会计英语第六章复习

立信《会计专业英语》课件LESSON-SIX教学提纲

payments journal to from a cash book.

NEW WORDS,PHRASES AND SPECIAL TERMS

Invoice 发票

A document stating the amount of money due to the organization issuing it for goods or services supplied.

sentences

When special journals are used, only those transactions that do not occur often enough to warrant entry in a special journal are recorded in the general journal.

The most common books of prime entry are

the day book(日记账), the cash book(现金 收支簿) and the journal.

NEW WORDS,PHRASES AND

SPECIAL TERMS

Day book 日记账

A specialized journal or book of prime entry recording specific transactions.

会计英语unit 6 Assets—Current Assets Ⅰ

(1)Accounts Used

Bonds

Stocks

Short-term investment ----Bonds

Interest Receivable Investment Income

Short-term investment -------Stocks

Dividend Receivable Investment Income

Dr. Cash 40,000 Cr. Short-term Investment ---- Stocks 30,600 Dividend Receivable 4,000 Investment Income 5,400

6

the actual amount of receipt and payment.

Cash and Cash Equivalents

Cash and Cash Equivalents is the amount of money the company has in bank accounts, savings bonds, certificates of deposit, and money market funds. It tells you how much money is available to the business immediately.

1)Purchases of Marketable Securities

Stocks

TJ Max purchased 2,000 shares from Big Lot. The market value was $55 per share, which included dividend of $10,000 having been declared but not yet realized.

会计英语——用英语了解会计的定义和运用

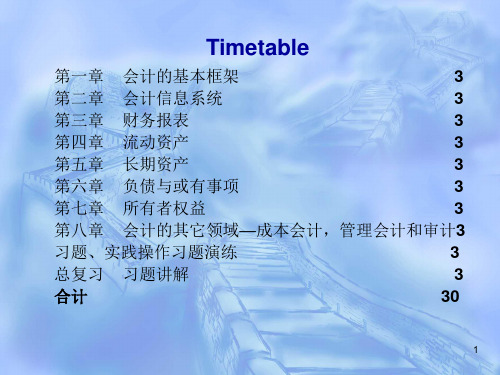

第一章 会计的基本框架

3

第二章 会计信息系统

3

第三章 财务报表

3

第四章 流动资产

3

第五章 长期资产

3

第六章 负债与或有事项

3

第七章 所有者权益

3

第八章 会计的其它领域—成本会计,管理会计和审计3

习题、实践操作习题演练

3

总复习 习题讲解

3

合计

30

1

Chapter 1

I. New words: 1. Account n. statement of money paid or owed for goods or services --The accounts show a profit of $9000. Open/close an account、account payable, account receivable, On account (1) pay part of the money (2)on credit --I will give you$30 on account. --buy things on account.

bank account -- Credit $8 to a customer / an account. Credit n. (1)permission to delay payment for goods and

services --No ~ is given at this shop. Payment must be in

prediction. --There is a lack of ~ between his promises

and his actions. ~ college, ~ column, ~course, ~school Corresponding a. more or less the same ~ fingerprints, the ~ period last year

财务会计英语 unit 6

Section 1 Outline of Costs and Expenses

• Non-production cost (非生产性成本) Non-production cost is also called period cost. It includes selling cost, research and development cost, general and administrative cost, and interest cost.

LOGO

Unit 6

Costs and Expenses

Financial Accountinቤተ መጻሕፍቲ ባይዱ English (Second Edition)

Contents

Section 1 Outline of Costs and Expenses

Section 2 Accounting for Costs

Section 3 Accounting for Expenses

Financial Accounting English (Second Edition)

Section 1 Outline of Costs and Expenses

• 1.1 Expenses Expenses are the decrease in owner’s equity caused by the business’s revenue-producing operation. • 1.2 Costs Cost is a measurement, in monetary terms, of the amount of resources used for business purposes

CPA 注册会计师 会计 讲义 会计英语 第六章 或有事项

2019年注册会计师考试辅导会计英语第六章或有事项本部分在历年专业阶段考试中涉及分数较少,但在2009年也独立考核过主观题,并可以选用英文作答。

本章内容比较简单,在复习中应熟练掌握或有事项的处理原则,争取在考试中对这部分题目做到“手到擒来”。

I.或有负债和或有资产或有负债无论是现时义务,还是潜在义务均不符合负债的确认条件,因而不能确认,只能在附注中披露。

No matter it is a current obligation or a potential obligation , contingent liability couldn’t be recognized because the liability recognition criteria are not met. It only can be disclosed in note.或有资产,是潜在资产,不符合资产的确认条件,因而不能确认,只有在很可能导致经济利益流入企业时才能在附注中披露。

Contingent asset is potential asset and should not be recognized because it is not satisfying the asset recognition criteria and will be disclosed in the notes once it would most likely lead to economic benefit flowing into the business.II. 预计负债的确认 Recognition of provision与或有事项相关的义务同时满足下列条件的,应当确认为预计负债:The obligation pertinent to a contingency shall be recognized as provision when the following conditions are satisfied simultaneously:(1)该义务是企业承担的现时义务;That obligation is a current obligation of the enterprise;(2)履行该义务很可能导致经济利益流出企业;It is likely to cause any economic benefit to flow out of the enterprise as a result of performance of the obligation;(3)该义务的金额能够可靠地计量。

会计英语第6章

If all required payments are made promptly to the pension fund trustee, no liability needs to be represented in the financial statements.

Short-term notes payable may be either interest-bearing or non-interest-bearing.

In theory, short-term notes payable should be recorded at the present value of the cash outflows associated with the note.

1. Taxes Payable

◦ Show the amount that the entity owes government offices for taxes.

2. Interest Payable

◦ Cost of borrowing and increases with the passage of time.

6.1.5 Short-term Borrowings

Short-term borrowings usually arise from cash borrowings and are generally payable to banks or loan companies.

CPA注册会计师会计讲义会计英语第六章或有事项

CPA注册会计师会计讲义会计英语第六章或有事项2019年注册会计师考试辅导会计英语第六章或有事项本部分在历年专业阶段考试中涉及分数较少,但在2009年也独立考核过主观题,并可以选用英文作答。

本章内容比较简单,在复习中应熟练掌握或有事项的处理原则,争取在考试中对这部分题目做到“手到擒来”。

I.或有负债和或有资产或有负债无论是现时义务,还是潜在义务均不符合负债的确认条件,因而不能确认,只能在附注中披露。

No matter it is a current obligation or a potential obligation , contingent liability couldn’t be recognized because the liability recognition criteria are not met. It only can be disclosed in note.或有资产,是潜在资产,不符合资产的确认条件,因而不能确认,只有在很可能导致经济利益流入企业时才能在附注中披露。

Contingent asset is potential asset and should not be recognized because it is not satisfying the asset recognition criteria and will be disclosed in the notes once it would most likely lead to economic benefit flowing into the business.II. 预计负债的确认 Recognition of provision与或有事项相关的义务同时满足下列条件的,应当确认为预计负债:The obligation pertinent to a contingency shall be recognized as provision when the following conditions are satisfied simultaneously:(1)该义务是企业承担的现时义务;That obligation is a current obligation of the enterprise;(2)履行该义务很可能导致经济利益流出企业;It is likely to cause any economic benefit to flow out of theenterprise as a result of performance of the obligation;(3)该义务的金额能够可靠地计量。

会计英语 lesson 6

• 6.3 Share Capital

• The capital of a limited company is divided into shares that have a nominal/ par value.

• 6. To understand different values of a stock.

• 7. To report stockholders’ equity transactions on The Cash Flow Statements

• 6.1 Introduction: Limited Company

LESSON SIX

OWNER’S EQUITY

• Aims:

• 1. To describe the characteristics of limited company.

• 2. To differentiate among authorized, issued, and outstanding shares.

• 6.5 Measure the Effect of Issuing Stock on a Company’s Financial Position

• Corporations issue stock to raise capital to finance operations.

• 1. A corporation issues (sells) all or part of the stock that is authorized in the corporate charter.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Acquisition Date

The cost of the asset is determined by the cash or cash-equivalent price paid to acquire the asset. There may be many cost components incurred to acquire and prepare the asset for its intended use. Purchase price Freight costs [freɪt] 运费 Installation cost [ɪnstə‘leɪʃ(ə)n] 安装成本 of a productive asset. Example P58

Depreciation cost per unit =

Depreciation expense for period= Depreciation cost per unit ×actual production amount during current period Note that the straight-line method provides a constant不变的 depreciation amount per year, but the units-of-production method provides a constant amount per unit of production.

During its useful life

After acquisition, tangible operational assets decrease in economic utility to the user because of a number of causative factors, such as wear and tear 磨损, the passage of time时光流逝, obsolescence [,ɒbsəʊ‘lesəns]过时, and technological changes技术进步. Depreciation is the accounting process of allocating the periodic expiration of capital assets against the periodic revenue earned.

2. Units-of-production method 工作量法 The Units-of-production method allocates the cost of an asset to usage rather than years. This method amortizes the cost of the asset over the estimated service life as measured by estimated units of production, not by estimated years. If the use of the asset varies and the contribution to revenue differs from period to period, the unitsof-production method may be appropriate. The depreciation per unit of production is determined as follows:

3. Accelerated methods Accelerated methods charge higher amounts of depreciation to the earlier years of an asset’s life. As an asset has greater economic benefit in the earlier years of its life than in the later years, depreciation should be allocated more in the early years of the asset’s life, the amount of depreciation charged period declines with time. Two common methods for allocating depreciation on an accelerated basis are sum-of-the-year’sdigits method年数总和法anddeclining-balance method双倍余额递减法

Depreciation methods

1. Straight-line method 直线折旧法 The straight-line method of depreciation allocates equal amounts of the cost of an asset to each accounting period during its estimated life. This method is the most common method used to allocate the cost of property, plant and equipment among accounting periods because it is easy and simple to calculate. A typical example would be depreciation for a building or for office furniture. The depreciation is computed as follows:

Chapter 6

Non-Current Assetsleting this chapter, you should be able to: 1. Describe the nature of depreciation. 2. Explain the factors that affect the determination of depreciation expense. 3. Calculate the amount of depreciation by the straight-line method. 4. Calculate the amount of depreciation by units-of-production methods. 5. Calculate accelerated depreciation under the decliningbalance method and the sum-of-the-years’-digits method.

Factors affecting depreciation

Factors that influence depreciation are cost of the asset; C estimated residual value (or salvage value); RV estimated service life; N or P depreciation rate; R Dollar amount of depreciation per period. D

Special Terms

(1) depreciation (n.) 折旧 (2) residual value (or salvage value) 残值 (3) straight-line method 直线法 (4) the units-of-production method 工作量法 (5) accelerated method 加速折旧法 (6) declining-balance method 余额递减法 (7) sum-of-the-years’-digits method 年数总和法 (8) double-declining-balance (DDB) method 双倍余额递减 法 (9) accumulated depreciation 累计折旧

The entry to record this depreciation expense would be Depreciation expense 90,000 Accumulated depreciation 90,000 On the balance sheet, accumulated depreciation is deducted from the cost of property , plant, and equipment, and difference, called the book value ( or property, plant, and equipment, net), is included in total assets.

Land, buildings , machinery[mə'ʃiːn(ə)rɪ], equipment, furniture, tools, vehicles ['viːɪk(ə)l] and natural resources.

The primary phases of accounting for operational assets are: 1. Measuring and recording the cost of the asset at acquisition date. 2. After acquisition, measuring the expense of using the asset during its useful life. 3. Recording disposal of operational assets.

Cost Residual value Depreciation per year Service life in years