高级财务会计作业三01

高级财务会计第3次在线作业答案

高级财务会计在线作业三1.某企业采用人民币作为记账本位币。

下列项目中,不属于该企业外币业务的是()A 与外国企业发生的以人民币计价结算的购货业务B 与国内企业发生的以美元计价的销售业务C 与外国企业发生的以美元计价结算的购货业务D 与中国银行之间发生的美元与人民币的兑换业务正确答案:A2.企业因经营所处的主要经济环境发生重大变化,确需变更记账本位币的,将所有项目折算为变更后的记账本位币应当采用的汇率是()。

A 变更当日的即期汇率B 变更当期期初的市场汇率C 按照系统合理的方法确定的、与交易发生日即期汇率近似的汇率D 资产负债表日汇率正确答案:A3.下列说法正确的是()正确答案:AA 企业记账本位币一经确定,不得随意变更,除非企业经营所处的主要经济环境发生重大变化。

B 企业的记账本位币一经确定,不得变更。

C 企业的记账本位币一定是人民币D 企业的编报货币可以是人民币以外的币种4.收到以外币投入的资本时,其对应的资产账户采用的折算汇率是()A 收到外币资本时的市场汇率B 投资合同约定汇率C 签订投资时的市场汇率D 第一次收到外币资本时的折算汇率正确答案:A5.国内甲公司的记账本位币为人民币。

2008年12月5日以每股7港元的价格购入乙公司的H股10 000股作为交易性金融资产,当日汇率为1港元=1元人民币,款项已支付。

2008年12月31日,当月购入的乙公司H股的市价变为每股8元,当日汇率为1港元=0.9元人民币。

假设不考虑相关税费的影响。

甲公司2008年12月31日应确认的公允价值变动损益为()元 A 2000 B 0 C -1000 D 1000 正确答案:A6.甲公司外币业务采用业务发生时的汇率进行核算,按月计算汇兑损益。

5月20日对外销售产品发生应收账款500万欧元,当日的市场汇率为1欧元=10.30元人民币。

5月31日的市场汇率为1欧元=10.28元人民币;6月1日的市场汇率为1欧元=10.32元人民币;6月30日的市场汇率为1欧元=10.35元人民币。

电大本科高级财务会计形成性考核册作业3答案

高级财务会计第三次作业答案一、单项选择题(每小题2分,共20分)1、D2、D3、A4、B5、D6、B7、C8、A9、A 10、D二、多项选择题(每小题2分,共20分)1、BCE2、ABC3、ABC4、BC5、BC6、AC7、CD8、ABD9、AB 10、ABC三、简答题(每小题5分,共10分)1、时态法的基本内容:(1)资产负债表:对货币性工程按现行汇率折算;对于按历史成本反映的非货币性工程按历史汇率折算,对于按现行成本表示的非货币性工程按现行汇率折算;对股本、资本公积工程按形成时的历史汇率进行折算,未分配利润为轧算的平衡数;(2)利润表:固定资产折旧费及无形资产摊销费按历史汇率进行折算外,销售成本工程按照“期初存货+当期购货–期末存货=当期销货”的公式计算确定的;其他收入、费用工程按平均汇率进行折算;2、对于衍生工具,表外应披露以下内容:(1)企业持有衍生工具的类别、意图、取得使得公允价值、期初公允价值以及期末的公允价值。

(2)在资产负债表中确认和停止确认该衍生工具的时间标准。

(3)与衍生工具有关的利率、汇率风险、价格风险、信用风险的信息以及这些信息对未来现金流量的金额和期限可能产生影响的重要条件和情况。

(4)企业管理当局为控制与金融工具相关的风险而采取的政策以及金融工具会计处理方面所采取的其他重要的会计政策和方法。

四、业务题(共50分)1、解:单位为元题目有误:缺少“销售成本的历史成本”这一数字,设该数字为X(1)计算非货币性资产的持有损益存货:未实现持有损益=400 000-240 000=160 000(元)已实现持有损益=608 000-X(元)固定资产:设备房屋未实现持有损益=(144 000-144 000/15)-112 000=134 400-112 000=22 400(元)设备房屋已实现持有损益=144 000/15-(120 000-112 000)=9 600-8 000=1 600(元)土地:未实现持有损益=720 000-360 000=360 000(元)已实现持有损益=0(2)重新编制资产负债表资产负债表(现行成本基础)金额:元注:“留存收益”来自于以现行成本基础编制的利润表。

17秋学期《高级财务会计》在线作业一二三满分标准答案

在线作业一一、单选题(共 10 道试题,共 40 分。

)1. 2006年3月10日,甲公司销售一批材料给乙公司,开出的增值税专用发票上注明的销售价款为200000元,增值税消项税额为34000元,款项尚未收到。

2006年6月4日,甲公司与乙公司进行债务重组;重组协议如下:甲公司同意豁免乙公司债务80000元;债务延长期间,每月加收余款2%的利息,利息和本金于2006年9月4日一同偿还。

假定甲公司为该项应收账款计提坏账准备2000元,整个债务重组交易没有发生相关税费。

在债务重组日,甲公司应确认的债务重组损失为()元。

A. 68760B. 78000C. 63960D. 0正确答案:A2. 下列有关股份支付的说法中,不正确的是()。

A. 股份支付是企业与职工或其他方之间发生的交易B. 股份支付是以获取职工或其他方服务为目的的交易C. 股份支付的对价或其定价与企业自身权益工具未来的价值密切相关D. 股份支付是企业与股东之间发生的交易正确答案:D3. 企业采用成本模式计量的投资性房地产,且投资性房地产不属于企业的主管业务,按期计提折旧或进行摊销,应该借记的科目是()。

A. 其他业务成本B. 管理费用C. 制造费用D. 营业外支出正确答案:A4. 不计提折耗的油气资产是()。

A. 探明矿区权益B. 未探明矿区权益C. 油气勘探形成的油气资产D. 油气开发形成的油气资产正确答案:B5. 法定清算按清算的法律程序不同,可以分为()。

A. 普通清算和特别清算B. 任意清算和强制清算C. 特别清算和破产清算D. 一般清算和普通清算正确答案:A6. 清算会计计量基础是()。

A. 历史成本B. 预计净残值C. 现行重置成本D. 变现价值正确答案:D7. 股份支付在下列时点一般不做会计处理的是()。

A. 授予日B. 等待期内的每个资产负债表日C. 可行权日D. 行权日正确答案:A8. 租赁开始日是指()。

A. 租赁协议日B. 租赁各方就主要租赁条款作出承诺日C. 租赁协议日与租赁各方就主要租赁条款作出承诺日中的较早者D. 租赁协议日与租赁各方就主要租赁条款作出承诺日中的较晚者正确答案:C9. 甲公司于2002年1月1日采用经营租赁方式从乙公司租入机器设备一台,租期为4年,设备价值为200万元,预计使用年限为12年。

中央电大形成性考核系统高级财务会计作业三

1。

解答:货币性资产:期初数=900*(132/100)=1188(万元)期末数=1000*(132*132)=1000(万元)货币性负债期初数=(9000+20000)*(132/100)=38280(万元)期末数=(800+16000)*(132/132)=24000(万元)存货期初数=9200*(132/100)=12144(万元)期末数=13000*(132/125)=13728(万元)固定资产净值期初数=36000*(132/100)=47520(万元)期末数=28800*(132/100)=38016(万元)股本期初数=10000*(132/100)=13200(万元)期末数=10000*(132/100)=13200(万元)盈余公积期初数=5000*(132/100)=6600(万元)期末数=6600+1000=7600(万元)留存收益期初数=(1188+12144+47520)—38280-13200=9372(万元)期末数=(100+1372838016)-24000—13200=15544(万元)未分配利润期初数=2100*(132/100)=2772(万元)期末数=15544-7600=7944(万元)2.解答:存货未实现持有损益=400000—24000=16000(元)已实现持有损益=60800—376000=232000(元)固定资产设备房屋未实现持有损益=134400—111200=22400(元)设备房屋已实现持有损益=9600—8000=1600(元)土地未实现持有损益=72000—36000=360000(元)未实现持有损益=160000+22400+360000=542400(元)已实现持有损益=23200+1600=233600(元)3A股份有限公司(以下简称A公司)对外币业务采用交易发生日的即期汇率折算,按月计算汇兑损益。

2007年6月30日市场汇率为1美元=7.25元人民币。

高级财务会计作业3参考答案

高级财务会计作业3参考答案一、单项选择题(每小题1分,共20分)1C 2B 3C 4A5B 6B 7D 8A9B 10C11A12B 13A14A15A16B 17B 18A19A20C二、多项选择题(每小题1分,共15分)1ACD 2ABE 3ABCD 4ACDE 5CE 6ABCE 7ACD 8ABCD9ABC 10BCE 11ACDE 12ABE 13AD 14CD 15AC三、简答题(每小题5分,共15分)1. 在期货交易中,浮动盈亏与平仓盈亏有何不同?期货交易所或期货投资企业会计对此应如何处理?答:浮动盈亏是指会员单位的持仓合约随着合约价格波动所形成的潜在盈利或亏损,是反映期货交易风险的一个重要指标。

平仓盈亏是指会员将持有合约进行平仓了结交易时,必然发生的盈亏。

浮动盈亏与平仓盈亏不同在于浮动盈亏是持仓合约尚未实现的盈亏,反映会员当日的潜在的获利机会或亏损风险;而平仓盈亏是已实现的盈亏,应根据合约的初始成交价、平仓价的差额及平仓量计算,反映会员累计的平仓盈亏。

期货交易所对会员盈亏的核算包括浮动盈亏和平仓盈亏两种。

在每日无负债结算制度下,交易所使用的是当日浮动盈亏概念,当日浮动盈亏是指持仓期内某个交易日产生的盈亏;开仓当日浮动盈亏应根据当日结算价与当日开仓价的差额计算。

平仓盈亏是已实现盈亏,应根据合约的初始成交价、平仓价的差额及平仓量计算;当日浮动盈亏与当日平仓盈亏之和构成会员当日盈亏。

盈利作为会员权益的增加,调整增加会员的结算准备金;亏损作为会员权益的减少,调整减少会员的结算准备金。

期货投资企业在持仓期内,主要核算浮动盈亏对期货保证金的影响,对持仓合约的浮动盈亏会计上不予确认。

仅在要求追加保证金的情况下,因涉及企业资金的实际运动,会计上才对保证金的增加进行核算。

期货合约平仓时,会计上一方面要确认平仓盈亏,企业确认的平仓盈亏是该合约的累计的平仓盈亏,另一方面要调整期货保证金余额。

2. 物价的持续变动对会计有何影响?答:一是对会计理论的影响,主要表现:1、对币值不变假设的冲击。

高级财务会计作业三答案(Adva...

高级财务会计作业三答案(Advanced financial accountingassignments three answers)See assignment 2010, fall semester, advanced financial accounting, online homework threeTotal score: 100 test time: - test scores: 100Multiple-choice questions, multiple-choice questions, judgment questionsFirst, radio questions (10 questions, 40 points) Score: 40V 1., according to "enterprise accounting standards - investment real estate", the following items do not belong to investment real estate is (D).A. rented buildingB. holds and intends to transfer land use rights after value-addedC. leased land use rightsD. holds and prepares value-added housing after transfer of buildingsFull Score: 4 points: 4TwoFor equity settled share based payment in return for services of employees, enterprises should be in the waiting period for each balance sheet date, the fair value of the equity instruments at the grant date, will be obtained in the current service included in the relevant asset costs or expenses of the current period, at the same time (included in the B).A. capital reserve - equity premiumB. capital reserves - other capital reservesC. surplus reserveD. payable to staff and workersFull Score: 4 points: 43. for cash settled share based payment enterprises after the vesting date to the settlement date before each balance sheet date due to changes in the fair value of liabilities should be included in the (D).A. management feesB. manufacturing expenseC. capital reserveD. fair gain or loss in valueFull Score: 4 points: 4FourThe third company for real estate development enterprises to invest in real estate in accordance with the fair value valuation model, in January 1, 2007 the company will have a book value of 40 million yuan, has been developed as a real estate inventory to business rental, the fair value of 50 million yuan; in December 31, 2007 the fair value of 49 million yuan, and the company confirmed the changes in the fair the value of the lease expires in July 2008 by the company to 53 million yuan price to sell, do not consider the hypothesis related taxes, profit and loss should be recognized when the third company sale is (CMillion yuan.A. 300B. 400C. 1300D. 2200Full Score: 4 points: 4FiveThe investment real estate of an enterprise adopts the fair value measurement model. A building was purchased for rent in January 1, 2007. The cost of the building is $5 million 100 thousand, payable in bank deposits. The building is expected to last 20 years. The net salvage value is expected to be $100 thousand. The fair value of the building was $5 million 80 thousand in June 30, 2007. The accounting treatment to be made in June 30, 2007 (D).A.: other business cost Credits: accumulated depreciationB.: management fee Credits: accumulated depreciationC.: investment real estate loan: fair value change profit and lossD. by: fair value changes in profits and losses Loans: investment real estateFull Score: 4 points: 4SixThe investment real estate of an enterprise adopts the model of cost value measurement. A building was purchased for rent in January 1, 2007. The cost of the building is $2 million 700 thousand and the estimated useful life is 20 years, with a net residual value of $300 thousand. Depreciation is calculated bythe straight-line method. The amount of depreciation that should be paid in 2007 is (CMillion yuan.A. 12B. 20C. 11D. 10Full Score: 4 points: 47. a Limited by Share Ltd is a listed company that needs to prepare quarterly financial statements. The following statements do not require the company to disclose in its financial accounting report for the third quarter of 2009 (D).A. balance sheet at the end of the third quarter of 2009B. profit statement for the third quarter of 2009C. from the beginning of 2009 to the end of the third quarterD. cash flow statement for the third quarter of 2009Full Score: 4 points: 48. the initial entry value of an investment real estate isgenerally recognized as (C).A. plan costB. book valueC. historical costD. fair valueFull Score: 4 points: 49., enterprises use the fair value model of investment real estate, "investment real estate" subject term debit balance reflects (B).A. enterprise investment real estate costThe fair value of investment real estate in B. EnterprisesC. excess amount of investment real estateD. variable profit or loss on investment real estateFull Score: 4 points: 4Between the 10. affiliated enterprises real estate leasing, lease rental real estate shall be confirmed as (A).A. investment real estateB. enterprises for their own use of real estateC. lessee's real estateInventory of D. EnterprisesFull Score: 4 points: 4Two, (a total of 10 multiple-choice questions, a total of 40 points.) VThe main factors to consider when determining the 1. business segment are (ABCDE).A. the nature of a product or serviceThe nature of the B. processC. types of customers who buy products or receive servicesD. the method of use in selling goods or servicesE. legal environment for the production of products and provision of labor servicesFull marks: 42. in the interim financial statements, the comparative accounting statements that the enterprise should provide include (ABCD).A. the balance sheet at the end of the year and the balance sheet of the previous year.B. this interim profit statement.C. from the beginning of the year to the end of the middle of the year, as well as the profit statement for the comparable period of the previous year.D. until the beginning of the cash flow statement at the end of last year the mid and early to mid late than the cash flow statement.E. current interim cash flow statementFull marks: 43. a division that meets one of the following conditions can be identified as reportable segments, and these conditions are (ABD).A. segment revenue accounts for 10% or more of all segment revenuesB. the absolute amount of the segment's profit or loss, which accounts for 10% of or above the total amount of all profit segments, the total amount of profits, or the absolute amount of the total loss of all loss segmentsC. segment costs for the division account for 10% or more of all departmental expensesD. the segment assets comprise 10% of or above the total assets of all segmentsE. segment liabilities account for 10% or more of the total liabilities of all segmentsFull marks: 44., dividing the mining area is the basic work of the oil and gas mining accounting, because the mining area is (ABC).A. determine the basis for oil and gas assetsThe basic B. provision of depletion of oil and gas assetsC. is the basis for impairment testingD. transfer of interests in mining areasFull marks: 45. operating costs mainly include (ABCDE).A. direct materials, direct fuels and direct laborB. production and management staff salariesC. downhole operation feeD. maintenance and repair costsE. gas purification feesFull marks: 46. the equity instruments that are equity settled share payments in the following are (AC).A. restricted stockB. simulated stockC. stock optionD. cash, stock appreciation rightsE. preferred stockFull marks: 47. at least the statutory content of the interim financial report shall include: (ABCE).A. balance sheetB. income statementC. cash flow statementD. owner's equity statementE. noteFull marks: 4The main factors to be considered when determining 8. regional divisions are (ABCDE).The similarity between the economic and political environment of A.B. relationship between operations in different regionsC. specific risks associated with the operation of a particular regionD. regulations on foreign exchange control and foreign exchange riskThe approximate size of the E. operationFull marks: 4Methods 9. depletion of oil and gas assets have (AB).A. yield methodB. year average methodC. line methodD. sum of year methodFull marks: 410. the information to be disclosed, regardless of which segment is the main form of reporting, is (ABCDE).A. segment revenueB. segment expensesC. segment profit or lossD. segment assetsE. segment liabilitiesFull marks: 4Three, the judgment question (altogether 5 test questions, altogether 20 points) V1. business segments are components within a business that are distinguishable and capable of providing individual items or a set of related products or services. The component assumes risks and rewards that are different from those of other components.A. errorB. correctB Full Score: 4 points2. interim financial statements may include monthly financial statements, quarterly financial statements, semi annual financial statements, and financial statements from the beginning of the year to the end of any medium term.A. errorB. correctB Full Score: 4 points3. the impairment losses of oil and gas assets shall not be reversed as soon as they are confirmed.A. errorB. correctB Full Score: 4 points4. the expenses for obtaining the rights and interests of the mining area shall be included in the profits and losses of the current period, and the expenses for purchasing the rights and interests of the mining area shall be capitalized and included in the value of the oil and gas assets.A. errorB. correctA Full Score: 4 points5. unused land does not belong to the land tenure that is held and ready for added value.A. errorB. correctB Full Score: 4 points。

高级财务会计网上形考作业3参考答案

点时购入1手指数合约,6月30日股指期货下降1%,7月1日该投资者在此指数水平下卖出股指合约平仓。

要求:做股指期货业务的核算。

参考答案:(1)6月29日开仓时,交纳保证金(4 365×100×8%)=34 920元,交纳手续费(4 365×100×0.0003)= 130.95元。

会计分录如下:借:衍生工具----股指期货合同34 920贷:银行存款34 920借:财务费用130.95贷:银行存款130.95(2)由于是多头,6月30日股指期货下降1%,该投资者发生亏损,需要按交易所要求补交保证金。

亏损额:4 365×1%×100=4 365元补交额:4 365×99%×100×8% -(34 920 - 4 365)=4 015.80借:公允价值变动损益 4 365贷:衍生工具----股指期货合同 4 365借:衍生工具----股指期货合同 4 015.80贷:银行存款 4 015.80在6月30日编制的资产负债表中,“衍生工具----股指期货合同”账户借方余额=34 920 – 4 365 + 4 015.8 =34 570.8元为作资产列示于资产负债表的“其他流动资产”项目中。

(3)7月1日平仓并交纳平仓手续费平仓金额= 4 365×99%×100 = 432 135手续费金额为=(4 365×99%×100×0.0003)=129.64。

借:银行存款432 135贷:衍生工具----股指期货合同432 135借:财务费用129.64贷:银行存款129.64(4)平仓损益结转借:投资收益 4 365贷:公允价值变动损益 4 3653.资料:A股份有限公司( 以下简称 A 公司)对外币业务采用交易发生日的即期汇率折算,按月计算汇兑损益。

2015年6月30日市场汇率为 1 美元=6.25 元人民币。

国家开放大学电大高级财务会计本形考任务三试题及答案三篇

国家开放大学电大高级财务会计本形考任务三试题及答案三篇国家开放大学电大《高级财务会计本》形考任务三试题及答案一篇一、单项选择问题。

1、新设并购是指并购是指两个或两个以上的企业共同成立一个新企业,用新企业的股份换取原各公司的股份。

通过合并()。

a、原企业失去法人资格,全部解散。

b、只有一家企业保留法人资格。

c、企业对市场有控制力。

d、企业减少了竞争风险。

2、合并会计报表主体为(-)a、由母公司b、母公司和子公司组成的企业集团。

c、由总公司d、总公司和分公司组成的企业集团。

3、国际会计准则委员会制台的有关会计报表的准则和我国有关会计报表的暂行规定所采用的合并理论为(上)a、股权理论b、经济实体理论c、子公司理论d、母公司理论。

4、通过扩大企业规模,扩大经营规模,增强竞争优势,降低管理成本和费用,扩大获得规模利益的行业专属管理资源,这种合并属于(前)。

a、混合和b、横向合并、c、纵向合并、控股合并。

5、以下各项中,()不属于企业合并购买法的特点。

a、购买企业在合并日资产负债表中以公允价值确定购买企业可以识别资产和负债。

b、购买企业将购买成本和获得的购买企业识别纯资产的公允价值差额作为营业权处理。

c、购买企业合并前的收益和剩馀收益不包括在合并后的主体报告中。

d、购买企业合并前的收益和剩馀收益纳入合并后主体的报告书。

6、购买企业购买的房屋、建筑物、机械设备等固定资产,如果可以继续使用,其公允价值应由(下)决定。

a、可变净值b、账面价值c、重置成本d、现行市场价格。

7、购买企业在确定所承担债务的公允价值时,一般应当按(签)确定。

a、可变净值b、账面价值c、重置成本d、现行市场价格。

8、第二期及以后各期连续编制会计报表时,编制基础为(.)。

a、前期制作的合并会计报告书。

b、前期编制合并会计报表的合并工作原稿。

c、企业集团母公司和子公司的个别会计报告。

d、企业集团母公司和子公司的账簿记录。

9、甲公司拥有乙公司60%的股份,丙公司30%的股份,乙公司拥有丙公司25%的股份,在这种情况下,甲公司在编制并购会计报表时,应将(a)纳入并购会计报表的并购范围。

高级财务会计三次作业题

《高级财务会计》作业一2009年12月经双方协商,甲股份公司以股权联合方式对同一控制下的乙企业进行控股合并,甲公司发行1000万股每股面值为1元,实际发行价为2元的普通股交换乙公司股东所持有的全部股份。

合并前甲、乙股企业资产负债表资料如下(单位:万元):2.作甲公司合并抵消分录3.作甲公司《合并资产负债表》工作底稿4.如果甲公司交换乙公司股东所持有的股份为90%,则请回答抵销分录会有什么变化《高级财务会计》作业二一、下面是集团企业公司内部销售和集团外部销售事项和交易示意图。

要求:1.作A、B、C和甲各自发生的经济业务会计分录。

2.A、B为全额销售,在C销售量为100%情况下。

分别作各种销售状况下母公司在编制合并报表时的抵消分录。

3.A、B为全额销售,在C销售量70%的情况下。

分别作各种销售状况下母公司在编制合并报表时的抵消分录。

二、甲企业和乙企业是不具有关联关系的两个独立的公司,即是非控制下的两家子公司。

2010年5月27日,这两个公司达成合并协议,由甲企业将乙企业合并。

2010年7月1日甲企业以公允价值为800万元、账面价值为1 200万元的无形资产作为对价对乙企业进行吸收合并,另用银行存款支付相关费用1万元。

购买日乙企业持有资产的情况如下(单位:万元):要求:1.计算甲企业购买成本和合并商誉价值2.作合并日甲企业会计分录3.如果甲企业的无形资产公允价值为1600万元,请回答会计处理有什么变化《高级财务会计》作业三一企业10月1日外币银行存款为28000美元,应收帐款为3000美元,汇率为8.45。

当月发生如下经济业务:(1).12日销售产品20000美元,汇率为8.30,产品已发出,货款尚未收到。

(2).16日银行通知收到上述销售货款16000美元,汇率为8.50。

(3).22日以30000美元外购材料,款已银行支付,材料已验收入库。

汇率8.40。

(4).28日以人民币兑换10000美元备购引进设备款,买入价8.55,卖出价8.6。

国家开放大学《高级财务会计》形考任务3参考答案

国家开放大学《高级财务会计》形考任务3参考答案答题要点:1)编制7 月份发生的外币业务的会计分录(1)借:银行存款($500000×6.24) ¥3120000贷:股本¥3120000 (2)借:在建工程¥2492000贷:应付账款($400000×6.23) ¥2492000 (3)借:应收账款($200000×6.22) ¥1244000贷:主营业务收入¥1244000 (4)借:应付账款($200000×6.21) ¥1242000贷:银行存款($200000×6.21) ¥1242000(5)借:银行存款($ 300000×6.20) ¥1860000贷:应收账款($300000×6.20) ¥18600002)分别计算7 月份发生的汇兑损益净额,并列出计算过程。

银行存款:外币账户余额= 100000 +500000-200000 +300000 =700000(美元)账面人民币余额=625000 +3120000-1242000 + 1860000 =4363000(元)汇兑损益金额=700000×6.2 - 4363000= -23000(元)应收账款:外币账户余额= 500000 +200000 -300000 =400000(美元)账面人民币余额=3125000+1244000-1860000 =2509000(元)汇兑损益金额=400000×6.2-2509000 = -29000(元)应付账款:外币账户余额=200000+400000-200000=400000(美元)账面人民币余额=1250000+2492000-1242000=2500000(元)汇兑损益金额=400000×6.2-2500000=-20000(元)汇兑损益净额=-23000-29000+20000=-32000(元)即计入财务费用的汇兑损益= - 32000(元)3)编制期末记录汇兑损益的会计分录借:应付账款20000财务费用32000贷:银行存款23000应收账款29000。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

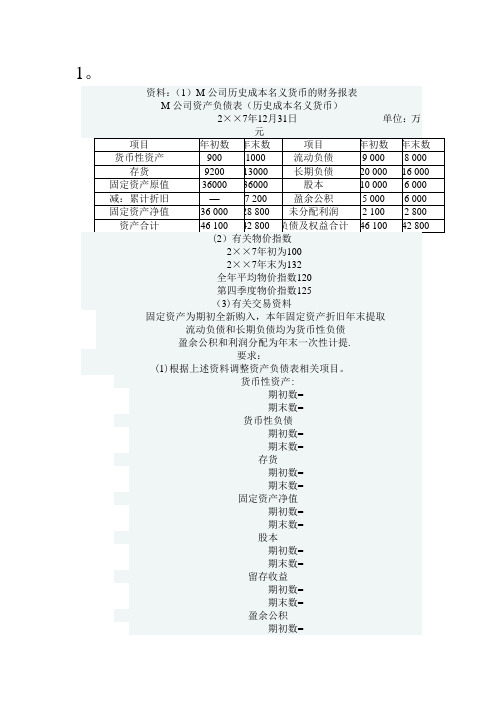

高级财务会计作业三

1.

资料:(1)M公司历史成本名义货币的财务报表

M公司资产负债表(历史成本名义货币) 2××7年12月31日 单位:万元项目年初数年末数项目年初数年末数

货币性资产9001000流动负债9 0008 000

存货920013000长期负债20 00016 000

3600036000股本10 000 6 000固定资产原

值

-7 200盈余公积 5 000 6 000减:累计折

旧

36 00028 800未分配利润 2 100 2 800

固定资产净

值

46 10042 800

资产合计46 10042 800负债及权益合

计

(2)有关物价指数

2××7年初为100

2××7年末为132

全年平均物价指数 120

第四季度物价指数125

(3)有关交易资料

固定资产为期初全新购入,本年固定资产折旧年末提取

流动负债和长期负债均为货币性负债

盈余公积和利润分配为年末一次性计提。

要求:

(1)根据上述资料调整资产负债表相关项目。

货币性资产:

期初数 = 900×(132÷100)=1188(万元)

期末数 = 1000×(132÷132)=1000(万元)

货币性负债

期初数 =(9000+20000)×(132÷100)=38280(万元)

期末数 = (800+16000)×(132÷132)=24000(万元)

存货

期初数 = 9200×(132÷100)=12144(万元)

期末数 = 13000×(132÷125)=13728(万元)

固定资产净值

期初数 =36000×(132÷100)=47520(万元)

期末数 = 28800×(132÷100)=38016(万元)

股本

期初数 =10000×(132÷100)=13200(万元)

期末数=10000×(132÷100)=13200(万元)

盈余公积

期初数 =5000×(132÷100)=6600(万元)

期末数 =6600+1000=7600(万元)

留存收益

期初数 =(1188+12144+47520)-38280-13200=9372(万元)

期末数 =(100+13728+38016)-24000-13200=15544(万元)

未分配利润

期初数 =2100×(132÷100)=2772(万元)

期末数 =15544-7600=7944(万元)

(2)根据调整后的报表项目重编资产负债表

M公司资产负债表(一般物价水平会计) 2××7年12月31日 单位:万元项目年初数年末数项目年初数年末数

货币性资产 11881000 流动负债 11880 8000

存货 1214413728 长期负债 26400 16000

47520 47520股本 13200 13200固定资产原

值

9504盈余公积 6600 7600减:累计折

旧

47520 38016未分配利润 2772 7944固定资产净

值

60852 52744资产合计 60852 52744负债及权益合

计。