Purchasing Portfolio Management (4)

2018 CFA level 1 知识点——Portfolio Management

Portfolio ManagementPortfolio Management: An OverviewDescribe the portfolio approach to investing1.The portfolio perspective refers to evaluating individual investments by theircontribution on the risk and return of an investor’s portfolio.投资组合视角指的是通过投资组合对风险和回报的贡献来评估个人投资。

2.把所有钱用于买一只股票并不是一种portfolio perspective,把钱分散在多只证券中才能降低风险,增加收益。

3.One measure of the benefits of diversification is the diversification ratio. It iscalculated as the ratio of the risk of an equally weighted portfolio of n securities to the risk of a single security selected at random from the n securities.衡量多样化的好处之一是多样化比率。

它计算的是n证券等加权组合的风险与随机从n证券中选择的单一证券的风险之比。

4.If the average standard deviation of returns for the n stocks is 25%, and thestandard deviation of returns for an equally weighted portfolio of the n stocks is 18%, the diversification ratio is 18/25=0.72.Describe types of investors and distinctive characteristics and needs of each1.Individual investor个人投资者就是个人为了满足生活目标而进行理财的投资者,是牺牲当前消费以期获得未来更高水平消费的个人。

portfolio management manager 工作职责

portfolio management manager 工作职责

作于投资银行或资产管理公司的投资组合管理经理是负责组织和管理投资组合的人。

以下是该职位的一些常见工作职责:

1. 客户咨询和支持:与客户合作,了解他们的投资目标和需求,并提供有关投资策略和产品的咨询和支持。

2. 投资策略制定:基于市场趋势、风险偏好和资产配置目标,制定适当的投资策略,以实现客户的投资目标。

3. 资产配置管理:根据投资策略,管理投资组合的资产配置,包括股票、债券、商品和其他投资工具。

4. 交易执行:负责执行投资决策,并进行交易以买卖股票、债券和其他金融产品。

5. 风险管理:监测投资组合的风险水平,并采取适当的措施来减少风险和保护客户的投资。

6. 绩效评估和报告:定期评估投资组合的绩效,并向客户提供报告,解释投资组合的表现和可能的风险。

7. 市场研究:跟踪全球金融市场的动向,并进行研究以寻找潜在的投资机会。

8. 团队管理:指导和管理投资组合管理团队,确保团队的协作和效率。

9. 持续教育:保持与投资市场的最新趋势和最佳实践保持熟悉,并持续学习和提升专业知识。

以上只是投资组合管理经理的一些常见职责,具体的职责可能会因公司和行业而有所不同。

cfa-level_III_essay_questions_2013

The Morning Session of the 2013 Level III CFA® Examination has 11 questions. For grading purposes, the maximum point value for each question is equal to the number of minutes allocated to that question.Question Topic Minutes1 Portfolio Management – Individual 202 Portfolio Management – Individual153 Portfolio Management – Individual/Behavioral164 Portfolio Management – Equity175 Portfolio Management – Economics206 Portfolio Management – Institutional187 Portfolio Management – Institutional148 Portfolio Management – Fixed Income179 Portfolio Management – Fixed Income 9– Risk Management 18Management10 Portfolio– Performance Evaluation16Management11 PortfolioTotal: 180THIS PAGE INTENTIONALLY LEFT BLANK ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 1 HAS FOUR PARTS (A, B, C, D) FOR A TOTAL OF 20 MINUTES. Thomas and Elizabeth Voort, both age 45, are meeting with their financial advisor, Marc Lenard. Lenard is creating an investment policy statement for the Voorts. Thomas sold his consulting business at year-end and retired. The Voorts will rely on their investment portfolio to meet future expenses in excess of Thomas’ retirement income. Elizabeth is not employed. Financial details include:IncomeThomas will receive retirement payments of USD 125,000 per year for his lifetime from the business he sold. The retirement payments are not indexed for future inflation and are fully taxable as ordinary income.ExpensesThe Voorts’ total living expenses last year were USD 300,000, and they are expected to grow each year at the inflation rate. Taxes are due immediately on the gain from the sale of the business at a rate of 15%. The Voorts do not expect any other significant cash outflows in the future.The tax rate on ordinary income and all investment returns is 30%. The inflation rate is expected to be 2.5% per year.AssetsThe Voorts own their home, valued at USD 1,250,000, mortgage-free. They have a taxable investment portfolio with a current market value of USD 2,500,000. This portfolio has no previous tax liability due in the coming year. Thomas received a lump-sum USD 10,000,000 payment from the sale of his business; his cost basis is zero. The net proceeds of the sale will be added to the Voorts’ investment portfolio. Their goals are to grow the asset base of the portfolio over time to maintain its after-tax purchasing power and to establish and maintain a cash reserve of USD 250,000.A. Determine the Voorts’ nominal after-tax required rate of return for the coming year.Show your calculations.(8 minutes)B. Statetwo reasons why the Voorts’ ability to assume risk in their investment portfolio is above average.(4 minutes)C. Determine the Voorts’ liquidity requirement (in USD) for the coming year. Show yourcalculations.(3 minutes)Two years later, the Voorts ask Lenard to construct a new long-term strategic asset allocation with a more aggressive goal of achieving at least 3.5% annualized growth in the after-taxpurchasing power of the portfolio. They indicate that the portfolio should have only a small probability of declining more than 10% in nominal pre-tax terms in any one year. Lenard explains to the Voorts that a normal distribution can be used to model the portfolio returns. The Voorts agree to use a two-standard-deviation approach to monitor the shortfall risk of the portfolio.Expected inflation remains 2.5% per year and the tax rate remains 30%. Based on his current market outlook, Lenard considers three potential portfolio allocations for the Voorts as shown in Exhibit 1.Exhibit 1Potential Long-Term Strategic PortfoliosAsset Class ExpectedAnnualReturnPortfolioXPortfolioYPortfolioZStocks 11.0%70%55%60% Bonds 6.0%25%35%35% Cash 2.5%5%10%5%Pre-tax expected return (nominal) 9.3% 8.4% 8.8%Expected standard deviation (nominal) 11.0% 8.7% 9.3%D. Determinethe most appropriate portfolio from Exhibit 1 for the Voorts, given theirobjectives and constraints. Justify your response with two reasons.(5 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDTHIS PAGE INTENTIONALLY LEFT BLANK ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 2 HAS FOUR PARTS (A, B, C, D) FOR A TOTAL OF 15 MINUTES.Gerardo Puente, age 70, is a retired entrepreneur with a desire for privacy in his financial affairs. His wife is 45 years old and they have three young sons. Puente has one daughter from a previous marriage.The Puentes live in a country that is a community property regime with the U.S. dollar as its currency. The community property regime entitles a surviving spouse to receive a one-half interest in assets accumulated during the marriage. Puente’s total estate has grown fromUSD 12 million to USD 26 million during his current marriage. The forced heirship rules in Puente’s country entitle his current wife to receive a minimum of 25% of the total estate and all children to equally share a minimum of 25% of the total estate.Puente would like to secure a sound financial future for his family. He worries about potential legal claims from outside the family and disputes among his children. As a result, Puente consults his investment advisor, who recommends that Puente establish a trust.A.Determine the minimum amount that Puente’s current wife would be entitled to receive,before estate taxes are considered, if he were to die today. Show your calculations.(4 minutes)B. Discuss two benefits, specific to Puente’s circumstances, of establishing a trust.(4 minutes)Puente’s daughter from his previous marriage is 30 years old. Her income tax rate is lower than Puente’s. Puente asks his investment advisor about the tax benefit of making a current gift to his daughter rather than transferring wealth to her through a bequest upon his death. The country’s gift tax rate is flat, with no annual or lifetime exemptions. The estate tax rate is also flat and equal to the gift tax rate. The laws of the country require the donor to pay any gift taxes. The investment advisor makes the following assumptions:∙Puente’s estate will be subject to estate tax.∙His daughter’s estate will not be taxed because its value will be below the minimum taxable threshold.∙His daughter’s pre-tax investment returns on any gifted assets will be equal to Puente’s.C. Justify with two reasons why tax considerations favor Puente making a current gift tohis daughter rather than transferring wealth to her upon his death.Note: No calculations are required.(4 minutes)Five years have passed and Puente’s daughter now has a three-year-old son who is Puente’s only grandchild. Puente believes he has USD 1 million of excess capital that could be transferred to his grandson. Due to a change in financial circumstances, the investment advisor now assumes that Puente’s daughter’s estate will be subject to estate tax.D. Explain the tax benefit of a direct transfer of assets from Puente to his grandson.Note: No calculations are required.(3 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 3 HAS THREE PARTS (A, B, C) FOR A TOTAL OF 16 MINUTES.Joyce Siosan is a 42-year-old lawyer at a prestigious law firm. She is meeting with Joel Murray, a financial advisor, to organize her finances. During the interview process, Siosan tells Murray that she has been purchasing short-term, out-of-the-money call and put options. Siosan acknowledges these options have a low probability of paying off and that the expected return from her options trading is negative. However, she states that she is attracted by the possibility of high returns when she can exercise in-the-money options. At the same time, Murray notes that Siosan has been purchasing low-payoff earthquake insurance on her home, which is located in a low-probability earthquake zone.A.Describe Siosan’s utility function. Contrast her utility function with that assumed intraditional finance theory.(5 minutes)Siosan purchases a new luxury vehicle every two years and takes expensive annual vacations. She has a reputation for paying the entire bill at the upscale restaurants where she dines regularly with her friends. Siosan’s annual consumption, options trading, and housing expenditures are paid for entirely out of her salary income and half of her modest annual bonus. She deposits the other half of her annual bonus and any other non-salary sources of income into her relatively small retirement account, which excludes her options trading. Siosan is reluctant to incur debt and has only a small mortgage on her home, despite the fact that she will soon be made a partner in her firm and will have much higher earnings. Murray believes that Siosan exhibits behavioral biases that interfere with an optimal savings and consumption allocation. In particular, he thinks that she is not saving enough for retirement.ANSWER QUESTION 3-B IN THE TEMPLATE PROVIDED ON PAGES 22 AND 23. B.Discuss how Siosan’s behavior reflects the bias of:i.self-control.ii.mental accounting.Explain how a rational economic individual in traditional finance would behavedifferently with respect to each bias.(6 minutes)Siosan’s retirement portfolio is allocated 50% to money-market securities and 50% to a few speculative stocks that she read about in an investment newsletter. Murray observes that Siosan’s retirement portfolio allocation is consistent with Behavioral Portfolio Theory and not consistent with a mean–variance framework.C. Determinewhether Murray’s observation about Siosan’s retirement portfolio allocation is correct. Justify your response with two reasons.(5 minutes)Answer Question 3 on This Page Template for Question 3-BBehavioral bias Discuss how Siosan’s behavior reflectseach bias.Explain how a rational economicindividual in traditional financewould behave differently with respectto each bias.i. self-controlTemplate for Question 3-B continued on page 23Answer Question 3 on This Page Template for Question 3-B (continued)Behavioral bias Discuss how Siosan’s behavior reflectseach bias.Explain how a rational economicindividual in traditional financewould behave differently with respectto each bias.ii. mental accountingTHIS PAGE INTENTIONALLY LEFT BLANK ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 4 HAS THREE PARTS (A, B, C) FOR A TOTAL OF 17 MINUTES.Kimi Capital Group is a provider of index services. A key growth strategy for Kimi is to develop market indices for use as benchmarks for exchange-traded index funds. Kimi’s management realizes that the criteria it uses to construct its indices will influence the resulting transaction costs incurred by funds attempting to track the indices. The lower the potential transaction costs of an index, the more attractive it will be to an index fund and to investors. Kimi regularly compares its index construction criteria to those of other index service providers to evaluate the competitiveness of its products. Exhibit 1 summarizes Kimi’s current criteria and the criteria currently used by its main competitor.Exhibit 1Comparison of Index Construction CriteriaIndex Construction Criterion Current Criterionfor Kimi CapitalCriterion Used by MainCompetitorIndex breadth as percent oftotal market capitalizationminimum 95% minimum 80% Float adjustment float bands single pointSelection of index constituents objective, clearlystated rulessubjective, flexible rulesANSWER QUESTION 4-A IN THE TEMPLATE PROVIDED ON PAGE 29.A.Determine if each of Kimi Capital’s index construction criteria in Exhibit 1 will mostlikely result in lower, no difference in, or higher transaction costs relative to each of the criteria of its main competitor. Justify each response with one reason.(9 minutes)Kimi Capital is evaluating the country of Badaar for inclusion in either its Developed Market Index or its Emerging Market Index, which are both capitalization-weighted. Badaar’s equity market has characteristics that make it a possible fit for either index. Relevant characteristics of Badaar’s equity market and of Kimi’s two indices are provided in Exhibit 2.Exhibit 2Equity Market and Index Characteristics(amounts in USD billions)Characteristic BadaarEquityMarketDevelopedMarketIndexEmergingMarketIndexAverage market capitalization 1.5 22.1 1.3Total market capitalization 300 10,000 550Stability of currency Stable Stable Mostly stableLiquidity ModerateVeryhighModerateB.Discuss one reason that supports each of the following statements:i.Badaar’s equity market will be positively impacted by Badaar’s inclusion in theDeveloped Market Index.ii.Index funds that track the Emerging Market Index will be negatively impacted by Badaar’s inclusion in that index.(4 minutes)Kimi Capital is planning to introduce style indices based on its Developed Market Index. The companies that make up the Developed Market Index will be placed into either a Growth Index or a Value Index, but not both. The placement of firms into either index will be based on an assessment of multiple growth and valuation characteristics. Kimi will rebalance the indices with no buffering. Holding companies will be excluded from both style indices.C.Discuss two aspects of Kimi Capital’s style index construction that will most likelyproduce higher turnover between the style indices.(4 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDAnswer Question 4 on This Page Template for Question 4-AIndex construction criterionDetermine if each ofKimi Capital’s indexconstruction criteria inExhibit 1 will mostlikely result in lower,no difference in, orhigher transactioncosts relative to each ofthe criteria of its maincompetitor.(circle one)Justify each response with one reason.Index breadth as percent of total market capitalizationlowerno difference higherFloat adjustmentlowerno difference higherSelection of index constituentslowerno difference higherTHIS PAGE INTENTIONALLY LEFT BLANK ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 5 HAS FOUR PARTS (A, B, C, D) FOR A TOTAL OF 20 MINUTES.Andrew Reed is a market strategist with a U.S.-based asset management firm. He is currently evaluating several emerging market economies in order to identify undervalued markets.Reed uses the Cobb-Douglas production function (under the assumption of constant returns to scale) to estimate the long-term growth in real GDP for the country of Westria. Exhibit 1 summarizes the projections that Reed has gathered for Westria.Exhibit 1Annualized Economic Projections for Westria(2013–2043)Growth in total factor productivity 1.3%Output elasticity of capital 0.7Growth in total population 1.8%Growth in capital stock 5.5%Growth in labor input 2.5%Unemployment rate 8.2%A.Calculate the projected annual growth in real GDP for Westria using the Cobb-Douglasproduction function and the information in Exhibit 1. Show your calculations.(4 minutes)Reed knows that economic growth forecasts are sensitive to the inputs to the Cobb-Douglas production function. He wants to assess the effect of two potential new economic policies on Westria’s future growth path. The newly elected government in Westria has proposed the following policies:Policy 1: Offer incentives to limit the average number of children per family.Policy 2: Increase the maximum allowable annual contribution to tax-freeretirement accounts.ANSWER QUESTION 5-B IN THE TEMPLATE PROVIDED ON PAGE 36.B.Determine whether each proposed policy will most likely decrease, have no effect on, orincrease the long-run Cobb-Douglas growth projection for Westria. Justify eachresponse with one reason.(6 minutes)Reed is discussing the valuation of Westria’s stock market with the firm’s equity strategist, Jill Shepherd. He produces the data for Westria shown in Exhibit 2. Reed tells Shepherd that he believes the Fed model is appropriate for valuing Westria’s stock market. Shepherd disagrees, stating that the Yardeni model is more suitable because the Fed model has several limitations.Exhibit 2Capital Markets Data for Westria10-year government bond yield 5.1%Yardeni weighting factor 0.2Average 10-year A-rated corporate bond yield 5.9%Broad equity index level (current) 800Broad equity index earnings (last four quarters) 35Projected long-term earnings growth rate 7.0%ANSWER QUESTION 5-C IN THE TEMPLATE PROVIDED ON PAGE 37.C.Determine whether Westria’s stock market (using the broad equity index as a proxy) isundervalued, fairly valued, or overvalued using the:i.Fed model.ii. Yardeni model.Justify each response with one reason.(6 minutes)Reed asks Shepherd about the extent to which the Fed and Yardeni models incorporate risk. Shepherd proposes using the average 10-year BB-rated corporate bond yield instead of the average 10-year A-rated corporate bond yield to assess the valuation of Westria’s stock market.D.Explain the effect of substituting the BB-rated corporate bond yield for the A-ratedcorporate bond yield on the fair value of Westria’s stock market as determined by the:i.Fed model.ii.Yardeni model.(4 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDAnswer Question 5 on This Page Template for Question 5-BPolicy Determine whethereach proposedpolicy will mostlikely decrease,have no effect on,or increase thelong-run Cobb-Douglas growthprojection forWestria.(circle one)Justify each response with one reason.Policy 1:Offer incentives to limit the average number of children per family. decrease no effect increasePolicy 2:Increase the maximum allowable annual contribution to tax-free retirement accounts. decrease no effect increaseAnswer Question 5 on This Page Template for Question 5-CModel Determine whetherWestria’s stockmarket (using thebroad equity indexas a proxy) isundervalued, fairlyvalued, orovervalued usingeach model.(circle one)Justify each response with one reason.i. Fed model undervalued fairly valued overvaluedii. Yardeni model undervalued fairly valued overvaluedTHIS PAGE INTENTIONALLY LEFT BLANK ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDQUESTION 6 HAS FOUR PARTS (A, B, C, D) FOR A TOTAL OF 18 MINUTES.Jason Pearce founded a social media company. When the company went public, Pearce became wealthy. He now wishes to start the Pearce Foundation to support the university he attended. Pearce wants the Foundation to make contributions to the university in perpetuity.The Foundation will be a tax-exempt entity. Pearce makes an initial gift to the Foundation of USD 100 million on 1 January of Year 1. In addition, Pearce intends to make ongoing annual contributions to the Foundation of USD 2 million on 1 January of each subsequent year. The Foundation will make a one-time distribution of USD 3 million at the beginning of Year 1 to fund a new computer lab at the university.Beginning in Year 2, the Foundation will have an annual spending requirement of 6% of the market value of its portfolio at the end of the preceding year. The annual contributions from the Foundation to the university will be used to cover a portion of the university’s operating expenses. The university’s expected inflation rate is 3.5% per year.The Foundation’s goal is to preserve the real value of its investment portfolio and any future contributions while also meeting its spending requirement. Pearce hires Maxine Smith as the investment advisor to the Foundation. Smith’s management fees will be 0.40% per year. These fees will be calculated based on the year-end value of the portfolio and paid in arrears on the first day of the following year.Pearce instructs Smith to prepare an investment policy statement (IPS) for the Foundation. Smith concludes that the Foundation has an above-average risk tolerance.A.Identify two factors that support Smith’s conclusion regarding the Foundation’s risktolerance.(4 minutes)B. Determine the nominal required rate of return for the Foundation in Year 2.(3 minutes)In the first year of the Foundation’s operation, the return on the benchmark was 9.8% and the return on the Foundation’s portfolio was 9.0%. The Foundation received the plannedUSD 2 million contribution on 1 January of Year 2.C. Determine the liquidity requirement (in USD) of the Foundation in Year 2. Show yourcalculations.(5 minutes)Three years have passed. During that time, the Foundation operated as planned. However, the social media company Pearce founded went bankrupt. Because Pearce had retained virtually allhis personal assets in shares of the company, he lost all of his wealth. He will not be able to make additional contributions to the Foundation. Smith is preparing a revised IPS to reflect the Foundation’s changed circumstances.ANSWER QUESTION 6-D IN THE TEMPLATE PROVIDED ON PAGE 46.D. Determine the effect (decrease, no change, increase) of these changed circumstances onthe Foundation’s return objective and liquidity requirement. Justify each response with one reason.(6 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADEDAnswer Question 6 on This Page Template for Question 6-DIPS component Determine the effect(decrease, nochange, increase) ofthese changedcircumstances onthe Foundation’sreturn objective andliquidityrequirement.(circle one)Justify each response with one reason.Return objectivedecrease no change increaseLiquidity requirementdecrease no change increaseQUESTION 7 HAS FOUR PARTS (A, B, C, D) FOR A TOTAL OF 14 MINUTES.Shire Manufacturing and Vermillion Enterprises are specialty steel fabricators based in Europe. Both companies provide defined benefit pension plans for their employees. Beth Hagar, Chief Financial Officer of Shire, is reviewing a consultant’s report that compares Shire’s and Vermillion’s pension plans. Both plans are large relative to each company’s total market capitalization, have a high percentage of inactive participants, match the duration offixed-income investments to the duration of pension liabilities, and are closed to new participants. Exhibit 1 presents selected attributes of the two pension plans.Exhibit 1Pension Plan Attributes as of 31 December 2012Pension Plan AttributeShireManufacturingVermillionEnterprisesAverage age of workforce 44 39 Average age of plan participants 56 56 Mandatory retirement age 65 65Plan surplus EUR 30,000,000 EUR 50,000,000 Market value of plan assets EUR 200,000,000 EUR 500,000,000Plan asset allocation60% equity,40% fixed income30% equity,70% fixed incomePrior year service cost EUR 14,375,000 EUR 35,000,000A. Describe one attribute of Vermillion’s pension plan that contributes to:i.lower shortfall risk relative to Shire’s pension plan.ii.higher shortfall risk relative to Shire’s pension plan.(4 minutes)Shire’s pension management process has historically followed an asset-only approach. However, the company is considering adopting a liability-relative approach. One of the firm’s investment advisors recently presented three structured products to Hagar as potential pension fund investments. Exhibit 2 presents selected data for the three structured products.Exhibit 2Structured Products Available to Shire Manufacturing Pension PlanStructured ProductExpectedAnnualizedReturnExpectedStandardDeviationof ReturnsExpectedCorrelationof Returnswith PensionLiabilitiesExpectedCorrelationof Returnswith PensionAssetsX 7.42% 2.80% 0.92 0.35 Y 8.44% 2.36% 0.22 0.75 Z 8.12% 3.02% 0.51 0.12B. Determine which structured product Shire should add to its pension plan assets toachieve the lowest shortfall risk if it adopts the liability-relative approach. Justify your response with one reason.(3 minutes)One year has passed and Shire’s pension plan assets now equal its liabilities. Hagar wants to determine the effect on her capital budgeting decisions of incorporating Shire’s pension plan assets and liabilities into a full economic balance sheet of the firm.Shire’s updated standard balance sheet is presented in Exhibit 3 and its full economic balance sheet is presented in Exhibit 4.Exhibit 3Shire Manufacturing (excluding pension plan)Standard Balance Sheet(EUR values in millions)Value (EUR)Risk(Beta)Value(EUR)Risk(Beta)Operating assets 400 0.71 Debt 196 0.00Equity 2041.40 Total assets 400 0.71 Total liabilities & equity 400 0.71Exhibit 4Shire Manufacturing (including pension plan)Full Economic Balance Sheet(EUR values in millions)Value (EUR)Risk(Beta)Value(EUR)Risk(Beta)Operating assets 400 0.42 Debt 196 0.00Pension assets 200 0.60 Pension liabilities 200 0.00Equity 2041.40Total assets 600 0.48 Total liabilities & equity 600 0.48C. Determine the most likely effect on Shire’s future firm value (lower, no effect, higher) ofusing the full economic balance sheet, rather than the standard balance sheet, whenmaking capital budgeting decisions. Justify your response with one reason.(4 minutes)Hagar decides to decrease the equity allocation in the pension plan from 60% of plan assets to40%, by shifting 20% of the portfolio from equity into fixed income.D. Explain the most likely effect on Shire’s cost of equity capital of making the change inthe plan’s asset allocation while using the full economic balance sheet.Note: No calculations are required.(3 minutes)ANY MARKS MADE ON THIS PAGE WILLNOT BE GRADED。

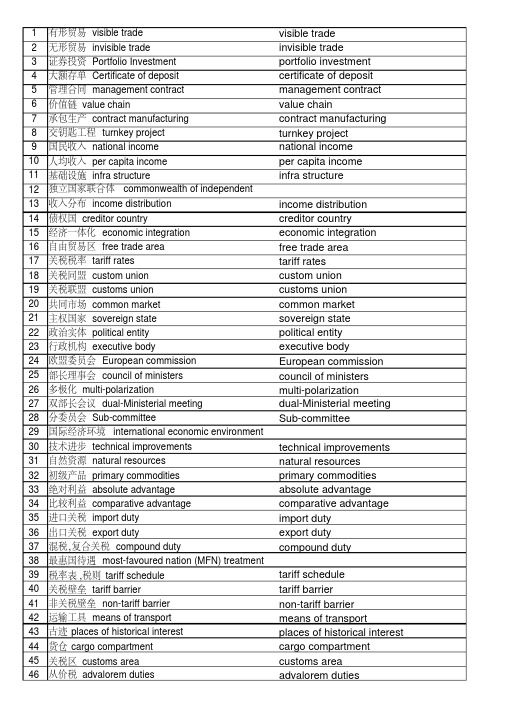

自考05844国际商务英语(真题-翻译)

1有形贸易 visible trade visible trade 2无形贸易 invisible tradeinvisible trade3证券投资 Portfolio Investment portfolio investment 4大额存单 Certificate of depositcertificate of deposit 5管理合同 management contract management contract 6价值链 value chainvalue chain7承包生产 contract manufacturing contract manufacturing 8交钥匙工程 turnkey project turnkey project 9国民收入 national income national income 10人均收入 per capita income per capita income 11基础设施 infra structureinfra structure1213收入分布 income distribution income distribution 14债权国 creditor countrycreditor country15经济一体化 economic integration economic integration 16自由贸易区 free trade area free trade area 17关税税率 tariff rates tariff rates 18关税同盟 custom union custom union 19关税联盟 customs union customs union 20共同市场 common market common market 21主权国家 sovereign state sovereign state 22政治实体 political entity political entity 23行政机构 executive bodyexecutive body24欧盟委员会 European commission European commission 25部长理事会 council of ministers council of ministers 26多极化 multi-polarization multi-polarization27双部长会议 dual-Ministerial meeting dual-Ministerial meeting 28分委员会 Sub-committeeSub-committee 2930技术进步 technical improvements technical improvements 31自然资源 natural resources natural resources 32初级产品 primary commodities primary commodities 33绝对利益 absolute advantage absolute advantage 34比较利益 comparative advantage comparative advantage 35进口关税 import duty import duty 36出口关税 export dutyexport duty 37混税,复合关税 compound dutycompound duty3839税率表,税则 tariff schedule tariff schedule 40关税壁垒 tariff barriertariff barrier41非关税壁垒 non-tariff barrier non-tariff barrier 42运输工具 means of transport means of transport43古迹 places of historical interest places of historical interest 44货仓 cargo compartment cargo compartment 45关税区 customs area customs area 46从价税 advalorem dutiesadvalorem duties独立国家联合体 commonwealth of independent 国际经济环境 international economic environment 最惠国待遇 most-favoured nation (MFN) treatment47贸易术语 trade terms trade terms48贸易惯例 trading practices trading practices49商品交易会 trade fairs trade fairs50长途电话 trunk call trunk call51有效期 validity period validity period52还盘 counter offer counter offer53销售合同 sales contract sales contract54销售确认书 sales (purchase) confirmation sales (purchase) confirmation55缔约方/合约各方 contracting parties contracting parties56不可抗力 force majeure force majeure57货号 article number article number58棉布 cotton piece goods cotton piece goods59棉纱 cotton yarns cotton yarns60对销贸易 counter trade counter trade61欧洲支付联盟 European payment union European payment union62竞争性贬值 competitive devaluation competitive devaluation63加工贸易 processing trade processing trade64清算系统 clearing system clearing system65实际头寸 net positions net positions66贸易信贷往来帐户 trade credit accounts trade credit accounts67反向购买 counter purchase counter purchase68回购交易 buyback buyback69租赁贸易 leasing trade leasing trade70财务状况 financial standing financial standing71资信可靠情况 credit worthiness credit worthiness72分阶段付款 periodic payments periodic payments73预付现金 cash in advance cash in advance74汇票 draft / bill of exchange draft/bill of exchange75远期汇票 usance draft usance draft76跟单汇票 documentary draft documentary draft77提单 bill of landing bill of landing78货物所有权 title to goods title to goods79保险单 insurance policy insurance policy80跟单托收 documentary collection documentary collection81付款交单 documents against payment (D/P)documents against payment (D/P) 82承兑交单 documents against acceptance (D/A)documents against acceptance (D/A) 83光票 clean draft clean draft84开证银行opening bank opening bank85往来行 correspondence bank correspondence bank86通知行 advising bank advising bank87保兑行 confirming bank confirming bank88分批装运 partial shipment partial shipment89保兑信用证 confirmed letter of credit confirmed letter of credit90价格条款 price term price term91光票信用证 clean credit clean credit92非贸易结算 non-trade settlement non-trade settlement93可撤销信用证 revocable credit revocable credit94不可撤销信用证 irrevocable credit irrevocable credit95双重保障 double assurance double assurance96即期信用证 sight credit sight credit97远期信用证 usance credit usance credit98面值 face value face value99可转让信用证 transferable credit transferable credit100不可转让信用证 non-transferable credit non-transferable credit101无汇票信用证 non-draft credit non-draft credit102推迟付款 deferred payment deferred payment103循环信用证 revolving credit revolving credit104唛头 shipping marks shipping marks105被通知人 notify party notify party106货运收据 cargo receipt cargo receipt107发运港 port of shipment port of shipment108海关发票 custom invoice custom invoice109领事发票 consular invoice consular invoice110装船通知 shipping advice shipping advice111产品自然领域 natural product provinces natural product provinces112公共承运人 common carrier common carrier113契约承运人 contract carrier contract carrier114自有承运人 private carrier private carrier115中间产品 intermediate product intermediate product116制成品 finished products finished products117最大诚信原则 utmost good faith utmost good faith118货物原产地港口 port of origin port of origin119交货费用 forwarding charges forwarding charges导致损失的直接原因 proximate cause of the loss120121汇率 exchange rate exchange rate122金本位制 gold standard gold standard123平价 par value par value124储备货币 reversed currency reversed currency125清洁浮动 clean float (free float-自由浮动)clean float 清洁浮动 (free float 自由浮动) 126肮脏浮动 dirt float (managed float-管理浮动)dirt float 肮脏浮动 (managed float 管理浮动) 127(汇率)直接标价 direct quote direct quote128(汇率)间接标价 indirect quote indirect quote129买入价 buying rate buying rate130卖出价 selling rate selling rate131中间价 medial rate medial rate132大萧条 Great Depression great depression133特别提款权 special drawing right special drawing right134国际收支赤字 BOP deficit BOP deficit135国际收支盈余 favorable balance of payment favorable balance of payment136贴现率 discount rate discount rate137外汇管制 foreign exchange control foreign exchange control138游资 idle funds (hot money)idle funds (hot money)139世界银行集团 word bank group word bank group140资本市场 capital market capital market141优惠期 grace period grace period142私营经济 private sector private sector143股权投资 equity investment equity investment144经济结构调整 economic restructuring economic restructuring145投票权 voting power voting power146黄金份额 gold tranche gold tranche147备用(信贷)安排 standby arrangement standby arrangement148客户流动 customer mobility customer mobility149免税期 tax holiday tax holiday150合资企业 joint venture joint venture151绿地战略 the greenfield strategy the greenfield strategy152战略联合 the strategic alliance the strategic alliance153知识产权 intellectual property intellectual property154常务委员会 standing committee standing committee155证券交易所 stock exchange stock exchange156长期资本 long-term capital long-term capital157二级资本市场 secondary capital market secondary capital market158交易场地 market floor (trading floor)market floor (trading floor)159挂牌证券交易市场 listed market listed market160所得税 income tax income tax161平衡帐目 balance the books balance the books 公共部门借贷需求 the public sector borrowing requirement162163金边证券 gilt-edged stocks / securities gilt-edged stocks/securities164事业机构投资商 institutional investors institutional investors165期权 options options166套期保值 hedge hedge167具体事场 particular market area particular market area168普惠制 generalized system of preferences generalized system of preferences 169关税减让 tariff concession tariff concession170制度力量 institutional strength institutional strength171反贴补措施 counter-veiling measures counter-veiling measures172反倾销 anti-dumping anti-dumping173国民待遇 national treatment national treatment174关税配额 tariff quota tariff quota175充分就业 full employment full employment176公平贸易 fair trade fair trade177贸易条款 term of trade term of trade178免责条款 escape clauses escape clauses179行动纲领 action programme action programme180联合国大会 united nations general assembly united nations general assembly 181较不发达国家 less-developed countries less-developed countries182无差别待遇 non-discrimination principle non-discrimination principle183差别待遇 differential treatment differential treatment184贸易条件 terms of trade terms of trade185186特惠税 preferential customs tariffs preferential customs tariffs 187技术转让 transfer of technology transfer of technology188金融市场 financial market financial market189中期贷款 extended fund facility extended fund facility190双边谈判 bilateral negotiation bilateral negotiation191特约条款 special clause special clause192董事会 board of directors board of directors193生产方式 production approach production approach194可保利益 insurable interest insurable interest195缓冲库存贷款 buffer stock financing facility buffer stock financing facility 196跨国公司母公司 parent MNC parent MNC197记帐交易 open credit open credit198滚装滚卸范畴运输 roll-on and roll-off traffic roll-on and roll-off traffic199规模经济 economies of scale economies of scale200有价保单 valued policy valued policy201从量税 specific duty specific duty202业务范围 business line business line203基础设施 capital infrastructure capital infrastructure204布雷顿森林会议 the Bretton woods convention the Bretton woods convention 205保证金 margin margin206统一关税制度 uniform tariff system uniform tariff system207208209210211212 213 214 215 216 217 218 219 220 221 222 223 224电子数据交换EDI (Electronic Data Interchange)国内生产总值GDP (Gross Domestic Product)国民生产总值GNP (Gross National Product)购买力平价PPP (Purchasing Power Parity)增值税VAT (value added tax)国际经济新秩序 new international economic order石油输出国组织OPEC (Organization of Petroleum Exporting Countries)东南亚国家联盟ASEAN (Association of SouthEast Asian Nations)北美自由贸易协定NAFTA (North American Free Trade Agreement)多边投资担保机构MIGA (Multilateral Investment Guarantee Agency)经济及社会理事会ECOSOC (economic social council)国际开发协会IDA (International Development Association)国际货币基金组织IMF (International Monetary Fund)经济合作与发展组织OECD (Organization of Economic Cooperation and Development)零库存 just-in-time delivery (JIT)自动出口限制VER (Voluntary Export Restriction)投资交易所RIE (Recognized Investment Exchange)国际复兴开发银行IBRD (International Bank for Reconstruction and Development)国际金融公司IFC (International Finance Corporation)。

【CFA笔记】portfolio_management(7%)_

Portfolio Management: An OverviewOne measure of the benefits of diversification is the diversification ratio. It is calculated as the ratio of the risk of an equally weighted portfolio of n securities (measured by its standard deviation of returns) to the risk of a single security selected at random from the n securities.例子:If the average standard deviation of returns for the n stocks is 25%, and the standard deviation of returns for an equally weighted portfolio of the n stocks is 18%, the diversification ratio is 18 / 25 = 0.72.Foundations and endowments typically have long investment horizons, high risk tolerance, and, aside from their planned spending needs, little need for additional liquidity.Banks seek to keep risk low and need adequate liquidity to meet investor withdrawals as they occur.Insurance companies invest customer premiums with the objective of funding customer claims as they occur. Life insurance companies have a relatively long-term investment horizon, while property and casualty财产和意外保险(P&C) insurers have a shorter investment horizon because claims are expected to arise sooner than for life insurers.Sovereign wealth funds refer to pools of assets owned by a government.A defined contribution pension plan is a retirement plan in which the firm contributes a sum each period to the employee’s retirement account.In a defined benefit pension plan, the firm promises to make periodic payments to employees after retirement.There are three major steps in the portfolio management process:Step 1: The planning step begins with an analysis of the investor’s risk tolerance, return objectives, time horizon, tax exposure, liquidity needs, income needs, and any unique circumstances or investor preferences.This analysis results in an investment policy statement (IPS)that details the investor’s investment objectives and constraints.Step 2: The execution step involves an analysis of the risk and return characteristics of various asset classes to determine how funds will be allocated to the various asset types.in what is referred to as a top-down analysis, a portfolio manager will examine current economic conditions and forecasts of such macroeconomic variables as GDP growth, inflation, and interest rates, in order to identify the asset classes that are most attractive.Step 3: The feedback step is the final step. Over time, investor circumstances will change, risk and return characteristics of asset classes will change, and the actual weights of the assets in the portfolio will change with asset prices.Mutual funds are one form of pooled investments (i.e., a single portfolio that contains investment funds frommultiple investors). Each investor owns shares representing ownership of a portion of the overall portfolio. The total net value of the assets in the fund (pool) divided by the number of such shares issued is referred to as the net asset value (NA V) of each share.With an open-end fund, investors can buy newly issued shares at the NA V. Newly invested cash is invested by the mutual fund managers in additional portfolio securities. Investors can redeem their shares (sell them back to the fund) at NA V as well. All mutual funds charge a fee for the ongoing management of the portfolio assets, which is expressed as a percentage of the net asset value of the fund. No-load funds免佣基金do not charge additional fees for purchasing shares (up-front fees) or for redeeming shares (redemption fees). Load funds charge either up-front fees, redemption fees, or both.Closed-end funds are professionally managed pools of investor money that do not take new investments into the fund or redeem investor shares. The shares of a closed-end fund trade like equity shares (on exchanges or over-the-counter). As with open-end funds, the portfolio management firm charges ongoing management fees.T ypes of Mutual Funds:Money market funds invest in short-term debt securities and provide interest income with very low risk of changes in share value.Bond mutual funds invest in fixed-income securities. They are differentiated by bond maturities, credit ratings, issuers, and types.A great variety of stock mutual funds are available to investors. Index funds are passively managed; that is, the portfolio is constructed to match the performance of a particular index, such as the Standard & Poor’s 500 Index. Actively managed funds refer to funds where the management selects individual securities with the goal of producing returns greater than those of their benchmark indexes.Other Forms of Pooled Investments:Exchange-traded funds (ETFs) are similar to closed-end funds in that purchases and sales are made in the market rather than with the fund itself.【相同之处】【ETFs和close end fund不同之处】While closed-end funds are often actively managed, ETFs are most often invested to match a particular index (passively managed). With closed-end funds, the market price of shares can differ significantly from their NA V due to imbalances between investor supply and demand for shares at any point in time. Special redemption provisions for ETFs are designed to keep their market prices very close to their NA Vs.【ETFs和open end fund不同之处】ETFs can be sold short, purchased on margin, and traded at intraday盘中交易价prices, whereas open-end funds are typically sold and redeemed only daily, based on the share NA V calculated with closing asset prices.Investors in ETFs must pay brokerage commissions when they trade, and there is a spread between the bid price at which market makers will buy shares and the ask price at which market makers will sell shares.With most ETFs, investors receive any dividend income on portfolio stocks in cash, while open- end funds offer thealternative of reinvesting dividends in additional fund shares.One final difference is that ETFs may produce less capital gains liability compared to open- end index funds. This is because investor sales of ETF shares do not require the fund to sell any securities. If an open-end fund has significant redemptions that cause it to sell appreciated portfolio shares, shareholders incur a capital gains tax liability.A separately managed account is a portfolio that is owned by a single investor and managed according to that investor’s needs and preferences. No shares are issued, as the single investor owns the entire account.Portfolio Risk and Return: Part IHolding period return (HPR) is simply the percentage increase in the value of an investment over a given time period:The geometric mean return is a compound annual rate. When periodic rates of return vary from period to period, the geometric mean return < the arithmetic mean return:The money-weighted rate of return is the internal rate of return on a portfolio based on all of its cash inflows and outflows.Gross return refers to the total return on a security portfolio before deducting fees for the management and administration of the investment account. Net return refers to the return after these fees have been deducted.Note that commissions on trades and other costs that are necessary to generate the investment returns are deducted in both gross and net return measures.Pretax nominal return refers to the return prior to paying taxes.After-tax nominal return refers to the return after the tax liability is deducted.year when inflation is 2%. The investor’s approximate real return is simply 7 - 2 = 5%. The investor’s exact real return is slightly lower, 1.07 / 1.02 - 1 = 0.049 = 4.9%.A leveraged return refers to a return to an investor that is a multiple of the return on the underlying asset.The leveraged return is calculated as the gain or loss on the investment as a percentage of an investor’s cash investment. An investment in a derivative security, such as a futures contract, produces a leveraged return because the cash deposited is only a fraction一小部分of the value of the assets underlying the futures contract. Leveraged investments in real estate are very common: investors pay for only part of the cost of the property with their own cash, and the rest of the amount is paid for with borrowed money.small-capitalization stocks have had the greatest average returns and greatest risk over the period.Covariance measures the extent to which two variables move together over time. A positive covariance means that the variables (e.g., rates of return on two stocks) tend to move together. Negative covariance means that the two variables tend to move in opposite directions.Here we will focus on the calculation of the covariance between two assets’ returns using historical data.The covariance of the returns of two securities can be standardized by dividing by the product of the standard deviations of the two securities. This standardized measure of co-movement is called correlation and is computed as:A risk-averse investor is simply one that dislikes risk (i.e., prefers less risk to more risk). Given two investments that have equal expected returns, a risk-averse investor will choose the one with less risk (standard deviation).A risk-seeking (risk-loving) investor actually prefers more risk to less and, given equal expected returns, willchoose the more risky investment. A risk-neutral investor has no preference regarding risk and would be indifferent between two such investments.The variance of returns for a portfolio of two risky assets is calculated as follows:Note that portfol io risk falls as the correlation between the assets’ returns decreases. This is an important result of the analysis of portfolio risk: The lower the correlation of asset returns, the greater the risk reduction (diversification) benefit of combining assets in a portfolio. If asset returns were perfectly negatively correlated, portfolio risk could be eliminated altogether for a specific set of asset weights.For each level of expected portfolio return, we can vary the portfolio weights on the individual ass ets to determine the portfolio that has the least risk. These portfolios that have the lowest standard deviation of all portfolios with a given expected return are known as minimum-variance portfolios. T ogether they make up the minimum-variance frontier. On a risk versus return graph, the portfolio that is farthest to the left (has the least risk) is known as the global minimum-variance portfolio整体最小方差投资组合.Assuming that investors are risk averse, investors prefer the portfolio that has the greatest expected return when choosing among portfolios that have the same standard deviation of returns. Those portfolios that have the greatest expected return for each level of risk (standard deviation) make up the efficient frontier.An investor’s utility function效用函数represents the investor’s preferences in terms of risk and return (i.e., his degree of risk aversion).An indifference curve is a tool from economics that, in this application, plots combinations of risk (standard deviation) and expected return among which an investor is indifferent.a more risk-averse investor will have steeper indifference curves, reflecting a higher risk aversion coefficient. Combining a risky portfolio with a risk-free asset is the process that supports the two- fund separation theorem, which states that all investors’ optimum portfolios will be made up of some combination of an optimal portfolio of risky assets and the risk-free asset. The line representing these possible combinations of risk-free assets and theoptimal risky asset portfolio is referred to as the capital allocation line.Now that we have constructed a set of the possible efficient portfolios (the capital allocation line) Portfolio Risk and Return: Part IIThe line of possible portfolio risk and return combinations given the risk-free rate and the risk and return of a portfolio of risky assets is referred to as the capital allocation line (CAL).A simplifying assumption underlying modern portfolio theory (and the capital asset pricing model, which is introduced later in this topic review) is that investors have homogeneous expectationsDepending on their preferences for risk and return (their indifference curves), investors may choose different portfolio weights for the risk-free asset and the risky (tangency) portfolio. Every investor, however, will use the same risky portfolio. When this is the case, that portfolio must be the market portfolio of all risky assets because all investors that hold any risky assets hold the same portfolio of risky assets.只有与有效边界相切的那条才是CML。

purchasing management外文文献

purchasing management外文文献Purc hasing ManagementAbstractThis paper will analyze the role of Purchasing Management in today’s business environment. The paper will discuss the various functions of Purchasing Management and how it has become an integral part of the Supply Chain Management (SCM) process. The paper will also focus on the role Purchasing Management has in helping organizations achieve efficiency and cost savings. Additionally, the paper will discuss some best practices that can be implemented to ensure that Purchasing Management is efficient, effective and beneficial to the organization.Keywords: Purchasing Management, Supply Chain Management, Efficiency, Cost Savings.IntroductionPurchasing Management is an essential function in any organization as it plays a critical role in the overall success of the organization. It is responsible for ensuring that the right goods and services are provided at the right price and to the right specifications in order to meet customer satisfaction and organizational objectives. The success of anyorganization depends upon efficient Purchasing Management processes that are able to deliver the desired results while at the same time reducing overall costs. This paper will analyze the various roles of Purchasing Management and how it has become an integral part of the Supply Chain Management (SCM) process. Additionally, it will discuss some best practices that can be implemented in order to ensure that Purchasing Management is efficient, effective and beneficial to the organization.AnalysisThe role of Purchasing Management is to ensure that the right goods and services are provided at the right price and to the right specifications in order to meet customer satisfaction and organizational objectives. The primary objective of Purchasing Management is to reduce the overall costs incurred by the organization. Purchasing Management is usually conducted through the procurement process which involves the identification, selection, negotiation and purchase of goods and services that are required by the organization. The procurement process can be divided into two main categories: direct procurement and indirect procurement. Direct procurement is the purchase of goods and services from external vendors, while indirect procurement is the purchaseof services and materials from within the organization.Purchasing Management is an integral part of the Supply Chain Management (SCM) process. SCM is a process that focuses on the coordination and optimization of supply and demand across multiple stages of the supply chain. Purchasing Management is responsible for managing the relationship between suppliers and customers, negotiating contracts and pricing, and ensuring that goods and services purchased meet the specifications of the customer and organization. Additionally, Purchasing Management is responsible for managing supplier performance to ensure that suppliers are able to deliver the desired quality and quantity of goods and services in a timely manner.Best PracticesIn order to ensure that Purchasing Management is efficient, effective and beneficial to the organization, the following best practices should be implemented:Develop effective policies and procedures: Organizations should develop policies and procedures that are simple, easy to understand and provide guidance on the purchasing process. Use technology to automate processes: Technology can be used to automate processes such as issuing purchase orders,tracking deliveries and managing inventory.Leverage supplier relationships: Organizations should strive to build strong relationships with suppliers in order to ensure that the best value for money is obtained.Negotiate contracts: Organizations should negotiate contracts with suppliers in order to ensure that prices remain competitive and the organization gets the best deal.Monitor supplier performance: Organizations should monitor suppliers performance in order to ensure that the desired quality and quantity of goods and services are delivered in a timely manner.ConclusionIn conclusion, Purchasing Management is an essential function in any organization as it plays a critical role in the overall success of the organization. The primary objective of Purchasing Management is to reduce the overall costs incurred by the organization. Additionally, Purchasing Management is an integral part of the Supply Chain Management (SCM) process as it is responsible for managing the relationship between suppliers and customers, negotiating contracts and pricing, and ensuring that goods and services purchased meet the specifications of the customer and organization. In order toensure that Purchasing Management is efficient, effective and beneficial to the organization, organizations should strive to implement the best practices discussed in this paper.。

必须将采购环节纳入供应管理【外文翻译】

外文翻译原文Purchasing Must Become Supply ManagementMaterial Source:Harvard Business School Author:Peter Kraljic Whenever a manufacturer must procure a volume of critical items competitively under complex conditions,supply management is relevant.The greater the uncertainty of supplier relationships,technological developments,and/or physical availability of those items,the more important supply management becomes.A company’s need for a supply strategy depends on two factors:(1)the strategic importance of purchasing in terms of the value added by product line,the percentage of raw materials in total costs and their impact on profitability,and soon;And(2)the complexity of the supply market gauged by supply scarcity,pace of technology and/or materials substitution,entry barriers,logistics cost or complexity,and monopoly or oligopoly conditions(see Exhibit I).By assessing the company’s situation in terms of thes two variables,top management and senior purchasing executives can determine the type of supply strategy the company needs both to exploit its purchasing power vis-á-vis important suppliers and to reduce its risks to an acceptable minimum.Attractive new options,or serious vulnerabilities,or both,may come to light as the assessment explores questions like these:1.Is the company making good use of opportunities for concerted action among different divisions and/or subsidiaries?Combining the supply requirements of different divisions can increase the corporation’s total buying clout.One in ternational transportation company was buying three kinds of fuel separately:bunker oil for shipping,jet fuel for airfreight, and gasoline for trucks.Only after consolidating and combining these volumes at the corporate level could the company bring its true bargaining weight to bear.2.Can the company avoid anticipated supply bottlenecks and interruptions?When an automotive parts maker analyzed its sintered metal components supply market,from which it had been sourcing for years,it discovered that poli tical instability was jeopardizing its supply.The company’s top management promptly ordered a change in purchasing policy to build up alternative domestic sources.3.How much risk is acceptable?Vendor mix,extent of contractualcoverage,regional spread of supply sources,and availability of scarce materials all contribute to the company’s supply risk profile.A company can often take action to lessen unacceptable risk.For example,a company that meets annual materials requirements exclusively through long-term contracts may achieve substantial savings through the use of“evergreen”contracts(annual agreements)that include a rollover option.Conversely,a manufacturer that relies solely on spot purchases may do well to mix spot purchases and supply contracts.4.What make or buy policies will give the best balance between cost and flexibility?If the company covers a large percentage of its supplies from sources it owns,it will be in a much better negotiating position to cover the remainder of its outside requirements than its less integrated competitors.Dow Chemical,BASF,and DuPont have all reduced their supply vulnerability through backward integration in response to long-term considerations.On the other hand,the company may find it more profitable to source outside if key suppliers have chronic overcapacity.5.To what extent might cooperation with suppliers or even competitors strengthen long-term supply relationships or capitalize on shared resources?Italy’s Alfa Romeo and Japan’s Nissan share the production o f certain critical car components that they could not produce cost-effectively on their own.General Motors is increasingly involving suppliers early in the design process in order to ensure better quality,lower cost,and“just in time”production.Shaping the Supply Strategy.To minimize their supply vulnerabilities and make the most of their potential buying power,a number of European companies have successfully used a four-stage approach to devise strategies.The approach has given them a simple but effective framework for collecting marketing and corporate data,forecasting future supply scenarios,and identifying available purchasing options as well as for developing individual supply strategies for critical items and materials.Following this approach,the company first classifies all its purchased materials or components in terms of profit impact and supply risk.Next it analyzes the supply market for these materials.Then it determines its overall strategic supply position.Finally,it develops materials strategies and action plans.Practical ApplicationsThe usefulness of the purchasing portfolio approach in a variety of industrialsituations can be seen in the diverse experience of four large companies.Not long ago a welding materials producer with plants and sales operations all over Europe found its profits squeezed by increased competition andslackening market growth.Searching for ways to improve the picture,the company found that supplies were critical to the production of its welding wires and electrodes.Together,just five out of the 470 different items it purchased accounted for more than 60% of the company’s total purchasing volume of$135 million.Taking into account demand growth,quality standards,and logistics,the company then analyzed the European market for these five items in light of its own plant-by-plant requirements.A third step determined the company’s position against a wide range of individual suppliers and assessed the risk of increasing the share sourced from each one.Finally,the company developed several strategic supply scenarios,each involving a different mix of suppliers and different assumptions about price,volume,and risk.The scenarios ranged from very low risk(total dependence on well-established sources)to very high(most purchases form lesser-known,geographically dispersed suppliers).Cost-benefit analyses of each enabled management to pinpoint several opportunities for substantial improvement.On one key item alone,electrode wire,the company’s potential annual savings ranged from$1.5 million to$6.3 million,or 3%to 12%of the total cost.Supply strategies the company worked out for other key items resulted in an overall saving of 10%on purchased materials,adding some 3%to 4%to the company’s pretax profits.Action plans and decision and monitoring rules developed for each item enabled buyers to implement the new sourcing strategy and permitted management to monitor purchasing activities regularly,in some cases on a day-to-day or bid-by-bid basis.A large U.S.-based maker of electrical equipment categorized castings as a keystrategic purchased item and systematically analyzed its own demand in terms of the annual volume and relative complexity of each type of casting.It assessed,foundry by foundry,the capabilities of each potential supplier and decided,by comparing alternative supply scenarios,which was the best fit.The resulting new mix of outside suppliers reduced the company’s outlays for castings by 5%to 15% and significantly improved its competitive cost position.Anxious to reduce the risks associated with current sources of feedstock supply,a multinational chemical company revamped its entire purchasing strategy and organization.Out of more than 5,000 purchased items,the company defined 75 as strategic or bottleneck feedstocks.Detailed analysis of both demand and supply confirmed that,thanks to the sheer volume of its purchases,the company enjoyed a strong position in most feedstock supply markets.Its risk profile,however, gave real cause for concern.Accordingly,the company spread its hydrocarbons procurement amongpetroleum-and coal-based feedstocks;balanced its geographic base among Middle Eastern,African,North Sea,North American,and Latin American sources;changed its contracts-to-spot-purchases ratio;optimized its make-or-buy mix by integrating backward;and began to rely on wholly owned subsidiaries for a bigger share of its feedstock requirements.In addition,a corporate-level review revealed attractive trade-off and substitution opportunities,which the corporation soon set about exploiting,once it had changed and upgraded its purchasing organization and systems in order to do so.Faced with sharp rises in the labor and overhead costs of producing highprecision parts in-house,a Europe-based heavy-equipment maker decided to review its make-or-buy strategy.Examining the supply market,it identified a group of obscure,small manufacturers of precision parts that had begun to use dedicated,numerically controlled equipment.Thanks to low overhead and economies of scale achieved through specialized production,they could supply high-quality parts at prices 10%to 20%below the cost of inhouse production.In consequence,the company shifted from making the parts to buying them.译文必须将采购环节纳入供应管理资料来源:哈佛商学院作者:Peter Kraljic 制造商在激烈的竞争环境下获得一个订单,并完成它,供应链管理起着很大的影响。

(工厂管理)工厂英文经典知识缩写

英文经典知识缩写AF Acceleration factorALT Accelerated life testANOVA Analysis of VarianceAOQL Average Outgoing Quality LevelAPO Auto Power OffAPQP Advanced Product Quality Planning and Control Plan ARE Area OptionsASIC Application Specific Integrated CircuitASSP Application Specific Standard PartATE Automatic test equipmentATO Assembly To OrderAVL RFQ IMPUT CHECKLIST里面用到BAC BackupBCI Bulk current injectionBD Business DeveloperBFR Batch Failure Ratebo BochumBOM Bill of MaterialBU Business Unitc acceptance level (= number of failed components accepted) CBD Cost Break DownCDM Contract Design ManufacturerCDM Charge Device Model –discharge typeCDM Original Design done by Partner specifically to support NokiaCDN Coupling and Decoupling Network.CE Concurrent EngineeringCE Concurrent Engineering (used for product development) CE. E0...E5 Concurrent Engineering (CE) Product Program MilestonesCEM Contract Electronic ManufacturerCER. FILTERS, MONOBL. DUPLEXERS Powder mixing, Block pressing, FiringCI Capacity ImplementationCIM Custom In MouldCLUSTER Group of companies, head by one Cluster leader CM Cost ManagementCMO Customer & Market Operationsco CopenhagenCOC Certificate of complianceCOO Country of OriginCp, Cpk Process Capability indicesCpk Capability IndexCPL Cost Part listCQE Component Quality EngineerCQP Component Quality PlanningCQS Component Quality SpecialistCR Change RequestCRR Component review reportCRYSTALS Crystal wafer manufacturingCSA Current State AnalysisCSMC-TPAT Customs-Trade Partners Against TerrorismCTS Cost Target SettingD Draft, first version of the documentda DallasDC DirectDC Direct CurrentDCN Design change noticeDES Deselect allDFA Design For AssemblyDFBA Design for Board AssemblyDFDS Design for Demand SupplyDfE Design for EnvironmentDFFA Design for Final AssemblyDFM Design For Manufacturing (includes DFPT, DFBA, DFFA) DFMEA Design Failure Mode and Effects AnalysisDFPT Design for Production TestDGDI-EL. DUPLEXERS Resonator preparingDIR Design Improvement ReportsDocMan Type of Lotus Notes database (for documents) DOE Design Of ExperimentDOE Design Of ExperimentDPM Defects Per MillionDSB Demand Supply BalanceDSN Demand Supplier NetworkDUT Device Under TestDV Demand VolumeDVRE0...E5 Concurrent Engineering (CE) MilestonesE0..E5 Concurrent engineering (CE) milestonesECN Engineering Change NoticeEFR Early Failure RateELMECH Electro MechanicalEMC Electro Magnetic CompatibilityEMI Electro Magnetic InterferenceEMS Environmental Management Sys-temEN European NormEoL End of LifeEPA ESD protected areaERPes EspooESD Electrostatic dischargeESDS Electrostatic discharge sensitive deviceESI Early Supplier InvolvementETA Estimate to be arriveEUT Equipment Under TestEV Enclosed volumeEVM Enhancements Version ManagementF Final, document to be archivedFA Failure AnalysisFAC Fully anechoic chamberFAQ Frequently Asked QuestionsFAI First article inspectionFEM Finite Element ModellingFFR Field Failure RateFIL Filter..FIML Fabric Inmold Labeling, same with CIM Custom In Mould FIT Failures in TimeFMEA Failure Mode and Effect AnalysisFORFOT 第一次试模FR Failure RateG.A. General AssemblyGauge R&R Gauge Repeatability and Reproducibility GCPMGD&T Geometrical Dimensioning & TolerancesGRP ground reference planeGRR Gauge Repeatability and ReproducibilityHBM Human Body ModelHBM Human Body Model –discharge typeHCP horizontal coupling planeHIGH Highlight selectedhk Hong KongHUB Warehousing and Shipping functionality locationICDR Integrated Circuit Design ReviewsICDR IC Design ReviewID Industrial DesignIFR Intrinsic Failure RateIMD Insert Mold DecorationIME Inject Mold EquipmentIML Insert Mold LabelingIML IN MOLD LABELINGIPQC In Process Quality ControlIPR Intellectual Property RightsISO International Standardization Organization jk JyväskyläJR&D Joint Research and developmentKCR Key Component ReviewKO Kick OffLA License Agreementla Los AngelesLAB LabelLCL Lower Control LimitLL Lesson LearnedLRVP Long Range Volume PlanLSL Lower Specification LimitLSSE Light SW Subcontractor EvaluationM&O Mechanics & OutsourcingM/C machineM3 Global quality databaseMAR Mechanics Acceptance ReportMAR’s Mechanical Acceptance Report’s MatCoMaMC Measuring CentreMD Mechanics DesginMDF Material Data FormMDFs material data formsME Manufacturing EngineerMECH MechanicsMFI Melt flow indexMISMM Machine Model –discharge typeMOR Monthly Operation ReviewMOSS Visual Quality Criteria’s procedureMPL Material Project LeaderMPL / M Material Project Leader / Manager MPL/MPM Material Project Leader/ ManagerMPM Material Project ManagerMR Measurements ReportMRPⅡMS Manufacturing SolutionsMS MilestoneMSA Measurement System AnalysisMSID Moisture-Sensitive IdentificationMSM Mechnical Supplier ManagementMSM Mechanics Sourcing ManagerMTO Make TO OrderMTS Mechanical Technology SourcingMULTIL.PRODUCTS Ceramic powder manuf, Sheet forming, Cutting, Printing, FiringNC non connectNCTNDA Non Disclosure AgreementNET Nokia NetworksNET NetworksNGP Nokia Global ProcessesNGS Nokia Global StandardsNGSW Nokia Global Supplier WebNMP Nokia Mobile Phones LtdNOSS Nokia Supplier Status databaseNPI Nokia Product IntegrationNPI New Product IntroductionNPSQS Nokia Part Specific Quality StandardsNRT Nokia Rapid ToolingNSL Nokia Substance ListNSM Nokia Supplier ManualNSR Nokia Supplier RequirementNTP Normal temperature and pressure, see laboratory environmentOAP Original Accessory PartnerOCAP Out-of-Control Action PlanOCV Open Circuit VoltageODM Original Design ManufacturerODM Original Design done by Partner independently OEM Original Equipment ManufactureOEM Original Design done by NokiaOPL Operations Project LeaderOQC Outgoing Quality ControlORS Operating Resource SourcingOT Over timeOTD On time deliveryou OuluPA Process AssessmentPA Product AgreementPC Product CreationPC PolycarbonatePCBAPCN Process Change NoticePCNs product change notification casesPCQE Program Component Quality EngineerPCQM Program Component Quality ManagerPD Product DeliveryPDM Product Development ManagerPDM Product Data ManagementPDM Product Data Management SystemPDT Project Development TeamPE Product Engineering (used for product in mass production)PFMEA Process Failure Mode and Effect AnalysisPGP Pretty Good PrivacyPI Product ImplementationPIRPLM Product Line ManagementPLP Product Lifetime ProfitabilityPLRM Program Loading Road mapPM Product ManagerPM Purchasing ManagerPM Project ManagerPM/MP Partner Manufacturing/Manufacturing Partner PMA Project Manager AssistantPMCPMM Program Portfolio ManagementPMT Project Management TeamPO Purchasing OrderPOKA-YOKE Mistake ProofingPOP Package Operation ProcedurePop-Port System connector in NOKIA mobile devices POWER AMPS MMIC and/or IC manufacturingPp, Ppk Process Performance IndicesPPA Product Purchase AgreementPPAP Production Part Approval ProcessPPM Product Program Managerppm Parts per millionPQ Process QualificationPQGFP Package qualification guideline for programs PQM Program Quality ManagerPQP Program Quality PlanPQP Package Qualification ProcedurePR1/2PTO Package TO OrderPV Product ValidationPVD Physical Vapor DepositionPWB Printed Wire BoardQA quality assurenQBR Quarterly Business ReviewQC quality controlQE Quality EngineerQFD Quality Function DeploymentQM quality managementQSR Quality System RequirementQTE Quality Technician EngineerQTE Quality and Technology EngineerQTE / QTM Quality Technology Engineer / ManagerQTE / QTM Quality Technology Engineer / ManagerQTM Quality and Technology ManagerQTY QuantityR&D Research and DevelopmentR&R Roles and ResponsibilitiesR&T Research and TechnologyRAM Random Access MemoryRamp Up/SAREC ReconsiderREL Related toRFP Request For ProposalRFQ Request For QuotationRIPS Recently Introduced Product SupportRMA Return Material AuthorizationSASAC semi anechoic chamberSAW /BAW FILTERS, SAW DUPLEXERS Die wafer manufacturing SCP Service Channel PreparationSEM Scanning Electron MicroscopeSG Save as groupSHO Showsi SingaporeSIDSIP Standard Inspection ProcedureSLI Supply Line Implementation processSLM Supply Line ManagementSLP Supply Line Preparation processSO Solution OfferingSOP Standard Operation ProcedureSOW statement of workSPC Statistical Process ControlSPPM Senior Product Program ManagerSPR Standard Product Requirement (Nokia)SQA Supplier Quality AssuranceSQC statistical quality controlSQE Supply Quality EngineerSQM Supply Quality Managerss sample sizeSTA Short Term AvailabilitySVP Senior Vice PresidentSW Softwaresy SydneyTCRM Technology Competence RoadmapTEC Technology Platformto TokyoTP Technology PlatformTPETPR Technical Product RequirementTPUtre TampereU Update, all updated documents that are not final U/I Voltage / CurrentU/I Voltage / CurrentUCL Upper Control LimitUG Use groupUI User Interfaceul Ulmvc Vancouver¨VCO IC manufacturing (discrete transistors, other ICs) VCTCXO Crystal wafer and IC (LSI-VCTCXO) manufacturing VIS VisibleVPQCT Volume Production Quality Control TestVQD Visual Quality EngineerVQE Visual Quality EngineerVQR Visual Quality RequirementsWBS Work Breakdown Structure。

商务英语阅读习题及答案一.doc

商务英语阅读习题及答案⼀.docII) Match each one on the left with its correct meaning on the right1. motivation2. pursue3. mark up4. procurement5. intangible6. cargoroyalty商务英语阅读习题(⼀)I) Comprehension1. What is international trade?2. What are the major motivations for private firm to operate international business?3. What measures do most companies usually adopt to avoid wild swings in the sales and profits?4. Pleas give the four major modes chosen by most companies when entering into international trade.5. Could you find any difference between Direct Investment and Portfolio Investment? If you can, please tell the main reasons.6. What is MNE? What are its synonyms?7. What limits a firm's sales?A. tomake continual efforts to gain sth. B. the action of obtaining, esp. by efforts of carefulattention. C. which by is its nature can not be known by senses, not clear and certain, not real. D. the goods (freight) carried by a ship, plane or vehicle.E. the amount by which a price is raised.F. profit, interest-G. the net value of assets or interest, invest.8. equity 股本,资产净值 H. not needing other things or people, taking decisions alone.9. yield I. a share of the profits.10. independent J. need or purpose.2. A3.E4.B5. C6.D7.18.G9.F 10.HHI) Fill in the blanks with the words or expressions given below and if necessary, put the word in the right form.A. orientationB. diversifyC. seek outD. differentiate...fromE. take advantage ofF. undergoG. bring aboutH. correspond L abandon J. amount to K. Come after L. approach1. That factory is trying to B its products to sell in different markets.2. A successful businessman is always skilled in E every possible opportunity.3. Reforming and opening to the world has G great changes in our lives.4. Can you D this kind of operating the others?5. Private firm going in for international business have a profit A6. He I his company and family and went away with all the money.7. The L of winter brings cold weather.8. The manager's words J a refusal to the proposal./doc/045460db492fb4daa58da0116c175f0e7dd11956.html pany is always C the best way to gain more while cost less.10.The city has F many changes during the last ten years.11.Direct investment usually K a firm has experience in exporting or importing.12.There goods don't H to the list of these I ordered.IV)Translate the following terms and phrases into Chinese;1.purchasing power lO.recovery2.sales potentials 11, recession3.mark-up 13. portfolio investment4.domestic markets 12. tangible goods5.finished goods 13. visible exports and imports6.profit margin 14. revenue and expenditure7.market share 15- excess capacity8.trade discrimination9.business cycles 16. licencing agreementsV)Translate the following sentences into Chinese;If the exporting market price exceeds the one at the importing country, a dumping margin exists on that particular sale. Then Under Article VI of GATT( General Agreement on Tariffs and Trade) 1994, and the Anti-Dumping Agreement, WTO Members can impose anti-dumping measures, if, after investigation in accordance with the Agreement, a determination is made (a) that dumping is occurring, (b) that the domestic industry producing the like product in the importing country is suffering material injury, and (c) that there is a causal link between the two. Typically anti-dumping action means charging extra import duty on the particular product from the particular exporting country in order to bring its price closer to the “normal value" or to remove the injury to domestic industry in the importing country.VI)Translate the following sentences into English;1.国际贸易有助于所有的国家促进经济的发展。

BEC高级商务英语必背词汇1

BEC高级商务英语必背词汇1 BEC高级商务英语必背词汇(1)p.a.(=per annum) n. 每年packaging n. 包装物;包装parent pany n. 母公司,总公司part-time adj. 部分时间工作的,业余的participate v. 参加,分享 (in)partnership n. 合伙(关系),合伙,合伙企业patent n. 专利pay n. 工资,酬金 v. 付钱,付报酬take-home pay 实得工资payroll n. 雇员名单,工资表peak n. 峰值,顶点penetrate v. 渗透,打入(市场)penetration n. 目标市场的占有份额pension n. 养老金,退休金perform v. 表现,执行performance n. 进行,表现工作情况performance appraisal n. 工作情况评估perk n. 额外待遇(交通、保健、保险等) personnel n. 员工,人员petty cash n. 零用现金phase out n. 分阶段停止使用pick v. 提取生产用零部件或给顾客发货picking list n. 用于择取生产或运输订货的表格pie chart n. 饼形图pilot n. 小规模试验pipeline n. 管道,渠道plant capacity n. 生产规模,生产能力plot v. 标绘,策划plough back n. 将获利进行再投资point of sale (POS) n. 销售点policy n. 政策,规定, 保险单portfolio n. (投资)组合portfolio management n. 组合证券管理post n. 邮件,邮局;职位position n. 职位potential n. 潜在力,潜势power n. 能力purchasing power 购买力PR=Public Relations 公共关系preference shares n. 优先股price n. 价格market price 市场价,市价retail price 零售价BEC高级商务英语必背词汇(2)probation n. 试用期product n. 产品production cycle n. 生产周期production schedule n. 生产计划product life cycle n. 产品生命周期product mix n. 产品组合(种类和数量的组合) productive adj. 生产的,多产的profile n. 简介形象特征profit n. 利润operating profit n. 营业利润profit and loss account n. 损益帐户project v. 预测promote v . 推销promotion n. 提升,升级proposal n. 建议,计划prospect n. 预期,展望prospectus n. 计划书,说明书prosperity n. 繁荣,兴隆prototype n. 原型,样品publicity n. 引起公众注意public adj. 公众的,公开的go public 上市public sector 公有企业publicity n. 公开场合,名声,宣传publics n. 公众,(有共同兴趣的)一群人或社会人士punctual adj. 准时的punctuality n. 准时purchase v. &n. 购买purchaser n. 买主,采购人)QC(=Quality Circle) n. 质检人员qualify v. 有资格,胜任qualified adj. 有资格的,胜任的,合格的qualification n. 资格,资格证明quality n. 质量quality assurance n. 质量保证quality control 质量控制,质量管理quarterly adj./adv. 季度的,按季度BEC高级商务英语必背词汇(3)reimburse v. 偿还,报销 reject n./v. 拒绝reliability n. 可靠性relief n. 减轻,解除,救济relocate v. 调动,重新安置remuneration n. 酬报,酬金rent v. 租 n. 租金rep (代表)的缩写report to v. 低于(某人),隶属,从属reposition v. (为商品)重新定位represent v. 代表,代理representative n. 代理人,代表tactic n. 战术,兵法tailor v. 特制产品tailor made products 特制产品take on 雇用takeover n. 接管target n. 目标v. 把……作为目标tariff n. 关税;价目表task n. 任务,工作task force n. 突击队,攻关小队(为完成某项任务而在一起的一组人)tax n. 税,税金capital gains tax n. 资本收益税corporation tax n. 公司税,法人税ine tax n. 所得税value added tax 增值税tax allowance 免减税tax avoidance 避税taxable 可征税的taxation 征税tax-deductible 在计算所得税时予以扣除的telesales n. 电话销售,电话售货temporary adj. 暂时的temporary post 临时职位tender n./v. 投标territory n. (销售)区域tie n. 关系,联系throughput n. 工厂的总产量TQC(=Total Quality Control) n. 全面质量管理track record n. 追踪记录,业绩trade n./v. 商业,生意;交易,经商balance of trade 贸易平衡trading profit 贸易利润insider trading 内部交易trade mark 商标trade union 工会trainee n. 受培训者transaction n. 交易,业务transfer n./v. 传输,转让transformation n. 加工BEC高级商务英语必背词汇(4)transparency n. (投影用)透明胶片treasurer n. 司库,掌管财务的人treasury n. 国库,财政部trend n. 趋势,时尚trouble-shooting n. 解决问题turnover n. 营业额,员工流动的比率staff turnover 人员换手率stock turnover 股票换手率undertake v. 从事、同意做某事undifferentiated marketing n. 无差异性营销策略uneconomical adj. 不经济的,浪费unemployment n. 失业unemployment benefit n. 失业津贴unit n. 单位unit cost n. 单位成本update v. 使现代化up to date adj./adv. 流行的,现行的,时髦的upgrade v. 升级,增加upturn n. 使向上,使朝上USP 唯一的销售计划reputation n. 名声,声望reputable adj. 名声/名誉好的reserves n. 储量金,准备金resign v. 放弃,辞去resignation n. 辞职resistance n. 阻力,抵触情绪respond v. 回答,答复response n. 回答,答复restore v. 恢复result/results n. 结果,效果retail n./v. 零售retailer n. 零售商retained earnings n. 留存收益retire v. 退休retirement n. 退休return n. 投资报酬return on investment (ROI) n. 投资收入,投资报酬revenue n. 岁入,税收review v./n. 检查reward n./v. 报答,报酬,奖赏rework v. (因劣质而)重作risk capital n. 风险资本rival n. 竞争者,对手adj. 竞争的rocket v. 急速上升,直线上升,飞升ROI Return on Investment 投资利润roughly adv. 粗略地round adj. 整数表示的,大约round trip 往返的行程royalty n. 特许权,专利权税run v. 管理,经营running adj. 运转的questionnaire n. 调查表,问卷quote n. 报价,股票牌价quotation n. 报价,股票牌价RR&D Research and Development 研究与开发radically adv. 根本地,彻底地raise n. (美)增加薪金v. 增加,提高;提出,引起range n. 系列产品rank n./v. 排名rapport n. 密切的关系,轻松愉快的气氛rate n. 比率,费用采集者退散fixed rate 固定费用,固定汇率going rate 现行利率,现行汇率rating 评定结果ratio n. 比率rationalise v. 使更有效,使更合理raw adj. 原料状态的,未加工的raw material n. 原材料receive v. 得到receipt n. 收据receiver n. 接管人,清算人accounts receivable 应收帐receivership n. 破产管理recession n. 萧条reckon v. 估算,认为recognise v. 承认reconcile v. 使……相吻合,核对,调和recoup v. 扣除,赔偿recover v. 重新获得,恢复recovery n. 重获,恢复recruit v. 招聘,征募 n. 新招收的人员recruitment n. 新成员的吸收red n. 红色in the red 赤字,负债reduce v. 减少reduction n. 减少redundant adj. 过多的,被解雇的redundancy n. 裁员,解雇reference n. 参考,参考资料reference number (Ref. No.) 产品的参考号码refund n./v. 归还,偿还region n. 地区。