ch 9 internatioanl financial market

国际商务International BusinessCh_9_Emerging_Markets

10

The New Global Challengers

Some 100 companies from Emerging Markets poised to become important 21st-century MNEs. Examples: • Brazil: Embraer, Sadia & Perdiago, Natura Mexico: America Movil, Groupo Modelo India: RanbGalanz, Haier, Chunlan Group Corp., Lenovo, Pearl River Piano Turkey: Koc Holding, Vestel & Sisecam

Chapter 9

Understanding Emerging Markets

International Business Strategy, Management & the New Realities by Cavusgil, Knight and Riesenberger

International Business: Strategy, Management, and the New Realities

International Business: Strategy, Management, and the New Realities

6

Developing Economies

• Low discretionary incomes; limited proportion of personal income spent on purchases other than food, clothing, and housing. • As a proportion of world population, 17% live on less than $1 per day; 40% live on less than $2 per day • Combination of low income and high birth rates tends to perpetuate poverty. • Sometimes called underdeveloped countries or third-world countries, but these terms are imprecise

国际金融英文版(全)

Short-and Medium-term Debt Markets

Euro-commercial paper (ECP)and Euro-medium-term

notes(EMTN) Floating rate Euro-notes(Floating rate notes(FRN)represent an early innovation in the eurobond market.Interest is usually paid semiannually and they trade at a spread of the reference rate,e.g.,LIBOR.Margin above LIBOR may amount to 25-100 basis points or more.After 6 months ,the rate is reset with the same margin. International REPO market(repurchase agreement ,or REPOS)

Non-bank

Public international financial institutions public global financial institutions regional public national public Private international financial institutions global private regional private national private

the balance of payment

3.the theories of foreign exchange rate determination 4.foreign exchange exposure

国际金融环境(英文版)International Financial Markets

Liquidity is a financial market’s most important characteristic

Liquidity - the ease of capturing an asset’s value

- Reflects a market’s operational efficiency - Impacts a market’s informational and

Part II

The International Financial Environment

Chapter 3 International Financial Markets Chapter 4 Foreign Exchange, Eurocurrencies,

and Currency Risk Management Chapter 5 The International Parity Conditions

3-17

Major domestic debt markets

(billions)

Source: Bank for International Settlements (June 2002)

3-18

Public debt markets

International markets

- Foreign bonds are issued in a domestic market by a foreign borrower Toronto Dominion 6.45 09 trade OTC in the U.S.

Rank Commercial bank 1 American Express Bank 2 UBS 3 Arab Banking Corp 4 Credit Suisse Group 5 Standard Chartered 6 Deutsche Bank 7 ABN-AMRO 8 BNP Paribas 9 Investec 10 KBC

Introduction of financial markets

Introduction

Week 1

Andy Adams

INTRODUCTION

• Real assets v financial assets • Main types of financial assets • The roles of financial markets • Types of investments • Types of investors

• The derivatives market also enables investors to control exposure to a given market (risk management)

Separation of ownership and management

• Financial markets enable firms with many shareholders to be formed • Shareholders elect a board of directors that in turn hires and supervises the management of the firm • This structure means that the owners and managers of the firm are different parties, which gives the firm stability that the ownermanaged firm cannot achieve • But potential conflicts of interest („agency problems‟) can arise because managers may pursue their own interests

Finance(国际金融)关键术语名词解释

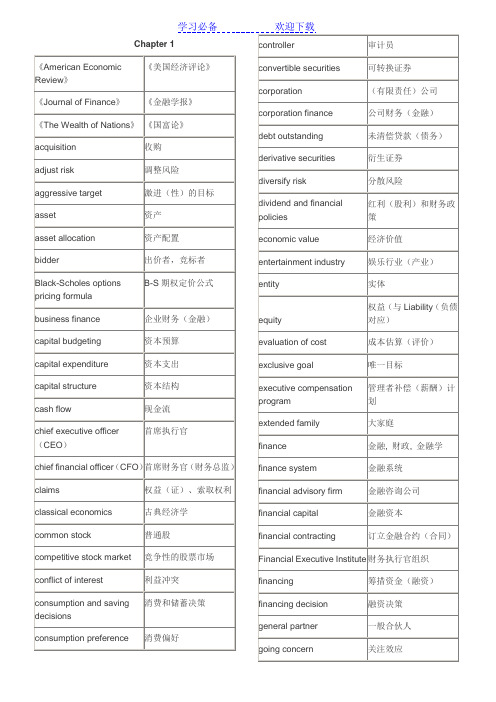

Chapter 1《American EconomicReview》《美国经济评论》《Journal of Finance》《金融学报》《The Wealth of Nations》《国富论》acquisition 收购adjust risk 调整风险aggressive target 激进(性)的目标asset 资产asset allocation 资产配置bidder 出价者,竞标者Black-Scholes optionspricing formulaB-S期权定价公式business finance 企业财务(金融)capital budgeting 资本预算capital expenditure 资本支出capital structure 资本结构cash flow 现金流chief executive officer(CEO)首席执行官chief financial officer(CFO)首席财务官(财务总监)claims 权益(证)、索取权利classical economics 古典经济学common stock 普通股competitive stock market 竞争性的股票市场conflict of interest 利益冲突consumption and savingdecisions消费和储蓄决策consumption preference 消费偏好controller 审计员convertible securities 可转换证券corporation (有限责任)公司corporation finance 公司财务(金融)debt outstanding 未清偿贷款(债务)derivative securities 衍生证券diversify risk 分散风险dividend and financialpolicies红利(股利)和财务政策economic value 经济价值entertainment industry 娱乐行业(产业)entity 实体equity权益(与Liability(负债对应)evaluation of cost 成本估算(评价)exclusive goal 唯一目标executive compensationprogram管理者补偿(薪酬)计划extended family 大家庭finance 金融, 财政, 金融学finance system 金融系统financial advisory firm 金融咨询公司financial capital 金融资本financial contracting 订立金融合约(合同)Financial Executive Institute 财务执行官组织financing 筹措资金(融资)financing decision 融资决策general partner 一般合伙人going concern 关注效应infrastructure 基础设施、架构initial outlay 初始投入integrated financial program 完整的财务计划investment decision 投资决策ITT corporation 国际电报电话公司learning curve 学习曲线liability 负债、债务、责任limited liability 有限责任limited partner 有限责任合伙人long-lived asset 长期资产long-range incentivesystem长期激励系统market discipline 市场规则market interest rate 市场利率market risk premium 市场风险价格market value of shares 股票市场价值(简称市值)marketing 营销maximize the wealth (使)财富最大化merger 兼并,合并mortgage loan 抵押贷款multinational conglomerate 跨国企业集团mutual fund 共同基金net worth 净资产operating margin 营业利润option 期权original core business 原始的核心业务partnership 合伙企业pension liabilities 养老金负债personal investing 个人投资physical capital 实物资本pool联营;集中使用的(资金,物)portfolio 投资组合portfolio of asset 资产组合preferred stock 优先股president 总裁primary commitment 首要(基本)任务private corporation 私人(非公众)公司professional managers 职业经理人profit 利润profit-maximizationcriterion利润最大化标准proposition 命题public corporation 公众公司quantitative model 定量模型regulatory body 监管机构resource allocationdecision资源配置决策retail outlet 零售摊点return 回报,收益risk-averse 风险厌恶(规避)security price 证券价格share price appreciation 股价上涨(增值)shareholder-wealth-maximization股东财富最大化sole proprietorship 个体(业主制)企业spin-off 配股spread out over time 跨时间分布stake 资助,资金stock option 股票期权strategic planning 战略规划supplier 供货商takeover 接管the exchange of assetsand risks资产和风险的交换the set of markets andother institutions市场及其它机构的集合trade off 权衡uncertain benefit 不确定性收益unlimited (limited)liability无(有)限责任vice-president forfinancial财务副总裁voting right (股东)投票权welfare 福利well-functioning capitalmarket高效的资本市场working capitalmanagement营运资本管理Chapter 2accounting procedure 会计程序adverse selection 逆向选择American Express 美国运通信用卡arithmetic mean 算术平均数asymmetry 不对称average risk premium 平均风险升水(溢价)Bank for InternationalSettlement(BIS)国际清算银行banking panic 银行危机bartern. 易货贸易;v. 讨价还价board of directors 董事会by-product 副产品call option 买入期权(看涨期权)capital gain(loss)资本收益(损失)Capital market资本市场(即长期资金市场)cash dividend 现金股利(红利)central bank 中央银行charge price 要价clearing and settlingpayment清算和结算支付closed-end 封闭式的collateral 担保品collateralization 以…担保commercial loan 商业贷款commercial loan rate 商业贷款利率credit card 信用卡default 违约、托债、弃权default risk 违约风险deficit unit 赤字部门defined-benefit pensionplan规定收益型养恤金制defined-contributionpension plan规定缴费型养恤金制depository savingsinstitution存款储蓄机构(系统)derivative 衍生(证券)Deutsche Bank 德意志银行dissemination 推广、传播dividend reinvestment 红利(股利)再投资dollar-denominated asset 以美元计价的资产double-entry-bookkeeping 复式记账法equity 权益equity-kickers 权益条件expected rates of return 期望(预期)收益率Federal Reserve System 联邦储备系统Finance AccountingStandardsBoard财务会计标准委员会financial instrument 金融工具financial intermediary 金融中介financial market parameters 金融市场参数financial variable 金融(财务)变量fixed-income-instruments 固定收益证券flow of fund 资金流flow of fund 资金流foreign exchange 外汇formation extraction 信息提取forward contract 远期合约functional perspective (从)功能(的角度或观点)future 期货German marks 德国马克go public 上市incentive problem 激励问题index fund 指数(化)基金index-linked bonds(与物价)指数联系的债券information service 信息咨讯(服务)insurance company 保险公司interest rate 利息率(简称利率)interest rate arbitrage 利率套利interest rate equalization 利率平价intermediary 中介International BankforReconstruction andDevelopment国际复兴开发银行International Monetary Fund(IMF)国际货币基金组织International Swap DealersAssociation国际掉期交易商协会intertemporal 跨期的(多阶段的)IOUI owe you的简称,喻指“借条”issuing stock 发行股票Japanese yen 日元life annuity 人寿年金limited liability 有限责任liquidity 流动性maturity (票据)到期日;期限money market货币市场(即短期资金市场)moral-hazard 道德风险mortgage 抵押mortgage rate 抵押利率mutual fund 共同基金New York Stock Exchange 纽约股票交易所nominal interest rate 名义利率offset 弥补、抵消open-end 开放式的option 期权Osaka Options and FuturesExchange大阪期货期权交易所over-the-counter-market(OTC)场外(交易)市场parties to contract 合约的参与者pool or aggregate 联营;集中使用的(资金或物品);premium 升水、溢价price appreciation 增值principal-agent problem 委托-代理问题pro rata 按比例的put option 卖出期权(看跌期权)qusai- 准、半rate of exchange 汇率rates of return 收益(回报)率rating agency 评级机构real interest rate 实际利率real rate of return 实际收益率redeem 赎回、偿还residual claim 剩余索取(求偿)权risk aversion 风险厌恶(规避)risk premium 风险升水(溢价)security dealer 证券交易商shed specific risk 规避(分散)特定(或私有)风险standard deviation 标准差standardized option contract (经)标准化的期权合约surplus unit 盈余部门trade-off 权衡trust company 信托公司U.S Treasury Bills 美国国库券underwrite 认购、包销unit of account 计值单位universal bank全能银行(指兼做中央银行和商业银行业务的银行)volatility 波动性well-information 信息充分的yen rate of return(以)日元(记值)的收益率yield curve 收益(率)曲线yield spread 收益价差Chapter 3accounting earnings 会计收入accounting rule 会计规则accrual 应计的accrual accounting 应计制(权责发生制)accumulated depreciation 累计折旧amortize 摊销、分期偿还apocryphal 伪经的、假冒的asset turnover(ATO)资产周转率(销售收入/总资产)audit 查账、审计balance sheet 资产负债表benchmark (比较)基准bond-rating 债券评级book value 账面价值capital structure 资本结构capital-incentive utility 资本密集型的公用事业(公司)cash and equivalents 现金及其等价物cash budget 现金预算cash cycle time 现金循环周期cash inflow 现金流入cash outflow 现金流出common stock outstanding 流通在外的普通股contingent liability 或有负债(如:可能发生的诉讼赔偿等)current asset 流动资产current liability 流动负债current ratio 流动比率depreciation 折旧、贬值disclose 披露dividend payout rate 股利支付率earnings before interest and tax (EBIT)息税前利润(=毛利- GS&A)earnings per share 每股盈余(收益)earnings retention rate (收益)留存比率expiration date 到期日external financing 外部融资(比如,发行股票和债券)financial distress 财务危机(困境)financial leverage 财务杠杆(率)financial ratio 财务比率financial statement 财务报表general, selling, andadministrative expenses(GS&A)管理及销售费用goodwill 商誉gross margin 毛利(润)(=销售收入-产品销售成本)income statement 损益表income tax 所得税intangible asset 无形资产inventory 库存、存货inventory turnover 存货周转率liquidity 流动性long-term debt 长期负债market to book 市值价值/账面价值marking to market 盯住市场net income(or net profit)净利润(即税后利润=EBIT-利息-所得税)net working capital 净营运资本(=流动资产-流动负债)net worth 净资产(即权益,=资产-负债)off-balance-sheet 表外项目operation income 营运收益(营业利润)opportunity cost 机会成本owner’s equity所有者权益paid-in capital 实收资本payable 应付账款percent-of-sales method 销售(收入)百分比法planning horizon 计划(时间)跨度price to earnings 市盈率(价格/盈余)profitability 盈利能力、盈利性property 土地、地产、所有权quick ratio 速动比率receivable 应收账款receivables turnover 应收账款周转率retained earnings 留存收益ROA(return on asset)资产收益率(EBIT/资产)ROE(return on equity)净资产收益率(即权益报酬率,=税后利润/净资产)ROS(return on sales)销售利润率(EBIT/销售收入)short-term debt 短期负债specify performance target 设定业绩目标statements of cash flow 现金流量表sustainable growth rate 持续增长率taxable income 应税收益(即税前利润=EBIT-利息)times interest earned 利息保障倍数Tobin’s Q托宾Q值(=资产市值/重置成本)total shareholder returns 总的股东收益(率)Chapter 4after-tax interest rate 税后利率amortization 分期偿还、摊销annual percentage rate(APR)年度百分比(利率)annuity 年金before-tax interest rate 税前利率compound interest 复利compounding 复和(与discounting 相反的概念)discount rate 折现率、贴现率discounted cash flow(DCF)折现现金流discounting 折现、折扣effective annual rate(EFF)有效年利率exchange rate 汇率future value 终值future value factor 终值系数(即由现值计算终值的换算因子)growth annuity 增长年金immediate annuity 即付年金implied interest rate 隐含利率installment 分期付款internal rate of return(IRR)内部报酬率market capitalizationrate市场资本化利率(简称市场利率)net present value(NPV)净现值opportunity cost ofcapital资本的机会成本ordinary annuity 普通年金(即后付年金)original principal (初始)本金outstanding balance 未平头寸payback period 回收期perpetual annuity(orperpetuity)永续年金present value 现值present value factor (终值)现值系数(终值系数的倒数)reinvest 再投资simple interest 单利tax-exempt 免税的time value of money (TVM)货币(或资金)的时间价值yield to maturity 到期收益率Chapter 5bequest 遗赠、遗赠物break-even 得失相当的,盈亏平衡的deductible 可扣除(或抵扣)的explicit cost 显性成本feasible plan 可行(的)计划human capital 人力资本implicit cost 隐性成本incremental 增量的、增值的intertemporal budgetconstraint跨期预算约束optimization model 优化模型permanent income 永久性收入provision 条文、条款tax deferred 税收(可)延缓的tax exempt 免税的trial-and-error 试错Chapter 6after-tax cash flow 税后现金流all-equity-financed firm 全权益融资公司annualized capital cost 年金化资本成本appropriation 拨款、占用break-even point 盈亏平衡点capital budgeting 资本预算cost of capital 资本成本coupon bond 息票债券cumulative present value 累计现值full-fledged 完备的、正式的horizontal axis 横轴(或横坐标)labor-intensive 劳动密集型的liquidate 清算、清偿market-related risk 市场相关(或者承认予以补偿)的风险,即系统风险(systematic risk)prototype 模型、原型residual value 残值risk premium 风险溢价risk-adjusted discountrate(经)风险调整的折现率sensitivity analysis 敏感性分析vertical axis 纵轴(或纵坐标)zero-inflation 零通涨(率)Chapter 7Arbitrage 套利arbitrageurs 套利(交易)者beverage 饮料bona fide 真正的bond 债券default risk 违约风险default-free 无违约(风险)的earnings per share 每股盈余efficient marketshypothesis(EMH)有效市场假说fetch 售得…fixed-income securities 固定收益证券foreign exchangemarket外汇市场fundamental value 基础价值information set 信息集interest-rate arbitrage 利率套利intrinsic value 内在价值laundry 洗衣店Law of One Price 一价定律price/earnings multiple 市盈率(倍数)real estate 房地产、不动产sibling 兄弟、同胞、氏族成员tautologically 同意反复地transaction costs 交易成本triangular arbitrage 三角套利vending 售货well-informed 信息充分的Chapter 8abscissa 横坐标ask price 卖价、要价(报价)bid price 买价、出价(询价)callable bond 可赎回债券convertible bond 可转换债券coupon bond 带息债券、息票债券current yield 即期收益(率)discount bond 折价债券face value/ par value 面值maturity 到期日ordinate 纵坐标par bond 平价债券premium bond 溢价债券pure discount bond 纯折现债券quote 牌价redeem 赎回、偿还risk-free interest rate 无风险利率yield curve 收益(率)曲线yield to maturity 到期收益(率)zero-coupon bond 零息(票)债券Chapter 9New York StockExchange纽约股票交易所cash dividend 现金股利(或红利、分红)closing price 收盘价Constant-Growth-RateDDM不变增长率股利折现模型current/existingstockholders现有股东、老股东discounted-dividendmodel(DDM)股利折现模型dividend policy 股利政策dividend yield 分利收益率ex-dividend price 除息(即股息)价格expected rate of return 期望收益率(或报酬率)infinite 无穷(或无限)的internal equity financing 内部权益融资Investment opportunity 投资机会market capitalization rate 市场资本化利率odd lots 零星(交易量)per se 亲自、亲身perpetual 永久的price/earnings ratio 市盈率Reinvested earnings 再投资收益required rate of return 必要报酬率(或收益率)risk-adjusted discountrate(经)风险调整折现率round lots 整批(交易量)share repurchase 股票回购skeptical 怀疑的stock dividend 股票股利stock splits 股票分割Chapter 10actuary 精算师caterer 酒席承办人colossal 巨大的、异常的confidence intervals 置信区间consortium 社团、合伙continuous probability distribution 连续概率分布diversification 分散化(投资)diversifying 分散化、多样化dunce 笨蛋、书呆子ex ante 事先的ex post 事后的expected rate of return 期望收益率(报酬率)flexibility 灵活性、柔性forward contract 远期合约hedger (套期)保值者、对冲者hedging 保值、对冲、对两方下注以防止(赌博、冒险等)的损失insuring 投保、给…保险jurisdiction 司法、权力、权限layoff 解雇、失业materialize 实现mean 均值normal distribution 正态分布overview 概述perverse 故意作对的、任性的portfolio 投资组合precautionary saving 预防性储蓄probability distribution 概率分布quadruple adj. 四倍的;v. 使…(增加)四倍recrimination 反责refund 退还risk assessment 风险评估risk aversion 风险规避risk avoidance 风险避免risk exposure 风险暴露risk identification 风险识别risk management 风险管理risk retention 风险保留risk transfer 风险转移sinful 有罪的、过错的、不道德的speculator 投机者square root 平方根stakeholder 利益相关者standard deviation 标准差swap 互换volatility 波动率Chapter 11American-type option 美式期权call option 买入期权(简称“买权”)cap (利率)上限condominium 公寓私有的共有方式co-payment 共同支付counterparty 交易对手credit guarantee 信用担保credit risk 信用风险deductible/deduction 免赔额delivery 交割delivery date 交割日derivative 衍生工具diversifiable risk 可分散的风险diversification principle 分散化(或多元化)原则European-type option 欧式期权exclusion 除外责任expiration date 到期日expire 到期face value 面值fictitious 虚构的firm-specific risk (公司)私有(或特有)风险forward contract 远期合约forward price 远期价格future contract 期货合约guarantee 保证、保证人、担保、担保品loan guarantee 债务保单long position 多头market risk 市场风险non-diversifiable risk 不可分散的风险premium 保险费、附加费、溢价proceed n. 盈利put option 卖出期权(简称“卖权”)rolling over 滚动(式)的short position 空头shortfall 不足之数、赤字spot price 即期价格standardized (经)标准化的strike price/ exerciseprice执行价格、行权价swap contract 互换合约、调期合约Chapter 12decision horizon 决策(修正)期限efficient portfolio 有效组合efficient portfolio frontier 有效组合前沿expected return 期望收益率mean-variance model 均值-方差模型minimum-varianceportfolio最小方差组合mutual fund 共同基金optimal combination ofrisky assets风险资产最优组合planning horizon 计划期、规划期point of tangency 切点portfolio selection (投资)组合选择risk premium 风险溢价risk tolerance 风险容忍(度)riskless asset 无风险资产risky-asset portfolio 风险资产组合set of……的集合tangency portfolio 切线组合target expected return 目标期望收益率trade-off 权衡、平衡trading horizon 交易(间隔)期限Chapter 13active investmentstrategies积极投资策略active portfolio selectionstrategy积极的组合选择策略Arbitrage Pricing Theory (APT)套利(定价)理论beat the market 打败市场benchmark 基准benchmark portfolio 基准组合Capital Asset PricingModel(CAPM)资本资产定价模型capital market line(CML)资本市场线consensus 一致、一致同意cost of capital 资本成本covariance 协方差equilibrium asset price 均衡(的)资产价格equilibrium expectedreturn均衡(的)期望收益率equilibrium price 均衡价格equilibrium risk premium 均衡风险溢价indexing 指数化irreducible 不能减少的、难复位的marginal contribution 边际贡献market portfolio 市场组合market-related risk 市场相关的(或承认的)风险multifactor IntertemporalCapital Asset PricingModel(ICAPM)多因子、跨期资本资产定价模型mutual fund 共同基金non-market risk 非市场风险passive investing 消极投资passive portfolio selectionstrategy消极的组合选择策略pension fund 养老基金regression coefficient 回归系数reward-to-risk ratio 风险补偿比率security market line(SML)证券市场线short-sale 卖空systematic risk 系统风险unsystematic risk 非系统风险Chapter 14arbitrageur 套利者bountiful 慷慨的、充足的casino 卡西诺赌场、小别墅closing out(one’s/a)position平仓continuouscompounding连续复利cost of carry 持有成本daily marking to market 逐日盯市(即每日无负债清算制度)delivery 交割delivery date 交割日delivery price 交割价格expectationshypothesis期望假说financial future 金融期货(即标的物为金融产品的期货合约)foreign-exchangeparity relation汇率平价关系forward contract 远期合约forward price 远期价格forward-spotprice-parity relation 远期-即期价格间的平价关系future contract 期货合约future price 期货价格future spot price 将来的现货价格hedger 套期保值者intrinsic value 内在价值margin 保证金open interest 未平仓合约数、头寸开放权益数position 头寸posting of margin (对)保证金(进行)过帐quasi-arbitrage 准套利(机会)replicate 复制speculator 投机者spoilage 损坏spot price 即期价格、现货价格spread 价差、差额the wall street journal 《华尔街日报》Chapter 15American-typeoption美式期权arrear 应付欠款、储备物at the money option 两平期权Black-Scholes model 布莱克-斯科尔斯期权定价模型boom 繁荣的bullish 乐观的call (option)买入期权(简称买权)、看涨期权capital-gain 资本(性)收益cash settlement 现金结算Chicago BoardOptions Exchange(CBOE)芝加哥期权交易所commission 佣金Contingent Claims 或有权益(简称或有权、或然权)credit guarantee 信用保证(或承诺)de facto 实际的、实际上decision tree 决策树delinquency 失职、违法行为dividend yield 股利收益率dividend-adjusted option formula 股利调整期权(定价)公式embedded option 嵌入式期权European put option 欧式卖权European-typeoption欧式期权evasion 逃避、躲避Exchange-traded option 场内(即在交易所交易的)期权exercise price/strikeprice执行价格/敲定价格expirationdate/maturity date到期日explicit 外生的flexibility 灵活性、柔性FutureOptions/Option onFutures期货期权growth option 增长期权guarantor 保证人hedge ratio 对冲比率、套期比率implicit 内生的implied volatility 隐含波动率in the money option 虚值期权incremental 增量的、增加的index option 指数期权intrinsicvalue/tangible value内在价值、执行价值junk bond 垃圾债券litigation 诉讼、争论mainline 主流的、传统的natural logarithm 自然对数normal distribution 正态分布Option 期权out of the moneyoption实值期权Over-the-counteroption场外(交易的)期权payoff diagrams 支付图plaintiff 起诉人provision 条文、条款put (option)卖出期权(简称卖权)、看跌期权put-call parityrelation买(权)与卖(权)间的平价关系real option 实物期权recession 衰退self-financinginvestment strategy自融资投资策略sequel 续篇、后果shortfall 不足之数、赤字stochastic 随机的 swap 互换 time value 时间价值 truncate截断two-state (binomial )option pricing model 两状态(二项式)期权定价模型 underlying asset 标的资产、基础资产Chapter 16account payable 应付账款accrued wage应计工资adjusted present value (APV )(经)调整的现值 after-tax incremental cash flow 税后增量现金流agency cost 代理成本 allegiance 忠诚、忠贞 all-equtiy financing 全权益融资 bankruptcy cost破产成本bankruptcy proceeding 破产程序、破产诉讼 Capital Structure资本结构capital structure irrelevance proposition 资本结构无关性定理 circumvent 绕过、智胜 collateral 担保品 common stock 普通股 corporate income tax公司所得税cost of financial distress 财务危机(危难)成本 debt financing 债务融资 entity实体、本质、存在 equity financing 权益融资 external financing外部融资(筹资) fiduciary受信托的 financial distress财务危机(危难) financing instrument 金融工具 franchise 特许权 free cash flow自由现金流 frictionless 无摩擦的gourmet供美食家的享用的、美食家imminent 临近的、迫在眉睫的 interest tax shield (债务)利息税盾 internal financing 内部融资(筹资) issuing new stock 发行新股leveraged investment 杠杆投资(即投资额中有部分债务融资) long-term lease 长期租赁 M & M proposition MM 定理market debt-to-equity ratio(用)市场(价值表示的)债务-权益比率market-value/economic balance sheet (用)市场价值(表示的)资产负债表 Modigliani & Miller (M 莫迪里阿尼和米勒& M )optimal capital structure 最优资本结构 pension liability 养老金(形式的)债务 perk额外补贴 personal income tax 个人所得税 preferred stock优先股学习必备欢迎下载prestige 威信、声望pro rata 按比例的realized capital gains 已实现资本收益redeploy 重新部署(布置、调派)repurchase stock 回购股票residual claim 剩余索取权(求偿权)retained earning 留存收益scrutiny 细致检查secured debt 安全债务stock option 股票期权subsidy 津贴、财政援助、特别津贴voting right 投票权warrant 认股权证、认股权weighted average costof capital(WACC)加权资本成本Chapter 17acquisition 收购bargain v. 讲价、讨价还价;n. 便宜货、交易、协定breakup 分散、中止、崩溃consolidation 合并、联合、巩固consummate 完成、使…完美contest 竞争、争夺corroborate 加强证实、巩固、支持discretion 决定权、谨慎、判断力divest 使…脱去information set 信息集loss carry-forward 亏损递延malevolence 恶意、坏影响merger 兼并opaqueness 不透明real option 实物期权spin-off 派生出、让产易股、抽资脱离synergy 协同增效takeover 接管。

国际营销

一、国际市场营销学International Marketing定义:是一门研究企业如何向一国以上的消费者或用户提供商品和劳务,以获得全球利益最大化的学科。

Definition: It is a subject to study how to supplycommodities and services to the consumers in more and more nations in orderto obtain global profits in maximization.二、国际市场营销的内涵和特点Intensions and Features of International Marketing1. 国际营销的主体是企业The principle of International marketing is the enterprise.2. 国际营销的范围是一国以上的市场,包括本国.The scopes of International Marketing are markets more over one nation, including domestic market.3. 国际营销的内容是提供产品和服务The content of International marketing is to supply products or services.4. 国际营销的目的是取得更大的经济利益.The purpose of International Marketing is to make bigger economic profits.三、国际营销的途径The Channels of International Marketing1. 被动的出口passive export中间商找生产企业购买产品出口,生产企业无需主动做国际市场营销。

Middleman buys product from producers for export, producers do not need to do international marketing actively2. 积极的出口active export企业有稳定的出口货源和自己的出口部,通过国内外展览、互联网广告等进行国际营销活动。

国际财务管理英文版第版马杜拉答案Chapter

Chapter 3International Financial Markets Lecture OutlineMotives for Using International Financial Markets Motives for Investing in Foreign MarketsMotives for Providing Credit in Foreign MarketsMotives for Borrowing in Foreign MarketsForeign Exchange MarketHistory of Foreign ExchangeForeign Exchange TransactionsExchange QuotationsForeignInterpretingCurrency Futures and Options MarketsInternational Money MarketOrigins and DevelopmentStandardizing Global Bank RegulationsInternational Credit MarketSyndicated LoansInternational Bond MarketEurobond MarketDevelopment of Other Bond MarketsComparing Interest Rates Among CurrenciesInternational Stock MarketsIssuance of Foreign Stock in the U.S.Issuance of Stock in Foreign MarketsComparison of International Financial MarketsHow Financial Markets Affect an MNC’s ValueChapter ThemeThis chapter identifies and discusses the various international financial markets used by MNCs. These markets facilitate day-to-day operations of MNCs, including foreign exchange transactions, investing in foreign markets, and borrowing in foreign markets.Topics to Stimulate Class Discussion1. Why do international financial markets exist?2. How do banks serve international financial markets?3. Which international financial markets are most important to a firm that consistently needsshort-term funds? What about a firm that needs long-term funds?Critical debateShould firms that go public engage in international offerings?Proposition Yes. When a firm issues shares to the public for the first time in an initial public offering (IPO), it is naturally concerned about whether it can place all of its shares at a reasonable price. It will be able to issue its shares at a higher price by attracting more investors. It will increase its demand by spreading the shares across countries. The higher the price at which it can issue shares, the lower is its cost of using equity capital. It can also establish a global name by spreading shares across countries.Opposing view No. If a firm spreads its shares across different countries at the time of the IPO, there will be less publicly traded shares in the home country. Thus, it will not have as much liquidity in the secondary market. Investors desire shares that they can easily sell in the secondary market, which means that they require that the shares have liquidity. To the extent that a firm reduces its liquidity in the home country by spreading its share across countries, it may not attract sufficient home demand for the shares. Thus, its efforts to create global name recognition may reduce its name recognition in the home country.With whom do you agree? State your reasons. Use InfoTrac or some other search engine to learn more about this issue. Which argument do you support? Offer your own opinion on this issue.ANSWER: The key is that students recognize the tradeoff involved. A firm that engages in a relatively small IPO will have limited liquidity even when all of the stock is issued in the home country. Thus, it should not consider issuing stock internationally. However, firms with larger stock offerings may be in a position to issue a portion of their shares outside the home country. They should not spread the stocks across several countries, but perhaps should target one or two countries where they conduct substantial business. They want to ensure sufficient liquidity in each of the foreign countries where they sell shares.Stock Markets are inefficientPropositionI cannot believe that if the value of the euro in terms of, say, the British pound increases three days in a row, on the fourth day there is still a 50:50 chance that it will go up or down in value. I think that most investors will see a trend and will buy, therefore the price is morelikely to go up. Also, if the forward market predicts a rise in value, on average, surely it is going to rise in value. In other words, currency prices are predictable. And finally, if it were so unpredictable and therefore unprofitable to the speculator, how is it that there is such a vast sum of money being traded every day for speculative purposes – there is no smoke without fire.The simple answer is that if that is what you believe, buy currencies that have viewOpposingincreased three days in a row and on average you should make a profit, buy currencies where the forward market shows an increase in value. The fact is that there are a lot of investors with just your sort of views. The market traders know all about such beliefs and will price the currency so that such easy profit (their loss) cannot be made. Look at past currency rates for yourself, check all fourth day changes after three days of rises, any difference is going to be not enough to cover transaction costs or trading expenses and the slight inaccuracy in your figures which are likely to be closing day mid point of the bid/ask spread. No, all currency movements are related to information and no-one knows if tomorrows news will be better or worse than expected.With whom do you agree? Could there be undiscovered patterns? Could some movements not be related to information? Could some private news be leaking out?ANSWER: Clearly there are no obvious patterns. Discussion on the impossibility of obvious patterns is worth emphasizing. However, does market inefficiency necessarily involve patterns, could market manipulation be occasional. There is worrying evidence from share price movements that there is unusual movement before announcements on many occasions, so the ideathat traders do not occasionally collude and move the price without supporting economic evidence is not an unreasonable view. Proof is however difficult as we have to separate anticipation from prior knowledge, the lucky speculator from the speculator who was in the know.Answers to End of Chapter Questions1. Motives for Investing in Foreign Money Markets. Explain why an MNC may invest fundsin a financial market outside its own country.ANSWER: The MNC may be able to earn a higher interest rate on funds invested in a financial market outside of its own country. In addition, the exchange rate of the currency involved may be expected to appreciate.2. Motives for Providing Credit in Foreign Markets. Explain why some financial institutionsprefer to provide credit in financial markets outside their own country.ANSWER: Financial institutions may believe that they can earn a higher return by providing credit in foreign financial markets if interest rate levels are higher and if the economic conditions are strong so that the risk of default on credit provided is low. The institutions may also want to diversity their credit so that they are not too exposed to the economic conditions in any single country.3. Exchange Rate Effects on Investing. Explain how the appreciation of the Australian dollaragainst the euro would affect the return to a French firm that invested in an Australian money market security.ANSWER: If the Australian dollar appreciates over the investment period, this implies that the French firm purchased the Australian dollars to make its investment at a lower exchange rate than the rate at which it will convert A$ to euros when the investment period is over.Thus, it benefits from the appreciation. Its return will be higher as a result of this appreciation.4. Exchange Rate Effects on Borrowing. Explain how the appreciation of the Japanese yenagainst the UK pound would affect the return to a UK firm that borrowed Japanese yen and used the proceeds for a UK project.ANSWER: If the Japanese yen appreciates over the borrowing period, this implies that the UK firm converted yen to pounds at a lower exchange rate than the rate at which it paid for yen at the time it would repay the loan. Thus, it is adversely affected by the appreciation. Its cost of borrowing will be higher as a result of this appreciation.5. Bank Services. List some of the important characteristics of bank foreign exchange servicesthat MNCs should consider.ANSWER: The important characteristics are (1) competitiveness of the quote, (2) the firm’s relationship with the bank, (3) speed of execution, (4) advice about current market conditions, and (5) forecasting advice.6. Bid/ask Spread. Delay Bank’s bid price for US dollars is £0.53 and its ask price is £0.55.What is the bid/ask percentage spread?ANSWER: (£0.55– £0.53)/£0.55 = .036 or 3.6%7. Bid/ask Spread. Compute the bid/ask percentage spread for Mexican peso in which the askrate is 20.6 New peso to the dollar and the bid rate is 21.5 New peso to the dollar.ANSWER: direct rates are 1/20.6 = $0.485:1 peso as the ask rate and 1/21.5 = $0.465:1 peso as the bid rate so the spread is[($0.485 – $0.465)/$0.485] = .041, or 4.1%. Note that the spread is fro the Mexiccan peso not the dollar.8. Forward Contract. The Wolfpack ltd is a UK exporter that invoices its exports to the UnitedStates in dollars. If it expects that the dollar will appreciate against the pound in the future, should it hedge its exports with a forward contract? Explain..ANSWER: The forward contract can hedge future receivables or payables in foreign currencies to insulate the firm against exchange rate risk. Yet, in this case, the Wolfpack Corporation should not hedge because it would benefit from appreciation of the dollar when it converts the dollars to pounds.9. Euro. Explain the foreign exchange situation for countries that use the euro when theyengage in international trade among themselves.ANSWER: There is no foreign exchange. Euros are used as the medium of exchange.10. Indirect Exchange Rate. If the direct exchange rate of the euro is worth £0.685, what is theindirect rate of the euro? That is, what is the value of a pound in euros?ANSWER: 1/0.685 = 1.46 euros.11. Cross Exchange Rate. Assume Poland’s currency (the zloty) is worth £0.17 and theJapanese yen is worth £0.005. What is the cross (implied) rate of the zloty with respect to yen?ANSWER: £0.17/£0.005 = 34 zloty:1 yen12. Syndicated Loans. Explain how syndicated loans are used in international markets.ANSWER: A large MNC may want to obtain a large loan that no single bank wants to accommodate by itself. Thus, a bank may create a syndicate whereby several other banks also participate in the loan.13. Loan Rates. Explain the process used by banks in the Eurocredit market to determine the rateto charge on loans.ANSWER: Banks set the loan rate based on the prevailing LIBOR, and allow the loan rate to float (change every 6 months) in accordance with changes in LIBOR.14. International Markets. What is the function of the international money market? Brieflydescribe the reasons for the development and growth of the European money market. Explain how the international money, credit, and bond markets differ from one another.ANSWER: The function of the international money market is to efficiently facilitate the flow of international funds from firms or governments with excess funds to those in need of funds.Growth of the European money market was largely due to (1) regulations in the U.S. that limited foreign lending by U.S. banks; and (2) regulated ceilings placed on interest rates of dollar deposits in the U.S. that encouraged deposits to be placed in the Eurocurrency market where ceilings were nonexistent.The international money market focuses on short-term deposits and loans, while the international credit market is used to tap medium-term loans, and the international bond market is used to obtain long-term funds (by issuing long-term bonds).15. Evolution of Floating Rates. Briefly describe the historical developments that led to floatingexchange rates as of 1973.ANSWER: Country governments had difficulty in maintaining fixed exchange rates. In 1971, the bands were widened. Yet, the difficulty of controlling exchange rates even within these wider bands continued. As of 1973, the bands were eliminated so that rates could respond to market forces without limits (although governments still did intervene periodically).16. International Diversification. Explain how the Asian crisis would have affected the returnsto a UK. firm investing in the Asian stock markets as a means of international diversification.[See the chapter appendix.]ANSWER: The returns to the UK firm would have been reduced substantially as a result of the Asian crisis because of both declines in the Asian stock markets and because of currency depreciation. For example, the Indonesian stock market declined by about 27% from June 1997 to June 1998. Furthermore, the Indonesian rupiah declined against the U.S. dollar by 84%.17.Eurocredit Loans.a.With regard to Eurocredit loans, who are the borrowers?b. Why would a bank desire to participate in syndicated Eurocredit loans?c. What is LIBOR and how is it used in the Eurocredit market?ANSWER:a. Large corporations and some government agencies commonly request Eurocredit loans.b. With a Eurocredit loan, no single bank would be totally exposed to the risk that theborrower may fail to repay the loan. The risk is spread among all lending banks within the syndicate.c. LIBOR (London interbank offer rate) is the rate of interest at which banks in Europe lendto each other. It is used as a base from which loan rates on other loans are determined in the Eurocredit market.18. Foreign Exchange. You just came back from Canada, where the Canadian dollar was worth£0.43. You still have C$200 from your trip and could exchange them for pounds at the airport, but the airport foreign exchange desk will only buy them for £0.40. Next week, you will be going to Mexico and will need pesos. The airport foreign exchange desk will sell you pesos for £0.055 per peso. You met a tourist at the airport who is from Mexico and is on his way to Canada. He is willing to buy your C$200 for 1500 New Pesos. Should you accept the offer or cash the Canadian dollars in at the airport? Explain.ANSWER: Exchange with the tourist. If you exchange the C$ for pesos at the foreign exchange desk, the C$200 is multiplied by £0.40 and then divided by £0.055 ie a ratio of £0.40/0.055 = 7.27 pesos to the C$. The total pesos would be 200 x 7.27 = 1454 pesos, a little less than is being offered by the tourist.19. Foreign Stock Markets. Explain why firms may issue stock in foreign markets. Why mightMNCs issue more stock in Europe since the conversion to a single currency in 1999?ANSWER: Firms may issue stock in foreign markets when they are concerned that their home market may be unable to absorb the entire issue. In addition, these firms may have foreign currency inflows in the foreign country that can be used to pay dividends on foreign-issued stock. They may also desire to enhance their global image. Since the euro can be used in several countries, firms may need a large amount of euros if they are expanding across Europe.20. Stock Market Integration. Bullet plc a UK firm, is planning to issue new shares on theLondon Stock Exchange this month. The only decision still to be made is the specific day on which the shares will be issued. Why do you think Bullet monitors results of the Tokyo stock market every morning?ANSWER: The UK stock market prices sometimes follow Japanese market prices. Thus, the firm would possibly be able to issue its stock at a higher price in the UK if it can use the Japanese market as an indicator of what will happen in the UK market. However, this indicator will not always be accurate.Advanced Questions21. Effects of September 11. Why do you think the terrorist attack on the U.S. was expected tocause a decline in U.S. interest rates? Given the expectations for a potential decline in U.S.interest rates and stock prices, how were capital flows between the U.S. and other countries likely affected?ANSWER: The attack was expected to cause a weaker economy, which would result in lower U.S. interest rates. Given the lower interest rates, and the weak stock prices, the amount of funds invested by foreign investors in U.S. securities would be reduced.22. International Financial Markets. Carrefour the French Supermarket chain has established retail outlets worldwide. These outlets are massive and contain products purchased locally as well as imports. As Carrefour generates earnings beyond what it needs abroad, it may remit those earnings back to France. Carrefour is likely to build additional outlets especially in China.a. Explain how the Carrefour outlets in China would use the spot market in foreign exchange.ANSWER:The Carrefour stores in China need other currencies to buy products from other countries, and must convert the Chinese currency (yuan) into the other currencies in the spot market to purchase these products. They also could use the spot market to convert excess earnings denominated in yuan into euros, which would be remitted to the French parent.b. Explain how Carrefour might utilize the international money markets when it isestablishing other Carrefour stores in Asia.ANSWER: Carrefour may need to maintain some deposits in the Eurocurrency market that can be used (when needed) to support the growth of Carrefour stores in various foreign markets. When some Carrefour stores in foreign markets need funds, they borrow from banks in the Eurocurrency market. Thus, the Eurocurrency market serves as a deposit or lending source for Carrefour and other MNCs on a short-term basis. (Eurocurrency refers to international currencies, most likely the dollar, not just the euro!)c. Explain how Carrefour could use the international bond market to finance theestablishment of new outlets in foreign markets.ANSWER: Carrefour could issue bonds in the Eurobond market to generate funds needed to establish new outlets. The bonds may be denominated in the currency that is needed; then, once the stores are established, some of the cash flows generated by those stores could be used to pay interest on the bonds.23.Interest Rates. Why do interest rates vary among countries? Why are interest rates normallysimilar for those European countries that use the euro as their currency? Offer a reason why the government interest rate of one country could be slightly higher than that of the government interest rate of another country, even though the euro is the currency used in both countries.ANSWER: Interest rates in each country are based on the supply of funds and demand for funds for a given currency. However, the supply and demand conditions for the euro are dictated by all participating countries in aggregate, and do not vary among participating countries. Yet, the government interest rate in one country that uses the euro could be slightly higher than others that use the euro if it is subject to default risk. The higher interest rate would reflect a risk premium.Blades plc Case Study。

国际金融课件internationalfinance

06

中国国际金融的实践与展望

中国国际金融业在规模和业务范围上不断扩大,成为全球金融市场的重要参与者。

中国国际金融业在推动经济增长、促进国际贸易和投资等方面发挥了重要作用。

改革开放以来,中国国际金融业经历了从无到有、从小到大的发展历程,逐步建立起较为完善的金融机构体系和金融市场体系。

中国国际金融的发展历程与现状

Global financial markets facilitate the flow of capital across borders, allowing for the efficient allocation of resources and the hedging of risks.

Regional financial markets serve specific geographical regions and are often associated with trade blocs or economic unions.

01

国际金融危机的定义

由于国际金融市场上的过度投机、金融监管缺失等原因,导致国际金融市场出现大规模动荡,影响各国经济的稳定。

02

国际金融危机的传染机制

通过贸易、金融和信息等渠道,将危机从一个国家传递到另一个国家。

国际金融危机及其传染机制

1

2

3

通过监测和分析国际金融市场的相关信息,及时发现潜在的风险点,采取应对措施。

02

03

04

05

Main International Financial Centers and Their Characteristics 主要国际金融中心及其特点

ห้องสมุดไป่ตู้

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

School of Economics and Management , NJUST

njustlzj@

Hale Waihona Puke UNIT TWO: INTERNATIONAL FINANCIAL MARKET

School of Economics and Management FRAMEWORK OF, NJUST

Category of bond

classified by place

Local market bond International bond

Foreign bond Euro-bond

njustlzj@

School of Economics and Management , NJUST

Category of bond

classified by interest rate:

Fixed interest rate bond Floating interest rate bond Zero interest bond

njustlzj@

School of Economics and Management , NJUST

School of Economics and Management , NJUST

2. The main conditions to and School of Economics Management , NJUST form a international financial market

1) political conditions:stable polity, complete legal system and successive policies 2) perfect financial system: domestic financial market---traditional international market -modern international financial market. 3) loose exchange control:convertible domestic currency, to loosen or abolish FX control 4) perfect market mechanism: communication, management, staff 5) ideal geographical location: New York, London and Hong Kong njustlzj@

1. The meanings of international financial market . 2. The main conditions to form a international financial market 3. The function of international financial market

3. Discount market: discount, rediscount, discount rate (cf. interest rate)

njustlzj@

II. Capital Market

1. International Banking Services eg. Long-term Loan from bank 2. Portfolio Market

3. The function of international financial market

1) Development in local market 2) Promotion to international trade 3) Promotion to development of world economy 4) Adjust the relationship between currency demand and supply globally.

2)Stock Market

Concept of Stock The significance of Stock market How to understand stock in China Category of stock: overseas and in China The value of stock: stock price index:

School of Economics and Management , NJUST

njustlzj@

School of Economics and Management , NJUST

1. International Banking Services

The world’s largest Banks can offer a lot of international banking services, we introduce one typical business as follow: Long-term Loan from bank Characteristic: large amount, spread risk (e.g. insurance ) The major content: content

School of Economics and Management , NJUST

Category of bond

classified by convertibility:

Common bond Convertible bond

njustlzj@

School of Economics and Management , NJUST

njustlzj@

School of Economics and Management , NJUST

2. Portfolio Market

1) Bond market

Category of bond issuance of bond The Evaluation and Listing for bond The price: safety, benefit, market rate The major bond market: Yankee, Samurai, Eurobond Market

njustlzj@

1. The meanings of international financial market

narrow sense of financial market: money market , capital market broad sense of financial market: financial business, including money, capital , foreign exchange , securities, gold market etc. traditional financial market: the main business traded between local resident and the foreigners. Modern financial market: main business between non-residents. off-shore financial market njustlzj@

money market, capital market, foreign exchange market, security market , gold market

njustlzj@

School of Economics and Management , NJUST

I. MONEY MARKET

Inter bank offered market: LIBOR 2. Transaction of short-term security

1.

Treasury Bill :compared to Government Bond Government bond was issued in 1981 but called treasury bill Commercial Bill :e.g. One of Chinese Corp. issued 0.2 billion USD commercial bill in United States. Certificate of Deposit :usually called CD. compared to time deposit

njustlzj@

School of Economics and Management , NJUST

Category of bond

classified by issuer:

Government bond Municipal bond Corporate bond

njustlzj@

The most famous evaluation companies in the world: Standard & Poor, Moody's com. AAA AA A BBB BB B CCC CC C D

njustlzj@

School of Economics and Management , NJUST

Issuance of bond

Issued by par value Issued by over value Issued by under value

njustlzj@

The Evaluation and Listing for bond

School of Economics and Management , NJUST

The price of bond

You should pay attention to the following three factors: safety benefit market rate