ACCT-8Property Inspection

FrequentlyUsedAcctCodes常用的科目代码

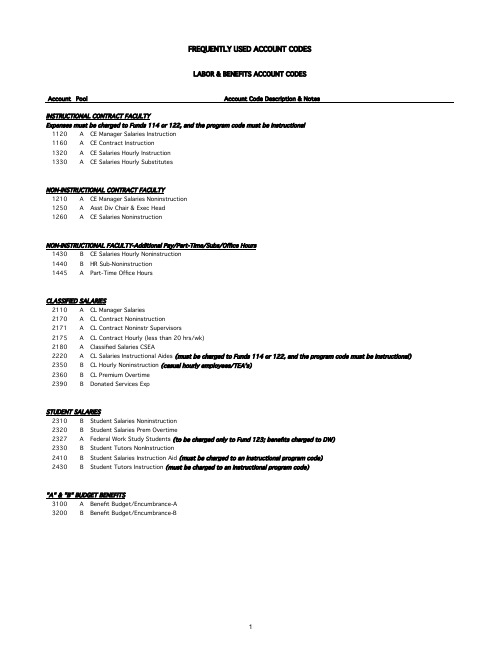

FREQUENTLY USED ACCOUNT CODESLABOR & BENEFITS ACCOUNT CODESAccount Pool Account Code Description & NotesINSTRUCTIONAL CONTRACT FACULTYExpenses must be charged to Funds 114 or 122, and the program code must be instructional1120A CE Manager Salaries Instruction1160A CE Contract Instruction1320A CE Salaries Hourly Instruction1330A CE Salaries Hourly SubstitutesNON-INSTRUCTIONAL CONTRACT FACULTY1210A CE Manager Salaries Noninstruction1250A Asst Div Chair & Exec Head1260A CE Salaries NoninstructionNON-INSTRUCTIONAL FACULTY-Additional Pay/Part-Time/Subs/Office Hours1430B CE Salaries Hourly Noninstruction1440B HR Sub-Noninstruction1445A Part-Time Office HoursCLASSIFIED SALARIES2110A CL Manager Salaries2170A CL Contract Noninstruction2171A CL Contract Noninstr Supervisors2175A CL Contract Hourly (less than 20 hrs/wk)2180A Classified Salaries CSEA2220A CL Salaries Instructional Aides (must be charged to Funds 114 or 122, and the program code must be instructional) 2350B CL Hourly Noninstruction (casual hourly employees/TEA's)2360B CL Premium Overtime2390B Donated Services ExpSTUDENT SALARIES2310B Student Salaries Noninstruction2320B Student Salaries Prem Overtime2327A Federal Work Study Students (to be charged only to Fund 123; benefits charged to DW)2330B Student Tutors NonInstruction2410B Student Salaries Instruction Aid (must be charged to an instructional program code)2430B Student Tutors Instruction (must be charged to an instructional program code)"A" & "B" BUDGET BENEFITS3100A Benefit Budget/Encumbrance-A3200B Benefit Budget/Encumbrance-BEXPENSE ACCOUNT CODESAccount Pool Account Code Description & Notes Account Pool Account Code Description & Notes "POOL" ACCOUNT CODESTo be used only for budget purposes; expenses should not becharged to pool account codes2000B Classified Salaries Pool4000B Supplies and Materials Pool5000B Operating Expenses Pool6000B Capital Outlay PoolCHARGEBACK ACCOUNT CODESTo be used when invoicing or charging another department forgoods or services4061B Chargeback-Printing4063B Chargeback-Reprographics/Bookstore5061B Chargeback-Misc.5062B Chargeback-La Voz5063B Chargeback-Facilities Rental5065B Chargeback-Short Courses5066B Chargeback-Plant Services5067B Chargeback-Quarterly Permit5069B Chargeback-Daily Permit5073B Chargeback-Postage5074B Chargeback-Utilities5079B Chargeback-SecuritySUPPLIES & MISCELLANEOUS SUPPLIES & MISCELLANEOUS - INSTRUCTIONAL4005B Cleaning Supplies4025B Instructional Materials4006B Paper Supplies4026B Instructional Equip-Noncapital4010B Miscellaneous Supplies4050B Printing-Instructional Materials4011B Fine Arts Production Supply4084B A/V Instructional Materials4012B Library Supplies4013B Promotional Items4014B Library Materials Noncapital4015B Food Supplies4016B Graphic Supplies4017B Photo Supplies4018B Testing Materials4020B Books-Capital4030B Periodicals4040B Firearms/Ammunition4041B Vehicle Supplies4042B Safety Supplies4060B Printing-General4065B Printing-Events CA4070B Gasoline & Oil4080B Lighting Supplies4085B A/V Materials4090B Parts & Accessories4095B Clothing/Uniforms4900B Procure Card ChargesOPERATING EXPENSES OPERATING EXPENSES - INSTRUCTIONAL502C B Commissioning Agent5101B Instructional Equip A.V.-Repair 5030B Dues and Memberships5112B Instructional Equip Science-Maint 5040B Claims Expense5113B Instructional Equip Science-Repair 5042B Attorney Fees5116B Instructional Equip Other-Maint 5045B Insurance-All Risk5117B Instructional Equip Other-Repair 5050B Insurance-Student Accident5051B Insurance-Foreign Student Man5055B Insurance-Student5056B Loss Prevention5060B Vehicle Repair5201B Architect & Design5202B Inspection5203B Capital Project Testing5204B Construction Management5205B Blueprints5206B Soil Investigations5207B Capital Project Consultants5208B Publication Distribution5209B Plant Service Contract Services (to be used only byPlant Services accountants)5211B Delivery Services5212B Modeling Services5213B Referees5214B Technical & Professional Services5215B Short Course Instruction5216B Fine Arts Production5217B Campus Security-Special Events5218B Admin Expenses5220B Temporary Services5223B Stipend Payments5225B Med Tests Consultant5226B Fingerprinting-DOJ5227B Fingerprinting-Processing Fee5228B Operational Moving Expense5229B Fingerprinting-FBI522C B Waterproofing Test/Inspect Roofing5230B Criminal Justice Database5231B Blueprint Reimbursement5232B Police Recruit Tests5233B Network Expense-Fund 765235B Lab Tests5237B ETS Standards Gen OH5238B EIR Fees5239B DSA Fees5241B Labor Compliance5244B Master Plan Expenses5245B Dispatch Communities Services5250B Custodial Expense5251B NSF Participant Support5252B NSF Subawards5260B Scholarships5261B Sponsorship5270B Program Management General OH5271B Construction/Design Management Fees5310B Equipment Rental/Lease5311B Trailer Rental5312B Computer Maintenance & Repair5315B Software Maintenance & RepairOPERATING EXPENSES (continued)5335B Donated Facilities Expense5340B Facilities Rental-Short Term 5341B Facilities Maintenance5350B Equipment Maintenance & Repair 5355B Building Maintenance5509B International Conference & Travel 5510B Domestic Conference & Travel 5512B Local Mileage5520B Field Trips5521B Host Foreign Students5621B Data Lines5624B Phone-Discretionary5630B Laundry & Dry Clean5710B Periodical & Book Bind5725B Training/Retraining Negot5730B Recruit Advertising5731B TB Exam5735B Postage & Mailing5738B Reimb Travel 2nd Int5740B Inservice Training Expense5741B Tuition Reimbursement5745B Advertising5746B P/R-Promotion5747B Classified Advertising5755B Litigation Expense-Fund 76 5775B Election Expense5790B Unrealized Hold Gain/Loss5792B Stewardship5793B Special Event Expense5903B Inventory Adjustments5905B Royalty Expense5907B Bank Service Charge5908B License Fees5909B Replacement Card Fee5910B Cash Over & Short5911B PARS Admin Fees5912B Freight Out5913B Misc Fees5914B Bad Debts5920B Security5921B Leed Expense-fund 765922B Misc Operating Expenses5923B Reimbursement Expense5924B Project Design5925B Project Containment5926B Project Display5930B Fundraising Expense5934B Volunteer Expense5936B Awards5940B HonorariumCAPITAL OUTLAY CAPITAL OUTLAY - INSTRUCTIONAL Minor - $1,000-$5,000Major - greater than $5,0006410B FH-CS Minor Computer Software6421B Minor-Instr Equip Replace 6411B DA Minor Computer Software6423B Minor-Instr Equipment 6420B Minor Cap-Equipment6425B Minor-Radio Equipment6430B Minor-Cap Equip Replace6461B FH-CS Minor Computer and Printer6462B DA Minor Computer and Printer6467B Minor Servers6470B Minor Multimedia and AV Equipment6480B Minor Network & Telephone Equipment6610B FH-CS Major Computer Software6611B DA Major Computer Software6620B Major-Cap Equipment6630B Major-Cap Equipment Replace6661B FH-CS Major Computer and Printer6662B DA Major Computer and Printer6667B Major Servers6670B Major Multimedia and AV Equipment6680B Major Network & Telephone EquipmentSTUDENT GRANTS IN AID7520B Student Grant In Aid7530B Student Grant In Aid-Books/OtherREVENUE ACCOUNT CODES• Income received from outside sources (ie. federal grants, state apportionment, sales or services provided to companies or organizations) are correctly posted to revenue account codes.• Purchase rebates are not considered revenue - they are offsets, or reductions, to expense - and should be credited to the account code that was originally charged.• When one department invoices another department for services provided, this is considered a chargeback. Paperwork should be sent to the campus budget analyst or to district accounting for processing.• Expenses should not be charged to revenue account codes.•The program code to be used with revenue account codes is always 900000.Account Account Code Description & Notes Account Account Code Description & NotesREVENUE - FEDERAL REVENUE - LOCAL8120Higher Education Act8711Parent Fees-Non Cert8121WIA8712Parent Fees8122TAA/NAFTA8721FH Enrollment-Regular8125TANF (50/Federal)8722DA Enrollment-Regular8140Administrative Allowance8723FH Enrollment Waived8150Vocational Ed Act8724DA Enrollment Waived8190Fed Food Reimburse8731Transcripts-Rush8191Title III8732Transcripts-Regular8192Asian American and Pacific8741FH Non-Res Tuition8193NASA Ames8742DA Non-Res Tuition8195NSF8751Parking-Quarterly Decal8198Veterans Report Fee8752Parking-Daily Permit8199Other Federal Revenue8753Parking-Special Events8754Parking-Daily Supplement8755Parking-Annual DecalREVENUE - STATE8811Secured Property Taxes8610Apportionment Apprenticeships8812Unsecured Property Taxes8611Apportionment General8814Property Taxes SB8138612Prior Year General Apportionment8816ERAF Revenues8613Apportionment-B.O.G.8817 D.S. Tax Revenue8614Part Time Faculty Equity8818RDA-Facilities Amount8616Equalization8819Donated Operating Revenue8620EOPS8820Donations8621Apportionment-Special Ed8821Local Grant Contract8622TANF (50/State)8822Restricted Donations8623Calworks8823Endowment Donations8624TTIP/Telecom Revenue8824Donated Services Revenue8625Matriculation8825Donated Facilities Revenue8626Non Credit Matriculation8826Restricted Corporate Gifts8627AB1725 Staff Development8827Restricted Individual Gifts8628Staff Diversity8828Restricted Foundation Gifts8629Basic Skills8829Unrestricted Corporate Gifts8630BFAP8830Unrestricted Individual Gifts8631CARE8831Unrestricted Foundation Gifts8632Career Tech Ed8832Planned Gift8633Can/Articulation8833Car Donations8634Instructional Equipment8834Special Events8650Community College Construction Act8835Royalty-Foundation8651Hazardous Materials8836Foundation Processing Fee8652Scheduled Maintenance/Spec Rep8839Contract Services8656Economic Development8840Sales-Event Tickets8657State Grants8842Sales-Taxable8658State Contracts8843Sales-Surplus Items8670Homeowners Property Tax Relief8844Sales-Nontaxable8672Timber Yield Tax8845Sales Discounts8680State Lottery8846Commissions8681State Mandated Costs8847Sales-Printed Materials8690Child Development Center Bailout8848Sales-Class Schedule8691State Meal Reimbursement8849Other Nontaxable Revenue8699Other State Revenues8850Facilities Rental• Income received from outside sources (ie. federal grants, state apportionment, sales or services provided to companies or organizations) are correctly posted to revenue account codes.• Purchase rebates are not considered revenue - they are offsets, or reductions, to expense - and should be credited to the account code that was originally charged.• When one department invoices another department for services provided, this is considered a chargeback. Paperwork should be sent to the campus budget analyst or to district accounting for processing.• Expenses should not be charged to revenue account codes.•The program code to be used with revenue account codes is always 900000.Account Account Code Description & Notes Account Account Code Description & NotesREVENUE - LOCAL (continued)8860Interest Income8861Tran Interest Income8865Tran Premium Revenue8867Other Investment Revenue8871Child Development Services8872Short Courses8874Enrollment Fee Revenue8875Field Trip Revenue8876Health Services Fees8877Material Fees8879Student Records8880Non-Resident Tuition8881Parking Revenue8882Fingerprinting Fees8883Campus Center Use Fees8884Registration Support Fee8885Fees, Other8886F1 Admissions Revenue8887Class Auditing8888Est. Active Benefit8889Est. Retiree Benefit8890Contribution-Employee8891Contribution-Retiree8892Contribution-PT Faculty8893Memberships8894Dept of Justice Fees8895FBI Fees8896Local Fingerprinting8897Misc. Admissions Rev8898Subscriptions8899Workshop Fees8900Library Fees8901Return Check Fees8902Other Local Revenue8903FH-Unclaimed Stud Rev8904DA-Unclaimed Stud Rev8906Parking Fines-FH8907Parking Fines-DA8908Library Fines8909Massages Fees8910Lost Book Fines8929Cashiering Exemption Clearing。

SpringBoot监控管理模块actuator没有权限的问题解决方法

SpringBoot监控管理模块actuator没有权限的问题解决⽅法SpringBoot 1.5.9 版本加⼊actuator依赖后,访问/beans 等敏感的信息时候报错,如下Tue Mar 07 21:18:57 GMT+08:00 2017There was an unexpected error (type=Unauthorized, status=401).Full authentication is required to access this resource.肯定是权限问题了。

有两种⽅式: 1.关闭权限:application.properties添加配置参数management.security.enabled=false2.添加权限(未测试):<dependency><groupId>org.springframework.boot</groupId><artifactId>spring-boot-starter-security</artifactId></dependency>在property中配置权限ID描述敏感(Sensitive)autoconfi g 显⽰⼀个auto-configuration的报告,该报告展⽰所有auto-configuration候选者及它们被应⽤或未被应⽤的原因truebeans显⽰⼀个应⽤中所有Spring Beans的完整列表true configprops显⽰⼀个所有@ConfigurationProperties的整理列表true dump执⾏⼀个线程转储true env暴露来⾃Spring ConfigurableEnvironment的属性truehealth 展⽰应⽤的健康信息(当使⽤⼀个未认证连接访问时显⽰⼀个简单的'status',使⽤认证连接访问则显⽰全部信息详情)falseinfo显⽰任意的应⽤信息falsemetrics展⽰当前应⽤的'指标'信息truemappings显⽰⼀个所有@RequestMapping路径的整理列表trueshutdown允许应⽤以优雅的⽅式关闭(默认情况下不启⽤)truetrace显⽰trace信息(默认为最新的⼀些HTTP请求)true总结以上所述是⼩编给⼤家介绍的SpringBoot 监控管理模块actuator没有权限的问题解决⽅法,希望对⼤家有所帮助,如果⼤家有任何疑问请给我留⾔,⼩编会及时回复⼤家的。

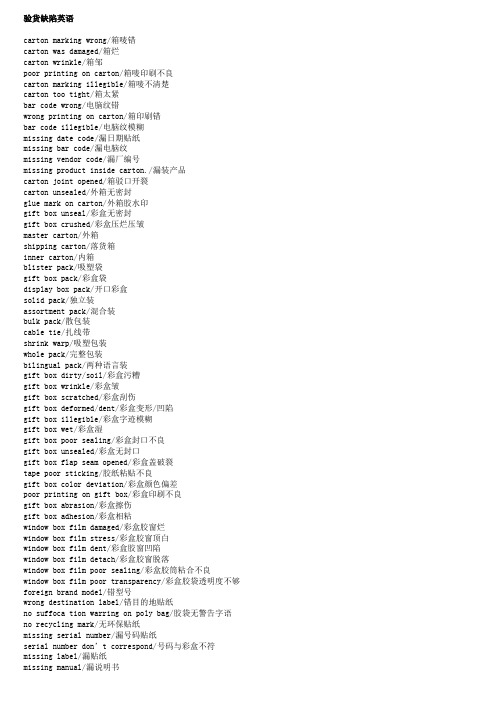

验货缺陷英语

验货缺陷英语carton marking wrong/箱唛错carton was damaged/箱烂carton wrinkle/箱邹poor printing on carton/箱唛印刷不良carton marking illegible/箱唛不清楚carton too tight/箱太紧bar code wrong/电脑纹错wrong printing on carton/箱印刷错bar code illegible/电脑纹模糊missing date code/漏日期贴纸missing bar code/漏电脑纹missing vendor code/漏厂编号missing product inside carton./漏装产品carton joint opened/箱驳口开裂carton unsealed/外箱无密封glue mark on carton/外箱胶水印gift box unseal/彩盒无密封gift box crushed/彩盒压烂压皱master carton/外箱shipping carton/落货箱inner carton/内箱blister pack/吸塑袋gift box pack/彩盒袋display box pack/开口彩盒solid pack/独立装assortment pack/混合装bulk pack/散包装cable tie/扎线带shrink warp/吸塑包装whole pack/完整包装bilingual pack/两种语言装gift box dirty/soil/彩盒污糟gift box wrinkle/彩盒皱gift box scratched/彩盒刮伤gift box deformed/dent/彩盒变形/凹陷gift box illegible/彩盒字迹模糊gift box wet/彩盒湿gift box poor sealing/彩盒封口不良gift box unsealed/彩盒无封口gift box flap seam opened/彩盒盖破裂tape poor sticking/胶纸粘贴不良gift box color deviation/彩盒颜色偏差poor printing on gift box/彩盒印刷不良gift box abrasion/彩盒擦伤gift box adhesion/彩盒相粘window box film damaged/彩盒胶窗烂window box film stress/彩盒胶窗顶白window box film dent/彩盒胶窗凹陷window box film detach/彩盒胶窗脱落window box film poor sealing/彩盒胶筒粘合不良window box film poor transparency/彩盒胶袋透明度不够foreign brand model/错型号wrong destination label/错目的地贴纸no suffoca tion warring on poly bag/胶袋无警告字语no recycling mark/无环保贴纸missing serial number/漏号码贴纸serial number don’t correspond/号码与彩盒不符missing label/漏贴纸missing manual/漏说明书missing accessories/漏附件gift box slightly damage/彩盒轻微损坏uneven coloring/颜色不平均illegible printing/印刷模糊wrong/missing coloring/错/漏颜色missing printing/漏印刷字句missing caution tags for transit漏搬运小心贴纸blister card was dirty/soil卡片是肮脏的/土壤insert(cardboakd)wrinkle 皱纹blister card damaged卡片损害blister card incorrect 备置卡片不正确的cardboard color deviationcardboard 彩色偏离shrinkage缩水deformed变形flash/gate remnantmatted无光泽flow line/stress mark夹水纹/顶白poor molding喷塑不良contamination mark混色,混料mark 痕迹,污点,标记colourized 混色color deviation 颜色偏差color mismatched 颜色不配合burnt mark 烧焦痕damaged 烂/损坏poor trimming 修整不良dull surface 哑色poor spraying 喷油不良over spraying 飞油paint under coverage油太薄paint chipped off脱油orange peel painting油面呈橙皮壮foreign painting染油poor re-painting touchup补油不良missing spraying漏喷油dirty on paint surface油面有尘点paint bubbles油泡paint color deviation油颜色偏差paint color mismatched喷油颜色不配合paint abrasion fail油漆被擦paint adhesion fail油漆被甩paint dirty油面污糟spraying scratched喷油刮花dull of paint surface喷油哑色paint matted/frayed喷油无光泽/磨损yellowish painting油面发黄paint peel off油面起皮spraying uneven喷油不整齐paint damped油漆不干paint abrasion甩油bubble冒泡,气泡uneven paint coverage 喷油厚薄,不均paint misregistration 错色poor coating油漆外层不良。

SafeCheck 8 安全检查器8说明书

This tester is ideal for use in the hire and service industry.SafeCheck8is a bench-mounted instrument for those who need a comprehensive tester memory which can provide result traceability.Operators can select one of the following tests from its clear user interface:Class I,Class Extension Power Cord.Equipment and tools are automatically sequenced through the test routine.The results are recorded, and information is displayed on a large clear LCD screen.SPECIFICATIONFlash/Hipot Test(Class I)Test Voltage Class l 1.25kV ACDisplay Range0.1-10mA ACResolution0.01mAAccuracy+/-5%+/-2digitsPass Levels selectable up to10mAFlash/Hipot Test(Class II)Test Voltage Class ll 2.5kV ACDisplay Range0.1-10mA AC.Resolution0.01mAAccuracy+/-5%+/-2digitsPass Levels selectable up to10mADC Insulation TestTest Voltage500VDisplay Range0.1-99.99MΩAccuracy+/-5%+/-2digits(up to19.99MΩ) Earth/Ground Bond TestTest Voltage6V AC(open circuit)Test Current25A,10A,4A,100mA AC into short circuit Range0.04Ω-20ΩResolution1mΩAccuracy+/-5%+/-2digitsPass Levels user selectableSubstitute Leakage(Short to Case Test)Test Voltage40V AC o/cDisplay Range0.1-20.0mA ACResolution0.01mAAccuracy+/-10%+/-2digits(1.00-20mA)Pass Levels selectable up to15mAEarth LeakageTest Voltage Mains SupplyDisplay Range0.1-20.0mA ACResolution0.01mAAccuracy+/-10%+/-2digits(1.00-20mA)Pass Levels selectable up to10mAPower/Run/Load TestsResolution0.01kVAMeasured Load0-4kVAAccuracy+/-10of reading,+/-2digits Optional ExtrasHardware194A922Barcode scanner312A912Desk Test n Tag printer3PHA Three phase adaptorSoftware352A910PATGuard Elite2-Premier352A920PATGuard Pro2-Professional 352A930PATGuard Lite2-Entry levelServicesService and CalibrationOrder NumberSC08UKSC08USASC08UKPackage Includes Test n Tag Printer and labelsSC08USAPackage Includes Test n Tag Printer and labelsIEC Power Cord Test Test Voltage 40V ACDetectsGood,Open,Short,ReversedADDITIONAL INFORMATION Mechanical Dimensions 450W x 410H x 155D mm Weight Approx 8.8kgElectricalSupply VoltageSelectable 115V /230V 50or 60Hz Operating Temperature 0°C to +40°C Storage Temperature -10°C to +50°CEN50191Compliant when used with appropriate accessories Supplied WithHT Probe3pin guard link connector Earth bond clip Mains leadInstruction ManualSafeCheck 8Solutions package for automation and traceability,includes:SafeCheck 8Desk Test n Tag printer Barcode Scanner 1000white labels PATGuard Lite 2CropicoHampton Road,Croydon,Surrey,United Kingdom,CR92RU T el:+44(0)2086844025Fax:+44(0)2086844094Web: Email:info@WORLD LEADERs IN SAFETY TEST AND MEASUREMENTG R O U PSEA W ARDPRECISION INSTRUMENTSCROPICOMEDICAL RIGELINDUSTRIAL SAFETY INSTRUMENTS CLAREPORTABLE ELECTRICAL SAFETY INSTRUMENTS SEA W ARD Seaward test and measurement companies include:。

灯具英文验货报告模板

灯具英文验货报告模板

1. 基本信息

•产品名称:

•产品型号:

•生产厂家:

•订单号:

•供货商名称:

2. 外观检查

•包装是否完好无损?

•外包装上的标签与订单信息是否一致?

•灯具有无明显损伤或变形?

•表面是否有砂眼、气孔、划痕等缺陷?

•护网和螺丝是否齐全,松动或缺失?

3. 功能检查

•按照产品说明书和安装说明进行组装和安装。

•是否符合安装要求,安装是否稳定。

•开启/关闭灯具的测试。

•改变灯具颜色和光强度的测试。

•开启/关闭遥控器的测试。

4. 其他检查

•接口测试(使用迫击炮和声光控制器进行测试)。

•配件齐全(说明书,遥控器等)。

•电气性能测试(电压、电流、功率因数等)。

•其他特殊要求测试(根据订单或客户需求)。

5. 结论

•该产品无明显缺陷。

•该产品部分存在缺陷,但不影响使用。

•该产品存在重大缺陷,不能正常使用。

6. 建议

•提出改进意见。

•反馈供货商和生产厂家问题。

•其他建议。

以上检查内容为常规要求,如有特殊要求,请在检查前和客户或订单那边进行确认。

PSC检查英语

第一章定义和常用缩略语一、定义1. Clear grounds: evidence that the ship, its equipment, or its crew does not correspond substantially with the requirements of the relevant conventions or that the master or crewmembers are not familiar with essential shipboard procedures relating to the safety of ships or the prevention of pollution.明显依据:船舶及其设备或其船员实质上不符合有关公约的要求的证据,或船长或船员不熟悉有关船舶安全或防止污染的船上基本程序的证据。

2. Deficiency: A condition found not to be in compliance with the requirements of the relevant convention.缺陷:发现的不符合有关公约要求的一种状况3. Detention: Intervention action taken by the port State when the condition of the ship or its crew does not correspond substantially with the applicable conventions to ensure that the ship will not sail until it can proceed to sea without presenting a danger to the ship or persons on board, or without presenting an unreasonable threat of harm to the marine environment.滞留:当船舶或船员实质上不符合适用公约要求时,港口国为保证该船舶只有在不会对船舶或船上人员构成危险或不会对海上环境造成损害威胁时方可开航所采取的干涉行动。

VCA810超强翻译版

VCA810高增益调节范围,宽带,可变增益放大器特点:1、高增益调节范围:±40分贝2、微分/单端输出3、低输入噪声电压:2.4nV/√Hz的4、恒定带宽与增益:达到35MHz5、较高的分贝/ V的增益线性度:±0.3分贝6、增益控制带宽:25MHz的7、低输出直流误差:<±40mv8、高输出电流:±60毫安9、低电源电流:24.8毫安(最大为-40° C至+85° C温度范围)应用:光接收器时间增益控制、声纳系统、电压可调主动滤波器、对数放大器、脉冲振幅补偿、带有RSSI的AGC接收机、改善更换为VCA610描述:VCA810是直流耦合,宽带,连续可变电压控制增益放大器。

它提供了差分输入单端输出转换,用来改变高阻抗的增益控制输入超过- 40DB增益至+40 dB的范围内成dB/ V的线性变化。

从±5V电源工作,将调整为VCA810的增益控制电压在0V输入- 40DB增益在-2V 输入到+40 dB。

增加地面以上的控制电压将衰减超过80dB的信号路径。

信号带宽和压摆率保持在整个增益的不断调整range.This40分贝/ V的增益控制精确到±1.5分贝(±0.9分贝高档),允许在一个AGC应用的增益控制电压为接收使用信号强度指示器(RSSI)的精度为±1.5分贝。

出色的共模抑制,并在两个高阻抗输入的共模输入范围,允许VCA810提供差分接收器的操作与增整。

以地为参考的输出信号。

零差分输入电压,给出了一个很小的直流偏移误差0V输出。

低输入噪声电压,确保在最高增益设置好输出信噪比。

在实际应用中,脉冲前沿的信息是至关重要的,和正在使用的VCA810,以平衡不同的信道损耗,群延迟变化最小增益设置将保留优秀的脉冲边沿信息。

一种改进的输出阶段提供足够的输出电流来驱动最苛刻的负载。

虽然主要用于驱动模拟到数字转换器(ADC)或第二阶段的放大器,±60毫安输出电流将轻松驱动双端接50Ω线或被动的后过滤超过±1.7V输出电压范围的阶段。

C-TPAP检查表(中英文对照)(免费)

工厂(车间)安全

b. Personnel Security?

个人安全

c. Subcontractor Security?

分包商安全

d. Conveyance/Transport Security?

运输安全

e. US Customs-Trade Partnership Against Terrorism (C-TPAT) Compliance?

工厂是否有ISO登记证,有请提供

a. Country of registration

登记的城市

b.Registration number

登记证号

c. Registrablished procedure to conduct periodic unannounced security checks to ensure that all of theabove security procedures are being performed properly?

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Property inspection

8.3 财产清查的方法

二、财产物资的清查方法

1.实物盘点法 适用范围广泛,如包装好的存货、固定资产等。 2.技术推算盘点法 主要适用于散装、大量成堆、难以清点的财产物资,如 矿产品、建筑用砂石、油罐等。 清查的结果可填制“盘存单”、“实存账存对比表”、 “积压变质报告单”

会计核算手续严密,要求对 财产物资的进出连续登记, 能及时反映各项财产物资的 收、发和结存情况,有利于 加强对财产物资的管理

核算工作量大

适用范围:通常企业的财产物资采用永续盘存制核算

8

Property inspection

8.3 财产清查的方法

实地盘存制( Periodic inventory system )

8

Property inspectiinspection

1 公司9月30日存入银行一张收到的转账支票36000元,银行尚未入帐 2 公司委托银行代收销货款31200元,银行已经入账,但公司尚未收到 收款通知 3 银行代付的电话费4000元,公司尚未收到付款通知 4 公司开出转账支票6400元,持票人尚未到银行办理转账 5 银行将公司存款户利息1600元记入公司存款户,公司尚未入账 6 公司银行存款日记账存在差错,多记入100元

8

Property inspection

8.3 财产清查的方法

三、货币资金的清查方法

(一)库存现金的清查

库存现金的清查是通过实地盘点,确定库存现金的实存 数,并与库存现金日记账的账面余额核对,查明盈亏情 况。清查时出纳员要在场,不允许用白条抵库。

8

Property inspection

8.3 财产清查的方法

8.2 财产清查的种类和准备工作

定期清查

是按预先计划安排的时间进行清查,一般是在年末、季 末、月末办理结账工作时进行的

不定期清查

主要包括:

(1)更换出纳员时对库存现金、银行存款所进行的清查; (2)更换仓库保管员时对其所保管的财产物资所进行的清查; (3)发生非常灾害和意外损失时,对受灾损失的财产所进行的清查; (4)其他特殊需要,必须进行清查时等。

营业外收入

营业外支出 管理费用

Non-operating Revenues

Non-operating Expenses Administrative Expenses

NI

NI NI

其他应收款

Other Receivables

A

8.4 财产清查结果的处理

财产清查中的主要业务 发生盘亏 区别不同原因处理盘亏 发生盘盈 区别不同原因处理盘盈

财产物资的减少没有经过严密 的会计核算手续,倒挤出的减 少数是建立在正常耗用的假定 基础之上的,无法揭示由于财 产物资的错发、毁损、盗窃、 丢失等非正常耗用引起的减少, 且只有月末盘点财产物资后才 能取得实存数和减少数资料, 不利于对财产物资的管理

适用范围:无法办理出库手续的小型企业、经营鲜活商品的 零售企业,或价值低且频繁发出的物资

8.4 财产清查结果的处理

8

Property inspection

8.4 财产清查的结果的处理

财产清查结果的处理步骤

核准 数字 查明 原因

调整 账簿

批准 后处 理

8

Property inspection

8.4 财产清查结果的处理

涉及的主要账户

待处理财产损溢 Property Gains and Losses of Suspense A 原材料 库存现金 Raw Materials Cash on Hand A A

请编制银行存款余额调节表。

358000

8

Property inspection

8.3 财产清查的方法

四、债权债务往来款项的清查方法 各项债权、债务等结算往来款项的清查是采用 发出函件查询核实的方法进行的。应编制“往 来款项对账单”“结算款项核对登记表” 。

8

Property inspection

Chapter8 Property inspection

【重点章节】

8.3 财产清查的方法

SKIP

8

Property inspection

Chapter8 Property inspection

8.1 财产清查的意义

8

Property inspection

8.1 财产清查的意义

财产清查是指通过对各种财产物资和库存现金的实 地盘点,对银行存款和债权债务的核对询证,确定 财产物资、货币资金和债权债务的实存数,并与账 存数核对,查明账实是否相符的一种会计核算的专 门方法。

8

Property inspection

8.3 财产清查的方法

银行存款余额调节表的编制方法

如果不存在记账错误,则经过调节后的双方余额应一致, 表示企业当时实际可以动用的款项;不需对未达账项进 行分录处理。

8

Property inspection

东方公司9月30日银行存款日记账余额为329300元,银行对账单余额为 328400元,经逐笔核对后,查明有以下账项:

1.保证账实相符,提高会计信息质量 2.促进企业改善经营管理

8

Property inspection

Chapter8 Property inspection

8.2 财产清查的种类和准备工作

8

Property inspection

8.2 财产清查的种类和准备工作

一、财产清查的种类

(一) 按照清查的范围分为全面清查和局部清查 (二)按照清查的时间分为定期清查和不定期清查

8

Property inspection

8.4 财产清查结果的处理

对于财产清查中债权、债务结算款项的处理,并不需要通 过“待处理财产损溢”账户,而是在原来账面记录的基础 上,按管理权限报经批准后,直接转账冲销债权或债务。 在年终财产清查中发现应收账款实际发生坏账损失2 000元。 在年终财产清查中发现长期无法支付的应付账款5 000元,核 实发现对方单位已解散,经批准销账。

也称为定期盘存制,是指平时只根据会计凭证在账簿中登记 财产物资的增加数,不登记减少数,月末需要对各项财产物 资进行盘点,根据实际盘点所确定的实存数,倒挤出本月财 产物资的减少数的方法。 本期减少额=账面期初余额+本期增加额-期末实际结存额

8

Property inspection

实地盘存制的优缺点

平时不需要登记财产物资的 减少情况,核算工作量小

8.4 财产清查结果的处理

在财产清查中,发现短缺机器一台,原价24 000元,已 提折旧16 000元。

在财产清查中,发现盘盈乙材料2吨,实际单位成本185 元,经查属于材料收发计量方面的错误。

8

Property inspection

8.4 财产清查结果的处理

新民企业进行库存现金清查,发现长款20元。 (1)批准处理前: (2)若经反复核查,应支付相关人员 (3)若经反复核查,属于无法查明的其他原因,批准处理

8

Property inspection

Chapter8 Property inspection

8.3 财产清查的方法

8

Property inspection

8.3 财产清查的方法

对于不同的项目采取不同的方法清查 (1)存货、固定资产等(清点) (2)库存现金和有价证券(清点) (3)银行存款、借款(核对) (4)应收款项、应付款项(核对)

Introduction to Financial Accounting

Chapter 8 Property Inspection

LIN TEACHER

2011 FALL

Introduction to Financial Accounting

第四部分 会计实务技术

CH6 会计凭证

CH7 会计账簿

CH8 财产清查

8

Property inspection

8.4 财产清查结果的处理

新民企业进行库存现金清查,发现短缺50元。 (1)批准处理前: (2)若经反复核查,属于出纳员的责任,应由出纳员赔偿 (3)若经反复核查,属于无法查明的其他原因,批准处理

8

Property inspection

8.4 财产清查结果的处理

8

Property inspection

8.2 财产清查的种类和准备工作

二、财产清查前的准备工作

1.清查小组制订清查工作计划,明确规定清查范围和工作进度; 2.会计部门应把截至清查日止全部有关会计凭证登记入账,结出总 账和相关明细账余额,并进行相互核对,做到账证相符、账账相 符,为财产清查提供可靠依据; 3.财产保管人员应将财产分类整理,悬挂标签注明财产名称、规格、 数量等,记好保管账卡,清查人员准备好经校正的计量仪器和必 要的凭证。

进行盘点,发现短缺产成品2件,单位成本700元。查明原因, 属于一般经营损失。 在财产清查中,发现甲材料毁损100吨,单位成本217元, 经查属于保管员过失造成的,应由其赔偿15 000元;毁损 材料残值5 000元;已办理入库手续;其余属一般经营损 失。 (假定不需考虑增值税)

8

Property inspection

三、货币资金的清查方法

现金盘点后,编制“库存现金盘点报告表”

(图片改编自:张捷 《基础会计》多媒体课件,2009)

8

Property inspection

8.3 财产清查的方法

(二)银行存款的清查 将企业的银行存款日记账与开户银行转来的对账单逐笔 进行核对。

不一致的原因?

1至少某一方记账有错误 2存在未达账项

账面期末余额=账面期初余额+本期增加额-本期减少额

8