12+财务报告

财务工作调研报告(精选12篇)

财务工作调研报告财务工作调研报告(精选12篇)在不断进步的时代,报告的用途越来越大,要注意报告在写作时具有一定的格式。

一听到写报告就拖延症懒癌齐复发?以下是小编为大家收集的财务工作调研报告,仅供参考,大家一起来看看吧。

财务工作调研报告篇1根据县政协统一安排部署,镇政协工委组织六人专门的调研小组,于本月26日、27日,利用两天时间对长铺社区和马塘村近一年来的财务管理情况进行调研,通过与村(社区)两委干部及部分群众座谈,广泛听取意见,形成本调研报告:一、村级当前财务管理的基本状况。

从调研的情况看,我镇村级财政资金使用情况总体上较好,基本上达到了制度建立、执行规范、监督有效的要求,村级组织运转逐步规范。

(一)建立了村级财政资金管理制度。

各村普遍较为重视村级财政资金的管理使用,按照镇党委、政府出台的《村级财务管理制度》,结合实际制定资金使用、监督管理等办法,对资金的拨付、流程、使用、报账、监督等都作出明确规定,切实管好用好村级财政资金。

通过各项管理制度的下发和完善,为村级资金的规范管理创造了良好的条件。

从而使村级财务工作规范化。

(二)全面实施了“村财村用镇代管”制度。

我镇在并村后,率先在全县实行村财镇管的办法,镇专门设立联管办,工作人员在镇财政所内调配、镇根据实际进行适当的补充,业务上接受上级部门的指导,在坚持村级资金所有权、使用权、自主权不变的前提下,按照集中管理、统一开户、分村设账等原则,将村级各类财政补助资金、专项资金纳入管理范围,严格按照财务制度和村级资金管理办法进行支出管理,确保了村级运转补助资金的安全运行,实行“村财村用镇代管”制度,确保了村级资金专款专用和集中核算,提高了资金的使用效益。

(三)对村级财政资金实施有效的监督管理。

在做好村级资金日常管理的同时,还高度重视资金的使用监管工作。

一是普遍推行村务公开、民主理财制度,定期向村民公开村级财务收支情况,自觉接受群众的监督。

村级支出票据须经经手人签字、书记审核、主任审批和村民理财小组负责人共同签字审核后才能予以报账。

第12章 财务报告练习题

第十二章财务报告练习题一、单项选择题1、以下资产负债表项目中,根据明细科目余额计算填列的是()。

A.货币资金 B.预付账款 C.应收票据 D.短期借款2、某企业期末“工程物资”科目的余额为100万元,“发出商品”科目的余额为50万元,“原材料”科目的余额为60万元,“材料成本差异”科目的贷方余额为5万元,“存货跌价准备”科目的余额为20万元,假定不考虑其他因素,该企业资产负债表中“存货”项目的金额为()万元。

A.85 B.95 C.185 D.1953、“应收账款”总账借方科目余额12 000万元,其明细账借方余额合计18 000万元,贷方明细账余额合计6 000万元;“预收账款”总账贷方科目余额15 000万元,其明细账贷方余额合计27 000万元,借方明细账余额合计12 000万元。

“坏账准备”科目贷方余额为3 000万元。

资产负债表中“应收账款”项目填列金额为()万元。

A.12 000 B. 27 000 C.24 000 D.18 0004、下列项目中,符合现金流量表中现金概念的是()。

A.企业销售商品收到为期1个月的商业汇票 B.企业存在银行两年的定期存款C.不能随时用于支取的存款 D.从购入日开始计算3个月内到期的国债5、在下列业务中,属于经营活动所产生的现金流量的是()。

A.支付印花税 B.支付耕地占用税C.支付购买工程物资款 D.预提短期借款利息6、甲公司2007年度发生的管理费用为1 000万元,其中以现金支付未参加统筹的退休人员工资30万元,管理人员工资800万元,支付房租5万元,支付失业保险金12万元,支付补充养老保险金8万元,支付矿产资源补偿费20万元,支付印花税1万元,计提坏账准备14万元,计提固定资产折旧100万元,库存商品盘亏损失10万元,若不考虑其他因素,甲公司2007年度现金流量表中“支付的其他与经营活动有关的现金”项目的金额为()万元。

A.5 B.35 C.55 D.757、企业支付给离退休人员的各项费用,在编制现金流量表时,应作为()项目填列。

第十二章 财务报告

项目 一、营业收入(主入+其本) 减:营业成本(主本+其本) 营业税金及附加 销售费用 管理费用 财务费用 资产减值损失 加:公允价值变动损益 投资收益 二、营业利润 加:营业外收入 减:营业外支出 三、利润总额 减:所得税费用 四、净利润 五、每股收益 (一)基本每股收益 (二)稀释每股收益 六、其他综合收益 七、综合收益总额

记账凭证

账务处理程序

现 金 银行存款

③

日记账

原始凭证

1

① ②

收 款

付 款

转 账 ⑤

⑥ 总 账 ⑦ 会计报表

记账凭证

2

原始凭证 汇总表 ④

⑥ 明细账

3

【例题1· 计算分析题】甲公司2012年12月31日结账后有关科目余额如下所示: 科目名称 应收账款 坏账准备——应收账款 借方余额 500 贷方余额 10 50

二、金融资产和金融负债允许抵消和不得相互抵消的要求 (一)金融资产和金融负债相互抵消的条件 金融资产和金融负债应当在资产负债表内分别列示,不得相互抵消。但是,同 时满足下列条件的,应当以相互抵消后的净额在资产负债表内列示: 1.企业具有抵消已确认金额的法定权利,且该种法定权利现在是可执行的; 2.企业计划以净额结算,或同时变现该金融资产和清偿该金融负债。 2 不满足终止确认条件的金融资产转移,转出方不得将已转移的金融资产和相关 负债进行抵消。 (二)金融资产和金融负债不能相互抵消的主要情形【例题1· 多选题】下列项 目中,金融资产和金融负债不可以相互抵消的有( )。 A.企业具有抵消已确认金额的法定权利,且该种法定权利现在是可执行的,但 企业计划以总额计算 B.企业具有抵消已确认金额的法定权利,且该种法定权利现在是可执行的,企 业计划以净额结算 C.企业将浮动利率长期债券与收取浮动利息、支付固定利息的互换组合在一起, 合成为一项固定利率长期债券 D.作为某金融负债担保物的金融资产与被担保的金融负债 E.保险公司在保险合同下的应收分保保险责任准备金与相关保险责任准备金 【答案】ACDE,【解析】金融资产和金融负债应当在资产负债表内分别列示, 不得相互抵消。但是,同时满足下列条件的,应当以相互抵消后的净额在资产负 债表内列示:(1)企业具有抵消已确认金额的法定权利,且该种法定权利现在 是可执行的;(2)企业计划以净额结算,或同时变现该金融资产和清偿该金融 5 负债。

中级财务会计第12章财务报表

会企01表 单位:元

期末余额 年初余额

29

编制单位:

资产负债表 年月日

会企01表 单位:元

资产

期末余额 年初余额 负债和所有者权益

流动资产:

流动负债:

货币资金

短期借款

交易性金融资产 84 000 应收票据

应付票据 应付账款

应收账款

预收账款

应收股利

应付职工薪酬

应收利息

应交税费

其他应收款

应付股利

存货

其他应付款

长期借款

期末余额 100 000

长期借款-X

期末余额 80 000

还款期2年

长期借款-Y

期末余额 20 000

还款期6个月

应填入资产负债表的 “长期借款”项目

应填入资产负债表的”一年 内到期的非流动负债“项目

32

(4)根据若干总账账户期末余额计算填列。

例如, 1、“货币资金”项目 应根据库存现金、银行存款和其他货币资金科目余额之和

计算填列; 2、“存货”项目 应根据材料采购、原材料、委托加工物资、包装物、低值

易耗品、材料成本差异、生产成本、自制半成品、产成品 等科目借贷方余额的差额计算填列; 3、“未分配利润” 应根据本年利润和利润分配科目余额计算填列

33

编制单位:

资产负债表 年月日

会企01表 单位:元

资产 流动资产: 货币资金 交易性金融资产 应收票据 应收账款 应收股利 应收利息 其他应收款 存货 待摊费用 一年内到期的非 流动资产 (略)

例如: 1、一年内到期的非流动资产 应根据持有至到期投资、长期应收款科目所属明

细科目余额中将于一年内到期的数额直接计算填 列; 2、一年内到期的非流动负债 应根据长期借款、应付债券、长期应付款等科目 需要进行类似分析填列

第12章 财务报告

企业的基本情况 财务报表的编制基础 重要会计政策和会计估计 会计政策和会计估计变更以及差错更正的说明 报表重要项目的说明,等等 Monday, June 03, 2013

4

财务报告的作用

有助于投资者和债权人等进行合理的决策;

反映企业管理当局的受托经管责任; 能够帮助企业管理当局改善经营管理;

Monday, June 03, 2013

27

2.下列各项关于甲公司合并现金流量表列报的表 述中,正确的有( )。 A.投资活动现金流入240万元 B.投资活动现金流出610万元 C.经营活动现金流入320万元 D.筹资活动现金流出740万元 E.筹资活动现金流入8 120万元 【答案】ABD 【解析】投资活动的现金流入=120(事项6)+120(事 项8)=240(万元);投资活动现金流出=150(事项4) +160(事项7)+300(事项9)=610(万元);经营活 动的现金流入=0;筹资活动的现金流出=680(事项1) +60(事项5)=740(万元);筹资活动的现金流入=8 000(事项2)+200(事项3)=8 200(万元)。

Monday, June 03, 2013

16

第三节

利润表(P212)

(一)利润表的内容和格式

利润表,是反映企业在一定会计期间经营成果的报表。 1.营业利润=营业收入-营业成本-营业税金及附加-销 售费用-管理费用-财务费用-资产减值损失+公允价值变动 收益(损失以“-”号填列)+投资收益(损失以“-”号 填列)

2.利润总额=营业利润(亏损以“-”号填列)+营业 外收入-营业外支出 3.净利润=利润总额(亏损总额以“-”号填列)-所 得税费用 4、每股收益 17 Monday, June 03, 2013 5、综合收益(P274)

ifrs12国际财务报告准则12号

IFRS12 International Financial Reporting Standard12Disclosure of Interests in Other EntitiesIn May2011the International Accounting Standards Board(IASB)issued IFRS12Disclosure of Interests in Other Entities.IFRS12replaced the disclosure requirements in IAS27Consolidated and Separate Financial Statements,IAS28Investments in Associates and IAS31Interests in Joint Ventures.In June2012,IFRS12was amended by Consolidated Financial Statements,Joint Arrangements and Disclosure of Interests in Other Entities:Transition Guidance(Amendments to IFRS10,IFRS11and IFRS12).These amendments provided additional transition relief in IFRS12,limiting the requirement to present adjusted comparative information to only the annual period immediately preceding the first annual period for which IFRS12is applied.Furthermore, for disclosures related to unconsolidated structured entities,the amendments removed the requirement to present comparative information for periods before IFRS12is first applied.Other IFRSs have made minor consequential amendments to IFRS12,including Investment Entities(Amendments to IFRS10,IFRS12and IAS27)(issued October2012).IFRS Foundation A505IFRS12C ONTENTSfrom paragraph INTRODUCTION IN1 INTERNATIONAL FINANCIAL REPORTING STANDARD12 DISCLOSURE OF INTERESTS IN OTHER ENTITIESOBJECTIVE1 Meeting the objective2 SCOPE5 SIGNIFICANT JUDGEMENTS AND ASSUMPTIONS7 Investment entity status9A INTERESTS IN SUBSIDIARIES10 The interest that non-controlling interests have in the group’s activities andcash flows12 The nature and extent of significant restrictions13 Nature of the risks associated with an entity’s interests in consolidatedstructured entities14 Consequences of changes in a parent’s ownership interest in a subsidiarythat do not result in a loss of control18 Consequences of losing control of a subsidiary during the reporting period19 INTERESTS IN UNCONSOLIDATED SUBSIDIARIES(INVESTMENT ENTITIES)19A INTERESTS IN JOINT ARRANGEMENTS AND ASSOCIATES20 Nature,extent and financial effects of an entity’s interests in jointarrangements and associates21 Risks associated with an entity’s interests in joint ventures and associates23 INTERESTS IN UNCONSOLIDATED STRUCTURED ENTITIES24 Nature of interests26 Nature of risks29 APPENDICESA Defined termsB Application guidanceC Effective date and transitionD Amendments to other IFRSsFOR THE ACCOMPANYING DOCUMENTS LISTED BELOW,SEE PART B OF THIS EDITIONAPPROVAL BY THE BOARD OF IFRS12ISSUED IN MAY2011APPROVAL BY THE BOARD OF CONSOLIDATED FINANCIAL STATEMENTS,JOINT ARRANGEMENTS AND DISCLOSURE OF INTERESTS IN OTHERENTITIES:TRANSITION GUIDANCE(AMENDMENTS TO IFRS10,IFRS11ANDIFRS12)ISSUED IN JUNE2012APPROVAL BY THE BOARD OF INVESTMENT ENTITIES(AMENDMENTS TOIFRS10,IFRS12AND IAS27)ISSUED IN OCTOBER2012A506IFRS FoundationIFRS12 BASIS FOR CONCLUSIONSIFRS Foundation A507IFRS12International Financial Reporting Standard12Disclosure of Interests in Other Entities (IFRS12)is set out in paragraphs1–31and Appendices A–D.All the paragraphs have equal authority.Paragraphs in bold type state the main principles.Terms defined in Appendix A are in italics the first time they appear in the IFRS.Definitions of other terms are given in the Glossary for International Financial Reporting Standards.IFRS12 should be read in the context of its objective and the Basis for Conclusions,the Preface to International Financial Reporting Standards and the Conceptual Framework for Financial Reporting.IAS8Accounting Policies,Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.A508IFRS FoundationIFRS12 IntroductionIN1IFRS12Disclosure of Interests in Other Entities applies to entities that have an interest in a subsidiary,a joint arrangement,an associate or an unconsolidatedstructured entity.IN2The IFRS is effective for annual periods beginning on or after1January2013.Earlier application is permitted.Reasons for issuing the IFRSIN3Users of financial statements have consistently requested improvements to the disclosure of a reporting entity’s interests in other entities to help identify theprofit or loss and cash flows available to the reporting entity and determine thevalue of a current or future investment in the reporting entity.IN4They highlighted the need for better information about the subsidiaries that are consolidated,as well as an entity’s interests in joint arrangements and associatesthat are not consolidated but with which the entity has a special relationship.IN5The global financial crisis that started in2007also highlighted a lack of transparency about the risks to which a reporting entity was exposed from itsinvolvement with structured entities,including those that it had sponsored.IN6In response to input received from users and others,including the G20leaders and the Financial Stability Board,the Board decided to address in IFRS12theneed for improved disclosure of a reporting entity’s interests in other entitieswhen the reporting entity has a special relationship with those other entities.IN7The Board identified an opportunity to integrate and make consistent the disclosure requirements for subsidiaries,joint arrangements,associates andunconsolidated structured entities and present those requirements in a singleIFRS.The Board observed that the disclosure requirements of IAS27Consolidatedand Separate Financial Statements,IAS28Investments in Associates and IAS31Interestsin Joint Ventures overlapped in many areas.In addition,many commented thatthe disclosure requirements for interests in unconsolidated structured entitiesshould not be located in a consolidation standard.Therefore,the Boardconcluded that a combined disclosure standard for interests in other entitieswould make it easier to understand and apply the disclosure requirements forsubsidiaries,joint ventures,associates and unconsolidated structured entities. Main features of the IFRSIN8The IFRS requires an entity to disclose information that enables users of financial statements to evaluate:(a)the nature of,and risks associated with,its interests in other entities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.IFRS Foundation A509IFRS12General requirementsIN9The IFRS establishes disclosure objectives according to which an entity discloses information that enables users of its financial statements(a)to understand:(i)the significant judgements and assumptions(and changes tothose judgements and assumptions)made in determining thenature of its interest in another entity or arrangement(iecontrol,joint control or significant influence),and indetermining the type of joint arrangement in which it has aninterest;and(ii)the interest that non-controlling interests have in the group’sactivities and cash flows;and(b)to evaluate:(i)the nature and extent of significant restrictions on its ability toaccess or use assets,and settle liabilities,of the group;(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities;(iii)the nature and extent of its interests in unconsolidatedstructured entities,and the nature of,and changes in,the risksassociated with those interests;(iv)the nature,extent and financial effects of its interests in jointarrangements and associates,and the nature of the risksassociated with those interests;(v)the consequences of changes in a parent’s ownership interest in asubsidiary that do not result in a loss of control;and(vi)the consequences of losing control of a subsidiary during thereporting period.IN10The IFRS specifies minimum disclosures that an entity must provide.If the minimum disclosures required by the IFRS are not sufficient to meet thedisclosure objective,an entity discloses whatever additional information isnecessary to meet that objective.IN11The IFRS requires an entity to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of therequirements in the IFRS.An entity shall aggregate or disaggregate disclosuresso that useful information is not obscured by either the inclusion of a largeamount of insignificant detail or the aggregation of items that have differentcharacteristics.IN12Investment Entities(Amendments to IFRS10,IFRS12and IAS27),issued in October 2012,introduced an exception to the principle in IFRS10Consolidated FinancialStatements that all subsidiaries shall be consolidated.The amendments define aninvestment entity and require a parent that is an investment entity to measureits investment in particular subsidiaries at fair value through profit or loss inaccordance with IFRS9Financial Instruments(or IAS39Financial Instruments: A510IFRS FoundationIFRS12Recognition and Measurement,if IFRS9has not yet been adopted)instead of consolidating those subsidiaries in its consolidated and separate financial statements.Consequently,the amendments also introduced new disclosure requirements for investment entities in this IFRS and IAS27Separate Financial Statements.IFRS Foundation A511IFRS12International Financial Reporting Standard12Disclosure of Interests in Other EntitiesObjective1The objective of this IFRS is to require an entity to disclose information that enables users of its financial statements to evaluate:(a)the nature of,and risks associated with,its interests in otherentities;and(b)the effects of those interests on its financial position,financialperformance and cash flows.Meeting the objective2To meet the objective in paragraph1,an entity shall disclose:(a)the significant judgements and assumptions it has made in determining:(i)the nature of its interest in another entity or arrangement;(ii)the type of joint arrangement in which it has an interest(paragraphs7–9);(iii)that it meets the definition of an investment entity,if applicable(paragraph9A);and(b)information about its interests in:(i)subsidiaries(paragraphs10–19);(ii)joint arrangements and associates(paragraphs20–23);and(iii)structured entities that are not controlled by the entity(unconsolidated structured entities)(paragraphs24–31).3If the disclosures required by this IFRS,together with disclosures required by other IFRSs,do not meet the objective in paragraph1,an entity shall disclosewhatever additional information is necessary to meet that objective.4An entity shall consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the requirements in thisIFRS.It shall aggregate or disaggregate disclosures so that useful information isnot obscured by either the inclusion of a large amount of insignificant detail orthe aggregation of items that have different characteristics(see paragraphsB2–B6).Scope5This IFRS shall be applied by an entity that has an interest in any of the following:(a)subsidiaries(b)joint arrangements(ie joint operations or joint ventures)A512IFRS FoundationIFRS12(c)associates(d)unconsolidated structured entities.6This IFRS does not apply to:(a)post-employment benefit plans or other long-term employee benefitplans to which IAS19Employee Benefits applies.(b)an entity’s separate financial statements to which IAS27SeparateFinancial Statements applies.However,if an entity has interests inunconsolidated structured entities and prepares separate financialstatements as its only financial statements,it shall apply therequirements in paragraphs24–31when preparing those separatefinancial statements.(c)an interest held by an entity that participates in,but does not have jointcontrol of,a joint arrangement unless that interest results in significantinfluence over the arrangement or is an interest in a structured entity.(d)an interest in another entity that is accounted for in accordance withIFRS9Financial Instruments.However,an entity shall apply this IFRS:(i)when that interest is an interest in an associate or a joint venturethat,in accordance with IAS28Investments in Associates and JointVentures,is measured at fair value through profit or loss;or(ii)when that interest is an interest in an unconsolidated structuredentity.Significant judgements and assumptions7An entity shall disclose information about significant judgements and assumptions it has made(and changes to those judgements andassumptions)in determining:(a)that it has control of another entity,ie an investee as described inparagraphs5and6of IFRS10Consolidated Financial Statements;(b)that it has joint control of an arrangement or significant influenceover another entity;and(c)the type of joint arrangement(ie joint operation or joint venture)when the arrangement has been structured through a separate vehicle.8The significant judgements and assumptions disclosed in accordance with paragraph7include those made by the entity when changes in facts andcircumstances are such that the conclusion about whether it has control,jointcontrol or significant influence changes during the reporting period.9To comply with paragraph7,an entity shall disclose,for example,significant judgements and assumptions made in determining that:(a)it does not control another entity even though it holds more than half ofthe voting rights of the other entity.(b)it controls another entity even though it holds less than half of thevoting rights of the other entity.IFRS Foundation A513IFRS12(c)it is an agent or a principal(see paragraphs B58–B72of IFRS10).(d)it does not have significant influence even though it holds20per cent ormore of the voting rights of another entity.(e)it has significant influence even though it holds less than20per cent ofthe voting rights of another entity.Investment entity status9A When a parent determines that it is an investment entity in accordance with paragraph27of IFRS10,the investment entity shall discloseinformation about significant judgements and assumptions it has made indetermining that it is an investment entity.If the investment entity does nothave one or more of the typical characteristics of an investment entity(seeparagraph28of IFRS10),it shall disclose its reasons for concluding that it isnevertheless an investment entity.9B When an entity becomes,or ceases to be,an investment entity,it shall disclose the change of investment entity status and the reasons for the change.Inaddition,an entity that becomes an investment entity shall disclose the effect ofthe change of status on the financial statements for the period presented,including:(a)the total fair value,as of the date of change of status,of the subsidiariesthat cease to be consolidated;(b)the total gain or loss,if any,calculated in accordance withparagraph B101of IFRS10;and(c)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in subsidiaries10An entity shall disclose information that enables users of its consolidated financial statements(a)to understand:(i)the composition of the group;and(ii)the interest that non-controlling interests have in thegroup’s activities and cash flows(paragraph12);and(b)to evaluate:(i)the nature and extent of significant restrictions on itsability to access or use assets,and settle liabilities,of thegroup(paragraph13);(ii)the nature of,and changes in,the risks associated with itsinterests in consolidated structured entities(paragraphs14–17);(iii)the consequences of changes in its ownership interest in asubsidiary that do not result in a loss of control(paragraph18);andA514IFRS FoundationIFRS12(iv)the consequences of losing control of a subsidiary duringthe reporting period(paragraph19).11When the financial statements of a subsidiary used in the preparation of consolidated financial statements are as of a date or for a period that is differentfrom that of the consolidated financial statements(see paragraphs B92and B93of IFRS10),an entity shall disclose:(a)the date of the end of the reporting period of the financial statements ofthat subsidiary;and(b)the reason for using a different date or period.The interest that non-controlling interests have in thegroup’s activities and cash flows12An entity shall disclose for each of its subsidiaries that have non-controlling interests that are material to the reporting entity:(a)the name of the subsidiary.(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary.(c)the proportion of ownership interests held by non-controlling interests.(d)the proportion of voting rights held by non-controlling interests,ifdifferent from the proportion of ownership interests held.(e)the profit or loss allocated to non-controlling interests of the subsidiaryduring the reporting period.(f)accumulated non-controlling interests of the subsidiary at the end of thereporting period.(g)summarised financial information about the subsidiary(seeparagraph B10).The nature and extent of significant restrictions13An entity shall disclose:(a)significant restrictions(eg statutory,contractual and regulatoryrestrictions)on its ability to access or use the assets and settle theliabilities of the group,such as:(i)those that restrict the ability of a parent or its subsidiaries totransfer cash or other assets to(or from)other entities within thegroup.(ii)guarantees or other requirements that may restrict dividendsand other capital distributions being paid,or loans and advancesbeing made or repaid,to(or from)other entities within thegroup.(b)the nature and extent to which protective rights of non-controllinginterests can significantly restrict the entity’s ability to access or use theassets and settle the liabilities of the group(such as when a parent isobliged to settle liabilities of a subsidiary before settling its ownIFRS Foundation A515IFRS12liabilities,or approval of non-controlling interests is required either toaccess the assets or to settle the liabilities of a subsidiary).(c)the carrying amounts in the consolidated financial statements of theassets and liabilities to which those restrictions apply.Nature of the risks associated with an entity’s interestsin consolidated structured entities14An entity shall disclose the terms of any contractual arrangements that could require the parent or its subsidiaries to provide financial support to aconsolidated structured entity,including events or circumstances that couldexpose the reporting entity to a loss(eg liquidity arrangements or credit ratingtriggers associated with obligations to purchase assets of the structured entity orprovide financial support).15If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to aconsolidated structured entity(eg purchasing assets of or instruments issued bythe structured entity),the entity shall disclose:(a)the type and amount of support provided,including situations in whichthe parent or its subsidiaries assisted the structured entity in obtainingfinancial support;and(b)the reasons for providing the support.16If during the reporting period a parent or any of its subsidiaries has,without having a contractual obligation to do so,provided financial or other support to apreviously unconsolidated structured entity and that provision of supportresulted in the entity controlling the structured entity,the entity shall disclosean explanation of the relevant factors in reaching that decision.17An entity shall disclose any current intentions to provide financial or other support to a consolidated structured entity,including intentions to assist thestructured entity in obtaining financial support.Consequences of changes in a parent’s ownershipinterest in a subsidiary that do not result in a loss ofcontrol18An entity shall present a schedule that shows the effects on the equity attributable to owners of the parent of any changes in its ownership interest in asubsidiary that do not result in a loss of control.Consequences of losing control of a subsidiary duringthe reporting period19An entity shall disclose the gain or loss,if any,calculated in accordance with paragraph25of IFRS10,and:(a)the portion of that gain or loss attributable to measuring any investmentretained in the former subsidiary at its fair value at the date whencontrol is lost;andA516IFRS FoundationIFRS12(b)the line item(s)in profit or loss in which the gain or loss is recognised(ifnot presented separately).Interests in unconsolidated subsidiaries(investment entities)19A An investment entity that,in accordance with IFRS10,is required to apply the exception to consolidation and instead account for its investment in a subsidiaryat fair value through profit or loss shall disclose that fact.19B For each unconsolidated subsidiary,an investment entity shall disclose:(a)the subsidiary’s name;(b)the principal place of business(and country of incorporation if differentfrom the principal place of business)of the subsidiary;and(c)the proportion of ownership interest held by the investment entity and,if different,the proportion of voting rights held.19C If an investment entity is the parent of another investment entity,the parent shall also provide the disclosures in19B(a)–(c)for investments that arecontrolled by its investment entity subsidiary.The disclosure may be providedby including,in the financial statements of the parent,the financial statementsof the subsidiary(or subsidiaries)that contain the above information.19D An investment entity shall disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements)on the ability of an unconsolidated subsidiary to transferfunds to the investment entity in the form of cash dividends or to repayloans or advances made to the unconsolidated subsidiary by theinvestment entity;and(b)any current commitments or intentions to provide financial or othersupport to an unconsolidated subsidiary,including commitments orintentions to assist the subsidiary in obtaining financial support.19E If,during the reporting period,an investment entity or any of its subsidiaries has,without having a contractual obligation to do so,provided financial orother support to an unconsolidated subsidiary(eg purchasing assets of,orinstruments issued by,the subsidiary or assisting the subsidiary in obtainingfinancial support),the entity shall disclose:(a)the type and amount of support provided to each unconsolidatedsubsidiary;and(b)the reasons for providing the support.19F An investment entity shall disclose the terms of any contractual arrangements that could require the entity or its unconsolidated subsidiaries to providefinancial support to an unconsolidated,controlled,structured entity,includingevents or circumstances that could expose the reporting entity to a loss(egliquidity arrangements or credit rating triggers associated with obligations topurchase assets of the structured entity or to provide financial support).IFRS Foundation A517IFRS1219G If during the reporting period an investment entity or any of its unconsolidated subsidiaries has,without having a contractual obligation to do so,providedfinancial or other support to an unconsolidated,structured entity that theinvestment entity did not control,and if that provision of support resulted inthe investment entity controlling the structured entity,the investment entityshall disclose an explanation of the relevant factors in reaching the decision toprovide that support.Interests in joint arrangements and associates20An entity shall disclose information that enables users of its financial statements to evaluate:(a)the nature,extent and financial effects of its interests in jointarrangements and associates,including the nature and effects of itscontractual relationship with the other investors with joint control of,or significant influence over,joint arrangements and associates(paragraphs21and22);and(b)the nature of,and changes in,the risks associated with its interestsin joint ventures and associates(paragraph23).Nature,extent and financial effects of an entity’sinterests in joint arrangements and associates21An entity shall disclose:(a)for each joint arrangement and associate that is material to thereporting entity:(i)the name of the joint arrangement or associate.(ii)the nature of the entity’s relationship with the joint arrangementor associate(by,for example,describing the nature of theactivities of the joint arrangement or associate and whether theyare strategic to the entity’s activities).(iii)the principal place of business(and country of incorporation,ifapplicable and different from the principal place of business)ofthe joint arrangement or associate.(iv)the proportion of ownership interest or participating share heldby the entity and,if different,the proportion of voting rightsheld(if applicable).(b)for each joint venture and associate that is material to the reportingentity:(i)whether the investment in the joint venture or associate ismeasured using the equity method or at fair value.(ii)summarised financial information about the joint venture orassociate as specified in paragraphs B12and B13.A518IFRS FoundationIFRS12(iii)if the joint venture or associate is accounted for using the equitymethod,the fair value of its investment in the joint venture orassociate,if there is a quoted market price for the investment.(c)financial information as specified in paragraph B16about the entity’sinvestments in joint ventures and associates that are not individuallymaterial:(i)in aggregate for all individually immaterial joint ventures and,separately,(ii)in aggregate for all individually immaterial associates.21A An investment entity need not provide the disclosures required by paragraphs21(b)–21(c).22An entity shall also disclose:(a)the nature and extent of any significant restrictions(eg resulting fromborrowing arrangements,regulatory requirements or contractualarrangements between investors with joint control of or significantinfluence over a joint venture or an associate)on the ability of jointventures or associates to transfer funds to the entity in the form of cashdividends,or to repay loans or advances made by the entity.(b)when the financial statements of a joint venture or associate used inapplying the equity method are as of a date or for a period that isdifferent from that of the entity:(i)the date of the end of the reporting period of the financialstatements of that joint venture or associate;and(ii)the reason for using a different date or period.(c)the unrecognised share of losses of a joint venture or associate,both forthe reporting period and cumulatively,if the entity has stoppedrecognising its share of losses of the joint venture or associate whenapplying the equity method.Risks associated with an entity’s interests in jointventures and associates23An entity shall disclose:(a)commitments that it has relating to its joint ventures separately fromthe amount of other commitments as specified in paragraphs B18–B20.(b)in accordance with IAS37Provisions,Contingent Liabilities and ContingentAssets,unless the probability of loss is remote,contingent liabilitiesincurred relating to its interests in joint ventures or associates(includingits share of contingent liabilities incurred jointly with other investorswith joint control of,or significant influence over,the joint ventures orassociates),separately from the amount of other contingent liabilities.IFRS Foundation A519。

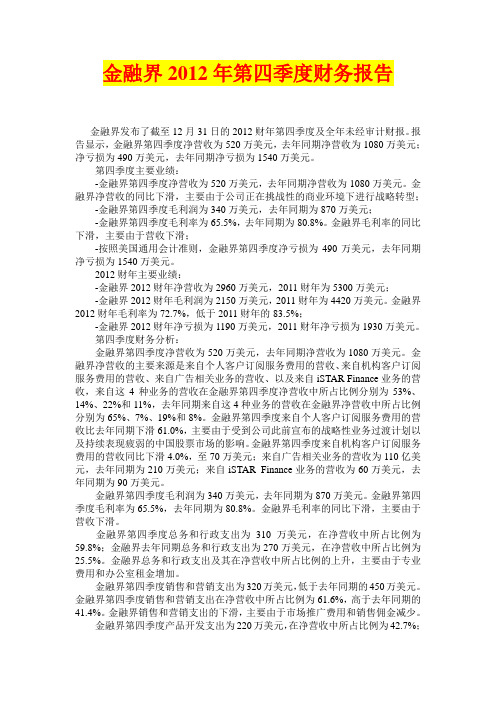

金融界2012年第四季度财务报告

金融界2012年第四季度财务报告金融界发布了截至12月31日的2012财年第四季度及全年未经审计财报。

报告显示,金融界第四季度净营收为520万美元,去年同期净营收为1080万美元;净亏损为490万美元,去年同期净亏损为1540万美元。

第四季度主要业绩:-金融界第四季度净营收为520万美元,去年同期净营收为1080万美元。

金融界净营收的同比下滑,主要由于公司正在挑战性的商业环境下进行战略转型;-金融界第四季度毛利润为340万美元,去年同期为870万美元;-金融界第四季度毛利率为65.5%,去年同期为80.8%。

金融界毛利率的同比下滑,主要由于营收下滑;-按照美国通用会计准则,金融界第四季度净亏损为490万美元,去年同期净亏损为1540万美元。

2012财年主要业绩:-金融界2012财年净营收为2960万美元,2011财年为5300万美元;-金融界2012财年毛利润为2150万美元,2011财年为4420万美元。

金融界2012财年毛利率为72.7%,低于2011财年的83.5%;-金融界2012财年净亏损为1190万美元,2011财年净亏损为1930万美元。

第四季度财务分析:金融界第四季度净营收为520万美元,去年同期净营收为1080万美元。

金融界净营收的主要来源是来自个人客户订阅服务费用的营收、来自机构客户订阅服务费用的营收、来自广告相关业务的营收、以及来自iSTAR Finance业务的营收,来自这4种业务的营收在金融界第四季度净营收中所占比例分别为53%、14%、22%和11%,去年同期来自这4种业务的营收在金融界净营收中所占比例分别为65%、7%、19%和8%。

金融界第四季度来自个人客户订阅服务费用的营收比去年同期下滑61.0%,主要由于受到公司此前宣布的战略性业务过渡计划以及持续表现疲弱的中国股票市场的影响。

金融界第四季度来自机构客户订阅服务费用的营收同比下滑4.0%,至70万美元;来自广告相关业务的营收为110亿美元,去年同期为210万美元;来自iSTAR Finance业务的营收为60万美元,去年同期为90万美元。

高级财务会计-第12章分部报告和中期财务报告

收入、利润或亏损、资产、 负债。

不包括递延所 得税负债

分部报告的 表达方式

企业编报分部的信息,可 用下述任何方式表达于 企业的财务报告中:

1、用固定的解释方式.

2、全部以报表附注的形 式表达.

3、作为报表中专门分列 表格表达.

会计差错的性质及其更

企业经营的季节性或者周期性特征。 存在控制关系的关联企业发生变化的情况,

关联方之间发生交易的,应当披露关联方 关系的性质、交易类型和交易要素。 合并财务报表的合并范围发生变化的情况。 对性质特别或者金额异常的财务报表项目 的说明。

证券发行、回购和偿还情况。

向所有者分配利润的情况,包括在中期内 实施的利润分配和已提出或者已批准但尚 未实施的利润分配情况。

另外,据上述计算结果,编报分部的营业收 入也应占汇总收入较大的比重,其重要的 标准是编报分部对外销售的数额应占企业 对外部销售收入额的75% 以 上.这种计算 应按每个财务报表编报期间确定.如果国 外的分部与国内产业基本 一致,也应作为 一个编报分部包括在计算之内(收入的比 重可由下面公式计算 得出.

分部报告按其报告的形式 分为主要报告形式和次要 报告形式。主要报告形式 需要披露详细信息,而次 要报告形式则只需披露简 略信息。

分类依据:企业的风险和报酬的主要来源方 式。

当企业的风险和报酬主要受产品和劳务差异 的影响,应以业务分部作为披露分部信息的 主要报告形式,以地区分部作为披露分部信 息的次要报告形式。

其他重大交易或者事项,包括重大的长期资产 转让及其出售情况、重 大的固定资产和无形资 产取得情况、重大的研究和开发支出、重大的 资产减值损 失情况等。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

二、财务报表列的基本要求:

——内容完整、数据真实、计算准确、编制及时 1. 企业应当以持续经营为基础。 2.遵循国家统一的会计准则规定的编制基础、编制 依据、编制原则和方法。

3. 财务报表项目的列报应当在各个会计期间保持一 致,不得随意变更,但下列情况除外:

① 会计准则要求改变财务报表项目的列报。 ② 企业经营业务的性质发生重大变化后,变更财务 报表项目的列报能够提供更可靠、更相关的会计信息。

7

资 产 负 债 表

8

二、金融资产和金融负债 允许抵销和不得抵销的要求 • 相互抵销的条件 P239

• 不得抵销的情形 P239-40

9

三、资产负债表的编制:

——编报之前,必须先结账

(一)排列规律

资产负债表的排列规律是:资产方按流动性 的大小排列,流动性大的排在前头,流动性小的 排在后头;权益方按偿还期的长短排列,偿还期 短的排在前头,偿还期长的排在后头,最后是不 用偿还的资本。

12

◆ 根据有关明细账科目的余额计算填列。

如“应付账款”项目,需要根据“应付账款” 和“预付账款”两个科目所属的相关明细科目的期 末贷方余额计算填列;“应收账款”项目,需要根 据“应收账款”和“预收账款”两个科目所属的相 关明细科目的期末借方余额计算填列。

13

第三节

(一)内容

利润表

一、利润表的内容及结构

3பைடு நூலகம்

4. 在编制的过程中,企业应当考虑项目的重要性。

(1)性质或功能不同的项目,一般应在财务报表中 单独列报。如“存货”与“固定资产”要单独列报。

(2)性质或功能类似的项目,一般可以合并列报。 如“原材料”与“低值易耗品”可以合并为“存货”。 (3)项目单独列报的原则不仅适用于报表,还适用 于附注。 (4)会计准则规定单独列报的,企业应当单独列报。

6

第二节 资产负债表

一、资产负债表的内容及结构

(一)内容:

反映企业在某一特定日期(月末、季末或年末)全 部的资产、负债和所有者权益情况的会计报表。 (二)结构:资产=负债+所有者权益 在我国,资产负债表采用账户式结构,报表分为左 右两方,左方列示资产各项目,反映全部资产的分布及 存在形态;右方列示负债和所有者权益各项目,反映全 部负债和所有者权益的内容及构成情况。

4

5. 财务报表项目金额间的相互抵销

财务报表中的资产项目和负债项目的金额不得相 互抵销;收入项目和费用项目的金额不得相互抵销;但 满足抵销条件的除外。下列情况,可以净额列示:

① 资产按扣除减值准备后的净额列示,不属于抵销。

② 非日常活动产生的损益,以收入扣减费用后的净 额列示,不属于抵销。

5

6. 比较信息的列报

11

◆ 根据总账科目的余额填列:直接填列或计算填列

资产负债表中的有些项目,可直接根据有关总账 科目的余额填列,如“交易性金融资产”、“短期借 款”、“应付票据”、“应付职工薪酬”等项目;有 些项目则需根据几个总账科目的余额计算填列如“货 币资金”项目,需根据“库存现金”、“银行存款”、 “其他货币资金”三个总账科目余额的合计数填列。

(一)上期余额:

根据上年该期利润表”本期金额“栏所列数字填列。

(二)本期余额:

根据损益类科目的本期发生额分析填列

三、利润表编制示例:

P245 例12-2、12-3

17

第十二章 财务报告

● 本章重点与学习方法

1. 财务报表的含义及种类

2. 资产负债表、利润表、现金流量表、所有者权 益变动表的含义、格式及编制方法 3. 报表附注的作用、内容 ● 会编制会计报表

1

第一节

财务报告概述

一、财务报表的定义和构成

1. 财务报告,是指企业对外提供的反映企业某一 特定日期的财务状况和某一会计期间的经营成果、现 金流量等会计信息的文件。财务报告包括财务报表和 其他应当在财务报告中披露的相关信息和资料。 2. 财务报表至少应当包括下列组成部分: (1)资产负债表;(2)利润表;(3)现金流量表; (4)所有者权益(或股东权益,下同)变动表; (5)附注。

总括反映企业在一定期间经营成果和分配情况的报 表。根据收入-费用=利润,按顺序排列收入、费用和 利润项目,将同一会计期内收入与费用进行配比,以求 得本年利润。 (二)结构 常见的利润表结构——单步式与多步式 我国基本上采用多步式

14

单 步 式 利 润 表

15

多 步 式 利 润 表

16

二、利润表的填列方法:简单

P240:资产负债表填列方法

(二)资产负债表的填列方法

期末余额

根据总账科目余额填列 根据明细账余额计算填列 根据总账科目和明细账科目余额分析计算填列 根据有关科目余额减去其备抵科目余额后的净额填列 综合

期初余额:上年期末余额 三、资产负债表编制示例:

P241 例12-1、12-3

当期财务报表的列报,至少应当提供所有列报项 目上一可比会计期间的比较数据,以及与理解当期财 务报表相关的说明,但其他会计准则另有规定的除外。 7. 财务报表表首的列报要求:

编报企业的名称、编报的日期或期间、货币名称 和单位、个别报表还是合并报表

8. 报告期间: 会计年度自公历1月1日起至12月31日止 不等于“财务报告批准报出日(如 3.31)”