米什金货币银行学topic 6 banking industry

广外货币银行学期末重点全英 米什金

考试题型以及分数分布:一、选择题:1’*20=20’二、名词解释:4’*5=20’三、简答题:8’*5=40’四、论述题:20’*1=20’重点制作思路:1.考虑到时间关系,抓大放小2.结合老师提及复习内容进行预测3.以理顺书本架构为主,看到一个知识点猜一下可能会出什么题The economics of money,banking and financial markets----by Kyle Chapter1:Why Study Money, Banking, and Financial Markets?(本章了解一下这个问题即可,最多考一下选择)Answer:•To examine how financial markets such as bond and stock markets work •To examine how financial institutions such as banks work•To examine the role of money in the economyChapter2:An Overview of the Financial System1. Function of Financial Markets•Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage of funds •Direct finance: borrowers borrow funds directly from lenders in financial markets by selling them securities.•Promotes economic efficiency by producing an efficient allocation(分配)of capital(资金), which increases production•Directly improve the well-being of consumers by allowing them to time purchases better2.Structure of Financial Markets•Debt and Equity (普通股) Markets•Primary and Secondary Markets•Exchanges and Over-the-Counter (OTC不通过交易所而直接售给顾客的) Markets •Money and Capital Markets(货币和资本市场)3. Financial Market Instruments(要能举出例子,很可能考选择)Money markets deal in short-term debt instrumentsCapital markets deal in longer-term debt and equity instruments.4.Internationalization of Financial Markets(重点,选择、名词解释都有可能)•Foreign Bonds & Eurobond?•Eurocurrencies & Eurodollars?•World Stock Markets5.Function of Financial Intermediaries: Indirect Finance(记一下金融中介机构的功能,交易成本很可能考名词解释)•Lower transaction costs (time and money spent in carrying out financial transactions).•Reduce the exposure of investors to risk•Deal with asymmetric 不对称 information problems•Conclusion:Financial intermediaries allow “small” savers and borrowers to benefit from the existence of financial markets.6. Types of Financial Intermediaries(会分类即可)Depository institutionsContractual saving institutionsInvestment intermediaries7. Regulation of the Financial System•To increase the information available to investors:•To ensure the soundness 健康稳固of financial intermediariesChapter3:What Is Money?1. Meaning of Money(即definition,必考名词解释!!)•Money (or the “money supply”): anything that is generally accepted in payment for goods or services or in the repayment of debts.2. Functions of Money(重点)•Medium of Exchange:• A medium of exchange must•Unit of Account:•Store 储藏 of Value:3. Evolution of the Payments System•Commodity 商品 Money•Fiat 法定 Money•Checks 支票Electronic Payment (e.g. online bill pay).•E-Money (electronic money):4. Measuring Money (重中之重,M1/M2都很有可能考名词解释)•Construct monetary aggregates using the concept of liquidity: (构建货币总量使用流动性的概念)•M1 (most liquid assets)= currency + traveler’s checks + demand deposits + other checkable deposits.•M2 (adds to M1 other assets that are not so liquid)= M1 + small denomination time deposits + savings deposits and money market deposit accounts + money market mutual fund shares.Chapter 4:Understanding Interest Rates1.measuring interest rates:Present Value(很可能考察名词解释)A dollar paid to you one year from now is less valuable than a dollar paidto you todaySimple Present Value:PV=CF/(1+i)n次方2.Four Types of Credit Market Instruments•Simple Loan•Fixed Payment Loan•Coupon Bond 附票债券•Discount Bond 贴现债券3.Yield to Maturity(重点,很可能名词解释)•The interest rate that equates the present value of cash flow payments received from a debt instrument with its value today计算4种不同信用工具外加Consol or Perpetuity(金边债券或永久债券)的YM4. Yield on a Discount Basis(了解即可)Current Yield当期收益率Yield on a Discount Basis 折价收益率Rate of Return 收益率5.Rate of Return and Interest Rates(收益率与利息率的distinction)•The return equals the yield to maturity only if the holding period equals the time to maturity• A rise in interest rates is associated with a fall in bond prices, resulting in a capital loss if time to maturity is longer than the holding period •The more distant a bond’s maturity, the gr eater the size of the percentage price change associated with an interest-rate change•The more distant a bond’s maturity, the lower the rate of return the occurs as a result of an increase in the interest rate•Even if a bond has a substantial initial interest rate, its return can be negative if interest rates rise6. Interest-Rate Risk•Prices and returns for long-term bonds are more volatile than those for shorter-term bonds•There is no interest-rate risk for any bond whose time to maturity matches the holding period7. Real and Nominal Interest Rates(重点,很可能考察简答题)•Nominal interest rate makes no allowance for inflation•Real interest rate is adjusted for changes in price level so it more accurately reflects the cost of borrowing•Ex ante real interest rate is adjusted for expected changes in the price level•Ex post real interest rate is adjusted for actual changes in the price level8. Fisher Equation(重点考察)Chapter5:The Behavior of Interest Rates1. Determining the Quantity Demanded of an Asset•Wealth: the total resources owned by the individual, including all assets •Expected Return: the return expected over the next period on one asset relative to alternative assets•Risk: the degree of uncertainty associated with the return on one asset relative to alternative assets•Liquidity: the ease and speed with which an asset can be turned into cash relative to alternative assets(流动性很有可能考名词解释)2.Theory of Asset Demand(必考,死活都得背下来)Holding all other factors constant:1.The quantity demanded of an asset is positively related to wealth2.The quantity demanded of an asset is positively related to its expectedreturn relative to alternative assets3.The quantity demanded of an asset is negatively related to the riskof its returns relative to alternative assets4.The quantity demanded of an asset is positively related to itsliquidity relative to alternative assets3. Supply and Demand for Bonds(见到看一下图)Market Equilibrium4. Shifts in the Demand for Bonds•Wealth: in an expansion with growing wealth, the demand curve for bonds shifts to the right•Expected Returns: higher expected interest rates in the future lower the expected return for long-term bonds, shifting the demand curve to the left •Expected Inflation: an increase in the expected rate of inflations lowers the expected return for bonds, causing the demand curve to shift to the left •Risk: an increase in the riskiness of bonds causes the demand curve to shift to the left•Liquidity: increased liquidity of bonds results in the demand curve shifting right5.Shifts in the Supply of Bonds•Expected profitability of investment opportunities: in an expansion, the supply curve shifts to the right•Expected inflation: an increase in expected inflation shifts the supply curve for bonds to the right•Government budget: increased budget deficits shift the supply curve to the right6. The Liquidity Preference Framework(重中之重)7.Demand for Money in the Liquidity Preference Framework•As the interest rate increases:–The opportunity cost of holding money increases…–The relative expected return of money decreases…•…and therefore the quantity demanded of money decreases.8.Shifts in the Demand for Money(都很重要)•Income Effect: a higher level of income causes the demand for money at each interest rate to increase and the demand curve to shift to the right •Price-Level Effect: a rise in the price level causes the demand for money at each interest rate to increase and the demand curve to shift to the right•Liquidity preference framework leads to the conclusion that an increase in the money supply will lower interest rates: the liquidity effect.•Income effect finds interest rates rising because increasing the money supply is an expansionary influence on the economy (the demand curve shifts to the right).Chapter9:Banking1.The Bank Balance Sheet•Liabilities–Checkable deposits–Nontransaction deposits–Borrowings–Bank capital•Assets–Reserves(准备金)–Cash items in process of collection–Deposits at other banks–Securities–Loans–Other assets2.Basic Banking:•Cash Deposit:Opening of a checking account leads to an increase in the bank’s reserves equal to the increase in checkable depositsCheck Deposit3.Inter-business•Bank settlement•Finance lease•Fiduciary business•Safe deposit box4. Off-Balance-Sheet Activities•Loan sales (secondary loan participation)•Generation of fee income. Examples:Chapter12:Central Banks and the Federal Reserve System(此章省略很多)1.Structure of theFed(了解即可)Board of Governors(7人)12 FRBs(9人)FOMC (7+1+4人)Federal Advisory Council (12人)2.Federal Reserve Bank(3+3+3人)Functions:Clear checksIssue new currencyWithdraw damaged currency from circulationAdminister and make discount loans to banks in their districtsEvaluate proposed mergers and applications for banks to expand their activities Act as liaisons between the business community and the Federal Reserve System Examine bank holding companies and state-chartered member banksCollect data on local business conditionsUse staffs of professional economists to research topics related to the conduct of monetary policyChapter13&14:The Money Supply Process:1.Players in the Money Supply Process Central bank (Federal Reserve System)Banks (depository institutions; financial intermediaries)Depositors (individuals and institutions)2.Fed’s Balance Sheet3.Monetary Base4.Open Market Purchase•The effect of an open market purchase on reserves depends on whether the seller of the bonds keeps the proceeds from the sale in currency or in deposits •The effect of an open market purchase on the monetary base always increases the monetary base by the amount of the purchaseOpen Market Sale•Reduces the monetary base by the amount of the sale•Reserves remain unchangedThe effect of open market operations on the monetary base is much more certain than the effect on reserves5.Fed’s Ability to Control the MonetaryBaseSplit the monetary base into two components :MBn= MB - BRthe non-borrowed monetary base :MBnborrowed reserves:BR6.The Formula for Multiple Deposit Creation(很重要!必考,记住公式)7. Factors that Determine the Money SupplyChanges in the nonborrowed monetary base MBnChanges in borrowed reserves from the FedChanges in the required reserves ratioChanges in currency holdingsChanges in excess reserves8. The Money Multiplier(重点)Assume that the desired holdings of currency C and excess reserves ER grow proportionally with checkable deposits D. Then,c = {C/D} = currency ratioe = {ER/D} = excess reserves ratioThe monetary base MB equals currency (C) plus reserves (R):MB = C + R = C + (r x D) + ERM=m*MB=m*(MBn+BR)M=1+c/r+e+cChapter 15:Tools of Monetary Policy1. Tools of Monetary PolicyOpen market operationsChanges in borrowed reservesChanges in reserve requirementsFederal funds rate: the interest rate on overnight loans of reserves from one bank to another2.Demand in the Market for ReservesSupply in the Market for Reserves3.Affecting the Federal Funds Rate4.Open Market Operations(超级重点)Advantages:The Fed has complete control over the volumeFlexible and preciseEasily reversedQuickly implemented5.Discount Policy(超级重点)Advantages:Used to perform role of lender of last resortdisadvantages:Cannot be controlled by the Fed; the decision maker is the bank 6.Reserve Requirements(超级重点)Advantages:•No longer binding for most banksdisadvantages:•Can cause liquidity problems•Increases uncertainty for banks7. Monetary Policy Tools of the European Central Bank•Open market operations•Lending to banks•Reserve RequirementsChapter16:The Conduct of Monetary Policy: Strategy and Tactics 1. Goals of Monetary Policy(1)The Price Stability Goal•Low and stable inflation•Inflation•Nominal anchor to contain inflation expectations•Time-inconsistency problem(2)Other Goals of Monetary Policy•High employment•Economic growth•Stability of financial markets•Interest-rate stability•Foreign exchange market stability2. Monetary Targeting•Advantages–Almost immediate signals help fix inflation expectations and produce less inflation–Almost immediate accountability•Disadvantages–Must be a strong and reliable relationship between the goal variable and the targeted monetary aggregat e3. Inflation Targeting•Public announcement of medium-term numerical target for inflation •Institutional commitment to price stability as the primary, long-run goal of monetary policy and a commitment to achieve the inflation goal •Information-inclusive approach in which many variables are used in making decisions•Advantages•Does not rely on one variable to achieve target•Easily understood•Reduces potential of falling in time-inconsistency trap•Stresses transparency and accountability•Disadvantages•Delayed signaling•Too much rigidity•Potential for increased output fluctuations•Low economic growth during disinflation4.Monetary Policy with an Implicit Nominal AnchorThere is no explicit nominal anchor in the form of an overriding concern for the Fed.Forward looking behavior and periodic “preemptive strikes”The goal is to prevent inflation from getting started.•Advantages–Uses many sources of information–Avoids time-inconsistency problem•Disadvantages–Lack of transparency and accountability–Strong dependence on the preferences, skills, and trustworthiness of individuals in charge–Inconsistent with democratic principles5. Tactics: Choosing the Policy Instrument•Tools–Open market operation–Reserve requirements–Discount rate•Policy instrument (operating instrument)–Reserve aggregates–Interest rates–May be linked to an intermediate target•Interest-rate and aggregate targets are incompatible (must chose one or the other).6.Linkages Between Central Bank Tools, Policy Instruments, Intermediate Targets, and Goals of Monetary Policy(中间目标是超级重点,死活都要背下来)Chapter19:The Demand for Money1.Velocity of Money and The Equation ofExchangeV=P*Y/MM*V=P*Y2.Quantity Theory of Money DemandSO: Demand for money is determined by:The level of transactions generated by the level of nominal income PYThe institutions in the economy that affect the way people conduct transactions and thus determine velocity and hence k3.Keynes’s Liquidity Prefe rence TheoryTransactions motivePrecautionary motiveSpeculative motiveVelocity is not constant:4.Friedman’s Modern Quantity Theory of Money(记住该公式及其含义)5. Differences between Keynes’s and Friedman’s Model (cont’d)•Friedman–Includes alternative assets to money–Viewed money and goods as substitutes–The expected return on money is not constant; however, r b –r m does stayconstant as interest rates rise–Interest rates have little effect on the demand for money •Friedman (cont’d)–The demand for money is stable ?–velocity is predictable–Money is the primary determinant of aggregate spendingChapter23:Transmission Mechanisms of Monetary Policy: The Evidence1.Framework(1)Structural Modelwhether one variable affects another•Transmission mechanism–The change in the money supply affects interest rates–Interest rates affect investment spending–Investment spending is a component of aggregate spending (output) Advantages and Disadvantages(2)Reduced-Form•Analyzes the effect of changes in money supply on aggregate output (spending) to see if there is a high correlationAdvantages and Disadvantages2.Transmission Mechanisms of Monetary Policy(1) Asset Price EffectsTraditional interest rate effectsExchange rate effects on net exports...(2)Credit ViewChapter24:Money and Inflation1.meaning of inflation(死活背下来)extremely high for a sustained period of time, its rate of money supply growth is also extremely high•Money Growth–High money growth produces high inflation•Fiscal Policy–Persistent high inflation cannot be driven by fiscal policy alone •Supply Shocks–Supply-side phenomena cannot be the source of persistent high inflation•Conclusion: always a monetary phenomenon2. Origins of Inflationary Monetary Policy•Cost-push inflation–Cannot occur without monetary authorities pursuing an accommodating policy•Demand-pull inflation•Budget deficits–Can be the source only if the deficit is persistent and is financed by creating money rather than by issuing bonds•Two underlying reasons–Adherence of policymakers to a high employment target–Presence of persistent government budget deficits3. The Discretionary (Activist)/ Nondiscretionary (Nonactivist) Policy Debate(1)Advocates of discretionary policy:regard the self-correcting mechanism as slowPolicy lags slow activist policy(2)Advocates of nondiscretionary policy:believe government should not get involvedDiscretionary policy produces volatility in both the price level and output。

货币金融学第10版米什金英文答案

货币金融学第10版米什金英文答案Chapter 1ANSWERS TO QUESTIONS1.The interest rate on three-month Treasury bills fluctuates more than the other interest rates and is loweron average. The interest rate on Baa corporate bonds is higher on average than the other interest rates.2.The lower price for a firm’s shares means that it can raise a smaller amount of funds, so investment infacilities and equipment will fall.3.H igher stock prices mean that consumers’ wealth is higher, and they will be more likely to increasetheir spending.4.They channel funds from people who do not have a productive use for them to people who do,thereby resulting in higher economic efficiency.5.The United States economy was hit by the worst financial crisis since the Great Depression. Defaultsin subprime residential mortgages led to major losses in financial institutions, producing not only numerous bank failures, but also the demise of two of the largest investment banks in the United States.These factors led to the “Great Recession” which began late in 2007.6.The basic activity of banks is to accept deposits and make loans.7.Savings and loan associations, mutual savings banks, credit unions, insurance companies, mutualfunds, pension funds, and finance companies.8.Answers will vary.9.In the period from 2007 to 2011, both inflation and interest rates have generally trended downwardcompared to before that period.10.The data in Figures 3, 5, and 6 suggest that real output, the inflation rate, and interest rates wouldall fall.11.Businesses would increase investment spending because the cost of financing this spending is nowlower, and consumers would be more likely to purchase a house or a car because the cost of financing their purchase is lower.12.No. It is true that people who borrow to purchase a house or a car are worse off because it costs themmore to finance their purchase; however, savers benefit because they can earn higher interest rates on their savings.13.Because the Federal Reserve affects interest rates, inflation, and business cycles, all of which have animportant impact on the profitability of financial institutions.14.The deficit as a percentage of GDP has expanded dramatically since 2007; in 2010 the deficit to GDPratio was 10%, well above the historical average of around 2% since 1950.15.It makes foreign goods more expensive, so British consumers will buy fewer foreign goods and moredomestic goods.62 Mishkin •The Economics of Money, Banking, and Financial Markets, Tenth Edition16.It makes British goods more expensive relative to American goods. Thus American businesses willfind it easier to sell their goods in the United States and abroad, and the demand for their products will rise.17.Changes in foreign exchange rates change the value of assets held by financial institutions and thuslead to gains and losses on these assets. Also changes in foreign exchange rates affect the profits made by traders in foreign exchange who work for financial institutions.18.In the mid- to late 1970s and in the late 1980s and early 1990s, the value of the dollar was low, makingtravel abroad relatively more expensive; thus it was a good time to vacation in the United States and see the Grand Canyon. With the rise in the do llar’s value in the early 1980s, travel abroad became relatively cheaper, making it a good time to visit the Tower of London. This was also true, to a lesser extent, in the early 2000s.19.When the dollar increases in value, foreign goods become less expensive relative to American goods;thus you are more likely to buy French-made jeans than American-made jeans. The resulting drop in demand for American-made jeans because of the strong dollar hurts American jeans manufacturers.On the other hand, the American company that imports jeans into the United States now finds that the demand for its product has risen, so it is better off when the dollar is strong.20.As the dollar becomes stronger (worth more) relative to a foreign currency, one dollar is equivalent to(can be exchanged for) more foreign currency. Thus, for a given face value of bond holdings, a stronger dollar will yield more home currency to foreigners, so the asset will be worth more to foreign investors.Likewise, a weak dollar will lead to foreign bond holdings worth less to foreigners.ANSWERS TO APPLIED PROBLEMS21.The best day is 4/25. At a rate of $1.6674/pound, you would have £119.95. The wo rst day is 4/7.At $1.961/pound, you would have £101.99, or a difference of £17.96.Part Three: Answers to End-of-Chapter Problems 63 Chapter 2ANSWERS TO QUESTIONS1. Yes, I should take out the loan, because I will be better off as a result of doing so. My interest paymentwill be $4,500 (90% of $5,000), but as a result, I will earn an additional $10,000, so I will be ahead of the game by $5,500. Since Larry’s loan-sharking business can make some people better off, as in this example, loan sharking may have social benefits. (One argument against legalizing loan sharking, however, is that it is frequently a violent activity.)2. Yes, because the absence of financial markets means that funds cannot be channeled to people whohave the most productive use for them. Entrepreneurs then cannot acquire funds to set up businesses that would help the economy grow rapidly.3. The share of Microsoft stock is an asset for its owner, because it entitles the owner to a share of theearnings and assets of Microsoft. The share is a liability for Microsoft, because it is a claim on its earnings and assets by the owner of the share.4. You would rather hold bonds, because bondholders are paid off before equity holders, who are theresidual claimants.5. This statement is false. Prices in secondary markets determine the prices that firms issuing securitiesreceive in primary markets. In addition, secondary markets make securities more liquid and thus easier to sell in the primary markets. Therefore, secondary markets are, if anything, more important than primary markets.6. Treasury bills are short-term debt instruments issued by the United States government to coverimmediate spending obligations, i.e. finance deficit spending. Certificates of deposit (CDs) areissued by banks and sold to depositors. Commercial paper is issued by corporations and large banks as a method of short-term funding in debt markets. Repos are issued primarily by banks, and funded by corporations and other banks through loans in which treasury bills serve as collateral, with an explicit agreement to pay off the debt (repurchase the treasuries) in the near future. Fed funds are overnight loans from one bank to another.7. Mortgages are loans to households or firms to purchase housing, land, or other real structures, wherethe structure or land itself serves as collateral for the loans. Mortgage-backed securities are bond-like debt instruments which are backed by a bundle of individual mortgages, whose interest and principal payments are collectively paid to the holders of the security. In other words, when an individual takes out a mortgage, that loan is bundled with other individual mortgages to create a composite debtinstrument, which is then sold to investors.8. The British gained because they were able to earn higher interest rates as a result of lending toAmericans, while the Americans gained because they now had access to capital to start up profitable businesses such as railroads.9. The international trade of mortgage-backed securities is generally beneficial in that the Europeanbanks that held the mortgages could earn a return on those holdings, while providing needed capital to U.S. financial markets to support borrowing for new home construction and other productive uses.In this sense, both European banks and U.S. borrowers should have benefitted. However, with the sharp decline in the U.S. housing market, default rates on mortgages rose sharply, and the value of64 Mishkin •The Economics of Money, Banking, and Financial Markets, Tenth Editionthe mortgage-backed securities held by European banks fell sharply. Even though the financialcrisis began primarily in the United States as a housing downturn, it significantly affected European markets; Europe would have been much less affected without such internationalization of financial markets.10. Financial intermediaries benefit by carrying risk at relatively low transaction costs. Since higherrisk assets on average earn a higher return, financial intermediaries can earn a profit on a diversified portfolio of risky assets. Individual investors benefit by earning returns on a pooled collection of assets issued by financial intermediaries at lower risk. Risk to individual investors is lowered through the pooling of assets by the financial intermediary.11. Because you know your family member better than a stranger, you know more about the borrower’shonesty, propensity for risk taking, and other traits. There is less asymmetric information than witha stranger and less likelihood of an adverse selection problem, with the result that you are more likelyto lend to the family member.12. The issuance of subprime mortgages represents lenders loaning money to the pool of potentialhomeowners who are the highest credit risk and have the lowest net wealth and other financialresources. In other words, this group of borrowers most in need of mortgage credit was also thehighest risk to lenders, a perfect example of adverse selection.13. Loan sharks can threaten their borrowers with bodily harm if borrowers take actions that mightjeopardize their paying off the loan. Hence borrowers from a loan shark are less likely to increase moral hazard.14. They might not work hard enough while you are not looking or may steal or commit fraud.15. Yes, because even if you know that a borrower is taking actions that might jeopardize paying off theloan, you must still stop the borrower from doing so. Because that may be costly, you may not spend the time and effort to reduce moral hazard, and so the problem of moral hazard still exists.16. True. If there are no informational or transactions costs, people could make loans to each other atno cost and would thus have no need for financial intermediaries.17. Because the costs of making the loan to your neighbor are high (legal fees, fees for a credit check,and so on), you will probably not be able earn 5% on the loan after your expenses even though it hasa 10% interest rate. You are better off depositing your savings with a financial intermediary and earning5% interest. In addition, you are likely to bear less risk by depositing your savings at the bank rather than lending them to your neighbor.18. Potentially competing interests may lead an individual or firm to conceal information or disseminatemisleading information. A substantial reduction in the quality of information in financial markets increases asymmetric information problems and prevents financial markets from channeling funds into the most productive investment opportunities. Consequently, the financial markets and the economy become less efficient. That is, false information as a result of a conflict of interest can lead to a more inefficient allocation of capital than just asymmetric information alone.19. Financial firms that provide multiple types of financial services can be more efficient througheconomies of scope, that is, by lowering the cost of information production. However, this can be problematic since it can also lead to conflicts of interest, in which the financial firm provides false orPart Three: Answers to End-of-Chapter Problems 65 misleading information to protect its own interests. This can lead to a worsening of the asymmetric information problem, making financial markets less efficient.20. You would likely use a credit union if you are a member, since their primary business is consumerloans. In some cases it is possible to borrow directly from pension funds, but it can come with high borrowing costs and tax implications. Investment banks do not provide loans to the general public. 21. Most life insurance companies hold large amounts of corporate bonds and mortgage assets, thus poorcorporate profits or a downturn in the housing market can significantly adversely impact the value of asset holdings of insurance companies.22. During the financial panic, regulators were concerned that depositors worried their banks would fail,and that depositors (especially with accounts over $100,000) would pull money from banks, leaving cash-starved banks with even less cash to satisfy customer demands and day-to-day operations. This could create a contagious bank panic in which otherwise healthy banks would fail. Raising the insurance limit would reassure depositors that their money was safe in banks and prevent a bank panic, helping to stabilize the financial system.ANSWERS TO APPLIED PROBLEMS23. a. With Option 1, since deposits are insured it can be assumed a riskless investment. Thus, theexpected total payoff would be $10,000 ⨯ 1.02 = $10,200. With Option 2, a bond return of5% implies a potential payoff of $10,000 ⨯ 1.05 = $10,500, and there is a 90% chance thatthis outcome will occur, thus the expected payoff is $10,500 ⨯ 0.9 = $9450. Under Option 3,the expected payoff is $10,000 ⨯ 1.08 ⨯ 0.93 = $10,044. Option 4 is riskless, so the expectedtotal payoff is $10,000. Given these choices and the assumption that you don’t care about risk,Option 1 is the best investment.b. This option implies the very real possibility of either receiving nothing (if he actually leaves town),or $10,800 (if he indeed pays as promised). If you don’t pay Mike, you have an expected returnof $10,044 as shown above. If you paid your friend the $100 and learned that Mike would leavewithout paying, then obviously you wouldn’t loan Mike the money, and you would be left with$9900. However, if you paid the friend $100 and learned that Mike would pay, you would have$10,700 (= $10,000 ⨯ 1.08 - $100). After paying your friend Mike, but before knowing the trueoutcome, your expected return would be $10,644 ($9900 ⨯ 0.07 + $10,700 ⨯ 0.93). Paying yourfriend the $100 is definitely worth it because it increases your expected return and in additiondramatically reduces the downside risk that you make a bad loan, and increases the certainty ofthe payoff amount. That is, with asymmetric information (not paying your roommate), you havea range of payoffs of $0 to $10,800 versus $9900 to $10,700 without asymmetric information.Thus, paying a small amount to improve risk assessment can be very beneficial, a task for which financial intermediaries are well suited.66 Mishkin •The Economics of Money, Banking, and Financial Markets, Tenth EditionChapter 3ANSWERS TO QUESTIONS1. Since a lot of other assets have liquidity properties that are similar to currency but can be used asmoney to purchase goods and services, not counting them would understate an economy’s access to liquidity for transactions purposes. For this reason, counting assets such as checking deposits or savings accounts more accurately reflects the stock of assets that can be considered money.2. Even if he or she is a non-smoker, since the prisoner knows that others in the prison will acceptcigarettes as a form of payment, they themselves would be willing to accept cigarettes as a form of payment. So, rather than prisoners having to barter and trade favors, cigarettes satisfy the double coincidence of wants in that both parties to a trade stand ready to use them to “purchase” goods or services.3. Because the orchard owner likes only bananas but the banana grower doesn’t like apples, thebanana grower will not want apples in exchange for his bananas, and they will not trade. Similarly, the chocolatier will not be willing to trade with the banana grower because she does not like bananas.The orchard owner will not trade with the chocolatier becau se he doesn’t like chocolate. Hence, in a barter economy, trade among these three people may well not take place, because in no case is therea double coincidence of wants. However, if money is introduced into the economy, the orchard ownercan sell his apples to the chocolatier and then use the money to buy bananas from the banana grower.Similarly, the banana grower can use the money he receives from the orchard owner to buy chocolate from the chocolatier, and the chocolatier can use the money to buy apples from the orchard owner.The result is that the need for a double coincidence of wants is eliminated, and everyone is better off because all three producers are now able to eat what they like best.4. Cavemen did not need money. In their primitive economy, they did not specialize in producing onetype of good and they had little need to trade with other cavemen.5. (a) This situation illustrates the medium-of-exchange function of money. We often do not think whywe accept money in exchange for hours spent working, as we are so accustomed to using money.The medium-of-exchange function of money refers to its ability to facilitate trades (hours worked for money and then money for groceries) in a society. (b) In this case we observe money performing its unit-of-account function. If modern societies did not use money as a unit of account, then the price of apples would have to be quoted in terms of all the other items in the market. This quickly becomes an impossible task. Suppose that a pound of apples sells for 0.80 pounds of oranges, half a gallon of milk, one third of a pound of meat, 2 razor blades, 1.5 pound of potatoes, etc., etc., etc! (c) Maria is contemplating the store-of-value function of money. As a medium of exchange and unit of account, measures of money known as M1 or M2 have no important rivals. With respect to the store-of-value function, however, there are many assets that can preserve value better than a checking account.Maria’s choice to preserve the purchasing power of her income by in creasing her savings account balance is fine for a small period of time. For a period of 20 years, however, you might choose to buy a U.S. Treasury bond that matures in 20 years (as many grandparents have done as a way to pay for their grandchildren’s ed ucations).6. Because of the rapid inflation in Brazil, the domestic currency, the real, was a poor store of value.Thus many people preferred to hold dollars, which were a better store of value, and used them in their daily shopping.Part Three: Answers to End-of-Chapter Problems 67 7. Because money was losing value at a slower rate (the inflation rate was lower) in the 1950s than inthe 1970s, it was a better store of value then, and you would have been willing to hold more of it.8. Money loses its value at an extremely rapid rate in hyperinflation, so you want to hold it for as shorta time as possible. Thus money is like a hot potato that is quickly passed from one person to another.9. Because a check was so much easier to transport than gold, people would frequently rather be paid bycheck even if there was a possibility that the check might bounce. In other words, the lower transactions costs involved in handling checks made people more willing to accept them.10. Wine is more difficult to transport than gold and is also more perishable. Gold is thus a better storeof value than wine and also leads to lower transactions cost. It is therefore a better candidate for use as money.11. Neither. Although PayPal and many other e-money systems work as other forms of money doto facilitate purchases of goods and services, it does not count in the M1 or M2 money supplies.Because PayPal and similar payment systems are generally credit-based, this requires payment ata future date for funds used today; those future payments must be made using existing money thatis already in the system, such as currency or funds in a bank deposit account. In other words, the M1 and M2 money supplies would theoretically remain the same, but money would move fromyour checking account to a third party, once the credit transaction is settled.12. The ranking from most liquid to least liquid is: (c), (a), (e), (f ), (d), and (b).13. M1 contains the most liquid assets. M2 is the largest measure.14. The degree of liquidity of an asset is measured by considering how much time and effort (i.e.,transaction costs) are needed to convert that asset into currency. Currency is by definition the most liquid type of money. Different types of money have different degrees of liquidity. A check, which represents a balance on a checking account, is a quite liquid type of money. After all, all that is needed to pay for a good or service using a check is the two minutes it takes to include the date and amount and sign the check. However, the above example shows that some merchants refuse to accept checks as a means of payment. (They cannot refuse to accept dollars, as dollars are legal tender in the United States.) This can result in significant transaction costs in trying to find a bank or an ATM. It is even possible that the transaction never takes place. This example illustrates the point that even inside the same monetary aggregate, different types of money do not have the same degree of liquidity.15. a. M1 and M2,b. M2,c. M2,d. M1 and M2.16. Your actions will reduce your checking account balance and increase your holdings of money marketmutual fund shares. Considering this transaction only, M1 will decrease as one of its components decreased. M2 will remain constant, as M2 is composed of all items that add up to M1 plus some other types of money that are not so liquid to be considered part of M1. One of these categories is money market mutual fund shares. The decrease in your checking account balance is offset by the increase in money market mutual fund shares, and therefore M2 remains constant.68 Mishkin •The Economics of Money, Banking, and Financial Markets, Tenth Edition17. During the period in question, the M1 growth rate increased by 17 percentage points, while the M2growth rate increased by only 3 percentage points. Although both measures are moving in the same direction, the magnitude of the difference in growth rates between the two makes it difficult tojudge the appropriateness of monetary policy by just looking at the money supply measures alone.For instance, if one focused just on the M2 money supply, knowing the economy was in severeeconomic contraction would suggest that the growth rate of M2 perhaps should be even higher than the 3 percentage point increase over this time. On the other hand, if one just focused on the M1 growth increase of 17 percentage points, this may seem alarmingly high and suggest an inflationary problem in the future.18. Not necessarily. Although the total amount of debt has predicted inflation and the business cyclebetter than M1 or M2, it may not be a better predictor in the future. Without some theoretical reason for believing that the total amount of debt will continue to predict well in the future, we may not want to define money as the total amount of debt.ANSWERS TO APPLIED PROBLEMS19. The M1 money supply is the sum of rows A, E, and G for each year. The M2 money supply is thesum of all components A–G for each year. Note that 3-month treasury bills are not considered part of the M1 or M2 money supply, even though they are fairly liquid assets. The table below shows the M1 and M2 money supplies, along with the growth rates from the previous year. Note that while the M1 money supply is relatively flat (and slightly negative for 2010), the M2 money supply grows ata much higher, positive rate. This is because the components of M2 are rising much more rapidlycompared to the components of M1 (which are also included in M2). In particular, small denomination time deposits increase 30% from 2010 to 2011, and 39% from 2011 to 2012, driving much of the growth in M2. Moreover, the narrower components which make up just the M1 money supply represent less than 20% (1904/10128) of the broader M2 indicators. Thus movements in the money market, savings account, and time deposit measures will have a much bigger impact on M2 growth than the narrower M1 components will.2009 2010 2011 2012A. Currency 900 920 925 931B. Money market mutual fund shares 680 681 679 688C. Savings account deposits 5500 5780 5968 6105D. Money market deposit accounts 1214 1245 1274 1329E. Demand and checkable deposits 1000 972 980 993F. Small denomination time deposits 830 861 1123 1566G. Traveler’s checks 4 4 3 2H. 3-month treasury bills 1986 2374 2436 2502Total M1 money stock 1904 1896 1908 1926Total M2 money stock 10128 10463 10952 11614M1 growth rate 0.4 0.6 0.9M2 growth rate 3.3 4.7 6.0Part Three: Answers to End-of-Chapter Problems 69 Chapter 4ANSWERS TO QUESTIONS1. It would be worth 1/(1 + 0.20) = $0.83 when the interest rate is 20%, rather than 1/(1 + 0.10) = $0.91when the interest rate is 10%. Thus, a dollar tomorrow is worth less with a higher interest rate today.2. $2,000 = $100/(1 +i) + $100/(1 +i)2+ . . . + $100/(1 +i)20+ $1,000/(1 + i)20. Solving for i gives theyield to maturity.3. If the interest rate were 12%, the present discounted value of the payments on the government loanare necessarily less than the $1,000 loan amount because they do not start for two years. Thus the yield to maturity must be lower than 12% in order for the present discounted value of these payments to add up to $1,000.4. When the yield to maturity increases, this represents a decrease in the price of the bond. If thebondholder were to sell the bond at a lower price, the capital gains would be smaller (capital losses larger) and therefore the bondholder would be worse off.5. No. If interest rates rise sharply in the future, long-term bonds may suffer such a sharp fall in pricethat their return might be quite low, possibly even negative.6. People are more likely to buy houses because the real interest rate when purchasing a house hasfallen from 3% (= 5% - 2%) to 1% (= 10% - 9%). The real cost of financing the house is thus lower, even though nominal mortgage rates have risen. (If the tax deductibility of interest payments isallowed for, then it becomes even more likely that people will buy houses.)7. The current yield will be a good approximation to the yield to maturity whenever the bond price isvery close to par or when the maturity of the bond is over about ten years. This is because cash flows farther in the future have such small present discounted values that the value of a long-term coupon bond is close to a perpetuity with the same coupon rate.8. The near-term costs to maintaining a given size loan are much smaller for a perpetuity than for a similarfixed payment loan, discount, or coupon bond. For instance, assuming a 5% interest rate over 10 years, on a $1000 loan, a perpetuity costs $50 a year (or $500 in payments over 10 years). For a fixedpayment loan, this would be $129.50 per year (or $1295 in payments over the same 10-year period).For a discount loan, this loan would require a lump sum payment of $1628.89 in 10 years. For acoupon bond, assuming the same $50 coupon payment as the perpetuity implies a $1000 face value.Thus, for the coupon bond, the total payments at the end of 10 years will be $1500.9. Whenever the current price P is greater than face value F of a discount bond, the yield to maturity willbe negative. It is possible for a coupon bond to have a negative nominal interest rate, as long as the coupon payment and face value are low relative to the current price. As an example, with a one-year coupon bond, the yield to maturity is given as i= (C+F-P)/P; in this case whenever C+F<P,i will be negative. It is impossible for a perpetuity to have a negative nominal interest rate, since thiswould require either the coupon payment or the price to be negative.10. True. The return on a bond is the current yield i C plus the rate of capital gain, g. A discount bond, bydefinition, has no coupon payments, thus the current yield is always zero (the coupon payment of zero divided by current price) for a discount bond.。

货币银行学PPT 米什金 [兼容模式]

![货币银行学PPT 米什金 [兼容模式]](https://img.taocdn.com/s3/m/ad5e772f4b35eefdc8d3339f.png)

Chapter 13 Banking Industry: Structure andCompetitionHistorical Development of theBanking System•Bank of North America chartered in 1782•Controversy over the chartering of banks.•National Bank Act of 1863 creates a new banking system of federally chartered banksg y y–Office of the Comptroller of the Currency–Dual banking system•Federal Reserve System is created in 1913.Figure 1 Time Line of the Early History of Commercial Banking in the United StatesPrimary Supervisory Responsibility ofBank Regulatory Agencies•Federal Reserve and state banking authorities: state banks that are members of the Federal Reserve System.the Federal Reserve System•Fed also regulates bank holding companies.•FDIC: insured state banks that are not Fed members.•State banking authorities: state banks without FDIC insurance.without FDIC insuranceFinancial Innovation and the Growthof the Shadow Banking Systemof the “Shadow Banking System”•Financial innovation is driven by the desire to earn profits•A change in the financial environment will stimulate a search by financial institutions for innovations that are likely to be profitable–Financial engineeringResponses to Changes in DemandConditions: Interest Rate Volatility •Adjustable rate mortgagesAdjustable-rate mortgages–Flexible interest rates keep profits high whenrates rise–Lower initial interest rates make them attractiveyto home buyers•Financial Derivatives–Ability to hedge interest rate risk–Payoffs are linked to previously issued (i.e.derived from) securities.Responses to Changes in SupplyConditions: Information Technology •Bank credit and debit cards–Improved computer technology lowerstransaction costs•Electronic banking–ATM, home banking, ABM and virtual bankingATM home banking ABM and virtual banking •Junk bonds•Commercial paper marketResponses to Changes in SupplyConditions: Information Technologygy (cont’d)•SecuritizationS iti ti–To transform otherwise illiquid financial assetsinto marketable capital market securities.i t k t bl it l k t iti–Securitization played an especially prominent role in the development of the subprime mortgagemarket in the mid 2000s.Avoidance of Existing Regulations: Loophole Mining•Reserve requirements act as a taxR i t t ton deposits•Restrictions on interest paid on deposits ledto disintermediation•Money market mutual funds•Sweep accountsFinancial Innovation and theDecline of Traditional Banking •As a source of funds for borrowers, market share has fallen•Commercial banks’ share of total financial intermediary assets has fallen•No decline in overall profitabilityIncrease in income from off-balance-sheet •Increase in income from off balance sheet activitiesFigure 2 Bank Share of TotalNonfinancial Borrowing, 19602011Nonfinancial Borrowing 1960–2011Source: Federal Reserve Flow of Funds; /releases/z1/Current/z1.pdf. Flow of Funds Accounts; Federal Reserve Bulletin.Financial Innovation and the Decline of Traditional Banking (cont d)of Traditional Banking (cont’d)g q g•Decline in cost advantages in acquiring funds (liabilities)–Rising inflation led to rise in interest rates anddisintermediation–Low-cost source of funds, checkable deposits, declined inimportance•Decline in income advantages on uses of funds (assets)–Information technology has decreased need for banks toI f ti t h l h d d d f b k tfinance short-term credit needs or to issue loans–Information technology has lowered transaction costs forother financial institutions, increasing competitionother financial institutions increasing competitionBanks’ Responses•Expand into new and riskier areas of lending –Commercial real estate loans–Corporate takeovers and leveraged buyoutsC t t k d l d b t •Pursue off-balance-sheet activities–Non-interest income–Concerns about riskStructure of the U.S. Commercial Banking Industry•Restrictions on branchingR t i ti b hig g–McFadden Act and state branching regulations.•Response to ranching restrictions–Bank holding companies.–Automated teller machines.Table 1 Size Distribution of Insured Commercial Banks, March 30, 2011Table 2 Ten Largest U.S. Banks, December 30, 2010December 30 2010Bank Consolidation andNationwide Banking•The number of banks has declined over the last 25 yearsBank failures and consolidation.–Bank failures and consolidation–Deregulation: Riegle-Neal Interstate Bankingand Branching Efficiency Act f 1994and Branching Efficiency Act f 1994.–Economies of scale and scope fromo at o tec o ogyinformation technology.•Results may be not only a smaller number of banks but a shift in assets to much larger banks.Benefits and Costs of BankConsolidation•Benefits–Increased competition, driving inefficient banks outof business–Increased efficiency also from economies of scale andscope–Lower probability of bank failure from more diversifiedportfolios•Costs–Elimination of community banks may lead to less lending to small business–Banks expanding into new areas may take increased risksi kB k di i k i dand failFigure 3 Number of Insured Commercial Banks in the United States, 1934–2010 (Third Quarter)(Thi d Q t)Source: /qbp/qbpSelect.asp?menuitem=STAT.Separation of the Banking and OtherFinancial Service Industriesg•Erosion of Glass-Steagall Act–Prohibited commercial banks from underwritingcorporate securities or engaging in brokerageactivities–Section 20 loophole was allowed by the FederalR bli ffili t f dReserve enabling affiliates of approvedcommercial banks to underwrite securities aslong as the revenue did not exceed a specifiedamountp–U.S. Supreme Court validated the Fed’s actionin 1988Separation of the Banking and Other Financial Service Industries (cont’d)Financial Service Industries (cont d)G amm Leach Blile Financial Se ices •Gramm-Leach-Bliley Financial Services Modernization Act of 1999Ab li h Gl St ll–Abolishes Glass-Steagall –States regulate insurance activities –SEC keeps oversight of securities activities –Office of the Comptroller of the Currency regulates bank subsidiaries engaged in securities underwriting F d lR b k h ldi–Federal Reserve oversees bank holding companiesSeparation of Banking and Other Financial Services Industries Throughout the World•Universal banking–No separation between banking and securitiesindustries•British-style universal banking–May engage in security underwriting•Separate legal subsidiaries are common•Bank equity holdings of commercial firms are lesscommon•Few combinations of banking and insurance firmsSeparation of Banking and Other Financial Services Industries Throughout the World (cont’d)•Some legal separation–Allowed to hold substantial equity stakes in commercialfirms but holding companies are illegalStructure•Savings and Loan Associations–Chartered by the federal government or by states–Most are members of Federal Home Loan Bank os a e e be s o ede a o e oa aSystem (FHLBS)–Deposit insurance provided by Savings AssociationInsurance Fund (SAIF) part of FDICInsurance Fund (SAIF), part of FDIC–Regulated by the Office of Thrift Supervision •Mutual Savings Banks–Approximately half are chartered by states–Regulated by state in which they are located–Deposit insurance provided by FDIC or state insuranceStructure (cont’d)•Credit Unions–Tax-exempt–Chartered by federal government or by states–Regulated by the National Credit Union Administration(NCUA)–Deposit insurance provided by National Credit Union Share Insurance Fund (NCUSIF)International Banking g•Rapid growth–Growth in international trade and multinational corporationsp–Global investment banking is very profitabley p–Ability to tap into the Eurodollar marketEurodollar MarketDollar denominated deposits held in banks •Dollar-denominated deposits held in banks outside of the U.S.•Most widely used currency in international M t id l d i i t ti l trade•Offshore deposits not subject to regulations •Important source of funds for U.S. banksI t t f f d f U S b kStructure of U.S. BankingOverseas•Shell operationSh ll ti•Edge Act corporation•International banking facilities (IBFs) ot subject to egu at o a d ta es –Not subject to regulation and taxes–May not make loans to domestic residentsForeign Banks in the U.S.•Agency office of the foreign bank–Can lend and transfer fund in the U.S.–Cannot accept deposits from domestic residents –Not subject to regulations•Subsidiary U.S. bankS b idi U S b k–Subject to U.S. regulations–Owned by a foreign bankForeign Banks in the U.S. (cont’d)•Branch of a foreign bank–May open branches only in state designated as home state or in state that allow entry of out-of-state banks–Limited-service may be allowed in any other statej g•Subject to the International Banking Act of 1978•Basel Accord (1988)–Example of international coordination of bank regulation p g –Sets minimum capital requirements for banksTable 3 Ten Largest Banks in the World, 2011World 20119)Before 1863,A) banks acquired funds by issuing bank notes.B) banks were chartered by state banking commissions.C) federally chartered banks had regulatoryC) federally-chartered banks had regulatory advantages not granted to state-chartered banks. )D) all of the above.E) only (a) and (b) of the above.15)Which bank regulatory agency has thesole regulatory authority over bank holding companies?A)The FDICB) The Comptroller of the CurrencyB) Th C t ll f th CC) The FHLBSD) The Federal Reserve System18)The Federal Reserve Act required all _____ banksThe Federal Reserve Act required all banks to become members of the Federal ReserveSystem, while _____ banks could choose tobecome members of the system.A)state; nationalB) state; municipalC) national; stateD) national; municipal27)The large number of banks in the United States is an indication of)g p g yA) vigorous competition within the banking industry.B) lack of competition within the banking industry.C) only efficient banks operating within the United States.)D) none of the above.)28)The McFadden Act of 1927A) effectively prohibited banks from branching across state lines.B) required that banks maintain bank capital equal to at least 6 percent of their assets.C) effectively required that banks maintain a correspondent relationship with large money center banks.D) did all of the above.37)Which of the following is not a reason for the rapid expansion of international banking.bankingA) The rapid growth in international trade.B) The desire for U.S. banks to expand.B) Th d i f U S b k t dC) The growth of multinational corporations.D) None of the above.47)Although it has a population about half that of the United States, Japan hasA) many more banks.A) many more banksB) only 10 percent of the number of banks.C) only 5 percent of the number of banks. )y pD) only 1 percent of the number of banks.61)The process in which people take theirmoney out of financial institutions seeking higher interest rates is calledA)capital mobility.B) loophole mining.B) l h l i iC) disintermediation.D) deposit jumping.65)The most important developments that have reduced banks' cost advantages in the p y ypast twenty years include:A) the growth of the junk bond market.B) the competition from money market mutual funds.C) the growth of securitization.D) all of the above.66)The most important developments that have reduced banks' income advantages in p y ythe past twenty years include:A) the growth of the commercial paper market.B) the growth of the junk bond market.C) the growth of securitization.D) all of the above.E) only (a) and (b) of the above.E) only (a) and (b) of the above78)The process of transforming otherwise illiquid financial assets into marketablepcapital market instruments is know asA) securitization.B) internationalization.C) arbitrage.D) program tradingD) program trading.E) none of the above.。

米什金 货币金融学 课件

• 所谓股票市场,是各种公司收益的权证 (股票)进行交易的场所,它在经济活 动中起着非常重要的作用。

• 股票市场作为最活跃的金融市场,其状 况往往是经济形势变化的晴雨表。股票 价格的上下波动是变幻莫测的,这种变 动对经济活动会产生很大影响 。

四.金融市场的重要性及其与货 币银行的联系

的统称,各种不同重要性

• 3.货币和其他经济现象 • (1)货币与经济周期。 • (2)货币与货币政策。 • (3)货币与预算赤字。

总结

• 总之,货币、银行与金融市场是非常重要的, 它们不仅与人们的日常生活密切相关,影响人 们的财富规模、投资和消费行为,而且会影响 企业的市场价值、生产和销售行为,同时也会 影响一个国家的财富总量、政局稳定和政策效 应。通过学习货币银行学的有关知识,我们可 以更透彻地理解各种经济现象,从而更好地安 排一生的投资、消费,最大限度地增进个人的 经济福利。

七.与货币银行学有关的几个事 实

• 1.大部分金融公式——无论它们有多么 复杂——都以复利为基础

• ⒉长期贷款的利率通常高于短期贷款的 利率

• ⒊ 为了理解利率如何影响经济决策,你 必须考虑预期通货膨胀

• ⒋购买股票是使你的财富增加的最好方 式——同时也是最坏方式

七.与货币银行学有关的几个事 实

五.银行和金融机构及其重要性

• 4.银行体系与金融创新 • (1)许多金融法规已经不能适应金融创新的发展,

管制当局对金融体系监管的难度加大了。 • (2)金融创新伴生的过度投机行为,不仅严

重损害了广大投资人的公共利益,而且妨碍了 金融体系的健康发展。 • (3)金融创新使国际金融市场的一体化程度 大大提高了。 • (4)金融创新对各国在金融体系监管的国际 协调提出了更高的要求。

货币银行学(米什金原书第4版)知识点串讲

货币银行学(米什金原书第4版) 串讲第一部分重要知识点梳理第二章重要知识点1.逆向选择(adverse selection)答:逆向选择是指在买卖双方信息非对称的情况下,差的商品总是将好的商品驱逐出市场;或者说拥有信息优势的一方,在交易中总是趋向于做出尽可能地有利于自己而不利于别人的选择。

逆向选择主要是交易前的信息不对称造成的。

逆向选择的存在使得市场价格不能真实地反映市场供求关系,导致市场资源配置的低效率。

一般在商品市场上卖者关于产品的质量。

保险市场上投保人关于自身的情况等等都有可能产生逆向选择问题。

解决逆向选择问题的方法主要有:政府对市场进行必要的干预和利用市场信号。

3.货币市场(money market)答:货币市场通常是指以短期金融工具为媒介,融资期限在一年以内(包括一年)的资金交易市场,又称短期资金市场。

货币市场主要是由短期信贷市场、短期证券市场、贴现市场等构成。

货币市场的主要特征表现为:期限短、流动性强、风险小等。

货币市场的主要交易对象有:银行存款、短期证券和商业票据等。

3.道德风险(moral hazard)答:道德风险是指在双方信息非对称的情况下,人们享有自己行为的收益,而将成本转嫁给别人,从而造成他人损失的可能性。

道德风险是信息不对称问题在交易后的影响产生的。

道德风险的存在不仅使得处于信息劣势的一方受到损失,而且会破坏原有的市场均衡,导致资源配置的低效率。

道德风险分析的应用领域主要是保险市场。

解决道德风险的主要方法是风险分担。

4.信息不对称(asymmetric information)答:信息不对称是指市场上的某些参与者拥有,但另一些参与者不拥有的信息;或指一方掌握的信息多一些,另一方所掌握的信息少一些。

信息不对称会导致资源配置不当,减弱市场效率,并且还会产生道德风险和逆向选择。

在很多情况下,市场机制并不能解决信息不对称问题,只能通过其他的一些机制来解决,特别是运用博奕论的相关知识来解决机制设计问题。

米什金版《货币金融学学》笔记(文内可搜索)

货币银行学笔记2.0【米什金笔记】序:货币银行学笔记1.0指的是本座在12年后编写的【胡庆康笔记】,由于缺少了货币理论的三个章节,所以该笔记是一部残篇。

为了能够更好的解释货币银行学,故引用米什金第九版货币金融学作为蓝本进行笔记升级。

笔记主体将由米什金组成,由黄达胡庆康等作品为辅助。

这本笔记的编撰主要是服务于本座的学习实践,所以有的本座认为不必赘述的就略过,不必证明的就直接给结论。

在阅读顺序上,建议读者先阅读笔者的《胡庆康笔记》,后阅读笔者的《米什金笔记》。

章节编写上,由【大纲】/导图,【内容】/主干知识,【补充】/边角知识,【关键术语】,【习题】,【胡说】/编者说(红字) 组成。

其中【胡说】均标红色,仅代表编者看法。

在写作上,笔记多表格少文字,多截图少写字。

表格看的更舒服,截图表示有根据。

【画外音:本座懒】本笔记撰写者:西班牙溃疡/西班牙流感/履虎尾。

天下学问,惟夜航船中最难对付。

2016年7月2日星期六福州 五四路第零章:大纲 我们将针对以下章节展开描述:第1篇 引言第1章 为什么研究货币、银行与金融市场第2章 金融体系概览第3章 什么是货币?第2篇 金融市场第4章 理解利率第5章 利率行为第6章 利率的风险结构与期限结构第7章 股票市场、理性预期理论与有效市场假定 第3篇 金融机构【略】第8章 金融结构的经济学分析第9章 金融危机与次贷风波第10章 银行业与金融机构的管理第11章 金融监管的经济学分析第12章 银行业:结构与竞争第4篇 中央银行与货币政策运作第13章 中央银行的结构与联邦储备体系【略】第14章 多倍存款创造和货币供给过程第15章 货币政策工具第16章 货币政策的操作:战略与战术第5篇 国际金融与货币政策第17章 外汇市场第18章 国际金融体系第19章 货币需求第20章 is-lm模型第21章 is—lm模型中的货币政策与财政政策第22章 总需求与总供给分析第23章 货币政策传导机制的实证分析第24章 货币与通货膨胀第25章 理性预期:政策意义第一章:为什么研究货币、银行与金融市场【胡说】要回答这个问题,首先要回答四个what和一个how1、为什么研究金融市场?2、为什么研究银行和其他金融机构?3、为什么研究货币和货币政策?4、为什么研究国际金融?5、我们如何研究货币、银行与金融市场?简单的说,为什么要研究市场,为什么要研究机构,为什么要研究政策,为什么要研究国际环境。

米什金货币银行学第6章-利率的期限结构

Term Structure Facts to be Explained

1. Interest rates for different maturities move together over time 2. Yield curves tend to have steep upward slope when short rates are low and downward slope when short rates are high 3. Yield curve is typically upward sloping Three Theories of Term Structure 1. Expectations Theory(理性预期的利率结构理论) (理性预期的利率结构理论) 2. Segmented Markets Theory 3. Liquidity Premium (Preferred Habitat) Theory

Chapter 6

The Rterest Rates

Risk Structure of Long-Term Bonds in the United States

© 2006 Pearson Addison-Wesley. All rights reserved

© 2006 Pearson Addison-Wesley. All rights reserved 6-6

Tax Advantages of Municipal Bonds

由于州具有相对独立的法律体系, 由于州具有相对独立的法律体系,导致了市政债券具有税收优势 .这里并没有考虑到市政债券的违约风险. ©这里并没有考虑到市政债券的违约风险. 2006 Pearson Addison-Wesley. All rights reserved 6-7

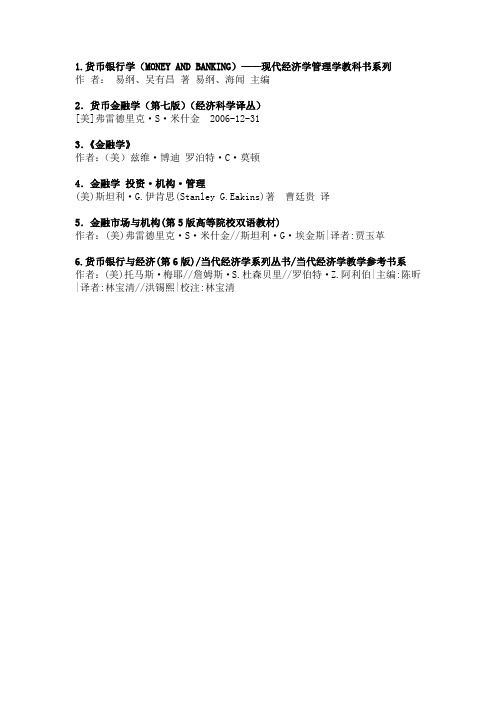

重点推荐货币银行学教材参考书

1.货币银行学(MONEY AND BANKING)——现代经济学管理学教科书系列作者:易纲、吴有昌著易纲、海闻主编2.货币金融学(第七版)(经济科学译丛)[美]弗雷德里克·S·米什金 2006-12-313.《金融学》作者:(美)兹维·博迪罗泊特·C·莫顿4.金融学投资·机构·管理(美)斯坦利·G.伊肯思(Stanley G.Eakins)著曹廷贵译5.金融市场与机构(第5版高等院校双语教材)作者:(美)弗雷德里克·S·米什金//斯坦利·G·埃金斯|译者:贾玉革6.货币银行与经济(第6版)/当代经济学系列丛书/当代经济学教学参考书系作者:(美)托马斯·梅耶//詹姆斯·S.杜森贝里//罗伯特·Z.阿利伯|主编:陈昕|译者:林宝清//洪锡熙|校注:林宝清书籍内容简介1.货币银行学(MONEY AND BANKING)——现代经济学管理学教科书系列作者:易纲、吴有昌著易纲、海闻主编出版社:上海人民出版社ISBN: 7208032750出版时间: 1999-9第1版书籍介绍:本书试图将现代货币银行理论与中国的具体实践有机地融合起来,从而形成一个既反映现代货币银行理论的优秀成果,又具有中国特色的货币银行学体系。

针对国内同类教科书大多只编重制度性和操作性方面内容的特点,我们试图在理论性内容方面有所加强。

本书结合课程内容设计了28个专栏,这些专栏有助于增强学生对所学内容的感性认识,培养学生关注现实问题的兴趣。

由于篇幅所限,同时也考虑到绝大多数高校的经济类院系都开设了专门的国际金融课程。

本书是“现代经济学管理学教科书系列”之一。

该教科书系列的主编易纲先生在编著本书时,力求了联系世界经济和中国经济的实际,在充分体现理论深度的同时注重教材的实用性。

本书共分6篇;基本概念;金融机构与金融市场;货币供求及利率决定;货币与经济;金融与经济发展;货币政策。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Cash items

–

Copyright @ 2009 School of Finance, SUFE

Deposits at Other Banks: (less important today than it was years ago) Securities:

– –

–

–

US government and US government agency securities State and local government (municipal) securities. By law, banks can only hold debt instruments; they cannot own equities short-term US government securities are sometimes considered as ’ ―secondary reserves.‖

Other Assets:

–

Copyright @ 2009 School of Finance, SUFE

T-account

A T-account is set up in the same format as a balance sheet, with assets on one side and liabilities on the other. But the T-account is simplified since it only shows the changes on each side that occur as a result of specific bank operations.

Copyright @ 2009 School of Finance, SUFE

outline

I.

the balance sheet of banks II. Basic Operation of a Bank: T-accounts III. Principles of Bank Management IV. Off-Balance-Sheet Activities V. Evolution of the Banking Industry VI. Basic Banking Frameworks in the World VII. Thrift Industry VIII. International Banking

Copyright @ 2009 School of Finance, SUFE

A

– – –

bank’s balance sheet lists:

Source of funds, or liabilities. Uses of funds, or assets. Bank Capital in defined as: Capital = Assets – Liabilities

Topic 6

Banking Industry

School of Finance, Shanghai University of

Finance and Economics

Copyright Copyright @ 2009 @School 2009 School of Finance, of Finance, SUFE SUFE

Copyright @ 2009 School of Finance, SUFE

2. Assets (Uses of Funds)

Reserves (pay no interest)

– – – –

The bank’s deposits at the Federal Reserve. Vault cash = currency that is physically held by the bank Required reserves: required reserve ratio. Excess reserves: additional reserves held by the bank to meet its customers’ requests for withdrawals A check that had been deposited at the bank, but not yet collected from the check writer’s bank, is a cash item in the process of collection.

Checkable +$100 Reserve +$100 deposits s

Opening of a checking account leads to an increase in the bank’s reserves equal to the increase in checkable deposits

which implies that capital serves as a measure of net worth

Copyright @ 2009 School of Finance, SUFE

Assets = Liabilities + Capital

–

–

it also implies that if we put assets on one side of the bank’s balance sheet, and liabilities plus capital on the other, then the two sides of the balance sheet will always balance banks make profits by charging an interest rate on their assets that exceeds the interest rate that they pay on their liabilities.

Reference

Chapter 9 : Banking and the Management of Financial Institutions

Chapter 10 : Banking Industry: Structure and Competition

Copyright @ 2009 School of Finance, SUFE

Copyright @ 2009 School of Finance, SUFE

Table 1 shows the combined balance sheet of all commercial banks as of January 2006, with all items listed as a percentage of total assets or liabilities.

Copyright @ 2009 School of Finance, SUFE

II.Basic Banking—Cash Deposit

First National Bank Assets Vault Cash +$100 Liabilities First National Bank Assets Liabilities Checkabl e deposits +$100

–

bank capital is a cushion against a drop in the value of the bank’s assets, since the bank becomes insolvent (bankrupt) if the value of its assets falls below the value of its liabilities

Copyright @ 2009 School of Finance, SUFE

I. the balance sheet of banks

Copyright @ 2009 School of Finance, SUFE

1. liabilities(Sources of Funds)

Checkable deposits

Copyright @ 2009 School of Finance, SUFE

In addition, Chapter 9 helps us identify and understand four basic principles of bank management:

– –

–

–

liquidity management asset management liability management capital adequacy management

–Demand

deposits (no interest) –NOW accounts –MMDAs (not included in M1 and so not subject to reserve requirements)

payable on demand, lowest-cost source of funds costly to maintain: process the check, maintain bank branches, etc.

Copyright @ 2009 School of Finance, SUFE

Loans:

–

–

– –

Commercial and industrial loans Real estate loans (mortgages) Consumer loans Interbank loans Physical assets owned by banks: buildings and land, computers and office equipment, etc.