会计英语 会计循环ppt

合集下载

会计英语培训资料(英文版)ppt(共29页)

► (1) unearned rent ► (2) tuition ► (3) annual retailer fee ► (4) premium ► (5) magazine subscriptions

► Accruals --------- are created by an unrecorded expense that has been incurred or an unrecorded revenue that has been earned.

► (1) supplies ► (2) prepaid insurance ► (3) prepaid advertising ► (4) prepaid interest

► ㈡ Deferred revenues (unearned revenue) → become revenues over time

► ㈢ Accrued expenses (accrued liabilities) →

► expense have been incurred but not recorded

► (1) accrued wages

► (2) accrued interest on notes payable

► (3) accrued taxes

► Current accounting period → ► ( cash received or paid )

( revenue or expense incurred ) ► →future accounting period ► ( revenue or expense incurred )

► The journal entries that bring the accounts up to gate at the end of the accounting period are called adjusting entries.

《会计循环》课件2

计量

计量是会计循环的第二个步骤,主要是对经济业务进行数 量和金额的确定,包括资产、负债、所有者权益、收入、 费用等会计要素的计量。

报告

报告是会计循环的最后一个步骤,主要是根据记录的信息 和数据编制财务报告,向外部利益相关者提供企业的财务 状况、经营成果和现金流量等信息。

会计循环的重要性

提供准确财务信息

资产负债表的编制

资产负债表概述

资产负债表是反映企业在特定日期财务状况的财务报表,包括资产 、负债和所有者权益三个部分。

资产负债表的编制方法

根据日常的会计记录和交易数据,按照一定的分类和汇总方法,编 制资产负债表。

资产负债表的分析

通过分析资产负债表,可以了解企业的资产结构、负债状况和所有 者权益状况,从而评估企业的财务状况和经营风险。

2023-2026

ONE

KEEP VIEW

《会计循环》PPT课 件

REPORTING

CATALOGUE

目 录

• 会计循环概述 • 会计凭证与账簿 • 会计循环流程 • 财务报表的编制 • 会计循环中的问题与对策 • 会计循环案例分析

PART 01

会计循环概述

会计循环的定义

会计循环定义

会计循环是指企业在一系列会计程序 和步骤中,按照规定的顺序,从处理 经济业务开始,到编制财务报告结束 的整个过程。

总结词

账簿是记录经济业务发生情况的重要工具,也是编制财务报表的基础。

详细描述

账簿的登记需要按照规定的分类和账户设置进行,包括总账、明细账、日记账 等。在登记账簿时,需要遵循平行登记原则,确保账簿记录与凭证内容一致, 并定期进行核对和调整。

对账与结账

总结词

对账与结账是会计循环中重要的环节,通过对账和结账,可以确保账务处理的准确性和 完整性。

第三章会计循环ppt课件

20 000

四、结账

(一)定义 就是在把一定时期内发生的经济业务在全部 登记入账的基础上,结出各账户的“本期发生额”和“期 末余额”,从而根据账簿记录编制会计报表。

1、实账户的结转: 实账户是指资产、负债及所有者权益类账户,即列示 在资产负债表的账户,这类账户的余额逐年递转延续,所 以此时的结账是指结出期末新余额。 2、虚账户的结清: 虚账户是指收入和费用两类账户,即列示在利润表的 账户,这类账户的余额应结平为“零”。

凭证

(2)按是否经过汇总 ①汇总记账凭证 A、分类汇总记账凭证 定期根据收款凭证、付款凭证和转账凭证分

别汇总编制汇总收款凭证、汇总付款凭证和汇总 转账凭证。

B、全部汇总记账凭证 将一定时期内编制的记账凭证全部汇总在一张 记账凭证上。 ②非汇总记账凭证 根据每一原始凭证或原始凭证汇总表单独填制 的记账凭证。

借:材料采购 800 贷:银行存款 800

(更正……错误记录)

记账 记账

对第二种错误: 所记金额>应记金额,则将差额用红字填制凭证并过账。

例2.用银行存款支付管理费用1500元。记账凭证中将1500 元写为5100元,并已入账。

更正

借:管理费用 3600 贷:银行存款 3600

(冲销 …… 多记数)

登账完毕,编制试算平衡表。

7、编制会计报表。

发生经济业务

传递原始凭证

交给会计

登记会计明细账 核对

登记会计总账

资产负债表

利润表

根据原始凭 证填制记账 凭证

账务处理程序

原始凭证

原始凭证 汇总表

收款凭证

2

现金日记账

银行存款日记账

1

付款凭证

5

4

会计英语课件ch2 accounting cycle

Date 2001 May 1

Cash Debit Credit 8,000

Accounting English @2011

Balance 8,000

13

Posting Journal Entries to the Ledger Accounts

GENERAL JOURNAL

Date 2001 May 1 Cash Jill Jones, Capital Owner investedGeneral cash in theLedger business. 8,000 8,000 Account Titles and Explanation Debit Credit

Accrual and cash basis accounting

Accrual accounting requires adjustments for prepaid, unearned, and accrued items; therefore, it reports revenues when earned and expenses when incurred. Cash basis accounting does not make adjustments; revenues are recorded when cash is received and expenses are recorded when cash is paid.

The Steps of Accounting cycle

The

term accounting cycle refers to the steps in preparing financial statements. The accounting cycle includes standardized procedures that are performed in sequence during every accounting period.

会计英语unit5CompletionoftheAccountingCycle精课件

The period of service is called the useful life or service life of the asset.

Depreciation is the process of allocating the cost of an asset to expense over its useful life.

The amount of interest accumulation is determined by three factors:

Interest = Face Value of Note x Annual Interest Rate x Time in Terms of One Year

21

Interest cost for a month : $10,000 x 12% x 1/12=$100

At the end of month

Dr. Interest Expense Cr. Interest Payable

100 100

22

Example(2) Accrued Salaries

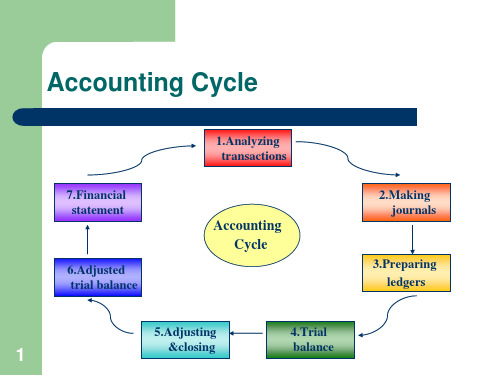

Accounting Cycle

7.Financial statement

6.Adjusted trial balance

1.Analyzing transactions

Accounting Cycle

2.Making journals

3.Preparing ledgers

5.Adjusting

4.Trial

At the end of month

Dr. Unearned Revenue 1,000 Cr. Service Revenue 1,000

Depreciation is the process of allocating the cost of an asset to expense over its useful life.

The amount of interest accumulation is determined by three factors:

Interest = Face Value of Note x Annual Interest Rate x Time in Terms of One Year

21

Interest cost for a month : $10,000 x 12% x 1/12=$100

At the end of month

Dr. Interest Expense Cr. Interest Payable

100 100

22

Example(2) Accrued Salaries

Accounting Cycle

7.Financial statement

6.Adjusted trial balance

1.Analyzing transactions

Accounting Cycle

2.Making journals

3.Preparing ledgers

5.Adjusting

4.Trial

At the end of month

Dr. Unearned Revenue 1,000 Cr. Service Revenue 1,000

会计英语PPT(完成版) Chapter 4-The Accounting Cycle

5

of

11

Posting to the General Ledger

The last step is to insert the ledger account number in the Posting Reference column (POST REF.) of the journal.

The last two steps both serve as a cross-reference, which enables us to trace a transaction from the journal to the ledger or from the ledger to the journal quickly. After the process of posting to the general ledger, the journal and the ledger should contain the same information

The accounting cycle usually can be divided into the following steps: ① analyzing transactions from source documents; ② posting journal entries to ledger accounts; ③ preparing a trial balance; ④ completing a work sheet; ⑤ preparing financial statements.

6

of

11Trial Balan来自eThe trial balance is a two- column schedule listing the names and balances of all the accounts appearing in the ledger with the purpose of verifying clerical accuracy and preparing financial statements. The debit balances are listed in the left-hand column and the credit balances in the right-hand column. Because the amounts of debits and credits are equal, the sum of all the debits in the ledger must be the same as the sum of all the credits.

《会计学》(第5版)课件:会计循环

22

Continued

❖ 按照复式记账的基本要求,借贷记账法的基本原则表述为“有 借必有贷,借贷必相等”。也就是说,任何一笔经济业务都必 须同时分别记录到两个或两个以上的账户中去;所记录的账户 必须包括借、贷两个记账方向,不能只记入借方或只记入贷方; 借贷金额的合计必须相等。在较为简单的经济业务中,会计记 录可能只包括一个借方和一个贷方,而对有些复杂的经济业务, 则需要将其登记在一个账户的借方和几个账户的贷方,或者登 记在一个账户的贷方和几个账户的借方。

经

会

济

计

业

记账方法

语

务

言

会 计会 凭计会 证账计

簿报 表

15

2.2.2 借贷记账法

❖ 记账方法的分类 单式记账

每一项经济业务的影响只记录在一个账户之中。例如,销售货品之后, 仅记录现金的增加,存货交付之后,仅记录存货的减少。

这种记账方式的优点是操作简单,缺点是对经济业务的反映比较片面, 账户之间联系不紧密,无法实现自我复核的作用。

❖ 账户也可以按照其他的标准进行分类。同会计科目分为总分类 科目和明细科目相对应,按照核算信息的详细程度及统驭关系 不同,账户还可以分为总分类账户(简称总账)和明细分类账 户(简称明细账)。

14

2.2.2 借贷记账法

❖ 记账方法的作用 企业的财务部门在经济业务发生之后,必须借助一定的记账 方法,将经济业务对企业各会计要素(资产、负债、所有者 权益、收入、费用和利润)的影响,结合确认和计量过程, 转换为会计语言,然后才有可能登记账簿和填列报表。

11

Continued

❖ 账户名称 “库存现金”明确了账户的核算对象。 ❖ 期初余额23,000元记录在账户左方(即借方)的第一行。期初

Continued

❖ 按照复式记账的基本要求,借贷记账法的基本原则表述为“有 借必有贷,借贷必相等”。也就是说,任何一笔经济业务都必 须同时分别记录到两个或两个以上的账户中去;所记录的账户 必须包括借、贷两个记账方向,不能只记入借方或只记入贷方; 借贷金额的合计必须相等。在较为简单的经济业务中,会计记 录可能只包括一个借方和一个贷方,而对有些复杂的经济业务, 则需要将其登记在一个账户的借方和几个账户的贷方,或者登 记在一个账户的贷方和几个账户的借方。

经

会

济

计

业

记账方法

语

务

言

会 计会 凭计会 证账计

簿报 表

15

2.2.2 借贷记账法

❖ 记账方法的分类 单式记账

每一项经济业务的影响只记录在一个账户之中。例如,销售货品之后, 仅记录现金的增加,存货交付之后,仅记录存货的减少。

这种记账方式的优点是操作简单,缺点是对经济业务的反映比较片面, 账户之间联系不紧密,无法实现自我复核的作用。

❖ 账户也可以按照其他的标准进行分类。同会计科目分为总分类 科目和明细科目相对应,按照核算信息的详细程度及统驭关系 不同,账户还可以分为总分类账户(简称总账)和明细分类账 户(简称明细账)。

14

2.2.2 借贷记账法

❖ 记账方法的作用 企业的财务部门在经济业务发生之后,必须借助一定的记账 方法,将经济业务对企业各会计要素(资产、负债、所有者 权益、收入、费用和利润)的影响,结合确认和计量过程, 转换为会计语言,然后才有可能登记账簿和填列报表。

11

Continued

❖ 账户名称 “库存现金”明确了账户的核算对象。 ❖ 期初余额23,000元记录在账户左方(即借方)的第一行。期初

《会计循环》PPT课件

登记账簿 账 簿

记账凭证

5

(二)原始凭证

真实凭证

1.原始凭证的概念

●经济业务发生时取得或填制的会计凭证

●证明经济业务的发生和完成情况

●作为记账原始依据的会计凭证

主要内容 载明经济业

填制程序 经济业务发 务内容及完成情况

主要作用 进行会计核

生时取得或填制

算的原始依据

原始凭证

经济业务

取得

(交易或

事项)

一次凭证 累计凭证

汇总原始凭证

账簿

账簿

会计 人员 填制

记账编制凭证

★记账编制凭证属于原始凭证的一种。 应与下面讲述的记账凭证严格区别!

13

(2)外来原始凭证——一般为一次凭证

企业之间发生交易时开具 的发票,不同于普通发票

外来原始凭证

普通增值税发票

14

3.原始凭证的填制(或取得)要求 ●反映的业务内容真实可靠。 ●内容完整、项目齐全,手续完备。 ●简洁清楚,符合规范要求。 ●填制及时并按规定程序传递。

18

• 支票的填制方法:

19

• 2007年2月10日,金鑫贸易有限公司(帐号 001009014413252)签发转账支票支付集盛 钢铁有限公司购货款500000元。支票如下:

20

4.原始凭证的审核 ★真实性的审核。 ★完整性的审核。 ★合法性的审核。

《中华人民共和国会计法》第十四条规定:会计机构、 会计人员必须按照国家统一的会计制度的规定对原始凭证 进行审核,对不真实、不合法的原始凭证有权不予接受, 并向单位负责人报告;对记载不准确、不完整的原始凭证 予以退回,并要求按照国家统一的会计制度的规定更正、 补充。

经济 业经业经务济务济

第2章 Accounting Cycle《会计英语》PPT课件

which decreases equity.

Unit 1 Accounting Equation and Double-entry Accounting

➢ DOUBLE-ENTRY ACCOUNTING.

➢The equilibrium which the bookkeeping record achieves through the

➢The following table summarizes the rule.

Assets and Expenses

Debit

+

Credit

-

Liabilities,Owners’Equity & Revenue

Debit

-

Credit

+

Special Terms

1. accounting equation

Business activities can be described in terms of transactions and

events. The first step will identify transactions and events that cause

a change in the firm’s resources or obligations and will collect

会计等式或会计平衡式。在复式记账法下,不论一个

期间发生多少经济业务,其记录的结果始终不会破坏会计等式三项要素之间的平

衡关系,即:

资产=负债+所有者权益

2. contributed capital 缴入股本,指股东投入企业的现金或其他资产,包括股

本和股本溢价两部分。

3. common stock 普通股,英国称ordinary share,是公司股票的主要种类,通

Unit 1 Accounting Equation and Double-entry Accounting

➢ DOUBLE-ENTRY ACCOUNTING.

➢The equilibrium which the bookkeeping record achieves through the

➢The following table summarizes the rule.

Assets and Expenses

Debit

+

Credit

-

Liabilities,Owners’Equity & Revenue

Debit

-

Credit

+

Special Terms

1. accounting equation

Business activities can be described in terms of transactions and

events. The first step will identify transactions and events that cause

a change in the firm’s resources or obligations and will collect

会计等式或会计平衡式。在复式记账法下,不论一个

期间发生多少经济业务,其记录的结果始终不会破坏会计等式三项要素之间的平

衡关系,即:

资产=负债+所有者权益

2. contributed capital 缴入股本,指股东投入企业的现金或其他资产,包括股

本和股本溢价两部分。

3. common stock 普通股,英国称ordinary share,是公司股票的主要种类,通

第章 会计循环2(共6张PPT)

会计学原理

Accounting

9 会计 Principles 循环

第1页,共6页。

会计学原理 9 会计循环

第一节 会计循环过程

一、会计循环的含义

对企业经济 与事项所进展的会计确认、计 量、记录

和报告实践上是一个延续不断、周而复始的过程,企业 会计

信息的这一处置过程,称为会计循环。

第2页,共6页。

会计学原理 9 会计循环

二、企业会计循环的根本过程 〔一〕分析经济

〔二〕记录经济 〔三〕期末账项调整 〔四〕核对账户记录 〔五〕结算账户记录

〔六〕编制财务报表

第3页,共6页。

会计学原理 9 会计循环

三、我国企业会计循环的详细过程

Principles 会计学原理 9 会计循环 二、企业会计循环的根本过程

和会报计告 学实原践理上9填是一制会个记计延循账续环凭不证断、(分周录而记复始录的) 过程,企业会计

填制记账凭证(分录记录) 会计学原理 9 会计循环

Principles 〔六〕编制财务报表

第二节 综合案例登记账簿(账户记录)

会计学原理 9 会计循环 对企业经济 与事项所进展的会计确认、计量、记录 二、企业会计循环的根本过程 〔三〕期末账项调整

第二节 综合案例期末调账户记录

经济 与事项

会计确认

会计计量 期末核对账目

过账 总分类账 明细分类账

编制试算表

任务底表 〔备选〕

调整后试算表

调整 应计工程 预付工程 估计工程等

第6页,共6页。

编制财务报表 期末结账

第4页,共6页。

会计学原理 9 会计循环

第二节 综合案例

〔详见教材〕

第5页,共6页。

会计学原理 9 会计循环

Accounting

9 会计 Principles 循环

第1页,共6页。

会计学原理 9 会计循环

第一节 会计循环过程

一、会计循环的含义

对企业经济 与事项所进展的会计确认、计 量、记录

和报告实践上是一个延续不断、周而复始的过程,企业 会计

信息的这一处置过程,称为会计循环。

第2页,共6页。

会计学原理 9 会计循环

二、企业会计循环的根本过程 〔一〕分析经济

〔二〕记录经济 〔三〕期末账项调整 〔四〕核对账户记录 〔五〕结算账户记录

〔六〕编制财务报表

第3页,共6页。

会计学原理 9 会计循环

三、我国企业会计循环的详细过程

Principles 会计学原理 9 会计循环 二、企业会计循环的根本过程

和会报计告 学实原践理上9填是一制会个记计延循账续环凭不证断、(分周录而记复始录的) 过程,企业会计

填制记账凭证(分录记录) 会计学原理 9 会计循环

Principles 〔六〕编制财务报表

第二节 综合案例登记账簿(账户记录)

会计学原理 9 会计循环 对企业经济 与事项所进展的会计确认、计量、记录 二、企业会计循环的根本过程 〔三〕期末账项调整

第二节 综合案例期末调账户记录

经济 与事项

会计确认

会计计量 期末核对账目

过账 总分类账 明细分类账

编制试算表

任务底表 〔备选〕

调整后试算表

调整 应计工程 预付工程 估计工程等

第6页,共6页。

编制财务报表 期末结账

第4页,共6页。

会计学原理 9 会计循环

第二节 综合案例

〔详见教材〕

第5页,共6页。

会计学原理 9 会计循环

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

6. Prepare financial statements

5. Prepare a worksheet

4. Determine account balances and prepare a trial balance

8. Make closing entries

9. Prepare a post-closing trial balance

Step 2. Journalize Transactions The second step in the accounting cycle is to record the results of transactions in a journal. Known as “book” books of original entry“, journals provide a chronological record of all entity transactions. They show the dates of the transactions, the amounts involved, and particular accounts affected by the transactions. Usually, an explanation of the transaction is also panies may use General Journals or special journals to record all transactions. This format can be called journal entry.

Step 6. Prepare Financial Statements Once all transactions have been analyzed, journalized, and posted and all adjusting entries have been made, the accounts can be summarized and presented in the form of financial statements. The information for the income statement and the balance sheet is taken directly form the worksheet, when one is used. When a worksheet is not used, financial statements are prepared directly from the data in the adjusted ledger accounts.

Step4. Determine Account Balances and Prepare a Trial Balance At the end of each accounting period, after all of the regular entries for completed transactions have been journalized and posted to the ledger, a trial balance should be prepared. This trial balance is prepared before the adjusting entries are made; therefore, it is often called the unadjusted trial balance.A trial balance lists each account with its debit or credit balance. These types of errors will not be discovered by preparing a trial balance; additional analysis would be required.

Step 9. Prepare a Post-Closing Trial Balance The purposes of a trial balance are (a) to verify the equality of the debits and credits and (b) to have the account balances ready for other uses. Two different trial balances have already been discussed: the unadjusted trial balance and the adjusted trial balance. A third trial balance usually is taken after the closing entries have been posted. It is called the post-closing trial balance. It is used to verify that the debits and credits are equal at the start of the next accounting period.

Step 3. Post Journal Entries to Accounts Once transactions have been analyzed and recorded in journal, it is necessary to classify and group all similar items. This is accomplished by the procedure of posting all the journal entries to appropriate accounts. A ledger, is a book of accounts in which data from transactions recorded in journals are posted and thereby classified and summarized. The list of accounts used by a company is known as its chart of accounts.

Step 8. Make Closing Entries After the financial statements are prepared and the adjusting entries have been journalized and posted, the closing process must be completed. The purpose of the closing process is to transfer the balances of all of the temporary accounts to the Retained Earnings account. The result is that (a) retained earnings will be increased by the amount of net income, or decreased by net loss, and (b) each temporary account will start the next year with a zero balance. The permanent accounts are not affected by the closing process except for the change in retained earnings.

The Accounting Cycle

The accounting cycle is the process by which accountants prepare financial statements for an entity for a specific period of time.

Steps in the accounting cycle

1. Analyze transactions and business documents 2. Journalize transactions 3. Post journal entries to accounts

7. Journalize and post adjusting entries

Step 5. prepare a Worksheet The financial statements cannot be prepared until all of the necessary adjusting entries have been formulated. The unadjusted trial balance must be adjusted to in corporate the effects of all of the adjusting entries. A separate worksheet is needed to develop the statement of changes in financial position. Notice that worksheet is not a part of the basic accounting records of the entity; it is a separate facilitation technique tnimizes processing errors. It does not replace the financial statements or any entries in the accounts.

10. Make reversing entries

Step 1. Analyze Transactions and Business Documents The first step in the accounting cycle is to analyze transactions and business documents-the sale invoices, check stubs, and other records that are evidence of those transactions. Business documents confirm that a transaction has occurred and establish the amounts to be recorded. This is the key step in the accounting cycle.