(完整word版)国际金融题库(英文版)

国际金融英文版第十五版复习资料

前言学弟学妹们,当你们看到这篇复习资料的时候, 学长已经在文档上传的当天上午参加了国际金融的考试, 本复习资料主要针对对象为成都信息工程学院(CUIT)英语系大三学生, 且立足教材也基于托马斯·A ·普格尔(Thomas A. Pugel)先生所著国际金融英文版·第15版, 其他版本或者相似教材也可作为参考, 本资料的整理除了参考维基百科,百度百科以及MBA 智库百科,当然最重要的是我们老师的课件. 为了帮助同学们顺利通过考试, 当然是拿到高分, 希望此资料能够帮助你们节省时间, 达到高效复习的效果.外国语学院2011级,陈爵歌(Louis) 2014年1月6日晚于宿舍 Chapter 2Transnationality Index (跨国化指数)(TNI ) is a means of ranking multinational corporations that is employed by economists and politicians. (反映跨国公司海外经营活动的经济强度,是衡量海外业务在公司整体业务中地位的重要指标) Foreign assets to total assets(外国资产占总资产比)Foreign sales to total sales(海外销售占总销售)Foreign employees to total employees(外籍雇员占总雇员)跨国化指数的构成联合国跨国公司与投资司使用的跨国化指数由三个指标构成:国外资产对公司总资产的百分比;国外销售对公司总销售的百分比;国外雇员人数对公司雇员总人数的百分比关于TNI 的计算公式:International Economic Integration( 国际经济一体化)International economic integration refers to the extent and strength of real -sector and financial -sector linkages among national economies.(国际经济一体化是指两个或两个以上的国家在现有生产力发展水平和国际分工的基础上,由政府间通过协商缔结条约,让渡一定的国家主权,建立两国或多国的经济联盟,从而使经济达到某种程度的结合以提高其在国际经济中的地位)Real Sector(实际经济部门): The sector of the economy engaged in the production and sale of goods and services(指物质的、精神的产品和服务的生产、流通等经济活动。

国际金融英语试题及答案

国际金融英语试题及答案1. 以下哪个选项不是国际货币基金组织(IMF)的主要职能?A. 提供技术援助B. 监督成员国的经济政策C. 促进国际贸易D. 提供紧急财政援助答案:C2. 世界银行的主要目标是什么?A. 促进全球贸易B. 减少全球贫困C. 维护国际货币稳定D. 促进全球金融市场发展答案:B3. 什么是外汇储备?A. 一个国家持有的外国货币和黄金B. 一个国家持有的国内货币和黄金C. 一个国家持有的外国货币和证券D. 一个国家持有的国内货币和证券答案:A4. 根据国际收支平衡表,以下哪项交易不属于经常账户?A. 商品出口B. 服务进口C. 外国直接投资D. 工人汇款回国答案:C5. 什么是货币贬值?A. 一个国家的货币价值相对于其他国家货币的减少B. 一个国家的货币价值相对于黄金的减少C. 一个国家的货币价值相对于商品和服务的减少D. 一个国家的货币价值相对于外国投资的减少答案:A6. 什么是浮动汇率制度?A. 货币价值由市场供求关系决定B. 货币价值由政府固定C. 货币价值由国际货币基金组织决定D. 货币价值由中央银行决定答案:A7. 什么是国际金融市场?A. 跨国公司进行商品和服务交易的市场B. 跨国公司进行货币和金融资产交易的市场C. 跨国公司进行商品和金融资产交易的市场D. 跨国公司进行服务和金融资产交易的市场答案:B8. 什么是国际货币体系?A. 国际货币的发行和流通体系B. 国际货币的监管和管理体系C. 国际货币的交换和结算体系D. 国际货币的发行、监管和管理体系答案:D9. 什么是外汇交易?A. 一种货币兑换成另一种货币的交易B. 一种商品兑换成另一种商品的交易C. 一种服务兑换成另一种服务的交易D. 一种资产兑换成另一种资产的交易答案:A10. 什么是国际金融危机?A. 一个国家内部的金融体系崩溃B. 一个国家内部的货币体系崩溃C. 多个国家金融体系的崩溃D. 多个国家货币体系的崩溃答案:C。

国际金融英文版(全)

Short-and Medium-term Debt Markets

Euro-commercial paper (ECP)and Euro-medium-term

notes(EMTN) Floating rate Euro-notes(Floating rate notes(FRN)represent an early innovation in the eurobond market.Interest is usually paid semiannually and they trade at a spread of the reference rate,e.g.,LIBOR.Margin above LIBOR may amount to 25-100 basis points or more.After 6 months ,the rate is reset with the same margin. International REPO market(repurchase agreement ,or REPOS)

Non-bank

Public international financial institutions public global financial institutions regional public national public Private international financial institutions global private regional private national private

the balance of payment

3.the theories of foreign exchange rate determination 4.foreign exchange exposure

(完整word版)《国际金融》期末考试试题

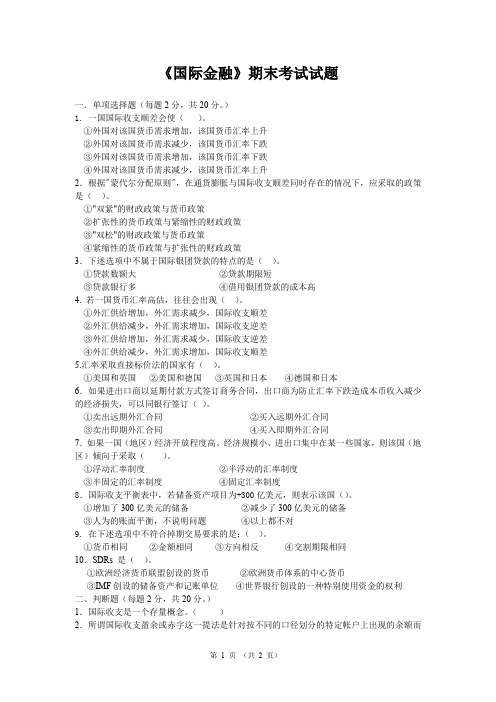

《国际金融》期末考试试题一.单项选择题(每题2分,共20分。

)1. 一国国际收支顺差会使()。

①外国对该国货币需求增加,该国货币汇率上升②外国对该国货币需求减少,该国货币汇率下跌③外国对该国货币需求增加,该国货币汇率下跌④外国对该国货币需求减少,该国货币汇率上升2.根据"蒙代尔分配原则",在通货膨胀与国际收支顺差同时存在的情况下,应采取的政策是()。

①"双紧"的财政政策与货币政策②扩张性的货币政策与紧缩性的财政政策③"双松"的财政政策与货币政策④紧缩性的货币政策与扩张性的财政政策3.下述选项中不属于国际银团贷款的特点的是()。

①贷款数额大②贷款期限短③贷款银行多④借用银团贷款的成本高4. 若一国货币汇率高估,往往会出现()。

①外汇供给增加,外汇需求减少,国际收支顺差②外汇供给减少,外汇需求增加,国际收支逆差③外汇供给增加,外汇需求减少,国际收支逆差④外汇供给减少,外汇需求增加,国际收支顺差5.汇率采取直接标价法的国家有()。

①美国和英国②美国和德国③英国和日本④德国和日本6.如果进出口商以延期付款方式签订商务合同,出口商为防止汇率下跌造成本币收入减少的经济损失,可以同银行签订()。

①卖出远期外汇合同②买入远期外汇合同③卖出即期外汇合同④买入即期外汇合同7.如果一国(地区)经济开放程度高、经济规模小、进出口集中在某一些国家,则该国(地区)倾向于采取()。

①浮动汇率制度②半浮动的汇率制度③半固定的汇率制度④固定汇率制度8.国际收支平衡表中,若储备资产项目为+300亿美元,则表示该国()。

①增加了300亿美元的储备②减少了300亿美元的储备③人为的账面平衡,不说明问题④以上都不对9. 在下述选项中不符合掉期交易要求的是:()。

①货币相同②金额相同③方向相反④交割期限相同10.SDRs 是()。

①欧洲经济货币联盟创设的货币②欧洲货币体系的中心货币③IMF创设的储备资产和记账单位④世界银行创设的一种特别使用资金的权利二、判断题(每题2分,共20分。

英文版国际金融试题和答案

Part Ⅰ.Decide whether each of the following statements is true or false (10%)每题1分,答错不扣分分,答错不扣分1. 1. If If If perfect perfect perfect markets markets markets existed, existed, existed, resources resources resources would would would be be be more more more mobile mobile mobile and and and could could could therefore therefore therefore be transferred be transferred to to those those countries more willing to pay a high price for them. ( T ) 2. The forward contract can h edge hedge hedge future receivables future receivables or or payables payables payables in in in foreign currencies to foreign currencies to i nsulate insulate insulate the the the firm firm against exchange rate risk. ( T ) 3. The primary objective of the multinational corporation is still the same primary objective of any firm, i.e., to maximize shareholder wealth. ( T ) 4. A low inflation rate tends to increase imports and decrease exports, thereby decreasing the current account deficit, other things equal. ( F ) 5. A capital account deficit reflects a net sale of the home currency in exchange for other currencies. This places up ward pressure on that home currency’s value. ( F ) 6. The theory of comparative advantage implies that countries should specialize in production, thereby relying on other countries for some products. ( T ) 7. 7. Covered Covered Covered interest interest interest arbitrage arbitrage arbitrage is is is plausible plausible plausible when when when the the the forward forward forward premium premium premium reflect reflect reflect the the the interest interest interest rate rate rate differential differential between two countries specified by the interest rate parity formula. ( F ) 8. The total impact of transaction exposure is on the overall value of the firm. ( F ) 9. A put option is an option to sell-by the buyer of the option-a stated number of units of the underlying instrument at a specified price per unit during a specified period. ( T ) 10. Futures must be marked-to-market. Options are not. ( T ) Part Ⅱ:Cloze (20%)每题2分,答错不扣分分,答错不扣分1. If inflation in a foreign country differs from inflation in the home country, the exchange rate will adjust to maintain equal( purchasing power )2. Speculators who expect a currency to ( appreciate ) could purchase currency futures contracts for that currency. 3. 3. Covered Covered Covered interest interest interest arbitrage arbitrage arbitrage involves involves involves the short-term the short-term investment investment in in in a a a foreign foreign foreign currency currency currency that that that is covered is covered by by a a ( forward contract ) to sell that currency when the investment matures. 4. ( Appreciation/ Revalue )of RMB reduces inflows since the foreign demand for our goods is reduced and foreign competition is increased. 5. ( PPP ) suggests a relationship between the inflation differential of two countries and the percentage change in the spot exchange rate over time. 6. 6. IFE IFE IFE is is is based based based on on on nominal nominal nominal interest interest interest rate rate rate ( ( differentials ), ), which which which are are are influenced influenced influenced by by by expected expected inflation. 7. Transaction exposure is a subset of economic exposure. Economic exposure includes any form by which the firm’s ( ( value ) will be affected. 8. 8. The The The option option option writer writer writer is is is obligated obligated obligated to to to buy buy buy the the the underlying underlying underlying commodity commodity commodity at at at a a a stated stated stated price price price if if if a a a ( ( put option ) is exercised 9. There are three types of long-term international bonds. They are Global bonds , ( eurobonds ) and ( foreign bonds ). 10. 10. Any Any Any good good good secondary secondary secondary market market market for for for finance finance finance instruments instruments instruments must must must have have have an an an efficient efficient efficient clearing clearing clearing system. system. system. Most Most Eurobonds are cleared through either ( Euroclear ) or Cedel. Part Ⅲ :Questions and Calculations (60%)过程正确结果计算错误扣2分1. Assume the following information: A Bank B Bank Bid price of Canadian dollar $0.802 $0.796 Ask price of Canadian dollar $0.808 $0.800 Given Given this this this information, information, information, is is is locational locational locational arbitrage arbitrage arbitrage possible? possible? If If so, so, so, explain explain explain the the the steps steps steps involved involved involved in in in locational locational arbitrage, and compute the profit from this arbitrage if you had $1,000,000 to use. (5%) ANSWER: Y es! One could purchase New Zealand dollars at Y Bank for $.80 and sell them to X Bank for $.802. With $1 million available, 1.25 million New Zealand dollars could be purchased at Y Bank. These New Zealand dollars could then be sold to X Bank for $1,002,500, thereby generating a profit of $2,500. 2. Assume that the spot exchange rate of the British pound is $1.90. How will this spot rate adjust in two years if if the the the United United United Kingdom Kingdom Kingdom experiences experiences experiences an an an inflation inflation inflation rate rate rate of of of 7 7 7 percent percent percent per per per year year year while while while the the the United United United States States experiences an inflation rate of 2 percent per year?(10%) ANSWER: According to PPP , forward rate/spot=indexdom/indexfor the exchange rate of the pound will depreciate by 4.7 percent. Therefore, the spot rate would adjust to $1.90 × [1 + (–.047)] = $1.8107 3. 3. Assume Assume Assume that that that the spot the spot exchange exchange rate rate rate of the of the Singapore Singapore dollar dollar dollar is is is $0.70. $0.70. The The one-year one-year one-year interest interest interest rate rate rate is is is 11 11 percent in the United States and 7 percent in Singapore. What will the spot rate be in one year according to the IFE? (5%) (5%) ANSWER: according to the IFE,St+1/St=(1+Rh)/(1+Rf) $.70 × (1 + .04) = $0.728 4. Assume that XYZ Co. has net receivables of 100,000 Singapore dollars in 90 days. The spot rate of the S$ is $0.50, and the Singapore interest rate is 2% over 90 days. Suggest how the U.S. firm could implement a money market hedge. Be precise . (10%) ANSWER: The firm could borrow the amount of Singapore dollars so that the 100,000 Singapore dollars to be be received received received could could could be be be used used used to to to pay pay pay off off off the the the loan. loan. This This amounts amounts amounts to to to (100,000/1.02) (100,000/1.02) (100,000/1.02) = = = about about about S$98,039, which S$98,039, which could could be be be converted converted converted to to to about about about $49,020 $49,020 $49,020 and and and invested. invested. The The borrowing borrowing borrowing of of of Singapore Singapore Singapore dollars dollars dollars has has has offset offset offset the the transaction exposure due to the future receivables in Singapore dollars. 5. 5. A A U.S. company ordered ordered a a a Jaguar Jaguar Jaguar sedan. In sedan. In 6 6 months , months , it will pay pay ££30,000 30,000 for for for the the the car. car. car. It It worried worried that that pound ster1ing might rise sharply from the current rate($1.90). So, the company bought a 6 month pound call (supposed contract size = £35,000) with a strike price of $1.90 for a premium of 2.3 cents/£. (1)Is hedging in the options market better if the £ rose to $1.92 in 6 months? (2)what did the exchange rate have to be for the company to break even?(15%)Solution: (1)If the £ rose to $1.92 in 6 months, the U.S. company would rose to $1.92 in 6 months, the U.S. company would exercise the pound call option. The sum of the strike price and premium is $1.90 + $0.023 = $1.9230/£This is bigger than $1.92. So hedging in the options market is not better. (2) when we say the company can break even, we mean that hedging or not hedging doesn’t matter. And only when (strike price + premium )= the exchange rate , hedging or not doesn’t matter. So, the exchange rate =$1.923/£. 6. Discuss the advantages and disadvantages of fixed exchange rate system.(15%) textbook page50 答案以教材第50 页为准页为准P AR T Ⅳ: Diagram(10%) The strike price for a call is $1.67/£. The premium quoted at the Exchange is $0.0222 per British pound. Diagram the profit and loss potential, and the break-even price for this call option Solution: Following diagram shows the profit and loss potential, and the break-even price of this put option: P AR T Ⅴ:Additional Question Suppose Suppose that that that you you you are are are expecting expecting expecting revenues revenues revenues of of of Y Y 100,000 100,000 from from from Japan Japan Japan in in in one one one month. month. Currently, Currently, 1 1 1 month month forward contracts are trading at $1 = $105 Y en. Y ou have the following estimate of the Y en/$ exchange rate in one month. Price Probability 90 Y en/$ 4% 95 Y en/$ 25% 100 Y/$ 45% 105 Y en/$ 20% 110 Y en/$ 6% a) What position in forward contracts would you take to hedge your exchange risk? b) Calculate the expected value of the hedge. c) How could you replicate this hedge in the money market? Y ou are expecting revenues of Y100,000 in one month that you will need to covert to dollars. Y ou could hedge this in forward markets by taking long positions in US dollars (short positions in Japanese Y en). By locking in your price at $1 = Y105, your dollar revenues are guaranteed to be Y100,000/ 105 = $952 On the other hand, you can wait and use the spot markets. Exchange Rate Probability Revenue w/Hedge Revenue w/out Hedge V alue of Hedge 90 Y/$ 4% $1,111 $952 -$159 95 Y/$ 25% $1,052 $952 -$100 100 Y/$ 45% $1,000 $952 -$48 105 Y/$ 20% $952 $952 $0 110 Y/$ 6% $909 $952 $43 Expected V alue = (.02)(-159) + (.25)(-100) + (.45)(-48) + (.20)(0) + (.08)(43) = -$24 Y ou could replicate this hedge by using the following: a) Borrow in Japan b) Convert the Y en to dollars c) Invest the dollars in the US d) Pay back the loan when you receive the Y100,000 。

国际金融英文版习题Chapter-3(1)

INTERNATIONAL FINANCEAssignment Problems (3) Name: Student#: I. Choose the correct answer for the following questions (only ONE correct answer) (2 credits for each question, total credits 2 x 25 = 50)1. Interbank quotations that include the United States dollars are conventionally given in __________, which state the foreign currency price of one U.S. dollar, such as a bid price of SFr 0.85/$.A. indirect quoteB. direct quoteC. American quoteD. European quote2. The spot exchange rate published in financial newspapers is usually the __________.A. nominal exchange rateB. real exchange rateC. effective exchange rateD. equilibrium exchange rate3. The foreign exchange refers to the __________.A. foreign bank notes and coinsB. demand deposits in foreign banksC. foreign securities that can be easily cashedD. all of the above4. The functions of the foreign exchange market come down to __________.A. converting the currency of one country into the currency of anotherB. providing some insurance against the foreign exchange riskC. making the foreign exchange speculation easyD. Only A and B are true.5. Which of the following is NOT true regarding the foreign exchange market?A. It is the place through which people exchange one currency for another.B. The exchange rate nowadays is mainly determined by the market forces.C. Most foreign exchange transactions are physically completed in this market.D. All of the above are true.6. The world largest foreign exchange markets are __________ respectively.A. London, New York and TokyoB. London, Paris and FrankfurtC. London, Hong Kong and SingaporeD. London, Zurich and Bahrain7. The foreign exchange market is NOT efficient because __________.A. monetary authorities dominate the foreign exchange market and everybody knows that by definition, central banks are inefficientB. commercial banks and other participants of the market do not compete with one another due to the fact that transaction takes place around the world and not in a single centralized locationC. foreign exchange dealers have different prices such as bid and ask pricesD. None of the reasons listed are correct because the foreign exchange market is an efficient market8. __________ earn a profit by a bid-ask spread on currencies they buy and sell. __________ on the other hand, earn a profit by bringing together buyers and sellers of foreign exchanges and earning a commission on each sale and purchase.A. Foreign exchange brokers; foreign exchange dealersB. Foreign exchange dealers; foreign exchange brokersC. arbitragers; speculatorsD. commercial banks; central banks9. Most foreign exchange transactions are through the U.S. dollars. If the transaction is expressed as the currencies per dollar, this is known as __________ whereas __________ are expressed as dollars per currency.A. direct quote; indirect quoteB. indirect quote; direct quoteC. European quote; American quoteD. American quote, European quote10. From the viewpoint of a Japanese investor, which of the following would be a direct quote?A. SFr 1.25/€B. $1.55/₤C. ¥ 110/€D. €0.0091/ ¥11. Which of the following is true about the foreign exchange market?A. It is a global network of banks, brokers, and foreign exchange dealers connected by electronic communications system.B. The foreign exchange market is usually located in a particular place.C. The foreign exchange rates are usually determined by the related monetary authorities.D. The main participants in this market are currency speculators from different countries.12. The extent to which the income from individual transactions is affected by fluctuations in foreign exchange values is considered to be _________.A. Translation exposureB. economic exposureC. transaction exposureD. accounting exposure13. Which of the following exchange rates is adjusted for price changes?A. nominal exchange rateB. real exchange rateC. effective exchange rateD. equilibrium exchange rate14. Suppose the exchange rate of the RMB versus U.S. dollar is ¥6.8523/$ now. If the RMB were to undergo a 10% depreciation, the new exchange rate in terms of ¥/$ would be:A. 6.1671B. 7.5375C. 6.9238D. 7.613515. At least in a U.S. MNC’s financial accounting statement, if the value of the euro depreciates rapidly against that of the dollar over a year, this would reduce the dollar value of the euro profit made by the European subsidiary. This is a typical __________.A. transaction exposureB. translation exposureC. economic exposureD. operating exposure16. A Japanese-based firm expects to receive pound-payment in 6 months. The company has a (an) __________.A. economic exposureB. accounting exposureC. long position in sterlingD. short position in sterling17 The exposure to foreign exchange risk known as Translation Exposure may be defined as __________.A. change in reported owner’s equity in consolidated financial statements caused by a change in exchange ratesB. the impact of settling outstanding obligations entered into before change in exchange rates but to be settled after change in exchange ratesC. the change in expected future cash flows arising from an unexpected change in exchange ratesD. All of the above18 When a firm deals with foreign trade or investment, it usually has foreign exchange risk exposure. So if an American firm expects to receive a dollar-paymentfrom a Chinese company in the next 30 days, the U.S. firm has the possible __________.A. economic exposureB. transaction exposureC. translation exposureD. none of the above19. In order to avoid the possible loss because of the exchange rate fluctuations, a firm that has a __________ position in foreign exchanges can __________ that position in the forward market.A. short; sellB. long; sellC. long; buyD. none of the above20. A forward contract to deliver Japanese yens for Swiss francs could be described either as __________ or __________,A. selling yens forward; buying francs forwardB. buying francs forward; buying yens forwardC. selling yens forward; selling francs forwardD. selling francs forward; buying yens forward21. Dollars are trading at S0SFr/$=SFr0.7465/$ in the spot market. The 90-day forward rate is F1SFr/$=SFr0.7432/$. So the forward __________ on the dollar in basis points is __________:A. discount, 0.0033B. discount, 33C. premium, 0.0033D. premium, 3322. If the spot rate is $1.35/€, 3-month forward rate is $1.36/€, which of the following is NOT true?A. euro is at forward premium by 100 points.B. dollar is at forward discount by 100 points.C. dollar is at forward discount by 55 points.D. euro is at forward premium by 2.96% p.a.23. If the spot C$/$ rate is 1.0305/15, forward dollar is 25/30 premium, the outright forward quote in American term should be __________.A. 1.0330 – 1.0345B. 1.0280 – 1.0285C. 0.9681 – 0.9667D. 0.9728 – 0.972324. If the spot C$/$ rate is 1.0305/15, forward dollar is 25/30 premium, the $/C$ forward quote in terms of points should be __________.A. 30/25B. 25/30C. – (23/28)D. – (28/23)25. The current U.S. dollar exchange rate is ¥85/$. If the 90-day forward dollar rate is ¥90/$, then the yen is selling at a per annum __________ of __________.A. premium; 5.88%B. discount; 5.56%C. premium; 23.52%D. discount; 22.23%II. ProblemsQuestions 1 through 10 are based on the information presented in Table 3.1. (2 credits for each question, total credits 2 x 10 = 20)Table 3.1Country Exchange rate Exchange rate CPI V olume of Volume of (2008) (2009) (2008) exports to U.S imports from U.S. Germany €0.75/$ €0.70/$ 102.5 $200m $350m Mexico Mex$11.8/$ Mex$12.20/$ 110.5 $120m $240mU.S. 105.31. The real exchange rate of the dollar against the euro in 2009 was __________.2. The real exchange rate of the dollar against the peso in 2009 was __________.3. The dollar was __________ against the euro in nominal term by __________.A. appreciated; 6.67%B. depreciated; 6.67%C. appreciated; 7.14%D depreciated; 7.14%4. The Mexican peso was __________ against the dollar in nominal term by __________.A. appreciated; 3.39%B. depreciated; 3.39%C. appreciated; 3.28%D. depreciated; 3.28%5. The volume of the German foreign trade with the U.S. was __________.6. The volume of the Mexican foreign trade with the U.S. was __________.7. Assume the U.S. trades only with the Germany and Mexico. Now if we want to calculate the dollar effective exchange rate in 2009 against a basket of currencies of euro and Mexican peso, the weight assigned to the euro should be __________.8. The weight assigned to the peso should be __________.9. Assume the 2008 is the base year. The dollar effective exchange rate in 2009 was __________.10. Was the dollar generally stronger or weaker in 2009 according to your calculation?11. The following exchange rates are available to you.Fuji Bank ¥80.00/$United Bank of Switzerland SFr0.8900/$Deutsche Bank ¥95.00/SFrAssume you have an initial SFr10 million. Can you make a profit via triangular arbitrage? If so, show steps and calculate the amount of profit in Swiss francs. (8 credits)12. If the dollar appreciates 1000% against the ruble, by what percentage does the ruble depreciate against the dollar? (5 credits)13. As a percentage of an arbitrary starting amount, about how large would transactions costs have to be to make arbitrage between the exchange rates S SFr/$= SFr1.7223/$, S$/¥= $0.009711/¥, and S¥/SFr = ¥61.740/SFr unprofitable? Explain. (7 credits14. You are given the following exchange rates:S¥/A$ = 67.05 – 68.75S£/A$ = 0.3590 – 0.3670Calculate the bid and ask rate of S¥/£: (5 credits)15. Suppose the spot quotation on the Swiss franc (CHF) in New York is USD0.9442 –52 and the spot quotation on the Euro (EUR) is USD1.3460 –68. Compute the percentage bid-ask spreads on the CHF/EUR quote. ( 5 credits)Answers to Assignment Problems (3)Part II1. 0.70 x (105.3/102.5) = 0.7 x 1.0273 = 0.71912. 12.2 x (105.3/110.5) = 12.2 x .9529 = 11.62593. B (0.7 /.75) – 1 = -6.67%4. D (1/12.2)/(1/11.8) – 1 = -3.28%5. 5506. 3607. 550/910 = 60.44%8. 360/910 = 39.569. (0.70/0.75)(60.44%) + (12.2/11.8)(39.56%) = .5641 + 0.4090 = .9731 = 97.31%10. weaker, because dollar depreciated by 2.69%.11. Since S¥/$S$/SFr S SFr/¥= 80 x 1/0.8900 x 1/95.00 = 0.946186 < 1, there is an arbitrage opportunity.Steps:①Buy ¥ from Deutsche Bank, SFr10 million x 95.00 = ¥950 million②Buy $from Fuji Bank, $950 m / 80.00 = $11.875 m③Buy SFr from UBS, $11.875 x 0.8900 = SFr10.56875 mProfit (ignoring transaction fees):SFr10.56875 – SFr10 = 0.56875 million = 568,75012. (x – 1) = 1000%; 1/11 – 1 = 90.9%13. S SFr/$ S$/¥S¥/SFr = SFr1.7223/$ x $0.009711/¥ x ¥61.740/SFr = 1.0326If transaction costs exceed $0.0326 (3.26%), the arbitrage is unprofitable.14. Given: S¥/A$ = 67.05 – 68.75S£/A$ = 0.3590 – 0.3670So, S¥/₤ = 67.05/0.3670 = 182.70 (bid)S£/₤ = 68.75/0.3590 = 191.50 (ask)15. Given: USD0.9442 – 52/SFrUSD1.3460 – 68/SFrSo, S SRr/€ = 1.3460/0.9452 =1.424 (bid)S SFr/€ = 1.3468/0.9442 = 1.4264 (ask)。

(完整word版)国际金融实务习题册及答案

《国际金融实务》练习册一、选择题(在每小题的四到五个答案中,选出正确的答案,并将其号码填在题干的括号内。

) 1.所谓外汇管制就是对外汇交易实行一定的限制,目的是()A、防止资金外逃B、限制非法贸易C、奖出限入D、平衡国际收支、限制汇价2.在英国货币市场上,以( )占有重要地位。

A.商业银行B.投资银行C.贴现行D.证券经纪商3.支出转换型政策主要包括()。

A.汇率政策B.政府补贴C.关税政策D.直接管制4.根据蒙代尔-弗莱明模型,在固定汇率制下()。

A.财政政策无效B.货币政策无效C.财政政策有效D.货币政策有效5.隐蔽的复汇率表现形式有()。

A.不同的财政补贴B.不同的附加税C.影子汇率D.不同的外汇留成比例6.布雷顿森林体系是采纳了()的结果。

A.怀特计划B.凯恩斯计划C.布雷迪计划D.贝克计划7.2003年6月底,欧洲经济货币联盟国家未参加欧元区接受统一货币欧元的国家有()。

A.英国B.希腊C.瑞典D.丹麦E.奥地利8.我国利用外资的方式有().A.设立中外合资经营企业B.开展补偿贸易C.发行A股D.发行B股E.出口买方信贷9.投资收益在国际收支平衡表中应列入( ).A.经常账户B.资本账户C.金融账户D.储备与相关项目10.我国目前对信用证抵押贷款的信贷条件规定是()。

A.贷款货币为外币B.贷款金额为信用证金额的90%C.企业使用贷款不受发放银行监督D.贷款期限原则上不超过90天11、国际债券包括( )A、固定利率债券和浮动利率债券B、外国债券和欧洲债券C、美元债券和日元债券D、欧洲美元债券和欧元债券12、二次世界大战前为了恢复国际货币秩序达成的(),对战后国际货币体系的建立有启示作用。

A、自由贸易协定B、三国货币协定C、布雷顿森林协定D、君子协定13、外汇远期交易的特点是()A、它是一个有组织的市场,在交易所以公开叫价方式进行B、业务范围广泛,合约具是非标准化的特点C、合约规格标准化D、交易只限于交易所会员之间14、金融汇率是为了限制()A、资本流入B、资本流出C、套汇D、套利15、汇率定值偏高等于对非贸易生产给予补贴,这样()A、对资源配置不利B、对进口不利C、对出口不利D、对本国经济发展不利16、国际储备运营管理有三个基本原则是()A、安全、流动、盈利B、安全、固定、保值C、安全、固定、盈利D、流动、保值、增值17、一国国际收支顺差会使( )A、外国对该国货币需求增加,该国货币汇率上升B、外国对该国货币需求减少,该国货币汇率下跌C、外国对该国货币需求增加,该国货币汇率下跌D、外国对该国货币需求减少,该国货币汇率上升18、金本位的特点是黄金可以()A、自由买卖、自由铸造、自由兑换B、自由铸造、自由兑换、自由输出入C、自由买卖、自由铸造、自由输出入D、自由流通、自由兑换、自由输出入19、布雷顿森林体系规定会员国汇率波动幅度为()A、±10%B、±2。

(完整word版)国际金融题库(英文版).doc

(完整word版)国际⾦融题库(英⽂版).doc Multiple-choice test(only one is correct):1.Gresham’ s Law states thata)Bad money drives good money out of circulation.b)Good money drives bad money out of circulationc)If a country bases its currency on both gold and silver, at an official exchange rate, it will be themore valuable of the two metals that circulate.d)None of the above.2.Balance of paymentsa) is defined as the statistical record of a country’ s international transactions over a certain period oftime presented in the form of a double-entry bookkeepingb) provides detailed information concerning the demand and supply of a country’ s currencyc)can be used to evaluate the performance of a country in international economic competitiond)all of the above3.If the United States imports more than it exports, thena)The supply of dollars is likely to exceed the demand in the foreign exchange market, ceteris paribus.b)One can infer that the U.S. dollar would be under pressure to depreciate against other currenciesc)a) and b)d)None of the above4. The current spot exchange rate is $1.55/ and the three-£month forward rate is $1.50/. You enter into£ a short position on 1,000£.At maturity, the spot exchange rate is $1.60/. How much have£ you made or lost?a) Lost $100b) Made £100c) Lost $50d) Made $1505. The sensitivity of“ realized” domestic currency values of the firm denomi’scontractualated cash flowsin foreign currency to unexpected changes in the exchange rate is:a)Transaction exposureb)Translation exposurec)Economic exposured)None of the above6.Three days ago, you ente red into a futures contract to sell ?62,500 at $1.20 per ?. Over the past three days the contract has settled at $1.20, $1.22, and $1.24. How much have you made or lost?a)Lost $0.04 per ? or $2,500b)Made $0.04 per ? or $2,500c)Lost $0.06 per ? or $3,750d)None of the above7.A swap banka)Can act as a broker, bringing together counterparties to a swapb)Can act as a dealer, standing ready to buy and sell swapsc)Both a) and b)d)Only sometimes a) but never ever b)8.Suppose that the one-year interest rate is 5.0 percent in the United States, the spot exchange rate is$1.20/?, and the one -year forward exchange rate is $1.16/?. What must one -year interest rate be in the euro zone?a) 5.0%b) 1.09%c) 8.62%d) None of the above.a b$1.89 =1£.00. If you were to buy $10,000,000 worth of British pounds and then sell them five minutes later, how much of your $10,000,000 would be“ eaten-ask”spread?bythe bida)$1,000,000b)$52,910.05c)$100,000d)$52,631.5810.Under the gold standard, international imbalances of payment will be corrected automatically underthea)Gresham Exchange Rate regimeb)European Monetary Systemc)Price-specie-flow mechanismd)Bretton Woods Accord11.With any hedgea)Your losses on one side should about equal your gains on the other sideb)You should try to make money on both sides of the transaction: that way you make money comingand goingc)You should spend at least as much time working the hedge as working the underlying deal itselfd)You should agree to anything your banker puts in front of your face12. Comparing“ forward” and“ futures” exchange contracts, we can say that:a)They are both“ marked-to-market” daily.b)Their major difference is in the way the underlying asset is priced for future purchase or sale:futures settle daily and forwards settle at maturity.c) A futures contract is negotiated by open outcry between floor brokers or traders and is traded on organized exchanges, while forward contract is tailor-made by an international bank for its clients and is traded OTC.d)b) and c)13.An “ option ” isa) a contract giving the seller (writer) the right, but not the obligation, to buy or sell a given quantityof an asset at a specified price at some time in the futureb) a contract giving the owner (buyer) the right, but not the obligation, to buy or sell a given quantity of an asset at a specified price at some time in the futurec)not a derivative, nor a contingent claim, securityd)unlike a futures or forward contract14.Economic exposure refers toa)the sensitivity of realized domestic currency values of the firm ’contractuals cash flows denominated in foreign currencies to unexpected exchange rate changesb)the extent to which the value of the firm would be affected by unanticipated changes in exchange ratec) the potential that the firm ’consolidated financial statement can be affected by changes in exchange ratesd)ex post and ex ante currency exposures15.Under a purely flexible exchange rate systema)Supply and demand set the exchange ratesb)Governments can set the exchange rate by buying or selling reservesc)Governments can set exchange rates with fiscal policyb) and c) are correct.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Multiple-choice test(only one is correct):1. Gresham’s Law states thata)Bad money drives good money out of circulation.b)Good money drives bad money out of circulationc)If a country bases its currency on both gold and silver, at an official exchange rate, it will be themore valuable of the two metals that circulate.d)None of the above.2. Balance of paymentsa)is defined as the statistical record of a country’s international transactions over a certain period oftime presented in the form of a double-entry bookkeepingb)provides detailed information concerning the demand and supply of a country’s currencyc)can be used to evaluate the performance of a country in international economic competitiond)all of the above3. If the United States imports more than it exports, thena)The supply of dollars is likely to exceed the demand in the foreign exchange market, ceterisparibus.b)One can infer that the U.S. dollar would be under pressure to depreciate against other currenciesc)a) and b)d)None of the above4. The current spot exchange rate is $1.55/£ and the three-month forward rate is $1.50/£. You enter into a short position on £1,000. At maturity, the spot exchange rate is $1.60/£. How much have you made or lost?a)Lost $100b)Made £100c)Lost $50d)Made $1505. The sensitivity of “realized” domestic currency values of the firm’s contractual cash flows denominated in foreign currency to unexpected changes in the exchange rate is:a)Transaction exposureb)Translation exposurec)Economic exposured)None of the above6. Three days ago, you ente red into a futures contract to sell €62,500 at $1.20 per €. Over the past three days the contract has settled at $1.20, $1.22, and $1.24. How much have you made or lost?a)Lost $0.04 per € or $2,500b)Made $0.04 per € or $2,500c)Lost $0.06 per € or $3,750d)None of the above7. A swap banka)Can act as a broker, bringing together counterparties to a swapb)Can act as a dealer, standing ready to buy and sell swapsc)Both a) and b)d)Only sometimes a) but never ever b)8. Suppose that the one-year interest rate is 5.0 percent in the United States, the spot exchange rate is$1.20/€, and the one-year forward exchange rate is $1.16/€. What must one-year interest rate be in the euro zone?a) 5.0%b) 1.09%c)8.62%d)None of the above.9. Suppose the spot ask exchange rate, S a($|£), is $1.90 = £1.00 and the spot bid exchange rate, S b($|£), is $1.89 = £1.00. If you were to buy $10,000,000 worth of British pounds and then sell them five minutes later, how much of your $10,000,000 would be “eaten” by the bid-ask spread?a)$1,000,000b)$52,910.05c)$100,000d)$52,631.5810. Under the gold standard, international imbalances of payment will be corrected automatically under thea)Gresham Exchange Rate regimeb)European Monetary Systemc)Price-specie-flow mechanismd)Bretton Woods Accord11. With any hedgea)Your losses on one side should about equal your gains on the other sideb)You should try to make money on both sides of the transaction: that way you make moneycoming and goingc)You should spend at least as much time working the hedge as working the underlying deal itselfd)You should agree to anything your banker puts in front of your face12. Comparing “forward” and “futures” exchange contracts, we can say that:a)They are both “marked-to-market” daily.b)Their major difference is in the way the underlying asset is priced for future purchase or sale:futures settle daily and forwards settle at maturity.c) A futures contract is negotiated by open outcry between floor brokers or traders and is traded onorganized exchanges, while forward contract is tailor-made by an international bank for its clients and is traded OTC.d)b) and c)13. An “option” isa) a contract giving the seller (writer) the right, but not the obligation, to buy or sell a given quantityof an asset at a specified price at some time in the futureb) a contract giving the owner (buyer) the right, but not the obligation, to buy or sell a givenquantity of an asset at a specified price at some time in the futurec)not a derivative, nor a contingent claim, securityd)unlike a futures or forward contract14. Economic exposure refers toa)the sensitivity of realized domestic currency values of the firm’s contractual cash flowsdenominated in foreign currencies to unexpected exchange rate changesb)the extent to which the value of the firm would be affected by unanticipated changes in exchangeratec)the potential that the firm’s consolidated financial statement can be affected by changes inexchange ratesd)ex post and ex ante currency exposures15. Under a purely flexible exchange rate systema) Supply and demand set the exchange ratesb) Governments can set the exchange rate by buying or selling reservesc) Governments can set exchange rates with fiscal policyb) and c) are correct.。