10st-plant assets

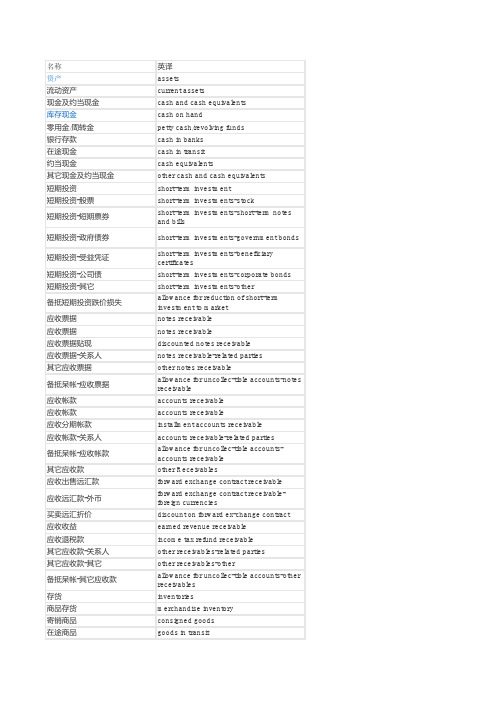

会计科目中英文对照

名称英译资产assets流动资产current assets现金及约当现金cash and cash equivalents库存现金cash on hand零用金/周转金petty cash/revolving funds银行存款cash in banks在途现金cash in transit约当现金cash equivalents其它现金及约当现金other cash and cash equivalents短期投资short-term investment短期投资-股票short-term investments-stock短期投资-短期票券short-term investments-short-term notesand bills短期投资-政府债券short-term investments-government bonds短期投资-受益凭证short-term investments-beneficiarycertificates短期投资-公司债short-term investments-corporate bonds 短期投资-其它short-term investments-other备抵短期投资跌价损失allowance for reduction of short-terminvestment to market应收票据notes receivable应收票据notes receivable应收票据贴现discounted notes receivable应收票据-关系人notes receivable-related parties其它应收票据other notes receivable备抵呆帐-应收票据allowance for uncollec-tible accounts-notesreceivable应收帐款accounts receivable应收帐款accounts receivable应收分期帐款installment accounts receivable应收帐款-关系人accounts receivable-related parties备抵呆帐-应收帐款allowance for uncollec-tible accounts-accounts receivable其它应收款other Receivables应收出售远汇款forward exchange contract receivable应收远汇款-外币forward exchange contract receivable-foreign currencies买卖远汇折价discount on forward ex-change contract应收收益earned revenue receivable应收退税款income tax refund receivable其它应收款-关系人other receivables-related parties其它应收款-其它other receivables-other备抵呆帐-其它应收款allowance for uncollec-tible accounts-otherreceivables存货inventories商品存货merchandise inventory寄销商品consigned goods在途商品goods in transit备抵存货跌价损失allowance for reduction of inventory tomarket制成品finished goods寄销制成品consigned finished goods副产品by-products在制品work in process委外加工work in process-Outsourced原料raw materials物料supplies在途原物料materials and supplies in transit备抵存货跌价损失allowance for reduction of inventory tomarket预付费用prepaid expenses预付薪资prepaid payroll预付租金prepaid rents预付保险费prepaid insurance用品盘存office supplies预付所得税prepaid income tax其它预付费用other prepaid expenses预付款项prepayments预付货款prepayment for purchases其它预付款项other prepayments其它流动资产other current assets进项税额VAT paid ( or input tax)留抵税额excess VAT paid (or overpaid VAT)暂付款temporary payments代付款payment on behalf of others员工借支advances to employees存出保证金refundable deposits受限制存款certificate of deposit-restricted递延所得税资产deferred income tax assets递延兑换损失deferred Foreign Exchange losses业主往来(股东往来)owners'(stockholders') current account 同业往来current account with others其它流动资产-其它other current assets-other基金及长期投资funds and long-term investments基金funds偿债基金redemption fund (or sinking fund)改良及扩充基金fund for improvement and expansion 意外损失准备基金contingency fund退休基金pension fund其它基金other funds长期投资long-term investments长期股权投资long-term equity investments长期债券投资long-term bond investments长期不动产投资long-term real estate in-vestments人寿保险现金解约价值cash Surrender value of life insurance 其它长期投资other long-term investments备抵长期投资跌价损失allowance for excess of cost over marketvalue of long-term investments固定资产property , plant, and equipment土地land土地land土地-重估增值land-revaluation increments土地改良物land improvements土地改良物land improvements土地改良物-重估增值land improvements-revaluation increments累积折旧-土地改良物accumulated depreciation-landimprovements房屋及建物buildings房屋及建物buildings房屋及建物-重估增值buildings-revaluation increments累积折旧-房屋及建物accumulated depreciation-buildings机(器)具及设备machinery and equipment机(器)具machinery机(器)具-重估增值machinery-revaluation increments累积折旧-机(器)具accumulated depreciation-machinery租赁资产leased assets租赁资产leased assets累积折旧-租赁资产accumulated depreciation-leased assets 租赁权益改良leasehold improvements租赁权益改良leasehold improvements累积折旧-租赁权益改良accumulated depreciation-leaseholdimprovements未完工程及预付购置设备款construction in progress and prepaymentsfor equipment未完工程construction in progress预付购置设备款prepayment for equipment杂项固定资产miscellaneous property, plant, andequipment杂项固定资产miscellaneous property, plant, andequipment杂项固定资产-重估增值miscellaneous property, plant, andequipment-revaluation increments累积折旧-杂项固定资产accumulated depreciation-miscellaneousproperty, plant, and equipment递耗资产depletable assets递耗资产depletable assets天然资源natural resources重估增值-天然资源natural resources-revaluation increments 累积折耗-天然资源accumulated depletion-natural resources 无形资产intangible assets商标权trademarks商标权trademarks专利权patents专利权patents特许权franchise特许权franchise著作权copyright著作权copyright计算机软件Computer Software计算机软件computer software cost商誉goodwill商誉goodwill开办费organization costs开办费organization costs其它无形资产other intangibles递延退休金成本deferred pension costs租赁权益改良leasehold improvements其它无形资产-其它other intangible assets-other其它资产other assets递延资产deferred assets债券发行成本deferred bond issuance costs长期预付租金long-term prepaid rent长期预付保险费long-term prepaid insurance递延所得税资产deferred income tax assets预付退休金prepaid pension cost其它递延资产other deferred assets闲置资产idle assets闲置资产idle assets长期应收票据及款项与催收帐款long-term notes , accounts and overduereceivables长期应收票据long-term notes receivable长期应收帐款long-term accounts receivable催收帐款overdue receivables长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables-related parties其它长期应收款项other long-term receivables备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts-long-term notes, accounts and overdue receivables出租资产assets leased to others出租资产assets leased to others出租资产-重估增值assets leased to others-incremental valuefrom revaluation累积折旧-出租资产accumulated depreciation-assets leased toothers存出保证金refundable deposit存出保证金refundable deposits杂项资产miscellaneous assets受限制存款certificate of deposit-restricted杂项资产-其它miscellaneous assets-other负债liabilities流动负债current liabilities短期借款short-term borrowings(debt)银行透支bank overdraft银行借款bank loan短期借款-业主short-term borrowings-owners短期借款-员工short-term borrowings-employees短期借款-关系人short-term borrowings-related parties短期借款-其它short-term borrowings-other应付短期票券short-term notes and bills payable应付商业本票commercial paper payable银行承兑汇票bank acceptance其它应付短期票券other short-term notes and bills payable 应付短期票券折价discount on short-term notes and billspayable应付票据notes payable应付票据notes payable应付票据-关系人notes payable-related parties其它应付票据other notes payable应付帐款accounts pay able应付帐款accounts payable应付帐款-关系人accounts payable-related parties应付所得税income taxes payable应付所得税income tax payable应付费用accrued expenses应付薪工accrued payroll应付租金accrued rent payable应付利息accrued interest payable应付营业税accrued VAT payable应付税捐-其它accrued taxes payable-other其它应付费用other accrued expenses payable其它应付款other payables应付购入远汇款forward exchange contract payable应付远汇款-外币forward exchange contract payable-foreigncurrencies买卖远汇溢价premium on forward exchange contract应付土地房屋款payables on land and building purchased 应付设备款Payables on equipment其它应付款-关系人other payables-related parties应付股利dividend payable应付红利bonus payable应付董监事酬劳compensation payable to directors andsupervisors其它应付款-其它other payables-other预收款项advance receipts预收货款sales revenue received in advance预收收入revenue received in advance其它预收款other advance receipts一年或一营业周期内到期长期负债long-term liabilities-current portion一年或一营业周期内到期公司债corporate bonds payable-current portion一年或一营业周期内到期长期借款long-term loans payable-current portion一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties-current portion其它一年或一营业周期内到期长期负债other long-term lia-bilities-current portion 其它流动负债other current liabilities销项税额VAT received(or output tax)暂收款temporary receipts代收款receipts under custody估计售后服务/保固负债estimated warranty liabilities递延所得税负债deferred income tax liabilities递延兑换利益deferred foreign exchange gain业主(股东)往来owners' current account同业往来current account with others其它流动负债-其它other current liabilities-others长期负债long-term liabilities应付公司债corporate bonds payable应付公司债corporate bonds payable应付公司债溢价(折价)premium(discount) on corporate bondspayable长期借款long-term loans payable长期银行借款long-term loans payable-bank长期借款-业主long-term loans payable-owners长期借款-员工long-term loans payable-employees长期借款-关系人long-term loans payable-related parties 长期借款-其它long-term loans payable-other长期应付票据及款项long-term notes and accounts payable长期应付票据long-term notes payable长期应付帐款long-term accounts pay-able长期应付租赁负债long-term capital lease liabilities长期应付票据及款项-关系人Long-term notes and accounts payable-related parties其它长期应付款项other long-term payables估计应付土地增值税accrued liabilities for land value incrementtax估计应付土地增值税estimated accrued land value incrementaltax pay-able应计退休金负债accrued pension liabilities应计退休金负债accrued pension liabilities其它长期负债other long-term liabilities其它长期负债-其它other long-term liabilities-other其它负债other liabilities递延负债deferred liabilities递延收入deferred revenue递延所得税负债deferred income tax liabilities其它递延负债other deferred liabilities存入保证金deposits received存入保证金guarantee deposit received杂项负债miscellaneous liabilities杂项负债-其它miscellaneous liabilities-other业主权益owners' equity资本capital资本(或股本)capital普通股股本capital-Common stock特别股股本capital-preferred stock预收股本capital collected in advance待分配股票股利stock dividends to be distributed资本capital资本公积additional paid-in capital股票溢价paid-in capital in excess of par普通股股票溢价paid-in capital in excess of par-commonstock特别股股票溢价paid-in capital in excess of par-preferredstock资产重估增值准备capital surplus from assets revaluation资产重估增值准备capital surplus from assets revaluation处分资产溢价公积capital surplus from gain on disposal ofassets处分资产溢价公积capital surplus from gain on disposal ofassets合并公积capital surplus from business combination 合并公积capital surplus from business combination 受赠公积donated surplus受赠公积donated surplus其它资本公积other additional paid-in capital权益法长期股权投资资本公积additional paid-in capital from investeeunder equity method资本公积-库藏股票交易additional paid-in capital-treasury stocktrans-actions保留盈余(或累积亏损)retained earnings (accumulated deficit)法定盈余公积legal reserve法定盈余公积legal reserve特别盈余公积special reserve意外损失准备contingency reserve改良扩充准备improvement and expansion reserve偿债准备special reserve for redemption of liabilities 其它特别盈余公积other special reserve未分配盈余(或累积亏损)retained earnings-unappropriated (oraccumulated deficit)累积盈亏accumulated profit or loss前期损益调整prior period adjustments本期损益net income or loss for current period权益调整equity adjustments长期股权投资未实现跌价损失unrealized loss on market value decline oflong-term equity investments长期股权投资未实现跌价损失unrealized loss on market value decline oflong-term equity investments累积换算调整数cumulative translation adjustment累积换算调整数cumulative translation adjustments未认列为退休金成本之净损失net loss not recognized as pension cost 未认列为退休金成本之净损失net loss not recognized as pension costs 库藏股treasury stock库藏股treasury stock库藏股treasury stock少数股权minority interest少数股权minority interest少数股权minority interest营业收入operating revenue销货收入sales revenue销货收入sales revenue销货收入sales revenue分期付款销货收入installment sales revenue销货退回sales return销货退回sales return销货折让sales allowances销货折让sales discounts and allowances劳务收入service revenue劳务收入service revenue劳务收入service revenue业务收入agency revenue业务收入agency revenue业务收入agency revenue其它营业收入other operating revenue其它营业收入-其它other operating revenue其它营业收入-其它other operating revenue-other营业成本operating costs销货成本cost of goods sold销货成本cost of goods sold销货成本cost of goods sold分期付款销货成本installment cost of goods sold进货purchases进货purchases进货费用purchase expenses进货退出purchase returns进货折让charges on purchased merchandise进料materials purchased进料material purchased进料费用charges on purchased material进料退出material purchase returns进料折让material purchase allowances直接人工direct labor直接人工direct labor制造费用manufacturing overhead间接人工indirect labor租金支出rent expense, rent文具用品office supplies (expense)旅费travelling expense, travel运费shipping expenses, freight邮电费postage (expenses)修缮费repair(s) and maintenance (expense )包装费packing expenses水电瓦斯费Utilities (expense)保险费insurance (expense)加工费manufacturing overhead-outsourced 税捐taxes折旧depreciation expense各项耗竭及摊提various amortization伙食费meal (expenses)职工福利employee benefits/welfare训练费training (expense)间接材料indirect materials其它制造费用other manufacturing expenses劳务成本制ervice costs劳务成本service costs劳务成本service costs业务成本gency costs业务成本agency costs业务成本agency costs其它营业成本other operating costs其它营业成本-其它other operating costs-other其它营业成本-其它other operating costs-other营业费用operating expenses推销费用selling expenses推销费用selling expenses薪资支出payroll expense租金支出rent expense, rent文具用品office supplies (expense)旅费travelling expense, travel运费shipping expenses, freight邮电费postage (expenses)修缮费repair(s) and maintenance (expense)广告费advertisement expense, advertisement 水电瓦斯费utilities (expense)保险费insurance (expense)交际费entertainment (expense)捐赠donation (expense)税捐taxes呆帐损失loss on uncollectible accounts折旧depreciation expense各项耗竭及摊提various amortization伙食费meal (expenses)职工福利employee benefits/welfare佣金支出commission (expense)训练费training (expense)其它推销费用other selling expenses管理及总务费用general & administrative expenses管理及总务费用general & administrative expenses薪资支出payroll expense租金支出rent expense, rent文具用品office supplies旅费travelling expense, travel运费shipping expenses,freight邮电费postage (expenses)修缮费repair(s) and maintenance (expense)广告费advertisement expense, advertisement水电瓦斯费utilities (expense)保险费insurance (expense)交际费entertainment (expense)捐赠donation (expense)税捐taxes呆帐损失loss on uncollectible accounts折旧depreciation expense a各项耗竭及摊提various amortization外销损失loss on export sales伙食费meal (expenses)职工福利employee benefits/welfare研究发展费用research and development expense佣金支出commission (expense)训练费training (expense)劳务费professional service fees其它管理及总务费用other general and administrative expenses 研究发展费用research and development expenses研究发展费用research and development expenses薪资支出payroll expense租金支出rent expense, rent文具用品office supplies旅费travelling expense, travel运费shipping expenses, freight邮电费postage (expenses)修缮费repair(s) and maintenance (expense)水电瓦斯费utilities (expense)保险费insurance (expense)交际费entertainment (expense)税捐taxes折旧depreciation expense各项耗竭及摊提various amortization伙食费meal (expenses)职工福利employee benefits/welfare训练费training (expense)其它研究发展费用other research and development expenses营业外收入及费用non-operating revenue and expenses,other income(expense)营业外收入non-operating revenue利息收入interest revenue利息收入interest revenue/income投资收益investment income权益法认列之投资收益investment income recognized under equitymethod股利收入dividends income短期投资市价回升利益gain on market price recovery of short-terminvestment兑换利益foreign exchange gain兑换利益foreign exchange gain处分投资收益gain on disposal of investments处分投资收益gain on disposal of investments处分资产溢价收入gain on disposal of assets处分资产溢价收入gain on disposal of assets其它营业外收入other non-operating revenue捐赠收入donation income租金收入rent revenue/income佣金收入commission revenue/income出售下脚及废料收入revenue from sale of scraps存货盘盈gain on physical inventory存货跌价回升利益gain from price recovery of inventory坏帐转回利益gain on reversal of bad debts其它营业外收入-其它other non-operating revenue-other items 营业外费用non-operating expenses利息费用interest expense利息费用interest expense投资损失investment loss权益法认列之投资损失investment loss recog-nized under equitymethod短期投资未实现跌价损失unrealized loss on reduction of short-terminvestments to market兑换损失foreign exchange loss兑换损失foreign exchange loss处分投资损失loss on disposal of investments处分投资损失loss on disposal of investments处分资产损失loss on disposal of assets处分资产损失loss on disposal of assets其它营业外费用other non-operating expenses停工损失loss on work stoppages灾害损失casualty loss存货盘损loss on physical inventory存货跌价及呆滞损失loss for market price decline and obsoleteand slow-moving inventories其它营业外费用-其它other non-operating expenses-other所得税费用(或利益)income tax expense (or benefit)所得税费用(或利益)income tax expense (or benefit)所得税费用(或利益)income tax expense (or benefit)所得税费用(或利益)income tax expense ( or benefit)非经常营业损益nonrecurring gain or loss停业部门损益gain(loss) from discontinued operations停业部门损益-停业前营业损益income(loss) from operations ofdiscontinued segments停业部门损益-停业前营业损益income(loss) from operations ofdiscontinued segment停业部门损益-处分损益gain(loss) from disposal of discontinuedsegments停业部门损益-处分损益gain(loss) from disposal of discontinuedsegment非常损益extraordinary gain or loss非常损益extraordinary gain or loss非常损益extraordinary gain or loss会计原则变动累积影响数cumulative effect of changes in accountingprinciples会计原则变动累积影响数cumulative effect of changes in accountingprinciples会计原则变动累积影响数cumulative effect of changes in accountingprinciples少数股权净利minority interest income少数股权净利minority interest income少数股权净利minority interest incom。

Chapter 7:Plant assets & Intangibles固定资产

Types of Assets

• Land • Buildings, machinery, equipment • Land improvements and leasehold improvements • Lump-sum (or basket) purchases of assets

Measuring the cost of a plant asset

EXERCISE-Choice

• Which of the following is NOT an intangible asset? • a. mineral rights • b. patent • c. copyright • d. goodwill • (a)

EXERCISE-Choice

Land improvements and leasehold improvements

• Land improvements accounts includes costs for such other items as driveways, signs, fences, and sprinkler systems. • Leasehold improvements.

Capital Expenditures

• Accounting errors sometimes occur for plant asset costs, for example, a company may:

Chapter-16-Plant-Assets

16-11

Cost

If a plant asset is purchased on credit the interests are not included in cost, but as expense for this period.

However, if the assets are constructed, the interests during the construction should be calculated as part of cost of the asset.

Fair value refers to the amount which is agreed by

two sides that are familiar with the transaction.

fair value

all the expenses incurred during the period when the donation is received

16-13

Depreciable cost

Depreciable value = The cost of an asset- Residual value

For example, if furniture’s cost is $10,000 and its residual value is $4,000, its depreciable cost will be $6,000.

西方财务会计_chapter8

5/1 Equipment 10593

Discount on Note payable

2407

Cash

3000

Notes payable

10000

12/31 interest expense 607

Discount on Note payable

607

($7593*12%*8/12=$607)

Depreciation exp. 706

6,000 100,000

19

Nonmonetary Transactions (Exchanges)

The types of nonmonetary exchanges we will be looking at are as follows:

$ 6,000

18

Prepare the journal entry to record the sale.

Date

Description

Sept. 30 Cash

Accumulated Depreciation

Gain on Sale

Machinery

Debit

60,000 46,000

Credit

3,000 1,000

4,000

13

Selling a Plant Asset

For book value: no gain or loss(example 1) Above book value: a gain is recorded(example 2) Below book value:a loss is recorded(example 3)

Compute the cost of Heat Co.’s new machine.

《会计学》(第7版)试题库 horngren_acct7_ch10tif

Chapter 10: Plant Assets and Intangibles1)The cost of land includes the cost of removing unwanted buildings.Answer:TRUEDiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-12)The cost of fencing around a building is included in the cost of the building.Answer:FALSEDiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-13)Treating a capital expenditure as an expense causes an understatement of net income.Answer:TRUEDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-14)Tangible assets are assets with no physical form that have value because of the special rightsthey carry.Answer:FALSEDiff: 1Page Ref: 506, 525Objective: 10-1EOC Ref: S10-15)The three major depreciation methods are straight-line, declining-balance, and specificidentification.Answer:FALSEDiff: 1Page Ref: 511Objective: 10-2EOC Ref: S10-46)Estimated residual value is the expected cash value of an asset at the end of its useful life.Answer:TRUEDiff: 1Page Ref: 511Objective: 10-2EOC Ref: S10-47)The straight-line method of depreciation assigns a fixed amount of depreciation to each unit ofoutput produced by an asset.Answer:FALSEDiff: 1Page Ref: 512Objective: 10-2EOC Ref: S10-48)Accelerated depreciation differs from straight line depreciation in that depreciation expense isgreater in the first year and less in the later years.Answer:TRUEDiff: 1Page Ref: 513Objective: 10-2EOC Ref: S10-49)The units-of-production method of depreciation always writes off more of the assetʹs cost nearthe start of its useful life than the declining-balance method.Answer:FALSEDiff: 1Page Ref: 513Objective: 10-3EOC Ref: S10-610)The double-declining balance method of depreciation computes annual depreciation bymultiplying the assetʹs decreasing book value by a constant percent that is two times thestraight-line rate.Answer:TRUEDiff: 1Page Ref: 513Objective: 10-3EOC Ref: S10-611)The MACRS depreciation method, required for purposes of determining taxable income,computes depreciation by using 150% declining balance depreciation (rather thandouble-declining balance) for most assets with a useful life of less than 20 years.Answer:FALSEDiff: 2Page Ref: 519Objective: 10-3EOC Ref: S10-612)For tax purposes, accelerated depreciation is generally preferable to straight-line becauseaccelerated depreciation reduces taxable income and taxes due.Answer:TRUEDiff: 1Page Ref: 519Objective: 10-3EOC Ref: S10-613)A loss on the sale of a plant asset is recorded when the sales price exceeds the book value.Answer:FALSEDiff: 1Page Ref: 522Objective: 10-4EOC Ref: S10-914)If assets are junked before being fully depreciated, there is a loss equal to the book value of theasset.Answer:TRUEDiff: 1Page Ref: 521Objective: 10-4EOC Ref: S10-915)A loss occurs on the exchange of a plant asset if the market value of the new asset received isgreater than the total amount given up in the exchange.Answer:FALSEDiff: 1Page Ref: 523, 524Objective: 10-4EOC Ref: S10-1016)A gain on the exchange of a plant asset is not recorded, but results in a smaller basis in thenew asset received.Answer:TRUEDiff: 1Page Ref: 523, 524Objective: 10-4EOC Ref: S10-1017)Depletion expense is the portion of a natural resourceʹs cost used up in a particular period.Answer:TRUEDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1118)Accumulated depletion is a contra-liability account.Answer:FALSEDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1119)Goodwill is not amortized, but evaluated each year for a decline in value.Answer:TRUEDiff: 2Page Ref: 526, 527Objective: 10-6EOC Ref: S10-1320)A patent is an exclusive right to reproduce and sell a book, musical composition, film, otherwork of art, or computer program, and must be amortized over the useful life of the patent.Answer:FALSEDiff: 2Page Ref: 526Objective: 10-6EOC Ref: S10-1321)Which of the following are included in the cost of land?A)The cost of clearing the landB)The cost of fencingC)The cost of pavingD)The cost of outdoor lightingAnswer:ADiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-122)Which of the following is included in the cost of a plant asset?A)The purchase price of the plant assetB)The taxes paidC)Amounts paid to ready the asset for its intended useD)All of the aboveAnswer:DDiff: 1Page Ref: 506Objective: 10-1EOC Ref: S10-123)Which of the following assets groups includes fencing?A)BuildingsB)LandC)Land improvementsD)Machinery and equipmentAnswer:CDiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-124)Which of the following assets groups includes the cost of clearing land and removingunwanted buildings?A)BuildingsB)LandC)Land improvementsD)Machinery and equipmentAnswer:BDiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-125)Which of the following is NOT considered a plant asset?A)LandB)BuildingC)CopyrightD)EquipmentAnswer:CDiff: 1Page Ref: 507, 508, 526Objective: 10-1EOC Ref: S10-126)Which of the following is a characteristic of a plant asset?A)The asset is used in the production of income for the business.B)The asset is available for resale to customers in the ordinary course of business.C)The asset lacks physical form.D)Both A and B are characteristics of a plant asset.Answer:ADiff: 1Page Ref: 506Objective: 10-1EOC Ref: S10-127)Hastings Company has purchased a group of assets for $350,000. The assets and their marketvalues are listed as follows:Land $125,000Equipment 75,000Building 200,000Which of the following amounts would be debited to the Land account?A)$ 65,625B)109,375C)125,000D)175,000Answer:BDiff: 1Page Ref: 507Objective: 10-1EOC Ref: S10-228)Which of the following would be capitalized and depreciated rather than expensed?A)Repair of engineB)Replacement of tiresC)Paint jobD)Modification for new useAnswer:DDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-329)Which of the following would be expensed rather than capitalized?A)Major engine overhaulB)Modification for new useC)Oil change and lubricationD)Addition to storage capacityAnswer:CDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-330)A companyʹs accountant capitalizes a payment that should be recorded as an expense. Whichof the following is TRUE?A)Assets are overstated.B)Liabilities are overstated.C)Revenue is overstated.D)Expenses are overstated.Answer:ADiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-331)A companyʹs accountant expenses a payment that should be capitalized. Which of thefollowing is TRUE?A)Assets are overstated.B)Liabilities are overstated.C)Revenue is overstated.D)Expenses are overstated.Answer:DDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-332)Which of the following expenditures would be debited to an expense account?A)The cost to overhaul the company carʹs engineB)The cost to replace the transmission of the company careC)The cost to change the company carʹs oilD)All of the aboveAnswer:CDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-333)Which of the following are expenditures that are periodic and routine?A)Capital expendituresB)Ordinary repairsC)Extraordinary repairsD)Asset expendituresAnswer:BDiff: 1Page Ref: 509, 510Objective: 10-1EOC Ref: S10-334)Roberts Construction Company paid $40,000 for equipment with a market value of $45,000. Atwhich of the following amounts should the equipment be recorded?A)$40,000B)$42,500C)$45,000D)None of the aboveAnswer:ADiff: 1Page Ref: 508Objective: 10-1EOC Ref: S10-235)A company purchased a used machine for $80,000. The machine required installation costs of$8,000 and insurance while in transit of $500. At which of the following amounts would the equipment be recorded?A)$80,000B)$80,500C)$88,000D)$88,500Answer:DDiff: 1Page Ref: 508Objective: 10-1EOC Ref: S10-236)Which of the following items should be depreciated?A)LandB)Tangible property, plant, and equipment other than landC)Intangible propertyD)Natural resourcesAnswer:BDiff: 1Page Ref: 506-508Objective: 10-2EOC Ref: S10-437)Which of the following items should NOT be depreciated because it doesnʹt wear out?A)LandB)Tangible property, plant, and equipment other than landC)Intangible propertyD)Natural resourcesAnswer:ADiff: 1Page Ref: 507Objective: 10-2EOC Ref: S10-438)Which of the following accounting principles requires depreciation?A)Entity conceptB)Reliability conceptC)The revenue conceptD)The matching conceptAnswer:DDiff: 1Page Ref: 510Objective: 10-2EOC Ref: S10-439)Which of the following items is a factor to consider when computing depreciation expense?A)The cost of the assetB)The useful life of the assetC)The residual value of the assetD)All of the aboveAnswer:DDiff: 1Page Ref: 511Objective: 10-2EOC Ref: S10-440)Which of the following factors are estimates?A)The cost of the assetB)The useful life of the assetC)The residual value of the assetD)Both B and CAnswer:DDiff: 1Page Ref: 511Objective: 10-2EOC Ref: S10-441)Which of the following depreciation methods allocates an equal amount of depreciation toeach year?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the aboveAnswer:ADiff: 1Page Ref: 512Objective: 10-2EOC Ref: S10-442)Which of the following depreciation methods allocates a fixed amount of depreciation toeach±miles driven, copies made, or some other number of components?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the aboveAnswer:BDiff: 1Page Ref: 513Objective: 10-2EOC Ref: S10-443)Which of the following depreciation methods writes off more depreciation near the start of anassetʹs life than in later years?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the aboveAnswer:CDiff: 1Page Ref: 513, 514Objective: 10-2EOC Ref: S10-444)Which of the following properly describes accumulated depreciation?A)Accumulated depreciation is a contra-asset account.B)Accumulated depreciation is a contra-liability account.C)Accumulated depreciation is an expense account.D)Accumulated depreciation is a contra-equity account.Answer:ADiff: 1Page Ref: 512Objective: 10-2EOC Ref: S10-445)Which of the following is the purpose of accumulated depreciation?A)Accumulated depreciation is an expense.B)Accumulated depreciationʹs purpose is to provide details about the cost expiration ofplant assets.C)Accumulated depreciationʹs purpose is to provide details about the cost expiration ofnatural assets.D)Accumulated depreciationʹs purpose is to provide details about the cost expiration ofintangible assets.Answer:BDiff: 1Page Ref: 512Objective: 10-2EOC Ref: S10-446)Which of the following depreciation methods does NOT use a residual method in the firstyear?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the aboveAnswer:CDiff: 1Page Ref: 513, 514Objective: 10-2EOC Ref: S10-447)Which of the following depreciation methods is used by MOST companies for their financialstatements?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the above methods are used about equallyAnswer:ADiff: 1Page Ref: 516Objective: 10-2EOC Ref: S10-448)Which of the following is the expected cash value of an asset at the end of its useful life?A)Book valueB)Carrying valueC)Market valueD)Residual valueAnswer:DDiff: 1Page Ref: 511Objective: 10-2EOC Ref: S10-4Table 10.1On January 1, 2011, Zane Manufacturing Company purchased a machine for $40,000. The company expects to use the machine a total of 24,000 hours over the next 6 years. The estimated sales price of the machine at the end of 6 years is $4,000. The company used the machine 8,000 hours in 2011 and 12,000 in 2012.49)Refer to Table 10.1. What is depreciation expense for 2011 if the company usesdouble-declining balance depreciation?A)$6,000B)$6,667C)$12,000D)$13,333Answer:DDiff: 2Page Ref: 513, 514Objective: 10-2EOC Ref: S10-450)Refer to Table 10.1. What is depreciation expense for 2012 if the company usesdouble-declining balance depreciation?A)$6,000B)$8,889C)$10,000D)$13,333Answer:BDiff: 2Page Ref: 513, 514Objective: 10-2EOC Ref: S10-451)Refer to Table 10.1. What is the book value of the machine at the end of 2012 if the companyuses double-declining balance depreciation?A)$13,333B)$17,778C)$20,000D)$28,000Answer:BDiff: 2Page Ref: 513, 514Objective: 10-2EOC Ref: S10-452)Refer to Table 10.1. What is depreciation expense for 2011 if the company uses straight-linedepreciation?A)$6,000B)$6,667C)$12,000D)$13,333Answer:ADiff: 1Page Ref: 512, 513Objective: 10-2EOC Ref: S10-453)Refer to Table 10.1. What is depreciation expense for 2012 if the company uses straight-linedepreciation?A)$6,000B)$9,000C)$10,000D)$13,333Answer:ADiff: 2Page Ref: 512, 513Objective: 10-2EOC Ref: S10-454)Refer to Table 10.1. What is the book value of the machine at the end of 2012 if the companyuses straight-line depreciation?A)$10,000B)$17,778C)$20,000D)$28,000Answer:DDiff: 1Page Ref: 512, 513Objective: 10-2EOC Ref: S10-455)Refer to Table 10.1. What is depreciation expense for 2011 if the company usesunits-of-production depreciation?A)$6,000B)$6,667C)$12,000D)$13,333Answer:CDiff: 2Page Ref: 513Objective: 10-2EOC Ref: S10-456)Refer to Table 10.1. What is depreciation expense for 2012 if the company usesunits-of-production depreciation?A)$6,000B)$9,000C)$10,000D)$18,000Answer:DDiff: 2Page Ref: 513Objective: 10-2EOC Ref: S10-457)Refer to Table 10.1. What is the book value of the machine at the end of 2012 if the companyuses units-of-production depreciation?A)$10,000B)$17,778C)$20,000D)$28,000Answer:ADiff: 3Page Ref: 513Objective: 10-2EOC Ref: S10-458)Which of the following is TRUE when the estimate of an assetʹs useful life is increased?A)Prior yearsʹ financial statements must be restated.B)Annual depreciation expense is decreased for the remaining years of the assetʹs life.C)The new estimate is ignored until the last year of the assetʹs life.D)Annual depreciation expense is increased for the remaining years of the assetʹs life.Answer:BDiff: 3Page Ref: 520, 521Objective: 10-2EOC Ref: S10-859)Lexis Company purchased equipment on January 1, 2005 for $35,500. The estimated useful lifeof the equipment was 7 years and the estimated residual value was $4,000. After using the straight-line method of depreciation for 3 years, the estimated useful life was revised to 9 years on January 1, 2008. How much is depreciation expense for 2008.A)$2,000B)$2,444C)$3,000D)$3,667Answer:CDiff: 3Page Ref: 520, 521Objective: 10-2EOC Ref: S10-860)Which of the following depreciation methods is used by MOST companies for their taxreturns?A)Straight-lineB)Units-of-productionC)Declining-balanceD)All of the above methods are used about equallyAnswer:CDiff: 1Page Ref: 519Objective: 10-3EOC Ref: S10-661)A company purchased a computer on July 1, 2009. The computer has an estimated useful lifeof 5 years and will have no salvage value. It is estimated that the computer can be used for 5,000 hours. The computer was used for 450 hours during 2009. If the goal is to reduce taxable income to the lowest amount, which method should be elected and how much depreciation can be deducted in 2009?A)Straight-line, $1,000B)Double declining-balance, $2,000C)Units-of-production, $900D)None of the aboveAnswer:BDiff: 1Page Ref: 519Objective: 10-3EOC Ref: S10-662)A company purchased equipment for $100,000 in 2008. The machine will be used for 10,000hours and will have a residual value of $20,000. The equipment was used for 2,400 hours in 2008. How much depreciation will be deducted if the company elects the units-of-production method for tax return purposes?A)$10,000B)$19,200C)$20,000D)$24,000Answer:BDiff: 1Page Ref: 519Objective: 10-3EOC Ref: S10-663)When is a gain on disposal of an asset recorded?A)A gain is recorded when the assetʹs residual value is less than the cash received.B)A gain is recorded when the asset is sold for a price greater than the assetʹs book value.C)A gain is recorded when accumulated depreciation is less than the cash received.D)A gain is recorded when the asset is sold for a price less than the assetʹs book value.Answer:BDiff: 1Page Ref: 522, 523Objective: 10-4EOC Ref: S10-964)When is a loss on disposal of an asset recorded?A)A loss is recorded when the assetʹs residual value is less than the cash received.B)A loss is recorded when the asset is sold for a price greater than the assetʹs book value.C)A loss is recorded when accumulated depreciation is less than the cash received.D)A loss is recorded when the asset is sold for a price less than the assetʹs book value.Answer:DDiff: 1Page Ref: 522, 523Objective: 10-4EOC Ref: S10-9residual value was $2,000. How much depreciation is deducted in the fourth year of use if the straight line method of depreciation was used?A)NoneB)$667C)$1,000D)$2,000Answer:ADiff: 2Page Ref: 512, 513Objective: 10-4EOC Ref: S10-966)An asset was purchased for $12,000. The assetʹs estimated useful life was 3 years and itsresidual value was $2,000. How much gain or loss is reported if the asset is sold for $3,000 at the beginning of the fourth year?A)No gain or lossB)$1,000 lossC)$1,000 gainD)$2,000 lossAnswer:CDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-967)An asset was purchased for $12,000. The assetʹs estimated useful life was 3 years and itsresidual value was $2,000. How much gain or loss is reported if the asset is sold for $3,000 at the end of the fourth year?A)No gain or lossB)$1,000 lossC)$1,000 gainD)$2,000 lossAnswer:CDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-9residual value was $2,000. How much gain or loss is reported if the asset is sold for $1,000 at the beginning for the fourth year?A)No gain or lossB)$1,000 lossC)$1,000 gainD)$2,000 lossAnswer:BDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-969)An asset was purchased for $12,000. The assetʹs estimated useful life was 3 years and itsresidual value was $2,000. How much gain or loss is reported if the asset is sold for $5,333 at the beginning for the third year if the straight line method of depreciation was used?A)No gain or lossB)$1,000 lossC)$1,000 gainD)$2,000 lossAnswer:ADiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-970)Which of the following items is included in the journal entry if a company sells equipment at aprice equal to its book value?A)A debit to equipment for its book valueB)A credit to accumulated depreciationC)A debit to loss on sale of equipmentD)A credit to equipment for its original costAnswer:DDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-971)Which of the following items is included in the journal entry if a company sells equipment at aprice greater than its book value?A)A debit to equipment for its book valueB)A credit to gain on sale of equipmentC)A debit to loss on sale of equipmentD)A credit to accumulated depreciationAnswer:BDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-972)Which of the following items is included in the journal entry if a company sells equipment at aprice less than its book value?A)A debit to equipment for its book valueB)A credit to accumulated depreciationC)A debit to loss on sale of equipmentD)A credit to gain on sale of equipmentAnswer:CDiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-973)Kelly Petroleum Products owns furniture that was purchased for $19,600. Accumulateddepreciation is $17,300. The furniture was sold for $3,800. Which of the following is the correct entry to record the transaction?A)Accumulated depreciation 17,300Cash 3,800Gain on sale of furniture 1,500Furniture 19,600B)Accumulated depreciation 17,300Cash 3,800Furniture 31,100C)Furniture 19,600Cash 2,700Gain on sale of furniture 5,000Accumulated depreciation 17,300D)Furniture 19,600Gain on sale of furniture 3,800Cash 2,700Accumulated depreciation 17,300Answer:ADiff: 2Page Ref: 522, 523Objective: 10-4EOC Ref: S10-1074)Kelly Petroleum Products owns fully depreciated equipment that was purchased for $26,500.The equipment had an estimated useful life of 8 years and an estimated residual value of $2,500. The equipment was sold for $2,700. Which of the following is the correct entry to record the transaction?A)Accumulated depreciation 26,500Cash 2,700Equipment 23,800B)Accumulated depreciation 26,500Cash 2,700Gain on sale of equipment 2,700Equipment 26,500C)Accumulated depreciation 24,000Cash 2,700Gain on sale of equipment 200Equipment 26,500D)None of the aboveAnswer:CDiff: 3Page Ref: 522, 523Objective: 10-4EOC Ref: S10-1075)Lowery Food Market owns refrigeration equipment that cost $10,000 and has accumulateddepreciation of $8,500. The company exchanges the equipment for new equipment worth $12,000. In addition to the old equipment, the company pays $10,000 for the new equipment.Which of the following is the correct entry to record the transaction?A)Refrigeration equipment 11,500Accumulated depreciation 8,500Cash 10,000Refrigeration equipment 10,000B)Refrigeration equipment 11,000Accumulated depreciation 8,500Loss on exchange of equipment 500Cash 10,000Refrigeration equipment 10,000C)Refrigeration equipment 12,000Accumulated depreciation 8,500Gain on exchange of equipment 500Cash 10,000Refrigeration equipment 10,000D)None of the aboveAnswer:ADiff: 2Page Ref: 523, 524Objective: 10-4EOC Ref: S10-1076)Lowery Food Market owns refrigeration equipment that cost $10,000 and has accumulateddepreciation of $7,400. The company exchanges the equipment for new equipment worth $12,000. In addition to the old equipment, the company pays $10,000 for the new equipment.Which of the following is the correct entry to record the transaction?A)Refrigeration equipment 12,000Accumulated depreciation 7,400Cash 10,000Refrigeration equipment 9,400B)Refrigeration equipment 12,000Accumulated depreciation 7,400Loss on exchange of equipment 600Cash 10,000Refrigeration equipment 10,000C)Refrigeration equipment 10,000Accumulated depreciation 10,000Gain on exchange of equipment 600Cash 12,000Refrigeration equipment 7,400D)None of the aboveAnswer:BDiff: 3Page Ref: 523, 524Objective: 10-4EOC Ref: S10-1077)Which of the following items should be depleted?A)LandB)Tangible property, plant, and equipment other than landC)Intangible propertyD)Natural resourcesAnswer:DDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1178)Which of the following is the expense resulting from a decline in the utility of naturalresource?A)DepreciationB)DepletionC)AmortizationD)ObsolescenceAnswer:BDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1179)Which of the following accounting methods is the method used to compute depletion?A)Straight-lineB)Units-of-productionC)Declining-balanceD)None of the aboveAnswer:BDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-11Table 10.2Navajo Mining Company purchased a mine in 2011 for $3,400,000. It was estimated that the mine contained 200,000 tons of ore and that the mine would be worthless after all of the ore was extracted. The company extracted 25,000 tons of are in 2011 and 30,000 tons of ore in 2012.80)Refer to Table 10.2. What is depletion expense for 2011?A)$340,000B)$425,000C)$510,000D)$680,000Answer:BDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1181)Refer to Table 10.2. What is depletion expense for 2012?A)$340,000B)$425,000C)$510,000D)$680,000Answer:CDiff: 1Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1182)Refer to Table 10.2. What is the book value of the mine at the end of 2012?A)$2,465,000B)$2,720,000C)$2,975,000D)$3,060,000Answer:ADiff: 2Page Ref: 524, 525Objective: 10-5EOC Ref: S10-1183)Which of the following is the amount capitalized as goodwill?A)The excess of the cost of an acquired company over the sum of the book value of its netassetsB)The excess of the cost of an acquired company over the sum of the book value of itsassetsC)The excess of the cost of an acquired company over the sum of the market value of its netassetsD)The excess of the cost of an acquired company over the sum of the market value of itsassetsAnswer:CDiff: 2Page Ref: 526, 527Objective: 10-6EOC Ref: S10-1284)Which of the following items should be amortized?A)LandB)Tangible property, plant, and equipment other than landC)Intangible propertyD)Natural resourcesAnswer:CDiff: 1Page Ref: 525, 526Objective: 10-6EOC Ref: S10-1285)Which of the following is the expense resulting from a decline in the utility of an intangibleasset?A)DepreciationB)DepletionC)AmortizationD)ObsolescenceAnswer:CDiff: 1Page Ref: 525, 526Objective: 10-6EOC Ref: S10-1286)Which of the following accounting methods is the method used to compute amortization?A)Straight-lineB)Units-of-productionC)Declining-balanceD)None of the aboveAnswer:ADiff: 1Page Ref: 525, 526Objective: 10-6EOC Ref: S10-1287)Which of the following is the proper accounting treatment for research and developmentcosts?A)Research and development costs must be capitalized and amortized over 20 years or less.B)Research and development costs must be capitalized and amortized over 70 years or less.C)Research and development costs must be capitalized and expensed each year to theextent that their value has declined.D)Research and development costs must be expensed.Answer:DDiff: 2Page Ref: 527Objective: 10-6EOC Ref: S10-12。

会计专业英语模拟试题及答案

《会计专业英语》模拟试题及答案一、单选题(每题1分,共20分)1. Which of the following statements about accounting concepts or assumptions are correct? 1) The money measurement assumption is that items in accounts are initially measured at their historical cost.2) In order to achieve comparability it may sometimes be necessary to override the prudence concept。

3)To facilitate comparisons between different entities it is helpful if accounting policies and changes in them are disclosed.4) To comply with the law, the legal form of a transaction must always be reflected in financial statements.A 1 and 3B 1 and 4C 3 onlyD 2 and 3Johnny had receivables of $5 500 at the start of 2010。

During the year to 31 Dec 2010 he makes credit sales of $55 000 and receives cash of $46 500 from credit customers。

What is the balance on the accounts receivables at 31 Dec 2010?$8 500 Dr$8 500 Cr$14 000 Dr$14 000 CrShould dividends paid appear on the face of a company’s cash flow statement?YesNoNot sureEitherWhich of the following inventory valuation methods is likely to lead to the highest figure for closing inventory at a time when prices are dropping?Weighted Average costFirst in first out (FIFO)Last in first out (LIFO)Unit cost5. Which of following items may appear as non—current assets in a company’s the statement of financial position?(1) plant,equipment, and property(2) company car(3) €4000 cash(4) €1000 chequeA. (1),(3)B。

Plant Assets, Natural Resources, and Intangibles

• Leasehold Improvement: Cost of improvements to leased assets • Depreciate (amortize) over term of the lease.

Exercise 7-1

Allocate Costs

Lump-Sum (or Basket) Purchase of Assets

What is the cost of the land?

Determining the Cost of Land

Purchase price of land Add related costs: Back property taxes Transfer taxes Removal of buildings Survey fees Total cost of land $300,000 $10,000 8,000 5,000 1,000

– – – – – $10,000 in back property tax $8,000 in transfer taxes $5,000 for removal of an old building $1,000 survey fee $260,000 to pave the parking lot.

• • • •

Purchase price Brokerage commissions Sales and other taxes Repairing or renovating building for its intended purpose

Determining the Cost of Machinery and Equipment

The Asset Rules

富达基金

The Best Overall Fund Management Firm (Asia Pacific ex-Japan) 2006, 2007, 2008 and 2009, Asia Pacific Survey 2006, 2007, 2008 and 2009 conducted by Thomson Extel Surveys. 2006、 2007、 2008及2009 Thomson Extel (亞太區)調查— 2006、 2007、 2008 及2009整體最傑出基金管理公司大獎—亞太區(日本除外)。 Fidelity, Fidelity International, and Fidelity International and Pyramid Logo are trademarks of FIL Limited. 「富達」及其標誌均為 FIL Limited的商標。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Land and Land Improvements

Land improvements: fences driveways and parking lots paving sprinkler systems lighting Subject to Depreciation. Practice:S10-1,p534.

Divide a Lump-sum Purchase

A $120,000 lump-sum purchase price for land, building, & equipment with estimated market values of $40,000, $95,000, & $15,000, respectively What’s the value of land, building, & equipment? Total market value = $40,000 + 95,000 + 15,000 = $150,000 Percentage of total value:

chapter10-plant asset-ym

11

Lump-sum (or Basket) Purchase (整批购买)

several assets purchases as a group relative-sales-value method (相对销 售价值法): the total cost (100%) is divided among the assets according to their relative sales values

Plant assets (fixed assets) : - long-lived - tangible in nature - used in the operation of the business Plant assets & related expense, Exhibit 10-1,p506.

chapter10-plant asset-ym 2

Categories of Assets

Tangible or Intangible assets

Tangible assets (plant assets) : generally useful for more than one year Intangible assets: no physical form

chapter10-plant asset-ym

6

Land and Land Improvements

Land cost: purchase price brokerage commission survey and legal fees back property taxes the cost of clearing the land the cost of removing unwanted buildings. Land is not depreciated.

13

Capital expenditures

Does the expenditure increase capacity or efficiency or extend useful life?

YES NO

Capital Expenditure Debit asset account

subject to depreciation

chapter10-plant asset-ym 9

Machinery and equipment

cost includes:

purchase price less discounts transportation charges insurance while in transit sales and other taxes purchase commissions installation costs cost to testing before the asset is used

LOGO

CHAPTER 10 Plant Assets and Intangible Assets

Charles T. Horngren

chapter10-plant asset-ym

1

Learning Objectives

1. Measure the cost of a plant asset 2. Account for depreciation 3. Select the best depreciation method for tax purposes 4. Account for the disposal of a plant asset 5. Account for natural resources 6. Account for intangible assets

chapter10-plant asset-ym 14

Expense Debit repairs and maintenance expense

Extraordinary Repair

A capital expenditure Increases capacity or efficiency or useful life

chapter10-plant asset-ym

18

Depreciation

not a process of valuation of the plant asset which is based on historical cost, not on current appraisal value. does not represent a fund of cash set aside to replace worn or obsolete assets. Accumulated Depreciation, a contraasset account, equals the portion of the asset’s cost that has already been depreciated (or expensed). The causes of depreciation include

chapter10-plant asset-ym

15

Ordinary Repair

does not extend an asset’s capacity merely maintains the asset or restores it to good working order, Examples are: - the cost of new tires for the truck, or - the cost of replacing a dead battery on the truck. Debited to an expense account, such as Repair and Maintenance Expense. Exhibit 10-3, p510. Practice: E10-16, p536.

chapter10-plant asset-ym 17

Depreciation

process of allocating a plant asset’s cost to expense over the asset’s useful life in a rational & systematic way based on the matching principle matches the cost of an asset with the revenue generated by the use of that asset.

used to allocate that cost among the various assets acquired. The allocation is based on the assets’ appraised or market values.

chapter10-plant asset-ym 12

subject to depreciation

chapter10-plant asset-ym

10

Furniture and fixtures

desks, chairs, file cabinet, display racks cost

purchase price (less any discount) shipping charges cost of assemble

chapter10-plant asset-ym 5

Types of Tangible Assets & Related Costs

A. Land & land improvement B. Buildings C. Machinery & Equipment D. Furniture & Fixture

40,000/150,000=26.7%x$120,000=$32,040 95,000/150,000=63.3% x 120,000 = 75,960 15,000/150,000= 10% x 120,000 = 12,000 $120,000

chapter10-plant asset-ym

Practice: S10-2, p534.

chapter10-plant asset-ym 16

Important!

record capital expenditures & ordinary repair and maintenance expenses correctly, as an error in recording causes errors on both the income statement and the balance sheet. Treating a capital expenditure as an expense: - overstates expenses - understates net income Capitalizing an expense: - understates expenses - overstates net income