[经济学]兹维博迪金融学第二版课件Chapter

合集下载

兹维博迪金融学第二版课件

兹维博迪金融学第二版

20

1.5 企业的组织形式

• 独资企业

• 一个人或家庭所有的企业 • 企业的资产和负债是所有者个人的资产和负债 • 无限责任 • 低管理成本

兹维博迪金融学第二版

21

• 合伙企业

• 至少有两个人分享所有权的企业。合伙协议通常 规定如何共同作出决策和利润(损失)如何共享 (共担)。

兹维博迪金融学第二版

8

• 人们利用金融系统来实施其金融决策。金融系统定义为用来订立 金融合约、交换资产与风险的一组市场和其他机构。

兹维博迪金融学第二版

9

• 金融理论包括:

• 一组概念,帮助一个人组织关于怎样跨时配置资 源的思考。

• 一组数量模型,帮助评估备选项、决策和实施决 策。

• 这些概念和模型适用于所有层次和规模的决策

预防损失 • 不动产管理

兹维博迪金融学第二版

41

税务管理

• 税务政策、程序的建立和管理 • 与税收征稽机构的关系 • 税务报告的准备 • 税务计划

兹维博迪金融学第二版

Hale Waihona Puke 42投资者关系• 建立和维护与投资群体的关系 • 建立和维护与公司股东的关系 • 向分析师咨询—公共财务信息

兹维博迪金融学第二版

43

离

• 1.7 管理的目标 • 1.8 市场性管束:收购 • 1.9 财务专家在公司中的

角色

兹维博迪金融学第二版

6

导言

• 我为退休储蓄。我应该用哪一种投资形式? 银行存单、共同基金还是直接买股票?

• 我想有一辆新车。我应该用存款购买还是租用? • 我正在考虑创业。它能带给我足够的回报吗? • 公司正寻求进军电信业。你应该给CFO提供怎样的建

《金融学教学课件》bodie2e_chapter11共65页文档

• Face Vas ‘forward price’

3 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Definitions of Terms

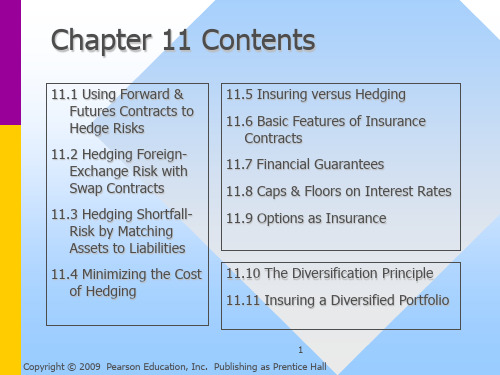

11.10 The Diversification Principle 11.11 Insuring a Diversified Portfolio

1 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

11.1 Using Forward and Futures Contracts to Hedge Risks

• Futures contracts for commodities and financial products includes such clauses, by standardization, to protect against unknown credit risks, and we leave the details of this to the course “financial derivatives”

Definitions of Terms

• Forward Price

– Price (agreed to today) of an item to be purchased, and paid for, at a given future date

• Spot Price

– Price (agreed to today) of an item to be purchased (and paid for) immediately

3 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Definitions of Terms

11.10 The Diversification Principle 11.11 Insuring a Diversified Portfolio

1 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

11.1 Using Forward and Futures Contracts to Hedge Risks

• Futures contracts for commodities and financial products includes such clauses, by standardization, to protect against unknown credit risks, and we leave the details of this to the course “financial derivatives”

Definitions of Terms

• Forward Price

– Price (agreed to today) of an item to be purchased, and paid for, at a given future date

• Spot Price

– Price (agreed to today) of an item to be purchased (and paid for) immediately

兹维博迪金融学第二版课件Chapter03

(2 1 .0 ) 3 9 .0

In c o m e ta x *N e t in c o m e

(1 5 .6 ) 2 3 .4

A llo c a tio n to d iv s *C h g re ta in e d e a rn

(1 0 .0 ) 1 3 .4

G P C C a s h F lo w S ta te m e n t, fo r th e Y e a r e n d in g D e c 3 1 , 2 x x 0

1 0 6 .6

1 3 .4 1 3 .4

1 2 0 .0

G e n s e ll, & a d m in e x p *O p e ra tin g in c o m e

(3 0 .0 ) 6 0 .0

In te re st e x p e n se *T a x a b le in c o m e

N e t in c o m e + D e p re c ia tio n - In c re a s e in a c c re c - In c re a s e in in v e n t + In c re a s e in a c c p a y *T o ta l c a s h fro m o p e ra tio n s

G P C In c o m e S ta te m e n t fo r Y e a r E n d in g 2 x x 1

S a le s re v e n u e s C o s t o f g o o d s s o ld *G ro s s m a rg in

2 0 0 .0 (1 1 0 .0 )

6 0 .0 9 0 .0 1 5 0 .0

兹维博迪金融学第二版课件Chapter02

通过中介和市场的资金流

Markets

Surplus Units

Deficit Units

Intermediaries

17 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

通过市场和中介的资金流

• 如通用汽车承兑公司(General Motors Acceptance Corporation)这样的中介发行商业 票据,为需要汽车贷款或租赁的家庭融资

23 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

在时间和空间上转移资源

• 金融系统提供方式以在时间上、地区之间 、行业之间转移经济资源

24 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

在时间和空间上转移资源(说明)

在时间上(跨期)转移资源的例子: –学生贷款:学生将未来能拥有的资源转移到现在;贷款 者将现在拥有的资源转移到未来。 –借款买房:买房者将未来能拥有的资源转移到现在。 –为退休储蓄:储蓄者将现在拥有的资源转移到未来。 –投资生产设备:投资者将现在拥有的资源转移到未来。

• 例:地方融资平台

14 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

通过中介的资金流

Markets

Surplus Units

Deficit Units

Intermediaries

15 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

滋维博迪投资学Chap02.ppt

INVESTMENTS | BODIE, KANE, MARCUS

23-3

Foreign Exchange Futures

• Foreign exchange risk: You may get more or less home currency than you expected from a foreign currency denominated transaction.

• Results: – Cheaper and more flexible – Synthetic position; instead of holding or shorting all of the actual stocks in the index, you are long or short the index futures

23-13

Table 23.2 Correlations among Major U.S. Stock Market Indexes

INVESTMENTS | BODIE, KANE, MARCUS

23-14

Creating Synthetic Positions with Futures

• Index futures let investors participate in broad market movements without actually buying or selling large amounts of stock.

INVESTMENTS | BODIE, KANE, MARCUS

23-15

Creating Synthetic Positions with Futures

• Speculators on broad market moves are major players in the index futures market. – Strategy: Buy and hold T-bills and vary the position in market-index futures contracts. – If bullish, then long futures – If bearish, then short futures

23-3

Foreign Exchange Futures

• Foreign exchange risk: You may get more or less home currency than you expected from a foreign currency denominated transaction.

• Results: – Cheaper and more flexible – Synthetic position; instead of holding or shorting all of the actual stocks in the index, you are long or short the index futures

23-13

Table 23.2 Correlations among Major U.S. Stock Market Indexes

INVESTMENTS | BODIE, KANE, MARCUS

23-14

Creating Synthetic Positions with Futures

• Index futures let investors participate in broad market movements without actually buying or selling large amounts of stock.

INVESTMENTS | BODIE, KANE, MARCUS

23-15

Creating Synthetic Positions with Futures

• Speculators on broad market moves are major players in the index futures market. – Strategy: Buy and hold T-bills and vary the position in market-index futures contracts. – If bullish, then long futures – If bearish, then short futures

兹维博迪金融学第二版课件Chapter05

n = 30, i = 3, FV = 0, PMT = 3,000, CPT PV, n = 45 CPT PMT gives $23,982

• The savings are then $30,000 - $23,982 = $6,018

Human Capital and Permanent Income

5.1 A Life-Cycle Model of Saving

• Assume that you are currently 35 years old, expect to retire in 30 years at 65, and then live for 15 more years until 80 • Your real labor income is $30,000/year until age 65 • Interest rates exceed inflation by 3%/ year

IRA Benefits

– The major benefits are more subtle. Assume:

• You can reserve $2,000 of pre-taxed income for investment, starting next year, for the next 40-years. This will grow at the rate of inflation of 3% • That the investment will return 10%/year • That you plan to remain retired for 20-years, and will require income that is indexed to inflation • The tax rate on all taxable income streams is 30%, both now and after retirement

• The savings are then $30,000 - $23,982 = $6,018

Human Capital and Permanent Income

5.1 A Life-Cycle Model of Saving

• Assume that you are currently 35 years old, expect to retire in 30 years at 65, and then live for 15 more years until 80 • Your real labor income is $30,000/year until age 65 • Interest rates exceed inflation by 3%/ year

IRA Benefits

– The major benefits are more subtle. Assume:

• You can reserve $2,000 of pre-taxed income for investment, starting next year, for the next 40-years. This will grow at the rate of inflation of 3% • That the investment will return 10%/year • That you plan to remain retired for 20-years, and will require income that is indexed to inflation • The tax rate on all taxable income streams is 30%, both now and after retirement

兹维博迪金融学第二版课件Chapter04

例:一次性投资的未来值

• 你的银行以3%的利 率、5年期限提供可 转让存单产品

• 你希望投资1500元、 5年,到期后该投资 价值多少?

FV PV * (1 i) $1500* (1 0.03) 5 $1738 .91111

n

n i PV FV Result

10

5 3% 1,500 ? 1738.911111

m

23 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

复利的频率

• 则等价于年化百分率18%的有效年利率是 e 0.18 - 1 = 19.72%

• 更高的精确度表明,从日复利到连续复利 可使有效年利率提高0.53个基点

15 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

例:一次性投资的利率

• 如果你投资15000元 ,期限10年,最终获 FV n i 1 得30000元,则年回 PV 报率是多少? 30000

10

24 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

复利的频率

• 一家银行决定对于中等风险的汽车贷款收 取12%的有效利率

• 则它应当开出的年化百分率是多少?

25 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

兹维博迪金融学第二版课件Chapter14

14.3 The Role of Speculators

– Hedger

• anyone using a futures market to reduce risk

– Speculator

• anyone who takes a position in the market (increasing his risk) in order to profit from his forecasts of future spot prices

14.2 The Economic Function of Futures Markets

• The futures markets facilitate the reallocation of exposure to commodity price risk among market participants • But:

• Futures are:

– standard contracts – immune from the credit worthiness of buyer and seller because

• exchange stands between traders • contracts marked to market daily • margin requirements

• provide liquidity when it is needed, which is when producers, distributors, and consumers can’t or won’t hedge

• more efficient by contributing towards recovering the fixed costs of providing a futures exchange

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

• Exchange-listed companies must comply with Securities and Exchange Commission (SEC) rules

5 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

4 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

The Balance Sheet

• Summarizes a firms assets, liabilities, and owner’s

equity at a moment in time

The Balance Sheet

• Major Divisions:

– Assets

• Current assets (less than a year) • Long-term assets (longer than a year

– Depreciation

– Liabilities and Stockholder’s Equity

3.1 பைடு நூலகம்unctions of Financial Statements

• Financial Statements:

– Provide information to the owners & creditors of a firm about the current status and past performance

– Provide a convenient way for owners & creditors to set performance targets & to impose restrictions of the managers of the firm

– Provide a convenient templates for financial planning

• 3.3 Market values v. Book Values

• 3.8 Constructing a Financial Planning Model

• 3.4 Accounting v. Economic • 3.9 Growth & the Need for

Measures of Income

• Major Divisions:

– Revenue & cost of goods sold

» Gross margin

– General administrative and selling expenses (GS&A)

» Operating income

– Debt service

» Taxable income

• Amounts measured at historical values and historical exchange rates

• Prepared according to GAAP, Generally Accepted Accounting Principles

– GAAP modified occasionally by the Financial Accounting Standards Board

Chapter 3 Contents

• 3.1 Functions of Financial Statements

• 3.6 Analysis Using Financial Ratios

• 3.2 Review of Financial Statement

• 3.7 The Financial Planning Process

• Liabilities

– Current Liabilities – Long-term debt

• Equity 6 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

GPC Balance Sheet on December 31

3 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

3.2 Review of Financial Statements

– Balance Sheets – Income Statements – Cash-Flow Statements

External Financing

• 3.5 Return on Shareholders v. Return on Book Equity

• 3.10 Working Capital Mgmt.

• 3.11 Liquidity & Cash Mgmt.

2

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Chapter 3: Managing Financial Health and Performance

Objectives

•Purpose of Financial Planning •Working Capital Management

1 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

7 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

The Income Statement

• Summarizes the profitability of a

company during a time period

– Corporate Taxes

» Net income

8

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

5 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

4 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

The Balance Sheet

• Summarizes a firms assets, liabilities, and owner’s

equity at a moment in time

The Balance Sheet

• Major Divisions:

– Assets

• Current assets (less than a year) • Long-term assets (longer than a year

– Depreciation

– Liabilities and Stockholder’s Equity

3.1 பைடு நூலகம்unctions of Financial Statements

• Financial Statements:

– Provide information to the owners & creditors of a firm about the current status and past performance

– Provide a convenient way for owners & creditors to set performance targets & to impose restrictions of the managers of the firm

– Provide a convenient templates for financial planning

• 3.3 Market values v. Book Values

• 3.8 Constructing a Financial Planning Model

• 3.4 Accounting v. Economic • 3.9 Growth & the Need for

Measures of Income

• Major Divisions:

– Revenue & cost of goods sold

» Gross margin

– General administrative and selling expenses (GS&A)

» Operating income

– Debt service

» Taxable income

• Amounts measured at historical values and historical exchange rates

• Prepared according to GAAP, Generally Accepted Accounting Principles

– GAAP modified occasionally by the Financial Accounting Standards Board

Chapter 3 Contents

• 3.1 Functions of Financial Statements

• 3.6 Analysis Using Financial Ratios

• 3.2 Review of Financial Statement

• 3.7 The Financial Planning Process

• Liabilities

– Current Liabilities – Long-term debt

• Equity 6 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

GPC Balance Sheet on December 31

3 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

3.2 Review of Financial Statements

– Balance Sheets – Income Statements – Cash-Flow Statements

External Financing

• 3.5 Return on Shareholders v. Return on Book Equity

• 3.10 Working Capital Mgmt.

• 3.11 Liquidity & Cash Mgmt.

2

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

Chapter 3: Managing Financial Health and Performance

Objectives

•Purpose of Financial Planning •Working Capital Management

1 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

7 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall

The Income Statement

• Summarizes the profitability of a

company during a time period

– Corporate Taxes

» Net income

8

Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall