《非居民纳税人税收居民身份信息报告表(企业适用)》#优选.

《中华人民共和国非居民企业所得税年度纳税申报表(2019年版)》及填报说明.doc

六、实际应纳所得税额(28+29-30-31)

33

减:本年累计实际已缴纳的所得税额

34

七、本年应补(退)所得税额(32-33)

汇总纳税税款分配

35

主要机构、场所填报

本机构、场所本年应分摊所得税额(36+37+38)

36

其中:主要机构、场所直接分摊所得税额

37

主要机构、场所财政集中分配所得税额

38

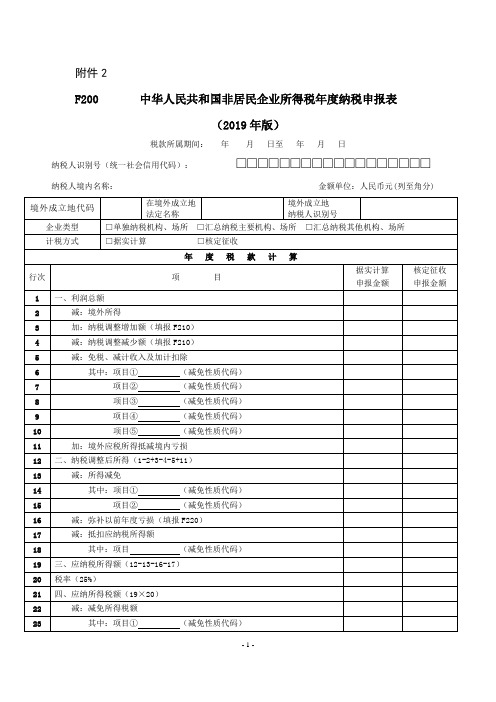

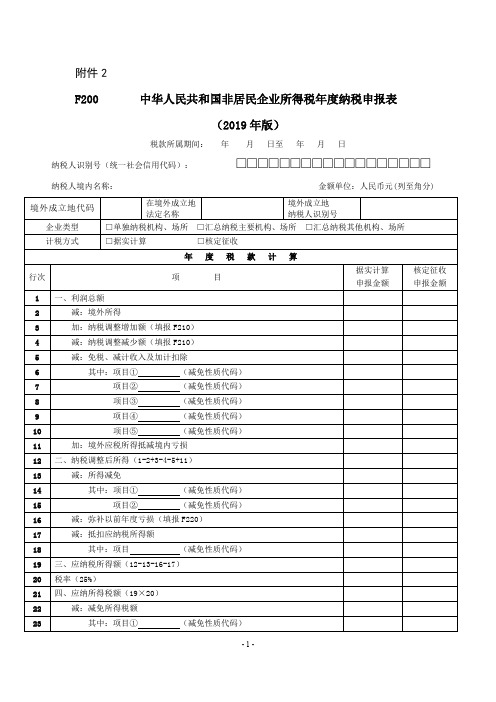

2.第1行“利润总额”:填报当期财务会计报表中的利润总额。

3.第2行“境外所得”:填报纳税人当期取得的发生在境外但与境内机构、场所有实际联系的所得数额。当期为境外盈利的,以正数表示;当期为境外亏损的,以负数表示。

4.第3行“纳税调整增加额”:填报纳税人会计处理与税收规定不一致,进行纳税调整增加的数额。本行根据《纳税调整项目明细表》(表F210)“调增数额”列填报。

行次

项目

据实计算

申报金额

核定征收

申报金额

1

一、利润总额

2

减:境外所得

3

加:纳税调整增加额(填报F210)

4

减:纳税调整减少额(填报F210)

5

减:免税、减计收入及加计扣除

6

其中:项目①(减免性质代码)

7

项目②(减免性质代码)

8

项目③(减免性质代码)

9

项目④(减免性质代码)

10

项目⑤(减免性质代码)

11

主要机构、场所从事主体生产经营业务分摊所得税额

39

减:本机构、场所本年累计实际已缴纳的所得税额

40

本机构、场所本年应补(退)所得税额(35-39)

41

其他机构、场所填报

《非居民纳税人享受协定待遇信息报告表》(附填表说明)

【分类索引】 业务部门 国际税务司 业务类别 自主办理事项 表单类型 纳税人填报 设置依据(表单来源) 政策规定表单 【政策依据】 《国家税务总局关于发布<非居民纳税人享受协定待遇管理办法>的公告》(国家税务总局公告2019年第35号) 【表单】

contracting jurisdiction to prove the residence status of

non-resident taxpayer for the year or its previous year during which

the payment is received

14.享受协定待遇所得金额 Amount of the income with respect to which tax treaty benefits are claimed

11.享受协定名称 The applicable treaty

8.在居民国(地区) 的联系电话 Telephone number in resident jurisdiction 10.电子邮箱 E-mail address 12.适用协定条款名 称 Applicable articles of the treaty

17.我谨声明:根据缔约对方法律法规和税收协定居民条款,我为缔约对方税收居民,相关安排 和交易的主要目的不是为了获取税收协定待遇。我自行判断符合协定待遇条件,自行享受协定待 遇,承担相应法律责任。我将按规定归集和留存相关资料备查,接受税务机关后续管理。 I hereby declare: According to the laws, regulations of the other contracting jurisdiction and the article of resident of the tax treaty, I am a resident of the other contracting jurisdiction, the principal purpose of the relevant arrangement and transaction is not to obtain tax treaty benefits. Through self-assessment, I believe that I am in conformity with the conditions for claiming tax treaty benefits, so I will enjoy tax treaty benefits. Therefore, I take due legal responsibilities. I will collect and retain relevant materials for review in accordance with the regulations, and accept the follow-up administration of the tax authority.

非居民纳税人享受税收协定待遇情况报告表(企业所得税B表)

(4)作业(包括试运行 作业)全部结束交付使用 日期或预计结束日期

The date of delivery of all the work (including trial work) or the estimated ending date

第 2 页,共 7 页

4.工程项目分包情况 Project subcontract information

1.非居民纳税人在中国从事工程具体类型(可多选) Types of projects engaged by non-resident taxpayer in China (multiple choices) □ 建筑工地 Building site □ 建筑、装配或安装工程 Construction, assembly or installation project □ 与建筑、装配或安装工程有关的监督管理活动 Supervisory activities in connection with construction, assembly or installation project □ 与建筑、装配或安装工程有关的咨询活动 Consultancy activities in connection with construction, assembly or installation project □ 其他 Others

2.工程项目名称 Name of project

工程项目地点 Location of project

工程项目总承包商名称 Name of general contractor

3.非居民纳税人在境内从事建筑、装配或安装工程,或相关监督管理活动时间情况 Time of construction, assembly or installation project or relevant supervisory activities by non-resident taxpayer in China

向非居民企业支付股息、红利的税收政策

向非居民企业支付股息、红利的税收政策根据《企业所得税法实施条例》第十七条规定,《企业所得税法》第六条第四项所称股息、红利等权益性投资收益,是指企业因权益性投资从被投资方取得的收入。

股息、红利等权益性投资收益,除国务院财政、税务主管部门另有规定外,按照被投资方作出利润分配决定的日期确认收入的实现。

第一:非居民企业取得的被投资企业在2008年以前实现的税后利润分红,不缴纳企业所得税。

《财政部、国家税务总局关于企业所得税若干优惠政策的通知》(财税〔2008〕1号)第四条规定,2008年1月1日以前外商投资企业形成的累积未分配利润,在2008年以后分配给外国投资者的,免征企业所得税。

2008年及以后年度外商投资企业新增利润分配给外国投资者的,依法缴纳企业所得税。

第二:2008年新《企业所得税法》实施后,非居民企业取得的分红需要按10%的税率缴税。

《企业所得税法》第三条第三款规定,非居民企业在中国境内未设立机构、场所的,或者虽设立机构、场所但取得的所得与其所设机构、场所没有实际联系的,应当就其来源于中国境内的所得缴纳企业所得税。

第四条第二款规定,非居民企业取得本法第三条第三款规定的所得,适用税率为20%。

第十九条规定,非居民企业取得股息、红利等权益性投资收益和利息、租金、特许权使用费所得,以收入全额为应纳税所得额。

《企业所得税法实施条例》第九十一条规定,非居民企业取得所得税法第三条第三项规定的所得,减按10%的税率征收企业所得税。

第三,虽然税法规定的税率是10%,但如果非居民企业所在国家或地区与我国签订有税收协定,协定的税率低于10%,则可以按协定的税率执行。

按照《内地和香港特别行政区关于对所得避免双重征税和防止偷漏税的安排》第十条第二款的规定,如果香港母公司持股比例超过25%,减按5%的优惠税率执行。

按照《中·澳(澳大利亚)税收协定》第十条的规定,所征税款不应超过股息总额的15%。

境外投资方要享受协定优惠税率,需向税务机关提交相关资料提出申请,经审查确认后才能享受;详细内容见《国家税务总局关于印发〈非居民享受税收协定待遇管理办法(试行)〉的通知》(国税发〔2009〕124号)。

非居民纳税人享受税收协定待遇情况报告表(企业所得税A表)

of the other contracting party, whether directly or indirectly

(3)□税收协定缔约对方政府直接或间接全部拥有资本的其他实体

Other entity with all its capital held by the government of the other tax treaty contracting party, whether directly or

which such guaranteed loans qualify for benefits under the terms of the treaty (3)□由税收协定缔约对方符合条件的政府或机构提供保险 Insurance is provided by a government or institution of the other tax treaty contracting party in circumstances in

□ 是 Yes □ 否 No

12.请简要描述据以产生特许权使用费所得的具体权利或财产。 Please give a brief description of the specific right or property from which the royalty income derives.

indirectly

(4)□其他公司

Other companies

(5)□合伙企业

Partnership enterprises

(6)□其他组织类型

请说明 Please specify:_____________________________________________

Other types of entity

非居民纳税人享受税收协定待遇情况报告表(企业所得税D表)

第 2 页,共 4 页

五、非居民纳税人取得同类所得及享受协定待遇情况 V. Income Received of the Same Type and Benefits Claimed under Tax Treaty or ITA by Non-resident Taxpayer 9.非居民纳税人近三年是否有来源于中国境内其他地区的同类所得? □是 Yes Has the non-resident taxpayer received any income of the same type sourced in other □否 No regions within China over the past three years? *10.非居民纳税人近三年是否就来源于中国境内其他地区的同类所得享受过协 定待遇? Has the non-resident taxpayer claimed treaty benefits for the income of the same type sourced in other regions within China over the past three years? □是 Yes □否 No

3.非居民纳税人所取得国际运输的附属活动收入是否超过总收入的10%? Does the income derived from activities affiliated to international transport by the non-resident taxpayer exceed 10% of the gross income? 4.运输线路及沿途停泊口岸情况 The situation of transport routes and ports of call alongside 序号 No. 航线 Transport routes

d31836daf08e4a2bb23a6549a85e0ff6

附件2F200 中华人民共和国非居民企业所得税年度纳税申报表(2019年版)税款所属期间:年月日至年月日纳税人识别号(统一社会信用代码):□□□□□□□□□□□□□□□□□□纳税人境内名称:金额单位:人民币元(列至角分)国家税务总局监制F200《中华人民共和国非居民企业所得税年度纳税申报表(2019年版)》填报说明一、适用范围本表及附表由办理年终汇算清缴所得税申报的非居民企业机构、场所(以下简称“纳税人”)填报。

在经营年度内无论盈利或者亏损,都应当按照有关规定报送本表和相关资料。

二、表头项目1.“税款所属期间”:填报税款所属年度的起止日期。

纳税人当年实际经营期间不足一个纳税年度的,填报当年实际经营期间的起止日期。

2.“纳税人识别号(统一社会信用代码)”:填报税务机关核发的纳税人识别号或有关部门核发的统一社会信用代码。

3.“纳税人境内名称”:填报营业执照、税务登记证等证件载明的纳税人名称。

三、有关项目填报说明(一)基本信息1.“境外成立地代码”:填报纳税人成立地国家(或地区)三字母代码(ISO 3166-1标准)。

2.“在境外成立地法定名称”:填报纳税人在其成立地国家(或地区)的法定名称。

3.“境外成立地纳税人识别号”:填报纳税人在其成立地国家(或地区)的纳税人识别号。

4.“企业类型”:纳税人根据情况勾选,填报人为单独申报纳税的非居民企业机构、场所的,勾选“单独纳税机构、场所”;填报人为汇总纳税非居民企业机构、场所中的主要机构、场所的,勾选“汇总纳税主要机构、场所”;填报人为汇总纳税非居民企业机构、场所中除主要机构、场所以外的其他机构、场所的,勾选“汇总纳税其他机构、场所”。

5. “计税方式”:纳税人根据情况勾选,据实申报纳税的填报人,勾选“据实计算”;采取核定征收方式申报纳税的填报人,勾选“核定征收”。

已经勾选“核定征收”的填报人,需要填报本表附表《非居民企业机构、场所核定计算明细表》(表F400)。

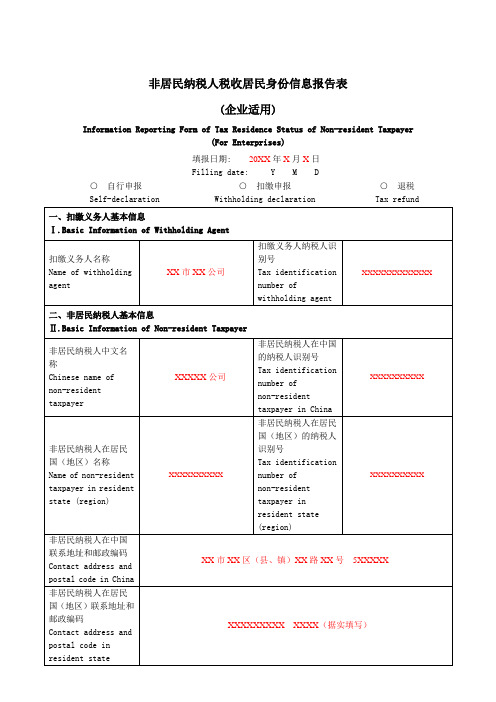

《非居民纳税人税收居民身份信息报告表(企业适用)》(填写示例)

非居民纳税人税收居民身份信息报告表(企业适用)Information Reporting Form of Tax Residence Status of Non-resident Taxpayer(For Enterprises)填报日期: 20XX年X月X日Filling date: Y M D○自行申报Self-declaration○扣缴申报Withholding declaration○退税Tax refund国家税务总局监制【表单说明】一、本表适用于需享受我国对外签署的避免双重征税协定(含与港澳避免双重征税安排)或国际运输协定待遇的企业所得税非居民纳税人。

I. This form is applicable to non-resident enterprise income taxpayer who claims tax benefits under a DoubleTaxation Agreement (DTA, including the DTAs with Hong Kong and Macau Special Administrative Regions) or International Transport Agreement signed by China.二、本表可用于自行申报或扣缴申报,也可用于非居民纳税人申请退税。

非居民纳税人自行申报享受协定待遇或申请退税的,应填写本表一式两份,一份在申报享受协定待遇或申请退税时交主管税务机关,一份由非居民纳税人留存;对非居民纳税人来源于中国的所得实施源泉扣缴或指定扣缴管理的,非居民纳税人如需享受协定待遇,应填写本表一式三份,一份交由扣缴义务人在扣缴申报时交主管税务机关,一份由扣缴义务人留存备查,一份由非居民纳税人留存。

II. This form can be used for self-declaration or withholding declaration, as well as for the non-resident taxpayer’s application for tax refund. The non-resident taxpayer initiating the self-declaration for claiming tax treaty benefits, or applying for tax refund, shall complete two copies of the form: one form is to be submitted to the in-charge tax authority at the time of such declaration or application, and the other form is to be kept by the non-resident taxpayer. Where the non-resident taxpayer’s China sourced income is subject to withholding tax, administered at source or by means of a designated withholding agent, and the non-resident taxpayer is entitled to tax treaty benefits, the non-resident taxpayer shall complete three copies of the form: one is to be given to the withholding agent to submit to the in-charge tax authority at the time of the withholding declaration, one is to be kept by the withholding agent and another is to be kept by the non-resident taxpayer.三、本表第一部分由扣缴义务人填写,如非居民纳税人自行申报纳税则无需填写。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

4.请简要说明非居民纳税人构成缔约对方税收居民的事实情况:

Please briefly describe the facts based on which the non-resident taxpayer qualifies as a tax resident of the other contracting party:

*12.非居民纳税人需享受的税收协定如包含“利益限制”条款或“享受协定优惠的资格判定”条款,请简要说明非居民纳税人是否符合相关条款要求。

If the treaty contains provisions of "Limitation on Benefits" or "Entitlement to Benefits", please briefly describe whether the non-resident taxpayer meets the requirements of these provisions.

非居民纳税人在中国联系地址和邮政编码

Contact address and postal code in China

非居民纳税人在居民国(地区)联系地址和邮政编码

Contact address and postal code in resident state (region)

非居民纳税人在中国的联系电话

五、备注

Ⅴ.Additional Notes

六、声明

Ⅵ.Declaration

我谨声明以上呈报事项真实、准确、无误。

I hereby declare that the information given above is true, accurate and error-free.

3.请引述非居民纳税人构成缔约对方税收居民的缔约对方国内法律依据:

Please cite the domestic legal basis based on which the non-resident taxpayer qualifies as a tax resident of the other contracting party:

非居民纳税人税收居民身份信息报告表

(企业适用)

Information Reporting Form of Tax Residence Status of Non-resident Taxpayer

(For Enterprises)

填报日期:年月日

Filling date: Y M D

○自行申报

Self-declaration

*9.享受税收协定股息、利息、特许权使用费、财产收益条款税收协定待遇的非居民纳税人,请填写直接或间接持有本企业权益额达到10%以上的股东情况(请全部列明)

For a non-resident enterprise claiming tax treaty benefits under the article of dividends, interest, royalties or capital gains, please provide information of all shareholders holding directly or indirectly at least 10 per cent of rights and interests of the enterprise.

□是Yes

□否No

7.非居民纳税人的注册地(国家或地区)

Place of registration (state or region)

非居民纳税人的实际管理机构所在地(国家或地区)

Place of effective management (state or region)

非居民纳税人的总机构所在地(国家或地区)

非居民企业已出示所在居民国税收居民身份证明

5.声明:

Declaration:

我谨声明,我为需享受税收协定缔约对方税收居民,我成为缔约对方税收居民并非为了获得税收协定利益而安排。

I hereby declare that I am a tax resident of the other contracting party to the tax treaty and the purpose of becoming such a tax resident is not to obtain the tax treaty benefits.

(4)

(5)

10.非居民纳税人从中国取得的所得在居民国(地区)纳税情况(限于列入税收协定适用范围的税种)

Information of taxes paid in the resident state (region) on the income derived from China by the non-resident taxpayer (for taxes covered by the tax treaty only)

1.非居民纳税人在缔约对方的组织类型

The organization type of the non-resident taxpayer in the other contracting party

□具有独立纳税地位的营利实体

Business entity with independent taxpayer status

Place of head office (state or region)

8.请简要说明非居民纳税人在居民国(地区)的主要经营活动内容。

Please briefly describe the main business activities of the non-resident taxpayer in the resident state (region).

税种名称

Name of tax

法定税率Statutory tax rate

享受居民国(地区)国内减免税优惠的法律依据及条文描述

Legal basis and provision description for the non-resident taxpayer to enjoy tax reduction or exemption in its resident state (region)

Telephone number in China

非居民纳税人在居民国(地区)的联系电话

Telephone number in resident state (region)

非居民纳税人的居民国(地区)

Resident state (region)

非居民纳税人享受税收协定名称

Name of the applicable tax treaty

(1)

(2)

(3)

11.根据第三国(地区)法律规定,非居民纳税人同时还构成哪些国家(地区)的税收居民(涉及多个国家或地区请全部列明)?

Does the non-resident taxpayer qualify as a tax resident of any other states (regions) based on the laws of such states (regions)? If yes, please specify the names of all such states (regions).

中日税收协定

三、扣缴义务人使用信息

Ⅲ.Information for Use by Withholding Agent据实勾选

提示:“税收居民”是指符合缔约国国内税法中对居民定义的人,包括企业和个人。如果非居民纳税人不是需享受税收协定缔约对方的税收居民,则不能享受税收协定待遇。

Note: The term "tax resident" means any person (e.g. an enterprise or individual) who, under the domestic tax law of a contracting state to the tax treaty, shall be regarded as a resident. If the non-resident taxpayer is not a resident of the other contracting party to the tax treaty, it shall not be entitled to the treatment under the tax treaty.

二、非居民纳税人基本信息必填

Ⅱ.Basic Information of Non-resident Taxpayer

非居民纳税人中文名称

Chinese name of non-resident taxpayer

非居民纳税人在中国的纳税人识别号

Tax identification number of non-resident taxpayer in China

The Enterprise Income Tax Law prescribes that a resident enterprise refers to an enterprise that is established within the territory of China pursuant to Chinese laws or an enterprise that is established within the territory of another country or region pursuant to that country or that region's laws whose place of effective management is located in China. According to such provision, is the taxpayer a tax resident of China?