外企审计报告中英文对照

审计报告英文版

XXXX ACCOUTANTS CO., LTD—————————————————————————————————No. (2012)0**AUDITOR’S REPORTWe have audited the accompanying balance sheet of ( the “Company”) as of Dec.31,2011, and the related cons olidated income statement for the 2011 then ended, and a summary of significant accounting policies and other expl anatory notes.1.Management’s Responsibility for the Financial StatementsThe management is responsible for the preparation and fair presentation of these financial st atements in accordance with the Accounting Standards for Business Enterprises and China Accou nting System for Business Enterprises. This responsibility includes: (1) designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial state ments that are free from material misstatement, whether due to fraud or error; (2) selecting and ap plying appropriate accounting policies; and (3) making accounting estimates that are reasonable i n the circumstances.2. Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit.We conducted our audit in accordance with the Standards on Auditing for Certified Public Accou ntants. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatementAn audit involves performing procedures to obtain audit evidence about the amounts and di sclosures in the financial statements. The procedures selected depend on the auditor’s judgment, i ncluding the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on thee ffectiveness of the entity’s internal control. An audit also includes evaluating the appropriatenessof accounting policies used and reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provi de a basis for our audit opinion.3. OpinionIn our opinion, the financial statements give a true and fair view of the financial position of the Company as of Dec.31, 2011, and of its financial performance for the 2011 years then ended in accordance with the Accounting Standards for Business Enterprises and China Accounting Syst em for Business Enterprises.Attachment: 1. Balance sheet of Dec.31, 20112. Income Statement and Profit Appropriation of 20113. Cash Flows Statement of 20114. Notes to Financial StatementCertified Public Accountant: ACCOUTANTS CO., LTDCertified Public Accountant:( City) ChinaTel: XX,XX,2012。

中英文对照的标准版审计报告

标准审计报告的参考格式Example of Standard Auditor’s Report审计报告Auditor’s ReportABC股份有限公司全体股东:To the shareholders of ABC Company Limited,我们审计了后附的ABC股份有限公司(以下简称ABC公司)财务报表,包括20×1年12月31日的资产负债表,20×1年度的利润表、股东权益变动表和现金流量表以及财务报表附注。

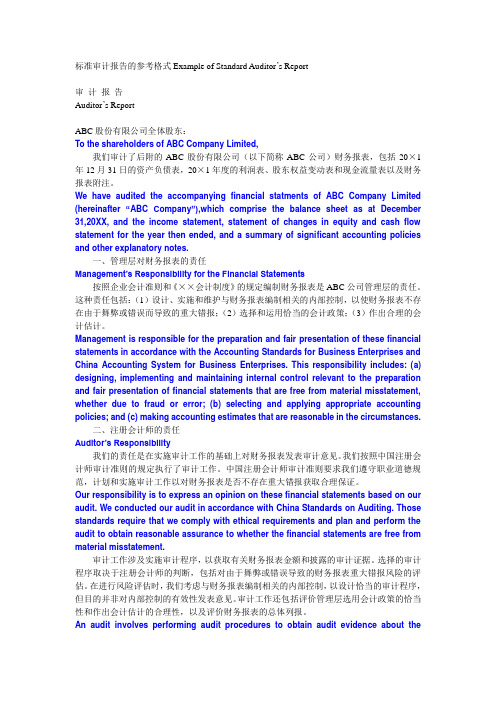

We have audited the accompanying financial statments of ABC Company Limited (hereinafter “ABC Company”),which comprise the balance sheet as at December 31,20XX, and the income statement, statement of changes in equity and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory notes.一、管理层对财务报表的责任Management’s Responsibility for the Financial Statements按照企业会计准则和《××会计制度》的规定编制财务报表是ABC公司管理层的责任。

这种责任包括:(1)设计、实施和维护与财务报表编制相关的内部控制,以使财务报表不存在由于舞弊或错误而导致的重大错报;(2)选择和运用恰当的会计政策;(3)作出合理的会计估计。

Management is responsible for the preparation and fair presentation of these financial statements in accordance with the Accounting Standards for Business Enterprises and China Accounting System for Business Enterprises. This responsibility includes: (a) designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; (b) selecting and applying appropriate accounting policies; and (c) making accounting estimates that are reasonable in the circumstances.二、注册会计师的责任Auditor’s Responsibility我们的责任是在实施审计工作的基础上对财务报表发表审计意见。

外企审计报告中英文对照

外企审计报告中英文对照(原创实用版)目录1.外企审计报告的概述2.外企审计报告中的主要内容3.外企审计报告的翻译技巧4.外企审计报告中英文对照的实践案例5.总结正文随着全球化的发展,越来越多的外企在中国开设分公司或代表处,因而审计报告的需求也日益增多。

对于外企来说,审计报告是公司财务状况的重要体现,也是公司治理的重要手段。

因此,外企审计报告的翻译质量直接影响到公司业务的顺利开展。

一、外企审计报告的概述外企审计报告是指由国际会计师事务所出具的,针对外商投资企业的财务报表和相关财务信息进行审核、核实和评价的书面文件。

一般来说,外企审计报告包括资产负债表、利润表、现金流量表和所有者权益变动表等。

二、外企审计报告中的主要内容外企审计报告的主要内容包括以下几个方面:1.对公司财务报表的审核:审计师会对公司财务报表进行详细审核,以确保财务报表的真实性、准确性和完整性。

2.对公司内部控制的评价:审计师会对公司的内部控制体系进行评价,以判断其是否有效。

3.对公司财务风险的评估:审计师会对公司的财务风险进行评估,以帮助公司及时发现和解决潜在的风险问题。

4.对公司业绩的评价:审计师会对公司的业绩进行评价,以帮助公司了解自身的经营状况,并制定相应的发展策略。

三、外企审计报告的翻译技巧外企审计报告的翻译要求准确、简洁、清晰。

在翻译过程中,需要注意以下几点:1.准确理解原文:在翻译之前,首先要对原文进行仔细阅读,以确保对原文的准确理解。

2.熟悉专业词汇:审计报告涉及很多专业词汇,如资产负债表、利润表等,需要熟悉这些词汇的英文表达。

3.注意语言风格:审计报告的语言风格要求正式、严谨,因此在翻译过程中要注意保持这种风格。

4.检查校对:翻译完成后,要对译文进行仔细检查,确保译文的准确性和流畅性。

四、外企审计报告中英文对照的实践案例以下是一个外企审计报告中英文对照的实践案例:【资产负债表】【审计报告】Audit ReportTo: Company NameRe: Financial Statements AuditThe purpose of this letter is to express our opinion on the financial statements of Company Name for the year ended December31, 2021.1.Assets and Liabilities:The balance sheet shows a total assets of $X, including $Y in cash and cash equivalents, $Z in receivables, $W in inventory, and $V in fixed assets.Total liabilities are $Y, including $Z in accounts payable, $W in accrued liabilities, and $V in long-term liabilities.The total shareholders" equity is $X.2.Income Statement:The income statement shows a total revenue of $X, including $Y in sales, $Z in interest income, and $W in other income.Total expenses are $Y, including $Z in cost of goods sold, $W in selling, general, and administrative expenses, and $V in interest income is $X.3.Cash Flow Statement:The cash flow statement shows a net increase in cash and cash equivalents of $X, including $Y in operating activities, $Z in investing activities, and $W in financing activities.4.Statement of Changes in Shareholders" Equity:The statement of changes in shareholders" equity shows an increase of $X, including $Y in net income, $Z in dividends declared, and $W in other comprehensive income.In our opinion, the financial statements present fairly, in all material respects, the financial position of Company Name as of December 31, 2021, and the results of its operations and its cash flows for the year then ended in conformity with accounting principles generally accepted in the United States of America.【结论】总之,外企审计报告的翻译对于准确反映公司的财务状况和业务运营具有重要作用。

外资企业中英文会计报表范本

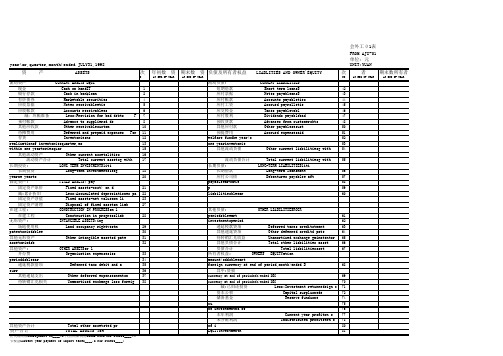

For the

year(or,quarter,month)ended JULY31,1998

行

资

产

ASSETS

L次INEN

O

流动资产

CURRENT ASSETS EQUI现金Cash on handIT

1

银行存款

Cash in bankloan

2

有价债券

Marketable securities

短期借款

Short term loansS

应付票据

Notes payableansS

应付帐款

Accounts payableties

应付工资

Accrued payrolletie

应交税金

Taxes payablevabl

应付股利

Dividends payablebad

预收货款

Advances from customersbts

payab一l年ee以ar上to的ri应e 付款项

Payable due after one yearentures 58

p 长期负债合计

Total long term

59

liabilitiesbleear

60

其他负筹债建:期间汇兑收益 OTHERExLcIhAaBnIgLeITgIaEiSnROdGuRring start-up

perio递d延sb投le资ea收rt益

Deferred gain on

61

investmentsperiod

62

递延税款贷项

Deferred taxes creditstment

63

其他递延贷项

Other deferred creditd pate

外企审计报告中英文对照

外企审计报告中英文对照摘要:1.外企审计报告的概述2.外企审计报告中英文对照的重要性3.外企审计报告中英文对照的实践4.外企审计报告中英文对照的挑战与解决方案5.结论正文:一、外企审计报告的概述外企审计报告是针对外资企业在我国进行的一系列经济活动和财务状况的审查,以确保企业的合规经营和财务数据的真实性。

外企审计报告通常包括对企业财务报表、内部控制、经营效益等方面的评估,并为企业提供改进建议。

二、外企审计报告中英文对照的重要性随着全球化的发展,越来越多的外资企业进入我国市场。

为了提高审计报告的国际化水平,满足国内外各方的阅读需求,外企审计报告中英文对照显得尤为重要。

这有助于增强审计报告的公信力,便于国内外企业、政府部门、投资者和其他利益相关者了解企业的经营状况。

三、外企审计报告中英文对照的实践在实际操作中,外企审计报告中英文对照需要遵循以下原则:1.保持内容的一致性:中英文对照的审计报告应确保内容一致,避免出现差异。

2.术语的统一性:在中英文对照过程中,应统一专业术语的翻译,以确保表达准确无误。

3.文本的可读性:中英文对照的审计报告应注重文本的可读性,方便读者阅读和理解。

四、外企审计报告中英文对照的挑战与解决方案1.挑战:外企审计报告中英文对照可能出现的挑战包括翻译质量、术语统一性、文本格式等。

2.解决方案:为了应对这些挑战,可以采取以下措施:(1) 加强翻译人员的培训和指导,提高翻译质量。

(2) 建立术语库,统一术语的翻译。

(3) 使用专业的翻译软件和工具,确保文本格式的一致性。

五、结论外企审计报告中英文对照是提高审计报告国际化水平的重要手段。

外企审计报告中英文对照

外企审计报告中英文对照(实用版)目录1.外企审计报告的概述2.外企审计报告中的主要内容3.外企审计报告的翻译技巧4.外企审计报告翻译的实践案例5.总结正文随着全球化的发展,越来越多的外企在中国开设分支机构,这就涉及到了审计报告的问题。

外企审计报告是对公司财务状况和经营情况的一种评估,它对于公司的运营和发展具有重要的指导意义。

同时,外企审计报告也是向外界展示公司透明度和公开透明的重要方式。

在外企审计报告中,主要包括以下几个方面:公司基本情况、财务报表、审计意见、审计依据、管理层对财务报表的责任等。

这些内容对于了解公司的财务状况、经营情况以及公司未来的发展方向都有着重要的参考价值。

对于外企审计报告的翻译,需要掌握一定的翻译技巧。

首先,需要对审计报告的内容进行全面了解,对于一些专业术语和行业惯例要有深入的理解。

其次,要注重语言的准确性和通顺性,确保翻译出来的审计报告能够让读者清晰地理解其含义。

最后,要注意格式和排版的美观性,保证翻译出来的审计报告整洁、易读。

以下是一个外企审计报告翻译的实践案例:原文:To the Shareholders of ABC Company:We have audited the accompanying financial statements of ABC Company as of December 31, 2021, and have issued our report thereon dated February 18, 2022.We conducted our audit in accordance with International Standards on Auditing (ISAs).Our audit opinion on the financial statements is as follows: The financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) and give a true and fair view of the financial position of the Company as at December 31, 2021, and its results of operations and cash flows for the year then ended.翻译:致 ABC 公司股东:我们已审计了截至 2021 年 12 月 31 日的 ABC 公司附带财务报表,并已于 2022 年 2 月 18 日发布了我们的审计报告。

英文审计报告(带中文翻译)

xx company limited

(a joint stock company incorporated in the xx with limited

liability)

we have audited the financial statements on pages 58 to 108 which

statements, and of whether the accounting policies are appropriate

to the company's circumstances, consistently applied and adequately

incorporation of the company) to xx and have been properly prepared

in accordance with the disclosure requirements of the hong kong

贵公司的董事负责编制真实与公平的财务报表。在编制该等真实与公平的财务报表时,董事必须选取并贯彻采用合适的会计政策。我们的责任乃根据我们审核工作的结果,对该等财务报表作出独立意见,并仅向贵公司全体股东报告我们的结论,及不作其它用途。我们并不就本报告的内容向任何其它人士负上责任或承担法律责任。

disclosed.

we planned and performed our audit so as to obtain all the

information and explanations which we considered necessary in order

for no other purpose. we do not assume responsibility towards or

审计报告中英文对照

最新审计报告中英文对照(转载)审计报告中英对照2008-12-27 13:38:21 阅读2557 评论5 字号:大中小订阅山西**联合会计师事务所ShanXi**Unite Accountant Office审计报告AUDITOR’S REPORT晋**审字(2007)第000**号Jin ** (2007) Audit No.00****铸造有限公司:To **foundry Co., Ltd:我们审计了后附的**铸造有限公司(以下简称贵公司)财务报表,包括2006年12月31 日的资产负债表,2006年度的利润表以及财务报表附注。

We have audited the accompanying balance sheet of ** foundry Co., Ltd (the “Company”) as of Dec.31,2006, and the related consolidated income statement for the 2006 then ended, and a summary of significant accounting policies and otherexplanatory notes.一、管理层对财务报表的责任1.Mana gement’s Responsibility for the Financial Statements按照企业会计准则和《企业会计制度》的规定编制财务报表是贵公司管理层的责任。

这种责任包括:(1)设计、实施和维护与财务报表编制相关的内部控制,以使财务报表不存在由于舞弊或错误而导致的重大错报:(2)选择和运用恰当的会计政策:(3)作出合理的会计估计。

The management is responsible for the preparation and fair presentation of these financial statements in accordance with the Accounting Standards for Business Enterprises and China Accounting System for Business Enterprises. This responsibility includes: (i) designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; (ii) selecting and applying appropriate accounting policies; and (iii) making accounting estimates that are reasonable in thecircumstances.二、注册会计师的责任2. Auditor’s Responsibility我们的责任是在实施审计工作的基础上对财务报表发表审计意见。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

外企审计报告中英文对照

摘要:

一、外企审计报告概述

1.外企审计报告的定义和作用

2.外企审计报告的基本要素

二、审计报告的编制与披露

1.审计报告的编制流程

2.审计报告的披露要求

三、审计报告的内容与结构

1.审计报告的封面及目录

2.审计报告的

正文:

外企审计报告是注册会计师事务所在完成对外企的财务报表审计后,出具的一份全面、明确、客观的书面文件。

它旨在为利益相关者提供关于被审计单位财务报表的公允性、合规性和有效性的独立意见。

本篇文章将对外企审计报告的概述、编制与披露、内容与结构、关键术语与概念以及英文表述进行详细阐述。

一、外企审计报告概述

外企审计报告,又称审计报告,是注册会计师在对企业的财务报表、经营状况以及内部控制等方面进行全面审计后,对其所出具的意见。

审计报告具有独立性、权威性和公信力,对于保障企业的财务信息质量、维护资本市场秩序

以及保护投资者利益具有重要意义。

二、审计报告的编制与披露

1.审计报告的编制流程:企业在年度财务报表审计前,需要与注册会计师事务所签订审计业务约定书,明确双方的权利和义务。

审计过程中,企业需配合会计师事务所提供所需的财务报表及支持性文件,以便审计人员顺利进行审计工作。

审计报告编制完成后,企业需对报告进行审阅并确认。

2.审计报告的披露要求:根据《企业会计准则》等相关法规,企业需在规定的时间和地点披露审计报告。

同时,企业还需将审计报告报送相关部门备案,如国家统计局、国家外汇管理局等。

三、审计报告的内容与结构

1.审计报告的封面及目录:审计报告的封面应包含报告名称、被审计单位名称、报告编号、报告日期等信息。

目录则需列明报告各部分的标题及页码。

2.审计报告的正文部分:

2.1 审计目的与范围:阐述审计的目的、范围及重点审计领域。

2.2 审计依据及方法:说明审计所依据的法规、准则及审计方法。

2.3 审计结果:描述审计过程中发现的问题、重大事项及对财务报表的影响。

2.4 审计意见:明确审计人员对财务报表的意见,包括无保留意见、保留意见、否定意见和无法表示意见等。

2.5 审计报告的日期和地点:报告完成的时间和地点。

四、审计报告中的关键术语与概念

1.财务报表:企业根据会计准则编制的反映企业财务状况、经营成果和现

金流量等信息的报表。

2.财务报表披露:企业对外披露的财务报表及相关解释说明。

3.审计风险:审计人员在审计过程中,因各种原因导致审计结论与实际情况存在差异的可能性。

4.内部控制:企业为保障财务报告的真实性、合规性和有效性,建立的一套内部控制制度。

5.审计证据:审计人员在对财务报表进行审计时所收集的、能够为审计结论提供依据的信息。

五、外企审计报告的英文表述

1.审计报告的基本结构与格式:英文审计报告的结构与中文审计报告相似,包括封面、目录、正文等部分。

在英文表述中,审计报告需遵循国际审计准则(ISA)及美国通用会计准则(GAAP)等相关规定。

2.审计报告中的专业术语翻译:英文审计报告中涉及的专业术语需进行准确翻译,如“财务报表”(financial statements)、“审计风险”(audit risk)等。

综上所述,外企审计报告作为企业财务报表的“体检报告”,对于企业的经营决策、投资者信心以及整个资本市场的稳定运行具有重要意义。