上海对外贸易学院财管中加财务报表分析期中考试(答案见其他word)

上海对外贸易财管中加国际财务管理C11期末简答题答案

CHAPTER 11 INTERNATIONAL BANKINGSUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTERQUESTIONS AND PROBLEMSQUESTIONS1. Briefly discuss some of the services that international banks provide their customers and the market place.Answer: International banks can be characterized by the types of services they provide that distinguish them from domestic banks. Foremost, international banks facilitate the imports and exports of their clients by arranging trade financing. Additionally, they serve their clients by arranging for foreign exchange necessary to conduct cross-border transactions and make foreign investments and by assisting in hedging exchange rate risk in foreign currency receivables and payables through forward and options contracts. Since international banks have established trading facilities, they generally trade foreign exchange products for their own account.Two major features that distinguish international banks from domestic banks are the types of deposits they accept and the loans and investments they make. Large international banks both borrow and lend in the Eurocurrency market. Moreover, depending upon the regulations of the country in which it operates and its organizational type, an international bank may participate in the underwriting of Eurobonds and foreign bonds.International banks frequently provide consulting services and advice to their clients in the areas of foreign exchange hedging strategies, interest rate and currency swap financing, and international cash management services. Not all international banks provide all services. Banks that do provide a majority of these services are known as universal banks or full service banks.2. Briefly discuss the various types of international banking offices.Answer: The services and operations which an international bank undertakes is a function of the regulatory environment in which the bank operates and the type of banking facility established.A correspondent bank relationship is established when two banks maintain a correspondent bank account with one another. The correspondent banking system provides a means for a bank’s MNC clients to conduct business worldwide through his local bank or its contacts.IM-1A representative office is a small service facility staffed by parent bank personnel that is designed to assist MNC clients of the parent bank in its dealings with the bank’s correspondents. It is a way for the parent bank to provide its MNC clients with a level of service greater than that provided through merely a correspondent relationship.A foreign branch bank operates like a local bank, but legally it is a part of the parent bank. As such, a branch bank is subject to the banking regulations of its home country and the country in which it operates. The primary reason a parent bank would establish a foreign branch is that it can provide a much fuller range of services for its MNC customers through a branch office than it can through a representative office.A subsidiary bank is a locally incorporated bank that is either wholly owned or owned in major part by a foreign subsidiary. An affiliate bank is one that is only partially owned, but not controlled by its foreign parent. Both subsidiary and affiliate banks operate under the banking laws of the country in which they are incorporated. U.S. parent banks find subsidiary and affiliate banking structures desirable because they are allowed to engage in security underwriting.Edge Act banks are federally chartered subsidiaries of U.S. banks which are physically located in the United States that are allowed to engage in a full range of international banking activities. A 1919 amendment to Section 25 of the Federal Reserve Act created Edge Act banks. The purpose of the amendment was to allow U.S. banks to be competitive with the services foreign banks could supply their customers. Federal Reserve Regulation K allows Edge Act banks to accept foreign deposits, extend trade credit, finance foreign projects abroad, trade foreign currencies, and engage in investment banking activities with U.S. citizens involving foreign securities. As such, Edge Act banks do not compete directly with the services provided by U.S. commercial banks. Edge Act banks are not prohibited from owning equity in business corporations as are domestic commercial banks. Thus, it is through the Edge Act that U.S. parent banks own foreign banking subsidiaries and have ownership positions in foreign banking affiliates.An offshore banking center is a country whose banking system is organized to permit external accounts beyond the normal economic activity of the country. Offshore banks operate as branches or subsidiaries of the parent bank. The primary activities of offshore banks are to seek deposits and grant loans in currencies other than the currency of the host government.In 1981, the Federal Reserve authorized the establishment of International Banking Facilities (IBF). An IBF is a separate set of asset and liability accounts that are segregated on the parent bank’s books; it is not a unique physical or legal entity. IBFs operate as foreign banks in the U.S. IBFs were established largely as a result of the success of offshore banking. The Federal Reserve desired to return a large share of the deposit and loan business of U.S. branches and subsidiaries to the U.S.IM-23. How does the deposit-loan rate spread in the Eurodollar market compare with the deposit-loan rate spread in the domestic U.S. banking system? Why?Answer: Competition has driven the deposit-loan spread in the domestic U.S. banking system to about the same level as in the Eurodollar market. That is, in the Eurodollar market the deposit rate is about the same as the deposit rate for dollars in the U.S. banking system. Similarly the lending rates are about the same. In theory, the Eurodollar market can operate at a lower cost than the U.S. banking system because it is not subject to mandatory reserve requirements on deposits or deposit insurance on foreign currency deposits.4. What is the difference between the Euronote market and the Eurocommercial paper market?Answer: Euronotes are short-term notes underwritten by a group of international investment or commercial banks called a “facility.” A client-borrower makes an agreement with a facility to issue Euronotes in its own name for a period of time, generally three to 10 years. Euronotes are sold at a discount from face value, and pay back the full face value at maturity. Euronotes typically have maturities of from three to six months. Eurocommercial paper is an unsecured short-term promissory note issued by a corporation or a bank and placed directly with the investment public through a dealer. Like Euronotes, Eurocommercial paper is sold at a discount from face value. Maturities typically range from one to six months.5. Briefly discuss the cause and the solution(s) to the international bank crisis involving less-developed countries.Answer: The international debt crisis began on August 20, 1982 when Mexico asked more than 100 U.S. and foreign banks to forgive its $68 billion in loans. Soon Brazil, Argentina and more than 20 other developing countries announced similar problems in making the debt service on their bank loans. At the height of the crisis, Third World countries owed $1.2 trillion!The international debt crisis had oil as its source. In the early 1970s, the Organization of Petroleum Exporting Countries (OPEC) became the dominant supplier of oil worldwide. Throughout this time period, OPEC raised oil prices dramatically and amassed a tremendous supply of U.S. dollars, which was the currency generally demanded as payment from the oil importing countries.OPEC deposited billions in Eurodollar deposits; by 1976 the deposits amounted to nearly $100 billion. Eurobanks were faced with a huge problem of lending these funds in order to generate interestIM-3income to pay the interest on the deposits. Third World countries were only too eager to assist the equally eager Eurobankers in accepting Eurodollar loans that could be used for economic development and for payment of oil imports. The high oil prices were accompanied by high interest rates, high inflation, and high unemployment during the 1979-1981 period. Soon, thereafter, oil prices collapsed and the crisis was on.Today, most debtor nations and creditor banks would agree that the international debt crisis is effectively over. U.S. Treasury Secretary Nicholas F. Brady of the first Bush Administration is largely credited with designing a strategy in the spring of 1989 to resolve the problem. Three important factors were necessary to move from the debt management stage, employed over the years 1982-1988 to keep the crisis in check, to debt resolution. First, banks had to realize that the face value of the debt would never be repaid on schedule. Second, it was necessary to extend the debt maturities and to use market instruments to collateralize the debt. Third, the LDCs needed to open their markets to private investment if economic development was to occur. Debt-for-equity swaps helped pave the way for an increase in private investment in the LDCs. However, monetary and fiscal reforms in the developing countries and the recent privatization trend of state owned industry were also important factors.Treasury Secretary Brady’s solution was to offer creditor banks one of three alternatives: (1) convert their loans to marketable bonds with a face value equal to 65 percent of the original loan amount; (2) convert the loans into collateralized bonds with a reduced interest rate of 6.5 percent; or, (3) lend additional funds to allow the debtor nations to get on their feet. The second alternative called for an extension the debt maturities by 25 to 30 years and the purchase by the debtor nation of zero-coupon U.S. Treasury bonds with a corresponding maturity to guarantee the bonds and make them marketable. These bonds have come to be called Brady bonds.6. What warning did David Hume, the 18th-century Scottish philosopher-economist, give about lending to sovereign governments?Answer: (From the February 21, 1989 article “LDC Lenders Should Have Listened To David Hume” by Thomas M. Humphrey in The Wall Street Journal.)Hume thought no good could result from borrowing:If the abuses of treasures [held by the state] be dangerous by engaging the state in rash enterprise in confidence of its riches; the abuses of mortgaging are more certain and inevitable: poverty, impotence, and subjection to foreign powers.Nations, presuming they can find the necessary lenders, are tempted to borrow without limit and to squander the funds on unproductive projects:IM-4It is very tempting to a minister to employ such an expedient as enables him to make a great figure during his administration without over burthening the people with taxes or exciting any immediate clamorous against himself. The practice, therefore, of contracting debt will almost infallibly be abused in every government. It would scarcely be more imprudent to give a prodigal son a credit in every banker’s shop in London than to empower a statesman to draw bills in this manner upon posterity.Eventually, however, interest must be paid and the burden of debt service charges will fall heavily on the poor:The taxes which are levied to pay the interest of these debts are . . . an oppression on the poorer sort.Those same taxes “hurt commerce and discourage industry” and thus inhibit economic development and condemn the borrowing nation to continuing poverty. The debt burden will also pauperize the prosperous merchant and landowning classes that constitute the main bulwark of political freedom and stability. With the pauperization of the middle class:No expedient at all remains for resisting tyranny: Elections are swayed by bribery and corruption alone: And the middle power between king and people being totally removed, a grievous despotism must infallibly prevail. The landholders [and merchants] despised for their oppressions, will be utterly unable to make any opposition to it.7. What are the approaches available to an internationally active bank for valuing its credit risk under Basel II.Answer: For valuing credit risk, banks may choose among the standardized approach, the internal rating-based (IRB) approach, and the securitization approach. The standardized approach provides for risk-weighting assets from five categories based on external credit agencies assessments of the credit risk inherent in the asset. The IRB approach allows banks that have received supervisory approval to rely on their own internal estimates of risk in determining the capital requirement for a given exposure. The key variables the bank must estimate to value credit risk under this approach are the probability of default and the loss given default for each asset. The securitization approach provides for determining the securitized value of a cash flow stream and then risk-weighting the value according to the standardized approach or (if the bank has received supervisory approval) by applying the IRB approach to determine the capital requirement.IM-5PROBLEMS1. Grecian Tile Manufacturing of Athens, Georgia, borrows $1,500,000 at LIBOR plus a lending margin of 1.25 percent per annum on a six-month rollover basis from a London bank. If six-month LIBOR is 4 ½ percent over the first six-month interval and 5 3/8 percent over the second six-month interval, how much will Grecian Tile pay in interest over the first year of its Eurodollar loan?Solution: $1,500,000 x (.045 + .0125)/2 + $1,500,000 x (.05375 + .0125)/2= $43,125 + $49,687.50 = $92,812.50.2. A bank sells a “three against six” $3,000,000 FRA for a three-month period beginning three months from today and ending six months from today. The purpose of the FRA is to cover the interest rate risk caused by the maturity mismatch from having made a three-month Eurodollar loan and having accepted a six-month Eurodollar deposit. The agreement rate with the buyer is 5.5 percent. There are actually 92 days in the three-month FRA period. Assume that three months from today the settlement rate is 4 7/8 percent. Determine how much the FRA is worth and who pays who--the buyer pays the seller or the seller pays the buyer.Solution: Since the settlement rate is less than the agreement rate, the buyer pays the seller the absolute value of the FRA. The absolute value of the FRA is:$3,000,000 x [(.04875-.055) x 92/360]/[1 + (.04875 x 92/360)]= $3,000,000 x [-.001597/(1.012458)]= $4,732.05.3. Assume the settlement rate in problem 2 is 6 1/8 percent. What is the solution now?Solution: Since the settlement rate is greater than the agreement rate, the seller pays the buyer the absolute value of the FRA. The absolute value of the FRA is:$3,000,000 x [(.06125-.055) x 92/360]/[1 + (.06125 x 92/360)]= $3,000,000 x [.001597/(1.015653)]= $4,717.16.IM-64. A “three-against-nine” FRA has an agreement rate of 4.75 percent. You believe six-month LIBOR in three months will be5.125 percent. You decide to take a speculative position in a FRA with a $1,000,000 notional value. There are 183 days in the FRA period. Determine whether you should buy or sell the FRA and what your expected profit will be if your forecast is correct about the six-month LIBOR rate.Solution: Since the agreement rate is less than your forecast, you should buy a FRA. If your forecast is correct your expected profit will be:$1,000,000 x [(.05125-.0475) x 183/360]/[1 + (.05125 x 183/360)]= $1,000,000 x [.001906/(1.026052)]= $1,857.61.IM-7。

2022年上海对外经贸大学财务管理专业《管理学》科目期末试卷B(有答案)

2022年上海对外经贸大学财务管理专业《管理学》科目期末试卷B(有答案)一、选择题1、如下选项中哪个不属于影响计划工作的权变因素?()A.组织的层次B.权力的大小C.环境的不确定性D.未来投入的持续时间2、以下哪一个不是激发组织创新力的因素?()A.结构因素 B.人力资源因素C.技术因素 D.文化因素3、一家公司董事会通过决议,计划在重庆建立汽车制造厂,建设周期为一年,需完成基础建设、设备安装、生产线调试等系列工作,()技术最适合来协调各项活动的资源分配。

A.甘特图B.负荷图C.PERT网络分析D.线性规划4、沸光广告公司是一家大型广告公司,业务包括广告策划、制作和发行。

考虑到一个电视广告设计至少要经过创意、文案、导演、美工、音乐合成、制作等专业的合作才能完成,下列何种组织结构能最好的支撑沸光公司的业务要求?()A.直线式B.职能制C.矩阵制D.事业部制5、下列选项中哪个不属于“组织”(organization)所共同具有的三个特性?()A.明确的目的或目标 B.精细的结构C.文化 D.人员6、在不确定情况下,除了有限信息的影响之外,另一个影响决策结果的因素是()。

A.风险性 B.环境的复杂性C.决策者心理定位 D.决策的时间压力7、()是第一个将管理定义为一组普遍适用的职能的人,他认为管理是人类所从事的一种共同活动。

A.明茨伯格B.法约尔C.德鲁克D.韦伯8、“奖金”在双因素理论中称为()。

A.保健因素B.激励因素C.满意因素D.不满意因素9、企业选择产业中的一个或者一组细分市场,制定专门的战略向此市场提供产品或者服务,这是典型的()。

A.增长型战略 B.别具一格战略 C.专一化战略 D.公司层战略10、以下哪一种组织结构违背了“统一指挥”的组织原则?()A.直线职能制 B.直线职能辅以参谋职能制C.事业部制 D.矩阵制二、名词解释11、强文化12、程序化决策13、领导者(leader)与管理者(manager)14、组织发展15、学习型组织16、组织结构17、竞争优势和竞争战略18、管理方格理论三、简答题19、什么联邦法律对员工多样性的创新措施非常重要?20、什么是组织绩效?21、简述泰勒科学管理理论的主要内容。

上海对外贸易财管中加国际财务管理C9期末简答题答案

CHAPTER 9 MANAGEMENT OF ECONOMIC EXPOSURESUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTERQUESTIONS AND PROBLEMSQUESTIONS1. How would you define economic exposure to exchange risk?Answer: Economic exposure can be defined as the possibility that the firm’s cash flows and thus its market value may be affected by the unexpected exchange rate changes.2. Explain the following statement: “Exposure is the regression coefficient.”Answer: Exposure to currency risk can be appropriately measured by the sensitivity of the firm’s future cash flows and the market value to random changes in exchange rates. Statistically, this sensitivity can be estimated by the regression coefficient. Thus, exposure can be said to be the regression coefficient.3. Suppose that your company has an equity position in a French firm. Discuss the condition under which the dollar/franc exchange rate uncertainty does not constitute exchange exposure for your company.Answer: Mere changes in exchange rates do not necessarily constitute currency exposure. If the French franc value of the equity moves in the opposite direction as much as the dollar value of the franc changes, then the dollar value of the equity position will be insensitive to exchange rate movements. As a result, your company will not be exposed to currency risk.4. Explain the competitive and conversion effects of exchange rate changes on the firm’s operating cash flow.Answer: The competitive effect: exchange rate changes may affect operating cash flows by altering the firm’s competitive position.The conversion effect: A given operating cash flows in terms of a foreign currency will be converted into higher or lower dollar (home currency)amounts as the exchange rate changes.IM-15. Discuss the determinants of operating exposure.Answer: The main determinants of a firm’s operating exposure are (1) the structure of the markets in which the firm sources its inputs, such as labor and materials, and sells its products, and (2) the firm’s ability to mitigate the effect of exchange rate changes by adjusting its markets, product mix, and sourcing.6. Discuss the implications of purchasing power parity for operating exposure.Answer: If the exchange rate changes are matched by the inflation rate differential between countries, firms’ competitive positions will not be altered by exchange rate changes. Firms are not subject to operating exposure.7. General Motors exports cars to Spain but the strong dollar against the peseta hurts sales of GM cars in Spain. In the Spanish market, GM faces competition from the Italian and French car makers, such as Fiat and Renault, whose currencies remain stable relative to the peseta. What kind of measures would you recommend so that GM can maintain its market share in Spain.Answer: Possible measures that GM can take include: (1) diversify the market; try to market the cars not just in Spain and other European countries but also in, say, Asia; (2) locate production facilities in Spain and source inputs locally; (3) locate production facilities, say, in Mexico where production costs are low and export to Spain from Mexico.8. What are the advantages and disadvantages of financial hedging of the firm’s operating exposure vis-à-vis operational hedges (such as relocating manufacturing site)?Answer: Financial hedging can be implemented quickly with relatively low costs, but it is difficult to hedge against long-term, real exposure with financial contracts. On the other hand, operational hedges are costly, time-consuming, and not easily reversible.9. Discuss the advantages and disadvantages of maintaining multiple manufacturing sites as a hedge against exchange rate exposure.Answer: To establish multiple manufacturing sites can be effective in managing exchange risk exposure, but it can be costly because the firm may not be able to take advantage of the economy of scale.IM-210. Evaluate the following statement: “A firm can reduce its currency exposure by diversifying across different business lines.”Answer: Conglomerate expansion may be too costly as a means of hedging exchange risk exposure. Investment in a different line of business must be made based on its own merit.11. The exchange rate uncertainty may not necessarily mean that firms face exchange risk exposure. Explain why this may be the case.Answer: A firm can have a natural hedging position due to, for example, diversified markets, flexible sourcing capabilities, etc. In addition, to the extent that the PPP holds, nominal exchange rate changes do not influence firms’ competitive positions. Under these circumstances, firms do not need to worry about exchange risk exposure.IM-3PROBLEMS1. Suppose that you hold a piece of land in the City of London that you may want to sell in one year. As a U.S. resident, you are concerned with the dollar value of the land. Assume that, if the British economy booms in the future, the land will be worth £2,000 and one British pound will be worth $1.40. If the British economy slows down, on the other hand, the land will be worth less, i.e., £1,500, but the pound will be stronger, i.e., $1.50/£. You feel that the British economy will experience a boom with a 60% probability and a slow-down with a 40% probability.(a) Estimate your exposure b to the exchange risk.(b) Compute the variance of the dollar value of your property that is attributable to the exchange rate uncertainty.(c) Discuss how you can hedge your exchange risk exposure and also examine the consequences of hedging.Solution: (a) Let us compute the necessary parameter values:E(P) = (.6)($2800)+(.4)($2250) = $1680+$900 = $2,580E(S) = (.6)(1.40)+(.4)(1.5) = 0.84+0.60 = $1.44Var(S) = (.6)(1.40-1.44)2 + (.4)(1.50-1.44)2= .00096+.00144 = .0024.Cov(P,S) = (.6)(2800-2580)(1.4-1.44)+(.4)(2250-2580)(1.5-1.44)= -5.28-7.92 = -13.20b = Cov(P,S)/Var(S) = -13.20/.0024 = -£5,500.You have a negative exposure! As the pound gets stronger (weaker) against the dollar, the dollar value of your British holding goes down (up).(b) b2Var(S) = (-5500)2(.0024) =72,600($)2(c) Buy £5,500 forward. By doing so, you can eliminate the volatility of the dollar value of your British asset that is due to the exchange rate volatility.IM-42. A U.S. firm holds an asset in France and faces the following scenario:State 1 State 2State 3 State 4 Probability 25% 25%25% 25%Spot rate $1.20/€ $1.10/€$1.00/€ $0.90/€P*€1500 €1400€1300 €1200P $1,800 $1,540$1,300 $1,080In the above table, P* is the euro price of the asset held by the U.S. firm and P is the dollar price of the asset.(a) Compute the exchange exposure faced by the U.S. firm.(b) What is the variance of the dollar price of this asset if the U.S. firm remains unhedged against thisexposure?(c) If the U.S. firm hedges against this exposure using the forward contract, what is the variance of thedollar value of the hedged position?Solution: (a)E(S) = .25(1.20 +1.10+1.00+0.90) = $1.05/€E(P) = .25(1,800+1,540+1,300 +1,080) = $1,430Var(S) = .25[(1.20-1.05)2 +(1.10-1.05)2+(1.00-1.05)2+(0.90-1.05)2]= .0125Cov(P,S) = .25[(1,800-1,430)(1.20-1.05) + (1,540-1,430)(1.10-1.05)(1,300-1,430)(1.00-1.05) + (1,080-1,430)(0.90-1.05)]= 30b = Cov(P,S)/Var(S) = 30/0.0125 = €2,400.(b) Var(P) = .25[(1,800-1,430)2+(1,540-1,430)2+(1,300-1,430)2+(1,080-1,430)2]= 72,100($)2.(c) Var(P) - b2Var(S) = 72,100 - (2,400)2(0.0125) = 100($)2.This means that most of the volatility of the dollar value of the French asset can be removed by hedging exchange risk. The hedging can be achieved by selling €2,400 forward.IM-5。

【智慧树知到】《财务报表分析(上海对外经贸大学)》章节测试题及答案2

【智慧树知到】《财务报表分析(上海对外经贸大学)》章节测试题及答案2绪论1、通过财务报表分析可以了解()。

A、企业财务状况B、企业盈利能力C、企业偿债能力D、企业的发展能力正确答案:ABCD第一章测试1、年度报告包括以下哪些内容()。

A、经营情况讨论与分析B、股份变动及股东情况C、公司治理D、财务报告正确答案:ABCD2、财务报表包括以下哪些内容()。

A、资产负债表B、利润表C、现金流量表D、报表附注正确答案:ABCD3、上市公司的信息披露文件主要包括()。

A、招股说明书B、上市公告书C、定期报告D、临时报告正确答案:ABCD4、审计机构的非正常更换可能是公司财务质量不佳甚至是信用资质恶化的重要信号。

()A.正确B.错误正确答案:A5、公司治理不是上市公司财务信息披露强制与监督机制的组成部分。

()A.正确B.错误正确答案:B6、公司的财务报表本质上不是其各种经济活动结果的分类反映。

()A.正确B.错误正确答案:B第二章测试1、在企业编制的会计报表中,反映财务状况变动的报表是资产负债表。

()A.正确B.错误正确答案:A2、决定企业货币资金持有量的因素有哪些?A、企业规模B、所在行业特性C、企业负债结构D、企业融资能力正确答案:ABCD3、影响应收账款坏账风险加大的因素是什么?A、账龄较短B、客户群分散C、信用标准严格D、信用期限较长正确答案:D4、按照我国现行会计准则的规定,确定发出存货成本时不可以采用的方法是什么?A、先进先出法B、后进先出法C、加权平均法D、个别计价法正确答案:B5、下列项目中,属于短期债权项目的是()。

A、融资租赁B、银行长期贷款C、商业信用D、长期债券正确答案:C6、通过资产负债表分析可以达到的目的有()。

A、分析债务的期限结构和数量B、分析资产的结构C、预测企业未来的现金流量D、判断所有者的资本保值增值情况正确答案:ABD第三章测试1、利润表的三大要素包括哪些?A、收入B、费用C、利润D、所得税正确答案:ABC2、下列公式计算正确的是()。

对外经贸大学财务报表分析考试复习-汇总

《财务报告分析》复习一、单选1.企业收益的主要来源是(A经营活动)A.经营活动B.投资活动C.筹资活动D.投资收益2.短期债权包括(C商业信用)。

A.融资租赁B.银行长期贷款C.商业信用D.长期债券3.下列项目中属于长期债权的是(B融资租赁)A.短期贷款B.融资租赁C.商业信用D.短期债券4.资产负债表的附表是(D应交增值税明细表)A.利润分配表B.分部报表C.财务报表附注D.应交增值税明细表5.利润表反映企业的(B经营成果)A.财务状况B.经营成果C.财务状况变动D.现金流动6.我国会计规范体系的最高层次是(C会计法)A.企业会计制度B.企业会计准则C.会计法D.会计基础工作规范7.注册会计师对财务报表的(A公允性)发表意见。

A.公允性B.真实性C.正确性D.完整性8.无形资产应按(D账面价值与可收回金额孰低)计量。

A.实际成本B.摊余价值C.账面价值D.账面价值与可收回金额孰低9.当法定盈余公积达到注册资本的(D50%)时,可以不再计提。

A.5%B.10%C.25%D.50%10.下列各项中(A固定资产净残值)不是影响固定资产净值升降的直接因素。

A.固定资产净残值B.固定资产折旧方法C.折旧年限的变动 D.固定资产减值准备的计提11.股份有限公司经登记注册,形成的核定股本或法定股本,又称为(D注册资本)。

A.实收资本B.股本C.资本公积D.注册资本12.可用于偿还流动负债的流动资产指(C现金)A.存出投资款B.回收期在一年以上的应收款项C.现金D.存出银行汇票存款13.酸性测试比率,实际上就是(D速动比率)A.流动比率B.现金比率C.保守速动比率D.速动比率14.现金类资产是指货币资金和(B短期投资净额)A.存货B.短期投资净额C.应收票据D.一年内到期的长期债权投资15.企业(D有可动用的银行贷款指标)时,可以增加流动资产的实际变现能力。

A.取得应收票据贴现款B.为其他单位提供债务担保C.拥有较多的长期资产D.有可动用的银行贷款指标16.减少企业流动资产变现能力的因素是(B未决诉讼、仲裁形成的或有负债)A.取得商业承兑汇票B.未决诉讼、仲裁形成的或有负债C.有可动用的银行贷款指标D.长期投资到期收回17.企业的长期偿债能力主要取决于(B获利能力)。

财务分析报告期中作业(3篇)

第1篇一、前言随着我国经济的快速发展,企业竞争日益激烈,财务管理在企业运营中的重要性愈发凸显。

财务分析作为财务管理的重要组成部分,对于企业决策者了解企业财务状况、预测企业未来发展趋势具有重要意义。

本报告以某公司为例,对其财务状况进行期中分析,旨在揭示企业存在的问题,为决策者提供参考。

二、公司概况某公司成立于2000年,主要从事XX行业的生产和销售。

经过多年的发展,公司已具备一定的规模和实力,产品远销国内外市场。

截至2021年6月30日,公司总资产为XX亿元,净资产为XX亿元,员工人数为XX人。

三、财务分析指标1. 盈利能力分析(1)毛利率毛利率是指企业销售收入与销售成本的差额与销售收入的比率。

根据某公司2021年上半年的财务数据,毛利率为XX%,较去年同期提高了XX个百分点。

这表明公司在成本控制方面取得了一定的成效。

(2)净利率净利率是指企业净利润与销售收入的比率。

某公司2021年上半年的净利率为XX%,较去年同期提高了XX个百分点。

这说明公司盈利能力有所增强。

2. 运营能力分析(1)应收账款周转率应收账款周转率是指企业在一定时期内收回全部应收账款的速度。

某公司2021年上半年的应收账款周转率为XX次,较去年同期提高了XX次。

这表明公司应收账款回收速度加快,运营效率有所提升。

(2)存货周转率存货周转率是指企业在一定时期内销售存货的速度。

某公司2021年上半年的存货周转率为XX次,较去年同期提高了XX次。

这说明公司存货管理得到加强,存货周转速度加快。

3. 偿债能力分析(1)流动比率流动比率是指企业流动资产与流动负债的比率。

某公司2021年上半年的流动比率为XX%,较去年同期提高了XX个百分点。

这表明公司短期偿债能力有所增强。

(2)速动比率速动比率是指企业速动资产与流动负债的比率。

某公司2021年上半年的速动比率为XX%,较去年同期提高了XX个百分点。

这说明公司短期偿债能力得到提高。

4. 营运资本分析营运资本是指企业流动资产与流动负债的差额。

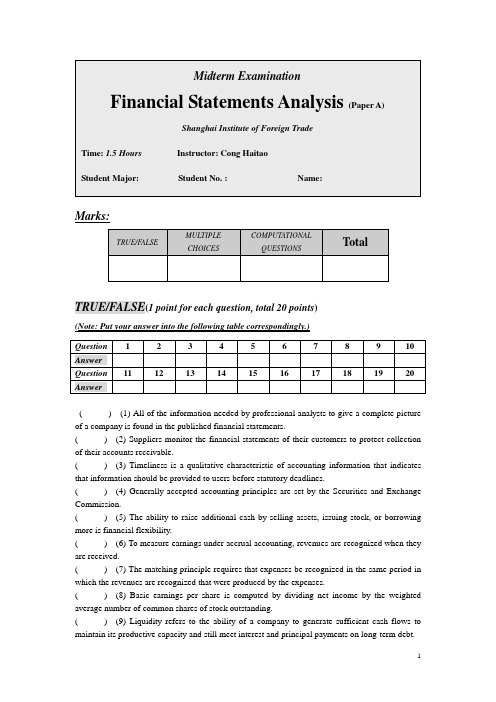

上海对外贸易学院财管中加财务报表分析期中考试(答案见其他word)

Marks:TRUE/FALSE(1 point for each question, total 20 points)(Note: Put your answer into the following table correspondingly.)( ) (1) All of the information needed by professional analysts to give a complete picture of a company is found in the published financial statements.( ) (2) Suppliers monitor the financial statements of their customers to protect collection of their accounts receivable.( ) (3) Timeliness is a qualitative characteristic of accounting information that indicates that information should be provided to users before statutory deadlines.( ) (4) Generally accepted accounting principles are set by the Securities and Exchange Commission.( ) (5) The ability to raise additional cash by selling assets, issuing stock, or borrowing more is financial flexibility.( ) (6) To measure earnings under accrual accounting, revenues are recognized when they are received.( ) (7) The matching principle requires that expenses be recognized in the same period in which the revenues are recognized that were produced by the expenses.( ) (8) Basic earnings per share is computed by dividing net income by the weighted average number of common shares of stock outstanding.( ) (9) Liquidity refers to the ability of a company to generate sufficient cash flows to maintain its productive capacity and still meet interest and principal payments on long-term debt.( ) (10) The change in cash during a period is equal to the net income for the period. ( ) (11) Depreciation is added back to net income to determine cash from operating activities under the indirect method.( ) (12) Current assets are listed on the balance sheet in descending order of liquidity. ( ) (13) The quick ratio measures the most immediate liquidity of a company.( ) (14) Activity ratios describe the profitability of a company.( ) (15) Financial leverage is beneficial when the company earns more than the incremental after-tax cost of debt.( ) (16) Managers’ ability to freely choose among several alternative reporting methods makes it more difficult for a financial analyst to evaluate the activities and condition of a company.( ) (17) Asset turnover is defined as sales divided by total assets.( ) (18) Beginning inventory plus inventory purchases equals cost of goods sold.( ) (19) Dividends paid by a corporation represent a distribution of earnings to stockholders.( ) (20) The direct approach and the indirect approach are two alternative methods of presenting cash flows from investing activities.MULTIPLE CHOICES(1.5 points for each question, total 30 points)(Note: Put your answer into the following table correspondingly.)Which of the following is included in other comprehensive income?A.Unrealized holding gains and losses on trading securities.B.Unrealized holding gains and losses that result from a debt security being transferred into theheld-to-maturity category from the available-for-sale category.C.Foreign currency translation adjustments.D.The difference between the accumulated benefit obligation and the fair value of pensionplan assets.( ) (2) A decrease in net assets arising from peripheral or incidental transactions is called a(n)A.capital expenditure.B.cost.C.loss.D.expense.( ) (3) According to generally accepted accounting principles, revenue should be recognized at the earliest time thatA.the “critical event” has taken place and the proceeds are collected.B.the “critical event” has taken place and the amount of revenue collected is reasonablyassured.C.collection is reasonably assured and the “critical event” can be mea sured.D.collection has taken place and the “critical event” can be measured.( ) (4) How are marketable securities valued on the balance sheet?A.Historical cost.B.At cost or fair value depending on how the securities are classified.C.Market value.D.At fair value with the difference between cost and fair value reported as revenue.( ) (5) Probable future economic benefits obtained or controlled by an entity as a result of past transactions or events defineA.assets.B.liabilities.C.equity.D.retained earnings.( ) (6) Which profit measure is best for assessing how well a firm operates within their industry?A.Gross profit.B.Operating profit.C.Earnings before taxes. profit.( ) (7) Operating and financial flexibility refers to a company’s ability toA.adjust to unexpected downturns in the economic environment in which it operates or totake advantage of profitable investment opportunities as they arise.B.generate sufficient cash flows to maintain its productive capacity and still meet interestand principal payments on long-term debt.C.readily convert assets to cash relative to how soon liabilities will have to paid in cash.D.finance debt in ratio to financing through equity sources.( ) (8) During 2007, Gomez Corporation disposed of Pine Division, a major component of its business. Gomez realized a gain of $1,200,000, net of taxes, on the sale of Pine's assets. Pine's operating losses, net of taxes, were $1,400,000 in 2007. How should these facts be reported in Gomez's income statement for 2007?Total Amount to be Included inIncome from Results ofContinuing Operations Discontinued OperationsA.$1,400,000 loss $1,200,000 gainB.200,000 loss 0C.0 200,000 lossD.1,200,000 gain 1,400,000 loss( ) (9) The amount of income taxes recognized on the income statement but not yetpayable to the government are found on theA.balance sheet in the account Deferred Income Taxes.B.balance sheet in the account Income Taxes Payable.C.income statement in the account Income Tax Expense Current.D.income statement in the account Income Tax Expense Deferred.( ) (10) Net income for Monique Inc. for the fiscal period ended December31, 2005 is $78,000.Its accounts receivable balance at December 31,2005 is $121,000 and it was $69,000 at December31, 2004. Its accounts payable balance at December 31, 2005 is $72,000 and it was $43,000 at December 31, 2004. Depreciation for 2005 is $12,000 and there is an unrealized gain of $15,000 included in 2005 income from the change in value of trading securities. Which of the following amounts represents Monique's cash flow from operations for 2005?A.$52,000.B.$67,000.C.$82,000.D.$98,000.( ) (11) Return on equity using the traditional DuPont formula equals :A.(net profit margin)(interest component)(solvency ratio).B.(net profit margin)(total asset turnover)(tax retention rate).C.(net profit margin)(total asset turnover)(financial leverage multiplier).D.(tax rate)(interest expense rate)(financial leverage multiplier).( ) (12) Financial statements followA.rigid guidelines that require specific adherence to regulated procedures.B.generally accepted guidelines that allow management to choose among differentprocedures.C.general guidelines with little choice among different procedures.D.legal requirements for uniform presentation and disclosure.( ) (13) Published reports of public companies include a description of the company’s business risks, results of operations, financial condition, and future plans for the company known as theA.management discussion and analysis.B.management representation letter.C.President’s message.D.Board of Directors’ analysis.( ) (14) Financial information that is verifiable, faithfully represented, and neutral isA.reliable.B.consistent.parable.D.relevant.( ) (15) Revenues are earned whenA. a contract is signed by both parties.B.the seller substantially completes performance required by an agreement.C.the buyer completes payment required under an agreement.D.the buyer accepts delivery and completes required payments.( ) (16) The bes t measure of a firm’s sustainable income isA.income from continuing operations.B.income before extraordinary items.C.income before extraordinary item and change in accounting principle. income.( ) (17) Working capital accounts includeA.all assets.B.all assets and liabilities.C.current assets and all liabilities.D.current assets and current liabilities.( ) (18) What impact does depreciation have on the cash account?A.Depreciation results in an increase to cash.B.Depreciation results in an decrease to cash.C.Depreciation has no impact on the cash account.D.Depreciation only impacts the cash account if inflation has occurred.( ) (19) The write-off of obsolete equipment would be classified as:A.operating cash flow.B.investment cash flow.C.financing cash flow.D.no cash flow impact.( ) (20) In a common-size balance sheet, each balance sheet is expressed as a percentage of totalA.liabilities.B.assets.C.shareholders’ equity.D.assets plus shareholders’ equity.COMPUTATIONAL QUESTIONS: (25 points each, total 50 points)(Note: Write your answer clearly into the space following each question.)1)Monsanto’s 1994 Annual Report stated that the Chairman and CEO, Richard J. Mahoney, would retire on March 31, 1995. Mahoney’s cash compensation for 1994 consisted of :Salary $950,000 Annual incentive award(based primarily on achieving or exceeding a net income goal) 1,680,000 Total cash compensation $2,630,000In addition, Mahoney participated in a long term compensation plan that granted annual stock option awards if the return on stockholder’s equity exceeded 20%. Monsanto’s reported ROE was Net income = $622 millionOpening stockholders’ equity = $2,855 millionClosing stockholders’ equity = $2,948 millionROE = Net income/average stockholders’ equity = $622/$2,902= 21.4%Excerpts from 1994 Annual Report (in $millions)1994 1993 1992 Net income (loss) $622 $494 ($88)ROE 21.4% 16.9% (2.6%) Note: Restructurings and Other ActionsIn December 1994, the board of directors approved a plan to eliminate redundant staff activities across the company and consolidate certain staff and administrative business functions. The plan will result in reductions in worldwide employment levels of approximately 500 people. In addition, the company will close or exit certain facilities and programs. These workforce reductions and closures will be substantially completed by the end of 1995. The pretax expense related to these actions was $89 million ($55 million after tax).In September 1994, Monsanto received $67 million from the U.S. Internal Revenue Service in settlement of certain tax matters related to the 1985 acquisition of Searle. This settlement included interest of $33 million ($21 million after tax), recorded as a one-time gain. Most of the remainder of the proceeds reduced the balance of unamortized goodwill related to the Searle acquisition….…Restructuring expenses are recorded based on estimates prepared at the time the restructuring actions are approved by the board of directors. In the fourth quarter of 1994, the board approved the reversal of $49 million of pretax excess restructuring reserves from prior years. The excess was primarily due to higher than expected proceeds and lower exit costs from the sale and shutdown of nonstrategic businesses and facilities included in the 1993 and 1992 restructuring actions. The balance in restructuring reserves as of Dec. 31, 1994, was $254 million, and consisted primarily of workforce reduction costs under the 1994 actions and planned facility dismantling and site closure costs remaining under previous restructurings. Management believes that the balance of these reserves as of Dec. 31, 1994, is adequate for completion of those activities….Given the reported ROE of 21.4%, Mahoney was granted options for 275,000 shares at $77.75per share, the market price on the grant date. At the end of November 1995, the market price of Monsanto shares was $120 per share. In exercised and sold, the option would have gained about $11,600,000( $42.25*275,000).ing the information presented, discuss whether Mahoney’s stock option were deserved.Provide at least one argument for and one argument against the option award.b.Discuss whether the nonrecurring events disclosed should be included in managementperformance measures such as ROE.ing the information presented, discuss the expected level of Monsanto’s future incomeand ROE.2)The balance sheet and income statement for the Green Company are presented in the Exhibit 1 .a. Based on the financial statements provided, prepare a statement of cash flows for 2001 using thei) Indirect methodii) Direct methodb. Calculate the company’s free cash flow.EXHIBIT 1 THE GREEN COMPANYBalance Sheet and Income StatementBalance Sheet Income Statement for the YearAs of December 31 2001 2000 Ending December 31,2001Assets Sales $10,000 Cash $1,000 $1,100 Cost of goods sold 6,000 Accounts receivable 1,500 1,650 Depreciation 600 Inventory 2,000 2,200 SG&A 1,000 Total current assets $4,500 $4,95 Interest expense 600Fixed assets—at cost*11,000 12,150 Taxable income $1,800 Accumulated depreciation 4,500 5,100 Taxes 720 Net fixed assets 6,500 7,050 Net income $1,080 Total assets $11,000 $12,000Liabilities and EquityAccrued liabilities $ 800 $880Accounts payable 1,200 1,320Notes payable 5,500 6,050Total current liabilities 7,500 8,250Long-term debt 2,000 1,620Common stock 1,000 1,000Retained earnings 500 1,148Total liabilities and equity $11,000 $12,000* No fixed assets were sold during 1996.。

智慧树知到《财务报表分析(对外经济贸易大学)》章节测试答案

智慧树知到《财务报表分析(对外经济贸易大学)》章节测试答案第一章章节测试1、系统的企业财务报表分析起源于美国银行家对企业进行的所谓决策分析。

()A.正确B.错误正确答案:B2、由以信用分析为重心转变为以投资分析为重心,并非是后者对前者的否定,而是由于资本市场的发展和企业融资来源构成的变化,使得这一时期的财务报表分析是以后者为重心的两者并存状况。

()A.正确B.错误正确答案:A3、企业财务报表分析只是用于外部分析,即企业外部利益相关者根据各自的需求进行分析。

()A.正确B.错误正确答案:B5、财务报表分析就由信用分析阶段进入投资分析阶段,其主要任务也从稳定性分析过渡到收益性分析。

()A.正确B.错误正确答案:A第二章章节测试1、可验证性是指企业的会计处理必须以实际发生的业务为基础,以取得的业务凭证为依据。

这样,就能保证企业的会计处理,从填制记账凭证、登记账簿到编制会计报表等过程都有可靠的凭证为依据,也能保证会计上的帐证、帐帐、帐表和帐实之间的相互一致。

()A.正确B.错误正确答案:B2、相关性原则是指企业提供的会计信息应当与财务会计报告信息使用者的经济决策需要相关,有助于财务会计报告使用者对企业过去、现在或者未来的情况做出评价或者预测。

()A.正确B.错误正确答案:A3、同一企业不同时期发生的相同或者相似的交易或者事项,必须采用一致的会计政策,不得变更。

()A.正确B.错误正确答案:B5、由于收付实现制是以企业实际收付现金的时间为确认收入和费用的基本标准,因而报表中所体现的企业当期经营成果与期末的现金余额相互一致,这样可以使得企业的经营成果具有非常高的含金量和可信度。

()A.正确B.错误正确答案:A第三章章节测试1、企业的行业特点也制约着货币资金规模。

()A.正确B.错误正确答案:A[$]2、企业过高的货币资金规模,一定意味着企业正在丧失潜在的投资机会。

()A.正确B.错误正确答案:B3、企业持有的货币资金规模越大越好。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Marks:TRUE/FALSE(1 point for each question, total 20 points)(Note: Put your answer into the following table correspondingly.)( ) (1) All of the information needed by professional analysts to give a complete picture of a company is found in the published financial statements.( ) (2) Suppliers monitor the financial statements of their customers to protect collection of their accounts receivable.( ) (3) Timeliness is a qualitative characteristic of accounting information that indicates that information should be provided to users before statutory deadlines.( ) (4) Generally accepted accounting principles are set by the Securities and Exchange Commission.( ) (5) The ability to raise additional cash by selling assets, issuing stock, or borrowing more is financial flexibility.( ) (6) To measure earnings under accrual accounting, revenues are recognized when they are received.( ) (7) The matching principle requires that expenses be recognized in the same period in which the revenues are recognized that were produced by the expenses.( ) (8) Basic earnings per share is computed by dividing net income by the weighted average number of common shares of stock outstanding.( ) (9) Liquidity refers to the ability of a company to generate sufficient cash flows to maintain its productive capacity and still meet interest and principal payments on long-term debt.( ) (10) The change in cash during a period is equal to the net income for the period. ( ) (11) Depreciation is added back to net income to determine cash from operating activities under the indirect method.( ) (12) Current assets are listed on the balance sheet in descending order of liquidity. ( ) (13) The quick ratio measures the most immediate liquidity of a company.( ) (14) Activity ratios describe the profitability of a company.( ) (15) Financial leverage is beneficial when the company earns more than the incremental after-tax cost of debt.( ) (16) Managers’ ability to freely choose among several alternative reporting methods makes it more difficult for a financial analyst to evaluate the activities and condition of a company.( ) (17) Asset turnover is defined as sales divided by total assets.( ) (18) Beginning inventory plus inventory purchases equals cost of goods sold.( ) (19) Dividends paid by a corporation represent a distribution of earnings to stockholders.( ) (20) The direct approach and the indirect approach are two alternative methods of presenting cash flows from investing activities.MULTIPLE CHOICES(1.5 points for each question, total 30 points)(Note: Put your answer into the following table correspondingly.)Which of the following is included in other comprehensive income?A.Unrealized holding gains and losses on trading securities.B.Unrealized holding gains and losses that result from a debt security being transferred into theheld-to-maturity category from the available-for-sale category.C.Foreign currency translation adjustments.D.The difference between the accumulated benefit obligation and the fair value of pensionplan assets.( ) (2) A decrease in net assets arising from peripheral or incidental transactions is called a(n)A.capital expenditure.B.cost.C.loss.D.expense.( ) (3) According to generally accepted accounting principles, revenue should be recognized at the earliest time thatA.the “critical event” has taken place and the proceeds are collected.B.the “critical event” has taken place and the amount of revenue collected is reasonablyassured.C.collection is reasonably assured and the “critical event” can be mea sured.D.collection has taken place and the “critical event” can be measured.( ) (4) How are marketable securities valued on the balance sheet?A.Historical cost.B.At cost or fair value depending on how the securities are classified.C.Market value.D.At fair value with the difference between cost and fair value reported as revenue.( ) (5) Probable future economic benefits obtained or controlled by an entity as a result of past transactions or events defineA.assets.B.liabilities.C.equity.D.retained earnings.( ) (6) Which profit measure is best for assessing how well a firm operates within their industry?A.Gross profit.B.Operating profit.C.Earnings before taxes. profit.( ) (7) Operating and financial flexibility refers to a company’s ability toA.adjust to unexpected downturns in the economic environment in which it operates or totake advantage of profitable investment opportunities as they arise.B.generate sufficient cash flows to maintain its productive capacity and still meet interestand principal payments on long-term debt.C.readily convert assets to cash relative to how soon liabilities will have to paid in cash.D.finance debt in ratio to financing through equity sources.( ) (8) During 2007, Gomez Corporation disposed of Pine Division, a major component of its business. Gomez realized a gain of $1,200,000, net of taxes, on the sale of Pine's assets. Pine's operating losses, net of taxes, were $1,400,000 in 2007. How should these facts be reported in Gomez's income statement for 2007?Total Amount to be Included inIncome from Results ofContinuing Operations Discontinued OperationsA.$1,400,000 loss $1,200,000 gainB.200,000 loss 0C.0 200,000 lossD.1,200,000 gain 1,400,000 loss( ) (9) The amount of income taxes recognized on the income statement but not yetpayable to the government are found on theA.balance sheet in the account Deferred Income Taxes.B.balance sheet in the account Income Taxes Payable.C.income statement in the account Income Tax Expense Current.D.income statement in the account Income Tax Expense Deferred.( ) (10) Net income for Monique Inc. for the fiscal period ended December31, 2005 is $78,000.Its accounts receivable balance at December 31,2005 is $121,000 and it was $69,000 at December31, 2004. Its accounts payable balance at December 31, 2005 is $72,000 and it was $43,000 at December 31, 2004. Depreciation for 2005 is $12,000 and there is an unrealized gain of $15,000 included in 2005 income from the change in value of trading securities. Which of the following amounts represents Monique's cash flow from operations for 2005?A.$52,000.B.$67,000.C.$82,000.D.$98,000.( ) (11) Return on equity using the traditional DuPont formula equals :A.(net profit margin)(interest component)(solvency ratio).B.(net profit margin)(total asset turnover)(tax retention rate).C.(net profit margin)(total asset turnover)(financial leverage multiplier).D.(tax rate)(interest expense rate)(financial leverage multiplier).( ) (12) Financial statements followA.rigid guidelines that require specific adherence to regulated procedures.B.generally accepted guidelines that allow management to choose among differentprocedures.C.general guidelines with little choice among different procedures.D.legal requirements for uniform presentation and disclosure.( ) (13) Published reports of public companies include a description of the company’s business risks, results of operations, financial condition, and future plans for the company known as theA.management discussion and analysis.B.management representation letter.C.President’s message.D.Board of Directors’ analysis.( ) (14) Financial information that is verifiable, faithfully represented, and neutral isA.reliable.B.consistent.parable.D.relevant.( ) (15) Revenues are earned whenA. a contract is signed by both parties.B.the seller substantially completes performance required by an agreement.C.the buyer completes payment required under an agreement.D.the buyer accepts delivery and completes required payments.( ) (16) The bes t measure of a firm’s sustainable income isA.income from continuing operations.B.income before extraordinary items.C.income before extraordinary item and change in accounting principle. income.( ) (17) Working capital accounts includeA.all assets.B.all assets and liabilities.C.current assets and all liabilities.D.current assets and current liabilities.( ) (18) What impact does depreciation have on the cash account?A.Depreciation results in an increase to cash.B.Depreciation results in an decrease to cash.C.Depreciation has no impact on the cash account.D.Depreciation only impacts the cash account if inflation has occurred.( ) (19) The write-off of obsolete equipment would be classified as:A.operating cash flow.B.investment cash flow.C.financing cash flow.D.no cash flow impact.( ) (20) In a common-size balance sheet, each balance sheet is expressed as a percentage of totalA.liabilities.B.assets.C.shareholders’ equity.D.assets plus shareholders’ equity.COMPUTATIONAL QUESTIONS: (25 points each, total 50 points)(Note: Write your answer clearly into the space following each question.)1)Monsanto’s 1994 Annual Report stated that the Chairman and CEO, Richard J. Mahoney, would retire on March 31, 1995. Mahoney’s cash compensation for 1994 consisted of :Salary $950,000 Annual incentive award(based primarily on achieving or exceeding a net income goal) 1,680,000 Total cash compensation $2,630,000In addition, Mahoney participated in a long term compensation plan that granted annual stock option awards if the return on stockholder’s equity exceeded 20%. Monsanto’s reported ROE was Net income = $622 millionOpening stockholders’ equity = $2,855 millionClosing stockholders’ equity = $2,948 millionROE = Net income/average stockholders’ equity = $622/$2,902= 21.4%Excerpts from 1994 Annual Report (in $millions)1994 1993 1992 Net income (loss) $622 $494 ($88)ROE 21.4% 16.9% (2.6%) Note: Restructurings and Other ActionsIn December 1994, the board of directors approved a plan to eliminate redundant staff activities across the company and consolidate certain staff and administrative business functions. The plan will result in reductions in worldwide employment levels of approximately 500 people. In addition, the company will close or exit certain facilities and programs. These workforce reductions and closures will be substantially completed by the end of 1995. The pretax expense related to these actions was $89 million ($55 million after tax).In September 1994, Monsanto received $67 million from the U.S. Internal Revenue Service in settlement of certain tax matters related to the 1985 acquisition of Searle. This settlement included interest of $33 million ($21 million after tax), recorded as a one-time gain. Most of the remainder of the proceeds reduced the balance of unamortized goodwill related to the Searle acquisition….…Restructuring expenses are recorded based on estimates prepared at the time the restructuring actions are approved by the board of directors. In the fourth quarter of 1994, the board approved the reversal of $49 million of pretax excess restructuring reserves from prior years. The excess was primarily due to higher than expected proceeds and lower exit costs from the sale and shutdown of nonstrategic businesses and facilities included in the 1993 and 1992 restructuring actions. The balance in restructuring reserves as of Dec. 31, 1994, was $254 million, and consisted primarily of workforce reduction costs under the 1994 actions and planned facility dismantling and site closure costs remaining under previous restructurings. Management believes that the balance of these reserves as of Dec. 31, 1994, is adequate for completion of those activities….Given the reported ROE of 21.4%, Mahoney was granted options for 275,000 shares at $77.75per share, the market price on the grant date. At the end of November 1995, the market price of Monsanto shares was $120 per share. In exercised and sold, the option would have gained about $11,600,000( $42.25*275,000).ing the information presented, discuss whether Mahoney’s stock option were deserved.Provide at least one argument for and one argument against the option award.b.Discuss whether the nonrecurring events disclosed should be included in managementperformance measures such as ROE.ing the information presented, discuss the expected level of Monsanto’s future incomeand ROE.2)The balance sheet and income statement for the Green Company are presented in the Exhibit 1 .a. Based on the financial statements provided, prepare a statement of cash flows for 2001 using thei) Indirect methodii) Direct methodb. Calculate the company’s free cash flow.EXHIBIT 1 THE GREEN COMPANYBalance Sheet and Income StatementBalance Sheet Income Statement for the YearAs of December 31 2001 2000 Ending December 31,2001Assets Sales $10,000 Cash $1,000 $1,100 Cost of goods sold 6,000 Accounts receivable 1,500 1,650 Depreciation 600 Inventory 2,000 2,200 SG&A 1,000 Total current assets $4,500 $4,95 Interest expense 600Fixed assets—at cost*11,000 12,150 Taxable income $1,800 Accumulated depreciation 4,500 5,100 Taxes 720 Net fixed assets 6,500 7,050 Net income $1,080 Total assets $11,000 $12,000Liabilities and EquityAccrued liabilities $ 800 $880Accounts payable 1,200 1,320Notes payable 5,500 6,050Total current liabilities 7,500 8,250Long-term debt 2,000 1,620Common stock 1,000 1,000Retained earnings 500 1,148Total liabilities and equity $11,000 $12,000* No fixed assets were sold during 1996.。