中级会计课后习题

中级会计职称第10章股份支付课后习题及答案

中级会计职称《中级会计实务》第十章课后练习题及答案第十章股份支付一、单项选择题1.下列关于股份支付的特征,表述不正确的是()。

A.股份支付是企业及职工或其他方之间发生的交易B.股份支付的目的是为了增加企业费用,合理避税C.股份支付交易的对价或其定价及企业自身权益工具未来的价值密切相关D.股份支付是以获取职工或其他方服务为目的的交易答案:B解析:股份支付的目的是为了获取职工服务和其他方提供服务,虽然这个过程增加了费用,但其主要目的却不是为了避税。

2.职工和其他方行使权利、获取现金或权益工具的日期是()。

A.授予日B.可行权日C.行权日D.出售日答案:C解析:行权日是指职工和其他方行使权利、获取现金或权益工具的日期。

3.信达公司为一上市公司,为了激励员工,制定了一份股份激励计划。

协议中规定信达公司将从市场上回购本公司股票,用于激励符合条件的高层管理人员。

信达公司这一举动属于()。

A.以权益结算的股份支付B.以现金结算的股份支付C.以负债结算的股份支付D.以净资产结算的股份支付答案:A解析:股份支付包括以现金结算的股份支付和以权益结算的股份支付。

信达公司从市场回购本公司股票用于行权,最终支付的是从市场上回购的本企业的股票,没有现金或其他资产流出企业,属于以权益结算的股份支付。

4.对于内在价值计量的权益结算的股份支付,结算发生在等待期的,结算时支付的款项应当作为回购该权益工具处理,结算支付的款项高于该权益工具在回购日内在价值的部分,计入()。

A.公允价值变动损益B.资本公积——股本溢价C.管理费用D.资本公积——其他资本公积答案:C解析:对于权益结算的股份支付,结算发生在等待期内的,企业应当将结算作为加速可行权处理,结算支付的款项高于该权益工具在回购日内在价值的部分,计入管理费用。

5.企业授予高层管理者的以权益结算的股份支付,至行权完毕,整个会计处理中不可能涉及的会计科目是()。

A.管理费用B.公允价值变动损益C.生产成本D.资本公积——股本溢价答案:B解析:授予高层管理者的以权益结算的股份支付,企业应在等待期内每个资产负债表日确认管理费用,选项A正确;授予一线生产员工的以权益结算的股份支付,企业应在等待期内每个资产负债表日确认生产成本,选项C正确;以权益结算的股份支付,行权时,差额会计入资本公积(股本溢价)中,选项D正确;以现金结算的股份支付,可行权日后,负债公允价值的变动计入公允价值变动损益,以权益结算的股份支付不会涉及该科目,选项B不正确。

中级财务会计第二章课后习题答案

第二章章节测验题一、单项选择题:(每题2分,共10分)1.对于银行已入账而企业尚未入账的未达账项,企业应当(D )。

A根据“银行对账单”入账B根据“银行存款余额调节表”入账C根据对账单和调节表自制凭证入账D待有关结算凭证到达后入账2.除中国人民银行另有规定外,支票的提示付款期限一般为自出票日起(B)天。

A 7B 10C 15D 203.根据《现金管理暂行条例》规定,下列经济业务中,不能用现金支付的是(C)。

A支付职工奖金5000元B支付零星办公用品购置费800元C支付材料采购货款1200元D支付职工差旅费2000元4.企业支付的银行承兑手续费应计入(B)账户。

A营业费用B财务费用C其他业务成本D营业外支出5.企业一般不得坐支现金,因特殊情况需要坐支现金的单位,应事先报(C)审查批准,并在核定的范围和限额内进行。

A税务部门B其他应付款C开户银行D上级主管单位二、多项选择题:(每题4分,共20分)1.下列各项,符合现金支付范围的是(ABD)。

A支付差旅人员现金2000元B向农民贾某收购农产品支付现金5000元C支付税务机关罚款现金3000元D支付职工奖金10000元2.企业资产负债表中“货币资金”项目的期末数包括(ABC)。

A“库存现金”总账期末余额B“银行存款”总账期末余额C“其他货币资金”总账期末余额D“其他应收款”总账期末余额3、根据《人民银行结算账户管理办法》将单位银行结算账户分为(ABCD)。

A基本存款账户B一般存款账户C专用存款账户D临时存款账户4、现金清查的主要内容有(ABD )。

A是否存在挪用B是否存在白条抵库C是否存在未达账项D是否存在超限额库存现金5、根据《企业会计制度》规定,下列各项,属于其他货币资金的有(ABD)。

A备用金B存出投资款C银行承兑汇票D银行汇票存款三、判断题(每题2分,共10分)1、为减少货币资金管理和控制中产生舞弊的可能,并及时发现有关人员的舞弊行为,对涉及货币资金管理和控制的业务人员应实行定期轮换岗位制度。

中级财务会计课后答案(王华主编)

第二章存货1、(1)3月1日,借:原材料贷:应付账款——应付暂估价(2)3月3日,借:原材料250 000贷:在途物资250 000 (3)3月8日借:原材料508 000 应交税费--应交增值税(进项税额) 85 000贷:银行存款593 000 (4)3月10日借:周转材料-—包装物20 000贷:委托加工物资20 000 (5)3月12日借:原材料108 000 应交税费—-应交增值税(进项税额)17 000贷:其他货币资金——银行汇票存款125 000借:银行存款175 000贷:其他货币资金——银行汇票存款175 000 (6)3月18日借:原材料150 000 应交税费——应交增值税(进项税额)25 500贷:应付票据175 500 (7)借:原材料53 000 应交税费—-应交增值税(进项税额)8 500贷:预付账款61 500 借:预付账款41 500贷:银行存款41 5002、(1)3月5日借:材料采购500 000 应交税费—-应交增值税(进项税额)85 000贷:应付票据585 000 (2)3月8日借:原材料650 000贷:材料采购500 000 材料成本差异150 000(3)3月20日,购入时,借:材料采购 1 020 000 应交税费--应交增值税(进项税额)170 000贷:银行存款 1 190 000 入库时,借:原材料 1 100 000贷:材料采购 1 020 000 材料成本差异80 000 (4) 借:生产成本 1 000 000制造费用50 000管理费用200 000贷:原材料 1 250 000 分配材料成本差异,①成本差异率=(100 000+150 000+80 000)÷(5 000 000+650 000+1 100 000)×100%=4.89%②应计入生产成本的材料成本差异=1 000 000×4。

89%=48 900③应计入制造费用的材料成本差异=50 000×4。

《中级财务会计》人大(第3版)课后习题答案完整版

第2章货币资金和应收款项教材练习题答案练习一(1)2日,从银行提取现金。

借:库存现金800 贷:银行存款800 (2)5日,以现金支票拨付备用金。

借:备用金----采购部门500 贷:银行存款500 (3)8日,以库存现金补足备用金。

借:制造费用350 贷:库存现金350 (4)12日,以库存现金支付办公费用。

借:管理费用280 贷:库存现金280 (5)15日,报销备用金。

借:管理费用360 贷:备用金----采购部门360 (6)16日,盘盈现金,转入营业外收入,并将现金存入银行。

借:库存现金480 贷:待处理财产损溢480 借:待处理财产损溢480 贷:营业外收入480 借:银行存款480 贷:库存现金480 (7)18日,购买原材料,款项以银行存款支付。

借:原材料10 000 应交税费----应交增值税(进项税额) 1 300贷:银行存款11 300 (8)19日,收到应收账款。

借:银行存款 3 500 贷:应收账款 3 500 (9)27日,发现库存现金短缺。

借:待处理财产损溢30 贷:库存现金30 (10)29日,现金短缺计入管理费用。

借:管理费用30 贷:待处理财产损溢30练习二(1)21日,办理银行汇票。

借:其他货币资金----银行汇票18 000贷:银行存款18 000 (2)23日,持银行汇票购买原材料。

借:原材料15 000 应交税费----应交增值税(进项税额) 1 950贷:其他货币资金----银行汇票16 950 (3)26日,将银行存款划入证券公司。

借:其他货币资金----存出投资款8 800 贷:银行存款8 800 (4)30日,收到银行汇票的多余退款。

借:银行存款 1 050 贷:其他货币资金----银行汇票 1 050练习三(1)20×1年3月6日,销售商品,收到商业承兑汇票。

借:应收票据226 000 贷:主营业务收入200 000 应交税费----应交增值税(销项税额)26 000 (2)20×1年5月6日,商业承兑汇票到期。

中级财务会计课后习题答案(全部)教材习题答案(全部).docx

教材练习题参考答案第二章货币资金【参考答案】(1)①出差借支时借:其他应收款一一张某1000贷:银行存款1000②归来报销时借:管理费用850库存现金150贷:其他应收款1000(2)①开立临时采购户吋借:其他货币资金一一外埠存款80 000贷:银行存款80 000②收到购货单位发票时借:原材料60 000应交税费一一应交增值税(进项税额)10 200贷:其他货币资金一一外埠存款70 200③将多余资金转回原来开户行时借:银行存款9 800贷:其他货币资金一一外埠存款9 800(3)①收到开户银行转来的付款凭证吋借:其他货币资金一一信用卡3 000贷:银行存款3 000②收到购物发票账单时借:管理费用2 520贷:其他货币资金一一信用卡25 20(4)拨出备用金时借:备用金1000贷:银行存款10 00(5)总务部门报销时借:管理费用900贷:库存现金9 00(6)①期末盘点发现短缺时借:待处理财产损溢一一待处理流动资产损溢50贷:库存现金50②经批准计入损益吋借:管理费用5 0贷:待处理财产损溢一一待处理流动资产损溢50第三章应收款项【参考答案】1.(1)办妥托收银行收款手续时:借:应收账款11700贷:主营业务收入10 000应交税费一应交增值税(销项税额)17 0 00(2)如在10天内收到货款时借:银行存款11 466财务费用23 4贷:应收账款11700(3)如在30内收到货款时借:银行存款11700贷:应收账款117002.(1)收到票据时借:应收票据93 6 00贷:主营业务收入80 000应交税费一应交增值税(销项税额)13 600(2)年终计提票据利息借:应收票据15 60贷:财务费用1560(3 )到期收回货款借:银行存款98 280贷:应收票据95 160财务费用3 1203.(1)第一年末借:资产减值损失5 000贷:坏账准备5 000(2)第二年末借:资产减值损失7 500贷:坏账准备7 500(3 )第三年末借:坏账進备1500贷:资产减值损失1500(3)第四年6月发生坏账时借:坏账准备18 000贷:应收账款18 00010月收回己核销的坏账时借:应收账款5 00 0贷:坏账准备5 000借:银行存款5 000贷:应收账款5000年末计提坏账准备时借:资产减值损失1 2 000贷:坏账准备12 00 0第四章存货【参考答案】1.(1)实际成本核算:该批甲材料的实际总成本=20 000+200=2 0 200 (元)借:原材料•甲材料20 2 00应交税费•应交增值税3 400贷:银行存款23 600(2)计划成本核算①购进借:材料采购■甲材料20 200应交税费•应交增值税3 400贷:银行存款23 600②入库材料成本差异=20 200-990X18 =2380元,超支差异借:原材料--- 甲材料17 820 (=990X18)材料成本差异2380贷:材料采购——甲材料20 20 02.(1)先进先出法6月7日①发出A材料的成本=200X 60+20 0X 66=25 20 0 (元)6月18日②发出A材料的成本=300X 66 +500X 70=54 800 (元)6月29日③发出A材料的成本=100 X70+200X68 =20 600 (元)期末结存A材料成本=300X68=20 400 (元)(2)月末一次加权平均法加权平均单位成本二(12 000+109 0 00) 4- (200+1 600) ^67.22 (元/公斤)期末结存A材料的成本=300 X67.22=201 66 (元)本月发出A 材料的成本二(12 000+109 00 0) -20166=1 00834 (元)(3 )移动加权平均法6月5日①购进后移动平均单位成本二(12000+33 000)一(200+500) =64.29 (元/公斤)6月7日结存A材料成本=300X64 .29=19287 (元)6 月7 日发出A 材料成本=(12000+330 00) -19287=25713 (元)6月16日②购进后移动平均单位成本二(19287+42 000) 4- (300+600) =68.10 (元/公斤)6月18日结存A材料成本=100X68 .10=6810 (元)6 月18 日发出A 材料成本二(19287+4200 0) -6810=54 477 (元)6月27日③购进后移动平均单位成本二(6810+34000 )0 (100+500 )=68.02 (元/公斤)6月29日结存A材料成本=300X68.02 =20406 (元)6月29日发出A材料成本二(68 10+34000)・20406=2040 4 (元)期末结存A材料成本=300X68 .02=20406 (元)3.A产品:有销售合同部分:A产品可变现净值=40X (1105)=4 20(万元),成本=40X10=400 (万元),这部分存货不需计提跌价准备。

中级会计课后试题及答案

中级会计课后试题及答案一、单项选择题(每题1分,共10分)1. 会计的基本职能是()。

A. 核算和监督B. 决策和控制C. 预测和评价D. 计划和预算答案:A2. 会计要素中的资产是指企业拥有或控制的()。

A. 经济资源B. 经济利益C. 经济权利D. 经济义务答案:A3. 会计信息质量要求中,要求企业应当以实际发生的交易或事项为依据,这体现了()。

A. 可靠性B. 相关性C. 可理解性D. 及时性答案:A4. 会计分期假设的基础是()。

A. 货币计量B. 持续经营C. 会计分期D. 历史成本答案:C5. 会计政策变更,如果能够提供更可靠、更相关的会计信息,应采用()。

A. 追溯调整法B. 未来适用法C. 重估法D. 直接变更法答案:A6. 对于固定资产的折旧,企业应当根据其使用情况和性能变化,合理选择折旧方法,这体现了会计信息质量要求中的()。

A. 重要性B. 谨慎性C. 一致性D. 可比性答案:A7. 企业在编制财务报表时,应当遵循()。

A. 权责发生制B. 收付实现制C. 历史成本D. 公允价值答案:A8. 企业在进行利润分配时,首先应当提取的是()。

A. 法定公积金B. 任意公积金C. 资本公积D. 盈余公积答案:A9. 企业对外提供的财务报表至少应当包括()。

A. 资产负债表B. 利润表C. 现金流量表D. 所有者权益变动表答案:A、B、C10. 会计估计变更采用未来适用法进行会计处理,不调整以前年度的相关项目,这体现了会计信息质量要求中的()。

A. 可靠性B. 相关性C. 可比性D. 及时性答案:C二、多项选择题(每题2分,共10分)1. 会计核算的基本前提包括()。

A. 会计主体B. 持续经营C. 货币计量D. 会计分期答案:A、B、C、D2. 会计政策变更的具体情况包括()。

A. 采用不同的存货计价方法B. 改变固定资产的折旧方法C. 改变投资性房地产的后续计量模式D. 改变财务报表的列报格式答案:A、B、C3. 会计估计的依据包括()。

中级财务会计课后习题答案详解首都经济贸易大学出版社

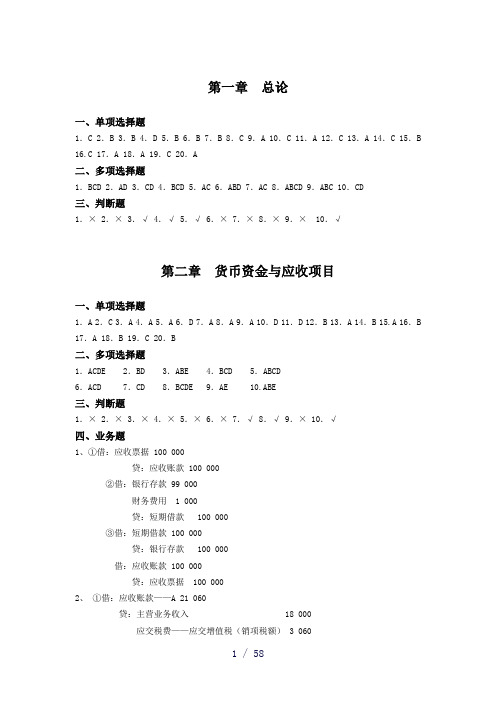

第一章总论一、单项选择题1.C 2.B 3.B 4.D 5.B 6.B 7.B 8.C 9.A 10.C 11.A 12.C 13.A 14.C 15.B16.C 17.A 18.A 19.C 20.A二、多项选择题1.BCD 2.AD 3.CD 4.BCD 5.AC 6.ABD 7.AC 8.ABCD 9.ABC 10.CD三、判断题1.× 2.× 3.√ 4.√ 5.√ 6.× 7.× 8.× 9.× 10.√第二章货币资金与应收项目一、单项选择题1.A 2.C 3.A 4.A 5.A 6.D 7.A 8.A 9.A 10.D 11.D 12.B 13.A 14.B 15.A 16.B 17.A 18.B 19.C 20.B二、多项选择题1.ACDE 2.BD 3.ABE 4.BCD 5.ABCD6.ACD 7.CD 8.BCDE 9.AE 10.ABE三、判断题1.× 2.× 3.× 4.× 5.× 6.× 7.√ 8.√ 9.× 10.√四、业务题1、①借:应收票据 100 000贷:应收账款 100 000②借:银行存款 99 000财务费用 1 000贷:短期借款 100 000③借:短期借款 100 000贷:银行存款 100 000借:应收账款 100 000贷:应收票据 100 0002、①借:应收账款——A 21 060贷:主营业务收入 18 000应交税费——应交增值税(销项税额) 3 060②借:应收账款——B 46 800贷:主营业务收入 40 000应交税费——应交增值税(销项税额) 6 800③借:银行存款 21 060贷:应收账款——A 21 060借:银行存款 46 000财务费用 800贷:应收票据 46 8003、①2007年借:资产减值损失——计提的坏账准备 4 000贷:坏账准备 4 000②2008年借:坏账准备 18 000贷:应收账款——甲 18 000借:资产减值损失——计提的坏账准备 26 500贷:坏账准备 26 500③2009年借:应收账款——丁 5 000贷:坏账准备 5 000借:银行存款 5 000贷:应收账款——丁 5 000借:坏账准备 11 500贷:资产减值损失——计提的坏账准备 11 500④2010年无分录。

中级财务会计上册课后习题答案

第二章货币资金参考答案1.(1)借:库存现金 6000贷:银行存款 6000(2)借:其他应收款——王芳 8000贷:库存现金 8000(3)借:银行存款 50000贷:应收账款——乙公司 50000(4)借:原材料 100000 应交税费——应交增值税(进项税额)17000贷:银行存款 117000 (5)借:应付账款——丁公司 30000贷:银行存款 30000 (6)借:管理费用 8236贷:其他应收款——王芳 8000库存现金 236(7)借:银行存款 10000贷:库存现金 10000(8)借:待处理财产损溢 200贷:库存现金 200(9)借:库存现金 200贷:待处理财产损溢 200(10)借:库存现金 702贷:主营业务收入 600应交税费——应交增值税(销项税额)102 (11)借:银行存款 23400贷:主营业务收入 20000应交税费——应交增值税(销项税额)3400银行存款余额调节表3、(1)借:其他货币资金——银行汇票 50000贷:银行存款 50000 (2)借:原材料 40000应交税费——应交增值税(进项税额)6800贷:其他货币资金——银行汇票 46800 (3)借:银行存款 3200贷:其他货币资金——银行汇票 3200 (4)借:管理费用 2100贷:其他货币资金——信用卡 21004、(1)借:财务费用 125贷:库存现金 125(2)借:管理费用 2000贷:银行存款 2000(3)借:银行存款 100000贷:应收账款——乙公司 100000(4)借:其他货币资金——银行汇票 500000贷:银行存款 500000(5)借:应付职工薪酬——工资 680000贷:银行存款 680000(6)借:其他货币资金——存出投资款 50000000贷:银行存款 50000000(7)借:其他货币资金——银行汇票 500000贷:银行存款 500000借:原材料 420000应交税费——应交增值税(进项税额)71400贷:其他货币资金——银行汇票 491400借:银行存款 8600贷:其他货币资金——银行汇票 8600(8)借:其他货币资金——信用卡 80000财务费用 1500贷:银行存款 81500(9)借:银行存款 200000贷:应收票据 200000(10)借:应付账款——乙公司 50000贷:银行存款 50000(11)借:应收账款 88180贷:主营业务收入 74000应交税费——应交增值税(销项税额)12580银行存款 1600借:银行存款 88180贷:应收账款 88180第三章练习题参考答案1.(1)借:应收账款——重汽公司 58 900贷:主营业务收入——A商品 50 000应交税费——应交增值税(销项税额) 8 500银行存款 400(2)不做处理(3)借:银行存款 58 900贷:应收账款——重汽公司 58 900(4)借:应收账款——重汽公司 10 530贷:主营业务收入——B商品 9 000应交税费——应交增值税(销项税额) 1 530 (5)借:应收票据 10 530贷:应收账款——重汽公司 10 530(6)借:应收账款——元首公司 5 8500贷:主营业务收入——A商品 50 000应交税费——应交增值税(销项税额) 8500(7)借:银行存款 6 830财务费用——现金折扣支出 1 170贷:应收账款——元首公司 58 5002.(1)借:应收票据 117 000贷:主营业务收入——A商品 100 000应交税费——应交增值税(销项税额) 17 000(2)到期值=117 000+117 000×5%×3÷12=118 462.50贴现息=118 462.50×6%÷360×56=1 105.65贴现所得=118 462.50-1 105.65=117 356.85票据利息=117 000×5%×3÷12=1 462.50计提的票据利息=117 000×5%÷12÷2=243.75借:银行存款 117 356.85财务费用(贴现利息) 1 105.65贷:应收票据 117 243.75财务费用(票据利息) 1 218.75将上述分录合并后如下:借:银行存款 117 356.85贷:应收票据 117 243.75财务费用 113.10(3)借:应收票据 234 000贷:主营业务收入——A商品 200 000应交税费——应交增值税(销项税额) 34 000(4)到期值=234 000+234 000×5%×90÷360=236 925贴现息=236 925×8%÷360×29=1 526.85贴现所得=236 925-1 526.85=235 398.15借:银行存款 235 398.15财务费用 1 526.85贷:短期借款——本金 236 9252009年6月30日,应计提应收票据利息(234 000×5%×70÷360=2 275),分录如下:借:应收票据 2 275贷:财务费用 2 275(5)借:短期借款——本金 236 925贷:应收票据 236 275财务费用 650(6)借:短期借款——本金 236 925贷:银行存款 236 925借:应收账款——济南灯泡厂 236 925贷:应收票据 236 275财务费用 650(7)按照算头不算尾,实际经历天数为3月份22天,4月份30天,5月份31天,6月份7天(2008.06.01至2008.06.08,8号这一天不算在内),一共90天。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

3. Reliant Pharmaceutical paid rent on its office building for the next two years and charged the entire expendi-ture to rent expense.4. Rockville Engineering records revenue only after products have been shipped, even though customers pay Rockville 50% of the sales price in advance.Indicate the organization related to IFRS that performs each of the following functions: 1. Obtains funding for the IFRS standard-setting process. 2. Det ermines IFRS. 3. Encourages cooperation among securities regulators to promote effective and efficient capital markets. 4. Provides input about the standard-setting agenda.5. Provides implementation guidance about relatively narrow issues.BE 1–6IFRS● LO1–11IFRSListed below are several transactions that took place during the first two years of operations for the law firm of Pete, Pete, and Roy.Year 1Year 2Amounts billed to customers for services rendered .....................................$170,000$220,000Cash collected from customers .....................................................................160,000190,000Cash disbursements: ...................................................................................... Salaries paid to employees for services rendered during the year ..........90,000100,000 Utilities .......................................................................................................30,00040,000 Purchase of insurance policy .....................................................................60,000–0–In addition, you learn that the company incurred utility costs of $35,000 in year 1, that there were no liabili-ties at the end of year 2, no anticipated bad debts on receivables, and that the insurance policy covers a three-year period.R equired: 1. Calculate the net operating cash flow for years 1 and 2. 2. Prepare an income statement for each year similar to I llustration 1–3 on page xxx according to the accrual accounting model.3. Determine the amount of receivables from customers that the company would show in its year 1 and year 2 balance sheets prepared according to the accrual accounting model.L isted below are several transactions that took place during the second two years of operations for RPG Consulting. Year 2Year 3Amounts billed to customers for services rendered$350,000$450,000Cash collected from credit customers 260,000400,000Cash disbursements: Payment of rent80,000–0– Salaries paid to employees for services rendered during the year 140,000160,000 Travel and entertainment 30,00040,000 Advertising15,00035,000In addition, you learn that the company incurred advertising costs of $25,000 in year 2, owed the advertising agency $5,000 at the end of year 1, and there were no liabilities at the end of year 3. Also, there were no antici-pated bad debts on receivables, and the rent payment was for a two-year period, year 2 and year 3.R equired: 1. Calculate accrual net income for both years.2. Determine the amount due the advertising agency that would be shown as a liability on the RPG’s balance sheet at the end of year 2.T he F ASB Accounting Standards Codification represents the single source of authoritative U.S. generallyaccepted accounting principles.R equired:1. Obtain the relevant authoritative literature on fair value measurements using the FASB’s Codification Research System at the FASB website ( w ). Identify the Codification topic number that provides guidance on fair value measurements.E 1–1Accrual accounting● LO1–2E 1–2A ccrual accounting● L O1–2E 1–3F ASB codification research● LO1–32. What is the specific citation that lists the disclosures required in the notes to the financial statements for each major category of assets and liabilities measured at fair value?3. List t he disclosure requirement s. A ccess the FASB’s Codification Research System at the FASB website ( w ). Det ermine t he specific citation for each of the following items:1. The topic number for business combinations.2. The topic number for related party disclosures.3. The topic, subtopic, and section number for the initial measurement of internal-use software.4. The topic, subtopic, and section number for the subsequent measurement of asset retirement obligations.5. The topic, subtopic, and section number for the recognition of stock compensation. Three groups that participate in the process of establishing GAAP are users, preparers, and auditors. These groups are represented by various organizations. For each organization listed below, indicate which of these groups it primarily represents. 1. Securit ies and Exchange Commission 2. Financial Execut ives Int ernat ional 3. American Institute of Certified Public Accountants 4. Institute of Management Accountants5. Association of Investment Management and Research F or each of the items listed below, identify the appropriate financial statement element or elements. 1. Obligation to transfer cash or other resources as a result of a past transaction. 2. Dividends paid by a corporation to its shareholders. 3. Inflow of an asset from providing a good or service. 4. The financial position of a company. 5. Increase in equity during a period from nonowner transactions.6. Increase in equity from peripheral or incidental transaction.7. Sale of an asset used in the operations of a business for less than the asset’s book value.8. The owners’ residual interest in the assets of a company.9. An item owned by the company representing probable future benefits. 10. Revenues plus gains less expenses and losses.11. An owner’s contribution of cash to a corporation in exchange for ownership shares of stock. 12. Outflow of an asset related to the production of revenue.Listed below are several terms and phrases associated with the FASB’s conceptual framework. Pair each item from List A (by letter) with the item from List B that is most appropriately associated with it.List AList B1. Predictive value a . Decreases in equity resulting from transfers to owners.2. Relevance b. Requires consideration of the costs and value of information.3. Timelinessc . Important for making interfirm comparisons. 4. Distribution to owners d. Applying the same accounting practices over time.5. Confirmatory value e . U sers understand the information in the context of the decisionbeing made. 6. Understandability f. A greement between a measure and the phenomenon it purportsto represent. 7. Gaing. Information is available prior to the decision. 8. Faithful representation h . Pertinent to the decision at hand.9. Comprehensive income i . Implies consensus among different measurers. 10. Materiality j . Information confirms expectations.11. Comparability k . The change in equity from nonowner transactions.12. Neutrality l . The process of admitting information into financial statements. 13. Recognition m. The absence of bias.14. Consistency n. Results if an asset is sold for more than its book value. 15. Cost effectiveness o. Information is useful in predicting the future.16. Verifiabilityp. Concerns the relative size of an item and its effect on decisions.CODEE 1–4F ASB codification research● LO1–3CODEE 1–5P articipants in establishing GAAP● LO1–3E 1–6 Financial statement elements● LO1–7E 1–7 Concepts; terminology; conceptual framework● LO1–7P hase A of the joint FASB and IASB conceptual framework project stipulates the desired fundamental and enhancing qualitative characteristics of accounting information. Several constraints impede achieving these desired characteristics. Answer each of the following questions related to these characteristics and constraints.1. Which component would allow a company to record the purchase of a $120 printer as an expense rather than capitalizing the printer as an asset?2. Donald Kirk, former chairman of the FASB, once noted that “ . . . there must be public confidence that the standard-setting system is credible, that selection of board members is based on merit and not the influence of special interests . . .” Which characteristic is implicit in Mr. Kirk’s statement?3. Allied Appliances, Inc., changed its revenue recognition policies. Which characteristic is jeopardized by this change?4. National Bancorp, a publicly traded company, files quarterly and annual financial statements with the SEC. Which characteristic is relevant to the timing of these periodic filings?5. In general, relevant information possesses which qualities?6. When there is agreement between a measure or description and the phenomenon it purports to represent, information possesses which characteristic?7. Jeff Brown is evaluating two companies for future investment potential. Jeff’s task is made easier because both companies use the same accounting methods when preparing their financial statements. Which charac-teristic does the information Jeff will be using possess?8. A company should disclose information only if the perceived benefits of the disclosure exceed the costs of providing the information. Which constraint does this statement describe? Listed below are several terms and phrases associated with basic assumptions, broad accounting principles, and constraints. Pair each item from List A (by letter) with the item from List B that is most appropriately associated with it.List AList B1. Matching principle a. The enterprise is separate from its owners and other entities.2. Periodicity b. A common denominator is the dollar.3. Historical cost principle c. The entity will continue indefinitely.4. Materiality d. R ecord expenses in the period the related revenue is recognized.5. Realization principle e . The original transaction value upon acquisition.6. Going concern assumption f . All information that could affect decisions should be reported.7. Monetary unit assumption g. T he life of an enterprise can be divided into artificial time periods.8. Economic entity assumption h . Criteria usually satisfied at point of sale.9. Full-disclosure principlei. Concerns the relative size of an item and its effect on decisions.Listed below are several statements that relate to financial accounting and reporting. Identify the basic assump-tion, broad accounting principle, or component that applies to each statement.1. Jim Marley is the sole owner of Marley’s Appliances. Jim borrowed $100,000 to buy a new home to be used as his personal residence. This liability was not recorded in the records of Marley’s Appliances.2. A pple Inc. distributes an annual report to its shareholders.3. H ewlett-Packard Corporation depreciates machinery and equipment over their useful lives.4. Crosby Company lists land on its balance sheet at $120,000, its original purchase price, even though the land has a current fair value of $200,000.5. H oneywell Corporation records revenue when products are delivered to customers, even though the cash has not yet been received.6. Liquidation values are not normally reported in financial statements even though many companies do go out of business.7. I BM Corporation , a multibillion dollar company, purchased some small tools at a cost of $800. Even though the tools will be used for a number of years, the company recorded the purchase as an expense. Identify the basic assumption or broad accounting principle that was violated in each of the following situations.1. Pastel Paint Company purchased land two years ago at a price of $250,000. Because the value of the land has appreciated to $400,000, the company has valued the land at $400,000 in its most recent balance sheet.2. Atwell Corporation has not prepared financial statements for external users for over three years.3. The Klingon Company sells farm machinery. Revenue from a large order of machinery from a new buyer was recorded the day the order was received.4. Don Smith is the sole owner of a company called Hardware City. The company recently paid a $150 utility bill for Smith’s personal residence and recorded a $150 expense.E 1–8 Qualitative characteristics● LO1–7E1–9 Basic assumptions, principles, and constraints● LO1–7 through LO1–9E1–10 Basic assumptions and principles● LO1–7 through LO1–9E1–11 Basic assumptions and principles● LO1–8, LO1–95. Golden Book Company purchased a large printing machine for $1,000,000 (a material amount) and recorded the purchase as an expense.6. Ace Appliance Company is involved in a major lawsuit involving injuries sustained by some of its employees in the manufacturing plant. The company is being sued for $2,000,000, a material amount, and is not insured. The suit was not disclosed in the most recent financial statements because no settlement had been reached.For each of the following situations, indicate whether you agree or disagree with the financial reporting practice employed and state the basic assumption, component, or accounting principle that is applied (if you agree) or violated (if you disagree).1. Wagner Corporation adjusted the valuation of all assets and liabilities to reflect changes in the purchasing power of the dollar.2. Spooner Oil Company changed its method of accounting for oil and gas exploration costs from successful efforts to full cost. No mention of the change was included in the financial statements. The change had a material effect on Spooner’s financial statements.3. Cypress Manufacturing Company purchased machinery having a five-year life. The cost of the machinery is being expensed over the life of the machinery.4. Rudeen Corporation purchased equipment for $180,000 at a liquidation sale of a competitor. Because the equipment was worth $230,000, Rudeen valued the equipment in its subsequent balance sheet at $230,000.5. Davis Bicycle Company received a large order for the sale of 1,000 bicycles at $100 each. The customer paid Davis the entire amount of $100,000 on March 15. However, Davis did not record any revenue until April 17, the date the bicycles were delivered to the customer.6. Gigantic Corporation purchased two small calculators at a cost of $32.00. The cost of the calculators was expensed even though they had a three-year estimated useful life.7. Esquire Company provides financial statements to external users every three years. For each of the following situations, state whether you agree or disagree with the financial reporting practice employed, and briefly explain the reason for your answer.1. The controller of the Dumars Corporation increased the carrying value of land from its original cost of $2 million to its recently appraised value of $3.5 million.2. The president of Vosburgh Industries asked the company controller to charge miscellaneous expense for the purchase of an automobile to be used solely for personal use.3. At the end of its 2013 fiscal year, Dower, Inc., received an order from a customer for $45,350. The merchan-dise will ship early in 2014. Because the sale was made to a long-time customer, the controller recorded the sale in 2013.4. At the beginning of its 2013 fiscal year, Rossi Imports paid $48,000 for a two-year lease on warehouse space. Rossi recorded the expenditure as an asset to be expensed equally over the two-year period of the lease.5. The Reliable Tire Company included a note in its financial statements that described a pending lawsuit against the company.6. The Hughes Corporation, a company whose securities are publicly traded, prepares monthly, quarterly, and annual financial statements for internal use but disseminates to external users only the annual financial statements.L isted below are the basic assumptions, broad accounting principles, and constraints discussed in this chapter. a . Economic entity assumptiong. Matching principleb . Going concern assumption h. Full-disclosure principlec . Periodicit y assumpt ion i. Cost effect iveness d. Monetary unit assumption j. Materiality e . Historical cost principle k. Conservatismf . Realizat ion principleI dentify by letter the assumption, principle, or constraint that relates to each statement or phrase below. 1. Revenue is recognized only after certain criteria are satisfied. 2. Information that could affect decision making should be reported. 3. Cause-and-effect relationship between revenues and expenses. 4. The basis for measurement of many assets and liabilities. 5. Relates to the qualitative characteristic of timeliness. 6. All economic events can be identified with a particular entity. 7. The benefits of providing accounting information should exceed the cost of doing so.E1–12 Basic assumptions and principles● LO1–7 through LO1–9E1–13 Basic assumptions and principles● LO1–7 through LO1–9E1–14 Basic assumptions and principles● LO1–7 through LO1–9T he following questions are adapted from a variety of sources including questions developed by the AICPA Board of Examiners and those used in the Kaplan CPA Review Course to study the environment and theoreti-cal structure of financial accounting while preparing for the CPA examination. Determine the response that best completes the statements or questions.1. Which of the following is n ot a qualitative characteristic of accounting information according to the FASB’s conceptual framework?a. Audit or independence. b. Neut ralit y. c. Timeliness. d. Predict ive value.2. According to the conceptual framework, neutrality is a characteristic of a. Underst andabilit y. b. Fait hful represent at ion. c. Relevance. d. Bot h relevance and fait hful represent at ion.3. The Financial Accounting Standards Board (FASB) a. Is a division of the Securities and Exchange Commission (SEC).b. Is a private body that helps set accounting standards in the United States.CPA Exam Questions● LO1–7● LO1–7● LO1–3C PA and CMA Exam QuestionsIFRS IFRS IFRSQuestionsimilar results being obtained by both the accountant and an independent party using the same measure-Recognition is the process of formally recording and reporting an item in the financial statements. In orderc. Mat erial.d. Realized or realizable.B roaden YourThese cases will provide you an opportunity toou will also work with other students, inte-This In 1934, Congress created the Securities and Exchange Commission (SEC) and gave the commission both the J udgmentThe purpose of t his case is t o int roduce you t o t he informat ion available on t he websit e of t he Int ernat ionalAccounting Standards Board (IASB).R equired:Access the IASB home page on the Internet. The web address is w .Answer t he following quest ions. 1. Describe the mission of the IASB.2. The IASB has how many board members?3. Who is the current chairman of the IASB?4. Where is t he IASB locat ed? Economic reforms in the People’s Republic of China are moving that nation toward a market-driven economy. China’s account ing pract ices must also change t o accommodat e t he needs of pot ent ial invest ors. In an art icle entitled “Institutional Factors Influencing China’s Accounting Reforms and Standards,” Professor Bing Xiang analyzes the changes in the accounting environment of China during the recent economic reforms and their impli-cations for the development of accounting reforms.R equired: 1. In your library or from some other source, locate the indicated article in A ccounting Horizons, June 1998.2. Briefly describe the economic reforms that led to the need for increased external financial reporting in China.3. Conformity with International Accounting Standards was specified as an overriding objective in formulating China’s accounting standards. What is the author’s opinion of this objective?Some t heorist s cont end t hat companies t hat creat e pollut ion should report t he social cost of t hat pollut ion in income statements. They argue that such companies are indirectly subsidized as the cost of pollution is borne by society while only production costs (and perhaps minimal pollution fines) are shown in the income statement. Thus, the product sells for less than would be necessary if all costs were included.A ssume that the FASB is considering a standard to include the social costs of pollution in the income state-ment. The process would require considering both relevance and faithful representation of the information pro-duced by the new standard. Your instructor will divide the class into two to six groups depending on the size of the class. The mission of your group is to explain how the concepts of relevance and faithful representation relate to this issue.R equired:Each group member should consider the question independently and draft a tentative answer prior to the class ses-sion for which the case is assigned.I n class, each group will meet for 10 to 15 minutes in different areas of the classroom. During that meeting, group members will take turns sharing their suggestions for the purpose of arriving at a single group treatment.A ft er t he allot t ed t ime, a spokesperson for each group (select ed during t he group meet ings) will share t he group’s solution with the class. The goal of the class is to incorporate the views of each group into a consensus answer to the question.One of your friends is a financial analyst for a major stock brokerage firm. Recently she indicated to you that shehad read an article in a weekly business magazine that alluded to the political process of establishing accounting standards. She had always assumed that accounting standards were established by determining the approach that conceptually best reflected the economics of a transaction.R equired:Write a one to two-page article for a business journal explaining what is meant by the political process for estab-lishing accounting standards. Be sure to include in your article a discussion of the need for the FASB to balance accounting considerations and economic consequences.It is the responsibility of management to apply accounting standards when communicating with investors and creditors through financial statements. Another group, auditors, serves as an independent intermediary to help ensure that management has in fact appropriately applied GAAP in preparing the company’s financial statements. Auditors examine (audit) financial statements to express a professional, independent opinion. The opinion reflects the auditors’ assessment of the statements’ fairness, which is determined by the extent to which they are prepared in compliance with GAAP.S ome feel that it is impossible for an auditor to give an independent opinion on a company’s financial statements because the auditors’ fees for performing the audit are paid by the company. In addition to the audit fee, quite often the auditor performs other services for the company such as preparing the company’s income tax returns.R equired:How might an auditor’s ethics be challenged while performing an audit?R esearch Case 1–4A ccessing IASB information through the Internet● LO1–3R esearch Case 1–5A ccounting standards in China● LO1–3, LO1–4Communication Case 1–6Relevance and reliability● LO1–7C ommunication Case 1–7A ccounting standard setting● LO1–4E thics Case 1–8T he auditors’ responsibility● LO1–4Generally accepted accounting principles do not require companies to disclose forecasts of any financial variablesto external users. A friend, who is a finance major, is puzzled by this and asks you to explain why such relevant information is not provided to investors and creditors to help them predict future cash flows.R equired:Explain to your friend why this information is not routinely provided to investors and creditors.Mary McQuire is trying to decide how to invest her money. A friend recommended that she buy the stock of one of two corporations and suggested that she should compare the financial statements of the two companies before making a decision.R equired: 1. Do you agree that Mary will be able to compare the financial statements of the two companies?2. What role does the auditor play in ensuring comparability of financial statements between companies? Phase A of the joint FASB and IASB conceptual framework project includes a discussion of the constraint cost effectiveness. Assume that the FASB is considering revising an important accounting standard.R equired: 1. What is the desired benefit from revising an accounting standard?2. What are some of the possible costs that could result from a revision of an accounting standard?3. What does the FASB do in order to assess possible benefits and costs of a proposed revision of an accounting standard? A new client, the Wolf Company, asks your advice concerning the point in time that the company should recog-nize revenue from the rental of its office buildings. Renters usually pay rent on a quarterly basis at the beginning of the quarter. The owners contend that the critical event that motivates revenue recognition should be the date the cash is received from renters. After all, the money is in hand and is very seldom returned.R equired: 1. Describe the two criteria that must be satisfied before revenue can be recognized.2. Do you agree or disagree with the position of the owners of Wolf Company? Support your answer.Revenues measure the accomplishments of a company during the period. Expenses are then matched with rev-enues to produce a periodic measure of performance called n et income.R equired: 1. Explain what is meant by the phrase m atched with revenues.2. Describe the four approaches used to implement the matching principle and label them 1 through 4.3. For each of the following, identify which matching approach should be used to recognize the cost as expense. a . The cost of producing a product. b . The cost of advertising.c . The cost of monthly rent on the office building.d . The salary of an office employee. e . Depreciat ion on an office building. When a company makes an expenditure that is neither a payment to a creditor nor a distribution to an owner, management must decide if the expenditure should be capitalized (recorded as an increase in an asset) or expensed (recorded as an expense thereby decreasing owners’ equity).R equired: 1. Which factor or factors should the company consider when making this decision?2. Which key accounting principle is involved?3. Are there any constraints that could cause the company to alter its decision?Selected financial statements from a recent annual report of The G ap Inc. follow. Use these statements to answer the following questions.R equired:1. What amounts did Gap report for the following items for the 2010 fiscal year ended January 29, 2011?a . Tot al net revenues b . Tot al operat ing expenses c . Net income (earnings)J udgment Case 1–9Q ualitative characteristics● LO1–7J udgment Case 1–10G AAP , comparability, and the role of the auditor● LO1–4, LO1–7J udgment Case 1–11C ost effectiveness● L O1–7J udgment Case 1–12T he realization principle● LO1–9A nalysis Case 1–13T he matching principle● LO1–9J udgment Case 1–14C apitalize or expense?● LO1–9R eal World Case 1–15E lements; disclosures; The Gap Inc.● LO1–7, LO1–9d. Tot al asset se. Tot al st ockholders’ equit y2. How many shares of common stock did the company have issued on January 29, 2011?3. Why do you think Gap reports more than one year of data in its financial statements? Real World FinancialsTHE GAP INC.Consolidated Balance Sheets($ and shares in millions except par value)January 29,2011January 30,2010AssetsCurrent assets:Cash and cash equivalents$ 1,561$ 2,348Short-term investments100225Merchandise inventory1,6201,477 Other current assets 645 614Total current assets3,9264,664 Property and equipment, net2,5632,628 Other long-term assets 576 693Total assets$ 7,065$ 7,985 Liabilities and Stockholders’ EquityCurrent liabilities:Accounts payable$ 1,049$ 1,027 Accrued expenses and other current liabilities9961,063 Income taxes payable 50 41Total current liabilities 2,095 2,131 Lease incentives and other long-term liabilities 890 963 Commitments and contingencies (see Notes 9 and 13)Stockholders’ equity:Common stock $0.05 par valueAuthorized 2,300 shares; Issued 1,106 for all periodspresented; Outstanding 588 and 676 shares5555 Additional paid-in capital2,9392,935Retained earnings11,76710,815 Accumulated other comprehensive earnings185155 Treasury stock, at cost (518 and 430 shares)(10,866) (9,069)Total stockholders’ equity 4,080 4,891 Total liabilities and stockholders’ equity$ 7,065$ 7,985THE GAP INC.Consolidated Statements of IncomeFiscal Year($ and shares in millions except per share amounts)201020092008 Net sales$14,664$14,197$14,526 Cost of goods sold and occupancy expenses 8,775 8,473 9,079 Gross profit5,8895,7245,447 Operating expenses 3,921 3,909 3,899 Operating income1,9681,8151,548 Interest expense (reversal)(8)61 Interest income (6) (7) (37) Income before income taxes1,9821,8161,584 Income taxes 778 714 617 Net income$ 1,204$ 1,102$ 967Weighted-average number of shares—basic636694716 Weighted-average number of shares—diluted641699719 Earnings per share—basic$1.89$1.59$1.35 Earnings per share—diluted$1.88$1.58$1.34 Cash dividends declared and paid per share$0.40$0.34$0.34。