , and beams , although they did not develop any adequate theo ries (by today’s standards ) to explain their test results . By contrast , the famous mathematician Leonhard Euler(1707-1783) developed the mathematical theory any of columns and calculated the critical load of a column in 1744 , long before any experimental evidence existed to show the significance of his results ②. Thus , Euler’s theoretical results remained unused for many years, although today they form the basis of column theory. The importance of combining theoretical derivations with experimentally determined properties of materials will be evident theoretical derivations with experimentally determined properties of materials will be evident as we proceed with

内部审计在公司治理中的价值【外文翻译】

外文翻译 原文: T h e V a l u e O f In t e r n a l A u d i t In C or p or a t e G ov e r n a n c e Today, corporate boards must provide close oversight of such vital issues as finance, accounting, risk management, and compliance in often-complex o r g anizati ons. Yet there i s an organization wi t hin the c ompa ny t hat ha s bee n shaping just the controls needed to effectively monitor these governance matters—internal audit. By making internal audit a stronger player in the governance team, smart boards can tap into a highly valuable source of expertise. Internal auditors are like a lighthouse. Their work provides a point of reference that enabl e s compani e s t o know w he re t hey are—and t heir gui dance c a n h elp provide the insights they need to navigate with confidence into the future. That is why expectations are high that internal auditors will “raise the bar”by continuing to improve operating efficiency as well as effectiveness—not just in controls, risk management, and governance, but across the enterprise as a whole. There a re th re e mess a ges I would like to shar e on how i nternal audi t ors ca n ke e p th e momentum going by building new value for today, and by becoming a source of leadership talent for business organizations tomorrow. First,internal auditors can help enable the“risk intelligent enterprise.” While management and the board may “o w n”risk, internal auditors can play a key role in ena b ling the “risk int e llige n t e nt erpri s e.”At D e loitt e, this is an outcome t hat we strongly advocate for our clients, for ourselves, and for any corporation that wants to grow and prosper. Think about it. In all companies, risk abounds—in governance, in strategy and execution, in operations, and in infrastructure. If the magnitude of this challenge were not already enough, other factors can leverage the impact of risk, from the speed at which events can unfold to the uncertainty that often accompanies them. It would be great if those were the only challenges but, of course, there are countless others to consider.

环境会计外文文献及其翻译

河南科技学院新科学院2013届本科毕业论文(设计) 外文文献及翻译 Environmental Accounting 学生姓名:叶乃润 所在系别:经济系 所学专业:国际经济与贸易 导师姓名:郭晓明(助教) 完成时间:2013年4月18日

Environmental Accounting by Joy E. Hecht Interest is growing in modifying national income accounting systems to promote understanding of the links between economy and environment. The field of environmental accounting has made great strides in the past two decades, moving from a rather arcane endeavor to one tested in dozens of countries and well established in a few. But the idea that nations might integrate the economic role of the environment into their income accounts is neither a quick sell nor a quick process; it has been under discussion since the 1960s. Despite the difficulties and controversies described in this article, however, interest is growing in modifying national income accounting systems to promote understanding of the links between economy and environment. Environmental accounting is underway in several dozen countries, where bureaucrats, statisticians, and other proponents both foreign and domestic have initiated activities over the past few decades. Several countries have made continuous investments in building routine data systems, which are integrated into existing statistical systems and economic planning activities. Others have made more limited efforts to calculate a few indicators, or analyze a single sector. Some of the earliest research on environmental accounting was done at RFF by Henry Peskin, working on the design of accounts for the United States. One of the first countries to build environmental accounts is Norway, which began collecting data on energy sources, fisheries, forests, and minerals in the 1970s to address resource scarcity. Over time, the Norwegians have expanded their accounts to include data on air pollutant emissions. Their accounts feed into a model of the national economy, which policymakers use to assess the energy implications of alternate growth strategies. Inclusion of these data also allows them to anticipate the impacts of different growth patterns on compliance with international conventions on pollutant emissions. More recently, a number of resource-dependent countries have become interested in measuring depreciation of their natural assets and adjusting their GDPs environmentally. One impetus for their interest was the 1989 study “Wasting Assets: Natural Resources in the National Income Accounts,” in which Robert Repetto and his colleagues at the World Resources Institute estimated the depreciation of Indonesia’s forests, petroleum reserves, and soil assets. Once adjusted to account for that depreciation, Indonesia’s GDP and growth rates both sank significantly below conventional figures. While “Wasting Assets” called many to action, it also op erated as a brake, leading many economists and statisticians to warn against a focus on green GDP, because it tells decision makers nothing about the causes or solutions for environmental problems. Since that time, several developing countries have made long-term commitments to broad-based environmental accounting. Namibia began work on resource accounts in 1994, addressing such questions as whether the government has been able to

国际贸易、市场营销类课题外文翻译——市场定位策略(Positioning_in_Practice)

Positioning in Practice Strategic Role of Marketing For large firms that have two or more strategic business units (SBUs), there are generally three levels of strategy: corporate-level strategy, strategic-business-unit-level (or business-level) strategy, and marketing strategy. A corporate strategy provides direction on the company's mission, the kinds of businesses it should be in, and its growth policies. A business-level strategy addresses the way a strategic business unit will compete within its industry. Finally, a marketing strategy provides a plan for pursuing the company's objectives within a specific market segment. Note that the higher level of strategy provides both the objectives and guidelines for the lower level of strategy. At corporate level, management must coordinate the activities of multiple strategic business units. Thus the decisions about the organization's scope and appropriate resource deployments/allocation across its various divisions or businesses are the primary focus of corporate strategy.Attempts to develop and maintain distinctive competencies tend to focus on generating superior financial, capital, and human resources; designing effective organizational structures and processes; and seeking synergy among the firm's various businesses. At business-level strategy, managers focus on how the SBU will compete within its industry. A major issue addressed in business strategy is how to achieve and sustain a competitive advantage. Synergy for the unit is sought across product-markets and across functional department within the unit. The primary purpose of a marketing strategy is to effectively allocate and coordinate marketing resources and activities to accomplish the firm's objectives within a specific product-market. The decisions about the scope of a marketing strategy involve specifying the target market segment(s) to pursue and the breadth of the product line to offered. At this level of strategy, firms seek competitive advantage and synergy through a well-integrated program of marketing mix elements tailored to the needs and wants of customers in the target segment(s). Strategic Role of Positioning Based on the above discussion, it is clear that marketing strategy consists of two parts: target market strategy and marketing mix strategy. Target market strategy consists of three processes: market segmentation, targeting (or target market selection), and positioning. Marketing mix strategy refers to the process of creating a unique

10kV小区供配电英文文献及中文翻译

在广州甚至广东的住宅小区电气设计中,一般都会涉及到小区的高低压供配电系统的设计.如10kV高压配电系统图,低压配电系统图等等图纸一大堆.然而在真正实施过程中,供电部门(尤其是供电公司指定的所谓电力设计小公司)根本将这些图纸作为一回事,按其电脑里原有的电子档图纸将数据稍作改动以及断路器按其所好换个厂家名称便美其名曰设计(可笑不?),拿出来的图纸根本无法满足电气设计的设计意图,致使严重存在以下问题:(也不知道是职业道德问题还是根本一窍不通) 1.跟原设计的电气系统货不对板,存在与低压开关柜后出线回路严重冲突,对实际施工造成严重阻碍,经常要求设计单位改动原有电气系统图才能满足它的要求(垄断的没话说). 2.对消防负荷和非消防负荷的供电(主要在高层建筑里)应严格分回路(从母线段)都不清楚,将消防负荷和非消防负荷按一个回路出线(尤其是将电梯和消防电梯,地下室的动力合在一起等等,有的甚至将楼顶消防风机和梯间照明合在一个回路,以一个表计量). 3.系统接地保护接地型式由原设计的TN-S系统竟曲解成"TN-S-C-S"系统(室内的还需要做TN-C,好玩吧?),严格的按照所谓的"三相四线制"再做重复接地来实施,导致后续施工中存在重复浪费资源以及安全隐患等等问题.. ............................(违反建筑电气设计规范等等问题实在不好意思一一例举,给那帮人留点混饭吃的面子算了) 总之吧,在通过图纸审查后的电气设计图纸在这帮人的眼里根本不知何物,经常是完工后的高低压供配电系统已是面目全非了,能有百分之五十的保留已经是谢天谢地了. 所以.我觉得:住宅建筑电气设计,让供电部门走!大不了留点位置,让他供几个必需回路的电,爱怎么折腾让他自个怎么折腾去.. Guangzhou, Guangdong, even in the electrical design of residential quarters, generally involving high-low cell power supply system design. 10kV power distribution systems, such as maps, drawings, etc. low-voltage distribution system map a lot. But in the real implementation of the process, the power sector (especially the so-called power supply design company appointed a small company) did these drawings for one thing, according to computer drawings of the original electronic file data to make a little change, and circuit breakers by their the name of another manufacturer will be sounding good design (ridiculously?), drawing out the design simply can not meet the electrical design intent, resulting in a serious following problems: (do not know or not know nothing about ethical issues) 1. With the original design of the electrical system not meeting board, the existence and low voltage switchgear circuit after qualifying serious conflicts seriously hinder the actual construction, often require changes to the original design unit plans to meet its electrical system requirements (monopoly impress ). 2. On the fire load and fire load of non-supply (mainly in high-rise building in) should be strictly sub-loop (from the bus segment) are not clear, the fire load and fire load of non-qualifying press of a circuit (especially the elevator and fire elevator, basement, etc.

财务内部审计风险中英文对照外文翻译文献

中英文对照外文翻译文献 (文档含英文原文和中文翻译) 译文: 浅析内部审计风险的成因及解决途径 摘要 内部审计风险成因包括内部审计机构的独立性不够,内部审计人员的业务不精,内部审计方法的科学性不强,内部审计管理的制度不健全。为了降低内部审计风险,应加强内部审计的法制建设,保证内部审计的独立性,提高内部审计人员的素质,执行科学合理的审计工作程序,正确处理降低风险与经济效益的关系,开

展以风险为导向的风险基础审计。 一、内部审计风险形成的原因 1.内部审计机构的独立性不够内部审计机构是单位内设机构,在单位负责人的领导下开展工作,为单位服务。因此,内部审计的独立性不如社会审计,在审计过程中,不可避免地受本单位的利益制约。内审人员面临的是与单位领导层之间的领导与被领导的关系以及与各科室、部门之间的同事关系,所涉及的人不是领导就是同事,非直接有关也是间接相关, 审计过程及结论然涉及到具体的个人利益,因而审计过程难免受到各类人员干扰。 2.内部审计人员的业务不精审计人员素质的高低是决定审计风险大小的主要因素。审计人员的素质包括从事审计需要的政策法规水平、专业知识、经验、技能、审计职业道德和工作责任。 审计经验是审计人员应有的一种重要技能,审计经验需要实践的积累。我国的内部审计人员中不少人仅熟悉财务会计业务,一些审计人员不了解本单位的经营活动和内部控制,审计经验有限。另外,内部审计人员工作责任和职业道德也是影响审计风险的因素。由于我国内审准则工作规范和职业道德标准方面还有一些空白,许多内审机构和人员缺乏应有的职业规范的约束和指导。总之,目前我国内审人员总体素质偏低,直接影响到内审工作开展的深度和广度。面对当今内审对象的复杂和内容的拓展,内审人员势单力簿,这将直接导致审计风险的产生。 3.内部审计方法的科学性不强 我国内审方法是制度基础审计,随着企业内部经营管理环境复杂化,这种审计模式不适应开展内部管理审计的需要,因为它过分依赖于对企业内部管理控制的测试,本身就蕴藏巨大的风险内部审计一般采用统计抽样方法,由于抽样审计本身是以样本的审查结果来推断总体的特征,因此,样本和总体之间必然会形成一定的误差,形成审计的抽样风险。随着信息化程度提高,被审计单位的会计信息资料会越来越多,差错和虚假的会计资料掺杂其中,失察的可能性也随之加大。虽然统计抽样是建立在坚实的数学理论基础之上,但其本身是允许存在一定的审计风险的。同样,大量的分析性审核也会产生相关风险,使审计风险的构成内容更4.内部审计管理的制度不健全

会计信息质量外文文献及翻译

会计信息质量在投资中的决策作用对私人信息和监测的影响 安妮比蒂,美国俄亥俄州立大学 瓦特史考特廖,多伦多大学 约瑟夫韦伯,美国麻省理工学院 1简介 管理者与外部资本的供应商信息是不对称的在这种情况下企业是如何影响金融资本 的投资的呢?越来越多的证据表明,会计质量越好,越可以减少信息的不对称和对融资成本的约束。与此相一致的可能性是,减少了具有更高敏感性的会计质量的公司的投资对内部产生的现金流量。威尔第和希拉里发现,对企业投资和与投资相关的会计质量容易不足,是容易引发过度投资的原因。 当投资效率低下时,会计的质量重要性可以减轻外部资本的影响,供应商有可能获得私人信息或可直接监测管理人员。通过访问个人信息与控制管理行为,外部资本的供应商可以直接影响企业的投资,降低了会计质量的重要性。符合这个想法的还有比德尔和希拉里的比较会计对不同国家的投资质量效益的影响。他们发现,会计品质的影响在于美国投资效益,而不是在日本。他们认为,一个可能的解释是不同的是债务和股权的美国版本的资本结构混合了SUS的日本企业。 我们研究如何通过会计质量灵敏度的重要性来延长不同资金来源对企业的投资现金 流量的不同影响。直接测试如何影响不同的融资来源会计,通过最近获得了债务融资的公司来投资敏感性现金流的质量的效果,债务融资的比较说明了对那些不能够通过他们的能力获得融资的没有影响。为了缓解这一问题,我们限制我们的样本公司有所有最近获得的债务融资和利用访问的差异信息和监测通过公共私人债务获得连续贷款的建议。我们承认,投资内部现金流敏感性可能较低获得债务融资的可能性。然而,这种可能性偏见拒绝了我们的假设。 具体来说,我们确定的数据样本证券公司有1163个采样公司(议会),通过发行资本公共债务或银团债务。我们限制我们的样本公司最近获得的债务融资持有该公司不断融资与借款。然而,在样本最近获得的债务融资的公司,也有可能是信号,在资本提供进入私人信息差异和约束他们放在管理中的行为。相关理论意味着减少公共债务持有人获取私人信息,因而减少借款有效的监测。在这些参数的基础上,我们预测,会计质量应该有一

跨境电商外文文献综述

跨境电商外文文献综述 (文档含英文原文和中文翻译) 译文: 本地化跨境电子商务的模型 摘要 通过对国际供应链的B2B电子商务交易量的快速增长和伊朗快速增加的跨境交易业务,跨境电商过程的有效管理对B2B电子商务系统十分重要。本文对局部模型的结构是基于B2B电子商务的基础设施三大层,消息层、业务流程层和内容层。由于伊朗的电子商务的要求,每一层的需要适当的标准和合适的方案的选择。当电子文件需要移动顺利向伊朗,建议文件的标准为文件内容支持纸质和电子文件阅读。验证提出的模型是通过案例研究方法呈现一到四阶段的情景。本文试图通过交换商业文件在贸易过程中这一局部模型,实现在全球电子贸易供应链更接近区域单一窗口建设的关键目标。 关键词:电子商务;跨境贸易;电子文档管理;国际供应链

1.简介 电子商务是关于在互联网或其他网络电子系统购买和销售产品或服务。术语B2B(企业对企业),描述了企业间的电子商务交易,如制造商和批发商,或批发商和零售商之间。本文的研究目标是上两个不同国家贸易商之间的通信。今天的世界贸易组织的主要目标之一是建立区域单一窗口,可以提高世界各地的贸易便利化。建立区域单一窗口需要跨境海关,可以有效地交换贸易文件。因此,首先,简化跨境贸易文件的关键在于朝着国家单一窗口移动。然后,区域单一窗口可以授权国家之间的通信。电子商务模型是基于三个主要逻辑层的研究。这三个层消息传输层,业务处理层和内容层。本文的局部模型是一种能够自动交换读取文件的过程。通过与东亚和中东国家的建立区域单一窗口可以在将来得到改善的更多的互操作性,从而建立伊朗国家单一窗口 在本文的第二部分讨论引进国际供应链中的跨境B2B模式所需的基本概念和标准。第三部分介绍在大的模型中引入的组件功能和范围。第四部分讨论了B2B交易层模型的定位,最后结束本文。 2.背景 在本节中,除了了解B2B电子商务在伊朗的情况,还有参考模型的背景等概念以及讨论B2B电子商务跨境模式的本土化。 2.1 B2B电子商务在伊朗 如今伊朗在贸易进程的变现是一个关键的贸易成功点。伊朗和许多其他国家接壤,它的进口和出口过程可以通过公路,铁路,海上和空中的方式来完成。因此,这个国家的中部和战略作用,使得它在亚洲和中东地区货物运输的主要贸易点。今天,在伊朗海关几乎所有的贸易过程通过纸质表格完成,由商务部提供的电子服务仅限于谁该国境内交易的商人。今天,伊朗海关几乎所有的贸易流程都是通过纸质表格来完成的,商务部给出的电子服务只限于该国的商人。介绍了模型试图简化在伊朗交易的跨境电子商务供应链交换电子文件的过程。这里提到的一些系统,由商务部在伊朗的电子服务被提及:进口订单管理系统。贸易统计制度。伊朗法典伊朗。这些电子系统的主要使用,以促进在伊朗贸易过程。这里提到的系统作为独立的贸易者可与建议本文模型在未来的作用。在亚洲的区域性单

英文论文及中文翻译

International Journal of Minerals, Metallurgy and Materials Volume 17, Number 4, August 2010, Page 500 DOI: 10.1007/s12613-010-0348-y Corresponding author: Zhuan Li E-mail: li_zhuan@https://www.360docs.net/doc/b33783605.html, ? University of Science and Technology Beijing and Springer-Verlag Berlin Heidelberg 2010 Preparation and properties of C/C-SiC brake composites fabricated by warm compacted-in situ reaction Zhuan Li, Peng Xiao, and Xiang Xiong State Key Laboratory of Powder Metallurgy, Central South University, Changsha 410083, China (Received: 12 August 2009; revised: 28 August 2009; accepted: 2 September 2009) Abstract: Carbon fibre reinforced carbon and silicon carbide dual matrix composites (C/C-SiC) were fabricated by the warm compacted-in situ reaction. The microstructure, mechanical properties, tribological properties, and wear mechanism of C/C-SiC composites at different brake speeds were investigated. The results indicate that the composites are composed of 58wt% C, 37wt% SiC, and 5wt% Si. The density and open porosity are 2.0 g·cm–3 and 10%, respectively. The C/C-SiC brake composites exhibit good mechanical properties. The flexural strength can reach up to 160 MPa, and the impact strength can reach 2.5 kJ·m–2. The C/C-SiC brake composites show excellent tribological performances. The friction coefficient is between 0.57 and 0.67 at the brake speeds from 8 to 24 m·s?1. The brake is stable, and the wear rate is less than 2.02×10?6 cm3·J?1. These results show that the C/C-SiC brake composites are the promising candidates for advanced brake and clutch systems. Keywords: C/C-SiC; ceramic matrix composites; tribological properties; microstructure [This work was financially supported by the National High-Tech Research and Development Program of China (No.2006AA03Z560) and the Graduate Degree Thesis Innovation Foundation of Central South University (No.2008yb019).] 温压-原位反应法制备C / C-SiC刹车复合材料的工艺和性能 李专,肖鹏,熊翔 粉末冶金国家重点实验室,中南大学,湖南长沙410083,中国(收稿日期:2009年8月12日修订:2009年8月28日;接受日期:2009年9月2日) 摘要:采用温压?原位反应法制备炭纤维增强炭和碳化硅双基体(C/C-SiC)复合材