Value Added Tax and Direct Taxation

阿根廷的税收政策(中英译文)

阿根廷的税收政策(中英译文)阿根廷的税收政策(中英译文)阿根廷中央政府、省及市政府负责征税。

税收形式大部分为间接消费税。

92年4月的税制改革摒弃了原有的原则,建立了以全球为基础的税收责任制。

凡居住在阿根廷的个人和企业,在全球范围经营的收入及利润要进行申报并交税。

阿主要税收有:1)企业所得税,每年交一次。

红利分配不再征税。

所得税为联邦税,地方政府不能再征所得税,在阿根廷的外国公司分公司及永久性代表机构的税率为33%。

有限责任合伙公司需申报收入,并说明每个合伙人的收入,以此作为纳税的基础.1992年4月阿根廷政府实行新的税收制度,所有公司均要申报其在全球范围的经营收入情况,如在国外的所得税已缴付,在国内可免税缴。

2)个人所得税:在阿根廷境内停留6个月以上的个人,须缴纳个人所得税。

确定纳税收入时,已缴纳的个人社会保障金、医疗保险、养老金及慈善性捐款等均属于从收入中扣除的款项。

个人所得税为累进制税率,最高33%。

3)外国企业来阿提供技术援助及咨询服务中所得收入,应缴税19.8%;非居民所获专利使用权收入应缴税26.4%;版权使用收入应缴税11.55%。

4)社会保障金(以工资为基础):税项雇主代雇员缴纳雇员白己缴纳养老全16% 11%家庭补贴9% -医疗保险6% 3%健康保险2% 3%总计33% 17%在阿根廷工作不足2年的外国专业技术人员、科学家可申请免缴社会保证金。

5)增值税:进口、生产、商止流通及各种服务行业均应缴纳21%的增值税。

只有刊物、证券及面包、牛奶、纯水销售等免征增值税。

6)资产税:按年缴纳资产值的0.5%。

个人净资产超过10万美元的,10万美元以上部分,需在每年的12月31日缴纳1%资产税。

股票、债券、在国内银行帐户上的定期存款免缴此税。

7)印花税:此税在首都已基本取消。

目前只对产权转移征此税,税率为交易价的O.75%-2.5%。

在各省该税是对各种交易,如抵押、合同、承兑等相关文件征收。

注册会计师-《税法》英语基础-专题一 增值税(20页)

专题一增值税目录1.考点一征税范围及纳税义务人2.考点二增值税计算3.考点三增值税抵扣&税收优惠4.考点四增值税的纳税义务发生时间5.同步系统训练考情分析增值税的考察,往往出现在计算题和综合题中。

可以单独考察,也可以结合其他税种出题。

本专题的内容是历年英文测试的考察重点增值税的考察主要有以下几种方式:(一)直接问税种的应纳税额为多少,计算金额即可。

(二)针对某些事项问是否应该纳税、应该缴纳哪些税种、如何纳税、计算是否正确,或者直接问税款征收方法。

(三)需要对一些方案进行比较分析。

考点一征税范围及纳税义务人专业词汇增值税:Value Added Tax(VAT)征税范围:Taxation scope销项税:Output Tax税率:Tax rate纳税人:Taxpayer一般纳税人: General taxpayer小规模纳税人: Small-scale taxpayer劳务:Labour service货物进口:Importation of goods货物出口:Exportation of goods非增值税应税项目:Non- VAT taxable items交通运输业:Transportation industry电信业:Telecommunication industry建筑业:Construction industry现代服务业:Modern service industry销售货物:Sales of goods提供劳务:Provision of labour services有形的:Tangible加工:Processing委托方:Consignor受托方:Consignee委托:Consignment委托代销:Consignment of goods for sale代销货物:Goods under consignment从事:Engage in委托加工货物:Consigned processing goods受限制:Be subject to金融租赁:Financial lease所有权:Ownership转移:Transfer征收:Levy销售量:Sales volume保险费:Insurance premium价外费用:Additional fee/charge条例:Provision资产重组:Asset restructuring发票:Invoice被视为/视同:Be deemed as重点、难点讲解增值税的征税范围Value added tax scope一、征税范围的一般规定General rule of taxation scope1.销售或者进口的货物Sales or importation of goods货物,是指有形动产,包括电力、热力、气体在内。

增值税value added tax

增值税value added tax(VAT)从计税原理上说,增值税是对商品生产、流通、劳务服务中多个环节的新增价值或商品的附加值征收的一种流转税。

实行价外税,也就是由消费者负担,有增值才征税没增值不征税,但在实际当中,商品新增价值或附加值在生产和流通过程中是很难准确计算的。

因此,我国也采用国际上的普遍采用的税款抵扣的办法,即根据销售商品或劳务的销售额,按规定的税率计算出销项税额,然后扣除取得该商品或劳务时所支付的增值税款,也就是进项税额,其差额就是增值部分应交的税额,这种计算方法体现了按增值因素计税的原则。

公式为:应纳税额=销项税额-进项税额增值税计算公式:含税销售额/(1+税率)=不含税销售额不含税销售额×税率=应缴税额上面说增值税是实行的“价外税”,什么是价外税?也就是价外征税,就是由消费者负担的。

比如:你公司向a公司购进货物100件,金额为10000元,但你公司实际上要付给对方的货款并不是10000元,而是10000+10000*17%(假设增值税率为17%)=11700元。

为什么只购进的货物价值才10000元,另外还要支付个1700元呢?因为这时,你公司作为消费者就要另外负担1700元的增值税,这就是增值税的价外征收。

这1700元增值税对你公司来说就是“进项税”。

a公司收了多收了这1700元的增值税款并不归a公司所有,a公司要把1700元增值税上交给国家。

所以a公司只是代收代缴而已,并不负担这笔税款。

再比如:你公司把购进的100件货物加工成甲产品80件,出售给b公司,取得销售额15000元,你公司要向b公司收取的甲产品货款也不只是15000元,而是15000+15000*17%=17550元,因为b公司这时作为消费者也应该向你公司另外支付2550元的增值税款,这就是你公司的“销项税”。

你公司收了这2550元增值税额也并不归你公司所有,你公司也要上交给国家的,所以,2550元的增值税款也不是你公司负担的,你公司也只是代收代缴而已。

税务专业英语常用词汇整理

税务专业英语常用词汇整理随着全球经济的发展和国际贸易的增加,税务专业英语的重要性日益凸显。

无论是从事税务工作的专业人士,还是对税务有兴趣的学习者,掌握一些常用的税务专业英语词汇是必不可少的。

本文将整理一些常用的税务专业英语词汇,帮助读者更好地理解和运用。

一、税收类型(Types of Taxes)1. Income Tax - 所得税2. Value Added Tax (VAT) - 增值税3. Corporate Tax - 企业所得税4. Sales Tax - 销售税5. Property Tax - 房产税6. Excise Tax - 特别消费税7. Customs Duty - 关税8. Gift Tax - 赠与税9. Inheritance Tax - 遗产税10. Payroll Tax - 工资税二、税务部门(Tax Authorities)1. Tax Administration - 税务管理机构2. Internal Revenue Service (IRS) - 美国国内税务局3. Her Majesty's Revenue and Customs (HMRC) - 英国国家税务和海关总署4. State Tax Department - 州税务部门5. Tax Inspectorate - 税务检查机构6. Tax Court - 税务法院三、纳税申报(Tax Filing)1. Tax Return - 纳税申报表2. Taxpayer Identification Number (TIN) - 纳税人识别号3. Taxable Income - 应税收入4. Deductions - 扣除项5. Tax Exemptions - 免税额6. Tax Refund - 税款退还7. Tax Evasion - 逃税8. Tax Avoidance - 避税四、税务审计(Tax Auditing)1. Tax Audit - 税务审计2. Audit Trail - 审计轨迹3. Tax Compliance - 税务合规4. Taxpayer's Rights - 纳税人权益5. Tax Assessment - 税务评估6. Tax Penalty - 税务罚款7. Tax Fraud - 税务欺诈五、国际税务(International Taxation)1. Double Taxation - 双重征税2. Tax Treaty - 税收协定3. Transfer Pricing - 转让定价4. Base Erosion and Profit Shifting (BEPS) - 基地侵蚀和利润转移5. Controlled Foreign Corporation (CFC) - 受控外国公司6. Permanent Establishment (PE) - 永久机构7. Thin Capitalization - 薄资本化六、税务报告(Tax Reporting)1. Financial Statements - 财务报表2. Tax Provision - 税务准备3. Taxable Year - 纳税年度4. Taxable Period - 纳税期间5. Taxable Event - 应税事件6. Withholding Tax - 预扣税7. Taxable Gain - 应税收益8. Tax Loss - 税务损失七、税务筹划(Tax Planning)1. Tax Incentives - 税收激励措施2. Tax Credits - 税收抵免3. Tax Shelters - 避税港4. Offshore Tax Planning - 离岸税务筹划5. Tax Optimization - 税务优化6. Tax Haven - 避税天堂八、税务法律(Tax Laws)1. Tax Code - 税法典2. Tax Regulations - 税法规定3. Tax Treaties - 税收协定4. Tax Court Rulings - 税务法院裁决5. Tax Dispute Resolution - 税务争议解决结语:以上是一些常用的税务专业英语词汇,涵盖了税收类型、税务部门、纳税申报、税务审计、国际税务、税务报告、税务筹划和税务法律等方面。

会计专业英语词汇

Depreciation 折旧

Direct method 直接法

Discontinued operation 终止营业

Distribution cost 销售费用

Equity method 权益法

Finance cost 财务费用

Financing activities 筹资活动

Investment 投资

Mortgage 抵押借款

Multiple-step from 多步式

Non-current asset 非流动资产

Notes payable 应付账款

Operating activities 投资活动

Operating cycle 营业周期

Prepaid expense 预付费用

Cash and cash equivalents 现金及现金等价物

Cash basis 现金收付制

Cash flow statement 现金流量表

Certified public accountant 注册会计师

Corporation 公司

Cost accounting 成本会计

Economic entity 经济实力

Internal auditing 内部审计

International Accounting StandardBoard 国际会计准则理事会

Managerial(management) accounting 管理会计

(monetary) unit of measurement 货币计量

Not-for-profits 非营利组织

Prudenceconcept 谨慎性原则

Raw material 原材料

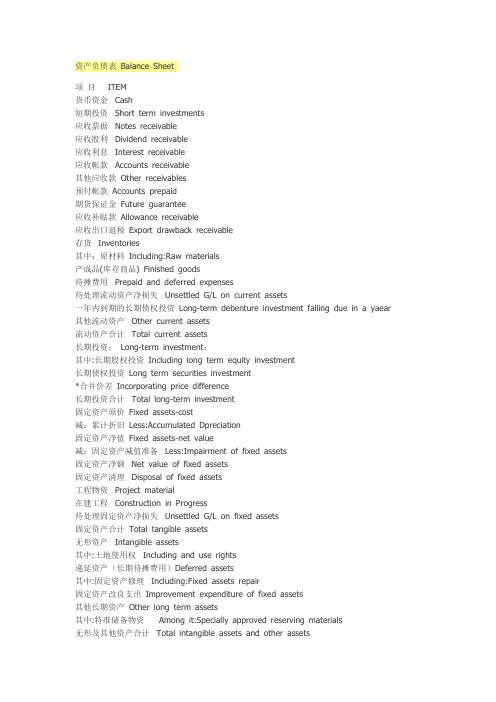

三大会计报表中英文对照

资产负债表Balance Sheet项目ITEM货币资金Cash短期投资Short term investments应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收帐款Accounts receivable其他应收款Other receivables预付帐款Accounts prepaid期货保证金Future guarantee应收补贴款Allowance receivable应收出口退税Export drawback receivable存货Inventories其中:原材料Including:Raw materials产成品(库存商品) Finished goods待摊费用Prepaid and deferred expenses待处理流动资产净损失Unsettled G/L on current assets一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets流动资产合计Total current assets长期投资:Long-term investment:其中:长期股权投资Including long term equity investment长期债权投资Long term securities investment*合并价差Incorporating price difference长期投资合计Total long-term investment固定资产原价Fixed assets-cost减:累计折旧Less:Accumulated Dpreciation固定资产净值Fixed assets-net value减:固定资产减值准备Less:Impairment of fixed assets固定资产净额Net value of fixed assets固定资产清理Disposal of fixed assets工程物资Project material在建工程Construction in Progress待处理固定资产净损失Unsettled G/L on fixed assets固定资产合计Total tangible assets无形资产Intangible assets其中:土地使用权Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理Including:Fixed assets repair固定资产改良支出Improvement expenditure of fixed assets其他长期资产Other long term assets其中:特准储备物资Among it:Specially approved reserving materials无形及其他资产合计Total intangible assets and other assets递延税款借项Deferred assets debits资产总计Total Assets资产负债表(续表) Balance Sheet项目ITEM短期借款Short-term loans应付票款Notes payable应付帐款Accounts payab1e预收帐款Advances from customers应付工资Accrued payro1l应付福利费Welfare payable应付利润(股利) Profits payab1e应交税金Taxes payable其他应交款Other payable to government其他应付款Other creditors预提费用Provision for expenses预计负债Accrued liabilities一年内到期的长期负债Long term liabilities due within one year 其他流动负债Other current liabilities流动负债合计Total current liabilities长期借款Long-term loans payable应付债券Bonds payable长期应付款long-term accounts payable专项应付款Special accounts payable其他长期负债Other long-term liabilities其中:特准储备资金Including:Special reserve fund长期负债合计Total long term liabilities递延税款贷项Deferred taxation credit负债合计Total liabilities* 少数股东权益Minority interests实收资本(股本) Subscribed Capital国家资本National capital集体资本Collective capital法人资本Legal person"s capital其中:国有法人资本Including:State-owned legal person"s capital 集体法人资本Collective legal person"s capital个人资本Personal capital外商资本Foreign businessmen"s capital资本公积Capital surplus盈余公积surplus reserve其中:法定盈余公积Including:statutory surplus reserve公益金public welfare fund补充流动资本Supplermentary current capital* 未确认的投资损失(以“-”号填列)Unaffirmed investment loss未分配利润Retained earnings外币报表折算差额Converted difference in Foreign Currency Statements所有者权益合计Total shareholder"s equity负债及所有者权益总计Total Liabilities & Equity利润表INCOME STATEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales减:销售折扣与折让Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales减:销售费用Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years利润总额Total profit减:所得税Less:Income tax净利润Net profit现金流量表Cash Flows StatementPrepared by:Period: Unit:Items1.Cash Flows from Operating Activities:01)Cash received from sales of goods or rendering of services02)Rental receivedValue added tax on sales received and refunds of value03)added tax paid04)Refund of other taxes and levy other than value added tax07)Other cash received relating to operating activities08)Sub-total of cash inflows09)Cash paid for goods and services10)Cash paid for operating leases11)Cash paid to and on behalf of employees12)Value added tax on purchases paid13)Income tax paid14)Taxes paid other than value added tax and income tax17)Other cash paid relating to operating activities18)Sub-total of cash outflows19)Net cash flows from operating activities2.Cash Flows from Investing Activities:20)Cash received from return of investments21)Cash received from distribution of dividends or profits22)Cash received from bond interest incomeNet cash received from disposal of fixed assets,intangible 23)assets and other long-term assets26)Other cash received relating to investing activities27)Sub-total of cash inflowsCash paid to acquire fixed assets,intangible assets28)and other long-term assets29)Cash paid to acquire equity investments30)Cash paid to acquire debt investments33)Other cash paid relating to investing activities34)Sub-total of cash outflows35)Net cash flows from investing activities3.Cash Flows from Financing Activities:36)Proceeds from issuing shares37)Proceeds from issuing bonds38)Proceeds from borrowings41)Other proceeds relating to financing activities42)Sub-total of cash inflows43)Cash repayments of amounts borrowed44)Cash payments of expenses on any financing activities45)Cash payments for distribution of dividends or profits46)Cash payments of interest expenses47)Cash payments for finance leases48)Cash payments for reduction of registered capital51)Other cash payments relating to financing activities52)Sub-total of cash outflows53)Net cash flows from financing activities4.Effect of Foreign Exchange Rate Changes on Cash Increase in Cash and Cash EquivalentsSupplemental Information1.Investing and Financing Activities that do not Involve in Cash Receipts and Payments56)Repayment of debts by the transfer of fixed assets57)Repayment of debts by the transfer of investments58)Investments in the form of fixed assets59)Repayments of debts by the transfer of investories2.Reconciliation of Net Profit to Cash Flows from Operating Activities62)Net profit63)Add provision for bad debt or bad debt written off64)Depreciation of fixed assets65)Amortization of intangible assetsLosses on disposal of fixed assets,intangible assets66)and other long-term assets (or deduct:gains)67)Losses on scrapping of fixed assets68)Financial expenses69)Losses arising from investments (or deduct:gains)70)Defered tax credit (or deduct:debit)71)Decrease in inventories (or deduct:increase)72)Decrease in operating receivables (or deduct:increase)73)Increase in operating payables (or deduct:decrease)74)Net payment on value added tax (or deduct:net receipts75)Net cash flows from operating activities Increase in Cash and Cash Equivalents76)cash at the end of the period77)Less:cash at the beginning of the period78)Plus:cash equivalents at the end of the period79)Less:cash equivalents at the beginning of the period80)Net increase in cash and cash equivalents现金流量表的现金流量声明拟制人:时间:单位:项目1.cash流量从经营活动:01 )所收到的现金从销售货物或提供劳务02 )收到的租金增值税销售额收到退款的价值03 )增值税缴纳04 )退回的其他税收和征费以外的增值税07 )其他现金收到有关经营活动08 )分,总现金流入量09 )用现金支付的商品和服务10 )用现金支付经营租赁11 )用现金支付,并代表员工12 )增值税购货支付13 )所得税的缴纳14 )支付的税款以外的增值税和所得税17 )其他现金支付有关的经营活动18 )分,总的现金流出19 )净经营活动的现金流量2.cash流向与投资活动:20 )所收到的现金收回投资21 )所收到的现金从分配股利,利润22 )所收到的现金从国债利息收入现金净额收到的处置固定资产,无形资产23 )资产和其他长期资产26 )其他收到的现金与投资活动27 )小计的现金流入量用现金支付购建固定资产,无形资产28 )和其他长期资产29 )用现金支付,以获取股权投资30 )用现金支付收购债权投资33 )其他现金支付的有关投资活动34 )分,总的现金流出35 )的净现金流量,投资活动产生3.cash流量筹资活动:36 )的收益,从发行股票37 )的收益,由发行债券38 )的收益,由借款41 )其他收益有关的融资活动42 ),小计的现金流入量43 )的现金偿还债务所支付的44 )现金支付的费用,对任何融资活动45 )支付现金,分配股利或利润46 )以现金支付的利息费用47 )以现金支付,融资租赁48 )以现金支付,减少注册资本51 )其他现金收支有关的融资活动52 )分,总的现金流出53 )的净现金流量从融资活动4.effect的外汇汇率变动对现金增加现金和现金等价物补充资料1.investing活动和筹资活动,不参与现金收款和付款56 )偿还债务的转让固定资产57 )偿还债务的转移投资58 )投资在形成固定资产59 )偿还债务的转移库存量2.reconciliation净利润现金流量从经营活动62 )净利润63 )补充规定的坏帐或不良债务注销64 )固定资产折旧65 )无形资产摊销损失处置固定资产,无形资产66 )和其他长期资产(或减:收益)67 )损失固定资产报废68 )财务费用69 )引起的损失由投资管理(或减:收益)70 )defered税收抵免(或减:借记卡)71 )减少存货(或减:增加)72 )减少经营性应收(或减:增加)73 )增加的经营应付账款(或减:减少)74 )净支付的增值税(或减:收益净额75 )净经营活动的现金流量增加现金和现金等价物76 )的现金,在此期限结束77 )减:现金期开始78 )加:现金等价物在此期限结束79 )减:现金等价物期开始80 ),净增加现金和现金等价物。

增值税暂行条例中英文对照

中华人民共和国增值税暂行条例The Provisional Regulations of the People‘s Republic of China on Value-Added Tax第一条在中华人民共和国境内销售货物或者提供加工、修理修配劳务以及进口货物的单位和个人,为增值税的纳税义务人(以下简称纳税人),应当依照本条例缴纳增值税。

Article 1 All units and individuals engaged in the sales of goods,provision of processing,repairs and replac ement services,and the importation of goods within the territory of the People“s Republic of China are taxpayers of Value-Added Tax (heteinafter referred to as ”taxpayers“),and shall pay VAT in acco rdance with these Regulations.第二条增值税税率:Article 2 VAT rates:(一)纳税人销售或者进口货物,除本条第(二)项、第(三)项规定外,税率为17%。

(1)For taxpayers selling or importing goods,other than those stipulated in items (2)and (3)of this Article,the tax rate shall be 17%.(二)纳税人销售或者进口下列货物,税率为13%:(2)For taxpayers selling or importing the following goods,the tax rate shall be 13%:1.粮食、食用植物油;i.Food grains,edible vegetable oils;2.自来水、暖气、冷气、热水、煤气、石油液化气、天然气、沼气、居民用煤炭制品;ii. Tap water,heating,air conditioning,hot water,coal gas,lipuefied petroleum gas,naturalgas,methane gas,coal/charcoal products for household use;3.图书、报纸、杂志;iii. Books,newspapers,magazines;4.饲料、化肥、农药、农机、农膜;iv. Feeds,chemical fertilizers,agricultural chemicals,agricultural machinery and covering plastic film for farming;5.国务院规定的其他货物。

税务相关英文单词

TAX营业税:business tax or turnover tax消费税:excise tax or consumption tax增值税:value added tax关税:custom duty印花税:stamp tax土地增值税:land appreciation tax or increment tax on land value个人所得税:individual income tax企业所得税:income tax on corporate business外商投资企业所得税:income tax on foreign investment enterprises城市维护建设税:city maintenance construction tax资源税:resource tax房产税:house property tax土地使用税:land use tax车船使用税:operation tax of vehicle and ship耕地占用税:farmland use tax教育费附加:extra charges of education fundsState Administration for Taxation 国家税务总局Yangzhou Taxation Training College of State Administration of Taxation国家税务总局扬州税务进修学院Local Taxation bureau 地方税务局外汇管理局:Foreign Exchange Control Board海关:customs财政局:finance bureau统计局:Statistics Bureau工商行政管理局:Administration of Industry and Commerce出入境检验检疫局:Administration for EntryExit Inspection and Quarantine 中国证监会:China Securities Regulatory Commission (CSRS)劳动和社会保障部:Ministry of Labour and Social Securitytax returns filing 纳税申报tax payable 应交税金the assessable period for tax payment 纳税期限the timing of tax liability arising 纳税义务发生时间consolidate reporting 合并申报the local competent tax authority 当地主管税务机关the outbound business activity 外出经营活动Tax Inspection Report 纳税检查报告tax avoidance 逃税tax evasion 避税tax base 税基refund after collection 先征后退withhold and remit tax 代扣代缴collect and remit tax 代收代缴income from authors remuneration 稿酬所得income from remuneration for personal service 劳务报酬所得income from lease of property 财产租赁所得income from transfer of property 财产转让所得contingent income 偶然所得resident 居民non-resident 非居民tax year 纳税年度temporary trips out of 临时离境flat rate 比例税率withholding income tax 预提税withholding at source 源泉扣缴State Treasury 国库tax preference 税收优惠the first profit-making year 第一个获利年度refund of the income tax paid on the reinvested amount 再投资退税export-oriented enterprise 出口型企业technologically advanced enterprise 先进技术企业Special Economic Zone 经济特区accept 受理accounting software 会计核算软件affix 盖章application letter 申请报告apply for reimbursement 申请退税apply for a hearing 申请听证apply for nullifying the tax registration 税务登记注销apply for reimbursement of tax payment 申请退税ask for 征求audit 审核author’s remuneration 稿酬;稿费averment 申辩bill/voucher 票证bulletin 公告bulletin board 公告牌business ID number 企业代码business license 营业执照call one’s number 叫号carry out/enforce/implement 执行check 核对check on the cancellation of the tax return 注销税务登记核查checking the tax returns 审核申报表city property tax 城市房地产税company-owned 公司自有的conduct an investigation/investigate 调查construction contract 建筑工程合同]cconsult; consultation 咨询<consulting service/advisory service 咨询服务contact 联系contract 承包copy 复印;副本deduct 扣除delay in filing tax returns 延期申报(缴纳)税款describe/explain 说明document 文件;资料examine and approve 审批extend the deadline for filing tax returns 延期税务申报feedback 反馈file tax returns(online) (网上)纳税申报fill out/in 填写foreign-owned enterprise 外资企业hearing 听证ID(identification) 工作证`Identical with the original 与原件一样IIT(Individual income tax) 个人所得税Implementation 稽查执行income 收入;所得inform/tell 告诉information desk 咨询台inspect 稽查inspection notice 稽查通知书instructions 使用说明invoice book(purchase) 发票购领本invoice 发票invoice tax control machine 发票税控机legal person 法人代表letter of settlement for tax inspection 稽查处理决定书list 清单local tax for education 教育地方附加费lunch breakmake a supplementary payment 补缴make one’s debut in handling tax affairs 初次办理涉税事项manuscript 底稿materials of proof 举证材料material 资料modify 修改modify one’s tax return 税务变更登记Nanjing Local Taxation Bureau 南京市地方税务局Notice 告知nullify 注销office building 办公楼office stationery 办公用品on-the-spot service 上门服务on-the-spot tax inspection 上门稽查opinion 意见original value 原值pay an overdue tax bill 补缴税款pay 缴纳penalty 处罚penalty fee for overdue payment 滞纳金penalty fee 罚款personal contact 面谈post/mail/send sth by mail 邮寄procedure/formality 手续proof material to backup tax returns 税收举证资料purchase 购领real estate 房产receipt 回执;反馈单record 记录reference number 顺序号register outward business administration 外出经营登记relevant materials of proof 举证资料rent 出租reply/answer 答复sell and pay foreign exchange 售付汇service trade 服务业settlement 处理settle 结算show/present 出示special invoice books of service trade 服务业发票stamp 公章submit a written application letter 提供书面申请报告supervision hotline 监督电话tax inspection bureau 稽查局tax inspection permit 税务检查证tax inspection 税务稽查tax law 税法tax officer 办税人tax payable/tax applicable 应缴税tax payment assessment 纳税评估tax payment receipt 完税凭证tax payment 税款tax rate 税率tax reduction or exemption 减免税tax registration number 纳税登记号tax registration certificate 税务登记证tax registration 税务登记tax related documents 涉税资料tax return/tax bill 税单tax return forms and the acknowledgement of receipt 申报表回执tax returns 纳税申报表tax voucher 凭证the accounting software 会计核算软件the acknowledgement of receipt 送达回证the application for an income refund 收入退还清单the author’s remuneration 稿费the business ID number 企业代码the certificate for outward business administration 外出经营管理证明the certificate for exchange of invoice 换票证the deadline 规定期限the inspection statement/report 检查底稿the legal person 法人代表the letter of statement and averment 陈述申辩书the online web address for filling tax returns 纳税申报网络地址the penalty fee for the overdue tax payment 税款滞纳金the penalty notice 处罚告知书the real estate 房产the registration number of the tax returns 纳税登记号the special invoice of service trade 服务业专用发票the special nationwide special invoice stamp 发票专用章the special nationwide invoice stamp 发票专用章the State Administration of Taxation 国家税务局supervision of taxation 税收监督tax inspection department 税务稽查局tax inspection permit 税务检查证tax officer 办税人员tax return form 纳税申报表格tax voucher application for the sale and purchase of foreign exchange 售付汇税务凭证申请审批表the use of invoice 发票使用trading contract 购销合同transportation business 运输业under the rate on value method 从价urban house-land tax 城市房地产税V AT(value-added tax, value added tax) 增值税Written application letter 书面申请报告。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Value Added Tax and Direct TaxationSimilarities and DifferencesSample excerptTAX TREATIES — A SOLUTION TO VAT/GST DOUBLE TAXATIONThomas Ecker1I. The problem of double taxation in VAT/GSTConsumption taxes, such as value added taxes (VAT), goods and services taxes (GST), or retail sales taxes, have been around for about 60 years and, thus, are fairly young compared to direct taxes. Nevertheless, VAT has been spreading with enormous speed and as of early 2006, there were around 140 countries with a VAT of some sort.2Over 100 of those countries have introduced VAT within the last 20 years.3 In the future, the number of countries relying on VAT is expected to increase further.Simultaneously, globalization and rapid improvements in technology have led to a drastic increase in global trade and international cross-border activities. The two developments — the spread of VAT and the increase in cross-border economic activities — have together led to a new situation where global actors regularly have to deal with two or more different VAT jurisdictions when carrying on international business. In some of these cases, as a consequence of the absence of internationally agreed principles, more than one country may want to levy tax on a cross-border transaction. The result is double or multiple taxation (or in the inverse case: double or multiple non-taxation).4 The harmful effects of double taxation (such as distortion of competition) on the exchange of goods and services and movements of capital, technology and persons are so well known that it is scarcely necessary to stress the importance of removing the obstacle that double taxation presents to the development of economic relations between countries.5The most common reasons for double taxation are:6−the use of different rules to determine the place of taxation;1The author would like to thank Prof. Rick Krever and Prof. Michael Lang for the discussion and helpful comments on this paper.2See Bird/Gendron, The VAT in Developing and Transitional Countries(2007) p. 16; see also OECD, Consumption Tax Trends 2008 (2008), p. 32.3International Tax Dialogue, The Value Added Tax: Experiences and Issues, prepared for the ITD Conference on the VAT, Rome March 15–16, 2005, p. 9.4For some examples see Millar, “Cross-Border Services: A Survey of the Issues”, New Zealand Journal of Taxation Law and Policy 2007, pp. 302 et seq.; OECD, Report – The application of consumption taxes to the trade in international services and intangibles, 2004, pp. 8 et seq.; see generally also Ruppe, General Report, Cahiers de Droit Fiscal International, Volume. LXVIIIb (1983) p. 109 (pp. 121 et seq.).5See para. 1 of the introduction to the OECD Model.6See OECD, The Application of Consumption Taxes to the International Trade in Services and Intangibles – Progress Report and Draft Principles, 2005, p. 3; Erikson, “Should Tax Treaties Play a Role for Consumption Taxes?”, Intertax 2005, p. 166 (p. 168); Millar, “GST issues for international services transactions”, Australian GST Journal 2004, p. 285 (pp. 288 et seq.).−different interpretation of (otherwise similar) place of taxation rules, the order of these rules, or a different interpretation of the surrounding key proxies and concepts for determining the place of taxation;−different characterization of a transaction (even if similar rules are in place to determine the place of taxation);−non-recoverability of tax; and−input taxation without the right to deduction in one country (e.g. because the taxpayer’s supplies are exempt in that country) while the same supply is subject to VAT/GST in another country.This paper will only deal with the first three of the above-mentioned reasons for double taxation. It aims especially at providing a contribution to solve double taxation caused by different place of taxation rules. The non-recoverability of tax7and the problem of input taxed supplies that are taxable in another country are not a subject of the paper.8As VAT is harmonized within the European Community (EC), it is not surprising that the risk of double taxation is not as common between the Member States of the European Union (EU) as it may be between EU Member States and third countries. And if, despite the harmonized rules, VAT double taxation occurs within the European Common Market, it is usually the responsibility of the European Court of Justice (ECJ) to solve this issue.9 Therefore, this contribution will not cover mere EU cases. It will only address the question of double taxation between an EU Member State and a non-EU Member State as well as between two non-EU Member States.10II. A proposed solution – VAT/GST treatiesThere are multiple ways to address the issue of double taxation in VAT/GST. One way to resolve double taxation problems is unilateral measures that by themselves avoid double taxation. One country voluntarily (i.e. without being obliged e.g. by means of a bi- or multilateral agreement) introduces a regulation into its domestic law to relieve a taxpayer if he is also taxed in another country. This domestic measure generally provides for an exemption of domestic tax or for a credit of foreign tax on the domestic tax liability. In practice, however, these unilateral measures for different reasons only rarely provide relief. In many countries, regulations that unilaterally avoid double taxation are not applicable to VAT or GST. Where consumption taxes fall under the scope of such a provision, it is often applied only in the case of reciprocity, i.e. the other country taxing the transaction has a similar provision in its domestic law. Furthermore, it is possible that countries that have unilateral domestic7The extensive use of the destination principle and the direct applicability of the treaty benefits should, however, be able to abate this problem.8Although, admittedly, tax treaties could also be used to foster recoverability of tax, e.g. through the inclusion of a reciprocity clause for refunds.9See e.g. European Commission, Consultation paper – Introduction of a mechanism for eliminating double imposition of VAT in individual cases, 5 January 2007, TAXUD/D1/…., p. 3; a different interpretation of facts may, however, still lead to double taxation. For this reason the Commission proposes the introduction of a mutual agreement and arbitration procedure in these cases (see same document).10The question as to who has the power to conclude treaties in an EU context is not treated in this paper. Further research is needed to assess whether the EU Member States still have the power to negotiate and conclude VAT/GST treaties. As VAT is harmonized within the European Union, it may be that this power now lies with the European Commission. It further has to be analysed whether the EU Member States even have the power to discuss and agree on a VAT/GST model convention, for example, in an OECD context.provisions to avoid double taxation, only apply them if the person liable for VAT/GST is a resident of that country.11 Additionally, these provisions often do not provide the taxpayer with an enforceable right but rather grant the tax administration a discretionary power to apply them. The consequence is legal uncertainty.Another means to avoid VAT/GST double taxation is through coordination of national tax laws. The idea behind this concept is to promote assimilation of the different national taxing regimes, for instance through the development of international consumption tax principles. This is the path currently followed by the OECD. Since the late 1990s, the OECD’s Committee on Fiscal Affairs (CFA) has been aware of the obstacles to economic activity of businesses that are created by today’s international consumption taxes environment. As a consequence, the CFA assigned Working Party No. 9 (WP9) with the development of international VAT/GST principles that should serve national legislators as basis for the design of their country’s VAT/GST and thus, should lead to an assimilation of the different legal consumption tax systems worldwide. In February 2006, the OECD published the first part of the International VAT/GST Guidelines.12 Since that time, WP9 and its Technical Advisory Groups have been working to further develop and complete these guidelines, a task that is expected to take another couple of years.A third and very innovative measure to avoid consumption tax double taxation would be the development of separate bi- or multilateral VAT/GST treaties. This approach is supported from many sides including scholars, business representatives, or officials of international organizations.13With respect to income taxes, tax treaties have established themselves as the most used and accepted measure to tackle double taxation. Nowadays over 3,000 tax treaties are in place between countries worldwide. The presented instruments to address the issue of VAT/GST double taxation are not mutually exclusive but rather can be combined. The use of one measure does not necessarily exclude the application of the other measures. The use of tax treaties might especially be considered relevant if international tax coordination (such as through OECD International VAT/GST Guidelines) proves to be ineffective or insufficient. In any way, the development of such guidelines will provide a useful basis for the development of a VAT/GST model tax convention as they are expected to represent internationally agreed principles.But if states decided to agree on VAT/GST treaties, what should these tax treaties look like? How should they work and how should they be structured? What should be their scope, and who should get a right to tax? These are questions that will be dealt in this paper. The drafting of a complete model tax treaty is not realistic at this point 11See, for example, the former practice of the Austrian Ministry of Finance until the Austrian Supreme Administrative Court (hereinafter VwGH) decided differently (see VwGH, 29 January 2008, 95/15/0043, Österreichische Steuerzeitung 1998, p. 609 et seq.).12OECD, International VAT/GST Guidelines (OECD VAT/GST Guidelines), February 2006.13See e.g. Williams, Trends in International Taxation(1991), p. 170; White, “The Serious Research Gap on VAT/GST: A New Zealand Perspective after 20 years of GST”, IBFD International VAT Monitor 2007, p. 343 (p. 349); Arnold/Sasseville/Zolt, “Summary of the Proceedings of an Invitational Seminar on Tax Treaties in the 21st Century”, IBFD Bulletin for International Taxation 2002, p. 233 (p. 235); Erikson, Intertax 2005, p. 166 et seq.; Westberg, Cross-Border Taxation of E-Commerce(2002) pp. 177 and 242; Westberg, Nordisk Mervärdesskatterät(1994) pp. 511 and 525; Angel Gurría and Jeffrey Owens, both at the 50th Anniversary of the OECD Model Tax Convention conference in Paris on 8 September 2008 (see e.g. OECD, Conference on the 50th Anniversary of the OECD Model Tax Convention, remarks by Angel Gurría, 2008); see also some of the contributions in this book.as we are only at the beginning of the scientific discourse on this topic.14 I will rather try to address some basic points, identify issues that have to be dealt with, show possible solutions, and make some suggestions on how such a VAT/GST tax treaty could be shaped. This paper should be understood as a starting point for discussion rather than as a complete proposal. It is meant to be a first step to close the “research gap”15 on consumption tax treaties.III. Income tax treaties as starting point for development of a VAT/GST treaty 1. Use of concept and structure of income tax treatiesCurrently, there are no consumption tax treaties in place16which could serve as a model for such VAT/GST treaties. Therefore, when designing a new VAT/GST Model Convention, it seems obvious to start with something that already exists and is already broadly accepted: income tax treaties. Although income taxes and indirect taxes are very different, the underlying ideas of such income tax treaties and — going even further — their concept and structure should be analysed to see if they can be used for VAT/GST treaty purposes.……………….3. Personal scope in separate independent VAT/GST treatiesIn case states prefer to develop independent VAT/GST treaties, separate from income tax treaties, the issue of a restriction of the personal scope of these treaties arises as well. Should treaty applicability be made dependent on residence of a taxpayer (or any other person) in one of the contracting states? Is a limitation of the personal scope necessary or desirable at all?If states decided that they do not want to make treaty application dependent on the residence of the taxpayer (e.g. for reasons mentioned in the previous section), it has to be analysed whether the treaty scope should be limited to other persons resident in one of the contracting states. Again, a difference between income taxes and VAT/GST may become an issue in this respect. Simply put, income taxes only know two connecting factors that allow taxation in a state: the person that derives the income and the source of the income. In contrast, VAT/GST generally knows three connecting factors that may allow taxation of a supply: the supplier, the customer and the “source” (i.e. for instance the place of performance or where property is situated, etc.). This phenomenon, however, is not unique to VAT/GST. There are also other taxes that use three connecting factors for taxation. And some of these taxes are also covered by tax treaties. Inheritance taxes, for instance, usually view the deceased, the heir (or legatee) and again the “source” (i.e. certain property such as immovable 14Eriksen accurately sees the international VAT environment in an “embryonic stage” compared to the international income tax environment (see Erikson, Intertax 2005, p. 166).15See e.g. White, IBFD International VAT Monitor 2007, pp. 343 et seq.16Admittedly, primary (together with secondary) EC law could be seen as treaties dealing with VAT. Furthermore, a few bilateral treaties mention VAT in respect of ships or aircraft in international traffic and some provisions of income tax treaties following the OECD Model are also applicable to VAT (see section Error! Reference source not found., see also the contribution by Bourgeois/Römer, “Effects of Existing Tax Treaties on VAT (Relevance of Arts. 24–27 OECD Model for VAT/GST)”, in this book. But there are no comprehensive VAT/GST treaties that are comparable to income tax treaties (see Erikson, Intertax 2005, p. 166).property) situated in their territory as connecting factors.17 Thus, it seems valuable to assess whether the path chosen for inheritance tax treaties may also be useful for VAT/GST treaty purposes.18The OECD Estates, Inheritances and Gifts Model Convention does not refer to a “taxpayer” for the personal scope of the treaty but to the deceased. Art. 1 of this convention provides that it applies “to estates and inheritances where the deceased was domiciled, at the time of his death, in one or both of the Contracting States”. Transforming this solution to VAT/GST, this would mean that treaty application is made dependent solely on the residence (or location) of the supplier or solely on the residence (or location) of the customer. However, there is one difference between inheritance tax treaties and potential VAT/GST treaties that might cause problems in this respect. Inheritance tax treaties only have one main rule which refers to the same criterion (the deceased) as the rule governing the personal scope of the treaty. Inheritance tax treaties usually apply if the deceased is domiciled in one of the contracting states.19At the same time, the main rule (if no exceptions are applied) allocates the right to tax to the state of domicile of the deceased. With respect to VAT/GST treaties, the situation could be different, especially if states were to use the 2010 EU place of supply rules as basis for VAT/GST treaty allocation rules. There would be two main rules for services (mainly depending on whether the supply is B2B or B2C) and again other rules for supplies of goods. So if, e.g. treaty entitlement would depend on the customer location and the main allocation rule for the supply in question (e.g. a B2C supply) would be the supplier location then there will be cases where double taxation cannot be effectively avoided despite the existence of tax treaties. The following cases should illustrate the issue:Assume a supplier in state A performs services in state B for a customer in state C. There are tax treaties between all three states. The tax treaties only apply if the customer is located in one of the contracting states. As the customer is located in state C, only state C’s tax treaties are applicable. The treaty between state A and state B is not applicable. The treaties further provide for the supply in question that only the state where the supplier is located (main rule) has the right to levy tax unless the service is performed in the other contracting state (exception to the main rule). Following these allocation rules, state A’s and state B’s taxing rights are not restricted by the treaties concluded with state C. As the treaty between state A and state B is not applicable, consequently (if both state A and state B tax the supply under their domestic law) there would be double taxation even though there is a treaty in place between these two countries.Under the OECD Estates, Inheritances and Gifts Model Convention this problem cannot occur. Both the personal scope provision of the convention and the main rule refer to the same person: the deceased. Thus, in a case where multiple states want to levy tax (e.g. because the deceased, the heir and immovable property are in different states), the treaties concluded by the state where the deceased was domiciled limit the taxing rights of all treaty partners except for the state where an exception to the main rule applies (e.g. where the immovable property is situated). Consequently, in a situation where all countries have concluded such treaties, it does 17See e.g. OECD Commentary on the Model Double Taxation Convention on Estates and Inheritances and on Gifts, Introductory report by the Committee on Fiscal Affairs, paras. 19–20.18See also section 0.19See Art. 1 OECD Inheritance Tax Model.not matter that the treaty between the heir’s state and the state where the immovable property is situated, does not apply. The heir’s state’s taxing rights are already limited by the treaty concluded with the state where the deceased was domiciled.To sum up, it has been shown that reference for treaty application to either only the supplier location or only the customer location might lead to situations where despite the existence of a tax treaty double taxation cannot always be avoided. This may happen if treaty allocation rules would follow two or more main rules (e.g. if they follow the two different main rules in the 2010 EU VAT system for B2B and B2C services). This could also happen — even if there is just one main rule — if not all states that claim taxing rights have concluded tax treaties with each other.20Thus, the issue remains how the personal scope of tax treaties should be limited. Should reference be made to the supplier, to the customer, or both? Or should VAT/GST treaties not be limited in their personal scope at all?………………….5. Distributive rulesAs already discussed,21 the use of distributive rules seems to be a well-suited way in a VAT/GST treaty to solve the conflict of competence between two or more states that would tax a transaction under their domestic law. Distributive rules generally limit the taxing rights of one or more of the contracting states. This is also the mechanism used in income tax treaties.Income tax treaties contain in Art. 21 of the OECD Model a distributive rule that is applicable if all other distributive rules in the treaty are not applicable. Thus, it is a kind of catch-all clause.22From its systematic function it can be compared to the main rule as identified for VAT purposes. It is applicable unless an “exception” is needed and consequently one of the other distributive rules (Arts. 6 to 20 of the OECD Model) is applied. The only problem is that, of course, for income tax the name “exceptions” would not really fit the other distributive rules as many of them are used more often than Art. 21 of the OECD Model.A similar concept seems appropriate for potential VAT/GST treaties as well. It would be desirable to have a main rule and — where necessary — exceptions to the main rule. Whether or not a different set of distributive rules (and consequently different main rules) may be desirable depending on the kind of supply and the type of customer needs further analysis. As income tax treaty rules generally refer to “income”, “profits”, “gains”, “capital”, and the like, they are currently not suited to allocating the VAT/GST taxing right for a supply. Thus, for VAT/GST purposes, 20Imagine, e.g. a supplier in State A providing a service in StateB for a customer in State C. Assume that all countries claim a taxing right under their domestic law on this supply. Further imagine that VAT/GST treaties have been concluded between State A and State B as well as between State B and State C. There is, however, no treaty between State A and State C. Further assume that in order for the treaties to apply, the treaties provide that the customer must be located in one of the contracting states. As a consequence, the treaty between State A and State B would not be applicable. Neither State A’s nor State B’s taxing rights would be limited by the applicable treaties. If now, for the service in question, the treaties allocate the taxing right to the state where the customer is located (main rule) unless the service is performed in the other contracting state (exception to the main rule), State B would keep its taxing right. Only StateC would be limited in its taxing right. As a result, both State A and State B would not be limited in their taxing rights. Double taxation would occur although there is a treaty in place between these two states.21See sections 0.22See Vogel, DTC³, Art. 21 MN 19.different, independent rules are needed or income tax rules would have to be adapted. For the development of independent allocation rules one should consider existing allocation rules. In this respect, the EU VAT system seems more useful as model for treaty allocation rules than, for example, the New Zealand system. The New Zealand rules merely decide on a yes/no basis whether the country applying the law has substantive jurisdiction. In contrast, the EU place of supply rules — at least for supplies within the Common Market – also decide which other country has substantive jurisdiction, in case the former country does not have substantive jurisdiction. Thus, the EU place of supply rules, as provided for in the EU VAT Directive, perform a more extensive allocation function.23The question of which allocation rules are the best suited for VAT/GST treaties needs further research. The decision should take into account the purpose and principles of VAT/GST and the rules should be neutral, efficient, certain and simple, effective and fair and flexible.24…………………IV. ConclusionIt has been shown that VAT/GST tax treaties, combined with measures of international cooperation, provide a useful instrument to tackle the problem of VAT/GST double taxation. The concept and structure of income tax treaties provide a good starting point for the discussion on how to shape such a VAT/GST treaty. As regards the scope of the treaty, adjustments have to be made since VAT/GST is an in rem tax and usually follows the territoriality principle. The question comes up to which persons the personal scope of the treaty should be limited. Should it refer to the taxpayer? Or should it refer to the supplier and/or customer? Or is there a limited personal scope useful for VAT/GST treaties at all? These issues have to be dealt with regardless of whether existing income tax treaties are extended to VAT/GST or whether a separate independent VAT/GST Model Convention is introduced. Furthermore, special attention has to be put on the risk of unintentional double non-taxation. It will be crucial for the political and factual success of potential VAT/GST treaties that this risk can be limited.We are only at the beginning of the scientific discourse on avoidance of double taxation in VAT/GST and further research is needed. This paper covers only some of the issues that should be considered with respect to designing potential VAT/GST treaties. Of course, there are many more issues, such as the treatment of permanent establishments, or group taxation, just to mention a few. With this paper I hope to stimulate the scientific discourse on the elimination of consumption tax double taxation. It is meant to be a first step to close the “research gap” on this issue. And who knows, maybe 50 years from now there will even be 3,000 VAT/GST treaties… or a global one.23See Millar, “Echoes of source and residence in VAT jurisdictional rules”, in this book, section III.2.1.24See also OECD VAT/GST Guidelines, I.B. para. 6.。