会计英语复习资料

会计英语期末考试复习(qq)

会计英语期末考试复习(unit1---unit8)1.词汇(英翻中)20*1’=20’(主要复习期中考试的词汇题及每个单元的词汇表)2.连线20*1’=20’(主要复习每个单元课后习题中的连线题)3.翻译(英翻中)5*6’=30’(复习范围见后面材料)4.会计分录15’(主要复习期中考试的分录题)5.制表15’(主要复习资产负债表和现金流量表,见课本43页和53页)翻译复习:1. The accounting information is primarily supplied to owners, managers and investors of every business, and other users to assist in the decision-making process. Therefore, accounting is also called “the language of business”. (page 3)会计信息主要提供给每家公司的所有者、管理者和投资者及其他用户以有助于决策过程。

因此,会计也被称为“商业语言”。

2. Assets are properties that are owned and have monetary value; for instance, cash, inventory, buildings, equipments. Liabilities are amounts owed to outsiders, such as notes payable, accounts payable, bonds payable. (page 16)资产是所拥有并有货币价值的财产;比如,现金、存货、建筑物、设备。

负债是欠外界人士的金额,比如应付票据、应付账款、应付债券。

3. Intangible assets are nonphysical assets that confer on their owners long-term rights, privileges, or competitive advantages, including patents, copyrights, licenses and trademarks. (page 25)无形资产是没有物质形态的资产,它赋予所有者长期的权利、优先权、或竞争优势,包括专利权、著作权、许可权、商标权。

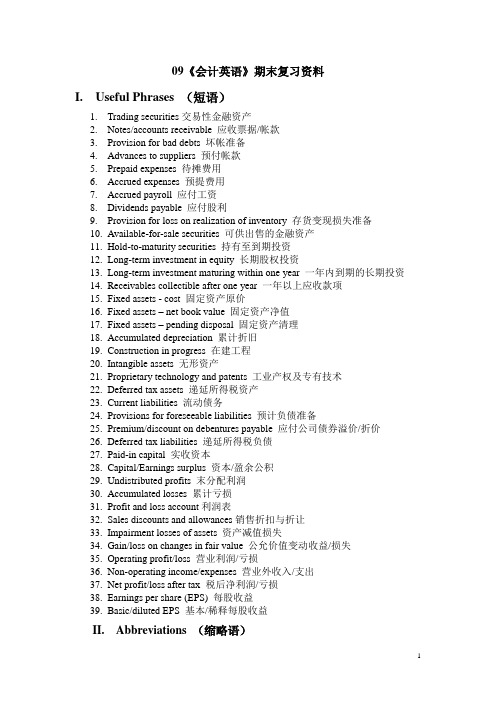

09《会计英语》期末复习资料v

09《会计英语》期末复习资料I. Useful Phrases (短语)1.Trading securities交易性金融资产2.Notes/accounts receivable 应收票据/帐款3.Provision for bad debts 坏帐准备4.Advances to suppliers 预付帐款5.Prepaid expenses 待摊费用6.Accrued expenses 预提费用7.Accrued payroll 应付工资8.Dividends payable 应付股利9.Provision for loss on realization of inventory 存货变现损失准备10.Available-for-sale securities 可供出售的金融资产11.Hold-to-maturity securities 持有至到期投资12.Long-term investment in equity 长期股权投资13.Long-term investment maturing within one year 一年内到期的长期投资14.Receivables collectible after one year 一年以上应收款项15.Fixed assets - cost 固定资产原价16.Fixed assets – net book value 固定资产净值17.Fixed assets – pending disposal 固定资产清理18.Accumulated depreciation 累计折旧19.Construction in progress 在建工程20.Intangible assets 无形资产21.Proprietary technology and patents 工业产权及专有技术22.Deferred tax assets 递延所得税资产23.Current liabilities 流动债务24.Provisions for foreseeable liabilities 预计负债准备25.Premium/discount on debentures payable 应付公司债券溢价/折价26.Deferred tax liabilities 递延所得税负债27.Paid-in capital 实收资本28.Capital/Earnings surplus 资本/盈余公积29.Undistributed profits 末分配利润30.Accumulated losses 累计亏损31.Profit and loss account利润表32.Sales discounts and allowances销售折扣与折让33.Impairment losses of assets 资产减值损失34.Gain/loss on changes in fair value 公允价值变动收益/损失35.Operating profit/loss 营业利润/亏损36.Non-operating income/expenses 营业外收入/支出 profit/loss after tax 税后净利润/亏损38.Earnings per share (EPS) 每股收益39.Basic/diluted EPS 基本/稀释每股收益II. Abbreviations (缩略语)1.GAAP : Generally Accepted Accounting Principles .公认会计原则2.FASB : Financial Accounting Standards Board. 财务会计准则委员会3.AICPA: American Institute of Certified Public Accountants. 美国注册会计师协会4.CICPA : Chinese Institute of Certified Public Accountants. 中国注册会计师协会5.MOF : the Ministry of Finance财政部6.SL Method : straight-line method. 直线法P.252/77.ROA : return on assets.资产报酬率P.267/78.EPS : earning per share.每股收益P.351/99.P/E Ratio : the price/earning ration 市盈率10.SCF : the statement of cash flows 现金流量表III. Questions (回答问题)Lesson 1 --- Home Assignments1.What are the four financial statements prepared by a proprietorship toprovide information for decision making?√They are: income statement (profit and loss account), statement of owner’s equity (capital statement, statement of retained earnings), balance sheet and cash flow statement.2.What is the proper formula presentation of the accounting equation? √Assets = Liabilities + [owner’s equity + (Revenue – Expenses)]3.What are the four key ethical standards that are expected of professionalaccountants?They are: integrity, confidentiality, competence, and objectivity.Exercise 1 - 2: p.2Foreman Corporation, engaged in a service business, completed the following selected transactions during the period: √1)Issued additional capital stock, receiving cash;2)Purchased supplies on account;3)Returned defective supplies purchased on account and not yet paid for;4)Received cash as a refund from the erroneous overpayment of anexpense;5)Charged customers for services sold on account;6)Paid utilities expense;7)Paid a creditor on account;8)Received cash on account from charge customers;9)Paid cash dividends to stockholders;10)Determined the amount of supplies used during the month.Using a tabular form with column headings entitled Transactions, Assets, Liabilities, and Capital respectively, indicate the effect of each transaction. Use + for increase and – for the decrease.Lesson 2 --- Home Assignments1.Does debit always mean increase and credit always mean decrease? √No, it does not. And debit or credit should not be confused with increase or decrease. It depends on which side of an account is used for debit or credit.2.Given that assets have economic value and that they have debit balances,why do expenses also have debit balances?√Because expenses have the effect of decreasing capital, and just as decreases in capital are recorded as debit, increases in expense accounts are recorded as debits. Lesson 3---Home Assignments1.Briefly explain the matching principle.√The matching principle states that expenses should be deducted (matched against) from the revenues earned in the same period.2.Why is an unearned revenue a liability?√Unearned revenue is a liability because the business owes the customer a good or service.Lesson 7---Home Assignments1.What do determinable current liabilities include? P.291 √They include trade accounts payable, current notes payable, current maturities of long-term obligations, cash dividends payable, accrued liabilities, and prepayments or deposits from customers.2.What does non-current liabilities represent? P.306√It represents obligations of the firm that generally are due more than one year after the balance sheet date.Lesson 8---Home Assignments1.What determines the yield rate of a company’s stock?√Dividends per share divided by market price per share determine the yield rate ofa company‘s stock.2.What is P/E ratio?√The Price/Earning (P/E) ratio is the ratio of the market price per share to earnings per share.Lesson 9---Home Assignments1.What are the three categories into which the SCF should be classified?They are a) cash flow from operating activities, b) cash flow from investing activities, cash flow from financing activities.2.What is the usefulness of the SCF?√From SCF, the information users can know the reasons for the difference between net income and net cash flows from operating activities.IV. E-C Translation (英汉语篇翻译)1.Preparing a Trial BalanceAccountants usually complete the posting of journal entries to the ledger accounts at the end of each month if they are using a manual system. With a computerized system, each posting is done automatically as each journal entry is recorded. The equality of debits and credits in the ledger should be verified at the end of each accounting period. T o verify the accuracy of the recording process, accountants prepare a trial balance of the ledger accounts.A trial balance not only provides a check on the equality of debits and credits but also is a useful summary of account balances for preparing financial statements.[参考译文] 编制试算表若使用的是手工录入系统的话,会计师通常是在每个月的月底完成日记帐到分类帐的过帐工作;若是用计算机系统的话,则每次过帐均在完成每笔日记帐的同时就自动完成了。

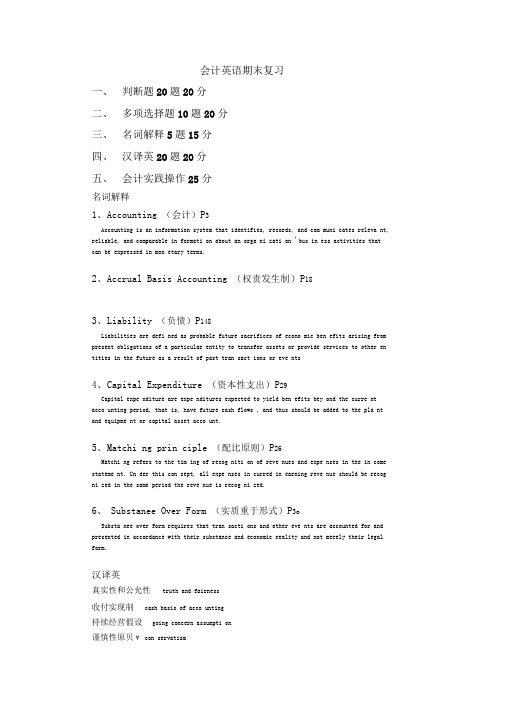

会计英语期末复习

会计英语期末复习一、判断题20题20分二、多项选择题10题20分三、名词解释5题15分四、汉译英20题20分五、会计实践操作25分名词解释1、A ccounting (会计)P3Accounting is an information system that identifies, records, and com muni cates releva nt, reliable, and comparable in formati on about an orga ni zati on 'bus in ess activities that can be expressed in mon etary terms.2、A ccrual Basis Accounting (权责发生制)P183、L iability (负债)P148Liabilities are defi ned as probable future sacrifices of econo mic ben efits arising from present obligations of a particular entity to transfer assets or provide services to other en tities in the future as a result of past tran sact ions or eve nts4、C apital Expenditure (资本性支出)P29Capital expe nditure are expe nditures expected to yield ben efits bey ond the curre nt acco unting period, that is, have future cash flows , and thus should be added to the pla nt and equipme nt or capital asset acco unt.5、M atchi ng prin ciple (配比原则)P26Matchi ng refers to the tim ing of recog niti on of reve nues and expe nses in the in come stateme nt. Un der this con cept, all expe nses in curred in earning reve nue should be recog ni zed in the same period the reve nue is recog ni zed.6、Substanee Over Form (实质重于形式)P3oSubsta nee over form requires that tran sacti ons and other eve nts are accounted for and presented in accordance with their substance and economic reality and not merely their legal form.汉译英真实性和公允性truth and fairness收付实现制cash basis of acco unting持续经营假设going concern assumpti on谨慎性原贝V con servatism资本性支出capital expe nditures配比原贝V matchi ng prin ciple临时性账户temporary acco unt经营成果operat ing results盈余公积surplus reserve 未分配利润un distributed profit银行对账单bank stateme nt应付票据no tes payable实质重于形式substa nee over form 货币计量假设mon etary un it assumpti on重要性原则materiality可变现净值net realizable value完工百分比法perce ntage-of-completi on method 会计主体假设separate en tity assumpti on交易与事项transactions and eve nts会计分期假设acco unting period assumpti on 会计循环acco un ti ng cycle多选题1.会计信息外部使用者有哪些?Suppliers, regulators, lawyers, brokers, the in vestors , le nders, non-executive directors2.资产负债表的构成项目(资产,负债,所有者权益)Assets, liabilities, owners 'equity3.现金流量表的构成项目(经营,投资,筹资)Operating, investing , financing activities4 •所有者权益变动表In vestors, capital reserve, surplus reserve,reta ined5.应收款项的分类Acco unts receivable, no tes receivable, other receivable6.存货的计价方法Specific ide ntificati on, average cost, first-i n first-out7.制造业企业存货的构成Raw materials, good in process of manufacture, fini shed goods8.固定资产折旧的方法press shareholders /un distributed profit first-out, last-i n6。

会计专业英语复习资料

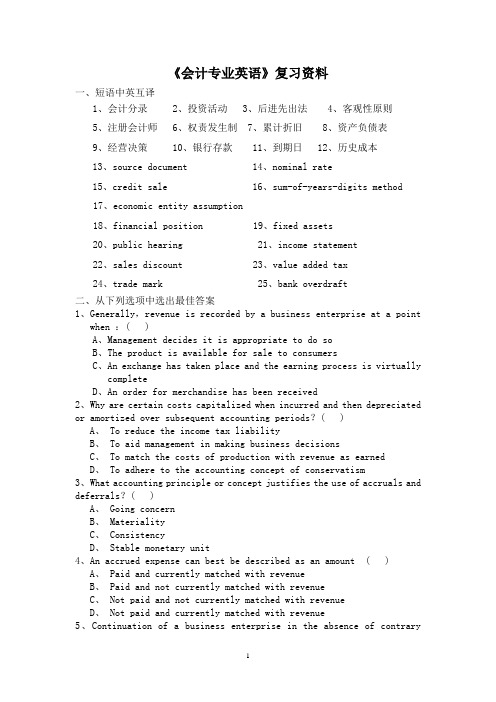

《会计专业英语》复习资料一、短语中英互译1、会计分录2、投资活动3、后进先出法4、客观性原则5、注册会计师6、权责发生制7、累计折旧8、资产负债表9、经营决策 10、银行存款 11、到期日 12、历史成本13、source document 14、nominal rate15、credit sale 16、sum-of-years-digits method17、economic entity assumption18、financial position 19、fixed assets20、public hearing 21、income statement22、sales discount 23、value added tax24、trade mark 25、bank overdraft二、从下列选项中选出最佳答案1、Generally,revenue is recorded by a business enterprise at a pointwhen :( )A、Management decides it is appropriate to do soB、The product is available for sale to consumersC、An exchange has taken place and the earning process is virtuallycompleteD、An order for merchandise has been received2、Why are certain costs capitalized when incurred and then depreciated or amortized over subsequent accounting periods?( )A、To reduce the income tax liabilityB、To aid management in making business decisionsC、To match the costs of production with revenue as earnedD、To adhere to the accounting concept of conservatism3、What accounting principle or concept justifies the use of accruals and deferrals?( )A、Going concernB、MaterialityC、ConsistencyD、Stable monetary unit4、An accrued expense can best be described as an amount ( )A、Paid and currently matched with revenueB、Paid and not currently matched with revenueC、Not paid and not currently matched with revenueD、Not paid and currently matched with revenue5、Continuation of a business enterprise in the absence of contraryevidence is an example of the principle or concept of ( )A、Business entityB、ConsistencyC、Going concernD、Substance over form6、In preparing a bank reconciliation,the amount of checks outstanding would be:( )A、added to the bank balance according to the bank statement.B、deducted from the bank balance according to the bank statement.C、added to the cash balance according to the depositor’s records.D、deducted from the cash balance according to the depositor’s records.7、Journal entries based on the bank reconciliation are required for:( )A、additions to the cash balance according to the depositor’s records.B、deductions from the cash balance according to the depositor’s records.C、Both A and BD、Neither A nor B8、A petty cash fund is :( )A、used to pay relatively small amounts。

会计英语复习资料

会计英语复习资料一.汉译英练习1.会计原则是每个会计人员在进行工作时必须遵守的规则。

2.编制会计分录是在会计期间经常要做的工作。

3.编制工作底稿是每个会计期末要做的工作。

4.实账户是负债表账户。

在月末,它们的余额应不被结平,而转入下一期。

5.虚账户是利润表账户。

在月末,它们的余额应结平,以便用来记录下一期的经营成果。

6.这个月费用很大,我们要查一下原因,分析一下有关经济业务。

7.如果销售商品时,若客户没有付现金,则这种销售被称为赊销。

8.赊销时,卖方会对卖方提出付款条件,这个条件被称为信用条件。

9.固定资产每月都必须计提折旧。

10.无形资产每月计提摊销。

11.企业外部的许多人关心企业的财务信息,而及时提供财务信息给他们是会计的工作。

12.财务报表是人们进行经营决策的依据之一。

13.我们必须准备足够的资金,这笔贷款下个月到期。

14.调整分录与结账分录必须计入日记账和分类账,否则账上的余额会与报表上数额不符。

15.在西方会计中,股份公司的权益科目与独资企业的权益科目是不同的。

16.销售商品的收入常被称为是销售收入。

17.本年利润是用于计算利润的账户,他与其他损益类科目一样,年末,都要被结平。

18.请给我看一下有关这个月应缴的税费的数据二.会计专业词汇练习会计词汇辨析()Dividends ()Cash()Inventory ()Accumulated depreciation()Accounts receivable ()Interest payable()Income taxes payable ()Owner’s capital()Retained earnings ()Closing entry()Journalizing ()Administrative expenses()Cost of goods sold ()Net income()Business transaction ()Unearned revenues()Ending balance ()Financial expenses()Prepaid expenses ()operating results()Withdrawals ()Sales( )Allowance for bad accounts ()Common stock()Office supplies inventory ()long-term bonds investments ()Accounts payable ()Cash basis accounting ()Office equipments ()Posting()Beginning balance ()Business transaction()Trial balance ()Financial statements()Selling expenses. ()Financial position()Marketable securities ( ) paid in capital( ) operating equipments ()Notes payable( ) Short term investment ( ) Gain()Extraordinary items ()Finished products()Salary expenses ()Interest receivable()Accrual basis accounting ()Income statements()Adjusting entry ()Intangible assets( ) Source documents ( ) Gross sales( ) Purchase ( ) Fixed assets1.期末余额28. 坏账准备2.应付所得税29. 应收账款3.销售费用30. 主营业务收入4.业主资本31. 经营成果5.主营业务成本32 管理费用6.应付利息33 存货7.留存收益34 调整分录8.预收账款35 结账分录9.累计折旧36 权责发生制10.经济业务37 应付票据11.财务报表38 编制分录12.试算平衡39. 期初余额13.现金收付制40. 应付账款14.财务费用41. 净利润15.普通股42. 财务状况16.营业外收支项目43. 过账17.应收利息44 办公用品库存18.实收资本45. 办公设备19.库存46. 股利20.经营设备47. 业主提取21.利得48. 产成品22.待摊费用49. 交易性金融资产23.长期债券投资50. 短期投资24.无形资产51. 工资费用25.生产设备52销售总额26.原始凭证53 固定资产27.采购54. 工资费用三.英译汉1.Revenue is the price of goods sold and services rendered during a given accounting period. Earning revenue causes owner’s equity to increase. When a business renders services of sells merchandise to its customers, it usually receives cash or acquires an account receivable from the customer.2.To clearly identify the effects of the business operations on each of the accounting elements, it is necessary to transfer those records from journal to each corresponding books used for recording different accounting element. This transfer process is called “posting”.3.The journal is a day-by-day record of business transactions. The information recorded about each transaction includes the date of the transaction, the debit and credit changes in specific ledger accounts, and a brief explanation of the transaction.4.The things a business owns can be classified into five categories, which also called accounting elements, they are: assets, liabilities, owners' equity, revenues, and expenses. Every business transaction of the business may affect more than one of the above elements。

会计英语复习资料答案

会计英语复习资料答案会计英语复习资料答案⼀、单词1.accounting 会计学2.accounting elements 会计要素3.accounting equation 会计等式4.assets 资产5.liabilities 负债6.owner`s equity 所有者权益7.revenue 收⼊8.expenses 费⽤9.profits 利润10.accounting period 会计期间11.transaction 经济业务/会计事项12.double-entry system 复式记账法13.debit 借⽅14.credit 贷⽅15.ledger 分类账16.chart of accounts 会计科⽬表17.journal ⽇记账18.current assets 流动资产19.cash 现⾦20.cash equivalents 现⾦等价物21.check ⽀票22.bank deposits 银⾏存款23.cash in bank 银⾏存款24.money orders 汇票25.cash on band 库存现⾦26.accounts receivable 应收账款27.allowance for bad debts 坏账准备/doc/6dfd370b4b35eefdc8d3335f.html realizable value 可变现净值29.inventory 存货30.finished goods 产成品31.semi-finished goods 半成品32.goods in process 在产品33.historical cost 历史成本34.specific identification 个别计价法35.first-in, first-out 先进先出法/doc/6dfd370b4b35eefdc8d3335f.html st-in, first-out 后进先出法37.weighted average 加权平均法38.raw materials 原材料39.short-term investment 短期投资40.marketable securities 有价证券41.shareholder 股东42.bonds 债券43.debentures 债券44.long-term assets 长期资产45.fixed assets 固定资产46.intangible assets ⽆形资产47.deferred assets 递延资产/doc/6dfd370b4b35eefdc8d3335f.html eful life 使⽤寿命49.depreciation 折旧50.depreciable amount 应计折旧额51.depreciation method 折旧⽅法52.estimated net residual value 预计净残值53.straight-line method 直线法54.units of production method ⼯作量法55.double declining balance method 双倍余额递减法56.sum-of-the-years-digits method 年数总和法57.amortization 摊销58.impairment 减值59.current liabilities 流动负债60.accounts payable 应付账款61.notes payable 应付票据62.unearned revenue 预收账款63.income taxes payable 应交所得税64.contingent liabilities 或有负债65.long-term liabilities 长期负债66.bonds payable 应付债券67.ownership 所有权68.sole proprietorship 独资企业69.partnership 合伙企业70.corporation 公司/doc/6dfd370b4b35eefdc8d3335f.html mon shareholders 普通股股东72.preferred shareholders 优先股股东/doc/6dfd370b4b35eefdc8d3335f.html mon stock 普通股74.preferred stock 优先股75.dividends 股利76.retained earnings 留存收益77.paid-in capital 实收资本78.capital stock 股本79.addtional paid-in capital 附加投⼊资本80.capital surplus 资本公积81.undistributed profit 未分配利润82.par value ⾯值83.fair value 公允价值84.reserve fund 盈余公积85.legal reserve 法定盈余86.stock split 股利分割87.cash dividends 现⾦股利88.stock dividends 股票股利89.sales revenue 销售收⼊90.service revenue 劳务收⼊91.product costs 产品成本92.direct material costs 直接材料成本93.direct labor costs 直接⼈⼯成本94.indirect costs 间接成本95.manufacturing overhead 制造费⽤96.period expenses 期间费⽤97.operating expense 营业费⽤98.administrative expense 管理费⽤99.finance expense 财务费⽤100.balance sheet 资产负债表101.income statement 利润表/损益表102.cash flow statement 现⾦流量表⼆、填空1. The accounting elements include assets, liabilities, owner`s equity, revenue, expenses, and profits.2. Liabilities are debts of a business.3. Borrowing cash from a bank does not belong to assets; it simply belongs to liability.4. Profit is the excess of revenue over expenses for the accounting period.5. The accounting equation is :assets = liabilities + owner`s equity.6.“Dr.” stands for debits ,while “Cr.” is the abbreviation for credit.7. Liability, owner`s equity, revenue and profit decreases are recorded as debits.8. Short-term investments refer to various of marketable securities.9. Marketable securities include stock and debentures to be realized within one year from the balance sheet date and shall be accounted for at cost.10. Depreciation refers to the systematic allocation of the depreciable amount of a fixed asset over its useful life.11. The four common depreciation methods are the straight-line method, the units of production method.12. The straight –line method shall be employed when it is assumed that an asset`s economic revenue is the same each year, and the repair and maintenance cost is also the same for each period.13. When depreciation is mainly due to wear and tear, the units of production method are usually used.14. The two types of intangible assets are finite and indenfinite intangibles.15. Please name five most commonly seen intangibles , i.e., patents, trademarks, copyrights, franchises and licenses, internet domain names and construction permit.16. Intangible assets do not include internally generated goodwill, brands and publishing titles.17. Intangible assets should be measured initially at cost.18. For intangible assets with finite useful lives enterprises shall consider their amortization while intangible assets with indefinite useful lives shall not be amortized.19. The account of unearned revenue should be decreased when the service paid for in advance has been provided.20. The account of accounts payable should be recorded when the business purchased supplies on credit.21. The account of notes payable used to show what the business owes the bank.22. A corporation`s balance sheet contains assets, liabilities, and shareholders` equity.23. Preferred stock and common stock are the two common capital stocks issued by a corporation.24. Cash dividends and stock dividend are the usual forms of distribution to share holders.25. A stock dividend is a proportional distribution to shareholders of additional shares of the corporation`s common or preferred stocks.26. Retained Earnings represents the corporation`s accumulated net income, less accumulated dividends and other amounts transferred to paid-in capital accounts.三、单选1. Matching each of the following statements with its poper term.(1) accounts receivable ( B )(2) dishonored notes receivable ( C )(3) allowance method ( A )(4) direct write-off method ( D )A. The method of accounting for un-collectible accounts that provides an expense for un-collectible receivables in advance of their write-off.B. A receivable created by selling merchandise or service on credit.C. A note that maker fails to pay on the due date.D. The method of accounting for un-collectible accounts that recognizes the expense only when accounts are judged to be worthless.2. At the end of the fiscal year, accounts receivable has a balance of $100000 and allowance for doubtful accounts has a balance of $7000, The expected net realizable value of the accounts receivable is ( B )A. $7000B. $93000C. $100000D. $1070003. If merchandise inventory is being valued at cost and the price level is steadily rising, the method of costing that will yield the higher net income is ( B )A.LIFOB.FIFOC.AverageD.Periodic4. Given the following information, which of the following accounting transactions is true?( B )Gross payroll $20000Federal income tax withheld $4000Social security tax withheld $1600A. $1600 is recorded as salary expense.B. $14400 is recorded as salary payableC. The $1600 deducted for employee social security tax belongs to the companyD. Payroll is an example of an estimated liability5.If a corporation has outstanding 1000 shares of $9 cumulative preferred stock of $100 par and dividends have been passed for the preceding three years, what is the amount of preferred dividends that must be declared in the current year before a dividend can be declared on common stock?( C ) A. $9000 B. $27000 C. $36000 D. $450006. All of the following are reasons for purchasing treasury stock except to ( B )A. make a market for the stockB. increase the number of shareholdersC. increase the earnings per share and return on equityD. give employee as compensation7. Paid-in capital for a corporation may arise from which of the following sources?( D )A. Issuing cumulative preferred stockB. Receiving donations of real estateC. Selling the corporation`s treasury stockD. All of the above8. Under the equity method, the investment account is decreased by all of the following except the investor`s proportionate share of ( B )A. dividends paid by the investeeB. declines in the fair value of the investmentC. the losses of the investeeD. all of the options9. Cash dividends are paid on the basis of the number of shares ( C )A. authorizedB. issuedC. OutstandingD. outstanding less the number of treasury shares10. The stockholders` equity section of the balance sheet may include ( D )A. common stockB. preferred stockC. donated capitalD. all of the above11. Declaration and issuance of a dividend in stock ( D )A. increases the current ratioB. decreases the amount of working capitalC. decreases total stockholders` equityD. has no effect on total assets, liabilities, or stockholders` equity12. If a corporation reacquires its own stock, the stock is listed on the balance sheet in the ( C )A. current assets sectionB. long term liability sectionC. stockholders` equity sectionD. investments section13. A corporation has issued 25000 shares of $100 par common stock and holds 3000 of these shares as treasury stock. If the corporation declares a $2 per share cash dividend, what amount will be recorded as cash dividend?( C )A. $22000B. $25000C. $44000D. $5000014. A company declared a cash dividend on its common stock on December 15, 2004, payable on January 12, 2005. How would this dividend affect shareholders` equity on the following dates? ( B ) December 15, January 122004 2005A. Decrease. Decrease.B. No effect. No effect.C. No effect. No effect.D. Decrease. Decrease.15. An example of a cash flow from an operating activity is ( D )A. the receipt of cash from issuing stockB. the receipt of cash from issuing bondsC. the payment of cash for dividendsD. the receipt of cash from customers on account16. An example of a cash flow from an investing activity is ( A )A. the receipt of cash from the sale of equipmentB. the receipt of cash from issuing bondsC. the payment of cash for dividendsD. the payment of cash to acquire treasury stock17. An example of a cash flow from a financing activity is ( C )A. the receipt of cash from customers on accountB. the receipt of cash from the sale of equipmentC. the payment of cash for dividendsD. the payment of cash to acquire marketable securities18. A receivable created by selling merchandise or services on credit. ( A )A. accounts receivableB. dishonored notes payableC. allowance methodD. direct write-off method19. At the end of the fiscal year, accounts receivable has a balance of $100000 and allowance for doubtful accounts has a balance of $7000. The expected net realizable value of the accounts receivable is ( B )A. $7000B. $93000C. $100000D. $10700020.( B ) are valuable resources owned by the entity.A. LiabilityB. AssetsC. EquityD. None of them21. Which is intangible asset ( C )A. internally generated goodwillB. internally generated publishing titlesC. franchises and licenseD. internally generated brands22.( A ) shall be employed when it is assumed that an asset`s economic revenue is the same each year, and the repair and maintenance cost is also the same for each period.A. straight-line methodB. units of production methodC. double declining balance methodD. sum-of-the-years-digits(SYD) method四、判断1. Fixed assets are intangible assets. ( F )2. Internally generated goodwill can be viewed as intangible assets. ( F )3. Land doesn`t need depreciation and is considered to have an infinite life. ( T )4. Fixed assets are usually subjected to depreciation. ( T )5. Bonds and stocks are classified as intangible assets.( F )6. Once the expected useful life and estimated net residual value are determined, they shall notbe changed under any circumstances.( F )7. When a corporation issues one type of capital stocks, common stocks are always issued. ( T )8. Par value is strictly a legal matter, and it establishes the legal capital of a corporation. ( T )9. The balance of the additional paid-in capital account represents a gain on the sale of stocks and increases net income. ( F )10. A corporation must, by law, pay a dividend once a year. ( T )11. Dividends are an expense of a corporation and should be charged to the periodic income. ( T )12. Revenue increase owner`s equity. ( T )13. Revenue is recognized when we receive cash from the buyers. ( F )14. Advertising expense is usually collected as period expense. ( T )15. Interest revenue should be measured based on the length of time. ( T )16. If revenue exceed expenses for the same accounting period, the entity is deemed to suffera loss. ( F )17. Asset = liabilities + Expense. ( F )18. Liabilities are debts of a business. ( T )19. Borrowing cash from a bank belongs to revenue. ( F )20. Increase in asset is recorded in credit side. ( F )21. When depreciation is mainly due to wear and tear, straight-line method shall be employed. ( F )22. Bonds payable belong to current liabilities.( F )23. All fixed assets are depreciable over their limited useful life.( F )24. Fixed assets are intangible assets. ( F )25. Internally generated goodwill can be viewed as intangible assets. ( F )26. Land doesn`t need depreciation and is considered to have an infinite life. ( T )五、翻译1. Accounting contains elements both of science and art. The important thing is that it is not merely a collection of arithmetical techniques but a set of complex processes depending on and prepared for people.会计既是科学,也是艺术。

会计专业英语期末复习资料

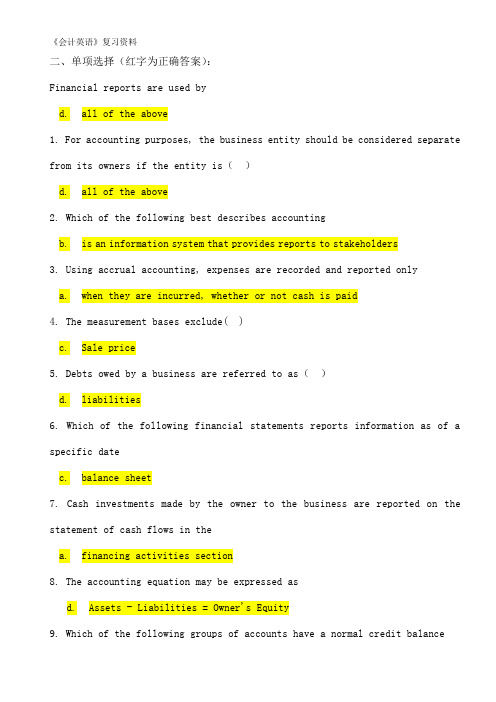

《会计英语》复习资料二、单项选择(红字为正确答案):Financial reports are used byd.all of the above1. For accounting purposes, the business entity should be considered separate from its owners if the entity is()d.all of the above2. Which of the following best describes accountingb.is an information system that provides reports to stakeholders3. Using accrual accounting, expenses are recorded and reported onlya.when they are incurred, whether or not cash is paid4. The measurement bases exclude( )c.Sale price5. Debts owed by a business are referred to as()d.liabilities6. Which of the following financial statements reports information as of a specific datec.balance sheet7. Cash investments made by the owner to the business are reported on the statement of cash flows in thea.financing activities section8. The accounting equation may be expressed asd.Assets - Liabilities = Owner's Equity9. Which of the following groups of accounts have a normal credit balancea.revenues, liabilities, capital10. Which of the following groups of accounts have a normal debit balanced.assets, expenses11. Which of the following types of accounts have a normal credit balancec.revenues and liabilities12. In the accounting cycle, the last step is()a.preparing a post-closing trial balance13. Which of the following should not be considered cash by an accountantc.postage stamps14. A bank reconciliation should be prepared periodically because ()c.any differences between the depositor's records and thebank's records should be determined, and any errors made byeither party should be discovered and corrected15. The amount of the outstanding checks is included on the bank reconciliationas a(n) ()c.deduction from the balance per bank statement16. The asset created by a business when it makes a sale on account is termedc.accounts receivable17. What is the type of account and normal balance of Allowance for Doubtful Accountsa.Contra asset, credit18. The term "inventory" indicates ()d.both A and B19. Merchandise inventory at the end of the year was understated. Which of the following statements correctly states the effect of the error income is understated20.Merchandise inventory at the end of the year is overstated. Which of the following statements correctly states the effect of the errorb.owner's equity is overstated21.The inventory method that assigns the most recent costs to cost of good sold isb.LIFO22.Under which method of cost flows is the inventory assumed to be composed of the most recent costsb.first-in, first-out23. When the perpetual inventory system is used, the inventory sold is debited to ( )b.cost of merchandise sold24.All of the following below are needed for the calculation of depreciation exceptd.book value25. A characteristic of a fixed asset is that it ised in the operations of a business26. Accumulated Depreciation ( )c.is a contra asset account27. The two methods of accounting for investments in stock are the cost method and the ()b.equity method28. A capital expenditure results in a debit to ()d.an asset account29. Current liabilities are()d.due and payable within one year30. The debt created by a business when it makes a purchase on account is referred to as anb.account payable31. Notes may be issued ()d.all of the above32.The cost of a product warranty should be included as an expense in thec.period of the sale of the product33. If the market rate of interest is 8%, the price of 6% bonds paying interest semiannually with a face value of $100,000 will bec.Less than $100,00034. The interest rate specified in the bond indenture is called the ()b.contract rate35. When the corporation issuing the bonds has the right to repurchase the bonds prior to the maturity date for a specific price, the bonds ared.callable bonds36. When the market rate of interest on bonds is higher than the contract rate, the bonds will sell atd. a discount37. One potential advantage of financing corporations through the use of bonds rather than common stock isc.the interest expense is deductible for tax purposes by thecorporation38. Characteristics of a corporation include ()d.shareholders who have limited liability39. Stockholders' equity ()c.includes retained earnings and paid-in capital40. The excess of issue price over par of common stock is termed a(n) ()d.premium41. Cash dividends are usually not paid on which of the followingc.treasury stock42. Which of the following accounts below is reported in the paid-in capital/stockholders' equity section of the corporate balance sheetd.Preferred Stock43. If preferred stock has dividends in arrears, the preferred stock must bed.convertible44. The primary purpose of a stock split is tob.reduce the market price of the stock per share45. Which statement below is not a reason for a corporation to buy back its own stock.d.to increase the shares outstanding46. The liability for a dividend is recorded on which of the following datesd.the date of declaration47. In credit terms of 2/10, n/30, the "2" represents thed.percent of the cash discount48. Revenue should be recognized when()b.the service is performed49. The ability of a business to pay its debts as they come due and to earn a reasonable amount of income is referred to as ()b.solvency and profitability50. Which of the following is not included in the computation of the quick ratioa.inventory四、问答题:3.Differentiate between financial accounting and managerial accounting.财务会计与管理会计的区别。

会计学位英语资料

会计学位英语资料1. Introduction to AccountingAccounting is a fundamental discipline in business and finance. It involves the process of recording, analyzing, and interpreting financial transactions of an organization. Accountants play a critical role in providing financial information that is used by decision-makers for various purposes, such as assessing the financial health ofa company, making investment decisions, and ensuring compliance with relevant regulations. 2. Overview of Accounting PrinciplesIn order to ensure consistency and reliability in financial reporting, there are generally accepted accounting principles (GAAP) that need to be followed. These principles govern the recognition, measurement, and presentation of financial information. Some key accounting principles include the accrual basis of accounting, thematching principle, and the principle of conservatism.3. Financial StatementsFinancial statements are the primary means of communicating financial information to external users. There are four mn types of financial statements: the balance sheet, the income statement, the cash flow statement, and the statement of changes in equity. Each statement provides different insights into the financial position and performance of a company.•The balance sheet presents the assets, liabilities, and equity of a company at a specific point in time.•The income statement summarizes the revenue, expenses, and net income of a company during a specific period.•The cash flow statement provides information about the cash inflows and outflows of a company during a specific period. •The statement of changes in equity shows the changes in equity during a specific period,including contributions, distributions, and net income.4. Understanding Financial RatiosFinancial ratios are used to assess the financial health and performance of a company. They provide insights into various aspects, such as liquidity, profitability, and solvency. Some commonly used financial ratios include the current ratio, the return on equity, and the debt-to-equity ratio. These ratios help analysts andinvestors evaluate the financial stability and potential risks of a company.5. International Financial Reporting Standards (IFRS)In addition to GAAP, there is another set of accounting standards called International Financial Reporting Standards (IFRS). These standards are used in many countries around the world, with the m of enhancing comparability and transparency in financial reporting. IFRS covers a wide range of topics, including revenuerecognition, lease accounting, and financial instruments.6. Professional Ethics in AccountingEthics plays a crucial role in the accounting profession. Accountants are expected to adhere to a code of professional ethics to mntn integrity and objectivity in their work. Some key ethical principles include confidentiality, professional competence, and independence. Violation of these principles can result in severe consequences, such as loss of reputation and legal implications.7. Career Opportunities in AccountingA degree in accounting opens up various career opportunities. Accountants can work in public accounting firms, private corporations, government agencies, and non-profit organizations. Some common job roles in the accounting field include financial analyst, auditor, tax accountant, and management accountant. The demand for accounting professionals is expected to remn strong, as businesses require skilled individuals to handle their financial affrs.ConclusionIn conclusion, obtning a degree in accounting provides a solid foundation for a career in finance. The knowledge and skills gned through an accounting program can be applied in a wide range of industries and sectors. Understanding accounting principles, financial statements, and ethical considerations are essential for aspiring accountants. By keeping up with the latest developments in accounting standards and staying vigilant about professional ethics,accountants can contribute to the success and stability of organizations.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

一.汉译英练习1.会计原则是每个会计人员在进行工作时必须遵守的规则。

2.编制会计分录是在会计期间经常要做的工作。

3.编制工作底稿是每个会计期末要做的工作。

4.实账户是负债表账户。

在月末,它们的余额应不被结平,而转入下一期。

5.虚账户是利润表账户。

在月末,它们的余额应结平,以便用来记录下一期的经营成果。

6.这个月费用很大,我们要查一下原因,分析一下有关经济业务。

7.如果销售商品时,若客户没有付现金,则这种销售被称为赊销。

8.赊销时,卖方会对卖方提出付款条件,这个条件被称为信用条件。

9.固定资产每月都必须计提折旧。

10.无形资产每月计提摊销。

11.企业外部的许多人关心企业的财务信息,而及时提供财务信息给他们是会计的工作。

12.财务报表是人们进行经营决策的依据之一。

13.我们必须准备足够的资金,这笔贷款下个月到期。

14.调整分录与结账分录必须计入日记账和分类账,否则账上的余额会与报表上数额不符。

15.在西方会计中,股份公司的权益科目与独资企业的权益科目是不同的。

16.销售商品的收入常被称为是销售收入。

17.本年利润是用于计算利润的账户,他与其他损益类科目一样,年末,都要被结平。

18.请给我看一下有关这个月应缴的税费的数据二.会计专业词汇练习会计词汇辨析()Dividends ()Cash()Inventory ()Accumulated depreciation()Accounts receivable ()Interest payable()Income taxes payable ()Owner’s capital()Retained earnings ()Closing entry()Journalizing ()Administrative expenses()Cost of goods sold ()Net income()Business transaction ()Unearned revenues()Ending balance ()Financial expenses()Prepaid expenses ()operating results()Withdrawals ()Sales( )Allowance for bad accounts ()Common stock()Office supplies inventory ()long-term bonds investments ()Accounts payable ()Cash basis accounting()Office equipments ()Posting()Beginning balance ()Business transaction()Trial balance ()Financial statements()Selling expenses. ()Financial position()Marketable securities ( ) paid in capital( ) operating equipments ()Notes payable( ) Short term investment ( ) Gain()Extraordinary items ()Finished products()Salary expenses ()Interest receivable()Accrual basis accounting ()Income statements()Adjusting entry ()Intangible assets( ) Source documents ( ) Gross sales( ) Purchase ( ) Fixed assets1.期末余额28. 坏账准备2.应付所得税29. 应收账款3.销售费用30. 主营业务收入4.业主资本31. 经营成果5.主营业务成本32 管理费用6.应付利息33 存货7.留存收益34 调整分录8.预收账款35 结账分录9.累计折旧36 权责发生制10.经济业务37 应付票据11.财务报表38 编制分录12.试算平衡39. 期初余额13.现金收付制40. 应付账款14.财务费用41. 净利润15.普通股42. 财务状况16.营业外收支项目43. 过账17.应收利息44 办公用品库存18.实收资本45. 办公设备19.库存46. 股利20.经营设备47. 业主提取21.利得48. 产成品22.待摊费用49. 交易性金融资产23.长期债券投资50. 短期投资24.无形资产51. 工资费用25.生产设备52销售总额26.原始凭证53 固定资产27.采购54. 工资费用三.英译汉1.Revenue is the price of goods sold and services rendered during a given accounting period. Earning revenue causes owner’s equity to increase. When a business renders services of sells merchandise to its customers, it usually receives cash or acquires an account receivable from the customer.2.To clearly identify the effects of the business operations on each of the accounting elements, it is necessary to transfer those records from journal to each corresponding books used for recording different accounting element. This transfer process is called “posting”.3.The journal is a day-by-day record of business transactions. The information recorded about each transaction includes the date of the transaction, the debit and credit changes in specific ledger accounts, and a brief explanation of the transaction.4.The things a business owns can be classified into five categories, which also called accounting elements, they are: assets, liabilities, owners' equity, revenues, and expenses. Every business transaction of the business may affect more than one of the above elements。

5. A set of financial statements consists of four related accounting reports that summarize in a few pages the financial resources, obligations, profitability, and cash transactions of a business. A complete set of financial statements includes:1 a balance sheet,2 an income statement3 a statement of owner”s equity,4 a statement of cash flows6.At the end of each period,the balance of each nominal account is closed to one account called “Income Summary”,and in turn the net result of the income summery (i.e., net income or net loss) is transferred from “Income Summary” account to owners’ equity account. These transferring process is called closing process, which can make the balance of the nominal accounts be zero, so they will be ready for reuse the next period.7.Liabilities are debts. All business concerns have liabilities; The liability arising form the purchase of goods or services on credit is called an account payable, and the person or company to whom the account payable is owed is called a creditor.9.Accounting is a kind of specific information processing system, in which all the monetary business transactions of a company and their economic effects on that company occurred in certain operating period are collected, recorded, classified, summarized, and reported. The people who conduct such work are called accountants.10。

During a given time period, changes in owners' equity result from the following factors:1). Investments by the owners,2). Withdrawals by the owners or the payment of owner’s dividends。