金融风险管理主编朱淑珍大学出社课后习题解答

金融风险管理(22金融升本)学习通课后章节答案期末考试题库2023年

金融风险管理(22金融升本)学习通课后章节答案期末考试题库2023年

1.结构风险的特征主要有()

参考答案:

是一种结果风险###伴随其他风险产生###不可避免性

2.存贷比例等于存款总额比贷款总额,比值越大,流动性越强,流动性风险越

小

参考答案:

错

3.关于资本金结构风险,以下说法正确的是()

参考答案:

保持较多的主动型负债,资本金结构风险小###定期存款和长期借款权重过高,资本金结构风险大###是由于金融机构资产、负债结构搭配不合理而引发的风险

4.()是指投资期限短,信誉好,变现能力强的资产。

参考答案:

流动性资产

5.结构风险的产生既有机构内部资产负债结构调整的因素,又有外部经济环境

的影响。

参考答案:

对

6.()认为保持金融机构资金流动性的最好办法是购买那些可以及时变现的资

产

参考答案:

资产转移理论

7.结构风险的动态度量法有()

参考答案:

流动性缺口度量法###现金流量分析法###净流动性资产度量法

8.关于预期收入理论,以下说法正确的是()

参考答案:

增强商业银行的地位###认为贷款的清偿依赖于借款者未来收入###促进贷款形式多样化

9.结构风险包括流动性风险

参考答案:

对

10.早期的结构风险管理侧重于对负债流动性的管理

参考答案:

错

11.资产质量好,资产结构合理,则资本金结构风险小

参考答案:

对。

风险管理与金融机构课后习题答案

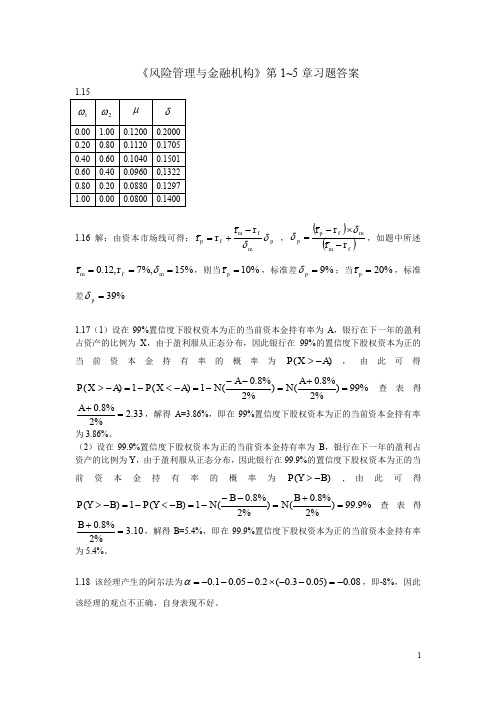

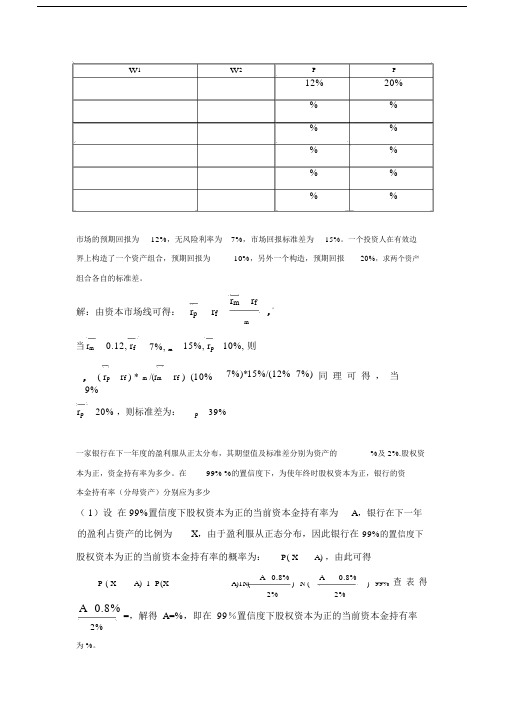

《风险管理与金融机构》第1~5章习题答案1.16 解:由资本市场线可得:p m fm f p r r r r δδ-+= ,()()f m m f p p r r r r -⨯-=δδ,如题中所述%15%,7,12.0===m f m r r δ,则当%10=p r ,标准差%9=p δ;当%20=p r ,标准差%39=p δ1.17(1)设在99%置信度下股权资本为正的当前资本金持有率为A ,银行在下一年的盈利占资产的比例为X ,由于盈利服从正态分布,因此银行在99%的置信度下股权资本为正的当前资本金持有率的概率为)(A X P ->,由此可得%99)%2%8.0()%2%8.0(1)(1)(=+=---=-<-=->A N A N A X P A X P 查表得33.2%2%8.0=+A ,解得A=3.86%,即在99%置信度下股权资本为正的当前资本金持有率为3.86%。

(2)设在99.9%置信度下股权资本为正的当前资本金持有率为B ,银行在下一年的盈利占资产的比例为Y ,由于盈利服从正态分布,因此银行在99.9%的置信度下股权资本为正的当前资本金持有率的概率为)(B Y P ->,由此可得%9.99)%2%8.0()%2%8.0(1)(1)(=+=---=-<-=->B N B N B Y P B Y P 查表得10.3%2%8.0=+B ,解得B=5.4%,即在99.9%置信度下股权资本为正的当前资本金持有率为5.4%。

1.18 该经理产生的阿尔法为08.0)05.03.0(2.005.01.0-=--⨯---=α,即-8%,因此该经理的观点不正确,自身表现不好。

2.15收入服从正太分布,假定符合要求的最低资本金要求为X ,则有)99.0(Φ=-σμx ,既有01.326.0=-X ,解得X=6.62,因此在5%的资本充足率水平下,还要再增加1.62万美元的股权资本,才能保证在99.9%的把握下,银行的资本金不会被完全消除。

《金融风险管理》复习习题全集包含答案

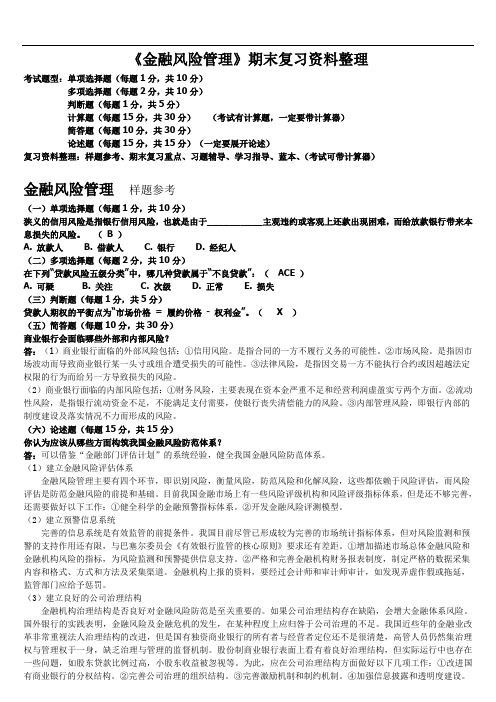

《金融风险管理》期末复习资料整理考试题型:单项选择题(每题1分,共10分)多项选择题(每题2分,共10分)判断题(每题1分,共5分)计算题(每题15分,共30分)(考试有计算题,一定要带计算器)简答题(每题10分,共30分)论述题(每题15分,共15分)(一定要展开论述)复习资料整理:样题参考、期末复习重点、习题辅导、学习指导、蓝本、(考试可带计算器)金融风险管理样题参考(一)单项选择题(每题1分,共10分)狭义的信用风险是指银行信用风险,也就是由于__________主观违约或客观上还款出现困难,而给放款银行带来本息损失的风险。

( B )A. 放款人B. 借款人C. 银行D. 经纪人(二)多项选择题(每题2分,共10分)在下列“贷款风险五级分类”中,哪几种贷款属于“不良贷款”:(ACE )A. 可疑B. 关注C. 次级D. 正常E. 损失(三)判断题(每题1分,共5分)贷款人期权的平衡点为“市场价格= 履约价格- 权利金”。

(X )(五)简答题(每题10分,共30分)商业银行会面临哪些外部和内部风险?答:(1)商业银行面临的外部风险包括:①信用风险。

是指合同的一方不履行义务的可能性。

②市场风险。

是指因市场波动而导致商业银行某一头寸或组合遭受损失的可能性。

③法律风险,是指因交易一方不能执行合约或因超越法定权限的行为而给另一方导致损失的风险。

(2)商业银行面临的内部风险包括:①财务风险,主要表现在资本金严重不足和经营利润虚盈实亏两个方面。

②流动性风险,是指银行流动资金不足,不能满足支付需要,使银行丧失清偿能力的风险。

③内部管理风险,即银行内部的制度建设及落实情况不力而形成的风险。

(六)论述题(每题15分,共15分)你认为应该从哪些方面构筑我国金融风险防范体系?答:可以借鉴“金融部门评估计划”的系统经验,健全我国金融风险防范体系。

(1)建立金融风险评估体系金融风险管理主要有四个环节,即识别风险,衡量风险,防范风险和化解风险,这些都依赖于风险评估,而风险评估是防范金融风险的前提和基础。

风险管理与金融机构第二版课后习题答案.doc

交易组合价值减少10500美元。

还有,当超过000美元的保证金帐户失去了补仓。发生这种情况时,小麦期货

价格上涨超过1000/5000=。还有,当小麦期货价格高于270美分补仓。的量,

1,500美元可以从保证金账户被撤销时,小麦的期货价格下降了1500/5000=。

停药后可发生时,期货价格下跌至220美分。

股票的当前市价为94美元,同时一个3个月期的、执行价格为95美元的欧式期权价格为美元,一个投资人认为股票价格会涨,但他并不知道是否应该买

A)1N(

) N (

) 99%

2%

2%

A0.8%=,解得A=%,即在99%置信度下股权资本为正的当前资本金持有率

2%

为%。

(2)设 在%置信度下股权资本为正的当前资本金持有率为B,银行在下一年的盈利占资产的比例为Y,由于盈利服从正态分布,因此银行在%的置信度下股权

资本为正的当前资本金持有率的概率为:P(YB),由此可得

P(YB) 1 P(Y

B

0.8%

B

0.8%

99.9%

查表得

B)1N(

)

N (

)

2%

2%

B 0.8%=,解得B=%即在%置信度下股权资本为正的当前资本金持有率为

%。

2%

一个资产组合经历主动地管理某资产组合,贝塔系数

.去年,无风险利率为

5%,回报-

30%。资产经理回报为-10%。资产经理市场条件下表现好。评价观点。

(2)当

X

95美元时,投资于期权的收益为:

( X

95)2000

9400美

元,投资于股票的收益为

( X

94)100美元 令

风险管理与金融机构第二版课后习题答案

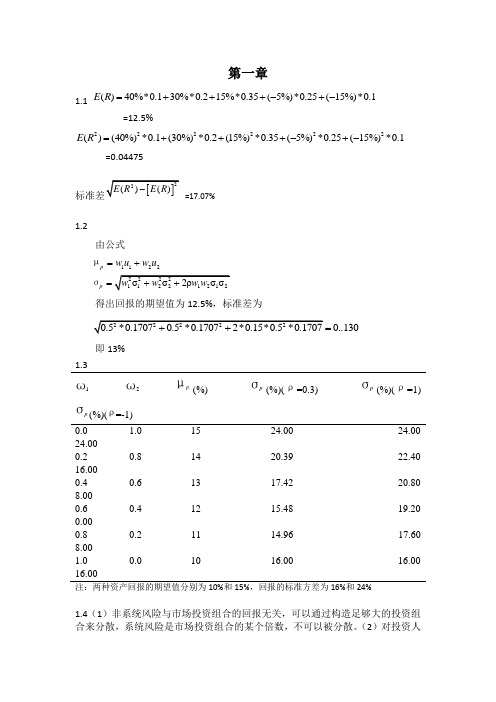

第一章1.1 ()40%*0.130%*0.215%*0.35(5%)*0.25(15%)*0.1E R =+++-+-=12.5%222222()(40%)*0.1(30%)*0.2(15%)*0.35(5%)*0.25(15%)*0.1E R =+++-+-=0.04475=17.07%1.2由公式1122p p w u w u =+=µσ得出回报的期望值为12.5%,标准差为0..130=即13%1.31ω 2ω p μ(%) p σ(%)(ρ=0.3) p σ(%)(ρ=1) pσ(%)(ρ=-1) 0.01.0 15 24.00 24.00 24.000.20.8 14 20.39 22.40 16.000.40.6 13 17.42 20.80 8.000.60.4 12 15.48 19.20 0.000.80.2 11 14.96 17.60 8.001.00.0 10 16.00 16.0016.00 注:两种资产回报的期望值分别为10%和15%,回报的标准方差为16%和24%1.4(1)非系统风险与市场投资组合的回报无关,可以通过构造足够大的投资组合来分散,系统风险是市场投资组合的某个倍数,不可以被分散。

(2)对投资人来说,系统风险更重要。

因为当持有一个大型而风险分散的投资组合时,系统风险并没有消失。

投资人应该为此风险索取补偿。

(3)这两个风险都有可能触发企业破产成本。

例如:2008年美国次贷危机引发的全球金融风暴(属于系统风险),导致全球不计其数的企业倒闭破产。

象安然倒闭这样的例子是由于安然内部管理导致的非系统风险。

1.5理论依据:大多数投资者都是风险厌恶者,他们希望在增加预期收益的同时也希望减少回报的标准差。

在有效边界的基础上引入无风险投资,从无风险投资F 向原有效边界引一条相切的直线,切点就是M ,所有投资者想要选择的相同的投资组合,此时新的有效边界是一条直线,预期回报与标准差之间是一种线性替代关系,选择M 后,投资者将风险资产与借入或借出的无风险资金进行不同比例的组合来体现他们的风险胃口。

02328《金融风险管理》参考答案

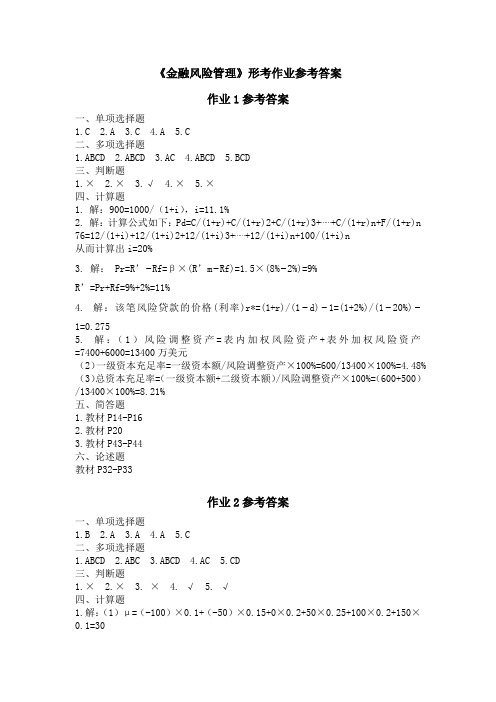

《金融风险管理》形考作业参考答案作业1参考答案一、单项选择题1.C2.A3.C4.A5.C二、多项选择题1.ABCD2.ABCD3.AC4.ABCD5.BCD三、判断题1.×2.×3.√4.×5.×四、计算题1.解:900=1000/(1+i),i=11.1%2.解:计算公式如下:Pd=C/(1+r)+C/(1+r)2+C/(1+r)3+⋯⋯+C/(1+r)n+F/(1+r)n 76=12/(1+i)+12/(1+i)2+12/(1+i)3+⋯⋯+12/(1+i)n+100/(1+i)n从而计算出i=20%3. 解:Pr=R’−Rf=β×(R’m−Rf)=1.5×(8%−2%)=9%R’=Pr+Rf=9%+2%=11%4. 解:该笔风险贷款的价格(利率)r*=(1+r)/(1−d)−1=(1+2%)/(1−20%)−1=0.2755. 解:(1)风险调整资产=表内加权风险资产+表外加权风险资产=7400+6000=13400万美元(2)一级资本充足率=一级资本额/风险调整资产×100%=600/13400×100%=4.48% (3)总资本充足率=(一级资本额+二级资本额)/风险调整资产×100%=(600+500)/13400×100%=8.21%五、简答题1.教材P14-P162.教材P203.教材P43-P44六、论述题教材P32-P33作业2参考答案一、单项选择题1.B2.A3.A4.A5.C二、多项选择题1.ABCD2.ABC3.ABCD4.AC5.CD三、判断题1.×2.×3. ×4. √5. √四、计算题1.解:(1)μ=(-100)×0.1+(-50)×0.15+0×0.2+50×0.25+100×0.2+150×0.1=30(2)σ2=0.1×(−100−30)2+0.15×(−50−30)2+0.2×(0−30)2+0.25×(50−30)2+0.3×(100−30)2+0.1×(150−30)2=53502. 解:(1)超额储备金=1000+20-4000×20%=220亿元(2)超额储备比例=220/4000×100%=5.5%(3)超额储备是商业银行在中央银行的存款和现金减去法定准备金,超额准备比例越高,银行流动性越强,但此指标局限性十分明显,它只是在一种狭窄的意义上体现金融机构的流动性状况,很容易导致低估流动性。

金融机构管理 课后习题答案

Chapter OneWhy Are Financial Intermediaries Special?Chapter OutlineIntroductionFinancial Intermediaries’ Specialness•Information Costs•Liquidity and Price Risk•Other Special ServicesOther Aspects of Specialness•The Transmission of Monetary Policy•Credit Allocation•Intergenerational Wealth Transfers or Time Intermediation •Payment Services•Denomination IntermediationSpecialness and Regulation•Safety and Soundness Regulation•Monetary Policy Regulation•Credit Allocation Regulation•Consumer Protection Regulation•Investor Protection Regulation•Entry RegulationThe Changing Dynamics of Specialness•Trends in the United States•Future Trends•Global IssuesSummarySolutions for End-of-Chapter Questions and Problems: Chapter One1. Identify and briefly explain the five risks common to financial institutions.Default or credit risk of assets, interest rate risk caused by maturity mismatches between assets and liabilities, liability withdrawal or liquidity risk, underwriting risk, and operating cost risks.2. Explain how economic transactions between household savers of funds and corporate users of funds would occur in a world without financial intermediaries (FIs).In a world without FIs the users of corporate funds in the economy would have to approach directly the household savers of funds in order to satisfy their borrowing needs. This process would be extremely costly because of the up-front information costs faced by potential lenders. Cost inefficiencies would arise with the identification of potential borrowers, the pooling of small savings into loans of sufficient size to finance corporate activities, and the assessment of risk and investment opportunities. Moreover, lenders would have to monitor the activities of borrowers over each loan's life span. The net result would be an imperfect allocation of resources in an economy.3. Identify and explain three economic disincentives that probably would dampen the flow offunds between household savers of funds and corporate users of funds in an economic world without financial intermediaries.Investors generally are averse to purchasing securities directly because of (a) monitoring costs, (b) liquidity costs, and (c) price risk. Monitoring the activities of borrowers requires extensive time, expense, and expertise. As a result, households would prefer to leave this activity to others, and by definition, the resulting lack of monitoring would increase the riskiness of investing in corporate debt and equity markets. The long-term nature of corporate equity and debt would likely eliminate at least a portion of those households willing to lend money, as the preference of many for near-cash liquidity would dominate the extra returns which may be available. Third, the price risk of transactions on the secondary markets would increase without the information flows and services generated by high volume.4. Identify and explain the two functions in which FIs may specialize that enable the smoothflow of funds from household savers to corporate users.FIs serve as conduits between users and savers of funds by providing a brokerage function and by engaging in the asset transformation function. The brokerage function can benefit both savers and users of funds and can vary according to the firm. FIs may provide only transaction services, such as discount brokerages, or they also may offer advisory services which help reduce information costs, such as full-line firms like Merrill Lynch. The asset transformation function is accomplished by issuing their own securities, such as deposits and insurance policies that are more attractive to household savers, and using the proceeds to purchase the primary securities ofcorporations. Thus, FIs take on the costs associated with the purchase of securities.5. In what sense are the financial claims of FIs considered secondary securities, while thefinancial claims of commercial corporations are considered primary securities? How does the transformation process, or intermediation, reduce the risk, or economic disincentives, to the savers?The funds raised by the financial claims issued by commercial corporations are used to invest in real assets. These financial claims, which are considered primary securities, are purchased by FIs whose financial claims therefore are considered secondary securities. Savers who invest in the financial claims of FIs are indirectly investing in the primary securities of commercial corporations. However, the information gathering and evaluation expenses, monitoring expenses, liquidity costs, and price risk of placing the investments directly with the commercial corporation are reduced because of the efficiencies of the FI.6. Explain how financial institutions act as delegated monitors. What secondary benefitsoften accrue to the entire financial system because of this monitoring process?By putting excess funds into financial institutions, individual investors give to the FIs the responsibility of deciding who should receive the money and of ensuring that the money is utilized properly by the borrower. In this sense the depositors have delegated the FI to act as a monitor on their behalf. The FI can collect information more efficiently than individual investors. Further, the FI can utilize this information to create new products, such as commercial loans, that continually update the information pool. This more frequent monitoring process sends important informational signals to other participants in the market, a process that reduces information imperfection and asymmetry between the ultimate sources and users of funds in the economy.7. What are five general areas of FI specialness that are caused by providing various servicesto sectors of the economy?First, FIs collect and process information more efficiently than individual savers. Second, FIs provide secondary claims to household savers which often have better liquidity characteristics than primary securities such as equities and bonds. Third, by diversifying the asset base FIs provide secondary securities with lower price-risk conditions than primary securities. Fourth, FIs provide economies of scale in transaction costs because assets are purchased in larger amounts. Finally, FIs provide maturity intermediation to the economy which allows the introduction of additional types of investment contracts, such as mortgage loans, that are financed with short-term deposits.8. How do FIs solve the information and related agency costs when household savers investdirectly in securities issued by corporations? What are agency costs?Agency costs occur when owners or managers take actions that are not in the best interests of the equity investor or lender. These costs typically result from the failure to adequately monitor theactivities of the borrower. If no other lender performs these tasks, the lender is subject to agency costs as the firm may not satisfy the covenants in the lending agreement. Because the FI invests the funds of many small savers, the FI has a greater incentive to collect information and monitor the activities of the borrower.9. What often is the benefit to the lenders, borrowers, and financial markets in general of thesolution to the information problem provided by the large financial institutions?One benefit to the solution process is the development of new secondary securities that allow even further improvements in the monitoring process. An example is the bank loan that is renewed more quickly than long-term debt. The renewal process updates the financial and operating information of the firm more frequently, thereby reducing the need for restrictive bond covenants that may be difficult and costly to implement.10. How do FIs alleviate the problem of liquidity risk faced by investors who wish to invest inthe securities of corporations?Liquidity risk occurs when savers are not able to sell their securities on demand. Commercial banks, for example, offer deposits that can be withdrawn at any time. Yet the banks make long-term loans or invest in illiquid assets because they are able to diversify their portfolios and better monitor the performance of firms that have borrowed or issued securities. Thus individual investors are able to realize the benefits of investing in primary assets without accepting the liquidity risk of direct investment.11. How do financial institutions help individual savers diversify their portfolio risks? Whichtype of financial institution is best able to achieve this goal?Money placed in any financial institution will result in a claim on a more diversified portfolio. Banks lend money to many different types of corporate, consumer, and government customers, and insurance companies have investments in many different types of assets. Investment in a mutual fund may generate the greatest diversification benefit because of the fund’s investment in a wide array of stocks and fixed income securities.12. How can financial institutions invest in high-risk assets with funding provided by low-riskliabilities from savers?Diversification of risk occurs with investments in assets that are not perfectly positively correlated. One result of extensive diversification is that the average risk of the asset base of an FI will be less than the average risk of the individual assets in which it has invested. Thus individual investors realize some of the returns of high-risk assets without accepting the corresponding risk characteristics.13. How can individual savers use financial institutions to reduce the transaction costs ofinvesting in financial assets?By pooling the assets of many small investors, FIs can gain economies of scale in transaction costs. This benefit occurs whether the FI is lending to a corporate or retail customer, or purchasing assets in the money and capital markets. In either case, operating activities that are designed to deal in large volumes typically are more efficient than those activities designed for small volumes.14. What is maturity intermediation? What are some of the ways in which the risks ofmaturity intermediation are managed by financial intermediaries?If net borrowers and net lenders have different optimal time horizons, FIs can service both sectors by matching their asset and liability maturities through on- and off-balance sheet hedging activities and flexible access to the financial markets. For example, the FI can offer the relatively short-term liabilities desired by households and also satisfy the demand for long-term loans such as home mortgages. By investing in a portfolio of long-and short-term assets that have variable- and fixed-rate components, the FI can reduce maturity risk exposure by utilizing liabilities that have similar variable- and fixed-rate characteristics, or by using futures, options, swaps, and other derivative products.15. What are five areas of institution-specific FI specialness, and which types of institutions aremost likely to be the service providers?First, commercial banks and other depository institutions are key players for the transmission of monetary policy from the central bank to the rest of the economy. Second, specific FIs often are identified as the major source of finance for certain sectors of the economy. For example, S&Ls and savings banks traditionally serve the credit needs of the residential real estate market. Third, life insurance and pension funds commonly are encouraged to provide mechanisms to transfer wealth across generations. Fourth, depository institutions efficiently provide payment services to benefit the economy. Finally, mutual funds provide denomination intermediation by allowing small investors to purchase pieces of assets with large minimum sizes such as negotiable CDs and commercial paper issues.16. How do depository institutions such as commercial banks assist in the implementation andtransmission of monetary policy?The Federal Reserve Board can involve directly the commercial banks in the implementation of monetary policy through changes in the reserve requirements and the discount rate. The open market sale and purchase of Treasury securities by the Fed involves the banks in the implementation of monetary policy in a less direct manner.17. What is meant by credit allocation regulation? What social benefit is this type ofregulation intended to provide?Credit allocation regulation refers to the requirement faced by FIs to lend to certain sectors of the economy, which are considered to be socially important. These may include housing and farming. Presumably the provision of credit to make houses more affordable or farms moreviable leads to a more stable and productive society.18. Which intermediaries best fulfill the intergenerational wealth transfer function? What isthis wealth transfer process?Life insurance and pension funds often receive special taxation relief and other subsidies to assist in the transfer of wealth from one generation to another. In effect, the wealth transfer process allows the accumulation of wealth by one generation to be transferred directly to one or more younger generations by establishing life insurance policies and trust provisions in pension plans. Often this wealth transfer process avoids the full marginal tax treatment that a direct payment would incur.19. What are two of the most important payment services provided by financial institutions?To what extent do these services efficiently provide benefits to the economy?The two most important payment services are check clearing and wire transfer services. Any breakdown in these systems would produce gridlock in the payment system with resulting harmful effects to the economy at both the domestic and potentially the international level.20. What is denomination intermediation? How do FIs assist in this process?Denomination intermediation is the process whereby small investors are able to purchase pieces of assets that normally are sold only in large denominations. Individual savers often invest small amounts in mutual funds. The mutual funds pool these small amounts and purchase negotiable CDs which can only be sold in minimum increments of $100,000, but which often are sold in million dollar packages. Similarly, commercial paper often is sold only in minimum amounts of $250,000. Therefore small investors can benefit in the returns and low risk which these assets typically offer.21. What is negative externality? In what ways do the existence of negative externalities justifythe extra regulatory attention received by financial institutions?A negative externality refers to the action by one party that has an adverse affect on some third party who is not part of the original transaction. For example, in an industrial setting, smoke from a factory that lowers surrounding property values may be viewed as a negative externality. For financial institutions, one concern is the contagion effect that can arise when the failure of one FI can cast doubt on the solvency of other institutions in that industry.22. If financial markets operated perfectly and costlessly, would there be a need forfinancial intermediaries?To a certain extent, financial intermediation exists because of financial market imperfections. If information is available costlessly to all participants, savers would not need intermediaries to act as either their brokers or their delegated monitors. However, if there are social benefits tointermediation, such as the transmission of monetary policy or credit allocation, then FIs would exist even in the absence of financial market imperfections.23. What is mortgage redlining?Mortgage redlining occurs when a lender specifically defines a geographic area in which it refuses to make any loans. The term arose because of the area often was outlined on a map with a red pencil.24. Why are FIs among the most regulated sectors in the world? When is netregulatory burden positive?FIs are required to enhance the efficient operation of the economy. Successful financial intermediaries provide sources of financing that fund economic growth opportunity that ultimately raises the overall level of economic activity. Moreover, successful financial intermediaries provide transaction services to the economy that facilitate trade and wealth accumulation.Conversely, distressed FIs create negative externalities for the entire economy. That is, the adverse impact of an FI failure is greater than just the loss to shareholders and other private claimants on the FI's assets. For example, the local market suffers if an FI fails and other FIs also may be thrown into financial distress by a contagion effect. Therefore, since some of the costs of the failure of an FI are generally borne by society at large, the government intervenes in the management of these institutions to protect society's interests. This intervention takes the form of regulation.However, the need for regulation to minimize social costs may impose private costs to the firms that would not exist without regulation. This additional private cost is defined as a net regulatory burden. Examples include the cost of holding excess capital and/or excess reserves and the extra costs of providing information. Although they may be socially beneficial, these costs add to private operating costs. To the extent that these additional costs help to avoid negative externalities and to ensure the smooth and efficient operation of the economy, the net regulatory burden is positive.25. What forms of protection and regulation do regulators of FIs impose to ensuretheir safety and soundness?Regulators have issued several guidelines to insure the safety and soundness of FIs:a. FIs are required to diversify their assets. For example, banks cannot lend morethan 10 percent of their equity to a single borrower.b. FIs are required to maintain minimum amounts of capital to cushion anyunexpected losses. In the case of banks, the Basle standards require a minimum core and supplementary capital of 8 percent of their risk-adjusted assets.c. Regulators have set up guaranty funds such as BIF for commercial banks, SIPCfor securities firms, and state guaranty funds for insurance firms to protectindividual investors.d. Regulators also engage in periodic monitoring and surveillance, such as on-siteexaminations, and request periodic information from the FIs.26. In the transmission of monetary policy, what is the difference between insidemoney and outside money? How does the Federal Reserve Board try to control the amount of inside money? How can this regulatory position create a cost for the depository financial institutions?Outside money is that part of the money supply directly produced and controlled by the Fed, for example, coins and currency. Inside money refers to bank deposits not directly controlled by the Fed. The Fed can influence this amount of money by reserve requirement and discount rate policies. In cases where the level of required reserves exceeds the level considered optimal by the FI, the inability to use the excess reserves to generate revenue may be considered a tax or cost of providing intermediation.27. What are some examples of credit allocation regulation? How can this attemptto create social benefits create costs to the private institution?The qualified thrift lender test (QTL) requires thrifts to hold 65 percent of their assets in residential mortgage-related assets to retain the thrift charter. Some states have enacted usury laws that place maximum restrictions on the interest rates that can be charged on mortgages and/or consumer loans. These types of restrictions often create additional operating costs to the FI and almost certainly reduce the amount of profit that could be realized without such regulation.28. What is the purpose of the Home Mortgage Disclosure Act? What are thesocial benefits desired from the legislation? How does the implementation of this legislation create a net regulatory burden on financial institutions?The HMDA was passed by Congress to prevent discrimination in mortgage lending. The social benefit is to ensure that everyone who qualifies financially is provided the opportunity to purchase a house should they so desire. The regulatory burden has been to require a written statement indicating the reasons why credit was or was not granted. Since 1990, the federal regulators have examined millions of mortgage transactions from more than 7,700 institutions each calendar quarter.29. What legislation has been passed specifically to protect investors who use investment banksdirectly or indirectly to purchase securities? Give some examples of the types of abuses for which protection is provided.The Securities Acts of 1933 and 1934 and the Investment Company Act of 1940 were passed byCongress to protect investors against possible abuses such as insider trading, lack of disclosure, outright malfeasance, and breach of fiduciary responsibilities.30. How do regulations regarding barriers to entry and the scope of permitted activities affectthe charter value of financial institutions?The profitability of existing firms will be increased as the direct and indirect costs of establishing competition increase. Direct costs include the actual physical and financial costs of establishing a business. In the case of FIs, the financial costs include raising the necessary minimum capital to receive a charter. Indirect costs include permission from regulatory authorities to receive a charter. Again in the case of FIs this cost involves acceptable leadership to the regulators. As these barriers to entry are stronger, the charter value for existing firms will be higher.31. What reasons have been given for the growth of investment companies at the expense of“traditional” banks and insurance companies?The recent growth of investment companies can be attributed to two major factors: a. Investors have demanded increased access to direct securities markets.Investment companies and pension funds allow investors to take positions indirect securities markets while still obtaining the risk diversification, monitoring, and transactional efficiency benefits of financial intermediation. Some experts would argue that this growth is the result of increased sophistication on the part of investors; others would argue that the ability to use these markets has caused the increased investor awareness. The growth in these assets is inarguable.b. Recent episodes of financial distress in both the banking and insuranceindustries have led to an increase in regulation and governmental oversight,thereby increasing the net regulatory burden of “traditional” companies. Assuch, the costs of intermediation have increased, which increases the cost ofproviding services to customers.32. What are some of the methods which banking organizations have employed to reduce thenet regulatory burden? What has been the effect on profitability?Through regulatory changes, FIs have begun changing the mix of business products offered to individual users and providers of funds. For example, banks have acquired mutual funds, have expanded their asset and pension fund management businesses, and have increased the security underwriting activities. In addition, legislation that allows banks to establish branches anywhere in the United States has caused a wave of mergers. As the size of banks has grown, an expansion of possible product offerings has created the potential for lower service costs. Finally, the emphasis in recent years has been on products that generate increases in fee income, and the entire banking industry has benefited from increased profitability in recent years.33. What characteristics of financial products are necessary for financial markets to becomeefficient alternatives to financial intermediaries? Can you give some examples of the commoditization of products which were previously the sole property of financial institutions?Financial markets can replace FIs in the delivery of products that (1) have standardized terms, (2) serve a large number of customers, and (3) are sufficiently understood for investors to be comfortable in assessing their prices. When these three characteristics are met, the products often can be treated as commodities. One example of this process is the migration of over-the-counter options to the publicly traded option markets as trading volume grows and trading terms become standardized.34. In what way has Regulation 144A of the Securities and Exchange Commission provided anincentive to the process of financial disintermediation?Changing technology and a reduction in information costs are rapidly changing the nature of financial transactions, enabling savers to access issuers of securities directly. Section 144A of the SEC is a recent regulatory change that will facilitate the process of disintermediation. The private placement of bonds and equities directly by the issuing firm is an example of a product that historically has been the domain of investment bankers. Although historically private placement assets had restrictions against trading, regulators have given permission for these assets to trade among large investors who have assets of more than $100 million. As the market grows, this minimum asset size restriction may be reduced.Chapter TwoThe Financial Services Industry: Depository InstitutionsChapter OutlineIntroductionCommercial Banks•Size, Structure, and Composition of the Industry•Balance Sheet and Recent Trends•Other Fee-Generating Activities•Regulation•Industry PerformanceSavings Institutions•Savings Associations (SAs)•Savings Banks•Recent Performance of Savings Associations and Savings BanksCredit Unions•Size, Structure, and Composition of the Industry and Recent Trends•Balance Sheets•Regulation•Industry PerformanceGlobal Issues: Japan, China, and GermanySummaryAppendix 2A: Financial Statement Analysis Using a Return on Equity (ROE) FrameworkAppendix 2B: Depository Institutions and Their RegulatorsAppendix 3B: Technology in Commercial BankingSolutions for End-of-Chapter Questions and Problems: Chapter Two1.What are the differences between community banks, regional banks, andmoney-center banks? Contrast the business activities, location, and markets of each of these bank groups.Community banks typically have assets under $1 billion and serve consumer and small business customers in local markets. In 2003, 94.5 percent of the banks in the United States were classified as community banks. However, these banks held only 14.6 percent of the assets of the banking industry. In comparison with regional and money-center banks, community banks typically hold a larger percentage of assets in consumer and real estate loans and a smaller percentage of assets in commercial and industrial loans. These banks also rely more heavily on local deposits and less heavily on borrowed and international funds.Regional banks range in size from several billion dollars to several hundred billion dollars in assets. The banks normally are headquartered in larger regional cities and often have offices and branches in locations throughout large portions of the United States. Although these banks provide lending products to large corporate customers, many of the regional banks have developed sophisticated electronic and branching services to consumer and residential customers. Regional banks utilize retail deposit bases for funding, but also develop relationships with large corporate customers and international money centers.Money center banks rely heavily on nondeposit or borrowed sources of funds. Some of these banks have no retail branch systems, and most regional banks are major participants in foreign currency markets. These banks compete with the larger regional banks for large commercial loans and with international banks for international commercial loans. Most money center banks have headquarters in New York City.e the data in Table 2-4 for the banks in the two asset size groups (a) $100million-$1 billion and (b) over $10 billion to answer the following questions.a. Why have the ratios for ROA and ROE tended to increase for both groupsover the 1990-2003 period? Identify and discuss the primary variables thataffect ROA and ROE as they relate to these two size groups.The primary reason for the improvements in ROA and ROE in the late 1990smay be related to the continued strength of the macroeconomy that allowedbanks to operate with a reduced regard for bad debts, or loan charge-offproblems. In addition, the continued low interest rate environment hasprovided relatively low-cost sources of funds, and a shift toward growth in fee income has provided additional sources of revenue in many product lines.。

金融机构管理 课后习题答案

Chapter OneWhy Are Financial Intermediaries Special?Chapter OutlineIntroductionFinancial Intermediaries’ Specialness•Information Costs•Liquidity and Price Risk•Other Special ServicesOther Aspects of Specialness•The Transmission of Monetary Policy•Credit Allocation•Intergenerational Wealth Transfers or Time Intermediation •Payment Services•Denomination IntermediationSpecialness and Regulation•Safety and Soundness Regulation•Monetary Policy Regulation•Credit Allocation Regulation•Consumer Protection Regulation•Investor Protection Regulation•Entry RegulationThe Changing Dynamics of Specialness•Trends in the United States•Future Trends•Global IssuesSummarySolutions for End-of-Chapter Questions and Problems: Chapter One1. Identify and briefly explain the five risks common to financial institutions.Default or credit risk of assets, interest rate risk caused by maturity mismatches between assets and liabilities, liability withdrawal or liquidity risk, underwriting risk, and operating cost risks.2. Explain how economic transactions between household savers of funds and corporate users of funds would occur in a world without financial intermediaries (FIs).In a world without FIs the users of corporate funds in the economy would have to approach directly the household savers of funds in order to satisfy their borrowing needs. This process would be extremely costly because of the up-front information costs faced by potential lenders. Cost inefficiencies would arise with the identification of potential borrowers, the pooling of small savings into loans of sufficient size to finance corporate activities, and the assessment of risk and investment opportunities. Moreover, lenders would have to monitor the activities of borrowers over each loan's life span. The net result would be an imperfect allocation of resources in an economy.3. Identify and explain three economic disincentives that probably would dampen the flow offunds between household savers of funds and corporate users of funds in an economic world without financial intermediaries.Investors generally are averse to purchasing securities directly because of (a) monitoring costs, (b) liquidity costs, and (c) price risk. Monitoring the activities of borrowers requires extensive time, expense, and expertise. As a result, households would prefer to leave this activity to others, and by definition, the resulting lack of monitoring would increase the riskiness of investing in corporate debt and equity markets. The long-term nature of corporate equity and debt would likely eliminate at least a portion of those households willing to lend money, as the preference of many for near-cash liquidity would dominate the extra returns which may be available. Third, the price risk of transactions on the secondary markets would increase without the information flows and services generated by high volume.4. Identify and explain the two functions in which FIs may specialize that enable the smoothflow of funds from household savers to corporate users.FIs serve as conduits between users and savers of funds by providing a brokerage function and by engaging in the asset transformation function. The brokerage function can benefit both savers and users of funds and can vary according to the firm. FIs may provide only transaction services, such as discount brokerages, or they also may offer advisory services which help reduce information costs, such as full-line firms like Merrill Lynch. The asset transformation function is accomplished by issuing their own securities, such as deposits and insurance policies that are more attractive to household savers, and using the proceeds to purchase the primary securities ofcorporations. Thus, FIs take on the costs associated with the purchase of securities.5. In what sense are the financial claims of FIs considered secondary securities, while thefinancial claims of commercial corporations are considered primary securities? How does the transformation process, or intermediation, reduce the risk, or economic disincentives, to the savers?The funds raised by the financial claims issued by commercial corporations are used to invest in real assets. These financial claims, which are considered primary securities, are purchased by FIs whose financial claims therefore are considered secondary securities. Savers who invest in the financial claims of FIs are indirectly investing in the primary securities of commercial corporations. However, the information gathering and evaluation expenses, monitoring expenses, liquidity costs, and price risk of placing the investments directly with the commercial corporation are reduced because of the efficiencies of the FI.6. Explain how financial institutions act as delegated monitors. What secondary benefitsoften accrue to the entire financial system because of this monitoring process?By putting excess funds into financial institutions, individual investors give to the FIs the responsibility of deciding who should receive the money and of ensuring that the money is utilized properly by the borrower. In this sense the depositors have delegated the FI to act as a monitor on their behalf. The FI can collect information more efficiently than individual investors. Further, the FI can utilize this information to create new products, such as commercial loans, that continually update the information pool. This more frequent monitoring process sends important informational signals to other participants in the market, a process that reduces information imperfection and asymmetry between the ultimate sources and users of funds in the economy.7. What are five general areas of FI specialness that are caused by providing various servicesto sectors of the economy?First, FIs collect and process information more efficiently than individual savers. Second, FIs provide secondary claims to household savers which often have better liquidity characteristics than primary securities such as equities and bonds. Third, by diversifying the asset base FIs provide secondary securities with lower price-risk conditions than primary securities. Fourth, FIs provide economies of scale in transaction costs because assets are purchased in larger amounts. Finally, FIs provide maturity intermediation to the economy which allows the introduction of additional types of investment contracts, such as mortgage loans, that are financed with short-term deposits.8. How do FIs solve the information and related agency costs when household savers investdirectly in securities issued by corporations? What are agency costs?Agency costs occur when owners or managers take actions that are not in the best interests of the equity investor or lender. These costs typically result from the failure to adequately monitor theactivities of the borrower. If no other lender performs these tasks, the lender is subject to agency costs as the firm may not satisfy the covenants in the lending agreement. Because the FI invests the funds of many small savers, the FI has a greater incentive to collect information and monitor the activities of the borrower.9. What often is the benefit to the lenders, borrowers, and financial markets in general of thesolution to the information problem provided by the large financial institutions?One benefit to the solution process is the development of new secondary securities that allow even further improvements in the monitoring process. An example is the bank loan that is renewed more quickly than long-term debt. The renewal process updates the financial and operating information of the firm more frequently, thereby reducing the need for restrictive bond covenants that may be difficult and costly to implement.10. How do FIs alleviate the problem of liquidity risk faced by investors who wish to invest inthe securities of corporations?Liquidity risk occurs when savers are not able to sell their securities on demand. Commercial banks, for example, offer deposits that can be withdrawn at any time. Yet the banks make long-term loans or invest in illiquid assets because they are able to diversify their portfolios and better monitor the performance of firms that have borrowed or issued securities. Thus individual investors are able to realize the benefits of investing in primary assets without accepting the liquidity risk of direct investment.11. How do financial institutions help individual savers diversify their portfolio risks? Whichtype of financial institution is best able to achieve this goal?Money placed in any financial institution will result in a claim on a more diversified portfolio. Banks lend money to many different types of corporate, consumer, and government customers, and insurance companies have investments in many different types of assets. Investment in a mutual fund may generate the greatest diversification benefit because of the fund’s investment in a wide array of stocks and fixed income securities.12. How can financial institutions invest in high-risk assets with funding provided by low-riskliabilities from savers?Diversification of risk occurs with investments in assets that are not perfectly positively correlated. One result of extensive diversification is that the average risk of the asset base of an FI will be less than the average risk of the individual assets in which it has invested. Thus individual investors realize some of the returns of high-risk assets without accepting the corresponding risk characteristics.13. How can individual savers use financial institutions to reduce the transaction costs ofinvesting in financial assets?By pooling the assets of many small investors, FIs can gain economies of scale in transaction costs. This benefit occurs whether the FI is lending to a corporate or retail customer, or purchasing assets in the money and capital markets. In either case, operating activities that are designed to deal in large volumes typically are more efficient than those activities designed for small volumes.14. What is maturity intermediation? What are some of the ways in which the risks ofmaturity intermediation are managed by financial intermediaries?If net borrowers and net lenders have different optimal time horizons, FIs can service both sectors by matching their asset and liability maturities through on- and off-balance sheet hedging activities and flexible access to the financial markets. For example, the FI can offer the relatively short-term liabilities desired by households and also satisfy the demand for long-term loans such as home mortgages. By investing in a portfolio of long-and short-term assets that have variable- and fixed-rate components, the FI can reduce maturity risk exposure by utilizing liabilities that have similar variable- and fixed-rate characteristics, or by using futures, options, swaps, and other derivative products.15. What are five areas of institution-specific FI specialness, and which types of institutions aremost likely to be the service providers?First, commercial banks and other depository institutions are key players for the transmission of monetary policy from the central bank to the rest of the economy. Second, specific FIs often are identified as the major source of finance for certain sectors of the economy. For example, S&Ls and savings banks traditionally serve the credit needs of the residential real estate market. Third, life insurance and pension funds commonly are encouraged to provide mechanisms to transfer wealth across generations. Fourth, depository institutions efficiently provide payment services to benefit the economy. Finally, mutual funds provide denomination intermediation by allowing small investors to purchase pieces of assets with large minimum sizes such as negotiable CDs and commercial paper issues.16. How do depository institutions such as commercial banks assist in the implementation andtransmission of monetary policy?The Federal Reserve Board can involve directly the commercial banks in the implementation of monetary policy through changes in the reserve requirements and the discount rate. The open market sale and purchase of Treasury securities by the Fed involves the banks in the implementation of monetary policy in a less direct manner.17. What is meant by credit allocation regulation? What social benefit is this type ofregulation intended to provide?Credit allocation regulation refers to the requirement faced by FIs to lend to certain sectors of the economy, which are considered to be socially important. These may include housing and farming. Presumably the provision of credit to make houses more affordable or farms moreviable leads to a more stable and productive society.18. Which intermediaries best fulfill the intergenerational wealth transfer function? What isthis wealth transfer process?Life insurance and pension funds often receive special taxation relief and other subsidies to assist in the transfer of wealth from one generation to another. In effect, the wealth transfer process allows the accumulation of wealth by one generation to be transferred directly to one or more younger generations by establishing life insurance policies and trust provisions in pension plans. Often this wealth transfer process avoids the full marginal tax treatment that a direct payment would incur.19. What are two of the most important payment services provided by financial institutions?To what extent do these services efficiently provide benefits to the economy?The two most important payment services are check clearing and wire transfer services. Any breakdown in these systems would produce gridlock in the payment system with resulting harmful effects to the economy at both the domestic and potentially the international level.20. What is denomination intermediation? How do FIs assist in this process?Denomination intermediation is the process whereby small investors are able to purchase pieces of assets that normally are sold only in large denominations. Individual savers often invest small amounts in mutual funds. The mutual funds pool these small amounts and purchase negotiable CDs which can only be sold in minimum increments of $100,000, but which often are sold in million dollar packages. Similarly, commercial paper often is sold only in minimum amounts of $250,000. Therefore small investors can benefit in the returns and low risk which these assets typically offer.21. What is negative externality? In what ways do the existence of negative externalities justifythe extra regulatory attention received by financial institutions?A negative externality refers to the action by one party that has an adverse affect on some third party who is not part of the original transaction. For example, in an industrial setting, smoke from a factory that lowers surrounding property values may be viewed as a negative externality. For financial institutions, one concern is the contagion effect that can arise when the failure of one FI can cast doubt on the solvency of other institutions in that industry.22. If financial markets operated perfectly and costlessly, would there be a need forfinancial intermediaries?To a certain extent, financial intermediation exists because of financial market imperfections. If information is available costlessly to all participants, savers would not need intermediaries to act as either their brokers or their delegated monitors. However, if there are social benefits tointermediation, such as the transmission of monetary policy or credit allocation, then FIs would exist even in the absence of financial market imperfections.23. What is mortgage redlining?Mortgage redlining occurs when a lender specifically defines a geographic area in which it refuses to make any loans. The term arose because of the area often was outlined on a map with a red pencil.24. Why are FIs among the most regulated sectors in the world? When is netregulatory burden positive?FIs are required to enhance the efficient operation of the economy. Successful financial intermediaries provide sources of financing that fund economic growth opportunity that ultimately raises the overall level of economic activity. Moreover, successful financial intermediaries provide transaction services to the economy that facilitate trade and wealth accumulation.Conversely, distressed FIs create negative externalities for the entire economy. That is, the adverse impact of an FI failure is greater than just the loss to shareholders and other private claimants on the FI's assets. For example, the local market suffers if an FI fails and other FIs also may be thrown into financial distress by a contagion effect. Therefore, since some of the costs of the failure of an FI are generally borne by society at large, the government intervenes in the management of these institutions to protect society's interests. This intervention takes the form of regulation.However, the need for regulation to minimize social costs may impose private costs to the firms that would not exist without regulation. This additional private cost is defined as a net regulatory burden. Examples include the cost of holding excess capital and/or excess reserves and the extra costs of providing information. Although they may be socially beneficial, these costs add to private operating costs. To the extent that these additional costs help to avoid negative externalities and to ensure the smooth and efficient operation of the economy, the net regulatory burden is positive.25. What forms of protection and regulation do regulators of FIs impose to ensuretheir safety and soundness?Regulators have issued several guidelines to insure the safety and soundness of FIs:a. FIs are required to diversify their assets. For example, banks cannot lend morethan 10 percent of their equity to a single borrower.b. FIs are required to maintain minimum amounts of capital to cushion anyunexpected losses. In the case of banks, the Basle standards require a minimum core and supplementary capital of 8 percent of their risk-adjusted assets.c. Regulators have set up guaranty funds such as BIF for commercial banks, SIPCfor securities firms, and state guaranty funds for insurance firms to protectindividual investors.d. Regulators also engage in periodic monitoring and surveillance, such as on-siteexaminations, and request periodic information from the FIs.26. In the transmission of monetary policy, what is the difference between insidemoney and outside money? How does the Federal Reserve Board try to control the amount of inside money? How can this regulatory position create a cost for the depository financial institutions?Outside money is that part of the money supply directly produced and controlled by the Fed, for example, coins and currency. Inside money refers to bank deposits not directly controlled by the Fed. The Fed can influence this amount of money by reserve requirement and discount rate policies. In cases where the level of required reserves exceeds the level considered optimal by the FI, the inability to use the excess reserves to generate revenue may be considered a tax or cost of providing intermediation.27. What are some examples of credit allocation regulation? How can this attemptto create social benefits create costs to the private institution?The qualified thrift lender test (QTL) requires thrifts to hold 65 percent of their assets in residential mortgage-related assets to retain the thrift charter. Some states have enacted usury laws that place maximum restrictions on the interest rates that can be charged on mortgages and/or consumer loans. These types of restrictions often create additional operating costs to the FI and almost certainly reduce the amount of profit that could be realized without such regulation.28. What is the purpose of the Home Mortgage Disclosure Act? What are thesocial benefits desired from the legislation? How does the implementation of this legislation create a net regulatory burden on financial institutions?The HMDA was passed by Congress to prevent discrimination in mortgage lending. The social benefit is to ensure that everyone who qualifies financially is provided the opportunity to purchase a house should they so desire. The regulatory burden has been to require a written statement indicating the reasons why credit was or was not granted. Since 1990, the federal regulators have examined millions of mortgage transactions from more than 7,700 institutions each calendar quarter.29. What legislation has been passed specifically to protect investors who use investment banksdirectly or indirectly to purchase securities? Give some examples of the types of abuses for which protection is provided.The Securities Acts of 1933 and 1934 and the Investment Company Act of 1940 were passed byCongress to protect investors against possible abuses such as insider trading, lack of disclosure, outright malfeasance, and breach of fiduciary responsibilities.30. How do regulations regarding barriers to entry and the scope of permitted activities affectthe charter value of financial institutions?The profitability of existing firms will be increased as the direct and indirect costs of establishing competition increase. Direct costs include the actual physical and financial costs of establishing a business. In the case of FIs, the financial costs include raising the necessary minimum capital to receive a charter. Indirect costs include permission from regulatory authorities to receive a charter. Again in the case of FIs this cost involves acceptable leadership to the regulators. As these barriers to entry are stronger, the charter value for existing firms will be higher.31. What reasons have been given for the growth of investment companies at the expense of“traditional” banks and insurance companies?The recent growth of investment companies can be attributed to two major factors: a. Investors have demanded increased access to direct securities markets.Investment companies and pension funds allow investors to take positions indirect securities markets while still obtaining the risk diversification, monitoring, and transactional efficiency benefits of financial intermediation. Some experts would argue that this growth is the result of increased sophistication on the part of investors; others would argue that the ability to use these markets has caused the increased investor awareness. The growth in these assets is inarguable.b. Recent episodes of financial distress in both the banking and insuranceindustries have led to an increase in regulation and governmental oversight,thereby increasing the net regulatory burden of “traditional” companies. Assuch, the costs of intermediation have increased, which increases the cost ofproviding services to customers.32. What are some of the methods which banking organizations have employed to reduce thenet regulatory burden? What has been the effect on profitability?Through regulatory changes, FIs have begun changing the mix of business products offered to individual users and providers of funds. For example, banks have acquired mutual funds, have expanded their asset and pension fund management businesses, and have increased the security underwriting activities. In addition, legislation that allows banks to establish branches anywhere in the United States has caused a wave of mergers. As the size of banks has grown, an expansion of possible product offerings has created the potential for lower service costs. Finally, the emphasis in recent years has been on products that generate increases in fee income, and the entire banking industry has benefited from increased profitability in recent years.33. What characteristics of financial products are necessary for financial markets to becomeefficient alternatives to financial intermediaries? Can you give some examples of the commoditization of products which were previously the sole property of financial institutions?Financial markets can replace FIs in the delivery of products that (1) have standardized terms, (2) serve a large number of customers, and (3) are sufficiently understood for investors to be comfortable in assessing their prices. When these three characteristics are met, the products often can be treated as commodities. One example of this process is the migration of over-the-counter options to the publicly traded option markets as trading volume grows and trading terms become standardized.34. In what way has Regulation 144A of the Securities and Exchange Commission provided anincentive to the process of financial disintermediation?Changing technology and a reduction in information costs are rapidly changing the nature of financial transactions, enabling savers to access issuers of securities directly. Section 144A of the SEC is a recent regulatory change that will facilitate the process of disintermediation. The private placement of bonds and equities directly by the issuing firm is an example of a product that historically has been the domain of investment bankers. Although historically private placement assets had restrictions against trading, regulators have given permission for these assets to trade among large investors who have assets of more than $100 million. As the market grows, this minimum asset size restriction may be reduced.Chapter TwoThe Financial Services Industry: Depository InstitutionsChapter OutlineIntroductionCommercial Banks•Size, Structure, and Composition of the Industry•Balance Sheet and Recent Trends•Other Fee-Generating Activities•Regulation•Industry PerformanceSavings Institutions•Savings Associations (SAs)•Savings Banks•Recent Performance of Savings Associations and Savings BanksCredit Unions•Size, Structure, and Composition of the Industry and Recent Trends•Balance Sheets•Regulation•Industry PerformanceGlobal Issues: Japan, China, and GermanySummaryAppendix 2A: Financial Statement Analysis Using a Return on Equity (ROE) FrameworkAppendix 2B: Depository Institutions and Their RegulatorsAppendix 3B: Technology in Commercial BankingSolutions for End-of-Chapter Questions and Problems: Chapter Two1.What are the differences between community banks, regional banks, andmoney-center banks? Contrast the business activities, location, and markets of each of these bank groups.Community banks typically have assets under $1 billion and serve consumer and small business customers in local markets. In 2003, 94.5 percent of the banks in the United States were classified as community banks. However, these banks held only 14.6 percent of the assets of the banking industry. In comparison with regional and money-center banks, community banks typically hold a larger percentage of assets in consumer and real estate loans and a smaller percentage of assets in commercial and industrial loans. These banks also rely more heavily on local deposits and less heavily on borrowed and international funds.Regional banks range in size from several billion dollars to several hundred billion dollars in assets. The banks normally are headquartered in larger regional cities and often have offices and branches in locations throughout large portions of the United States. Although these banks provide lending products to large corporate customers, many of the regional banks have developed sophisticated electronic and branching services to consumer and residential customers. Regional banks utilize retail deposit bases for funding, but also develop relationships with large corporate customers and international money centers.Money center banks rely heavily on nondeposit or borrowed sources of funds. Some of these banks have no retail branch systems, and most regional banks are major participants in foreign currency markets. These banks compete with the larger regional banks for large commercial loans and with international banks for international commercial loans. Most money center banks have headquarters in New York City.e the data in Table 2-4 for the banks in the two asset size groups (a) $100million-$1 billion and (b) over $10 billion to answer the following questions.a. Why have the ratios for ROA and ROE tended to increase for both groupsover the 1990-2003 period? Identify and discuss the primary variables thataffect ROA and ROE as they relate to these two size groups.The primary reason for the improvements in ROA and ROE in the late 1990smay be related to the continued strength of the macroeconomy that allowedbanks to operate with a reduced regard for bad debts, or loan charge-offproblems. In addition, the continued low interest rate environment hasprovided relatively low-cost sources of funds, and a shift toward growth in fee income has provided additional sources of revenue in many product lines.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

金融风险管理主编朱淑珍大学出社课后习题解答集团标准化工作小组 [Q8QX9QT-X8QQB8Q8-NQ8QJ8-M8QMN]第一章【习题答案】1.系统性金融风险2.逆向选择;道德风险3.正确。

心理学中的“乐队车效应”是指在游行中开在前面,载着乐队演奏音乐的汽车,由于音乐使人情绪激昂,就影响着人们跟着参加游行。

在股市中表现为,当经济繁荣推动股价上升时,幼稚的投资者开始拥向价格处于高位的股票,促使市场行情飙升。

4.错误。

不确定性是指经济主体对于未来的经济状况的分布范围和状态不能确知;而风险是一个二维概念,它表示了损失的大小和损失发生概率的大小。

5.A(本题目有错别字,内存,应改为内在)6.A7.略。

提示:金融风险的定义。

8.金融风险的一般特征:客观性:汇率的变动不以任何金融主体的主观意志为转移。

普遍性:每一个具体行业、每一种金融工具、每一个经营机构和每一次交易行为中,都有可能潜伏着金融风险、扩张性:美国次贷危机将整个世界拖入金融海啸、多样性与可变性:期货期权等金融衍生品不断创新,影响风险的因素变得多而复杂、可管理性:运用恰当手段可套期保值达到避险的目的;金融风险的当代特征:高传染性:由于金融的高度自由化和一体化,美国次贷危机成为引发欧债危机的导火线、“零”距离化:1997年泰国金融危机使东南亚国家相继倒下、强破坏性:由于金融深化,美国发生的“次债危机”从2007年8月开始席卷美国、欧盟和日本等世界主要金融市场,以及2009年发生的欧洲主权债务危机,截至2012年仍然对全球经济产生巨大的负面作用。

9.按照金融风险的形态划分:价格风险(利率风险、汇率风险、证券价格风险、金融衍生品价格风险、通货膨胀风险);信用风险;流动性风险;经营或操作风险;政策风险;金融科技风险;其他形态的风险(法律风险、国家风险、环境风险、关联风险)。

根据金融风险的主体划分:金融机构风险;个人金融风险;企业金融风险;国家金融风险。

根据金融风险的产生根源划分:客观金融风险;主观金融风险。

根据金融风险的性质划分:系统性金融风险;非系统性金融风险(经营风险、财务风险、信用风险、道德风险等)。

根据金融风险的层次划分:微观金融风险;宏观金融风险。

10.金融风险的效应可以划分为经济效应、政治效应和社会效应三个方面,经济效应主要包括微观经济效应和宏观经济效应。

11.要了解金融风险形成机理,需要了解金融风险产生的必要条件和充分条件。

金融风险产生的必要条件,也就是金融风险因素,金融风险产生的充分条件,也就是金融风险事故,两者结合就形成了金融风险,在两者的交错作用下,金融风险可能进一步加剧,导致金融危机。

12.现代理论认为,信用的脆弱性,是由信用过度扩张和金融业的过度竞争造成的,这可以从信用运行特征来解释:信用是联系国民经济运行的网络,这个网络使国民经济各个部门环节相互依存、共同发展,但是这个网络的任一环节即使是偶然的破坏都势必引起连锁反应,信用的广泛连锁性和依存性是信用脆弱、产生金融风险的一个重要原因。

金融业的过度竞争以及信用监管制度的不完善是信用脆弱性的又一表现。

13.略。

第二章【习题答案】1.金融风险管理衡量系统2.风险的计量问题3.正确。

人们越来越深刻的认识到,金融机构不仅是现代经济体的支付中介和信用中介,更重要的金融机构是作为风险中介而存在着,是“通过交易金融资产而经营金融风险的机构”。

有效的风险管理具有减少损失,合理避税、增加投资机会、降低管理成本等为金融机构创造价值的效用。

4.正确。

缺乏统一的组织和协调,使得在同一个机构内不同业务风险之间难以进行对比分析,难以从机构层面来把握整体风险;随着金融衍生业务的发展,各种风险的边界越来越模糊,呈现出越来越多的交叉与融合,从而要求人们全面把握风险。

5. 金融风险管理是指以消除或减少金融风险及其不利影响为目的,人们通过实施一系列的政策和措施来控制金融风险的行为。

根据管理学的定义,经济行为主体的管理行为是为实现一定的目标而对其经济经营活动采取的计划、组织、协调、控制的完整过程。

对金融风险进行管理也应是一整套系列性、完整性的管理行为,包括对金融风险的预测、识别、度量、策略选择及评估等内容。

但是,由于金融风险复杂善变的特性,这系列的管理行为并不是孤立发生的,它们相互融合,交互产生,以在动态管理行为中有效减少或消除金融风险产生的后果、维护经济主体的目标实现为己任。

略。

6.略。

提示:加强对自身金融风险的认识、以较低成本来避免或减少损失等。

7.略。

提示:保持整个金融系统的稳定性;促进金融市场有序、高效率地发展。

8.略。

第三章【习题答案】1.均值-方差模型(Mean-Variance Model)2.灵敏度方法3.正确。

要保证风险分析的准确性,就必须进行全面系统地调查分析,对金融风险进行综合归类,以揭示其性质、类型及后果。

否则,就不可能对风险有一个总体的综合认识,就难以确定哪种风险具有发生的可能性,就难以合理地选择控制和处置风险的方法。

因此风险分析必须坚持系统化原则。

同时,由于风险随时存在于单位的生产经营活动中,所以金融风险的识别和衡量也必须是一个连续不断的、制度化的过程,这就是风险识别的制度化、经常化原则。

4.错误。

方差作为风险度量,缺点主要在于组合证券的风险表达式比较复杂,其复杂性超过了Markowitz的方差风险度量,这为实际计算带来了困难,半方差方法同方差法一样,也没有给出风险(损失)的期望值。

5.A6.B7.它是金融风险管理第一步的、最基本的程序;它是整个金融风险管理过程中极为艰难和复杂的工作;它是一项连续性和制度性的工作。

8.提示:金融风险识别的要求。

9.提示:均值——方差选择为基础的马克维兹模型、资本资产定价模型、资本资产套利定价理论、行为金融理论、VaR方法等。

10.定量方法的运用大大地提高了风险度量的精确性,但是有些风险难以度量,比如信用风险;定性方法可以用于当一些影响因素不能量化,或者影响因素过多,难以使用严格的数学模型进行量化分析时的情况,但难以对风险作出准确的计量。

11.金融风险预测是金融风险管理的先行步骤,它要求我们应该能够在现存环境下分析各类因素,运用一定的定量分析方法预测出将要面临的金融风险,做到“防范于未然”,因此属于对潜在金融风险的管理。

第四章【习题答案】1.选择控制型2.预防3.正确。

摩根规则假设现在是过去的重复,将来是现在的重复。

在经济上升期企业收益表现得比预期要好,收回贷款自然没有问题;但一旦经济下行,银行对企业未来收益的预测就显得过于乐观,资产的安全就得不到保障。

4.B5.经济主体的金融风险管理策略的选择是基于风险管理战略确定后的择优挑选,也就是说,金融风险管理策略是以金融风险管理战略为指导的(亦即战略指导策略)。

金融风险管理策略的着眼更为具体细致,相对而言也更具有挑战性,而主要的实施和评估对象也是金融风险管理策略。

6.①预防策略优点:可以事前防范风险。

缺点:防范风险需要以减少业务量和储备一定流动性为代价,会减少收入。

②规避策略优点:可以设想“躲避”掉一些高风险的项目。

缺点:在规避风险的同时也放弃了因承担风险而获得的收益,同时规避风险需要一定的技巧,对金融工具的运用能力方面要求较高。

③分散策略优点:通过分散投资可以再总体上达到风险抵消的目的。

缺点:分散策略只能抵消非系统性风险,系统性风险不能被抵消,随着投资的分散,管理成本也将上升。

④转嫁策略优点:可以将风险转移给别人。

缺点:必须以有人承担风险为前提条件,风险并没有被消除,只是改变了风险的承担者。

⑤保值策略优点:简便、有效。

缺点:套期保值存在成本,并且所使用的金融工具必须以发达完全的资本市场为前提。

⑥补偿策略优点:能对已发生或将发生的损失追寻补偿。

缺点:取决于对未来判断的准确程度和议价能力。

7.略8.略第五章【习题答案】1.开业资本金是否充足2.资本的组成、风险加权的计算、标准比率的目标、过渡期及实施的安排3.最低资本金要求、外部监管、市场约束4.错误。

解释:在初级法中,银行测算与每个借款人相关的违约概率,其他数值由监管部门提供。

高级法中,则允许内部资本配置方式较发达的银行自己测算其他必需的数值。

5.A6.准入监管是指对于银行业注册登记的严格程序和开业条件的具体要求,以防止不合格的金融机构进入金融市场,保持合理的机构数量,避免恶性竞争。

日常经营监管主要是指银行日常审慎监管以及现场稽核与非现场稽核。

其中银行日常审慎监管包括:对银行业务范围的限制、风险控制、流动性要求、资本充足率、盈利能力、内部控制。

市场退出监管是指对出现问题的银行进行及时处理。

7.提示:可以从市场准入的监管、日常经营的监管和市场退出的监管三方面考虑。

8.《新巴塞尔协议》以三大支柱:最低资本金要求、外部监管、市场约束为主要内容。

最低资本金要求主要包括提出了两种信用风险的基本计量方法(即标准法和内部评级法)和对操作风险提资本准备。

外部监管主要包括监督检查应遵循的四大原则、检查各项最低标准的遵守情况、监督检查的其它内容包括监督检查的透明度以及对银行账簿利率风险的处理。

市场约束是指提出了信息披露的有关强制性规定和建议,并在四个领域制定了更为具体的定量及定性的信息披露内容,包括适用范围、资本构成、风险暴露的评估和管理程序以及资本充足率。

第六章【习题答案】1.“信用悖论”2.违约概率、给定违约概率下的损失率、风险暴露、有效期限3.错误。

现代意义上的广义的商业银行信用风险还应包括由于借款人信用水平的变动和履约能力的变化导致其债务市场价值下降而给银行造成损失的可能性。

4.错误。

信用风险概率分布曲线是向左倾斜,厚尾现象仅出现在左侧。

5.B6.C7.狭义上的商业银行的信用风险是指借款人到期不能或不愿履行借款协议,未能如期偿还其债务,致使银行遭受损失的可能性;广义上的商业银行信用风险还应包括由于借款人信用水平的变动和履约能力的变化导致其债务市场价值下降而给银行造成损失的可能性。

信贷风险是指在信贷过程中,由于各种不确定性,使借款人不能按时偿还贷款,造成银行贷款本金及利息损失的可能性。

二者的主要差异在于其所包含的金融资产的范围不同,信用风险不仅包括贷款风险,还包括存在于其他表内、表外业务(如贷款承诺、证券投资、金融衍生工具)中的风险。

8.内部评级法是巴塞尔新资本协议框架中有关信用风险的管理办法。

内部评级法作为一套商业银行信用风险管理的国际准则。

其体系结构包括了商业银行自身的内部评级体系与监管机构的外部监管两个部分。

内部评级法有以下四个基本要素:敞口的分类、风险要素、风险权重和最低要求。

(展开:略)9.传统信用风险的度量:专家评定方法:主观性较强;Z评分模型:运用5个财务比率进行评分; ZETA评分模型:将Z评分模型中的变量由5个增加到7个;现代信用风险的度量:Credit Metrics模型构建在资产组合理论、VaR等理论和方法基础之上;Credit Risk+模型:应用保险经济学中的保险精算方法来计算债务组合的损失分布;Credit Portfolio View模型:从宏观经济环境的角度来分析债务人的信用等级迁移;KMV模型:以期权定价理论为基础,通过计算预期违约频率,对所有其股权公开交易的公司和银行的违约可能性做出了预测。