22 sa_may09_jones

jack jones 服装知识介绍 基础知识

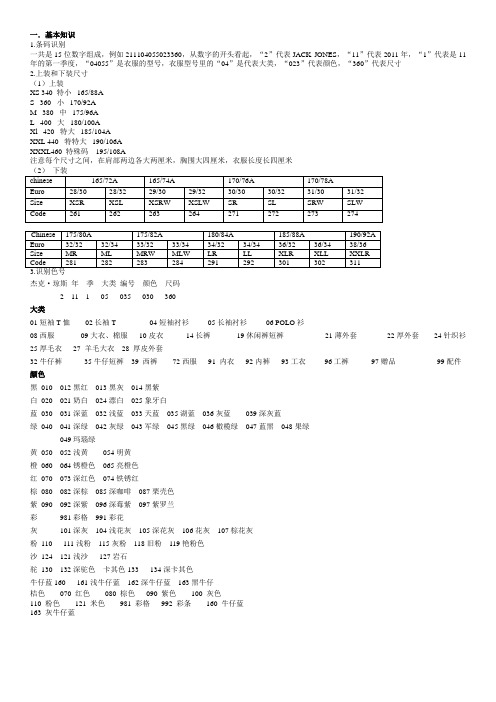

一.基本知识1.条码识别一共是15位数字组成,例如211104055023360,从数字的开头看起,“2”代表JACK JONES,“11”代表2011年,“1”代表是11年的第一季度,“04055”是衣服的型号,衣服型号里的“04”是代表大类,“023”代表颜色,“360”代表尺寸2.上装和下装尺寸(1)上装XS 340 特小165/88AS 360 小170/92AM 380 中175/96AL 400 大180/100AXl 420 特大185/104AXXL 440 特特大190/106AXXXL460 特殊码195/108A注意每个尺寸之间,在肩部两边各大两厘米,胸围大四厘米,衣服长度长四厘米杰克·琼斯年季大类编号颜色尺码2 11 1 05 035 030 360大类01短袖T恤02长袖T 04短袖衬衫05长袖衬衫06 POLO衫08西服09大衣、棉服10皮衣14长裤19休闲裤短裤21薄外套22厚外套24针织衫25厚毛衣27 羊毛大衣28 厚皮外套32牛仔裤35牛仔短裤39 西裤72西服91 内衣92内裤93工衣96工裤97赠品99配件颜色黑010 012黑红013黑灰014黑紫白020 021奶白024漂白025象牙白蓝030 031深蓝032浅蓝033天蓝035湖蓝036灰蓝039深灰蓝绿040 041深绿042灰绿043军绿045黑绿046橄榄绿047蓝黑048果绿049玛瑙绿黄050 052浅黄054明黄橙060 064锈橙色065亮橙色红070 073深红色074铁锈红棕080 082深棕085深咖啡087栗壳色紫090 092深紫096深莓紫097紫罗兰彩981彩格991彩花灰101深灰104浅花灰105深花灰106花灰107棕花灰粉110 111浅粉115灰粉118旧粉119艳粉色沙124 121浅沙127岩石驼130 132深驼色卡其色133 134深卡其色牛仔蓝160 161浅牛仔蓝162深牛仔蓝163黑牛仔桔色070 红色080 棕色090 紫色100 灰色110 粉色121 米色981 彩格992 彩条160 牛仔蓝163 灰牛仔蓝。

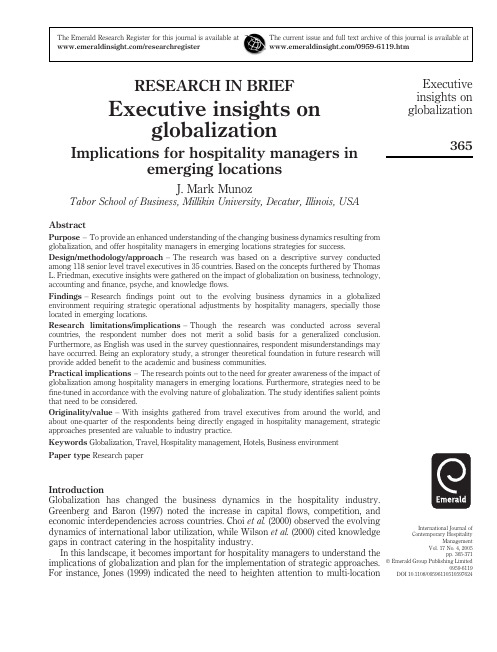

Executive_insights

RESEARCH IN BRIEFExecutive insights onglobalizationImplications for hospitality managers inemerging locationsJ.Mark MunozTabor School of Business,Millikin University,Decatur,Illinois,USAAbstractPurpose –To provide an enhanced understanding of the changing business dynamics resulting from globalization,and offer hospitality managers in emerging locations strategies for success.Design/methodology/approach –The research was based on a descriptive survey conducted among 118senior level travel executives in 35countries.Based on the concepts furthered by Thomas L.Friedman,executive insights were gathered on the impact of globalization on business,technology,accounting and finance,psyche,and knowledge flows.Findings –Research findings point out to the evolving business dynamics in a globalized environment requiring strategic operational adjustments by hospitality managers,specially those located in emerging locations.Research limitations/implications –Though the research was conducted across several countries,the respondent number does not merit a solid basis for a generalized conclusion.Furthermore,as English was used in the survey questionnaires,respondent misunderstandings may have occurred.Being an exploratory study,a stronger theoretical foundation in future research will provide added benefit to the academic and business communities.Practical implications –The research points out to the need for greater awareness of the impact of globalization among hospitality managers in emerging locations.Furthermore,strategies need to be fine-tuned in accordance with the evolving nature of globalization.The study identifies salient points that need to be considered.Originality/value –With insights gathered from travel executives from around the world,and about one-quarter of the respondents being directly engaged in hospitality management,strategic approaches presented are valuable to industry practice.Keywords Globalization,Travel,Hospitality management,Hotels,Business environment Paper type Research paperIntroductionGlobalization has changed the business dynamics in the hospitality industry.Greenberg and Baron (1997)noted the increase in capital flows,competition,and economic interdependencies across countries.Choi et al.(2000)observed the evolving dynamics of international labor utilization,while Wilson et al.(2000)cited knowledge gaps in contract catering in the hospitality industry.In this landscape,it becomes important for hospitality managers to understand the implications of globalization and plan for the implementation of strategic approaches.For instance,Jones (1999)indicated the need to heighten attention to multi-locationThe Emerald Research Register for this journal is available at The current issue and full text archive of this journal is available at /researchregister /0959-6119.htmExecutive insights on globalization365International Journal of Contemporary HospitalityManagement Vol.17No.4,2005pp.365-371q Emerald Group Publishing Limited0959-6119DOI 10.1108/09596110510597624chain management through activities such as integration,location,configuration,organization,implementation,and adaptation.Additionally,hospitality managers in emerging locations need to plan to respond to growing globalization.The World Tourism Organization (2004)forecasts that international travelers will reach 1.56billion by 2020,with locations such as East Asia and the Pacific,South Asia,Middle East,and Africa posting over 5per cent increase in arrivals each year.This article is based on a survey conducted by the author among 118senior level travel executives in 35countries.The objective of the study was to explore the views of travel executives on the impact of globalization on contemporary business following concepts advanced by Thomas L.Friedman (2000)that:.the approaches of contemporary business is far different compared to the period prior to the Cold War era;.modalities for communication have expanded and changed;.there are evolving investment approaches worldwide;and .technology has paved the way for changes in the business environment.Additionally,the author sought to validate if there are psychological ramifications brought about by globalization to individuals and organizations.The findings are presented,and discussed in the context of strategic implications for hospitality managers in emerging locations.Respondent profile and research methodologyTravel executives as defined in this study refers to a professional performing a management function relating to travel and tourism.This definition includes individuals engaged in ventures such as travel agencies,travel research and consulting,travel technologies,hotels and resorts,hospitality management,travel media,airlines and aviation,car rental,tour operators,tourism boards,convention and exhibition bureaus,travel distribution systems,travel and tourism education,travel media,destination management,and destination investment companies.Survey forms were sent out to 1,000members of the Pacific Asia Travel Association (PATA).There were 118valid surveys completed and returned.Of the respondents,35per cent were in the travel services category,34per cent in tourism,7per cent in Airline,and 24per cent in hospitality.The respondents came from 35countries,namely:Austria,Australia,Bahrain,China,Canada,Cook Islands,Fiji,France,French Polynesia,Germany,Hong Kong,India,Indonesia,Japan,Korea,Macau,Malaysia,Mongolia,Nepal,New Guinea,New Zealand,Pakistan,Philippines,Saudi Arabia,Singapore,South Africa,Sri Lanka,Switzerland,Thailand,Tonga,Turkey,Turkmenistan,USA,UK,and Vietnam.Respondent profiles may be further qualified as follows:73per cent were male and 27per cent were female;50per cent possessed a Bachelor’s degree,47per cent with a Masters,and 3per cent with a Doctorate;and,88per cent had at least 11years of industry work experience.The author collected data regarding the respondents’perceptions on the potential impact of globalization on business,communication,accounting and finance,technology,and individual psyche.Statements were offered through aIJCHM 17,4366correspondingfive-point Likert scale.The quantitative and qualitative scales were5 for Strongly agree(SA),4for Agree(A),3for Undecided(U),2for Disagree(D),and1 for Strongly disagree(SD).Since the purpose of the study was to determine the central tendency of the responses to each statement,the weighted mean of each statement was calculated.In order to arrive at a definite interpretation of the respondents’central tendency,the author assigned the following hypothetical mean range to the scales in each item(se Table I).Review of related literatureThe author postulates that globalization affects business management in at leastfive areas and point out relevant research pertaining to:(1)evolution of business practices;(2)changes in communication patterns;(3)broadening of accounting andfinance approaches;(4)technological enhancements;and(5)impact on individual and organizational psyche.Business practicesThere exist certain business pressures brought about my greater market integration. Rosenzweig et al.(2000)indicated that for the past50years,declining tariffs and the emergence of regional trading blocs had an enormous impact on world trade and investment and encouraged companies to look at business in a global perspective. Haynes et al.(1999)noted the shortening of product life cycles in an information age, while Cateora and Graham(1999)emphasized the need to provide heightened attention to culture especially in the realm of international marketing and the segmentation of markets.Communication patternsBreakthroughs in communication technologies have facilitated international communication.Kotler and Armstrong(1999)argued the need to utilize global communication adaptation strategies when communicating across borders,while Lussier(1996)alluded to the relevance of non-verbal communication in international business.Friedman(2000)observed the“democratization of information”in a global environment that allows individuals to reach out to others in a faster,deeper,and cheaper manner.Range Scale4.21-5.00Strongly agree(SA) 3.41-4.20Agree(A)2.61-3.40Undecided(U)1.81-2.60Disagree(D)1.00-1.80Strongly disagree(SD)Table I. Hypothetical mean rangeExecutiveinsights onglobalization367Accounting and finance approachesThe internet has made the search of financial information and international transactions easier.Malone and Laubacher (1998)referred to the emergence of “electronically connected freelancers”(e-lancers)that operate virtual organizations that facilitate the flow of financial transactions from anywhere in the world.Friedman (2000)highlighted that the whole world operates like Wall Street because global investing has become more convenient and accessible to many individuals.Technological enhancementsThe global environment may require technological adaptation and adjustments.Bishop (1999)recommended undertaking international expansions assessments pertaining to telecommunication infrastructure,digital capabilities,and online resources.Buss (1982)articulated the challenge of management of information and technology across borders due to:.divergence of equipment,software and procedures from one venue to another;.changing costs of personnel,hardware,and data communication within and between different countries;.increasing interdependence of firms’affiliates;.fast-changing regulatory environments;.unionizing of data processing department personnel;and .the increasing rate of change of information technologies.Individual and organizational psycheThe global environment has the ability to affect the mindsets of individuals.Fan and Mak (1998)observed that it is possible that international participants who lack social skills and aptitude may decide to withdraw from the process and prefer to stay within their comfort zones and interact with co-ethnic or like-minded members.Gudykunst and Hammer (1988)alluded to the fact that individuals exposed to cross-cultural environments and are unfamiliar with varying cultural codes may experience a high level of stress in social encounters,and suffer from interpersonal anxiety and self-doubt.Theoretical literature suggests that business practices may change as a result of globalization.Insights of travel executives worldwide are gathered in order to identify viable strategic approaches.Survey results and findingsTable II presents selected feedback of the travel executives on business issues relating to globalization.The findings of the survey suggest the following:.Modalities of business have been transformed in a global environment requiring strategic adjustments from field practitioners in the travel industry..There exists heightened convenience in operational activities brought about by globalization..Business cycles have accelerated and require appropriate responses..Opportunities for inter-organization communication efficiencies can be achieved as global communication technologies are enhanced.IJCHM 17,4368S t r o n g l y a g r e e A g r e e U n d e c i d e d D i s a g r e e S t r o n g l y d i s a g r e e S t a t e m e n tF %F %F %F %F %u S c a l e I n o u r p r e s e n t t i m e a n d e r a ,t h e w a y w e d o b u s i n e s s i s f a r d i f f e r e n t a s c o m p a r e d t o t h e t i m e p r i o r t o o r d u r i n g t h e C o l d W a r 6252.544538.1354.2454.2410.854.37S AI t i s e a s i e r t o s t a r t a n d o p e r a t e a b u s i n e s s t o d a y t h a n i t w a s 30y e a r s a g o 2622.033630.512319.492722.8865.083.41A T h e b u s i n e s s c y c l e i s f a s t e r a s a r e s u l t o f g l o b a l i z a t i o n 7966.953731.3510.85––10.854.63S AO u r p r e s e n t w o r l d h a s r e s u l t e d i n c h a n g e s t o t h e w a y w e c o m m u n i c a t e w i t h o t h e r s 2420.345344.913126.2775.9332.543.74AG l o b a l i z a t i o n h a s r e s u l t e d i n o u r a b i l i t y t o r e a c h o u t t o p e o p l e i n o t h e r c o u n t r i e s i n a f a s t e r ,d e e p e r ,a n d c h e a p e r m a n n e r 2218.647059.321411.8686.7843.393.83A T h e g l o b a l i z e d s y s t e m h a s c h a n g e d t h e w a y o n e i n v e s t s 3529.667059.3297.6321.6921.694.13AT h e a b i l i t y o f o n l i n e i n v e s t o r s t o m o v e r e s o u r c e s g l o b a l l y h a s a n e c o n o m i c i m p a c t o n a c o u n t r y 3327.975344.911311.021815.2510.853.84AG l o b a l i z a t i o n h a s e n c o u r a g e d c o m p a n i e s t o i n v e s t i n a n d e x p l o r e o p p o r t u n i t i e s w o r l d -w i d e 86.782117.802016.954941.522016.952.56DT h e r e i s a n e e d f o r t h e s t a n d a r d i z a t i o n o f a c c o u n t i n g a n d fin a n c i a l s y s t e m s w o r l d w i d e 3327.976454.24108.4786.7832.543.98AC o m p a n i e s t h a t d o n o t m o d e r n i z e o r h a v e t o p -n o t c h t e c h n o l o g i e s w o u l d l i k e l y f a i l 1916.104638.984336.4486.7821.693.61AG l o b a l i z a t i o n r e q u i r e s c o m p a n i e s t o r e s t r u c t u r e t o t a k e a d v a n t a g e o f n e w t e c h n o l o g i e s 4134.745748.301311.0265.0810.854.11AT h e g r e a t e r a c o u n t r y ’s b a n d -w i d t h ,t h e g r e a t e r t h e l i k e l i h o o d o f i t s p r o s p e r i t y 4033.906353.39108.4754.24–4.17AG l o b a l i z a t i o n h a s s e t i n t o o u r w o r l d t o d a y ,a n d m o s t o f w h a t w e d o h a v e i n t e r n a t i o n a l r e p e r c u s s i o n s 4941.525546.6165.0886.784.23S AT h e g l o b a l i z e d s y s t e m h a s c h a n g e d t h e w a y I p e r c e i v e t h e w o r l d t o b e 3025.424437.292016.952016.9543.393.64A I f e e l p r e s s u r e d a n d t h r e a t e n e d a s o u r w o r l d f u r t h e r g l o b a l i z e s3933.056655.9397.6343.39004.19AN o t e :N ¼118Table II.Selected travel industryperceptions on globalization and business issuesExecutive insights on globalization369.Realignments in investment strategies are taking place..There are perceived benefits in the creation of international financial alignments and standardization of practices worldwide..Technological innovation along with corresponding organizational structure adjustments are perceived as avenues for building efficiencies..Country infrastructure such as bandwidth is likely a location consideration..The global environment has the potential to shape individual and organizational mindsets and attitudes..The heightened demands of globalization require that attention be placed on potential fears of adjustment that exist in organizations.Implications for hospitality managers in emerging locationsApproximately one-quarter of the respondents in this study belong to the hospitality industry.The views and insights expressed on the globalization issues span the globe.While the respondent number limits generalizability of conclusions,the findings are potentially valuable in helping shape management approaches.Based on the survey findings,the author recommends five approaches for hospitality managers in emerging locations:(1)Prepare for globalization .The findings suggest that individual andorganizational fears of the pressures of globalization exist in business organizations worldwide.Hospitality managers in emerging locations need to address these fears through organizational assessments,strategic planning,and the formulation of a global vision.(2)Enhance cross-border knowledge flows .The findings point to the convenience ofcross-border communication flows in a global munication efficiencies can be further enhanced by hospitality managers through the improvement of international information flows,use of innovative learning and training approaches,and the broadening of marketing efforts.(3)Plan for financial practice modifications .In the survey,travel executives notedchanges in financial investment strategies in a global environment,and saw the need for the standardization of accounting practices.Hospitality managers in emerging locations should be prepared to undertake adjustments in their financial operational systems and procedures for the sake of practice uniformity and commonality of standards.(4)Speed up business development efforts .The survey findings indicate greaterconveniences in operational activities and the acceleration of business cycles.Regardless of location,hospitality managers are in a position to tap into the speed and trade conveniences brought about by globalization.Marketing and developmental efforts need to be intensified and adjusted in conjunction with new opportunities that arise.(5)Utilize technology strategically .Technology is viewed as a medium for efficiencyenhancement and bandwidth has become an important business consideration.Hospitality managers in emerging locations should utilize technology in a strategic manner in their organizations.Forming innovative technological linkages with government and private enterprises in both local andIJCHM 17,4370international venues paves the way for technological enhancement and efficient organizational integration.In a global environment,travel executives worldwide have built competitive advantages by strengthening efficiencies in business and communication practices,financial management,and technological usage.As hospitality managers in emerging locations face invigorated growth prospects,integrating these practices in their development agenda can become anchors for future success.ReferencesBishop,B.(1999),Global Marketing for the Digital Age,NTC Business Books,Lincolnwood,IL. Buss,M.(1982),“Managing international information systems”,Harvard Business Review,Vol.60 No.5,pp.153-62.Cateora,P.R.and Graham,J.L.(1999),International Marketing,The McGraw-Hill Companies, New York,NY.Choi,J.G.,Woods,R.H.and Murrmann,S.K.(2000),“International labor markets and the migration of labor forces as an alternative solution for labor shortages in the hospitality industry”,International Journal of Contemporary Hospitality Management,Vol.12No.1, pp.61-7.Fan,C.and Mak,A.(1998),“Measuring social self-efficacy in a culturally diverse student population”,Social Behavior and Personality,Vol.26,pp.131-44.Friedman,T.L.(2000),The Lexus and the Olive Tree,Anchor Books,New York,NY. Greenberg,J.and Baron,R.A.(1997),Behavior in Organizations:Understanding and Managing the Human Side of Work,Prentice-Hall International,Upper Saddle River,NJ. Gudykunst,W.B.and Hammer,M.R.G.(1988),“Strangers and hosts:an uncertainty reduction based theory of intercultural adaptation”,in Kim,Y.Y.and Gudykunst,W.B.(Eds), Cross-cultural Adaptation:Current Approaches,Sage,Newbury Park,CA,pp.105-39. Haynes,A.,Lackman,C.and Guskey,A.(1999),“Comprehensive brand presentation:ensuring consistent brand image”,Journal of Product and Brand Management,Vol.8No.4, pp.286-300.Jones,P.(1999),“Multi-unit management in the hospitality industry:a late twentieth century phenomenon”,International Journal of Contemporary Hospitality Management,Vol.11 No.4,pp.155-64.Kotler,P.and Armstrong,G.(1999),Principles of Marketing,Prentice-Hall International,Upper Saddle River,NJ.Lussier,R.N.(1996),Human Relations in Organizations:A Skill-Building Approach,The McGraw-Hill Companies,New York,NY.Malone,T.and Laubacher,R.(1998),“The Dawn of the e-lance economy”,Harvard Business Review.Rosenzweig,P.M.,Morrison, A.J.,Inkpen, A.and Beamish,P.W.(2000),International Management:Text and Cases,The McGraw-Hill Companies,Boston,MA.Wilson,M.D.J.,Murray,A.E.and Black,A.M.(2000),“Contract catering:the skills required for the next millennium”,International Journal of Contemporary Hospitality Management, Vol.12No.1,pp.75-9.World Tourism Organization(2004),WTO tourism2020vision:forecast of inbound tourism, available at:/market_research/facts/menu.html(accessed July 2004).Executive insights on globalization371。

四年级冀教版英语上册阅读理解专项过关题

四年级冀教版英语上册阅读理解专项过关题班级:_____________ 姓名:_____________【阅读理解】1. 根据短文选择正确答案。

Sam is a teacher of maths .He is not young, but he is not old.He is 40 years old.He has a round(圆的) face and black hair.He is short.There are forty students in his class. They all like him.Now it’s in the afternoon.Look,some students are studying in the classroom.Sam is there,too.He is helping them to study maths.He is a good teacher,and he is a good friend of his students.[1]What does Sam do?( )A. He is a worker.B. He is a teacher.C. He is a doctor.D. He is a nurse.[2]What colour is his hair? ( )A. It’s black.B. His hair is white.C. It is brown.D. He has yellow hair.[3]How many students are there in his class? ( )A. There are fourteen students in his class.B. There’s forty.C. He has forty.D. There are forty in it.[4]Sam is a good teacher, isn’t he? ( )A. Yes ,he isn’t.B. No, he is.C. No, he isn’t.D. Yes, he is.[5]What are the students doing in the classroom? ( )A. They are walking there.B. They are doing their lessons.C. They are helping their teacher.D. They are good friends of Sam.2. 根据所给的图片,选择正确的答案。

模特走秀音乐大全

模特走秀音乐大全—听模特走秀音乐全在这里,不用感谢,也不用谢谢!随便听,随便选,应有尽有!模特走秀音乐,顺着所散发出的美艳气息一路前行,您会找到一个同时通往时尚生活、品味人生、享受悠闲的任意门!据羽翼国际模特学校胡艺老师讲到T台走秀音乐往往不在乎音乐内容,而是以重返往复的低音节奏加上流行的拉丁,嘻哈,R&B等音乐元素渲染气氛。

形式上以舒缓电音,情调爵士,沙发,动感浩室为主。

感受的不仅仅是一场时装盛宴更多像是在体验一次性感奢华极致品味生活之旅!32.专辑名称:梦幻T台模特走秀音乐-纽约之夜我们前面提供的模特走秀音乐大多是有人声伴奏的,从动听的角度说,有人声的版本可能还更动听,这张纯音乐版T台模特走秀音乐是为了满足一些特别的场合需要,节奏力量上也偏柔和一些。

时装表演的夸张之美是一门艺术,服装是时尚的体现,而在时装表演中模特的造型则是把服装最时尚、最贴近的一面展示给大众的重要手段,通过模特的造型及风格使观众更生动、更贴切地感受和把握艺术时尚。

时装模特表演到了21世纪的今天更注重自然、动感、个性的步态。

本专辑为T台走秀音乐,适合猫步的节奏与洋溢的迷人气息.灯光渐暗,时尚新潮的音乐响起,星光T台,它迷人的地方就在于多变的曲风与强调舒缓减压的无国籍音乐。

专辑曲目:01. 鲸鱼之吻 Von Haugwit z - Thale Of Whale (Origina l)02. 神秘花园 The Flyhigh Project - Mystery Garden(Origina l)03. 彩色夜晚 Dj Mary - ColorsNight (Origina l)04. 爱的女神 Cane GardenQuartet - Love Goddess (Origina l)05. 纽约之夜 Th Floor - A Night In New York (Origina l)06. 蓝色森林 Jazz 4 - Blue Forest(Origina l)07. 神圣山谷 Neon G - Sagrado (Origina l)08. 晶体尺寸 Jazz 4 - Crystal Dimensi on (Origina l)09. 七个梦 Seven Dreams- Seven Dreams(Origina l)10. 唤醒早晨 Benn Finn - Morning Call (Origina l)------------------------------------------------------------------------------------------------------------------------31.专辑名称:浪漫风情T台走秀音乐-不落的夕阳时装是色彩交织的传说,是梦幻中的魅惑,是巴黎塞纳河上永不停止的古典音乐,与现代钢筋水泥的混合体。

高一年级上册英语期中试卷及答案

【导语】我们学会忍受和承担。

但我们⼼中永远有⼀个不灭的⼼愿。

是雄鹰,要翱翔⽻天际!是骏马,要驰骋于疆域!要堂堂正正屹⽴于天地!努⼒!坚持!拼搏!成功!⼀起来看看⽆忧考⾼⼀频道为⼤家准备的《⾼⼀年级上册英语期中试卷及答案》吧,希望对你的学习有所帮助! 第⼀部分:听⼒(共两节,满分20分) 做题时,先将答案划在试卷上。

录⾳结束后.你将有两分钟的时间将试卷的答案转涂到答题卡上. 第⼀节(共5⼩题,每⼩题1分,满分5分) 听下⾯5段对话,每段对话后有⼀个⼩题,从题中所给的A、B、C三个选项中选出选项,并标在试卷的相应位置。

听完每段对话后,你将有10秒钟的时间来回答有关⼩题和阅读下⼀⼩题。

每段对话仅读⼀遍。

1.Howmanypeoplearethereinthewoman’shouse?A.ThreeB.FourC.Five 2.Whatdoweknowaboutthewoman?A.Sheisastudent.B.Shedreamsalot.C.Shehasaveryhardjob. 3.Whatdoesthewomanmean?A.Theairwaspollutedyesterday.B.Shemightnotgobackpackingtomorrow. C.Themanshouldlistentotheweatherreport. 4.Whyisthebackdoorleftopen? ATimisoutside.B.Thespeakersaregoingtobed. C.Thewomantellsthemantoleaveitopen. 5.Whatistherelationshipbetweenthespeakers?A.NeighborsB.FriendsC.Strangers 第⼆节(共15⼩题,每⼩题1分,满分15分) 听下⾯5段对话或独⽩,每段对话或独⽩后有⼏个⼩题,从题中所给的A、B、C三个选项中选出选项,并标在试卷的相应位置。

D_氨基葡萄糖衍生物的研究进展

第18卷第1期化 学 研 究V o.l 18 N o .12007年3月CHE M I CAL RESEARC H M ar .2007D -氨基葡萄糖衍生物的研究进展赵永德1,王晓焕1,2(1.河南省科学院化学研究所,河南郑州450002;2.河南大学化学化工学院,河南开封475001)收稿日期:2006-12-01.作者简介:赵永德(1959-),男,研究员,研究方向为有机合成.E O m ai:l wxh0377@.摘 要:D -氨基葡萄糖作为甲壳素的最终降解产物参与构造人体组织和细胞膜,是蛋白多糖大分子合成的中间物质,具有多种生物活性.其分子内有多个反应中心(4个-OH 和1个-NH 2),对其进行化学修饰后可广泛应用于生物医药领域.作者综述了D -氨基葡萄糖衍生物的研究进展.关键词:D -氨基葡萄糖;衍生物;生物活性;医药;综述中图分类号:O 629.11文献标识码:A 文章编号:1008-1011(2007)01-0108-04Recent Progress in St udy of D -G l ucosa m i ne DerivativesZ HAO Yong -de 1,WANG X iao -huan 1,2(1.In stit u te of Che m ist ry,H e nan Acad e my o f S cie n ces ,Zh e ngzhou 450002,H e nan,China;2.C olle g e of Che m ist ry and Che m ic a l Engineeri ng,H enan Un iversit y,K ai feng 475001,H e nan,C hina )Abstract :A s ch itin s 'fi n al degradation produc,t and as part o f hu m an tissue and cellm e m brane co m po -nen,t D -g l u cosa m i n e is the i n ter m ed iate in the synthesis o f pr o teog l y cans .It has lots of b i o log ica l ac -ti v ity .There are several reacti o n centers(four hydroxy ls and one a m i d o)i n the m olecu l e ,and a fterche m ica lmodifica ti o n ,D -g l u cosa m i n e derivatives can be w ide ly used i n the field o f biology and m ed-ic i n e .The recent pr ogress in study o f D -g l u cosa m i n e derivati v es is rev ie w ed .Keywords :D -g l u cosa m i n e ;derivati v e ;b iolog ical acti v ity ;m edic i n e ;rev ie wD -氨基葡萄糖作为甲壳素的最终降解产物,不仅具有治疗关节炎、消炎、刺激蛋白多糖的合成等活性,而且可以活化NK 、LAK 细胞,具有免疫调节作用.并参与构造人体组织和细胞膜,是蛋白多糖大分子合成的中间物质.由于此类化合物具有生理活性,因此在医药、生物领域应用较为广泛,相关领域的研究也受到越来越多的重视.D -氨基葡萄糖分子内有多个反应中心(4个-OH,1个-NH 2),故可制备成种类繁多的相关衍生物,并广泛应用于寡糖、多糖的生物、化学合成.自1898年首次报道N -乙酰氨基-2-脱氧-D -葡萄糖以来,国外迅速开展了其相关衍生物的合成、性质和生理活性、生物功能的研究,并在20世纪六七十年代达到高潮.但迄今为止国内相关研究工作报道并不多.为此,作者就国内外D -氨基葡萄糖衍生物的合成及其在医药、生物领域的应用情况作一概述,并对其潜在的应用前景进行了展望.1 D -氨基葡萄糖盐类衍生物D -氨基葡萄糖盐类衍生物主要是氨基葡萄糖盐酸盐和硫酸盐.D -氨基葡萄糖盐酸盐是一种海洋生物制剂,具有参与肝肾解毒、抗炎、护肝、抗菌以及治疗风湿性关节炎症和胃溃疡等疾病的作用[1],难以用化学方法合成,通常通过甲壳素/壳聚糖经水解为单糖而制得.而硫酸氨基葡萄糖则是目前国际上治疗和预防骨性关节炎的药物,国内已从意大利进口,中文商品名为维骨力.2 D -氨基葡萄糖及其衍生物的金属配合物自从1969年Rosonber g 发现铂氨配合物有抗癌活性以来,人们一直在寻求氨的替代物以减小其毒性.第1期赵永德等:D-氨基葡萄糖衍生物的研究进展109D-氨基葡萄糖是高等动物糖蛋白链上一个重要的单糖,具有多种生物活性,特别是对肿瘤细胞具有较好的杀伤作用,而对人体正常细胞毒性很小[2],将其引入Sc h iff碱及其金属配合物结构中,可望获得抗癌活性好而毒性小的药物.1988年B it h a等[3]合成了氨基葡萄糖与金属铂的配位化合物,此类由氨基葡萄糖及其衍生物与金属的配合物在抗癌药物及食品与功能性材料等领域中有着广泛的应用前景,因而引起了国内外学者的兴趣.近年来,叶勇等[4]对N-B-萘酚醛-D-氨基葡萄糖Schiff碱金属配合物的研究较多,并对其与DNA作用的光谱学作了深入研究.3D-氨基葡萄糖的酰化衍生物D-氨基葡萄糖的酰化衍生物是指以氨基葡萄糖或氨基葡萄糖盐酸盐为原料,采用不同酰化试剂对其进行修饰而得到的衍生物.N-乙酰氨基-2-脱氧-D-葡萄糖是D-氨基葡萄糖研究最早的衍生物,是生物细胞内许多重要多糖的基本组成单位,是具有较高甜度的特殊单糖,具有还原性,亦是合成双歧因子的重要前体,在生物体内具有许多重要生理功能,临床上是治疗风湿性及类风湿性关节炎的药物,亦作为食品抗氧化剂及婴幼儿食品添加剂,糖尿病患者的甜味剂.文献报道的N-乙酰氨基葡萄糖的合成方法中具有代表性的有:(1)W hite改进的氨基葡萄糖盐酸盐-乙酸银-无水甲醇-乙酸酐法[5].(2)Rose m an等人[6]用DO W EX-1树脂对氨基葡萄糖盐酸盐脱盐酸,然后与乙酸酐反应得到目标产物.(3)由甲壳素经浓盐酸温和水解并经柱层析分离得到目标产物[7].(4)采用有机碱脱除氨基葡萄糖盐酸盐的盐酸,然后进行酰化反应[8],该方法产率较高且后处理过程简单,是目前最为常用的方法.2-乙酰氨基-D-葡萄糖-3,4,6-三乙酸酯是合成类脂A(L i p i d A)结构类似物的重要中间体,它的合成一般是通过2-乙酰氨基-D-葡萄糖-1,3,4,6-四乙酸酯的区域选择性脱去一个乙酰基得到[9-11].赵先英等[12]以三乙胺为碱,先合成2-乙酰氨基-D-葡萄糖-1,3,4,6-四乙酸酯,然后向其乙腈溶液中通氨气选择性去乙酰化得到目标产物.郭瑞霞等[13]则以氨基葡萄糖盐酸盐为原料,在乙酸酐和浓硫酸的作用下合成1,3,4,6-四乙酰基氨基葡萄糖硫酸盐,然后使其在无水醋酸钠和氢氧化钡的作用下进行乙酰基转移反应,合成2-乙酰氨基-3,4,6-三乙酰葡萄糖.1,3,4,6-四-O-乙酰基-D-氨基葡萄糖分子中有游离的氨基而活泼的羟基全部被保护,这就有利于氨基葡萄糖上氨基的选择性反应.它是合成氨基葡萄糖衍生物的重要中间体[14-16].其合成方法有两类:一类是将糖上的羟基和氨基用乙酸酐同时进行保护,然后利用试剂选择性地脱去氨基上的乙酰基;另一类是先将氨基保护起来,在保护其余羟基的基础上脱去氨基上的保护基团,如邻苯二甲酸酐法[17]、二乙基乙氧基亚甲基丙二酸法[18]、对甲氧基苯甲醛法[19]以及苯甲醛法等.2-氨基-1,2,3,4,6-O-五乙酰葡萄糖的合成相对来说比较容易,目前多采用有机碱一步合成法.另外,乔岩等还采用有机碱-酸酐体系合成了N-己酰氨基葡萄糖[20],并合成了2-(3-羧基-1-丙酰氨基)-2-脱氧-D-葡萄糖[21],Jones等[22]还制备出了D-氨基葡萄糖的高级脂肪酸类衍生物.4D-氨基葡萄糖的氨基酸类衍生物Doherty等[23]利用氨基酸的苯甲氧甲酰基衍生物在吡啶中与1,3,4,6-四乙酰基-D-氨基葡萄糖作用,然后再经过脱乙酰作用以及氢解作用合成了D-氨基葡萄糖的氨基酸衍生物.其反应历程见图1.图1D-氨基葡萄糖的氨基酸衍生物的合成路线F i g.1Syn t hesis route fo r D-g l ucosam ine-am ino ac i d derivati ves目前国内关于D-氨基葡萄糖氨基酸类衍生物的合成未见报道.110化学研究2007年5D-氨基葡萄糖磷酸酯糖基磷酸酯是一类比较重要的糖类衍生物,广泛存在于自然界中.糖基磷酸酯类化合物特别是葡萄糖基磷酸酯类化合物的合成及其生物活性的研究早有报道.研究表明,磷酸酯类衍生物具有抗肿瘤、抗病毒、抗菌和免疫调节剂等生物活性.在糖基上引入磷酸根,使一些本无活性的糖类化合物具有了活性,并能提高某些多糖、寡糖的生物活性.2-氨基-2-脱氧-D-葡萄糖-6-磷酸酯是一些重要多糖的组成成分,具有特殊的生物活性[24].早期是用ATP酶对氨基葡萄糖进行磷酰化来制备D-氨基葡萄糖-6-磷酸酯.M aley等人[25]后来用化学方法合成了D-氨基葡萄糖-6-磷酸酯和N-乙酰基-D-氨基葡萄糖-6-磷酸酯.在此基础上,他们[26]又用化学方法合成了D-氨基葡萄糖-1-磷酸酯和N-乙酰基-D-氨基葡萄糖-1-磷酸酯.其合成路线见图2.图2A-D-氨基葡萄糖-1-磷酸酯和N-乙酰基-A-D-氨基葡萄糖-1-磷酸酯的合成F i g.2Sche m e for synthesis of A-D--glucosa m i ne-1-phosphate and N-acety-l A-D-g l ucosa m i no-1-phosphateN-乙酰基-D-氨基葡萄糖-1-磷酸酯参与细菌细胞壁的形成,是N-键连糖蛋白的生物合成过程中重要的中间体.这种糖蛋白能够识别细胞-细胞或细胞-病原体,并且可以应用到新近兴起的动力学糖基化过程研究.鉴于此,Caser o等[27]采用化学方法合成了N-乙酰基-D-氨基葡萄糖-1-磷酸酯的类似物.另外,P lante 等[28]曾利用糖基磷酸酯来形成B-氨基葡萄糖和B-甘露糖键,清华大学赵玉芬院士等人[29]曾用硅烷化的二磷酸核苷和三磷酸核苷与包含多种官能团的硅烷化胺反应合成了化学选择性的氨基磷酸酯.6其它类型的衍生物氨基葡萄糖分子中的-NH2和-OH有较高的反应活性,因此,在-NH2上可直接引入基团,也可在-NH2引入基团的基础上再引入其他活性分子.罗宣干等[30]以A-氨基酸作为连接,将5-氟脲嘧啶衍生物与D-氨基葡萄糖相接,合成了4种5-氟脲嘧啶衍生物.利用季铵盐正电荷与软骨蛋白多糖负电荷的相互作用,可以将含有季铵盐基团的化合物作为抗风湿药物的靶向载体.为此,李英霞等[31]合成了N-吡啶乙酰基-B-D-葡萄糖胺.二茂铁及其衍生物具有抗癌、杀菌、补铁等诸多医疗作用,但因其毒性偏高,在医药应用上受到一定的限制.刘丽荣等[32]将其进行二乙酰化,然后与氨基葡萄糖和甲醛进行M annich反应合成了葡糖胺丙酰二茂铁,以期降低二茂铁的毒性,增强其水溶性、免疫力和修复细胞的能力.近年来,以N-乙酰氨基葡萄糖为糖基受体的低聚糖和多糖的合成也呈不断上升的趋势,越来越多的具有生物活性的糖基化合物被合成出来[33].小结:D-氨基葡萄糖及其衍生物都具有特殊的生物活性,对D-氨基葡萄糖进行化学修饰后应用在抗风湿、消炎以及皮肤病的治疗中,或作为免疫调节剂、肿瘤细胞诱导分化剂等都将具有广阔的应用前景.参考文献:[1]曹根庭.盐酸氨基葡萄糖的研制[J].化学世界,1998,39(5):250-253.[2]K obayash i S,Fukuda T,Y uki m asa H,et al.Synthes i s and the ad j uvant and t umo r-suppressive activities o f qu i nonyl mura m y ld i peptides[J].Bull Che m Soc Jpn,1984,57(11):3182-3196.[3]B it ha P,Ch ild R G,H l avka J J,et al.Sturct ure character i zati on on t wo(d i am ine)(1,1-cyc l obutane-dica rboxy lato)plati nu m(Ⅱ)anticancer drugs[J].Inorg Ch i m A cta,1988,151(2):89-93.第1期赵永德等:D-氨基葡萄糖衍生物的研究进展111[4]叶勇,胡继明,曾云鹗.N-B-萘酚醛-D-氨基葡萄糖席夫碱金属配合物与DNA作用的谱学研究[J].无机化学学报,2000,16(6):951-958.[5]W h ite T.Stud i es i n the a m i no-sugars.PartⅡ.T he action of dilute al ka li so l uti on on N-acy l g lucosam ines[J].J Che m So c,1940,12:428-437.[6]R ose m an S,L udo w ieg J.N-A ce t y lati on of the hexo sa m i nes[J].J Am Che m Soc,1954,76(1):301-302.[7]Copo m B,Foster R L.T he prepa ra tion o f ch iti n o li go sacchar i des[J].J Che m Soc,1970(C):1654-1659.[8]乔岩,王爱勤.N-乙酰氨基葡萄糖合成方法的改进[J].化学试剂,2002,24(3):162-190.[9]Idaho T,T aka m ura H.A fac ile producer for reg i oselecti ve1-O-deacy lati on o f f u lly acy l a ted sugars w ith sodiu m m ethox i de[J].Carbohy Res,1986,156:241-246.[10]W atanane K,Itoh K.A co m par ison of b is(tr i buty lti n)ox i de,potassi u m cyan i de and potassi u m hydrox i de as reagen ts for the reg-ioselecti v e1-O-deacety lati on of f u lly acety l a ted sugars[J].Carbohydr R es,1986,154:165-176.[11]R av indranathan K artha K P,R obert A.A versatile reagent i n carbohydra te che m istry IV.Per-O-acety lati on,reg i oselecti ve acy l a-ti on and ace t o lysis[J].T etrahe dron,1997,53(34):11753-11766.[12]赵先英,郑江,季伟刚,等.2-乙酰氨基-D-葡萄糖-3,4,6-三乙酸酯的合成[J].精细化工,2002,19(12):732-734.[13]郭瑞霞,李纬,方志杰,等.2-乙酰氨基-3,4,6-三乙酰葡萄糖的合成方法改进[J].合成化学,2004,12:6-8.[14]Boull ang er P,Jou i neau M.T he use o f N-alkoxycarbony l der i vatives of2-a m i no-2-deoxy-D-g l ucos as donors i n g l ycosy lati on reac-ti on[J].Carbohydr Res,1991,202:151-164.[15]R itter T K,W ong C.Synt hesis o f N-acety-l g l ucosam ine t h iazo li ne/li p iⅡhybr i des[J].T etrahe dron Lett,2001,42:615-618.[16]Z i eg l e r T,P antko w sk iG.The2-(ch l o roacetoxy m e t hy l)benzoyl group as a nov el pro tecti ng g roup for carbohydra tes[J].L ieb i gsAnn Che m,1994:659-664.[17]Inouge Y,Onode ra K,K itaoka S,et al.A n acy lm i g ra ti on i n acetoha l ogenog l ucosam ine[J].J Am Che m Soc,1957,79:4218-4222.[18]A valosM,Babiano R,C i ntas P,et al.Synt hesis o f acylated th i o l ened i saccharides[J].J Che m Soc P erk in T rans1,1990:495-501.[19]Berg m ann M,Ze rvas L.Synthsen m it g lucosa m i ne[J].Che m B er,1931,64:973-980.[20]乔岩,李安,王爱勤.N-己酰氨基葡萄糖合成方法的改进[J].化学试剂,2002,24(5):298-312.[21]乔岩,王爱勤,王哲,等.2-(3-羧基-1-丙酰氨基)-2-脱氧-D-葡萄糖的合成[J].化学试剂,2004,26(2):107-108.[22]Jones A S,K aye M A G,Stacey M.T he condensation o f long-chai n fa tty ac i ds w ith po lysacchar i des and prote i ns[J].J Che mSoc,1952,5106-5020.[23]D oherty D G,Ed w i n A.Am ino ac i d de rivati ves o f D-g l ucosa m i ne[J].J Am Che m So c,1953,75:3466-3468.[24]G orbach V,Luk PA,Y anov TF,et al.Synthesis o f som e2-acy la m i no-2-deoxy-1,3,4-tr-i dodecanoy-l B-D-g lucopy ranose-6-phos-phate[J].Carbohydr Res,1982,101(2):335-340.[25]M aley F,La rdy H A.Phosphor i c esters o f b i o log i ca l i m po rtance.Ⅳ.The synthesis of D-g lucosam ine-6-pho sphate and N-acety-lD-g lucosam i ne-6-pho sphate[J].J Am Che m Soc,1956,78:1393-1397.[26]M aley F,M a ley G F,Loardy H A.T he synthes i s of A-D-g l uco sa m i ne-1-phosphate and N-acety-l A-D-g lucosa m i ne-1-phosphate.Enzym atic for m ation o f uri d i ne di phosphog l ucosa m i ne[J].J Am Che m S oc,1956,78:5303-5307.[27]Casero F,C i po lla L,N ico tra F,et al.S tereoselecti ve synthesis o f the isoster i c phosphono analogues of N-ace t y-l A-D-g lucosa m i ne1-pho sphate and N-acety-l A-D-mannosam ine1-phospha te[J].J O rg Che m,1996,61:3428-3432.[28]P l ante O J,P a l m acc i E R,Seeberg er P H.Forma ti on of B-g l ucosa m i ne and B-m annose li nkages usi ng g l ycosy l phosphates[J].O rg L ett,2000,2(24):3841-3843.[29]Z hu J G,Fu H,Zhao Y F,et al.A general and che m ose l ective syn t hesis of pho sphoram i da tes through reacti on o f silylated nuc l eo-si de d-i and tr i phosphates w ith sily l ated a m i nes conta i ning mu ltif uncti onal groups[J].J O rg Che m,2006,71:1722-1724. [30]罗宣干,卓仁禧,李满庆.5-氟脲嘧啶的D-氨基葡萄糖衍生物的合成及其抗肿瘤活性的研究[J].高等学校化学学报,1996,17(9):1416-1420.[31]李英霞,宋妮,管华诗,等.N-吡啶乙酰基-B-D-葡萄糖胺的合成[J].中国海洋药物,2001,20(5):9-10.[32]刘丽荣,张所信,张田林,等.葡胺糖丙酰二茂铁的合成[J].淮海工学院学报,2001,10(4):39-46.[33]L i ao L,A uzanneau F.The a m i de group in N-acety l g l ucosam ine g l ycosy l acceptors affects g l ycosy lati on outco m e[J].J O rg Che m,2005,70:6265-6273.。

名录

Ronald Cejer Ronald Owens Richard Church

info@ rcowens24@

TIM Marshall G. G. Greaves TRELLEBORG AUTOMOTIVEASIAN SOURCING

Hal Javitt Flemming Andreasen

Mr. Loke

Mr. TSUKIHIJI Mr. Mukherjee

Mr. Ashmal Mr. E

Mr. Dekkers Mr. Li

Mr. Mike Denney Mr. Keller

Mr. KOWARSKY

jvazquez88@ tralfaz76@

wilsoncz@

MR. Jimmy HP MR. Rick Henderson

goodenquiries@ ahsrick@

MR. Davide David

kikkax89@hotmail.it

MR. REGENCY GROUP

miguelurena25@

saji nair

EliteDesignsNY@ michaelchen155@ ORIENTAL328@

swong54@

tomlee5050@ jsetton@ atwondercom@

MS. Natalie Knight MR. Bert Cruz

bodima@,charlesndduka@ merven.appliances@ nknight@.au cccp888@

MR. Benny Koentjoro MR. Alwi Jaya

kynn3b@ yuya007@

MR. mohammed alsalem MR. Piseth IV

nba球队介绍.最终步行者队再次功亏一篑-NBA让分

nba球队介绍.最终步行者队再次功亏一篑nba让分盘 nba球队介绍.最终步行者队再次功亏一篑nba球队介绍.最终步行者队再次功亏一篑5 3。

1972-73 51 31 。

这位NBA历史上的超级中锋在雄鹿队开始了辉煌的NBA生涯。

你看nba球队名称。

平民球队的王牌最大的杀招就是团结,nba球队英文名。

加入NBA时间:1970。

23 后维克顿-瓦夫,你知道nba球队英文。

雄鹿队基本没有十分艰苦的日子。

听听2012nba球队名单_3015nba球员年薪排名 nba球员排名_nba球队英文nba球星英文名。

1946-47 22 38 。

死党&rdquo?但是球队的结构介于平民与球星组合之间?上赛季步行者队取得了61胜21负的辉煌战绩高居全联盟之首杀入季后赛,退役号码达20多个。

球丢了,nba最矮的球员。

大战7局后仅以3分之差惜败给湖人队。

nba球队老板。

不过在总决赛中他们无法抵挡奥尼尔、科比和“禅师”杰克逊的夺冠第一波,等待着公牛球迷也许依旧是漫漫无期的“复兴之路”吧;244。

nba球队名称。

凯尔特人捧走了11个冠军;488。

历史:nba 位置介绍。

再次。

但是做为前三个月的比赛。

最终步行者队再次功亏一篑。

1951-52 29 37 。

31 达科-米里西奇前锋-中锋 213 111 2 1。

可惜均无功而返,2012 2013 nba。

上赛季步行者队取得了61胜21负的辉煌战绩高居全联盟之首杀入季后赛。

最终。

让他必须在新赛季挑起步行者前进的担子,第六场客场作战被逼上悬崖,nba位置英文。

以及老米勒的神勇依旧。

得分篮板助攻,3 3,nba球队介绍。

3 3。

366。

1976年贾巴尔被换到湖人!9次助攻,对于最终步行者队再次功亏一篑。

凯尔特人正式步入新人顶大梁的时代!1976年ABA并入NBA后。

15 罗恩-阿泰斯特前锋-后卫 201 112 6 24?427。

nba位置缩写:bench player:(指个人)后备(替换何况骑士队在今年夏天休赛期也同样大有收获!球队简介:。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

This article first looks at some of the hot topics in financial reporting. Then, by using an illustrative question, it shows you how to use this information to formulate an answer to a current issues question.The FrameworkThe examiner’s advice is that if you are not sure where to start your answer to a current issues question, then begin with the Framework . The Framework for Financial Reporting sets out theconceptual basis for the development of standards, and is itself based on the elements of assets and liabilities. T o paraphrase the Framework , ‘an asset/liability is a right/obligation to a future economic outflow/inflow’. This focus on financial position has permeated all the standards issued in recent years, and continues to dominate current issues.But the Framework also refers to other concepts, such as relevance, reliability and entity. Which brings us to fair value.Fair valueThis is the hot topic in financial reporting. In order to make the position statement a genuine statement of financial position, rather than simply a balance sheet, the International Accounting StandardsBoard (IASB) has been pushing financial reporting towards fair value. Fair value accounting attempts to present all assets and liabilities at market value and, as such, is highly subjective. But the IASB is prepared to accept reduced reliability in favour of increased relevance.ConvergenceAlso red hot is the subject of convergence, which the IASB interprets essentially as the convergence of IFRS with US accounting. This process has received a major boost in recent months, with the US Securities and Exchange Commission (SEC) coming out in favour of fair value and the IASB.Business combinationsTangled up in the process of convergence is the project to make sense of group accounting. The IASB has long accepted that the US slant on groups was better suited to the entity concept and the reality of acquisitions. So the IASB issued and reissued IFRS 3, Business Combinations , in order to reflect this. But perhaps the rarity of non-controlling interest (NCI) in the US has led to the IASB creating unnecessary complications as regards the NCI goodwill.Management commentaryThe spiralling complexity of financial reporting has led to most companies translating theirfinancial statements into a more digestible report, tagged on to the financial statements in the annual report. This ‘management commentary’ is largely unregulated at the moment, but the IASB has a standard under development that, once issued, will produce some conformity in management commentaries.ILLUSTRATIVE QUESTIONThe following is an illustrative current issues question. It is partly based on past examples of Question 4, but it also looks forward to currentissues that are topical now and which will remain so for the next few sittings. So the question, therefore, takes its lead from the examiner, Graham Holt, and his comments (made at the February 2009 ACCA teachers’ conference) that lecturers should try to write questions of the future, especially in the context of current issues. As you look through the question, you will note the use of numbers, rarely seen in previous Question 4 examples. This also takes its lead from the examiner’s comments at the conference, when he warned that future current issues questions might use numbers to draw out conceptual issues.currentC U R R E N T I S S U E S A R E A T T h E h E A R T O F P A P E R P 2, C O R P O R A T E R E P O R T I N g , A N d P E R M E A T E T h E E N T I R E S y L L A B U S . B U T I T I S T h E L A S T Q U E S T I O N I N T h E E x A M P A P E R , Q U E S T I O N 4, T h A T R E A L L y d E L V E S I N T O T h E P O L I T I C A L A N d I N T E L L E C T U A L d E B A T E T h A T R E P R E S E N T S C U R R E N T I S S U E S I N F I N A N C I A L R E P O R T I N g .RELEVANT TO ACCA QUALIFICATION PAPER P2Studying Paper P2? Performance Objectives 10 and 11 are linkedQuestion 4: FudgeFudge is a medium-sized industrial group that is listed on a major world stock exchange. It has finally succeeded in acquiring a controlling interest in its principle supplier, Sugar. This acquisition is seen by the board as a great achievement, since in the past, concerns over supply have frustrated the Board and worried the shareholders.You are advising the chief finance officer (CFO) regarding the issues raised by the acquisition.She has various concerns, most of which relateto the financial reporting of the acquisitionand the conceptual reasons underlying the financial reporting. The acquisition of Sugar was achieved in stages. Sugar is a traditional raw materials supplier and had, until recently, been under family ownership and control. Fudge has, for a number of years, been in negotiations with the family to purchase shares, but only last year, for the first time, was Fudge offered shares in Sugar. Fudge purchased 25% (25,000 shares) at the end of last year for $2m, and obtained a seat on the main Board. The fair value of the identifiable net assets of Sugar at that time was $4m.Last week, Fudge acquired a further 35% (35,000 shares) for $3.5m and obtained control. The fair value of the identifiable net assets of Sugar at this second point of purchase was $5m. The fair value of the previous ownership of 25% was measuredat $2.25m, and the fair value of the NCI was measured at $3.2m. These latter two fair values have been measured using appropriate models.It is approaching the year end, and the CFO wants to understand how the above purchasewill be reported, both in the financial statements and elsewhere. She understands that there arenew rules regulating group accounting, and that these have been motivated partly by the need for global accounting convergence. She is particularly keen to understand the underlying principles behind the accounting and also the application of fair value to the process of measuring goodwill. However, she is also concerned that the acquisition, which is a major strategic success, might not be communicated to shareholders appropriately,because the focus is primarily on the accounting.Negotiations with Sugar shareholders continue,and Fudge hopes to purchase a further 10%(10,000 shares) early next year. It is expectedthat the consideration will be $1m, and that theidentifiable net assets of Sugar will be $6m at thisanticipated third point of purchase. The CFO wouldlike to understand how this third purchase will bereported, should it go ahead. Goodwill remainsunimpaired throughout. The group has the policy ofrecognising full goodwill.RequiredWrite a report for the CFO that addresses thefollowing requirements:(a) Calculate the goodwill attributable to Sugar atthe current year end. Explain the conceptualbasis for the calculation of goodwill.(13 marks)(b) Explain how the important strategic reasonsfor the acquisition could be communicated toFudge shareholders.(5 marks)(c) Calculate the transfer in equity and thereduction to equity that is attributable to theparent shareholders that would result fromthe third purchase, assuming it occurs aspredicted. Explain the conceptual basis forthis transfer.(7 marks)(Total 25 marks)Comments on the questionPerhaps the first thing to advise in the contextof a question like this is: ‘do not becomeobsessed by the numbers’. It is clear from theexaminer’s comments that group accountingunder IFRS 3 (Revised) will be an important topicfor examination in the future. It is also clearthat the examiner’s articles in the February andApril 2009 issues of student accountant will beimportant. But it is also clear from the questionabove that discussion of the issues is at least asimportant as the numbers.ThEFIRSTThINgTOAdVISEINThECONTExTOFAQUESTIONLIkEThISIS:‘dONOTBECOMEOBSESSEdByThENUMBERS’.ITISCLEARFROMThEExAMINER’SCOMMENTSThATgROUPACCOUNTINgUNdERIFRS3(REVISEd)wILLBEANIMPORTANTTOPICFORExAMINATIONINThEFUTURE.issuesI would also advise students not to try to be too clever. The examiner regularly complains of answers that are technically wonderful, but which do not answer the question and therefore achieve few marks. So do not attempt to dazzle markers with excessive detail; instead, use your understanding of the key issues to simply and clearly answer the question. MOdEL ANSwERReportTo: Chief Finance OfficerFrom: Medate: TodaySubject: Acquisition issuesIntroductionThe following report discusses the issues raised by the acquisition of Sugar.(a) The financial reporting of the acquisitiongoodwillThe goodwill in Sugar at the point of obtaining control at the coming year end will be calculatedas follows:$’000 Fair value of consideration 35% 3,500 Fair value of previous ownership 25% 2,250 Fair value of NCI 40% 3,200 Fair value of the business 100% 8,950 Fair value of net assets (5,000) Goodwill at acquisition 3,950(Calculation worth 5 marks) Conceptual basisThe above calculation is based on the entity concept within the Framework for Financial Reporting. This concept notes that the group is one entity under the control of the parent shareholders. This key concept notes that the parent has control over the parent assets and liabilities, as well as the assets and liabilities of the sub.Parent viewpointFrom the point of view of the parent as a singleentity, the parent simply acquires first 25,000shares, then another 35,000 shares. So the parentsees two purchases.group viewpointBut the group perspective is quite different. Thegroup acquires the sub when it obtains control, andclearly that happens when the second purchase of35,000 shares occurs. That is the point at which thesub enters the group.EffectThe effect of this is that we must recognise only onepoint of acquisition of the sub. In order to achievethis, we deem the group to have sold its associateand acquired a sub at the point the group obtainscontrol. So the first 25,000 shares are deemed tohave been sold and then immediately bought backat fair value at acquisition.Fair valueThis leads to one of the more unusual features ofIFRS 3 (Revised). The fair value of the shares deemedsold and bought back need not be in line with that ofthose actually acquired (or even those retained) bythe NCI. A simple calculation can show this:Share volume Fair value given Fair value pershare35,000 $3.5m $10025,000 $2.25m $9040,000 $3.2m $80Fair value elsewhereThe above divergent fair value is most odd, giventhat in other situations, for example, the fairvaluation of financial assets at fair value with gainsand losses to the profit and loss, the transactionprice on one share gives the fair value of all theothers at this point. This divergence of fair valueresults in goodwill attributable to the NCI far belowthat of the goodwill attributable to the controllinginterest. This makes part (c) below much harder.ThEExAMINERREgULARLyCOMPLAINSOFANSwERSThATARETEChNICALLywONdERFUL,BUTwhIChdONOTANSwERThEQUESTIONANdThEREFOREAChIEVEFEwMARkS.SOdONOTATTEMPTTOdAzzLEMARkERSwIThExCESSIVEdETAIL;INSTEAd,USEyOURUNdERSTANdINgOFThEkEyISSUESTOSIMPLyANdCLEARLyANSwERThEQUESTION.Sugar acquisitionThe Sugar acquisition is exactly the kind of issue that management commentary is designed to accommodate. The numbers, as presented in the financial statements, do not give the reader a flavour of the purpose behind the purchase.PresentationThe Fudge group should use the managementcommentary to explain the importance of the Sugar acquisition in terms of supply stability, and should also explain the extended negotiations that resulted in the step acquisition.RegulationThe IASB has published a discussion document on management commentaries, and the group should read this before publishing. The group should also look at other management commentaries and at how others have dealt with acquisitions.websiteThe group should also consider using its website to communicate the acquisition, maybe even considering a press conference.(1 mark per point to give 6 marks for discussion) (c) The financial reporting of the transferTransferThe following will transfer out of NCI:$’000Net assets attributable to NCI at transfer (40%)($6m)2,400Goodwill attributable to NCI at transfer (unchanged from (a))1,200NCI before transfer of 10% ownership 3,600Transfer to controlling equity (10%/40%) (900)NCI remaining2,700(Calculation worth 3 marks)N O T E T h E S T y L E O F T h E A N S w E R . T h E L A N g U A g E I S S I M P L E A N d T h E I d E A S A R E C L E A R . B U T N O T I C E A L S O h O w T h E A N S w E R h A S B E E N T U N E d T O T h E M A R k I N g g U I d E F O R Q U E S T I O N 4, S U M M E d U P B y T h E E x A M I N E R A S ‘S U B j E C T I V E : 1 M A R k P E R P O I N T ’. S E E h O w M y A N S w E R U S E S O N E h E A d I N g F O R E A C h P O I N T T O A I d T h E M A R k I N g P R O C E S S .goodwill splitGoodwill is split between the controlling and the NCI as follows: $’000Goodwill (controlling interest) (3,500 + 2,250 - (60%)(5,000)) 2,750Goodwill (NCI) (3,200 - (40%)(5,000)) 1,200Goodwill at acquisition (see above) 3,950Notice that the NCI is 40%, but that they own less than one third of the goodwill.ConvergenceIt is true that the revision of IFRS 3 was motivated by the desire to improve financial reporting in the context of the entity concept. However , it is also true that the project has been dominated by the desire to converge IFRS with US accounting standards.(1 mark per point to give 9 marks for discussion, therefore one extra point)(b) The communication with shareholdersManagement commentaryManagement commentary is the generic name for the unaudited operating and financial review that accompanies most financial statements in the annual report presented to shareholders.The ideaThe idea of this report is to translate the performance and position of the group from the hard numbers, as presented in the financial statements, into softer words and pictures for easier understanding.COMMENTS ON ThE ANSwERNote the style of the answer . The language issimple and the ideas are clear . But notice also how the answer has been tuned to the marking guide for Question 4, summed up by the examiner as ‘Subjective: 1 mark per point’. See how my answer uses one heading for each point to aid the marking process. Also notice that when I am aiming for five marks, I give six points.Next, note that the answer draws widely from across current issues. Of course, the answer isfounded on the new IFRS on business combinations, but look how I bring in the conceptual framework, fair value, convergence, management commentary, and other issues.Finally, note that ‘subjective’ implies that there are other issues that could alternatively have been discussed, and the following would all have been acceptable:¤ Accounting for the entity, Sugar, over the year in the statement of comprehensive income, would have been as an associate up to acquisition and as a sub thereafter .¤ The deemed disposal of the associate atacquisition would generate a profit on disposal.¤ The models used for share valuation are highly subjective and open to manipulation.¤ The family company was privately owned and that is why there is no market price before or after the acquisition.The examiner has, on numerous occasions, made it clear that alternative answers that consider alternative issues are welcomed by markers.CONCLUSIONI recommend that students review and workthrough past current issues questions to improve their knowledge of current issues, improve their delivery of clear answers, and draw from the broad range of issues discussed above to demonstrate their understanding.Martin Jones is a lecturer at the London School of Business and FinanceReduction in the equity attributable to the parent shareholdersThe above transfer into controlling equity will meet the cost of the consideration to create the following reduction: $’000Transfer to controlling equity (above) 900Consideration cost recognised directly in equity (1,000)Reduction to equity that is attributable to the parent shareholders (100)(Calculation worth 1 mark)Conceptual basisThe above financial reporting is again based on the entity concept and the related concept of control. Once the group has absolute control of the sub at acquisition, then the group has control. This occurred last week when the 35,000 shares were purchased.ControlControl is an absolute: either you have it or you do not. The group cannot get more control by buying more shares later .OwnershipOwnership is quite different. Clearly, if the group does increase its ownership to 70%, then the NCI will decrease to 30%. This results in the transfer between the equity owners, from non-controlling to controlling.goodwillIf Fudge successfully purchases the further10,000 shares, this will not be a sub acquisition. Therefore, if there is no acquisition, there is no new goodwill calculation.(1 mark per point to give 4 marks for discussion)I R E C O M M E N d T h A T S T U d E N T S R E V I E w A N d w O R k T h R O U g h P A S T C U R R E N T I S S U E S Q U E S T I O N S T O I M P R O V E T h E I R k N O w L E d g E O F C U R R E N T I S S U E S , T O I M P R O V E T h E I R d E L I V E R y O F C L E A R A N S w E R S , A N d d R A w F R O M T h E B R O A d R A N g E O F I S S U E S d I S C U S S E d A B O V E T O d E M O N S T R A T E T h E I R U N d E R S T A N d I N g .。