FRM一级练习题(3)答案

CFA考试一级章节练习题精选0329-60(附详解)

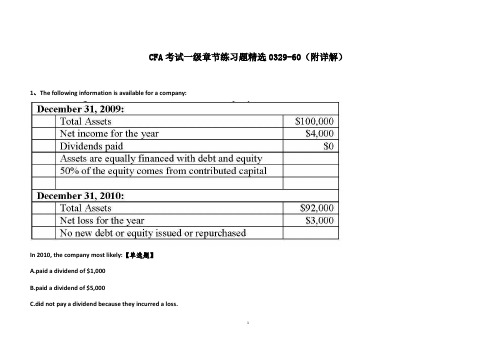

CFA考试一级章节练习题精选0329-60(附详解)1、The following information is available for a company:In 2010, the company most likely:【单选题】A.paid a dividend of $1,000B.paid a dividend of $5,000C.did not pay a dividend because they incurred a loss.正确答案:B答案解析:“Financial Reporting Mechanics,” Thomas R. Robinson, CFA, Jan Hendrik van Greuning, CFA, Karen O’Connor Rubsam, CFA, R. Elai ne Henry, CFA, and Michael A. Broihahn, CFA2010 Modular Level 1, Vol.3, pp. 43Study Session: 7-30-b, cExplain the accounting equation in its basic and expanded forms.Explain the process of recording business transactions using an accounting system based on the accounting equations.2、An analyst does research about gross profit margin and gathers the following informationabout a company in 2012 :● Average inventory is $2 000● Ending inventory of the year is $2 500● Total revenue is $20 000● Inventory turnover ratio is 5.5● Ta x rate is 40%The gross profit margin for the company is closest to:【单选题】A.27%B.31%C.45%正确答案:C答案解析:inventory turnover ratio = cost of goods sold/ average inventorygross profit = revenue - cost of goods soldgross profit margin = gross profit/ revenue所以,边际毛利率的计算如下:($20 000 - 5.5 × $2 000)/$20 000 = 45%。

FRM一级模考

FRM一级模拟题1 .If the daily returns of two assets are positively correlated, then:A. the covariance of their daily returns must be positiveB. the covariance of their daily returns must be zeroC. the covariance of their daily returns must be negativeD. nothing can be said about the covariance of their daily returnsAnswer: AIf variables are positively correlated, the covariance between the Variables will also be positive.2 .You are given that X and Y are random variables, and each of which follows a standard normal distribution with Covariance (X, Y) = 0.4. What is the variance of (5X+2Y)?A. 11.0B. 29.0C. 29.4D. 37.0Answer: DSince each variable is standardized, its variance is one. Therefore, Var(5X+2Y) = 25 x Var(X)+4xVar(Y)+2 x 5x2x Cov(X,Y) =25+4+8 = 373 . What is the covariance between populations A and B?If the variance ofA is 12, what is the variance of B?A. 10.00B. 2.89C. 8.33D. 14.40Answer:C5 . Which one of the following statements about the correlation coefficient is FALSE?A. It always ranges from -1 to +1B. A correlation coefficient of zero means that two random variables are independentC. It is a measure of linear relationship between two random variablesD. It can be calculated by scaling the covariance between two random variables Answer:BCorrelation describes the linear relationship between two variables. While we would expect to find a correlation of zero for independent .variables, finding a correlation of zero does not mean that two variables are independent.。

FRM一级模考

FRM一级模拟题1 . Assuming other things constant, bonds of equal maturity will still have different DV01 per USD 100 face value. Their DV01 per USD 100 face value will be in the following sequence of highest value to lowest value:A. Premium bonds, par bonds, zero coupon bondsB. Zero coupon bonds, Premium bonds, par bonds .C. Premium bonds, zero coupon bonds, par bondsD. Zero coupon bonds, par bonds, Premium bondsAnswer: ADVOI=PxMD/10000, price influences DVOI is larger than MD influence DVOI, zero-coupon bond have largest modified duration,premium bond smallest, But premium bond price is largest.So A is right not answer D.Duration2 .3 . What is the best estimate of the market value of a portfolio of USD 100 million invested in recently issued 6% 10-year bonds (its duration 7.802) and USD 100 million of long l0-year zero coupon bond if interest rates decline by 0.50%.A. USD 219 millionB. USD 195 millionC. USD 209 millionD. USD 206 m川ionAnswer: CStep I Total market initial value of the ponfolio =l00m+l00m=200mStep 2 WA=WB=l00m/200m=0.5Step 3 modified duration of the ponfolio = WA DA + WBDB =0.5x7.802+0.5x 10=8.901 Step4 AP = -MD x Po x Ay = -8.90lx200Mx(-50BP)/10000=8.901 MStep5 Total best estimate total market value =200 M+8.901 M=208.901 M209 M is close t0 208.901 M, so choice C4 . Which of the following is not a property of bond duration?A. For zero-coupon bonds, Macaulay duration of the bond equals its years to maturity.B. Duration is usually inversely related to the coupon of a bond.C. Duration is usually higher for higher yields to maturity.D. Duration is higher as the number of years to maturity for a bond selling at par or above increases.Answer: CIn general, the longer the term to maturity, all else equal, the greatei- the bond's duration. The greater the yield to maturity, all else equal, the lower the bond's duration. As yield decrease, theduration of bond increase at an increasing rate. So the convexity increases as the yieldsHolding yield constant, the lower the coupon, the higher the duration and the groater the convexity.So A, B and D are all right, we choice C.5 . A money markets desk holds a floating-rate note with an eight-year maturity. The interest rate is floating at three-month LIBOR rate, reset quarterly. The next reset is in one week. What is the approximate duration of the floating-rate note?A. 8 years .B. 4 yearsC. 3 months 'D. 1 weekAnswer: DDuration is not related to maturity when coupons are not fixed over the life of the investment. We know that at the next reset, the coupon on the FRN will be set at the prevailing rate. Hence, the market value of the note will be equal to par at that time. The duration or price risk is only related to the time to the next reset, which is I week here.。

FRM一级模考

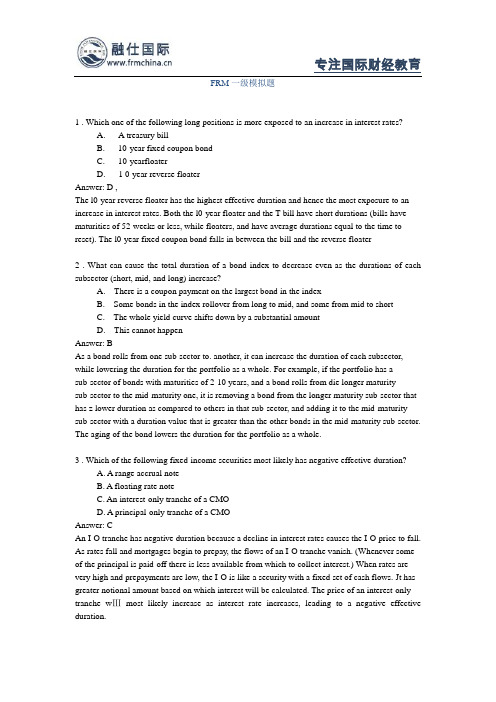

FRM一级模拟题1 . Which one of the following long positions is more exposed to an increase in interest rates?A. A treasury billB. 10-year fixed coupon bondC. 10-yearfloaterD. 1 0-year reverse floaterAnswer: D ,The l0-year reverse floater has the highest effective duration and hence the most exposure to an increase in interest rates. Both the l0-year floater and the T-bill have short durations (bills have maturities of 52-weeks or less, while floaters, and have average durations equal to the time to reset). The l0-year fixed coupon bond falls in between the bill and the reverse floater2 . What can cause the total duration of a bond index to decrease even as the durations of each subsector (short, mid, and long) increase?A. There is a coupon payment on the largest bond in the indexB. Some bonds in the index rollover from long to mid, and some from mid to shortC. The whole yield curve shifts down by a substantial amountD. This cannot happenAnswer: BAs a bond rolls from one sub-sector to. another, it can increase the duration of each subsector, while lowering the duration for the portfolio as a whole. For example, if the portfolio has asub-sector of bonds with maturities of 2-10 years, and a bond rolls from die longer maturitysub-sector to the mid-maturity one, it is removing a bond from the longer maturity sub-sector that has z lower duration as compared to others in that sub-sector, and adding it to the mid-maturity sub-sector with a duration value that is greater than the other bonds in the mid-maturity sub-sector. The aging of the bond lowers the duration for the portfolio as a whole.3 . Which of the following fixed-income securities most likely has negative effective duration?A. A range accrual noteB. A floating rate noteC. An interest-only tranche of a CMOD. A principal-only tranche of a CMOAnswer: CAn I-O tranche has negative duration because a decline in interest rates causes the I-O price to fall. As rates fall and mortgages begin to prepay, the flows of an I-O tranche vanish. (Whenever some of the principal is paid-off there is less available from which to collect interest.) When rates are very high and prepayments are low, the I-O is like a security with a fixed set of cash flows. Jt has greater notional amount based on which interest will be calculated. The price of an interest-only tranche wⅢmost likely increase as interest rate increases, leading to a negative effective duration.to maturity of 8%. Assume par value of the bond to be $1,000:A. 2.00 yearsB. 1.94 yearsC. 1.87 yearsD. 1.76 years5 . The option-adjusted duration of a callable bond will be close to the duration of a similar non-callable bond when the:A. Bond trades above the call priceB. Bond has a high volatilityC. Bond trades much lower than the call priceD. ' Bond trades above parity。

FRM一级模考

FRM一级模考FRM一级模拟题1 .Which concept gives a measure of historical value added per unit of risk taken and can be useful, among other tools, to risk managers?A. Trackingerror' B. Model alphaC. Information ratioD. HeteroskedasticityAnswer: CWilliam Sharpe developed the concept of information ratio to describe the value added per unit of risk by a manager or activity. It is usually developed by analyzing at least 36 months of returns. Tracking error is an estimate ofhow much risk a manager takes as a measure ofthe deviation from a benchmark.2.A stack-and-roti hedge as described in the Metallgesellschaft case is best described as:A. Buying futures contracts of different expirations and allowing them to expire in sequence.B. Buying futures contracts of different expirations and closing out the position shortly before expiration.C. Using short-term futures to hedge a long-term risk exposure by replacing them with longer-term contracts shortly before they expire.D. Using short-term futures contracts with a larger notional value than the long-term risk they are meant to hedge.Answer: CA stack is a bundle of futures contracts with the same expiration. Over time, a firm may acquire stacks with variousexpiry dates. To hedge a long-term risk exposure, a firm would close out each stack as it approaches expiry and enter into a contract with a more distant delivery, known as a roll.This strategy is called a stack-and-roll hedge and is designed to hedge long-term risk exposures with short-term contracts. Using short-term futures contracts with a larger notional value than the. long-term risk they are meant to hedge could result in over hedging" depending on.the hedge ratio.3 . Past financial disasters have resulted when a firm allows a trader to have dual roles as both the head of trading and the head of the back-office support function. Which of the following case studies did not involve this particular operational risk oversight?IDrysdale SecuritiesII DaiwaIII AlliedIrish BankIV BaringsA. IonlyB. II and IVC. I and IIIAnswer: CThe rogue traders for both Daiwa and Barings had dual rojes as both the head of trading and the head of the back-office support function. This operational risk oversight allowed them to hide millions in losses from senior management. In the Allied Irish Bank case, John Rusnak did not run the back-office operations. The Drysdale Securities case did not deal with a rogue trader.4 .Which of the following reasons does not help explain the problems -of LTCM inAugust and September 1998:A. A spike in correlationsB. An increase in stock index volatilitiesC. A drop in liquidity ' 'D. An increase in interest rates on on-the-run TreasuriesAnswer: DIncreased volatility and higher correlations led to substantial losses in LTCM's highly-leveraged portfolio. A significant drop in market liquidity forced LTCM to liquidate these highly-leveraged positions at substantial discounts. An increase in the spread between U.S. treasury rates and Russian government rates resulted in significant losses.5 .The following is not a problem of having one employee perform trading functionsand back office function s:A. The employee gets paid more because he performs two functions.B. The employee can hide trading mistakes when processing the trades.C. The employee can hide the size of his book.D. The employee firm may not know its true exposure.Answer: ATo minimize operational risk, trading and back office functions should not be performed by the same employee. The risks of doing so include hiding trading mistakes and hiding the size of exposures in the trading book. The extra direct compensation cost of paying the same employee to perform both functions is minimal compared to the potential operational risk costs.。

FRM一级模考

专注国际财经教育FRM一级模拟题1 . When a bank decides to lend amount of money to borrowers, several considerations must be taken into account, based on the following statement which one is incorrect.A. Outstanding represent the total credit available to the borrower.B. Borrowers in distress often draw down on their unused commitment, so the adjusted exposure is outstanding plus usage given default times unused commitment.C. Credit optionality denotes the call option the borrower has purchased on the commitment for "a commitment fee".D. Collateral and seniority are the two most important factors in assessing recovery rates. Answer: ACommitment is the total credit available to the borrower.2 . Suppose ABC bank has booked a loan with following characteristics, it has total commitment of 3,000,000, 2,000,000 is outstanding. T he bank estiamate l% default probability (EDF) in one year, and draw down on default is 65%. The bank is currently experienced 60% of loss given default. The standard deviation of EDF and LGD is 5% and 30%, respectively. Please find the adjusted exposure.3 . The one-day Credit at Risk (CaR) of a portfolio is $1,000,000. What is the ten-day credit at risk?A. $10,000,000B. $3,162,278C. $5,136,498' .D. $1,923,657Answer: B。

FRM一级练习题(1)

FRM一级练习题(1)1、An investment manager is given the task of beating a benchmark. Hence the risk shoul d be measured in terms ofA. Loss relative to the initial investmentB. Loss relative to the expected portfolio valueC. Loss relative to the benchmarkD. Loss attributed to the benchmark2、Based on the risk assessment of the CRO, Bank United's CEO decid ed to make a large investment in a levered portfolio of CDOs. The CRO had estimated that the portfolio had a 1% chance of l osing $1 billion or more over one year, a loss that would make the bank insolvent. At the end of the first year the portfolio has lost $2 billion and the bank was cl osed by regulator. Which of the foll owing statement is correct?A. The outcome d emonstrates a risk management failure because the bank did not eliminate the possibility of financial distress.B. The outcome demonstrates a risk management failure because the fact that an extremely unlikely outcome occurred means that the probability of the outcome was poorly estimated.C. The outcome demonstrates a risk management failure because the CRO failed to go to regulators to stop the shutd own.D. Based on the information provid ed, one cannot determine whether it was a risk management failure.3、An analyst at CARM Research Inc. is projecting a return of 21% on Portfolio A. The market risk premium is 11%, the volatility of the market portfolio is 14%, and the risk-free rate is 4.5%. Portfolio A has a beta of 1.5. According to the capital asset pricing model which of the foll owing statements is true?A. The expected return of Portfolio A is greater than the expected return of the market portfolio.B. The expected return of Portfolio is less than the expected return of the market portfolio.C. The return of Portfolio A has l ower volatility than the mark t portfolio.D. The e peered return of Portfolio A is equal to the expected return of the market portfolio.4、Suppose Portfolio A has an expected return of 8%, volatility of 20%, and beta of 0.5. Suppose the market has an expected return of 10% and volatility of 25%. Finally suppose the risk-free rate is 5%. What is Jensen’s Alpha for Portfolio A?A. 10.0%B. 1.0%C. 0.5%D. 15%5、Which of the foll owing statement about the Sharpe ratio is false?A. The Sharpe ratio consid ers both the systematic and unsystematic risk of a portfolio.B. The Sharpe ratio is equal to the excess return of a portfolio over the risk-free rate divided by the total risk of the portfolio.C. The Sharpe ratio cannot be used to evaluate relative performance of undiversified portfolios.D. The Sharpe ratio is derived from the capital market line.6、A portfolio manager returns 10% with a volatility of 20%. The benchmark returns 8% with risk of 4%. The correlation between the two is 0.98. The risk-free rate is 3%. Which of the foll owing statement is correct?A. The portfolio has higher SR than the benchmark.B. The portfolio has negative IR.C. The IR is 0.35.D. The IR is 0.29.7、In perfect markets risk management expenditures aimed at reducing a firm' diversifiable risk serve toA. Make the firm more attractive to sharehol ders as long as costs of risk management are reasonable.B. Increase the firm's value by lowering its cost of equity.C. Decrease the firm's value whenever the costs o f such risk management are positive.D. Has no impact on firm value.8、By reducing the risk of financial distress and bankruptcy, a firm's use of d erivatives contracts to hedge it cash fl ow uncertainty willA. Lower its value due to the transaction costs of derivative trading.B. Enhance its value since investors cannot hedge such risks by themselves.C. Have no impact on its value as investor costless diversify this risk.D. Have no impact as only systematic risks can be hedged with derivatives.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。

FRM一级模考

FRM一级模拟题1 . A covered call writing position is equivalent to:A a long position in the stock and a long position in the call optionB. a short put positionC. a short position in the stock and a long position in the call optionD. a short call positionAnswer: BA covered call position is a long position in the stock and a short position on the call option. The payoff to this position is equivalent to a short put position, in which both have eliminated the upside potential but still have the downside exposure.2 . A portfolio manager wants to hedge his bond portfolio against changes in interest rates. He intends to buy a put option with a strike price below the portfolio's current price in order to protect against rising interest rates. He also wants to sell a call option with a strike price above the portfolios current price in order to reduce the cost of buying the put option. What strategy is the manager using?A.Bear spreadB. StrangleC. CollarD. StraddleAnswer: CA. Incorrect. The description is not for bear spread. A bear spread is created by buying a nearby put and selling a more distant put. A bear spread can also be set up using calls.B. Incorrect. The description is not for box spread. If the options are correctly priced, then the risk free rate will be earned for a box spread.C. Correct. The description is for a collar strategy which limits changes in the portfolio value in either direction. In other words, a collar is defined around the current portfolio value.D. Incorrect. The description is not for straddle. A straddle is created by buying a put and a call atthe same strike price and expiration to take advantage of significant portfolio moves in either direction.3 . A butterfly spread involves positions in options with three difference strike prices. It can be created by buying a call option with a low strike of _Xi; buying a call option with a high strike X3; and selling two call options with a strike X2 halfway between X] and X3. What can be said about the upside and downside of the strategy?A. Both the upside and downside is unlimitedB. Both the upside and downside is limitedC. The upside is unlimited but the downside is limitedD. The upside is limited but the downside is unlimitedAnswer: BThe pay-off structure to this strategy leaves the upside and downside potential 'at the difference between the premium collected on the calls sold and the premium paid on the calls purchased4 . Which of the following will create a bull spread?A. Buy a put with a strike price of X = 50, and sell a put with a strike price of 55.B. Buy a put with a strike price of X= 55, and sell a put with a strike price of 50.C. Buy a call with a premium of 5, and sell a call with a premium of 7D. . Buy a call with a strike price of X = 50, and sell a put with a strike price of 55.Answer: AIf an investor buys a put with a mike _of 50 and sells a put with a strike of 55, he or she will gain the value of the premium on the put sold at 55 less the call of the premium purchased at 50j as long as the value of the stock is 55 0r more. If the value falls below 50, the most he or she will lose is $5.00.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

FRM一级练习题(3)答案1. Here the t-reliability factor is used since the population variance is unknown. Since there are 30 observations, the degrees of freedom are 30 – 1 = 29. The t-test is a two-tailed test. So the correct critical t-value is2.045; thus the 95% confidence interval for the mean return is = [-3.464%, 11.464%].2. Assuming the l ong-run estimated variance remains unchanged, the reversion rate defined by the GARCH(1,1) model is (1- - ), which implies that the volatility term structure predicted by the GARCH(1,1) model reverts to the l ong-run estimated variance more sl owly.3. The cal culation is as foll ows:Two-thirds of the equity fund is worth USD 40 million. The optimal hedge ratio is given byh = 0.89 * 0.51 / 0.48 = 0.945The number of futures contracts is given byN = 0.945 * 40,000,000 / (910 * 250) = 166.26 c 167, rounded up to nearest integer.Incorrect:(A)—This is obtained if you hedge the full portfolio instead of two-thirds.Incorrect:(B)—This is obtained if you use the S&P 500 index l evel of 900 instead of the futures price of 910. Incorrect:(D)—This is obtained if the volatilities of the portfolio and the futures in the formula for the optimal hedge ratio are incorrectly invested.4. Due to the fact that the American option under consideration is on the stock, which does not pay dividends during the period, its value is equal to the European option with the same parameters. Thus, we can apply the put-call parity to determine the l evel of interest rates.C – P = S – K e – rT0.46 – 2.25 = 22 – 24 e – 0.25r–23.79 = –24e – 0.25rr = 3.52%(A) Incorrect answer.(B) Correct answer.(C) Incorrect answer: This is obtained if 0.5 year expiration is used instead of three months.(D) Incorrect answer: Because there are no dividends during the life of the option, put-call parity can be used and the interest rate can indeed be calculated.5. It is a butterfly spread strategy that can maximize the profit at the target level of USDJPY 97 while limiting the loss to the difference between the premiums of the two long and short calls. Incorrect:(A)—It is a strad dle strategy suitable for high expected volatility.Incorrect:(B)—It is a bull spread strategy suitable for bull expectation on USD.Incorrect:(C)—It is a bull spread strategy for USD.6. The key concept here is the box spread. A box spread with strikes at 120 and 150 gives you a payoff of 30 at expiration irrespective of the spot price. In a sense, it is like a zero coupon bond. Now recall the put-call parity relation:p + S = c + price of zero coupon bond with face value of strike red eeming at the maturity of the options.Since the strike is 120, the price of a zero coupon bond with face value of 120 can be expressed as four units of box spread.If there is any way you can sell any one side of the equation at a price higher than the other there is an arbitrage opportunity.(A) is correct.Short one put: +25Short one spot: +100Buy one call: –5Buy six box spreads: –120Net cash fl ow: 0At expiry, if spot is greater than 120, call is exercised, and if it is less than 120, put is exercised. In either case you end up buying one spot at 120. This can be used to cl ose the short position. The six spreads will provid e a cash fl ow of 6 * 30 = 180. The net profit is therefore = 180 – 120 = 60.(B) is incorrect.Buy one put: –25Short one spot: +100Short one call: +5Buy four box spreads: –80Net cash fl ow: 0At expiry, if spot is greater than 120, call is exercised, and if it is less than 120, put is exercised. In either case you end up selling one spot, at 120. However, you are already short one spot, which you have to cl ose. The four box-spreads provide a cash flow of 4 * 30 = 120. The net cash outfl ow = K – S – S – 120 = –2S. You have mad e a loss unless the spot price is zero.(C) is incorrect. This is exactly the reverse strategy of(A) And will give you a loss of 60.(D) is incorrect. You will choose this if you cannot figure out the similarity of the box-spread payoff to that of a zero coupon bond.7. The cheapest-to-deliver bond on maturity is defined as the one for which the adjusted spot price is the l owest. Adjusted spot price = Spot price/Conversion factor. Computation of adjusted price for each of the bonds is as foll ows:Bond A = (10214/32)/0.98 = 104.53%Bond B = (10619/32)/1.03 = 103.49%Bond C = (9812/32)/0.95 = 103.55%So, bond B is the cheapest-to-deliver bond, and option (B) is correct.8.(1) is false. Basis risk can also arise if the underlying asset and hedge asset are id entical. This can happen ifthe maturity of hedge contract and delivery date of asset does not match.(2) is true. Short hedge position or short forward contract benefits from unexpected decline in future prices and consequent strengthening of basis. The payoff to short hedge position is spot price at maturity (S2) and difference between futures price, i.e. (F1 – F2). Thus, payoff = S2 + F1 – F2 = F1 + b2, where b2 is the basis.(3) is false. Long hedge position benefits from weakening of basis.(A) is incorrect.(B) is incorrect.(C) is correct.(D) is incorrect.9.The value of the swap increases / decreases with an increase / decrease in the U.S. five-year fixed rate.The value of the swap increases / decreases with a d ecrease / increase in the USD-JPY rate.In(A), the value of the swap will increase.(A) is incorrect.In(B), the value of the swap will decrease.(B) is incorrect.In(C), the value of the swap will decrease.(C) is incorrect.In (D), both factors will cause a decrease in the value of the swap. Hence, (D) is correct.10. (A) is incorrect. The larger the debt repayments in hard currencies are in relation to export revenues, the greater the probability that the country will have to reschedul e its debt. (B) is incorrect. Since the first use of reserves is to buy vital imports, the greater the ratio of imports to foreign exchange reserves, the higher the probability that the country will have to reschedule its debt repayments. This is the case because the repayment of foreign debt hol ders is generally viewed by countries as being less important than supplying vital goods to the domestic population.(C) is correct. The investment ratio measures the d egree to which a country is all ocating resources to real investment in factories, machines, and so on, rather than to consumption. The higher this ratio is, the more productive the economy shoul d be in the future and the l ower the probability that the country will need to reschedul e its debt. An opposing view argues for a positive relationship, especially if the country invests heavily in import-competing industries. However, the relationship between the INVR and the probability of rescheduling is most likely to be negative among the four options given.(D) is incorrect. The more volatile a country's export earnings, the l ess certain creditors can be that at any time in the future it will be abl e to meet its repayment commitments. That is, there should be a positive relationship between VAREX and the probability of rescheduling.参与FRM的考生可按照复习计划有效进行,另外高顿网校官网考试辅导高清课程已经开通,还可索取FRM 考试通关宝典,针对性地讲解、训练、答疑、模考,对学习过程进行全程跟踪、分析、指导,可以帮助考生全面提升备考效果。