No.1 Solution CPA MA1 练习 No.1

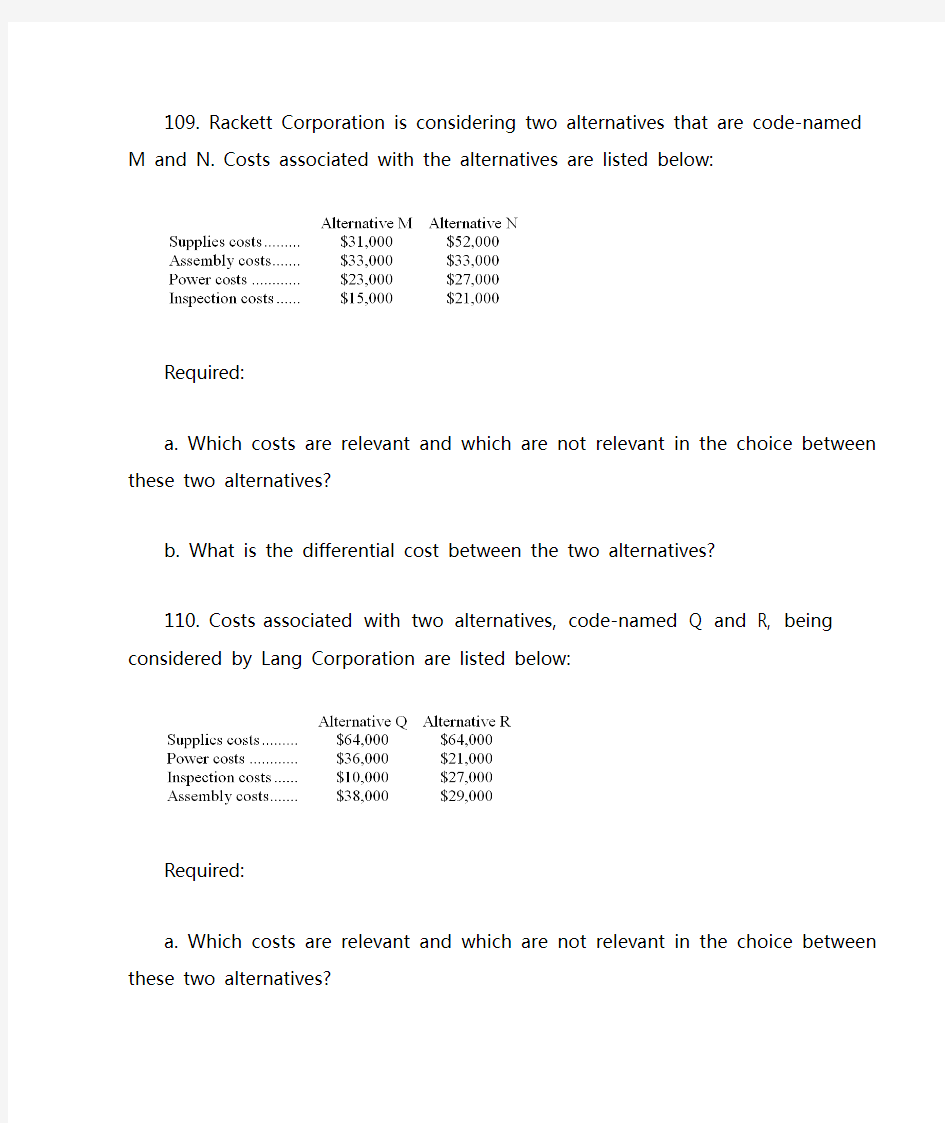

109. Rackett Corporation is considering two alternatives that are code-named M and N. Costs associated with the alternatives are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two alternatives?

b. What is the differential cost between the two alternatives?

110. Costs associated with two alternatives, code-named Q and R, being considered by Lang Corporation are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two alternatives?

b. What is the differential cost between the two alternatives?

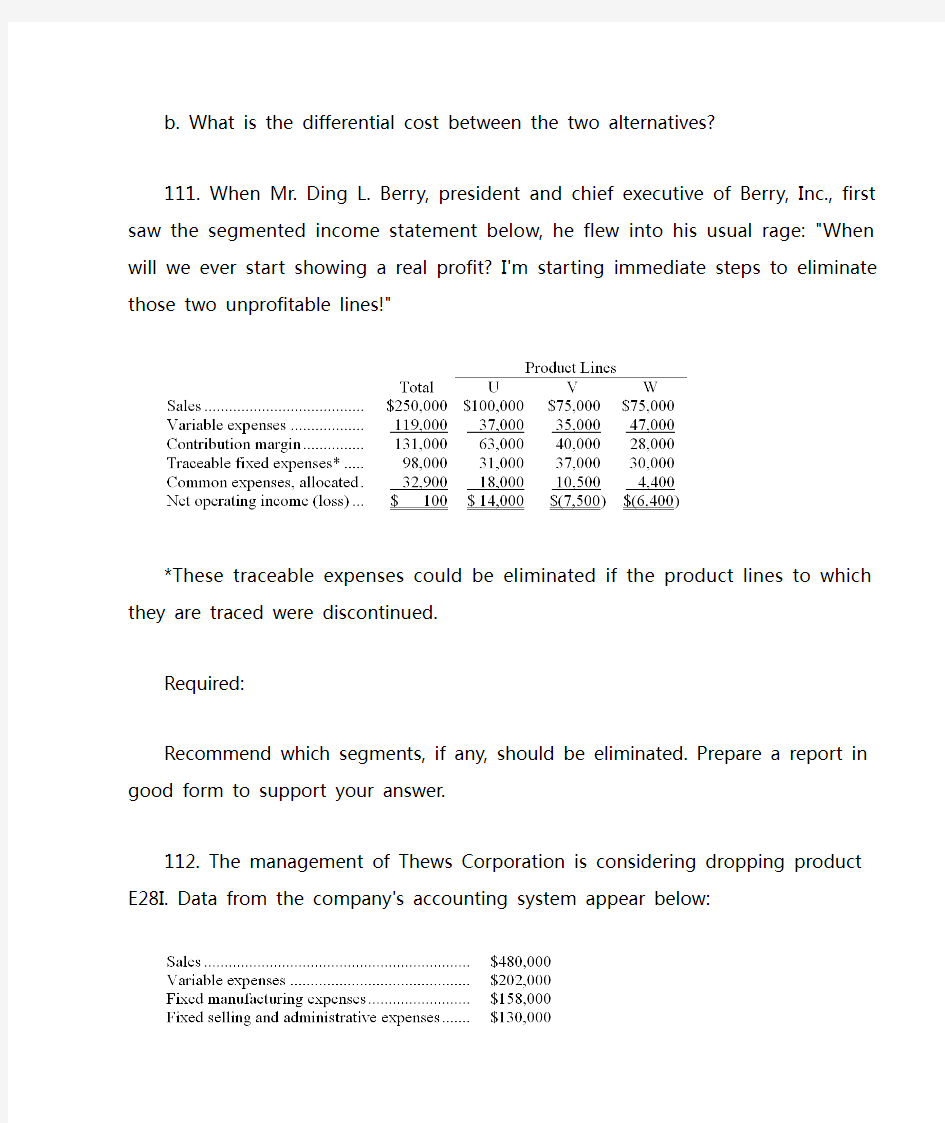

111. When Mr. Ding L. Berry, president and chief executive of Berry, Inc., first saw the segmented income statement below, he flew into his usual rage: "When will we ever start showing a real profit? I'm starting immediate steps to eliminate those two unprofitable lines!"

*These traceable expenses could be eliminated if the product lines to which they are traced were discontinued.

Required:

Recommend which segments, if any, should be eliminated. Prepare a report in good form to support your answer.

112. The management of Thews Corporation is considering dropping product E28I. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $86,000 of the fixed manufacturing expenses and $67,000 of the fixed selling and administrative expenses are avoidable if product E28I is discontinued.

Required:

a. What is the net operating income earned by product E28I according to the company's accounting system? Show your work!

b. What would be the effect on the company's overall net operating income of dropping product E28I? Should the product be dropped? Show your work!

113. Tjelmeland Corporation is considering dropping product S85U. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $55,000 of the fixed manufacturing expenses and $71,000 of the fixed selling and administrative expenses are avoidable if product S85U is discontinued.

Required:

a. According to the company's accounting system, what is the net operating income earned by product S85U? Show your work!

b. What would be the effect on the company's overall net operating income of dropping product S85U? Should the product be dropped? Show your work!A06

114. The management of Drummer Corporation is considering dropping product

D84L. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $201,000 of the fixed manufacturing expenses and $156,000 of the fixed selling and administrative expenses are avoidable if product D84L is discontinued.

Required:

What would be the effect on the company's overall net operating income if product D84L were dropped? Should the product be dropped? Show your work!

115. Fouch Company makes 30,000 units per year of a part it uses in the products it manufactures. The unit product cost of this part is computed as follows:

An outside supplier has offered to sell the company all of these parts it needs for $51.90 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $219,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $6.20 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

Required:

a. How much of the unit product cost of $52.30 is relevant in the decision of whether to make or buy the part?

b. What is the net total dollar advantage (disadvantage) of purchasing the part rather than making it?

c. What is the maximum amount the company should be willing to pay an outside supplier per unit for the part if the supplier commits to supplying all 30,000 units required each year?

116. Janeiro Skate, Inc. currently manufactures the wheels that it uses for its in-line skates. The annual costs to manufacture the 150,000 wheels needed each year are as follows:

Kasba Rubber Company has offered to provide Janeiro with all of its annual wheel needs for $3.50 per wheel. If Janeiro accepts this offer, 75% of the fixed overhead above could be totally eliminated. Also, Janeiro would be able to rent out the freed up space and could generate $72,000 of income annually.

Required:

Based on this information, would Janeiro be better off to continue making the wheels or

117. Tingstrom Inc. makes a range of products. The company's predetermined overhead rate is $20 per direct labor-hour, which was calculated using the following budgeted data:

Component B6 is used in one of the company's products. The unit cost of the component according to the company's cost accounting system is determined as follows:

An outside supplier has offered to supply component B6 for $76 each. The outside supplier is known for quality and reliability. Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by this decision. Tingstrom chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

118. Rosiek Corporation uses part A55 in one of its products. The company's Accounting Department reports the following costs of producing the 4,000 units of the part that are needed every year.

An outside supplier has offered to make the part and sell it to the company for $32.30 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $4,000 of these allocated general overhead costs would be avoided. In addition, the space used to produce part A55 could be used to make more of one of the company's other products, generating an additional segment margin of $26,000 per year for that product.

Required:

a. Prepare a report that shows the effect on the company's total net operating income of buying part A55 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?

119. Part F77 is used in one of Wilcutt Corporation's products. The company's Accounting Department reports the following costs of producing the 7,000 units of the part that are needed every year.

An outside supplier has offered to make the part and sell it to the company for $28.30

each. If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company. If the outside supplier's offer were accepted, only $9,000 of these allocated general overhead costs would be avoided.

Required:

a. Prepare a report that shows the effect on the company's total net operating income of buying part F77 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?

120. Julison Company produces a single product. The cost of producing and selling a single unit of this product at the company's normal activity level of 60,000 units per month is as follows:

The normal selling price of the product is $79.80 per unit.

An order has been received from an overseas customer for 2,000 units to be delivered this month at a special discounted price. This order would have no effect on the company's normal sales and would not change the total amount of the company's fixed costs. The variable selling and administrative expense would be $0.30 less per unit on this order than on normal sales.

Direct labor is a variable cost in this company.

Required:

a. Suppose there is ample idle capacity to produce the units required by the overseas customer and the special discounted price on the special order is $71.60 per unit. By how much would this special order increase (decrease) the company's net operating income for the month?

b. Suppose the company is already operating at capacity when the special order is received from the overseas customer. What would be the opportunity cost of each unit delivered to the overseas customer?

c. Suppose there is not enough idle capacity to produce all of the units for the overseas customer and accepting the special order would require cutting back on production of 700 units for regular customers. What would be the minimum acceptable price per unit for the special order?

121. Zaccagnino Corporation makes a range of products. The company's predetermined overhead rate is $14 per direct labor-hour, which was calculated using the following budgeted data:

Management is considering a special order for 300 units of product D03C at $119 each. The normal selling price of product D03C is $157 and the unit product cost is determined as follows:

If the special order were accepted, normal sales of this and other products would not be affected. The company has ample excess capacity to produce the additional units. Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by the special order.

Required:

If the special order were accepted, what would be the impact on the company's overall profit?

122. Biello Co. manufactures and sells medals for winners of athletic and other events. Its manufacturing plant has the capacity to produce 15,000 medals each month; current monthly production is 14,250 medals. The company normally charges $115 per medal. Cost data for the current level of production are shown below:

The company has just received a special one-time order for 600 medals at $102 each. For this particular order, no variable selling and administrative costs would be

incurred. This order would also have no effect on fixed costs.

Required:

Should the company accept this special order? Why?

123. Manning Co. manufactures and sells trophies for winners of athletic and other events. Its manufacturing plant has the capacity to produce 18,000 trophies each month; current monthly production is 15,300 trophies. The company normally charges $141 per trophy. Cost data for the current level of production are shown below:

The company has just received a special one-time order for 900 trophies at $73 each. For this particular order, no variable selling and administrative costs would be incurred. This order would also have no effect on fixed costs.

Required:

Should the company accept this special order? Why?

124. Ries Corporation has received a request for a special order of 8,000 units of product R34 for $34.20 each. The normal selling price of this product is $35.70 each, but the units would need to be modified slightly for the customer. The normal unit product cost of product R34 is computed as follows:

Direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like some modifications made to product R34 that would increase the variable costs by $6.30 per unit and that would require a one-time investment of $40,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample spare capacity for producing the special order.

Required:

Determine the effect on the company's total net operating income of accepting the special order. Show your work!

125. A customer has asked Clougherty Corporation to supply 4,000 units of product M97, with some modifications, for $40.10 each. The normal selling price of this product is $48.00 each. The normal unit product cost of product M97 is computed as follows:

Direct labor is a variable cost. The special order would have no effect on the company's total fixed manufacturing overhead costs. The customer would like some modifications made to product M97 that would increase the variable costs by $5.70 per unit and that would require a one-time investment of $31,000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales. The company has ample spare capacity for producing the special order.

Required:

Determine the effect on the company's total net operating income of accepting the special order. Show your work!

126. Gloster Company makes three products in a single facility. These products have the following unit product costs:

The mixing machines are potentially the constraint in the production facility. A total of 27,400 minutes are available per month on these machines.

Direct labor is a variable cost in this company.

Required:

a. How many minutes of mixing machine time would be required to satisfy demand for all three products?

b. How much of each product should be produced to maximize net operating income? (Round off to the nearest whole unit.)

c. Up to how much should the company be willing to pay for one additional hour of mixing machine time if the company has made the best use of the existing mixing

machine capacity? (Round off to the nearest whole cent.)

Essay Questions

109. Rackett Corporation is considering two alternatives that are code-named M and N. Costs associated with the alternatives are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two alternatives?

b. What is the differential cost between the two alternatives?

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 1

Level: Easy

110. Costs associated with two alternatives, code-named Q and R, being considered by Lang Corporation are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two alternatives?

b. What is the differential cost between the two alternatives?

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 1

Level: Easy

111. When Mr. Ding L. Berry, president and chief executive of Berry, Inc., first saw the segmented income statement below, he flew into his usual rage: "When will we ever start showing a real profit? I'm starting immediate steps to eliminate those two unprofitable lines!"

*These traceable expenses could be eliminated if the product lines to which they are traced were discontinued.

Required:

Recommend which segments, if any, should be eliminated. Prepare a report in good form to support your answer.

A segmented income report, without the allocation of common fixed expenses, will provide the basis for deciding which segments to drop.

The only segment that possibly should be eliminated is segment W, which shows a negative segment margin of $2,000.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 2

Level: Medium

112. The management of Thews Corporation is considering dropping product E28I. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $86,000 of the fixed manufacturing expenses and $67,000 of the fixed selling and administrative expenses are avoidable if product E28I is discontinued.

Required:

a. What is the net operating income earned by product E28I according to the company's accounting system? Show your work!

b. What would be the effect on the company's overall net operating income of dropping product E28I? Should the product be dropped? Show your work!

a. According to the company's accounting system, the product's net operating loss is $10,000.

b. Net operating income would decline by $125,000 if product E28I were dropped. Therefore, the product should not be dropped.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 2

Level: Easy

113. Tjelmeland Corporation is considering dropping product S85U. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $55,000 of the fixed manufacturing expenses and $71,000 of the fixed selling and administrative expenses are avoidable if product S85U is discontinued.

Required:

a. According to the company's accounting system, what is the net operating income earned by product S85U? Show your work!

b. What would be the effect on the company's overall net operating income of dropping product S85U? Should the product be dropped? Show your work!

a. According to the company's accounting system, the product's net operating loss is $11,000.

b. Net operating income would decline by $76,000 if product S85U were dropped. Therefore, the product should not be dropped.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 2

Level: Easy

114. The management of Drummer Corporation is considering dropping product

D84L. Data from the company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further investigation has revealed that $201,000 of the fixed manufacturing expenses and $156,000 of the fixed selling and administrative expenses are avoidable if product D84L is discontinued.

Required:

What would be the effect on the company's overall net operating income if product D84L were dropped? Should the product be dropped? Show your work!

Net operating income would decline by $3,000 if product D84L were dropped. Therefore, the product should not be dropped.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 2

Level: Easy

115. Fouch Company makes 30,000 units per year of a part it uses in the products it manufactures. The unit product cost of this part is computed as follows:

An outside supplier has offered to sell the company all of these parts it needs for $51.90 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $219,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $6.20 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

Required:

a. How much of the unit product cost of $52.30 is relevant in the decision of whether to make or buy the part?

b. What is the net total dollar advantage (disadvantage) of purchasing the part rather than making it?

c. What is the maximum amount the company should be willing to pay an outside supplier per unit for the part if the supplier commits to supplying all 30,000 units required each year?

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 3

Level: Hard

116. Janeiro Skate, Inc. currently manufactures the wheels that it uses for its in-line skates. The annual costs to manufacture the 150,000 wheels needed each year are as

follows:

Kasba Rubber Company has offered to provide Janeiro with all of its annual wheel

needs for $3.50 per wheel. If Janeiro accepts this offer, 75% of the fixed overhead

above could be totally eliminated. Also, Janeiro would be able to rent out the freed up

space and could generate $72,000 of income annually.

Required:

Based on this information, would Janeiro be better off to continue making the wheels or to buy them from Kasba? SHOW YOUR COMPUTATIONS.

It would be better by $42,000 to buy.

($165,000 + $45,000 + $60,000 + $225,000 + $72,000) >

($3.50 x 150,000)

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 3

Level: Hard

117. Tingstrom Inc. makes a range of products. The company's predetermined overhead rate is $20 per direct labor-hour, which was calculated using the following budgeted data:

Component B6 is used in one of the company's products. The unit cost of the component according to the company's cost accounting system is determined as follows:

An outside supplier has offered to supply component B6 for $76 each. The outside supplier is known for quality and reliability. Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by this decision. Tingstrom chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

Direct materials, direct labor, and variable manufacturing overhead are relevant in this decision. Fixed manufacturing overhead is not relevant since it would not be affected by the decision. The variable portion of the manufacturing overhead rate is computed as follows:

Since the outside supplier has offered to sell the component for $76.00 each, but it only costs the company $57.60 to make the component internally, this is not a financially attractive offer.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement

Learning Objective: 3

Level: Hard

Source: CIMA, adapted

118. Rosiek Corporation uses part A55 in one of its products. The company's Accounting Department reports the following costs of producing the 4,000 units of

the part that are needed every year.

CPA《审计》知识点 (2)

2015年注册会计师考试《审计》知识点(2) 第二章审计计划 初步业务活动: 初步业务活动就是编制审计计划前所需要完成的工作。 一、初步业务活动的目的 1.具备执行业务所需要的独立性和专业胜任能力; 2.不存在因管理层诚信问题而影响注册会计师保持该项业务意愿的情况; 3.与被审计单位不存在对业务约定条款的误解。 二、初步业务活动的内容 1.针对保持客户关系和具体审计业务实施相应的质量控制程序; 2.评价遵守职业道德规范的情况; 3.就审计业务约定条款达成一致意见。 虽然保持客户关系及具体审计业务和评价职业道德的工作贯穿审计业务的全过程,但是这两项活动需要安排在其他审计工作之前,以确保注册会计师已具备执行业务所需要的独立性和专业胜任能力,且不存在因管理层诚信问题而影响注册会计师保持该项业务意愿等情况。 在作出接受或保持客户关系及具体审计业务的决策后,在审计业务开始前,注册会计师与被审计单位就审计业务约定条款达成一致意见,签订或修改审计业务约定书。重要性: 一、重要性的含义 重要性概念可从下列方面进行理解: (1)如果合理预期错报(包括漏报)单独或汇总起来可能影响财务报表使用者依据财务报表作出的经济 决策,则通常认为错报是重大的; (2)对重要性的判断是根据具体环境作出的,并受错报的金额或性质的影响,或受两者共同作用的影响; (3)判断某事项对财务报表使用者是否重大,是在考虑财务报表使用者整体共同的财务信息需求的基础上作出的。

第一,不考虑错报对个别财务报表使用者可能产生的影响; 第二,重要性确定包括财务报表层次的重要性和特定交易类别、账户余额和披露的重要性水平; 第三,在计划审计工作和形成审计结论阶段都要运用重要性水平; 第四,重要性水平与审计证据成反向关系; 第五,注册会计师应当制定一个比重要性水平更低的金额(实际执行的重要性),以便评估风险和设计进一步审计程序。注册会计师使用整体重要性水平(将财务报表作为整体)的目的有:(1)决定风险评估程序的性质、时间安排和范围;(2)识别和评估重大错报风险;(3)确定进一步审计程序的性质、时间安排和范围。在形成审计结论阶段,要使用整体重要性水平和为了特定交易类别、账户余额和披露而制定的较低金额的重要性水平来评价已识别的错报对财务报表的影响和对审计报告中审计意见的影响。 二、重要性水平的确定 确定的时间:在计划审计工作时 确定时需要考虑的因素:对被审计单位及其环境的了解;审计的目标,包括特定报告要求;财务报表各项目的性质及其相互关系;财务报表项目的金额及其波动幅度。 1.财务报表整体的重要性 注册会计师通常先选择一个恰当的基准,再选用适当的百分比乘以该基准,从而得出财务报表整体的重要性。 注意: 第一,在选择基准时应考虑的因素:财务报表要素;财务报表使用者特别关注的项目;被审计单位的性质、所处的生命周期阶段、所处行业和经济环境;被审计单位所有权结构和融资方式;基准的相对波动性。 第二,注册会计师在确定重要性水平时,不需考虑与具体项目计量相关的固有不确定性。 2.特定类别交易、账户余额或披露的重要性水平 (三)实际执行的重要性 通常而言,实际执行的重要性通常为财务报表整体重要性的50%-75%。 注意: 实际执行的重要性为整体重要性50%的情况:(1)非连续审计;(2)以前年度审计调整较多;(3)项目总体

注册会计师审计综合实训五应收帐款实质性测试底稿课件

【最新资料,Word版,可自由编辑!】 计划实施的实质性程序 被审计单位:安琪儿食品有限责任公司索引号:ZD1 项目:应收账款报表截止日: 编制人:罗紫云复核人: 编制日期:复核日期: 一、审计目标: 1.存在:资产负债表中记录的应收账款是存在的. 2.完整性:所有应当记录的应收账款均已记录. 3.权利和义务:记录的应收账款由审计单位拥有或控制. 4.计价和分摊:应收账款以恰当的金额包括在财务报表中,与之相关的计价调整已恰当记录. 5.列报:应收账款以恰当的金额包括在财务报表中,与之相关的计价调整已恰当记录. 注;1.结果取自风险评估工作底稿. 2.结果取自该项目所属业务循环内部控制测试工作底稿. 3.计划实施的实质性程序与财务报表认定之间的对应关系用"√"表示.

应收账款审定表 被审计单位:安琪儿食品有限责任公司项目:应收账款索引号:ZD2 报表截止日:2010年12月31日 编制人:罗紫云复核人:编制日期:复核日期:

应收账款明细表 被审计单位:安琪儿食品有限责任公司索引号:ZD3 项目:应收账款 编制人:罗紫云复核人: 编制日期:复核日期:

编制说明:外币应收账款应列明原币金额及折合汇率. 审计说明: 1、经查明,应收账款明细账中浙江省宁波市柏胜商厦存在虚构应收账款、串户等情况,对其进行查明并进行调整后确认其应收账款为-1986170元,相应调整分录见表ZD4-1; 2、经查明,应收账款明细账中南京市永嘉商场存在串户情况,对其进行查明并进行调整后确认其应收账款为400478元,相应调整分录见表 ZD4-2; 3、经查明,应收账款明细账中上海市佳加汇商场存在串户情况,对其进行查明并进行调整后确认其应收账款为1979055元,相应调整分录见表ZD4-3; 4、经查明,应收账款明细账中江苏省芜湖市百华商场存在串户情况,对其进行查明并进行调整后确认其应收账款为266292元,相应调整分录见表ZD4-4; 5、经查明,应收账款明细账中的其他账户,发生在2012年12月31日的调整应收应账款余额事项没有附相应的原始凭证,该笔业务的实质是被审计单位在收到江苏省扬州百货前欠货款451620元时,在填写分录记账时间记为436320元,被审计单位为了调平银行对账单和银行存款日记账之间的差额,故做应收账款—其他该笔分录,该分录为错误分录,建议对其进行相应的调整;调整分录为: ①借:银行存款 15300 贷:应收账款—其他 15300 ②借:银行存款 15300 贷:应收账款—江苏省扬州市百货大楼 15300

2019秋东财《审计实务》在线作业一-3(100分)

2019秋东财《审计实务》在线作业一-3(100分) 【奥鹏】-[东北财经大学]东财《审计实务》在线作业一 试卷总分:100 得分:100 第1题,对确实属于预付账款的应付账款明细账户借方余额,应作调整分录为()。 A、借记预付账款,贷记应付账款 B、借记应收账款,贷记应付账款 C、借记应付账款,贷记应收账款 D、借记应付账款,贷记预付账款 正确答案: 第2题,对存货进行监督性盘点是()。 A、会计师事务所的质量控制程序 B、被审计单位管理层的责任 C、被审计单位的内部控制制度 D、注册会计师的责任 正确答案: 第3题,下列关于银行存款函证对象的说法中,表达最准确的是()。 A、向本年度的所有开户银行函证 B、向存款账户已经结清的开户银行函证

C、向存款账户尚未结清的开户银行函证 D、向有其他货币资金存款的开户银行函证 正确答案: 第4题,固定资产的账簿体系不包括()。 A、固定资产总账 B、固定资产日记账 C、固定资产明细账 D、固定资产卡片 正确答案: 第5题,注册会计师监盘库存现金时,被审计单位必须参加的人员是()。 A、财务总监和内部审计人员 B、出纳员和总会计师 C、出纳员和会计主管 D、出纳员和应收账款记账员 正确答案: 第6题,如果需要坐支现金,应当()。

A、经财务经理审批 B、经开户银行审批 C、经董事长审批 D、经企业管理层的集体审批 正确答案: 第7题,如果会计估计的结果与财务报表中原来已确认或披露的金额存在差异,则()。 A、并不必然表明财务报表存在错报 B、必然表明财务报表存在错报 C、必须要求被审计单位调整 D、必然表明会计估计是不恰当的 正确答案: 第8题,判断报表数据之间是否存在异常关系或偏离预期的关系,最有效的审计程序是()。 A、询问 B、检查实物资产 C、函证 D、分析程序 正确答案:

CPA审计精华知识点汇总

审计要素:财务报表编制基础(标准) 标准的特征:相关性、完整性、可靠性、中立性、可理解性。 知识点:审计目标 (一)与所审计期间各类交易和事项相关的认定和具体审计目标 准确性与发生、完整性之间存在区别。 例如,若已记录的销售交易是不应当记录的(如发出的商品是寄销商品),则即使发票金额是准确计算的,仍违反了发生目标。 再如,若已入账的销售交易是对正确发出商品的记录,但金额计算错误,则违反了准确性目标,但没有违反发生目标。在完整性与准确性之间也存在同样的关系。 (二)与期末账户余额相关的认定和具体审计目标

(三)与列报和披露相关的认定 知识点:审计风险 (一)重大错报风险 1.两个层次的重大错报风险 财务报表层次重大错报风险与财务报表整体存在广泛联系,可能影响多项认定。此类风险通常与控制环境有关。 注册会计师同时考虑各类交易、账户余额和披露认定层次的重大错报风险,考虑的结果直接有助于注册会计师确定认定层次上实施的进一步审计程序的性质、时间安排和围。 2.固有风险和控制风险 认定层次的重大错报风险又可以进一步细分为固有风险和控制风险。 (二)检查风险 检查风险取决于审计程序设计的合理性和执行的有效性。检查风险不可能降低为零。 1.固有风险是指在考虑相关的部控制之前,某类交易、账户余额或披露的某一认定易发生错报(该错报单独或连同其他错报可能是重大的)的可能性。 2.控制风险是指某类交易、账户余额或披露的某一认定发生错报,该错报单独或连同其他错报是重大的,但没有被部控制及时防止或发现并纠正的可能性。 3.检查风险是指如果存在某一错报,该错报单独或连同其他错报可能是重大的,注册会计师为将审计风险降至可接受的 一、审计计划的容 审计计划包括总体审计策略和具体审计计划。 (一)总体审计策略 1.概念:总体审计策略用以确定审计围、时间安排和方向,并指导制定具体审计计划的制定。

注会审计·作业答案·第二章

第二章注册会计师管理制度 一、单项选择题 1.申请人申请注册会计师的,必须满足从事()工作两年以上。 A.审阅业务 B.税务代理业务 C.审计业务 D.代理记账业务 2.申请人申请注册会计师,以下说法中正确的是()。 A.申请人必须取得注册会计师证书,并从事税务服务工作两年以上 B.申请人可以向省财政厅申请注册,并报经中国注册会计师协会备案 C.申请人必须具备完全民事行为能力 D.申请人必须具有本科学历 3.验证企业资本,出具验资报告,是()业务。 A.审计 B.审阅 C.其他鉴证业务 D.相关服务 4.下列选项中,不属于注册会计师的其他审计业务的是()。 A.对财务信息执行商定程序 B.按照特殊目的编制基础编制的财务报表审计 C.单一财务报表或财务报表特定要素审计 D.简要财务报表审计 5.当今世界中,成为注册会计师职业界组织形式发展的一大趋势的是()。 A.独资会计师事务所 B.普通合伙会计师事务所 C.有限责任会计师事务所 D.有限责任合伙会计师事务所 6.设立合伙会计师事务所的条件是()。 A.合伙人共同制定的章程 B.有会计师事务所的名称 C.有不少于人民币30万元的注册资本 D.有5名以上的专职从业人员 二、多项选择题 1.申请人申请注册会计师的,不予注册的情形有()。 A.不具有完全民事行为能力 B.因为抢劫,被判以刑事处罚 C.因在学校上学时打伤同学,被判以行政拘留 D.自行停止执行注册会计师业务满半年的 2.常见的其他鉴证业务有()。 A.审阅业务 B.简要财务报表审计 C.预测性财务信息审核 D.系统鉴证 3.常见的相关服务业务有()。 A.对财务信息执行商定程序 B.税务筹划 C.验资 D.会计咨询

注册会计师审计实务入门第二章 谈谈我对考注册会计师的几点看法

注册会计师审计实务入门 上部 第二章谈谈我对考注会的几点看法及学习心得注册会计师证书,现在可谓是炙手可热。报名考注会的人越来越多,为什么这么多人要考注会?主要是以下几个原因: 1、刚毕业的学生当中,有的人觉得自己上的不是重点大学或名牌大学,为了增强自己的就业实力,而考注会。这些学生里面有的人是会计专业,有的人是非会计专业。 2、大部分考注会的人还是在职人员,从年龄上来说,这部分人的年龄主要集中在23至45岁之间,当然比这年龄更大的人也不在少数。这些人当中有的是正在从事会计工作,有一部分人从事的是非会计工作,但基本上都是由于对目前工作不满意,想通过考注会来改变未来的职业生涯。 还有一部分人认为注会的工资很高,觉得考下注会,能拿到比现在高的多的工资。其实,注册会计师之所以这么火,这里面有实火,更有虚火。虚火是部分培训学校夸大宣传,使人们对注册会计师产生了错误的认识。 不论是由于哪种原因,对于正在打算考注会的朋友,我提这么几个建议,也许能对你有非常大的帮助。 1、关于注会考试科目顺序的建议 如果你对目前工作不满意,想急于通过考注会,去会计师事务所

做审计的话,我建议先考会计和审计,为什么是这两门呢?我们都知道,注会专业阶段考6门,每门的有效期是5年,如果你从最简单的开始考,如果在5年内考不完,那么从第6年开始,第一年及格的科目就作废了。在现实中,我也碰到过不少这样的朋友。 另外,把会计和审计这两门通过后,就可以给会计师事务所投递简历了,如果在这时能够找到一家还不错的会计师事务所的话,边工作边学习,等注会全部及格了,也有一定的审计工作经验了。 这个建议尤其适用年龄稍微大一点的朋友。因为,你如果等所有的科目都通过之后再去会计师事务所的话,此时年龄可能偏大了,在加上没有审计经验,对自己会非常不利。 2、关于年龄方面的建议 经常有朋友问,我年龄较大了,现在考注会还来得及吗?我只能这样回答你,有注会证书总比没有强,如果想改变自己目前的窘境,就下定决心吧,不要犹豫了。 3、关于学习方法方面的建议 学习注会一定要讲究方法,我建议看一章辅导教材,就做一章练习题,对于近4年的全国统一考试试题,一定要做3遍以上,对于你第一次就做错的题目,一定要做3遍以上,一定把这些题目搞懂了。一定要把重要章节的辅导教材内容和习题彻底搞懂了。 不吃苦,想考过注会,是根本不可能的。如果你根本吃不了苦,我建议你还是别浪费时间了。

注会审计2018真题答案

审计 一、单项选择题 本题型共25小题,每小题1分,共25分。每小题只有一个正确答案,请从每小题的备选答案中选出一个你认为正确的答案,用鼠标点击相应的选项。 1.下列各项中,注册会计师在确定某项重大错报风险是否为特别风险时,通常无需考虑的是( )。 A.交易的复杂程度 B.风险是否涉与重大的关联方交易 C.被审计单位财务人员的胜任能力 D.财务信息计量的主观程度 【答案】C 【知识点】确定特别风险时考虑的事项 【解析】被审计单位财务人员的胜任能力在确定一项重大错报风险是否为特别风险时,通常无须考虑,选项C 错误。 2.下列各项中,不属于财务报表审计的前提条件的是( )。 A.管理层设计、执行和维护必要的内部控制,以使财务报表不存在由于舞弊或错误导致的重大错报 B.管理层按照适用的财务报表编制基础编制财务报表,并使其实现公允反映

C.管理层承诺将更正注册会计师在审计过程中识别出的重大错报 D.管理层向注册会计师提供必要的工作条件 【答案】C 【知识点】审计的前提条件 【解析】审计工作的前提条件包括:(1)按照适用的财务报告编制基础编制财务报表,并使其实现公允反映(如适用)。(2)设计、执行和维护必要的内部控制,以使财务报表不存在由于舞弊或错误导致的重大错报。(3)向注册会计师提供必要的工作条件,包括允许注册会计师接触与编制财务报表相关的所有信息(如记录、文件和其他事项),向注册会计师提供审计所需要的其他信息,允许注册会计师在获取审计证据时不受限制地接触其认为必要的内部人员和其他相关人员。 3.下列各项中,通常不属于审计报告预期使用者的是( )。 A.被审计单位的股东 B.被审计单位的管理层 C.对被审计单位财务报表执行审计的注册会计师 D.向被审计单位提供贷款的银行 【答案】C 【知识点】预期使用者

CPA审计知识点归纳

第一编审计基本原理 接受业务委托→计划审计工作→评估重大错报风险→应对重大错报风险→编制审计报告。 第一章审计概述5 【掌握】审计的定义和保证程度(相关服务不保证) 审计是指注册会计师对财务报表是否不存在由于舞弊或错误导致的重大错报提供合理保证,以积极方式提出意见,增强除管理层之外的预期使用者对财务报表信赖的程度。 合理保证业务是综合运用各种方法,将审计业务风险降至该业务环境下可接受的低水平,以此作为以积极方式提出结论的基础。 有限保证业务是注册会计师主要运用询问、分析程序等方法将审阅业务风险降至该业务环境下可接受的水平,以此作为以消极方式提出结论的基础。 一、审计业务的三方关系2014 注册会计师对由被审计单位管理层(责任方)负责的财务报表(鉴证对象信息)发表审计意见(提出结论),以增强除管理层之外的预期使用者对财务报表的信任程度。 如不存在除责任方之外的其他预期使用者,那么该业务不构成鉴证业务。 二、鉴证对象:历史的财务状况、经营成果和现金流量,鉴证对象信息:财务报表 三、财务报表编制基础(标准):相关性、完整性、可靠性、中立性、可理解性。 通用目的编制基础,主要是指会计准则和会计制度。特殊目的编制基础,是指旨在满足财务报表特定使用者对财务信息需求的财务报告编制基础,包括计税核算基础、监管机构的报告要求和合同的约定等。分为公允列报编制基础和遵循性编制基础。 四、审计证据。信息缺乏也构成证据。 五、审计报告 【掌握】审计目标 总目标:1 不存在重大错报;2出具报告并沟通。 一、遵守审计准则、职业道德守则 二、保持职业怀疑 一种态度,采取质疑的思维方式,对可能导致错报的迹象保持警觉,进行审慎评价证据。 相互矛盾的证据;对文件记录和询问的答复的可靠性产生怀疑的信息;可能存在舞弊的情况;需要实施除审计准则规定外的其他审计程序的情形; 三、合理运用职业判断 (1)确定重要性和评估审计风险;(2)确定所需实施的审计程序的性质、时间安排和围;(3)评价审计证据的充分性和适当性;(4)评价管理层在应用适用的财务报告编制基础时作出的判断; (5)根据已获取的审计证据得出结论。 【掌握】审计风险 一、重大错报风险 财务报表层次重大错报风险与财务报表整体存在广泛联系,通常与控制环境有关。 交易、账户余额和披露认定层次的重大错报风险,进一步分为:

会计师事务所实习报告(完整版)

报告编号:YT-FS-6467-23 会计师事务所实习报告 (完整版) After Completing The T ask According To The Original Plan, A Report Will Be Formed T o Reflect The Basic Situation Encountered, Reveal The Existing Problems And Put Forward Future Ideas. 互惠互利共同繁荣 Mutual Benefit And Common Prosperity

会计师事务所实习报告(完整版) 备注:该报告书文本主要按照原定计划完成任务后形成报告,并反映遇到的基本情况、实际取得的成功和过程中取得的经验教训、揭露存在的问题以及提出今后设想。文档可根据实际情况进行修改和使用。 xx年3月10日我进入了会计师事务所,开始了 我的实习生活。这是一家小会计师事务所,包括所长 在内有5名注册会计师,每个注册会计师都是事务所 的股东。事务所的业务主要为年报审计、法人离任经 济责任审计、改制审计、破产审计、代理记账、资产 评估等业务。 我一直跟着事务所的高老师做事情。我很佩服她, 佩服她之前考注册会计师时的聪明与坚持,佩服她的 处事能力,也佩服她那超强的专业胜任能力。高老师 在成为一名执业的注册会计师之前,一点会计审计方 面的专业知识都没有。她完全凭自己的努力,在5年 内通过了注册会计师的考试。这一点给了我很大的鼓 舞,让我以更加饱满的热情投入到今年的注册会计师

的考试中。在实习的那段时间,高老师一直都很照顾我。她告诉我,这家会计师事务所一般都是不接收实习生的,因为实习生的问题很多,会影响她们工作的效率。虽然这样说,但是每次我问她问题,她都不厌其烦地耐心讲解。因为是第一次接触到审计这个东西,也因为是实施了审计程序就要直接形成工作底稿,所以我都不敢贸然下定论,每次我都要先去问问高老师,征求一下她的意见。每次问她,她都会停下她手中的工作,仔细地跟我一起分析。 为了能够在实习过程中学到东西,就得先要有扎实的专业知识。在去参加实习之前,我花了差不多半个月的时间学习审计的cpa教材,巩固了审计的一些基本知识。比如一些基本的审计程序呀,还有就是各个业务循环的一些知识,还有关于风险导向审计,关于一些重点会计科目的审计要点。之前的关于理论知识的学习,对我后来的实习奠定了坚实的基础。在实习那段期间,我参与了三个项目,一个年报审计,一个破产审计,一个改制审计。从第一天进会计师事

2019秋东财《审计实务》在线作业三-1(100分)

2019秋东财《审计实务》在线作业三-1(100分) 【奥鹏】-[东北财经大学]东财《审计实务》在线作业三 试卷总分:100 得分:100 第1题,需要作出会计估计的交易、事项或情况得以解决时发生的实际货币金额称为()。 A、会计估计的结果 B、管理层的点估计 C、会计估计的不确定性 D、注册会计师的点估计或区间估计 正确答案: 第2题,对确实属于预付账款的应付账款明细账户借方余额,应作调整分录为()。 A、借记预付账款,贷记应付账款 B、借记应收账款,贷记应付账款 C、借记应付账款,贷记应收账款 D、借记应付账款,贷记预付账款 正确答案: 第3题,为测试所记录的成本是否均已发生而非虚构,注册会计师应()。 A、对重大在产品项目进行计价测试 B、抽取料工费的原始记录,与成本明细账进行核对

C、检查各项费用的归集和分配以及成本的计算是否正确 D、从成本明细账中选取项目,与料工费记录核对 正确答案: 第4题,判断报表数据之间是否存在异常关系或偏离预期的关系,最有效的审计程序是()。 A、询问 B、检查实物资产 C、函证 D、分析程序 正确答案: 第5题,如果会计估计的结果与财务报表中原来已确认或披露的金额存在差异,则()。 A、并不必然表明财务报表存在错报 B、必然表明财务报表存在错报 C、必须要求被审计单位调整 D、必然表明会计估计是不恰当的 正确答案:

第6题,如果发货则销售实现,那么证明销售发生最重要的原始凭证是()。 A、销售单 B、发运单 C、销售发票 D、验收单 正确答案: 第7题,在财务报表审阅业务中,注册会计师()。 A、应当询问在资产负债表日后发生的、可能需要在财务报表中调整或披露的期后事项 B、不需要询问在资产负债表日后发生的、可能需要在财务报表中调整或披露的期后事项 C、应当询问在审阅报告日后发生的、可能需要在财务报表中调整或披露的事项 D、有责任实施程序以识别审阅报告日后发生的事项 正确答案: 第8题,固定资产的账簿体系不包括()。 A、固定资产总账 B、固定资产日记账 C、固定资产明细账 D、固定资产卡片

2021年注册会计师考试知识点:《审计》第四章(3)

2021年注册会计师考试知识点:《审计》第 四章(3) (2021最新版) 作者:______ 编写日期:2021年__月__日 审计抽样在控制测试中的运用: 一、使用统计抽样(控制测试) 1.注册会计师可以使用样本量表确定样本规模(查表法)。掌握教材P153查表确定样本规模的例题。 2.评价样本结果。分别掌握教材P155和P156的总体偏差率高于

或低于偏差率情况的举例,注意形成的结论不同,结合【考点五】分析。记住公式: 二、使用非统计抽样(控制测试) 了解教材P77“表4-7人工控制最低样本规模表”确定所需的样本规模的方法,掌握: 假设被审计单位2010年发生了500笔采购交易,注册会计师初步评估该控制运行有效,那么所需的样本数量至少是25.如果25个样本中没有发现偏差,那么控制测试的样本结果支持计划的控制运行有效性和重大错报风险的评估水平。如果25个样本中发现了1个偏差,注册会计师有两种处理办法:其一,认为控制没有有效运行,控制测试样本结果不支持计划的控制运行有效性和重大错报风险的评估水平,因而提高重大错报风险评估水平,增加对相关账户的实质性程序;其二,再测试25个样本,如果其中没有再发现偏差,也可以得出样本结果支持控制运行有效性和重大错报风险的初步评估结果,反之则证明控制无效。 三、样本结果评价,形成审计结论(考虑抽样风险)

偏差率上限估计值=总体偏差率+抽样风险允许限度 统计抽样总体偏差率上限“大于或等于”可容忍偏差率总体“不能接受”,应当增加控制测试的范围,或修正重大错报风险评估水平,并增加实质性程序的数量;或对其他控制进行测试,以支持计划的重大错报风险评估水平。总体偏差率上限“低于”可容忍偏差率总体“可以接受”总体偏差率上限“低于但接近”可容忍偏差率“考虑是否接受”总体,并考虑是否需要扩大测试范围非统计抽样样本偏差率“大于”可容忍偏差率总体“不能接受”样本偏差率“大大低于”可容忍偏差率总体“可以接受”样本偏差率“低于但接近”可容忍偏差率总体“不可接受”样本偏差率“低于”可容忍偏差率,其差额“不大不小”“考虑是否接受”总体,考虑扩大样本规模以进一步收集证据

2020注会(CPA) 审计 第一编 审计基本原理——第二章 审计计划

考情分析: 本章属于比较重要的内容,通过学习,考生应能够明确计划审计工作的主要内容。在考试中可涉及各种题型,客观题命题几率较高,特别是涉及重要性,几乎每年必考,此外,还可以考查简答题或在综合题中涉及审计计划。 具体要求如下: 1.了解初步业务活动 2.了解审计业务约定书的内容 3.理解总体审计策略和具体审计计划 4.掌握审计重要性的含义及其运用 【知识点】初步业务活动 一、初步业务活动的目的和内容★ (一)初步业务活动的目的——核心目的是确定是否接受业务委托。 ●具备执行业务所需的独立性和能力 ●不存在因管理层诚信问题而可能影响注册会计师保持该项业务的意愿的事项 ●与被审计单位之间不存在对业务约定条款的误解 (二)初步业务活动的内容 初步业务活动包括:针对保持客户关系和具体审计业务实施相应的质量控制程序;评价遵守相关职业道德要求的情况;就审计业务约定条款达成一致意见。 补充: 初步业务活动工作底稿——业务承接评价表。 业务承接评价表 1.客户法定名称(中/英文): 2.客户地址: 3.客户性质(国有/外商投资/民营/其他): 4.客户所属行业、业务性质与主要业务: 5.最初接触途径(详细说明) (1)本所职工引荐______________________ (2)外部人员引荐______________________ (3)其他(详细说明)__________________ 6.客户要求我们提供审计服务的目的以及出具审计报告的日期: 7.治理层及管理层关键人员(姓名与职位): 8.主要财务人员(姓名与职位): 9.直接控股母公司、间接控股母公司、最终控股母公司的名称、地址、相互关系、主营业务及持股比例:

注册会计师考试审计科目要点

2007年注册会计师考试审计科目要点 注册会计师作为向社会提供审计、咨询等专业服务的执业人员,必须具备与其所操作业务相匹配的知识与技能。而注册会计师全国统一考试的目的,就是要考察考生是否具备这种执业知识和技能。特别是审计这一科目,它是注册会计师在执业中经常使用的本领,比如说出具财产损失报告、出具税收筹划报告等,都少不了要对企业账务进行审计。 去年CPA考试,审计科目合格率仅为13% XXXX年,参加审计科目考试的考生,全国共有9395名,及格率达13.22%。总的来说,XXXX年审计科目的考试题型相对稳定,共分五种,即单项选择题、多项选择题、判断题、简答题、综合题。其中单项选择题、多项选择题、判断题为客观题,简答题、综合题为主观题。XXXX年审计科目客观题分值比重下降,占卷面分值的35%,主观题分值比重上升,6道主观题占卷面分值的65%。 分析XXXX年审计科目的命题特点,发现试题着重突出实务性,审计实务章节题量占总题量的80%。其中财务报表审计实务,主要是测试考生如何运用审计理论,分析处理被审计单位出现的会计实务问题,考核考生分析判断能力,以及将审计理论与实务融会贯通的把握程度。 今年审计科目考试注意新执业准则 考生今年参加CPA审计科目考试应注意如下要点。

1.熟知科目命题原则。 审计科目以“全面考核、重点突出、理论与实务相结合”为基本命题原则。所谓“全面考核”是要求考生通读并熟悉教材每章节的内容。“重点突出”则是在全面复习的基础上,抓重点、抓重点章节里分值占比重大的部分。“理论与实务相结合”是把注册会计师的基本审计理论与审计实务相结合,做到学以治用,这是历年该科目的主要命题思路。 2.掌握注册会计师新执业准则。 XXXX年2月,财政部发布了48项注册会计师执业准则,标志着适应我国市场经济发展要求、与国际惯例趋同的注册会计师执业准则体系正式建立。执业准则的具体内容,是注册会计师进行财务报表审计的理论依据。考生要结合教材涉及的准则内容融会贯通,加深对准则的理解和记忆。根据以往的经验,例年考题的重点都考核考生对最新内容的掌握程度,今年这部分考试内容,也是审计科目的新难点和重点。同时,执业准则中对新审计风险导向理念的理解,考生也要深刻把握。 3.注重财务报表审计的操作实务。 审计科目的测试,强调站在注册会计师的角度,依据执业准则对被审计单位年度财务报表进行审计。因此,在考试中客观题和主观题部分,将涉及大量企业销售与收款循环、购货与付款循环、生产循环、筹资与投资循环、特殊项目等会计实务的审计问题。其命题思路是:综合考核考生将审计理论运用于审计实务中

2021注册会计师考试《审计》知识点第七章(3)

2021注册会计师考试《审计》知识点第七章 (3) (2021最新版) 作者:______ 编写日期:2021年__月__日 控制环境: 在审计业务承接阶段,注册会计师就需要对控制环境作出初步了解和评价。 财务报表层次的重大错报风险很可能源于薄弱的控制环境。控制环境本身并不能防止或发现并纠正各类交易、账户余额和披露认定层次的重大错报。控制环境与报表层次重大错报风险相关。

在评价控制环境的设计时,注册会计师应当考虑构成控制环境的下列因素: (1)对诚信和道德价值观念的沟通与落实; (2)对胜任能力的重视; (3)治理层的参与程度; (4)管理层的理念和经营风格; (5)组织结构及职权与责任的分配; (6)人力资源政策与实务。 整体层面控制与业务流程层面控制: 1.整体层面控制:控制环境、风险评估、监督、信息技术一般控制等。(与“报表”层次的重大错报风险相关) 整体层面内控要素控制环境、风险评估、监督、信息技术一

般控制了解的人员项目组中对被审计单位情况比较了解且较有经验的成员负责,同时需要项目组其他成员的参与和配合了解的内容在了解内部控制的各构成要素时,注册会计师应当对被审计单位整体层面的内部控制的设计进行评价,并确定其是否得到执行了解的方法注册会计师可以考虑将询问被审计单位人员、观察特定控制的应用、检查文件和报告、执行穿行测试等风险评估程序相结合,以获取审计证据与“控制环境”的关系财务报表层次的重大错报风险很可能源于薄弱的控制环境与“业务流程层面控制有效性”的关系被审计单位整体层面的内部控制是否有效将直接影响重要业务流程层面控制的有效性,进而影响注册会计师拟实施的进一步审计程序的性质、时间安排和范围 2.业务流程层面控制:控制活动、信息系统、信息技术应用控制等。(与“认定”层次的重大错报风险相关) 业务层面内控要素信息系统与沟通、控制活动、信息技术的应用控制了解的时间在“初步计划审计工作”时,注册会计师需要确定在被审计单位财务报表中可能存在重大错报风险的重大账户及其相关认定。了解的步骤(1)确定被审计单位的重要业务流程和重要交易类别;(2)了解重要交易流程,并记录获得的了解;(3)确定可能发生错报的环节;(4)识别和了解相关控制;(5)执行穿行测试,证实对交易流程和相关控制的了解;(6)进行初步评价和风险评估了

注会2020《审计》第二章经典练习题

注会2020《审计》第二章经典练习题 一、单项选择题 1、注册会计师应当在审计业务开始时开展初步业务活动。下列各项中,不属于初步业务活动的是()。 A.针对保持客户关系和具体审计业务实施相应的质量控制程序 B.评价遵守相关职业道德要求的情况 C.在执行首次审计业务时,查阅前任注册会计师的审计工作底稿 D.就审计业务的约定条款与被审计单位达成一致意见 【答案】C 【解析】查阅前任注册会计师的审计工作底稿是在接受委托后才会涉及的,初步业务活动的目的是确定是否接受委托,因此该环节不涉及查阅前任注册会计师审计工作底稿的情况。 2、在完成审计业务前,如果审计客户要求将财务报表审计业务变更为财务报表审阅业务,下列理由中,注册会计师认为合理的是()。 A.注册会计师不能获取完整和令人满意的信息 B.注册会计师不能获取充分、适当的审计证据 C.被审计单位提出大幅度削减审计费用 D.被审计单位对原来要求的审计业务的性质存在误解 【答案】D 【解析】注册会计师认为变更业务的合理理由有两种情况:① 环境变化对审计服务的需求产生影响; ②被审计单位对原来要求的审计业务的性质存在误解。 3、如果是连续审计业务,在下列情况中,需要注册会计师提醒被审计单位管理层关注或修改现有业务的约定条款的是()。

A.注册会计师对前期财务报表出具了保留意见审计报告 B.注册会计师更换两名审计助理人员 C.被审计单位对前期财务报表作出重述 D.被审计单位更换了董事长和总经理 【答案】D 【解析】选项D属于被审计单位高级管理人员发生变动,注册会计师应该修改审计业务约定书或提醒被审计单位注意现有的业务约定条款。 4、在制定总体审计策略时,注册会计师应当考虑的主要因素是()。 A.推断的控制有效性高于其实际有效性的风险 B.推断某一重大错报不存在而实际存在的风险 C.潜在的重大错报风险 D.推断某一重大错报存在而实际不存在的风险 【答案】C 【解析】注册会计师应当考虑潜在的重大错报风险的领域,从而合理的安排审计范围、时间和方向。选项ABD均为实施具体审计程序需要考虑的因素。 5、注册会计师在确定财务报表整体的重要性时通常选定一个基准。下列各项因素中,在选择基准时不需要考虑的是()。 A.被审计单位所处的生命周期阶段 B.基准的重大错报风险 C.基准的相对波动性 D.被审计单位的所有权结构和融资方式 【答案】B

《注册会计师审计综合实训》十三.业务完成阶段工作底稿

五、业务完成阶段工作底稿

业务完成阶段审计工作 被审计单位:安琪儿食品有限责任公司项目:业务完成阶段审计工作 编制:罗紫云 日期:索引号: E 财务报表截止日/期间:2010.12.31 复核: 日期: 审计工作索引号执行人 1.召开项目组会议,汇总审计过程中发现的审计差异,根据错报的重要性确定建议被审计单位调整的事项,编制账项调整分录汇总表、重分类调整分录汇总表、列报调整汇总表、未更正错报汇总表以及试算平衡表草表。EA EB EC ED EE 2.与被审计单位召开总结会,就下列事项进行沟通,形成总结会会议纪要 并经双方签字认可: (1) 审计意见的类型及审计报告的措辞; (2) 账项调整分录汇总表、重分类调整分录汇总表、列报调整汇总表、 未更正错报汇总表以及试算平衡表草表; (3)对被审计单位持续经营能力具有重大影响的事项; (4)含有已审计财务报表的文件中的其他信息对财务报表的影响; (5)对完善内部控制的建议; (6)执行该项审计业务的注册会计师的独立性。 获得被审计单位同意账项调整、重分类调整和列报调整事项的书面确 认;如果被审计单位不同意调整,应要求其说明原因。根据未更正错报 的重要性,确定是否在审计报告中予以反映,以及如何反映。 在就上述有关问题与治理层沟通时,提交书面沟通函,并获得治理层的 确认。 EF EG 3.编制正式的试算平衡表。EE 4.对财务报表进行总体复核,评价财务报表总体合理性。如果识别出以前 未识别的重大错报风险,应重新考虑对全部或部分交易、账户余额、列 报评估的风险是否恰当,并在此基础上重新评价之前实施的审计程序是 否充分,是否有必要追加审计程序。 略 5.将项目组成员间意见分歧的解决过程,记录于专业意见分歧解决表中。汇总重大事项,编制重大事项概要。EH EI 6.评价审计结果,形成审计意见,并草拟审计报告: (1)对重要性和审计风险进行最终评价,确定是否需要追加审计程序或提 请被审计单位做出必要调整: 1)按财务报表项目确定可能的错报金额; 2)确定财务报表项目可能错报金额的汇总数(即可能错报总额)对财 务报表层次重要性水平的影响程度。 (2)对被审计单位已审计财务报表形成审计意见并草拟审计报告。 略

审计实务各章习题

第一章销售与收款循环审计练习题 一、填空题 1.在审计过程中,交易和账户余额的实质性测试既可以按进行,也 可以按实施。 2.分项审计与按业务循环进行的严重脱节,导致控制测试与相 背离。 3.在对被审计单位的内部控制进行了解与测试后,注册会计师应当对其 作出评价,并对的内容作出相应的调整。 4.对主营业务收入实施截止测试,其目的主要在于确定应记入本期或下期 的主营业务收入有否或。 5.肯定式函证就是向债务人发出,要求其证实所函的欠款是否正确,无论对错都要求。 6.应收票据是企业的资产,对应收票据的审计应结合业 务 一起进行。 二、判断题(正确的划“√”,错误的划“×”) 1.主营业务收入审计应检查有无特殊的销售行为,以确定适当的审计程序 进行审核。 ( ) 2.询证函由注册会计师利用被审计单位提供的应收账款明细账户名称及地 址编制,并由被审计单位寄发;回函也应直接寄给被审计单位并由其转交给会计 师事务所。 ( ) 3.肯定式函证方式没有得到复函的,应采用追查程序,一般说来应第二次 乃至第三次发送询证函,如果仍得不到答复,注册会计师应考虑采用必要的替代 审计程序。 ( ) 4.如果函证结果表明没有审计差异,则注册会计师可以合理地推论,全部 应收账款总体是正确的。 ( ) 三、单项选择题 1.下列各项中,不属于应收票据实质性测试的审计目标的是( )。 A.确定应收票据的内部控制是否存在、有效且得到一贯遵循 B.确定应收票据是否存在、完整并归被审计单位所有 C.确定应收票据的年末余额是否正确 D.确定应收票据在财务报表上的披露是否恰当 2.注册会计师对被审计单位实施销货业务的截止测试,其主要目的是检查 ( )。 A.年底应收账款的真实性 B.是否存在过多的销货折扣 C.销货业务的人账时间是否正确 D.销货退回是否已经核准 3.对大额逾期应收账款如无法获取询证函回函,则注册会计师应( )。 A.审查所审计期间应收账款回收情况

注会审计重点总结

第一章审计概述 重大错报风险与被审计单位风险相关,其独立于财务报表审计而存在(重大错报风险是客观存在的,注册会计师只能识别评估重大错报风险,不能通过审计工作控制或降低重大错报风险;注册会计师只能控制检查风险) 财务报表审计和企业内部控制审计均属于合理保证的鉴证业务,审阅属于有限保证的鉴证业务,其他鉴证业务可能是合理保证鉴证业务,也可能是有限保证鉴证业务。 相关服务(会计服务管理咨询税务服务代编财务信息商定程序)均不需要提供保证(没有第三方) 职业怀疑是保证审计质量的关键要素;职业怀疑与客观和公正、独立性两项职业道德基本原则密切相关,保持独立性可以增强注册会计师在审计中保持客观公正、职业怀疑的能力。 在评估一项重大错报风险时是否为特别风险时,注册会计师不应考虑控制对风险的抵消作用 财务报表层次的重大错报风险与财务报表整体存在广泛联系,可能影响多项认定,无法与特定的交易、账户余额和披露的认定相联系 审计的目的是改善财务报表质量,增强预期使用者对财务报表的信赖程度 审计的核心工作是围绕管理层认定获取和评价审计证据 第二章审计计划 审计的前提条件:

①管理层在编制财务报表时采用可接受的财务报告编制基础 ②管理层对注会执行审计工作的前提的认同(执行审计工作的前提—管理层已认可并 理解其承担的责任3点) 只有将审计业务变更为执行商定程序业务,注册会计师才可在报告中提及已执行的程序 除非法律法规禁止,注册会计师应当及时将审计过程中累积的所有错报与适当层级的管理层进行沟通,并要求管理层更正这些错报(没有超过明显微小错报临界值的可以不用更改) 财务报表整体重要性水平的应用: ①决定风险评估程序的性质、时间安排和范围 ②识别和评估重大错报风险 ③确定进一步审计程序的性质、时间安排和范围 ④在形成审计结论阶段,使用整体重要性水平和为了特定交易较低的重要性水平来评 价已识别的错报对财务报表的影响;评价未更正错报对审计报告中审计意见的影响实际执行重要性的运用:确定需要对哪些类型的交易、账户余额和披露实施进一步审计程序,通常选取金额超过实际执行重要性的财务报表项目 注册会计师不能对所有金额低于实际执行重要性的财务报表项目不实施进一步审计程序(单个金额低于实际执行重要性的财务报表项目汇总起来可能金额重大;存在低估风险的财务报表项目;识别出存在舞弊风险的财务报表项目)

审计学练习题答案及解析(第二章)

第二章》 一、单选题共29 道 【题目1】注册会计师考试需要进行论文和口试的国家为( D ) 。 (A) 美国 (B) 英国 (C) 加拿大 (D) 日本 【题目2】注册会计师要取得注册会计师执业资格,除具备相应学历并通过全国统一考试外,还应具备的条件是( A ) 。 (A) 接受后续教育 (B) 一定时间的从业经验 (C) 经过专门的专业训练 (D) 不能从事注册会计师行业以外的工作 【题目3】下列人员中,可以申请免予专业阶段考试 1 个专长科目考试的是( A ) 。 (A) 会计学教授并具有会计工作经验 (B) 会计专业中级以上专业技术职称 (C) 会计专业学士学位获得者 (D) 会计专业硕士学位获得者 【题目4】下列各项中,不属于会计咨询、会计服务业务内容的是( C ) 。 (A) 管理咨询 (B) 代理记账 (C) 审查中期财务报表 (D) 税务代理 【题目5】与鉴证业务相比较,咨询服务的特点是( C ) 。 (A) 由CPA、信息使用者和信息提供者三方达成合约 (B) 以适当保证和提高财务信息质量为目标 (C) 以财务信息的使用为目标 (D) 以独立性与专业性为主要基础 【题目6】我国《注册会计师法》规定,会计师事务所的组织形式不包括( A ) 。 (A) 独资公司 (B) 普通合伙会计师事务所 (C) 有限责任会计师事务所 (D) 特殊普通合伙会计师事务所 【题目7】中国注册会计师协会的最高权力机构是( B ) 。 (A) 财政部 (B) 全国会员代表大会 (C) 中国注册会计师协会理事会

(D) 中国注册会计师协会秘书处 【题目8】注册会计师从事的下列工作中,属于审计业务的是( B ) 。 (A) 审查企业内部控制制度,提出管理建议书 (B) 参与企业破产清算,出具审计报告 (C) 参与企业合并事宜,代编合并财务报表 (D) 参与企业管理,起草投资协议书 【题目9】注册会计师事务所从事的下列业务中,不属于审计等鉴证业务的是( B ) 。 (A) 验资 (B) 税务咨询 (C) 财务报表审计 (D) 内部控制审核 【题目12】下列各项中,能够成为中国注册会计师协会团体会员的是( A ) (A) 会计师事务所 (B) 5 名以上注册会计师组成的科研团体 (C) 高等科研院校的相关机构 (D) 境外会计师组织 、多选题共30 道 【题目1】具有( ABCD )条件的中国公民可以申请参加注册会计师全国统一考试。 (A) 大学本科学历以上 (B) 大专或大专学历以上 (C) 会计及相关专业高级技术职称 (D) 会计及相关专业中级或中级以上技术职称 【题目2】中国注册会计师协会的会员包括( ABC ) 。 (A) 个人会员 (B) 团体会员 (C) 名誉会员 (D) 临时会员 【题目3】准予注册的注册会计师发生( ABCD ) 情况时,注册会计师协会将撤销注册、收回注册会计师证书。 (A) 完全丧失民事行为能力的 (B) 受刑事处罚的 (C) 因在财务、会计、审计、企业管理或者其他经济管理工作中犯有严重错误受行政处罚、撤职以上处分的 (D) 自行停业满一年的 【题目4】下列关于我国会计师事务所业务承接和承办的说法中正确的有( AC ) 。 (A) 以会计师事务所名义承接业务 (B) 特殊情况下可以以主任会计师的个人名义接受委托 (C) 由于委托人不同,会计师事务所在承办业务时被授予的权限也不同 (D) 出具审计报告时,只需注册会计师个人的签章