09金融数学试题

09年9月CIIA真题卷二

试卷二:固定收益分析和估值衍生产品分析和估值组合管理试题ACIIA®试题最终考试 II – 2009年9月问题 1:固定收益分析与估值(46分) 作为固定收益分析师,你正面临如下市场环境:金融市场持续动荡,导致了大量信用连接产品定价混乱。

飞往高品质(flight to quality)的投资行为压低了政府债券收益率,而利差(信用)产品在经历评级下调和利差扩大后,损失惨重。

政府债券收益率和利差走势如下:▪当初发行时期限为3年、目前剩余期限为2年的政府债券到期收益率在去年下降了0.85%;▪当初发行时期限为3年、评级AA级的公司债券,目前剩余期限为2年,评级为A级,其相对于政府债券收益率的到期利差在去年扩大了2.75%。

a) 在这种背景下,你需要对一只剩余期限为2年、评级为A的公司债券(息票:4.0%;债券于一年前以面值发行,发行时评级为AA,利率计算惯例:30/360)进行绩效分析。

a1) 在不考虑利差扩大的情况下,仅基于政府债券收益率的变动,计算去年的持有期回报。

(5分)a2) 在只考虑信用利差扩大(忽略政府债券收益率变化)的情况下,计算去年公司债券的回报。

(5分)a3) 计算包括上述政府债券收益率变化和利差变动两者导致的总回报。

(5分)a4) 假设由于市场流动性不足,而不能卖出公司债券。

如果预期利差进一步扩大,你会推荐什么类型的对冲策略。

(仅进行定性评估,不需要计算)(5分)b)政府债券收益率曲线和利差曲线目前有如下特点(指到期收益率和到期利差,利率计算惯例:30/360)▪政府债券平价收益率曲线(年化到期收益率):1年2.15%,2年3.15%▪利差曲线(A级公司债券高于政府债券到期收益率的利差):1年1.5%,2年2.75%。

b1) 计算一年后政府债券的一年期远期利率。

(4分)b2) 计算一年后A级公司债券的一年期远期利率(提示:综合考虑上面给出的政府债券收益率曲线和利差曲线)。

金融数学基础理论题集

金融数学基础题集一、选择题1. 下列哪项是利息的本质?A. 货币的存储成本B. 借贷资本的增值额C. 银行的服务费用D. 投资的风险补偿答案:B2. 名义利率与实际利率的区别主要在于?A. 通货膨胀率B. 存款准备金率C. 贷款期限D. 利率浮动范围答案:A3. 在复利计算中,如果年利率为10%,本金为1000元,投资期限为2年,则两年后的终值是多少?(使用复利公式计算)A. 1100元B. 1210元C. 1200元D. 1020元答案:B4. 哪种计息方式使得利息收益在投资期限内更加均匀?A. 单利B. 复利C. 贴现率D. 浮动利率答案:B5. 当名义利率高于通货膨胀率时,实际利率为?A. 负值B. 零C. 正值D. 不确定答案:C6. 下列哪种情况会导致债券价格下跌?A. 市场利率下降B. 债券信用等级提升C. 预期通货膨胀率上升D. 债券到期期限缩短答案:C7. 年金是指在一定期限内,每隔相等时间(如每年、每季、每月等)收入或支出相等金额的款项。

以下哪项不属于年金?A. 养老保险金B. 房屋租金(每季度固定支付)C. 一次性奖金D. 每月房贷还款答案:C8. 假设年利率为5%,每季度复利一次,则年化有效利率是多少?(使用公式(1 + r/n)^n - 1计算,其中r为年利率,n为每年复利次数)A. 5.00%B. 5.13%C. 5.25%D. 5.38%答案:B9. 利率平价理论主要解释了什么?A. 汇率与利率之间的关系B. 股票价格与利率之间的关系C. 债券价格与通货膨胀率之间的关系D. 货币供应量与利率之间的关系答案:A10. 假设某债券的面值为1000元,息票率为6%,每年支付一次利息,到期期限为5年。

如果当前市场利率为5%,则该债券的市场价格(使用适当的方法估算)大致为?A. 小于1000元B. 等于1000元C. 大于1000元D. 无法确定答案:C11. 贴现函数在连续复利下与累计函数的关系是?A. 贴现函数是累计函数的倒数B. 贴现函数是累计函数的导数C. 贴现函数是累计函数的积分D. 两者无直接关系答案:A12. 如果贴现率增加,那么使用贴现函数计算得到的债券当前价格会?A. 增加B. 减少C. 不变D. 无法确定答案:B13. 在考虑信用风险时,贴现率应该如何调整?A. 保持不变B. 根据信用风险降低C. 根据信用风险增加D. 与信用风险无关答案:C14. 下列哪个选项正确地描述了贴现函数的应用场景?A. 预测股票价格B. 计算股票的内在价值C. 评估债券的当前市场价格D. 估算未来现金流的终值答案:C15. 若债券的票面利率高于市场贴现率,则该债券的当前市场价格将?A. 低于票面价值B. 等于票面价值C. 高于票面价值D. 无法确定答案:C16. 累计函数和贴现函数在金融数学中的主要用途是?A. 预测未来利率变动B. 管理市场风险C. 对金融产品进行定价D. 评估股票波动率答案:C17. 当计算一笔贷款在不同利率下的累计还款额时,通常使用的是?A. 贴现函数B. 累计函数C. 现值函数D. 收益率函数答案:B18. 在复利计算中,若名义年利率为12%,每年复利4次,则有效年利率约为?A. 12.00%B. 12.36%C. 12.55%D. 12.75%答案:C19. 有效率利率与名义利率之间的关系主要取决于?A. 初始投资金额B. 利息支付频率C. 贷款期限D. 利率类型(固定或浮动)答案:B20. 当名义年利率固定,但复利频率增加时,有效年利率会?A. 保持不变B. 减少C. 增加D. 先增后减答案:C21. 在连续复利计算中,有效年利率与名义年利率相等的情况发生在?A. 名义年利率为0%时B. 名义年利率为无穷大时C. 利息支付频率为无限大时D. 利息支付周期为无限短时答案:A(注意:这里A选项其实是一个特殊情况,通常连续复利下两者不等。

09年SOA北美精算师考试第二门FM官方样题第一部分(主要是金融数学)答案

09年SOA北美精算师考试第二门FM官方样题第一部分(主要是金融数学)答案SAMPLE SOLUTIONS FOR DERIVATIVES MARKETSQuestion #1Answer is DIf the call is at-the-money, the put option with the same cost will have a higher strike price.A purchased collar requires that the put have a lower strike price. (Page 76)Question #2Answer is C66.59 – 18.64 = 500 – K exp(–0.06) for K = 480 (Page 69)Question #3Answer is DThe accumulated cost of the hedge is (84.30-74.80)exp(.06) = 10.09.Let x be the market price.If x < 0.12 the put is in the money and the payoff is 10,000(0.12 – x) = 1,200 – 10,000x. The sale of the jalapenos has a payoff of 10,000x –1,000 for a profit of 1,200 –10,000x + 10,000x – 1,000 – 10.09 = 190.From 0.12 to 0.14 neither option has a payoff and the profit is 10,000x – 1,000 – 10.09 = 10,000x – 1,010.If x >0.14 the call is in the money and the payoff is –10,000(x – 0.14) = 1,400 – 10,000x. The profit is 1,400 – 10,000x + 10,000x – 1,000 – 10.09 = 390.The range is 190 to 390. (Pages 33-41)Question #4Answer is BThe present value of the forward prices is 10,000(3.89)/1.06 + 15,000(4.11)/1.0652 +20,000(4.16)/1.073 = 158,968. Any sequence of payments with that present value is acceptable. All but B have that value. (Page 248)Question #5Answer is EIf the index exceeds 1,025, you will receive x – 1,025. After buying the index for x you will have spent 1,025. If the index is below 1,025, you will pay 1,025 – x and after buying the index for x you will have spent 1,025. One way to get the cost is to note that the forward price is 1,000(1.05) = 1,050. You want to pay 25 less and so must spend 25/1.05 = 23.81 today. (Page 112) Question #6Answer is EIn general, an investor should be compensated for time and risk. A forward contract has no investment, so the extra 5 represents the risk premium. Those who buy the stock expect to earn both the risk premium and the time value of their purchase and thus the expected stock value is greater than 100 + 5 = 105. (Page 140)Question #7Answer is CAll four of answers A-D are methods of acquiring the stock. The prepaid forward has the payment at time 0 and the delivery at time T. (Pages 128-129)Question #8Answer is BOnly straddles use at-the-money options and buying is correct for this speculation. (Page 78)Question #9Answer is DThis is based on Exercise 3.18 on Page 89. To see that D does not produce the desired outcome, begin with the case where the stock price is S and is below 90. The payoff is S + 0 + (110 – S) –2(100 – S) = 2S – 90 which is not constant and so cannot produce the given diagram. On the other hand, for example, answer E hasa payoff of S + (90 – S) + 0 – 2(0) = 90. The cost is 100 + 0.24 +2.17 – 2(6.80) = 88.81. With interest it is 93.36. The profit is 90 –93.36 = –3.36 which matches the diagram.Question #10Answer is D[rationale-a] True, since forward contracts have no initial premium[rationale-b] True, both payoffs and profits of long forwards are opposite to short forwards.[rationale-c] True, to invest in the stock, one must borrow 100 at t=0, and then pay back 110 = 100*(1+.1) at t=1, which is like buying a forward at t=1 for 110. [rationale-d] False, repeating the calculation shown above in part c), but with 10% as a continuously compounded rate, the stock investor must now pay back100*e.1 = 110.52 at t=1; this is more expensive than buying a forward at t=1for 110.00.[rationale-e] True, the calculation would be the same as shown above in part c), but now the stock investor gets an additional dividend of 3.00 at t=.5, which theforward investor does not receive (due to not owning the stock until t=1). [This is based on Exercise 2-7 on p.54-55 ofMcDonald][McDonald, Chapter 2, p.21-28]Question #11Answer is CSolution: The 35-strike call has future cost (at t=1) of 9.12*(1+.08) = 9.85The 40-strike call has future cost (at t=1) of 6.22*(1+.08) = 6.72The 45-strike call has future cost (at t=1) of 4.08*(1+.08) = 4.41If S1<35, the profits of the 3 calls, respectively, are -9.85, -6.72, and -4.41.If 35<s1<="" -6.72,="" 3="" and="" are="" bdsfid="114" calls,="" of="" p="" profits="" respectively,="" s1-44.85,="" the=""></s1If 40<s1<="" 3="" and="" are="" bdsfid="116" calls,="" of="" p="" profits="" respectively,="" s1-44.85,="" s1-46.72,="" the=""></s1If S1>45, the profits of the 3 calls, respectively, are S1-44.85, S1-46.72, and S1-49.41.The cutoff points for when the relative profit ranking of the 3 calls change are:S1-44.85=-6.72, S1-44.85=-4.41, and S1-46.72=-4.41, yielding cutoffs of 38.13, 40.44, and 42.31.If S1<38.13, the 45-strike call has the highest profit, and the 35-strike call the lowest.If 38.13<s1<="" p="" profit,="" the=""></s1If 40.44<s1<="" p="" profit,="" the=""></s1If S1<42.31, the 35-strike call has the highest profit, and the 45-strike call the lowest.We are looking for the case where the 35-strike call has the highest profit, and the 40-strike call has the lowest profit, which occurs when S1 is between 40.44 and 42.31.[This is based on Exercise 2-13 on p.55-56 of McDonald][McDonald, Chapter 2, p.33-37]Question #12Answer is BSolution: The put premium has future value (at t=.5) of 74.20 * (1+(.04/2)) = 75.68 Then, the 6-month profit on a long put position is: max(1,000-S.5,0)-75.68. Correspondingly, the 6-month profit on a short put position is 75.68-max(1,000-S.5,0). These two profits are opposites (naturally, since long and short positions have opposite payoff and profit). Thus, they can only be equal if producing 0 profit. 0 profit is only obtained if 75.68 = max(1,000-S.5,0), or 1,000-S.5 = 75.68, or S.5 = 924.32. [McDonald, Chapter 2, p.39-42]Question #13Answer is DSolution: Buying a call, in conjunction with a short position in a stock index, is a form of insurance called a cap. Answers (A) and (B) are incorrect because they relate to a floor, which is the purchase of a put to insure against a long position in a stock index. Answer (E) is incorrect because it relates to writing a covered call, which is the sale of a call along with a long position in the stock index, so that the investor is selling rather than buying insurance. Note that a cap can also be thought of as ‘buying’ a covered call. Now, let’s calculate the profit: 2-year profit = payoff at time 2 – the future value of the initial cost to establish the position = (-75 + max(75-60,0)) –(-50 + 10)*(1+.03)2 = -75+15+40*(1.03)2 = 42.44-60 = -17.56. Thus,we’ve lost more from holding the short position in the index (since the index went up) than we’ve gained from owning the long call option.[McDonald, Chapter 3, p.59-65]Question #14Answer is ASolution: This consists of standard applications of the put-call parity equation on p.69. Let C be the price for the 40-strike call option. Then, C + 3.35 is the price for the 35-strike call option. Similarly, let P be the price for the 40-strike put option. Then, P –x is the price for the 35-strike put option, where x is what we’re trying to find. Using put-call parity, we have:(C + 3.35) + 35*e-.02 - 40 = P – x (this is for the 35-strike options)C + 40*e-.02 – 40 = P (this is for the 40-strike options)Subtracting the first equation from the second, 5*e-.02 – 3.35 = x = 1.55.[McDonald, Chapter 3, p.68-69]Answer is CSolution: The initial cost to establish this position is 5*2.78 –3*6.13 = -4.49. Thus, you are receiving 4.49 up front. This grows to 4.49*e .08*.25 = 4.58 after 3 months. Then, the following payoff/profit table can be constructed at T=.25 years: S T : 5*max(S T – 40, 0) – 3*max(S T – 35, 0) + 4.58 = Profit S T <35 0 - 0 + 4.58 = 4.58 35 <= S T <= 40 0 - 3*(S T – 35) + 4.58 = 109.58-3S T S T > 40 5*(S T -40) - 3*(S T – 35) + 4.58 = 2S T -90.42Thus, the maximum profit is unlimited (as S T increases beyond 40, so does the profit) Also, the maximum loss is 10.42(occurs at S T = 40, where profit = 109.58-120 = -10.42) [Notes] The above problem is an example of a ratio spread.[McDonald, Chapter 3, p.73]Question #16Answer is DSolution: The ‘straddle’ consists of buying a 40-strike call and buying a 40-strike put. This costs 2.78 + 1.99 = 4.77 at t=0, and grows to 4.77*e .02 = 4.87 at t=.25. The ‘strangle’ consists of buying a 35-strike put and a 45-strike call. This costs 0.44 + 0.97 = 1.41 at t=0, and grows to 1.41*e .02 = 1.44 at t=.25. For S T <40, the ‘straddle’ has a profit of 40-S T -4.87 = 35.13, and for S T >=40, the ‘straddle’ has a profit of S T -40-4.87 = 44.87. For S T <35, the ‘strangle’ has a profit of 35-S T -1.44 = 33.56, and for S T >45, the ‘strangle’ has a profit of S T -45-1.44 = 46.44. However, for 35<=S T <=45, the ‘strangle’ has a profit of -1.44 (since both options would not be exercised). Comparing the payoff structures between the ‘straddle’ and ‘strangle,’ we see that if S T <35 or if S T >45, the ‘straddle’ would outperform the ‘strangle’ (since 35.13 > 33.56,and since -44.87 > -46.44). However, if 35<=S T <=45, we can solve for the two cutoff points for S T , where the ‘strangle’ would outperform the ‘straddle’ as follows:-1.44 > 35.13 – S T, and -1.44 > S T - 44.87. The first inequality gives S T > 36.57, and the second inequality gives S T < 43.43. Thus, 36.57 < S T < 43.43.[McDonald, Chapter 3, p.78-80]Answer is B[rationale I] Yes, since Strategy I is a bear spread using calls, and bear spreads perform better when the prices of the underlying asset goes down.[rationale II] Yes, since Strategy II is also a bear spread – it just uses puts instead! [rationale III] No, since Strategy III is a box spread, which has no price risk; thus, the payoff is the same (1,000-950 = 50), no matter what the price of theunderlying asset.[Note]: An alternative, but much longer, solution is to develop payoff tables for all 3 strategies.[McDonald, Chapter 3, p.70-73]Question #18Answer is BSolution: First, let’s calculate the expected one-year profit without using the forward. This would be .2*(700+150-750) + .5(700+170-850) + .3*(700+190-950) = 20 + 10 - 18 = 12. Next, let’s calculate the expected one-year profit when buying the 1-year forward for 850. This would be 1*(700+170-850) = 20. Thus, the expected profit increases by 20 - 12 = 8 as a result of using the forward.[This is based on Exercise 4-7 on p.122 of McDonald][McDonald, Chapter 4, p.98-100]Question #19Answer is DSolution: There are 3 cases, one for each row in the above probability table.For all 3 cases, the future value of the put premium (at t=1) = 100*e.06 = 106.18.In Case 1, the 1-year profit would be: 750 - 800 - 106.18 + max(900-750,0) = -6.18In Case 2, the 1-year profit would be: 850 - 800 - 106.18 + max(900-850,0) = -6.18In Case 3, the 1-year profit would be: 950 - 800 - 106.18 +max(900-950,0) = 43.82 Thus, the expected 1-year profit = .7 * -6.18 + .3 * 43.82 = -4.326 + 13.146 = 8.82.[This is based on Exercise 4-3 on p.121 of McDonald][McDonald, Chapter 4, p.92-96]Answer is BSolution: This is an example of pricing a forward contract using discrete dividends. Thus, we need the future value of the current stock price minus the future value of each of the 12 dividends, where the valuation date is T=3. Thus, the valuation equation is: Forward price = 200*e.04(3) –[1.50*e.04(2.75) + 1.50*1.01*e.04(2.5) + 1.50*(1.01)2*e.04(2.25) + …1.50*(1.01)12] = 200*e.12 - 1.50*e.11{[1-(1.01*e-.01)12]/[1-(1.01*e.01)]}, using the geometric series formula from interest theory. This simplifies numerically to 225.50 -1.67442*11.99666 = 205.41.[This problem combines the material from interest theory and derivatives, although one could also simplify the above expression by brute force (instead of geometric series), since there are only 12 dividends to accumulate forward to T=3.] [McDonald, Chapter 5, p.133-134]Question #21Answer is ESolution: Here, the fair value of the forward contract is given by S0 * e(r-d)T =110 * e(.05-.02).5 = 110 * e.015 = 111.66. This is 0.34 less than the observed price. Thus, one could exploit this arbitrage opportunity by selling the observed forward at 112 and buying a synthetic forward at 111.66, making 112-111.66 = 0.34 profit.[This is based on Exercise 5-8 on p.163-164 of McDonald][McDonald, Chapter 5, p.135-138]Answer is BSolution: First, we must determine the present value of the forward contracts. On a per ton basis, this is: 1,600/1.05 + 1,700/(1.055)2 + 1,800/(1.06)3 = 4,562.49.Then, we must solve for the level swap price, which is labeled x below, as follows:4,562.49 = x/1.05 + x/(1.055)2 + x/(1.06)3 = x*[1/1.05 + 1/(1.055)2 + 1/(1.06)3] =2.69045*x.Thus, x = 4,562.49 / 2.69045 = 1,695.81.Thus, the amount he would receive each year is 50*1,695.81 = 84,790.38. [McDonald, Chapter 8, p.247-248]Question #23Answer is ESolution: First, note that the notional amount and the future 1-year LIBOR rates (not given) do not factor into the calculation of the swap’s fixed rate. All we need at the various zero-coupon bond prices P(0, t) for t=1,2,3,4,5, along with the 1-year implied forward rates, which are given by r0(t-1,t), for t=1,2,3,4,5. These calculations are shown in the following table:t 1 2 3 4 5P(0,t) (1.04)-1(1.045)-2 (1.0525)-3 (1.0625)-4 (1.075)-5=.96154 =.91573 =.85770 =.78466 =.69656 r0(t-1,t) s1[1.0452/1.04]-1 [1.05253/1.0452]-1 [1.06254/1.05253]-1 [1.0755/1.06254]-1 =.04000 =.05002 =.06766 =.09307 =.12649 Thus, the fixed swap rate = R = [(.96154)*(.04)+…+(.69656)*(.12649)] / [.96154 +…+.69656]= [.03846 + .04580 + .05803 + .07303 + .08811]/[.96154 + .91573 + .85770 + .78466 +.69656]= .30344 / 4.21619 = .07197 = 7.20% (approximately).[Note: This is much less calculation-intensive if you realize that the numerator (.30344) for R can also be obtained by taking 1- P(0,n) = 1 – P(0,5) = 1 - .69656 = .30344. Then, you would not need to calculate any of the implied forward rates!][McDonald, Chapter 8, p.255-258]Answer is D[rationale-a] True, hedging reduces the risk of loss, which is a primary function of derivatives.[rationale-b] True, derivatives can be used the hedge some risks that could result in bankruptcy.[rationale-c] True, derivatives can provide a lower-cost way to effect a financialtransaction.[rationale-d] False, derivatives are often used to avoid these types of restrictions. [rationale-e] True, an insurance contract can be thought of as a hedge against the risk of loss.[McDonald, Chapter 1, p.2-3]Question #25Answer is C[rationale-a] True, both types of individuals are involved in the risk-sharing process. [rationale-b] True, this is the primary reason reinsurance companies exist.[rationale-c] False, reinsurance companies share risk by issuing rather than investing in catastrophic bonds. In effect, they are ceding this excess risk to thebondholder.[rationale-d] True, it is diversifiable risk which is reduced or eliminated when risks are shared.[rationale-e] True, this is a fundamental idea underlying risk management andderivatives.[McDonald, Chapter 1, p.5-6]Question #26Answer is B[rationale-I] True, the forward seller has unlimited exposure if the underlying asset’s price increases.[rationale-II] True, the call issuer has unlimited exposure if the underlying asset’s price rises.[rationale-III] False, the maximum loss on selling a put is FV(put premium) – strike price. [McDonald, Chapter 2, p.43 (Table 2.4)]Answer is A[rationale-I] True, as prices go down, the value of holding a put option increases.canbe thought of as a put option.insuranceHomeowner’s[rationale-II] False, returns from equity-linked CDs are zero if prices decline, but positive if prices rise. Thus, owners of these CDs benefit from rising prices. [rationale-III] False, a synthetic forward consists of a long call and a short put, both of which benefit from rising prices (so the net position also benefits as such). [McDonald, Chapter 2, p.44-48]Question #28Answer is E[rationale-a] True, derivatives are used to shift income, thereby potentially lowering taxes.[rationale-b] True, as with taxes, the transfer of income lowers the probability ofbankruptcy.[rationale-c] True, hedging can safeguard reserves, and reduce the need for external financing, which has both explicit (e.g. – fees) and implicit (e.g. –reputational) costs.[rationale-d] True, when operating internationally, hedging can reduce exchange rate risk. [rationale-e] False, a firm that credibly hedges will reduce the riskiness of its cash flows, and will be able to increase debt capacity, which will lead to tax savings, since interest is deductible.[McDonald, Chapter 4, p.103-106]Question #29Answer is ASolution: If S0 is the price of the stock at time-0, then the following payments are required: Outright purchase – payment at time 0 – amount of payment = S0.Fully leveraged purchase – payment at time T – amount of payment = S0*e rT.Prepaid forward contract – payment at time 0 – amount of payment = S0*e-dT.Forward contract – payment at time T – amount of payment = S0*e(r-d)T.Since r>d>0, it must be true that S0*e-dT < S0 < S0*e(r-d)T < S0*e rT.Thus, the correct ranking is given by choice (A).[McDonald, Chapter 5, p.127-134]Answer is C[rationale-a] True, marking to market is done for futures, andcan lead to pricedifferences relative to forward contracts.[rationale-b] True, futures are more liquid; in fact, if you use the same broker to buy and sell, your position is effectively cancelled.[rationale-c] False, forwards are more customized, and futures are more standardized. [rationale-d] True, because of the daily settlement, credit risk is less with futures (v.forwards).[rationale-e] True, futures markets, like stock exchanges, do have daily price limits. [McDonald, Chapter 5, p.142]。

09金融数学试题

数学09,计算09金融数学试题(河海大学理学院13-01-15)姓名__________学号__________专业________成绩_______一.填空题(每空2分,36%)1.已知累积函数的形式为a(t)=at2+b,若0时刻投入100元累积到3时刻为172元则a=_________;b=_________;又设5时刻投入100元,则在10时刻的终值为________;2.已知600元投资两年产生利息264元(复利方式)则i=______;若2000元以同样的利率投资3年的终值为_________;3.如果δt=0.01t,则100元在第10年末的累计值=___________;4.已知基金A以单利10%累积则累积函数为a A(t)=_______;基金B以单贴现率5%累积则累积函数为a B(t)=_______;5. 在证劵交易中,卖出的一方称为_____头;而买入的一方称为____头;6.在年利率i=_______时,每月初支付100元的永久年金的现值为20644.22元。

7.已知i(4)=0.16,则的d(2)=_________;8.期货合同与远期合约的理论定价采用的是_________定价法;9.证劵的风险主要可分为________风险和_________风险;它们是以收益率的_____________来衡量;10.按期权买方的权利划分,期权可划分为_________期权和__________期权;二.计算题(52%)1某人以年实际利率5%借款100万元,并承诺分30次付清,后20次的付款是前10次的2倍,在第10年末,他可以选择一次性付清全部剩余款项X,,这会使借款人在10年间获得的年实际利率为5.5%,求X (8%)2一笔60万元的贷款,计划在今后的5年内按月偿还,如果年实际利率为5%,试计算每月初的付款金额。

(8%)3.一笔100万元的贷款,期限为6年,年实际利率为6%,每年末等额分期偿还,试计算下列各项:(1)每年末应该偿还的金额;(2)每年末的未偿还本金;(3)在每年偿还的金额中,利息和本金分别是多少?(要列表)(10%)4.某员工选择如下方式获得他的20年期退休金:从现在开始一个月后每月领取2000元月度退休金每年增加10%,每月复利一次的年名义利率为6%,计算该退休金的现值。

金融数学复习题

金融数学复习题第一篇:金融数学复习题金融数学复习题一、填空1.一股股票价值100元,一年以后,股票价格将变为130元或者90元。

假设相应的衍生产品的价值将为U=10元或D=0元。

即期的一年期无风险利率为5%。

则t=0时的衍生产品的价格_______________________________。

(利用博弈论方法)2.股票现在的价值为50元,一年后,它的价值可能是55元或40元,一年期利率为4%,则执行价为45元的看跌期权的价格为__________________。

(利用资产组合复制方法)3.对冲就是卖出________________,同时买进_______________。

4.Black-Scholes公式_________________________________________________。

5.我们准备卖出1000份某公司的股票期权,这里s0=50,X=40,r=0.05,σ=0.30,T=1.因此为了对我们卖出的1000份股票期权进行对冲,我们必须购买___________股此公,N(1.100)=0.8643)司的股票。

(参考N(1.060)=0.85546.股票衍生产品定价的三种方法:______________, ________________, ______________.7.Black-Scholes微分方程_________________________________________________。

二、计算题1.假设股票价格模型参数是:u=1.5,d=0.6,S0=110.一个欧式看涨期权到期时间t=3,执行价格X=115,利率r=0.05。

请用连锁法则方法求出在t=0时刻期权的价格。

2.假设股票价格模型参数是:u=1.2,d=0.8,S0=120.p=0.85一个美式看跌期权到期时间t=3,执行价格X=105,利率r=0.06。

请用连锁法则方法求出在t=0时刻期权的价格。

金融数学附答案

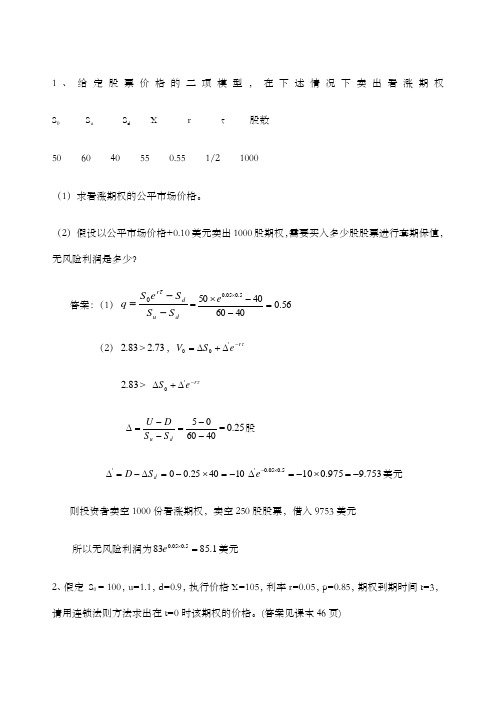

1、给定股票价格的二项模型,在下述情况下卖出看涨期权 S 0 S u S d X r τ 股数50 60 40 55 0.55 1/2 1000(1)求看涨期权的公平市场价格。

(2)假设以公平市场价格+0.10美元卖出1000股期权,需要买入多少股股票进行套期保值,无风险利润是多少?答案:(1)d u d r S S S e S q --=τ0=56.0406040505.005.0=--⨯⨯e (2)83.2>73.2,τr e S V -∆+∆='0083.2> τr e S -∆+∆'0406005--=--=∆d u S S D U =25.0股 104025.00'-=⨯-=∆-=∆d S D 753.9975.0105.005.0'-=⨯-=∆⨯-e 美元则投资者卖空1000份看涨期权,卖空250股股票,借入9753美元所以无风险利润为1.85835.005.0=⨯e 美元2、假定 S 0 = 100,u=1.1,d=0.9,执行价格X=105,利率r=0.05,p=0.85,期权到期时间t=3,请用连锁法则方法求出在t=0时该期权的价格。

(答案见课本46页)3、一只股票当前价格为30元,六个月期国债的年利率为3%,一投资者购买一份执行价格为35元的六个月后到期的美式看涨期权,假设六个月内股票不派发红利。

波动率σ为0.318.问题:(1)、他要支付多少的期权费?【参考N(0.506)=0.7123;N(0.731)=0.7673 】{提示:考虑判断在不派发红利情况下,利用美式看涨期权和欧式看涨期权的关系}解析:在不派发红利情况下,美式看涨期权等同于欧式看涨期权!所以利用B—S公式,就可轻易解出来这个题!同学们注意啦,N(d1)=N(-0.506),N(d2)=N(-0.731)。

给出最后结果为0.6084、若股票指数点位是702,其波动率估计值σ=0.4,指数期货合约将在3个月后到期,并在到期时用美元按期货价格计算,期货合约的价格是715美元。

09金融真题-32页word资料

2009 年金融学硕士研究生招生联考“金融学基础”试题一、单项选择题(每小题各有4 个备选答案,请选出最合适的1 个答案。

本题共30 小题,每小题1.5 分,共计45 分)1.边际替代率递减要求偏好满足()。

A.单调性B.凸性 C.完备性和传递性 D.单调性和凸性2.科斯定理是关于()A.不对称信息对市场效率的影响 B.公共决策的特性C.股票市场的无套利条件 D.产权界定和外部效应的关系3.已知某商品的需求函数和供给函数分别为:QD =14 −3P,QS = 2 + 6P,该商品的均衡价格是()。

A.4/3 B.4/5 C.2/5 D.5/24.某个国家在充分就业情况下的产出是5000 亿美元,而自然失业率是5%。

假定现在的失业率为8%,那么奥肯系数为2 时,根据奥肯法则,该国目前的产出()。

A.4500 亿美元 B.4900 亿美元 C.4800 亿美元 D.4700 亿美元5.下列关于需求函数说法错误的是()。

A.当需求函数为直线时,在不同价格下会有不同的弹性系数;B.当需求函数不为直线时,在不同价格下也必然有不同的弹性系数;C.一般来说,消费者的需求行为的调整时间越长,需求就越具有弹性;D.一种商品的用途越多,其需求价格弹性往往越大。

6.用来反映收入或财产分配平等程度的曲线和指标分别是()。

A.劳伦斯曲线和基尼系数 B. 劳伦斯曲线和恩格尔系数C.罗尔斯曲线和基尼系数 D. 罗尔斯曲线和恩格尔系数7.根据IS-BP-LM 模型,在浮动汇率且资本完全流动下()。

A.财政政策有效 B. 财政政策无效C.货币政策无效 D. 货币政策有效8.国内生产总值总值是指()。

A.生产要素收入+利润;B.NI+来自国外的净要素收入;C.NI+间接企业税+折旧;D.NI+间接企业税+折旧+来自国外的净要素收入。

9.根据哈罗德增长模型,若资本——产量比为5,储蓄率为20%,要使储备全部转化为投资,增长率应该为()。

大学金融数学试题及答案

大学金融数学试题及答案一、单项选择题(每题2分,共20分)1. 金融数学中,以下哪个概念是用来描述资产未来价值的?A. 现值B. 终值C. 贴现率D. 复利答案:B2. 在连续复利情况下,如果本金为P,利率为r,时间为t,那么资产的未来价值FV的计算公式是:A. FV = P(1 + r)^tB. FV = P(1 - r)^tC. FV = P * e^(rt)D. FV = P / e^(rt)答案:C3. 以下哪个不是金融衍生品?A. 期货B. 期权C. 股票D. 掉期答案:C4. 标准普尔500指数的计算方式是:A. 算术平均B. 加权平均C. 几何平均D. 调和平均答案:B5. 以下哪个不是金融市场的基本功能?A. 资金融通B. 风险管理C. 价格发现D. 产品制造答案:D6. 以下哪个不是金融市场的参与者?A. 银行B. 保险公司C. 政府机构D. 制造业公司答案:D7. 以下哪个不是金融市场的分类?A. 货币市场B. 资本市场C. 外汇市场D. 商品市场答案:D8. 以下哪个不是金融监管机构的职能?A. 制定和执行金融政策B. 维护金融市场稳定C. 促进金融创新D. 保护消费者权益答案:C9. 以下哪个不是金融风险管理的工具?A. 套期保值B. 风险转移C. 风险分散D. 风险接受答案:D10. 以下哪个不是金融数学中常用的数学工具?A. 概率论B. 统计学C. 微分方程D. 线性代数答案:D二、计算题(每题10分,共40分)1. 假设某投资者以10%的年利率投资10000元,投资期限为5年,请计算5年后的终值。

答案:终值为16105.10元。

2. 假设某投资者希望在10年后获得50000元,年利率为5%,请问现在需要投资多少本金?答案:现在需要投资32,143.68元。

3. 假设某公司发行了一张面值为1000元的债券,年利率为6%,期限为3年,每年支付利息,到期还本。

如果投资者在第二年购买了这张债券,购买价格为950元,请计算投资者的年收益率。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

数学09,计算09金融数学试题

(河海大学理学院13-01-15)

姓名__________学号__________专业________成绩_______

一.填空题(每空2分,36%)

1.已知累积函数的形式为a(t)=at2+b,若0时刻投入100元累积到3时刻

为172元则a=_________;b=_________;又设5时刻投入100元,则在

10时刻的终值为________;

2.已知600元投资两年产生利息264元(复利方式)则i=______;若2000

元以同样的利率投资3年的终值为_________;

3.如果δt=,则100元在第10年末的累计值=___________;

4.已知基金A以单利10%累积则累积函数为a A(t)=_______;

基金B以单贴现率5%累积则累积函数为a B(t)=_______;

5. 在证劵交易中,卖出的一方称为_____头;而买入的一方称为____头;

6.在年利率i=_______时,每月初支付100元的永久年金的现值

为元。

7.已知i(4)=,则的d(2)=_________;

8.期货合同与远期合约的理论定价采用的是_________定价法;

9.证劵的风险主要可分为________风险和_________风险;它们是以收益率的_____________来衡量;

10.按期权买方的权利划分,期权可划分为_________期权和__________期权; 二.计算题(52%)

1某人以年实际利率5%借款100万元,并承诺分30次付清,后

20次的付款是前10次的2倍,在第10年末,他可以选择一次性

付清全部剩余款项X,,这会使借款人在10年间获得的年实际利率

为%,求X (8%)

2一笔60万元的贷款,计划在今后的5年内按月偿还,如果

年实际利率为5%,试计算每月初的付款金额。

(8%)

3.一笔100万元的贷款,期限为6年,年实际利率为6%,每年末

等额分期偿还,试计算下列各项:

(1)每年末应该偿还的金额;

(2)每年末的未偿还本金;

(3)在每年偿还的金额中,利息和本金分别是多少(要列表)(10%)

4.某员工选择如下方式获得他的20年期退休金:从现在开始一个月

后每月领取2000元月度退休金每年增加10%,每月复利一次的年

名义利率为6%,计算该退休金的现值。

(8%)

5. 甲基金按6%的年利率增长,乙基金按8%的年利率增长,

在第20 年的年末两个基金之和为200000,在第10 年末

甲基金是乙基金的一半,求第5 年年末两基金之和。

(10%)

6. 某人留下遗产100000元,第一个10年将每年的利息

给收益人甲,底二个10年将每年的利息给受益人乙,20年

后将每年的利息付给收益人丙,并且一直进行下去,均为

年底支付,如果年利率为7%,试计算三个收益人的相对收益比例。

(8%)三.证明题(12%)

证明下列各式:

1 求证:|10||101011s a s v

∞+=- 2.|||)1()()(n n n a n Da Ia +=+。