微观经济学原理曼昆英文第四章讲解学习

微观经济学-第四章(曼昆)

What Is Competition?

• 垄断 只有一个卖者,卖者控制价格

• 寡头

• 很少卖者 • 不存在激烈的竞争

• 垄断竞争

• 很多卖方 • 微小的产品差别Slightly differentiated products • 每个卖方可以制定自己产品的价格

案例分析:减少香烟需求量的方法

每包香烟 的价格

© 2007 Thomson South-Western

• 需求表

• 表示一种物品的价格与需求量之间关系的表格 。

• Demand Schedule

• The demand schedule is a table that shows the relationship between the price of the good and the quantity demanded.

© 2007 Thomson South-Western

什么是市场?

• 供给和需求是指人们在市场上进行交易 时的行为

• 买方决定需求 • 卖方决定供给

© 2007 Thomson South-Western

什么是竞争? • 竞争市场是指有许多买者与卖者,以至于每

个人对市场价格的影响都微乎其微的市场。 • A competitive market is a market in which there

© 2007 Thomson South-Western

需求曲线的移动

• 收入

• 随着收入的增加,正常物品的需求增加。 As income increases the demand for a normal good will increase. • 随着收入的增加,低档物品的需求减少。 As income increases the demand for an inferior good will decrease.

曼昆微观经济学原理 第四章 PPT

THE MARKET FORCES OF SUPPLY AND DEMAND

14

Demand Curve Shifters: Expectations

Expectations affect consumers’ buying decisions. Examples: If people expect their incomes to rise, their demand for meals at expensive restaurants may increase now. If the economy sours and people worry about their future job security, demand for new autos may fall now.

THE MARKET FORCES OF SUPPLY AND DEMAND

13

Demand Curve Shifters: Tastes

Anything that causes a shift in tastes toward a good will increase demand for that good and shift its D curve to the right. Example: The diet became popular in the ’90s, caused an increase in demand for diet Coke, shifted the diet Coke demand curve to the right.

Q

THE MARKET FORCES OF SUPPLY AND DEMAND

Demand Curve Shifters: Income

曼昆_经济学原理答案_英文版chp4

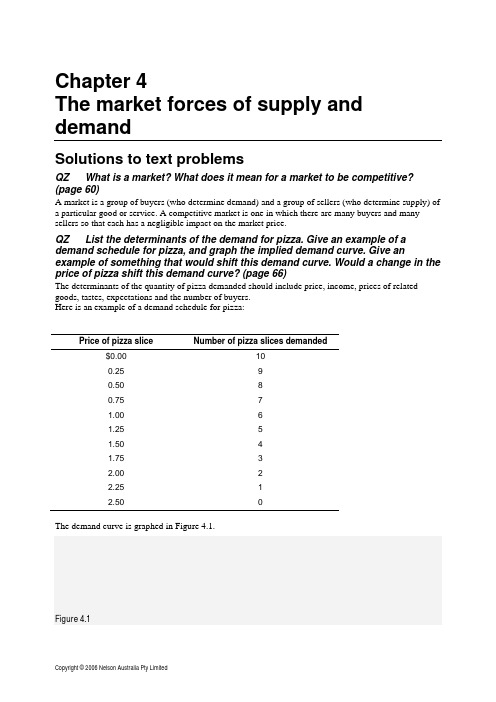

Chapter 4The market forces of supply and demandSolutions to text problemsQZ What is a market? What does it mean for a market to be competitive? (page 60)A market is a group of buyers (who determine demand) and a group of sellers (who determine supply) of a particular good or service. A competitive market is one in which there are many buyers and many sellers so that each has a negligible impact on the market price.QZ List the determinants of the demand for pizza. Give an example of a demand schedule for pizza, and graph the implied demand curve. Give an example of something that would shift this demand curve. Would a change in the price of pizza shift this demand curve? (page 66)The determinants of the quantity of pizza demanded should include price, income, prices of related goods, tastes, expectations and the number of buyers.Here is an example of a demand schedule for pizza:Price of pizza slice Number of pizza slices demanded$0.00 100.25 90.50 80.75 71.00 61.25 51.50 41.75 32.00 22.25 12.50 0The demand curve is graphed in Figure 4.1.Figure 4.1Chapter 4: The market forces of supply and demand 31Examples of things that would shift the demand curve include changes in income, prices of related goods like soft drink or hot dogs, tastes, and expectations about future income or prices.A change in the price of pizza would not shift this demand curve; it would only move from one point to another along the curve.QZ List the determinants of the supply of pizza. Give an example of a supply schedule for pizza, and graph the implied supply curve. Give an example of something that would shift this supply curve. Would a change in the price of pizza shift this supply curve? (page 71)The determinants of the quantity of pizza supplied include the price of pizza, the prices of inputs into pizza production, the technology for producing pizza, expectations about things like the future price of pizza and the number of suppliers of pizza.Here is an example of a supply schedule for pizza:Price of pizza slice Number of pizza slices supplied$0.00 00.25 1000.50 2000.75 3001.00 4001.25 5001.50 6001.75 7002.00 8002.25 9002.50 1000The supply curve is graphed in Figure 4.2.Figure 4.232 Principles of Economics, Third edition, Instructor’s ManualExamples of things that would shift the supply curve include changes in prices of inputs like tomato sauce and cheese, changes in technology like more efficient pizza ovens or automatic dough makers, and changes in expectations about the future price of pizza.A change in the price of pizza would not shift this supply curve; it would only move from one point to another along the curve.QZ Analyse what happens to the market for pizza if the price of tomatoes rises. Analyse what happens to the market for pizza if the price of hamburgers falls. (page 75)If the price of tomatoes rises, the supply curve for pizza shifts to the left because of the increased price of an input into pizza production, however there is no effect on demand. The shift to the left of the supply curve causes the equilibrium price to rise and the equilibrium quantity to decline, as Figure 4.3 shows.Figure 4.3Chapter 4: The market forces of supply and demand 33 If the price of hamburgers falls, the demand curve for pizza shifts to the left because the lower price of hamburgers will lead consumers to buy more hamburgers and less pizza, but there is no effect on supply. The shift to the left of the demand curve causes the equilibrium price to fall and the equilibrium quantity to decline, as Figure 4.4 shows.Figure 4.434 Principles of Economics, Third edition, Instructor’s ManualQuestions for review (page 79)1 A competitive market is a market in which there are many buyers and many sellers so that each has anegligible impact on the market price.2The quantity of a good that buyers demand is determined by the price of the good, income, the prices of related goods, tastes, expectations and the number of buyers.3The demand schedule is a table that shows the relationship between the price of a good and the quantity demanded. The demand curve is the downward-sloping line relating price and quantity demanded. The demand schedule and demand curve are related because the demand curve is simplya graph showing the points in the demand schedule.4The demand curve slopes downward because of the law of demand—other things equal, when the price of a good rises, the quantity demanded of the good falls. People buy less of a good when its price rises, both because they can't afford to buy as much and because they switch to purchasing other goods.5 A change in consumers' tastes leads to a shift of the demand curve. A change in price leads to amovement along the demand curve.6The quantity of a good that sellers supply is determined by the price of the good, input prices, technology, expectations and the number of suppliers.7 A supply schedule is a table showing the relationship between the price of a good and the quantity aproducer is willing and able to supply. The supply curve is the upward-sloping line relating price and quantity supplied. The supply schedule and the supply curve are related because the supply curve is simply a graph showing the points in the supply schedule.8The supply curve slopes upward because when the price is high, suppliers' profits increase, so they supply more output to the market. The result is the law of supply—other things equal, when the price of a good rises, the quantity supplied of the good also rises.9 A change in producers' technology leads to a shift in the supply curve. A change in price leads to amovement along the supply curve.10The equilibrium of a market is the point at which the demand and supply curves intersect. At the equilibrium price, the quantity of the good that buyers are willing and able to buy exactly balances the quantity that sellers are willing and able to sell. If the price is above the equilibrium price, sellers want to sell more than buyers want to buy, so there is a surplus. Sellers try to increase their sales by cutting prices; that continues until they reach the equilibrium price. If the price is below theequilibrium price, buyers want to buy more than sellers want to sell, so there is a shortage. Sellers can raise their price without losing customers; that continues until they reach the equilibrium price. 11When the price of beer rises, the demand for pies declines, because beer and pies are complements and people want to buy less beer. When we say the demand for pies declines, we mean that the demand curve for pies shifts to the left as in Figure 4.5 below. The supply curve for pies isn'taffected. With a shift to the left in the demand curve, the equilibrium price and quantity both decline, as the figure shows. Thus the quantity of pies supplied and demanded both fall. In summary, supply is unchanged, demand is decreased, quantity supplied declines, quantity demanded declines, and the price falls.Chapter 4: The market forces of supply and demand 35Figure 4.512 Prices play a vital role in market economies because they bring markets into equilibrium. If the priceis different from its equilibrium level, quantity supplied and quantity demanded aren't equal. The resulting surplus or shortage leads suppliers to adjust the price until equilibrium is restored. Prices thus serve as signals that guide economic decisions and allocate scarce resources.Problems and applications (page 80)1 a The cyclone damages the banana harvest, reducing the supply of bananas. This can be seen inFigure 4.6 as a shift to the left in the supply curve for bananas. The new equilibrium price is higher than the old equilibrium price. Figure 4.6P r i c e o f p i e sQuantity of bananasP r i c e o f b a n a n a sQuantity of pies36 Principles of Economics, Third edition, Instructor’s Manualb People often go to the pictures during school holidays so demand for picture tickets is highduring school holidays. When school holidays end, fewer people go to the pictures. The result, as shown in Figure 4.7, is a shift to the left in the demand curve. The equilibrium price of picture tickets is thus lower when school holidays end, as the figure shows. Figure 4.7c When a war breaks out in the Middle East, many markets are affected. Since much oilproduction takes place there, the war disrupts oil supplies, shifting the supply curve for petrol tothe left, as shown in Figure 4.8. The result is a rise in the equilibrium price of petrol. With a higher price for petrol, the cost of operating a big car, like a Ford Falcon, will increase. As a result, the demand for used Ford Falcons will decline, as people in the market for cars won't find Falcons as attractive. In addition, some people who already own Falcons will try to sell them. The result is that the demand curve for used Falcons shifts to the left, while the supply curve shifts to the right, as shown in Figure 4.9. The result is a decline in the equilibrium price of used Falcons.Figure 4.8Quantity of theatre tickets P r i c e o f t h e a t r e t i c k e t sP r i c e o f p e t r o l Quantity of petrolChapter 4: The market forces of supply and demand 37Figure 4.92 The statement that ‘an increase in the demand for notebooks raises the quantity of notebooksdemanded, but not the quantity supplied’ is false, in general. As Figure 4.10 shows, the increase in demand for notebooks results in an increased quantity supplied. The only way the statement would be true is if the supply curve were perfectly inelastic, as shown in Figure 4.11. Figure 4.10P r i c e o f u s e d F o r d F a l c o n sQuantity of used Ford Falcons38 Principles of Economics, Third edition, Instructor’s ManualFigure 4.113 a If people decide to have more children (a change in tastes), they'll want larger vehicles forhauling their kids around, so the demand for station wagons will increase. Supply won't be affected. The result is a rise in both price and quantity, as Figure 4.12 shows. Figure 4.12Quantity of Station WagonsP r i c e o f S t a t i o n W a g o n sChapter 4: The market forces of supply and demand 39b If a strike by steelworkers raises steel prices, the costs of producing a station wagon rise (a risein input prices), so the supply of station wagons decreases. Demand won't be affected. The result is a rise in the price of station wagons and a decline in the quantity, as Figure 4.13 shows.Figure 4.13c The development of new automated machinery for the production of station wagons is animprovement in technology. The reduction in firms' costs results in an increase in supply. Demand isn't affected. The result is a decline in the price of station wagons and an increase in the quantity, as Figure 4.14 shows.Figure 4.14d The rise in the price of minivans affects station wagon demand because minivans are substitutesfor station wagons (that is, there's a rise in the price of a related good). The result is an increase in demand for station wagons. Supply isn't affected. In equilibrium, the price and quantity of station wagons both rise, as Figure 4.12 shows.P r i c e o f S t a t i o n W a g o n sQuantity of Station WagonsP r i c e o f S t a t i o n W a g o n sQuantity of Station Wagonse The reduction in peoples' wealth caused by a stock market crash reduces their income, leading toa reduction in the demand for station wagons, since station wagons are a normal good. Supply isn’t affected. As a result, both price and quantity decline, as Figure 4.15 shows. Figure 4.154 Technological advances that reduce the cost of producing computer chips represent a decline in aninput price for producing a computer. The result is a shift to the right in the supply of computers, as shown in Figure 4.16. The equilibrium price falls and the equilibrium quantity rises, as the figure shows. Figure 4.16Quantity of Station WagonsP r i c e o f S t a t i o n W a g o n sSince computer software is a complement to computers, the increased equilibrium quantity of computers increases the demand for software. As Figure 4.17 shows, the result is a rise in both the equilibrium price and quantity of software.Figure 4.17Since typewriters are substitutes for computers, the increased equilibrium quantity of computers reduces the demand for typewriters. As Figure 4.18 shows, the result is a decline in both theequilibrium price and quantity of typewriters.Figure 4.185 a When an outbreak of ‘foot and mouth’ disease hits sheep farms in New Zealand, it raises inputprices for producing woollen jumpers. As a result, the supply of woollen jumpers shifts to the left, as shown in Figure 4.19. The new equilibrium has a higher price and lower quantity of woollen jumpers. Figure 4.19b A decline in the price of leather jackets leads more people to buy leather jackets, reducing thedemand for woollen jumpers. The result, shown in Figure 4.20, is a decline in both theequilibrium price and quantity of woollen jumpers.Figure 4.20Quantity of woollen jumpers P r i c e o f w o o l l e n j u m p e r sQuantity of woollen jumpersP r i c e o f w o o l l e n j u m p e r sc Kylie wearing a woollen jumper raises the demand for woollen jumpers, as shown in Figure4.21. The result is an increase in both the equilibrium price and quantity of woollen jumpers. Figure 4.21d The invention of new knitting machines increases the supply of woollen jumpers. As Figure 4.22shows, the result is a reduction in the equilibrium price and an increase in the equilibriumquantity of woollen jumpers.Figure 4.22P r i c e o f W o o l l e n J u m p e r sQuantity of Woollen Jumpers Quantity of Woollen JumpersP r i c e o f W o o l l e n J u m p e r s6 A temporarily high birth rate in the year 2005 leads to opposite effects on the price of babysittingservices in the years 2010 and 2020. In the year 2010, there are more 5-year-olds who need sitters, so the demand for babysitting services rises, as shown in Figure 4.23. The result is a higher price for babysitting services in 2010. However, in the year 2020, the increased number of 15-year-olds shifts the supply of babysitting services to the right, as shown in Figure 4.24. The result is a decline in the price of babysitting services.Figure 4.23Figure 4.247Since tomato sauce is a complement for hot dogs, when the price of hot dogs rises, the quantity demanded of hot dogs falls, thus reducing the demand for tomato sauce, causing both price and quantity of tomato sauce to fall. Since the quantity of tomato sauce falls, the demand for tomatoes by tomato sauce producers falls, so both price and quantity of tomatoes fall. When the price of tomatoes falls, producers of tomato juice face lower input prices, so the supply curve for tomato juice shifts down, causing the price of tomato juice to fall and the quantity of tomato juice to rise. The fall in the price of tomato juice causes people to substitute tomato juice for orange juice, so the demand for orange juice declines, causing the price and quantity of orange juice to fall. Now you can see clearly why a rise in the price of hot dogs leads to a fall in price of orange juice!8 a Cigars and chewing tobacco are substitutes for cigarettes, since a higher price for cigaretteswould increase demand for cigars and pipe tobacco.b An increase in the tax on cigarettes leads to increased demand for cigars and pipe tobacco. Theresult, as shown in Figure 4.25 for cigars, is a rise in both the equilibrium price and quantity of cigars and pipe tobacco.Figure 4.25c The results in part (b) showed that a tax on cigarettes leads people to substitute cigars and pipetobacco for cigarettes when the tax on cigarettes rises. To reduce total tobacco usage,policymakers might also want to increase the tax on cigars and pipe tobacco, or pursue sometype of public education program.9Quantity supplied equals quantity demanded at a price of $6 and quantity of 81 pizzas (Figure 4.26).If price were greater than $6, quantity supplied would exceed quantity demanded, so suppliers would reduce their price to gain sales. If price were less than $6, quantity demanded would exceed quantity supplied, so suppliers could raise their price without losing sales. In both cases, the price would continue to adjust until it reached $6, the only price at which there is neither surplus nor shortage. Figure 4.2610 a If the price of flour falls, since flour is an ingredient in bagels, the supply curve for bagels wouldshift to the right. The result, shown in Figure 4.27, would be a fall in the price of bagels and arise in the equilibrium quantity of bagels. Since cream cheese is a complement to bagels, the rise in quantity demanded of bagels increases the demand for cream cheese, as shown in Figure 4.28.The result is a rise in both the equilibrium price and quantity of cream cheese. So, a fall in theprice of flour indeed raises both the equilibrium price of cream cheese and the equilibriumquantity of bagels.Figure 4.27Figure 4.28What happens if the price of milk falls? Since milk is an ingredient in cream cheese, the fall in the price of milk leads to an increase in the supply of cream cheese. This leads to a decrease in the price of cream cheese (Figure 4.29), rather than a rise in the price of cream cheese. So a fall in the price of milk couldn't have been responsible for the pattern observed.Figure 4.29b In part (a), we found that a fall in the price of flour led to a rise in the price of cream cheese anda rise in the equilibrium quantity of bagels. If the price of flour rose, the opposite would be true;it would lead to a fall in the price of cream cheese and a fall in the equilibrium quantity ofbagels. Since the question says the equilibrium price of cream cheese has risen, it couldn't have been caused by a rise in the price of flour.What happens if the price of milk rises? From part (a), we found that a fall in the price of milk caused a decline in the price of cream cheese, so a rise in the price of milk would cause a rise in the price of cream cheese. Since bagels and cream cheese are complements, the rise in the price of cream cheese would reduce the demand for bagels, as Figure 4.30 shows. The result is adecline in the equilibrium quantity of bagels. So a rise in the price of milk does cause both a rise in the price of cream cheese and a decline in the equilibrium quantity of bagels.Figure 4.3011 a As Figure 4.31 shows, the supply curve is vertical. The constant supply makes sense because thepicture theatre has a fixed number of seats no matter what the price.Figure 4.31b Quantity supplied equals quantity demanded at a price of $8. The equilibrium quantity is 800tickets. cPriceQuantity demandedQuantity supplied$4 1400 800 8 1100 800 12 800 800 16 500 800 20 200800The new equilibrium price will be $12, which equates quantity demanded to quantity supplied. The equilibrium quantity is 800 tickets.P r i c e o f p i c t u r e t h e a t r e t i c k e t sQuantity of picture theatre tickets 80012The executives are confusing changes in demand with changes in quantity demanded. Figure 4.32 shows the demand curve prior to the marketing campaign (D1), and after the campaign (D2). The marketing campaign increased the demand for champagne, as shown, leading to a higher equilibrium price and quantity. The influence of the higher price on demand is already reflected in the outcome.It's impossible for the scenario outlined by the executives to occur.Figure 4.3213 At equilibrium Q S=Q D. Therefore here:1400 + 700P = 1600 – 300P1000P = 200P = $0.20The equilibrium price is $0.20 per bar of chocolate. Substitute this into either Q S or Q D to get the equilibrium quantity of 1540 bars of chocolate.。

微观经济学学习笔记(曼昆经济学原理)04章节

经济学习笔记第4章供给与需求的市场力量一、重要名词解释市场:由某种物品或服务的买者与卖者组成的一个群体。

竞争市场:有许多买者与卖者,以至于每个人对市场价格的影响都微乎其微的市场。

(竞争市场一般指完全竞争市场。

完全竞争,又称为纯粹竞争,是指不存在任何阻碍和干扰竞争因素的市场情况,亦即没有任何垄断因素的市场结构。

完全竞争市场需要具备四个条件:市场上有大量的买者和卖者;市场上每一个厂商提供的商品都是同质的;所有的资源具有完全的流动性;信息是完全的。

)需求量:买者愿意并且能够购买的一种物品的数量。

需求定理:认为在其他条件不变时,一种物品的价格上升,对该物品的需求量减少的观点。

需求表:表示一种物品的价格与需求量之间关系的表格。

需求曲线:表示一种物品的价格与需求量之间关系的图形。

正常物品:在其他条件相同时,收入增加引起需求量增加的物品。

低档物品:在其他条件相同时,收入增加引起需求量减少的物品。

替代品:一种物品价格的上升引起另一种物品需求量的增加的两种物品。

互补品:一种物品价格的上升引起另一种物品需求量的减少的两种物品。

供给量:卖者愿意并且能够出售的一种物品的数量。

供给定理:认为在其他条件不变时,一种物品的价格上升,该物品的供给量增加的观点。

供给表:表示一种物品的价格与供给量之间关系的表格。

供给曲线:表示一种物品的价格与供给量之间关系的图形。

均衡:市场价格达到使供给量与需求量相等的水平时的状态。

均衡价格/市场出清价格:使供给与需求平衡的价格。

均衡数量:均衡价格下的供给量与需求量。

过剩:供给量大于需求量的状态,也称为超额供给状态。

短缺:需求量大于供给量的状态,也称为超额需求状态。

供求定理:认为任何一种物品的价格都会自发调整,使该物品的供给与需求达到平衡的观点。

(供求定理是指在其他条件不变的情况下,需求变动分别引起均衡价格和均衡数量的同方向变动;供给变动分别引起均衡价格的反方向变动和均衡数量的同方向变动。

)二、重要摘抄1.供给与需求是使市场经济运行的力量。

曼昆经济学原理英文版教案加习题答案第4章THE MARKET FORCES OF SUPPLY AND DEMAND

51WHAT’S NEW IN THE S EVENTH EDITION:The In the News feature “Price Increases after Disasters” has been updated with a new article.LEARNING OBJECTIVES:By the end of this chapter, students should understand:➢ what a competitive market is.➢ what determines the demand for a good in a competitive market.➢ what determines the supply of a good in a competitive market.➢ how supply and demand together set the price of a good and the quantity sold.➢ the key role of prices in allocating scarce resources in market economies.CONTEXT AND PURPOSE:Chapter 4 is the first chapter in a three-chapter sequence that deals with supply and demand and how markets work. Chapter 4 shows how supply and demand for a good determines both the quantity produced and the price at which the good sells. Chapter 5 will add precision to the discussion of supply and demand by addressing the concept of elasticity —the sensitivity of the quantity supplied and quantity demanded to changes in economic variables. Chapter 6 will address the impact of government policies on prices and quantities in markets.The purpose of Chapter 4 is to establish the model of supply and demand. The model of supply and demand is the foundation for the discussion for the remainder of this text. For this reason, time spent studying the concepts in this chapter will return benefits to your students throughout their study of economics. Many instructors would argue that this chapter is the most important chapter in the text.THE MARKET FORCES OF SUPPLY AND DEMAND52 ❖Chapter 4/The Market Forces of Supply and DemandKEY POINTS:• Economists use the model of supply and demand to analyze competitive markets. In a competitive market, there are many buyers and sellers, each of whom has little or no influence on the market price.• The demand curve shows how the quantity of a good demanded depends on the price. According to the law of demand, as the price of a good falls, the quantity demanded rises. Therefore, the demand curve slopes downward.• In addition to price, other determinants of how much consumers want to buy include income, the prices of substitutes and complements, tastes, expectations, and the number of buyers. If one of these factors changes, the demand curve shifts.• The supply curve shows how the quantity of a good supplied depends on the price. According to the law of supply, as the price of a good rises, the quantity supplied rises. Therefore, the supply curve slopes upward.• In addition to price, other determinants of how much producers want to sell include input prices, technology, expectations, and the number of sellers. If one of these factors changes, the supply curve shifts.• The intersection of the supply and demand curves determines the market equilibrium. At the equilibrium price, the quantity demanded equals the quantity supplied.• The behavior of buyers and sellers naturally drives markets toward their equilibrium. When the market price is above the equilibrium price, there is a surplus of the good, which causes the market price to fall. When the market price is below the equilibrium price, there is a shortage, which causes the market price to rise.• To analyze how any event influences a market, we use the supply-and-demand diagram to examine how the event affects equilibrium price and quantity. To do this we follow three steps. First, we decide whether the event shifts the supply curve or the demand curve (or both). Second, we decide which direction the curve shifts. Third, we compare the new equilibrium with the initial equilibrium.• In market economies, prices are the signals that guide economic decisions and thereby allocate scarce resources. For every good in the economy, the price ensures that supply and demand are in balance. The equilibrium price then determines how much of the good buyers choose to consume and how much sellers choose to produce.Chapter 4/The Market Forces of Supply and Demand ❖ 53CHAPTER OUTLINE: I. Markets and CompetitionA. What Is a Market?1. Definition of market: a group of buyers and sellers of a particular good or service.2. Markets can take many forms and may be organized (agricultural commodities) or lessorganized (ice creamB. What Is Competition?1. Definition of competitive market: a market in which there are so many buyers andso many sellers that each has a negligible impact on the market price.2. Each buyer knows that there are several sellers from which to choose. Sellers know that each buyer purchases only a small amount of the total amount sold.C. In this chapter, we will assume that markets are perfectly competitive.1. Characteristics of a perfectly competitive market:a. The goods being offered for sale are exactly the same.b. The buyers and sellers are so numerous that no single buyer or seller has any influence over the market price.2. Because buyers and sellers must accept the market price as given, they are often called "price takers."3. Not all goods are sold in a perfectly competitive market.a. A market with only one seller is called a monopoly market.b. Other markets fall between perfect competition and monopoly.54 ❖ Chapter 4/The Market Forces of Supply and DemandD. We will start by studying perfect competition.1. Perfectly competitive markets are the easiest to analyze because buyers and sellers take the price as a given.2. Because some degree of competition is present in most markets, many of the lessons that we learn by studying supply and demand under perfect competition apply in morecomplicated markets.II. DemandA. The Demand Curve: The Relationship between Price and Quantity Demanded1. Definition of quantity demanded: the amount of a good that buyers are willing andable to purchase.2. One important determinant of quantity demanded is the price of the product.a. Quantity demanded is negatively related to price. This implies that the demand curve isdownward sloping.b. Definition of law of demand: the claim that, other things being equal, thequantity demanded of a good falls when the price of the good rises .3. Definition of demand schedule: a table that shows the relationship between theprice of a good and the quantity demanded. Price of Ice-Cream ConeQuantity of Cones Demanded$0.0012 $0.5010 $1.008 $1.506 $2.004 $2.502 $3.00Figure 1Make sure that you explain that, when we discuss the relationship between quantity demanded and price, we hold all other variables constant. You will need toemphasize this more than once to ensure that students understand why a change inprice leads to a movement along the demand curve.Chapter 4/The Market Forces of Supply and Demand ❖ 554. Definition of demand curve: a graph of the relationship between the price of a good and the quantity demanded.a. Price is generally drawn on the vertical axis.b. Quantity demanded is represented on the horizontal axis. B. Market Demand versus Individual Demand1. The market demand is the sum of all of the individual demands for a particular good orservice.2. The demand curves are summed horizontally —meaning that the quantities demanded are added up for each level of price.3. The market demand curve shows how the total quantity demanded of a good varies with the price of the good, holding constant all other factors that affect how much consumers want to buy.C. Shifts in the Demand Curve1. Because the market demand curve holds other things constant, it need not be stable overtime.56 ❖ Chapter 4/The Market Forces of Supply and Demand2. If any of these other factors change, the demand curve will shift.a. An increase in demand is represented by a shift of the demand curve to the right.b. A decrease in demand is represented by a shift of the demand curve to the left.3. Incomea. The relationship between income and quantity demanded depends on what type of good the product is.b. Definition of normal good: a good for which, other things equal, an increase in income leads to an increase in demand.c. Definition of inferior good: a good for which, other things equal, an increase inincome leads to a decrease in demand.4. Prices of Related Goodsa. Definition of substitutes: two goods for which an increase in the price of one good leads to an increase in the demand for the other.b. Definition of complements: two goods for which an increase in the price of one good leads to a decrease in the demand for the other.5. Tastes6. Expectationsa. Future incomeb. Future prices7. Number of BuyersChapter 4/The Market Forces of Supply and Demand ❖57D. Case Study: Two Ways to Reduce the Quantity of Smoking Demanded1. Public service announcements, mandatory health warnings on cigarette packages, and theprohibition of cigarette advertising on television are policies designed to reduce the demandfor cigarettes (and shift the demand curve to the left).2. Raising the price of cigarettes (through tobacco taxes) lowers the quantity of cigarettesdemanded.a. The demand curve does not shift in this case, however.b. An increase in the price of cigarettes can be shown by a movement along the originaldemand curve.3. Studies have shown that a 10% increase in the price of cigarettes causes a 4% reduction inthe quantity of cigarettes demanded. For teens, a 10% increase in price leads to a 12% dropin quantity demanded.4. Studies have also shown that a decrease in the price of cigarettes is associated with greateruse of marijuana. Thus, it appears that tobacco and marijuana are complements.III. SupplyA. The Supply Curve: The Relationship between Price and Quantity Supplied1. Definition of quantity supplied: the amount of a good that sellers are willing andable to sell.a. Quantity supplied is positively related to price. This implies that the supply curve will beupward sloping.b. Definition of law of supply: the claim that, other things equal, the quantitysupplied of a good rises when the price of the good rises.2. Definition of supply schedule: a table that shows the relationship between the priceof a good and the quantity supplied.58 ❖ Chapter 4/The Market Forces of Supply and Demand3. Definition of supply curve: a graph of the relationship between the price of a good and the quantity supplied. Price of Ice-Cream ConeQuantity of Cones Supplied$0.000 $0.50 0 $1.001 $1.502 $2.003 $2.504 $3.005B. Market Supply versus Individual Supply1. The market supply curve can be found by summing individual supply curves.2. Individual supply curves are summed horizontally at every price.3. The market supply curve shows how the total quantity supplied varies as the price of thegood varies.C. Shifts in the Supply Curve1. Because the market supply curve holds other things constant, the supply curve will shift ifany of these factors changes.a. An increase in supply is represented by a shift of the supply curve to the right.b. A decrease in supply is represented by a shift of the supply curve to the left.Figure 5Figure 7Figure 6You will want to take time to emphasize the difference between a “change in supply” and a “change in quantity supplied.”Chapter 4/The Market Forces of Supply and Demand ❖ 592. Input Prices3. Technology4. Expectations5. Number of Sellers IV. Supply and Demand TogetherA. Equilibrium1. The point where the supply and demand curves intersect is called the market’s equilibrium.2. Definition of equilibrium: a situation in which the market price has reached thelevel at which quantity supplied equals quantity demanded.3. Definition of equilibrium price: the price that balances quantity supplied andquantity demanded.4. The equilibrium price is often called the "market-clearing" price because both buyers andsellers are satisfied at this price.Table 2Figure 8 Students will benefit from seeing equilibrium using both a graph and a supply-and-demand schedule. The schedule will also make it easier for students to understand concepts such as shortages and surpluses.60 ❖Chapter 4/The Market Forces of Supply and Demand5. Definition of equilibrium quantity: the quantity supplied and the quantitydemanded at the equilibrium price.6. If the actual market price is higher than the equilibrium price, there will be a surplus of thegood.Figure 9a. Definition of surplus: a situation in which quantity supplied is greater thanquantity demanded.b. To eliminate the surplus, producers will lower the price until the market reachesequilibrium.7. If the actual price is lower than the equilibrium price, there will be a shortage of the good.a. Definition of shortage: a situation in which quantity demanded is greater thanquantity supplied.b. Sellers will respond to the shortage by raising the price of the good until the marketreaches equilibrium.8. Definition of the law of supply and demand: the claim that the price of any goodadjusts to bring the supply and demand for that good into balance.B. Three Steps to Analyzing Changes in Equilibrium 1. Decide whether the event shifts the supply or demand curve (or perhaps both). 2. Determine the direction in which the curve shifts.3. Use the supply-and-demand diagram to see how the shift changes the equilibrium price andquantity. C. Example: A change in market equilibrium due to a shift in demand —the effect of hot weather onthe market for ice cream.D. Shifts in Curves versus Movements along Curves1. A shift in the demand curve is called a "change in demand." A shift in the supply curve iscalled a "change in supply."2. A movement along a fixed demand curve is called a "change in quantity demanded." Amovement along a fixed supply curve is called a "change in quantity supplied." E. Example: A change in market equilibrium due to a shift in supply —the effect of a hurricane thatdestroys part of the sugar-cane crop and drives up the price of sugar.F. Example: Shifts in both supply and demand —the effect of hot weather and a hurricane thatdestroys part of the sugar cane crop. G. Summary1. When an event shifts the supply or demand curve, we can examine the effects on theequilibrium price and quantity.ALTERNATIVE CLASSROOM EXAMPLE:Go through these examples of events that would shift either the demand or supply of #2 lead pencils:▪ an increase in the income of consumers▪ an increase in the use of standardized exams (using opscan forms) ▪ a decrease in the price of graphite (used in the production of pencils) ▪ a decrease in the price of ink pens ▪ the start of a school year▪ new technology that lowers the cost of producing pencils.2. Table 4 reports the end results of these shifts in supply and demand.H. In the News: Price Increases after Disasters1. When a disaster strikes a region, many good experience an increase in demand or a decreasein supply resulting in upward pressure on prices.2. This article from defends price increases following natural disasters as a naturalresult of market interactions.V. Conclusion: How Prices Allocate ResourcesA. The model of supply and demand is a powerful tool for analyzing markets.B. Supply and demand together determine the prices of the economy’s goods and services.1. These prices serve as signals that guide the allocation of scarce resources in the economy.2. Prices determine who produces each good and how much of each good is produced.SOLUTIONS TO TEXT PROBLEMS:Quick Quizzes1. A market is a group of buyers (who determine demand) and a group of sellers (whodetermine supply) of a particular good or service. A perfectly competitive market is one inwhich there are many buyers and many sellers of an identical product so that each has anegligible impact on the market price.2. Here is an example of a monthly demand schedule for pizza:Price of Pizza Slice Number of Pizza Slices Demanded$ 0.00 100.25 90.50 80.75 71.00 61.25 51.50 41.75 32.00 22.25 12.50 0The demand curve is graphed in Figure 1.Figure 1Examples of things that would shift the demand curve include changes in income, prices ofrelated goods like soda or hot dogs, tastes, expectations about future income or prices, andthe number of buyers.A change in the price of pizza would not shift this demand curve; it would only lead to amovement from one point to another along the same demand curve.3. Here is an example of a monthly supply schedule for pizza:Price of Pizza Slice Number of PizzaSlices Supplied$ 0.00 00.25 1000.50 2000.75 3001.00 4001.25 5001.50 6001.75 7002.00 8002.25 9002.50 1000The supply curve is graphed in Figure 2.Figure 2Figure 3Examples of things that would shift the supply curve include changes in prices of inputs like tomato sauce and cheese, changes in technology like more efficient pizza ovens or automatic dough makers, changes in expectations about the future price of pizza, or a change in the number of sellers.A change in the price of pizza would not shift this supply curve; it would only lead to amovement from one point to another along the same supply curve.4. If the price of tomatoes rises, the supply curve for pizza shifts to the left because there hasbeen an increase in the price of an input into pizza production, but there is no shift indemand. The shift to the left of the supply curve causes the equilibrium price to rise and the equilibrium quantity to decline, as Figure 3 shows.If the price of hamburgers falls, the demand curve for pizza shifts to the left because thelower price of hamburgers will lead consumers to buy more hamburgers and fewer pizzas,but there is no shift in supply. The shift to the left of the demand curve causes theequilibrium price to fall and the equilibrium quantity to decline, as Figure 4 shows.Figure 4Questions for Review1. A competitive market is a market in which there are many buyers and many sellers of anidentical product so that each has a negligible impact on the market price. Another type ofmarket is a monopoly, in which there is only one seller. There are also other markets that fallbetween perfect competition and monopoly.2. The demand schedule is a table that shows the relationship between the price of a good andthe quantity demanded. The demand curve is the downward-sloping line relating price andquantity demanded. The demand schedule and demand curve are related because thedemand curve is simply a graph showing the points in the demand schedule.The demand curve slopes downward because of the law of demand—other things beingequal, when the price of a good rises, the quantity demanded of the good falls. People buyless of a good when its price rises, both because they cannot afford to buy as much andbecause they switch to purchasing other goods.3. A change in consumers' tastes leads to a shift of the demand curve. If the change inconsumers' tastes leads to an increase in demand, consumers want to buy more of this goodat every price level. A change in price leads to a movement along the demand curve.Because price is measured on the vertical axis, a change in the price represents a movementalong the demand curve.4. Because Popeye buys more spinach when his income falls, spinach is an inferior good for him.His demand curve for spinach shifts out to the right as a result of the decrease in his income.5. A supply schedule is a table showing the relationship between the price of a good and thequantity a producer is willing and able to supply. The supply curve is the upward-sloping linerelating price and quantity supplied. The supply schedule and the supply curve are related because the supply curve is simply a graph showing the points in the supply schedule.The supply curve slopes upward because when the price is high, suppliers' profits increase, so they supply more output to the market. The result is the law of supply—other things being equal, when the price of a good rises, the quantity supplied of the good also rises.6. A change in producers' technology leads to a shift in the supply curve. A change in priceleads to a movement along the supply curve.7. The equilibrium of a market is the point at which the quantity demanded is equal to quantitysupplied. If the price is above the equilibrium price, sellers want to sell more than buyers want to buy, so there is a surplus. Sellers try to increase their sales by cutting prices. That continues until they reach the equilibrium price. If the price is below the equilibrium price, buyers want to buy more than sellers want to sell, so there is a shortage. Sellers can raise their price without losing customers. That continues until they reach the equilibrium price.8. When the price of beer rises, the demand for pizza declines, because beer and pizza arecomplements and people want to buy less beer. When we say the demand for pizza declines, we mean that the demand curve for pizza shifts to the left as in Figure 5. The supply curve for pizza is not affected. With a shift to the left in the demand curve, the equilibrium price and quantity both decline, as the figure shows. Thus, the quantity of pizza supplied anddemanded both fall. In sum, supply is unchanged, demand is decreased, quantity supplied declines, quantity demanded declines, and the price falls.Figure 59. Prices play a vital role in market economies because they bring markets into equilibrium. Ifthe price is different from its equilibrium level, quantity supplied and quantity demanded are not equal. The resulting surplus or shortage leads suppliers to adjust the price untilequilibrium is restored. Prices thus serve as signals that guide economic decisions andallocate scarce resources.Quick Check Multiple Choice1. b2. b3. d4. b5. a6. cProblems and Applications1. a. Cold weather damages the orange crop, reducing the supply of oranges and raising theprice of oranges. This leads to a decline in the supply of orange juice because orangesare an important input in the production of orange juice. This can be seen in Figure 6 asa shift to the left in the supply curve for orange juice. The new equilibrium price is higherthan the old equilibrium price.Figure 6b. People often travel to the Caribbean from New England to escape cold weather, so thedemand for Caribbean hotel rooms is high in the winter. In the summer, fewer peopletravel to the Caribbean, because northern climates are more pleasant. The result, asshown in Figure 7, is a shift to the left in the demand curve. The equilibrium price ofCaribbean hotel rooms is thus lower in the summer than in the winter, as the figureshows.Figure 7c. When a war breaks out in the Middle East, many markets are affected. Because a largeproportion of oil production takes place there, the war disrupts oil supplies, shifting thesupply curve for gasoline to the left, as shown in Figure 8. The result is a rise in theequilibrium price of gasoline. With a higher price for gasoline, the cost of operating agas-guzzling automobile like a Cadillac will increase. As a result, the demand for usedCadillacs will decline, as people in the market for cars will not find Cadillacs as attractive.In addition, some people who already own Cadillacs will try to sell them. The result isthat the demand curve for used Cadillacs shifts to the left, while the supply curve shifts to the right, as shown in Figure 9. The result is a decline in the equilibrium price of used Cadillacs.Figure 8 Figure 92. The statement is false. As Figure 10 shows, in equilibrium the increase in demand fornotebooks results in an increased quantity demanded and the quantity supplied.Figure 10 Figure 113. a. If people decide to have more children, they will want larger vehicles for hauling theirkids around, so the demand for minivans will increase. Supply will not be affected. The result is a rise in both the price and the quantity sold, as Figure 12 shows.Figure 12 Figure 13b. If a strike by steelworkers raises steel prices, the cost of producing a minivan rises andthe supply of minivans decreases. Demand will not be affected. The result is a rise in the price of minivans and a decline in the quantity sold, as Figure 13 shows.c. The development of new automated machinery for the production of minivans is animprovement in technology. This reduction in firms' costs will result in an increase in supply. Demand is not affected. The result is a decline in the price of minivans and an increase in the quantity sold, as Figure 14 shows.Figure 14d. The rise in the price of sport utility vehicles affects minivan demand because sport utilityvehicles are substitutes for minivans. The result is an increase in demand for minivans.Supply is not affected. The equilibrium price and quantity of minivans both rise, as Figure12 shows.e. The reduction in peoples' wealth caused by a stock-market crash reduces their income,leading to a reduction in the demand for minivans, because minivans are likely a normal good. Supply is not affected. As a result, both the equilibrium price and the equilibrium quantity decline, as Figure 15 shows.Figure 154. a. DVDs and TV screens are likely to be complements because you cannot watch a DVDwithout a television. DVDs and movie tickets are likely to be substitutes because a movie can be watched at a theater or at home. TV screens and movie tickets are likely to besubstitutes for the same reason.b. The technological improvement would reduce the cost of producing a TV screen, shiftingthe supply curve to the right. The demand curve would not be affected. The result is that the equilibrium price will fall, while the equilibrium quantity will rise. This is shown inFigure 16.Figure 16c. The reduction in the price of TV screens would lead to an increase in the demand forDVDs because TV screens and DVDs are complements. The effect of this increase in the demand for DVDs is an increase in both the equilibrium price and quantity, as shown inFigure 17.Figure 17The reduction in the price of TV screens would cause a decline in the demand for movie tickets because TV screens and movie tickets are substitute goods. The decline in thedemand for movie tickets would lead to a decline in the equilibrium price and quantitysold. This is shown in Figure 18.Figure 185. Technological advances that reduce the cost of producing computer chips represent a declinein an input price for producing a computer. The result is a shift to the right in the supply of computers, as shown in Figure 19. The equilibrium price falls and the equilibrium quantity rises, as the figure shows.Figure 19Because computer software is a complement to computers, the lower equilibrium price of computers increases the demand for software. As Figure 20 shows, the result is a rise in both the equilibrium price and quantity of software.Figure 20Because typewriters are substitutes for computers, the lower equilibrium price of computers reduces the demand for typewriters. As Figure 21 shows, the result is a decline in both the equilibrium price and quantity of typewriters.Figure 216. a. When a hurricane in South Carolina damages the cotton crop, it raises input prices forproducing sweatshirts. As a result, the supply of sweatshirts shifts to the left, as shownin Figure 22. The new equilibrium price is higher and the new equilibrium quantity ofsweatshirts is lower.。

微观经济学原理曼昆英文第四章讲解学习

?Suppose Helen and Ken are the only two buyers in

the Latte market. (Qd = quantity demanded)

Price Helen's Qd Ken's Qd

?In a perfectly competitive market: ?All goods exactly the same ?Buyers & sellers so numerous that no one can

affect market price – each is a “price taker ”

0

Q

5 10 15 20 25

P

$0.00 1.00 2.00 3.00 4.00 5.00 6.00

Qd (Market)

24 21 18 15 12 9 6

THE MARKET FORCES OF SUPPLY AND DEMAND

7

Demand Curve Shifters

?The demand curve shows how price affects

a good and the quantity sold?

?How do changes in the factors that affect demand

or supply affect the market price and quantity of a good?

?How do markets allocate resources?

THE MARKET FORCES OF SUPPLY AND DEMAND

曼昆经济学原理目录

曼昆经济学原理目录曼昆经济学原理(Principles of Economics)是由美国经济学家尼古拉斯·格里高里·曼昆(N. Gregory Mankiw)所著的一本经济学教科书,旨在向大学学生介绍经济学基本原理和理论。

该教材分为三个部分,涵盖了微观经济学、宏观经济学和国际经济学三个领域。

下面将对每个部分的目录进行详细介绍。

第一部分:微观经济学第一章:经济学原理和经济思维- 经济学的基本原理和概念- 经济学家如何思考和分析经济问题第二章:在十大原则中思考- 十大原则介绍:如人们如何面对稀缺性和权衡取舍- 供求原则和市场机制- 政府干预经济的原则第三章:供需:一种模型的起点- 供给和需求的概念- 市场均衡和市场价格的形成- 自由市场与政府管制的比较第四章:市场效果:量与质的考虑- 市场效率和福利经济学- 市场失灵和外部性- 公共物品和共享资源第五章:务实的消费者和无穷的厂商- 消费者选择行为和效用最大化- 企业产量选择和生产成本- 供给曲线和市场调整第六章:市场均衡和资源配置- 市场均衡的概念和效率性- 供求关系和经济的资源配置- 政府政策和市场效率的影响第二部分:宏观经济学第七章:储蓄、投资和资本市场- 储蓄、投资和财务体系- 成本效益分析和资本市场的理论第八章:经济增长和生产函数- 国民收入和生产函数的概念- 技术进步和经济增长- 资本积累对经济增长的影响第九章:失业和通货膨胀- 失业和就业水平- 失业的成因和传统观点- 通货膨胀和货币政策第十章:货币和银行体系- 货币和货币供给- 银行体系和货币创造- 中央银行政策和货币政策工具第十一章:货币市场和货币政策- 资本市场和货币市场的联系- 货币市场利率和货币政策的影响- 货币供给和货币创造的影响第三部分:国际经济学第十二章:国际贸易的原理和比较优势- 国际贸易的原理和概念- 绝对优势和比较优势- 贸易制度和贸易政策第十三章:国际贸易的应用和政策- 暂定均衡和相对比较优势- 贸易政策和进出口管制- 贸易摩擦和贸易战争第十四章:国际金融与公共金融- 汇率和外汇市场- 货币政策和国际金融体系- 公共债务和国际金融危机曼昆经济学原理目录总共包括了14个章节,它们涵盖了经济学的基本原理和概念,并且深入探讨了微观经济学、宏观经济学和国际经济学的各个领域。

曼昆的《微观经济学基础》课业笔记 英文版

曼昆的《微观经济学基础》课业笔记英文版IntroductionThis document presents my notes on "Microeconomics: Principles and Applications" by N. Gregory Mankiw. These notes summarize key concepts and ideas covered in the book, aiming to provide a helpful overview of microeconomics.Chapter 1: Ten Principles of Economics- People face trade-offs: individuals and societies must make choices due to scarcity.- The cost of something is what you give up to get it: when making decisions, considering both the direct and opportunity costs is crucial.- Rational people think at the margin: making decisions by evaluating incremental benefits and costs.- People respond to incentives: incentives can influence individuals' behavior and decision-making.- Trade can make everyone better off: voluntary exchange benefits all parties involved.- Markets are usually a good way to organize economic activity: markets coordinate exchanges efficiently.- A country's standard of living depends on its ability to produce goods and services: productivity is key.- Prices rise when the government prints too much money: inflation can be caused by excessive money supply growth.- Society faces a short-run trade-off between inflation and unemployment: the Phillips curve illustrates this trade-off.Chapter 2: Thinking Like an Economist- Economists use models to simplify reality and understand economic behavior.- Assumptions in economic models help focus on essential elements.- Opportunity cost is the true cost of something and is measured by what we give up to obtain it.Chapter 3: Interdependence and the Gains from Trade- Specialization and international trade result in greater production efficiency and consumption possibilities.- Both parties benefit from trade even if one has an absolute advantage in both goods.- Prices reflect the opportunity cost and guide resources to their most valued uses.Chapter 4: The Market Forces of Supply and Demand- Markets consist of buyers and sellers, and their interactions determine prices and quantities.- Demand curve shows the relationship between price and quantity demanded, while supply curve reflects the relationship between price and quantity supplied.- Market equilibrium occurs when quantity demanded equals quantity supplied.- Changes in demand or supply shift their respective curves, leading to changes in equilibrium price and quantity.ConclusionThese notes provide a brief summary of the key concepts covered in "Microeconomics: Principles and Applications." Studying this bookallows for a deeper understanding of microeconomic principles and their applications in the real world.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Markets and Competition

▪ A market is a group of buyers and sellers of a

particular product.

▪ A competitive market is one with many buyers

and sellers, each has a negligible effect on price.

12

3.00

10

4.00

8

5.00

6

6.00

4

THE MARKET FORCES OF SUPPLY AND DEMAND

4

Helen’s Demand Schedule &a

$6.00

$5.00

$4.00

Price Quantity of of lattes

0

Q

5 10 15 20 25

P

$0.00 1.00 2.00 3.00 4.00 5.00 6.00

Qd (Market)

24 21 18 15 12 9 6

THE MARKET FORCES OF SUPPLY AND DEMAND

7

Demand Curve Shifters

▪ The demand curve shows how price affects

quantity demanded, other things being equal.

▪ These “other things” are non-price determinants

quantities demanded by all buyers at each price.

▪ Suppose Helen and Ken are the only two buyers in

the Latte market. (Qd = quantity demanded)

Price Helen’s Qd Ken’s Qd

▪ In this chapter, we assume markets are perfectly

competitive.

THE MARKET FORCES OF SUPPLY AND DEMAND

2

Demand

▪ The quantity demanded of any good is the

▪ In a perfectly competitive market: ▪ All goods exactly the same ▪ Buyers & sellers so numerous that no one can

affect market price – each is a “price taker”

a good and the quantity sold?

▪ How do changes in the factors that affect demand

or supply affect the market price and quantity of a good?

▪ How do markets allocate resources?

Market Qd

$0.00

16

+8

=

24

1.00

14

+7

=

21

2.00

12

+6

=

18

3.00

10

+5

=

15

4.00

8

+4

=

12

5.00

6

+3

=

9

6.00

4

+2

=

6

6

The Market Demand Curve for Lattes

P

$6.00 $5.00 $4.00 $3.00 $2.00 $1.00 $0.00

amount of the good that buyers are willing and able to purchase.

▪ Law of demand: the claim that the quantity

demanded of a good falls when the price of the good rises, other things equal

THE MARKET FORCES OF SUPPLY AND DEMAND

3

The Demand Schedule

▪ Demand schedule:

a table that shows the relationship between the price of a good and the quantity demanded

lattes demanded

$0.00 16

1.00

14

2.00

12

$3.00

3.00

10

$2.00

4.00

8

$1.00

5.00

6

6.00

4

$0.00 0

Quantity

5

10

15 of Lattes

THE MARKET FORCES OF SUPPLY AND DEMAND

5

Market Demand versus Individual Demand ▪ The quantity demanded in the market is the sum of the

4 C H A P T E R

The Market Forces of Supply and Demand

Economics P R I N C I P L E S O F

N. Gregory Mankiw

© 2009 South-Western, a part of Cengage Learning, all rights reserved

▪ Example:

Helen’s demand for lattes.

▪ Notice that Helen’s

preferences obey the Law of Demand.

Price Quantity of of lattes

lattes demanded

$0.00 16

1.00

14

2.00

In this chapter, look for the answers to these questions:

▪ What factors affect buyers’ demand for goods? ▪ What factors affect sellers’ supply of goods? ▪ How do supply and demand determine the price of