中国汽车产业发展趋势2002年

中国汽车产业集中度的一些分析

中国汽车产业市场集中度的一些研究摘要:中国虽然已经是汽车产销大国,但是虽大却不强。

目前,中国汽车行业面临的问题颇多,其中市场集中度偏低的问题比较突出,而且研究表明,中国汽车行业市场集中度与发达国家相比差距甚大,严重影响了其自主创新能力。

采用行业集中度指标对中国汽车产业的市场集中度进行分析,并提出了提高中国汽车行业市场集中度的相关政策建议。

关键词:汽车产业;市场集中度;自主创新。

一、中国汽车产业的现状中国汽车工业发展的历史,是从1956年开始的。

1955~1957年的三年间只有一汽;20世纪70年代开始,中国出现了大量的自主品牌企业。

20世纪80年代开始,中央政府开始鼓励民族汽车厂商和国外接触,中国的汽车业缓缓对外开启大门,利用外资发展中国的汽车工业成为一种新的趋势。

1984年1月,中国汽车的第一个中外合资企业——北京吉普诞生。

国家在缜密研究了中国未来轿车工业的发展道路之后,确定了“三大三小两微”的总体格局,轿车工业开始向规模化方向发展。

20世纪90年代以来,中国汽车行业实现了突破。

1992年,中国汽车的总产量以完美的成绩突破了百万辆大关。

从2002年开始,中国汽车行业进入飞速发展的高峰时期,中国汽车业三大集团掀起了与国内外产业资本的兼并合作的浪潮。

在2009的上半年,中国汽车的市场销售量,已经超过以往,一跃而上,超越美国与其他国家成为世界第一。

我们可以看出,汽车产业作为国民经济支柱产业的地位越来越突出,影响力也与日俱增。

同时调查显示,中国汽车产业与国外相比较,总体规模是很大的,但是,单一企业的规模却相对很小,所以排在前面的几家厂商的市场占有率就比较低,表现在市场集中度比较低[1]。

同时中国的零部件行业,百强企业的市场份额仅占整个行业的50%,远低于美国、日本的汽车行业市场集中度。

可以看出,尽管中国汽车产业在发展中形成的多、小、散、乱等现象有所改观,中美两国汽车行业的集中度差异仍然非常巨大。

二、汽车产业市场集中度的测度贝恩(J.Bain)在1959年系统地论述了产业组织理论的基本框架,提出了现代产业组织理论的三个基本范畴:市场结构、市场行为和市场绩效。

环境分析及发展趋势预测

汽车行业现状国内方面,自2002年之后,中国汽车行业开始进入爆发式增长阶段,特别是随着私人消费的兴起,轿车需求量开始迅速攀升,并成为推动中国汽车发展的一股重要力量。

与此同时,中国在全球汽车产业中的地位也逐渐上升。

2007年,中国汽车需求总量为879万辆,在全球市场占比从2001年4.3%上升到2007年的12.2%。

2009年,中国国内市场销售了1360万辆汽车,而此前世界最大的汽车市场——美国仅销售1034万辆。

中国已成为世界上最大的轿车和面包车市场。

目前我国汽车市场自主品牌发展态势良好。

2010年前10个月,自主品牌乘用车共销售503.81万辆,占乘用车销售总量的45.39%,同比增长1.18个百分点。

受经济危机影响,我国经济发展速度放缓,为了保增长、扩内需、调结构,我国开始实施扩大内需政策、产业调整和振兴规划,促进汽车消费及汽车产业组织结构优化升级,刺激了国内汽车市场的快速复苏并呈现出较快的发展势头。

未来我国汽车行业发展前景看好。

从2004年至今,国内轿车市场不同国别汽车产品市场占有率发生了一定程度的变化。

自主品牌市场占有率从2004年的两成左右,发展到2009年自主品牌攫取近45%的市场,赶超日系车,坐拥最大市场份额,德系车位列第三。

德系车市场份额缩减趋势初现;韩系车则在2008年、2009年两年其他车系市场减弱时迅速抢占国内市场。

国际方面,在跨入21世纪的第二个十年之时,世界汽车格局正发生着深刻的变化,一方面,原有汽车集团竞争更加激烈,中国汽车也更多的参与到世界范围竞争的行列;同时,消费者高品质生活要求下的汽车安全、环保、健康成为发展趋势。

当前世界汽车格局长期被大企业集团控制,也就是业内所说的“6+3”格局,“6”即通用、福特、戴姆勒、丰田、大众、日产-雷诺联盟,“3”即宝马、本田和PSA。

根据其区域可简单划分为三大派系:以通用、福特、克莱斯勒为代表的美国派系,以丰田、本田、日产为骨干的日本派系,以及包括戴姆勒、大众、雷诺、宝马等在内的欧洲派系。

我国汽车行业发展现状及前景

我国汽车行业发展现状及前景探析摘要:本文通过我国汽车行业的现状分析,探讨汽车行业的发展趋势前景,由汽车制造向汽车服务发展。

关键词:汽车行业;现状分析;发展前景一、我国汽车行业的现状我国汽车行业从2002年开始进入快速增长期,轿车开始走近人们的日常生活,需求量的迅速加大,推动我国汽车行业不断发展。

随着汽车行业的飞速发展,我国汽车销售市场日益扩大,到2009年,我国汽车产量远远超过日本、美国,成为全球最大的市场,进而取代了美国的长期统治地位,在这一年里,我国汽车产量达到了1300多万辆,同比增长了48.3%,汽车销量也超过了1300多万辆,同比增长了46.2%。

2010年,我国汽车工业保持稳定的发展势头,我国出台了一系列的政策,以促进汽车行业的发展,如需求扩大,结构调整,促进转变等措施和政策,汽车行业的结构得到调整,大大推动了我国自主品牌汽车大的发展,在汽车的生产和销售市场中,自主品牌站的比例大幅度提升,这一年中,我国汽车生产了1826.47万辆,同比增长了32.4%,销售汽车1806.19万辆,同比增长了32.4%。

2011年,我国汽车产量为1841.9万辆,同比增长了0.8%,同比增长率比2010年下降了31.6个百分点,汽车销量为1850.5万辆,同比增长了2.5%,同比增长率比2010年下降了29.9个百分点。

我国汽车行业虽然从这一年开始进入理性发展阶段,整体出现市场淡化,但是仍然保持着全球汽车行业的产销首位。

2012年,我国汽车的产量和销量均超过了1900万辆,增长速度超过了4%,仍然稳定全球第一。

我国汽车行业已经成为世界汽车行业的重要组成部分,随着我国汽车行业的飞速发展,我国汽车自主品牌的产量和销量日益提高,在世界汽车中所占的份额越来越大,正在由制造国向创造国稳步跨越,在未来的汽车行业中,我国将继续保持产销大国位置,但是在这个发展过程中,也随之出现了一些问题亟待解决,最主要的就是汽车行业的经济效益不增反退。

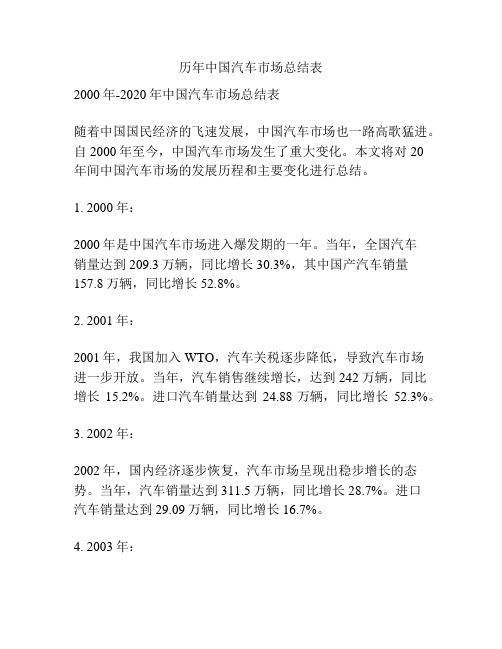

历年中国汽车市场总结表

历年中国汽车市场总结表2000年-2020年中国汽车市场总结表随着中国国民经济的飞速发展,中国汽车市场也一路高歌猛进。

自2000年至今,中国汽车市场发生了重大变化。

本文将对20年间中国汽车市场的发展历程和主要变化进行总结。

1. 2000年:2000年是中国汽车市场进入爆发期的一年。

当年,全国汽车销量达到209.3万辆,同比增长30.3%,其中国产汽车销量157.8万辆,同比增长52.8%。

2. 2001年:2001年,我国加入WTO,汽车关税逐步降低,导致汽车市场进一步开放。

当年,汽车销售继续增长,达到242万辆,同比增长15.2%。

进口汽车销量达到24.88万辆,同比增长52.3%。

3. 2002年:2002年,国内经济逐步恢复,汽车市场呈现出稳步增长的态势。

当年,汽车销量达到311.5万辆,同比增长28.7%。

进口汽车销量达到29.09万辆,同比增长16.7%。

4. 2003年:2003年,SARS疫情席卷全国,汽车市场受到一定程度的影响。

当年,汽车销量达到379.2万辆,同比增长21.7%。

进口汽车销量达到33.43万辆,同比增长14.9%。

5. 2004年:2004年,国内汽车市场进一步放开,给予外资企业更多发展机会。

当年,汽车销量达到573.2万辆,同比增长51.2%。

进口汽车销量达到42.82万辆,同比增长28.3%。

6. 2005年:2005年,汽车市场继续高速增长,但较2004年有所降温。

当年,汽车销量达到580.5万辆,同比增长1.3%。

进口汽车销量也出现小幅下降,为40.49万辆,同比下降5.6%。

7. 2006年:2006年,国内政策环境逐渐趋向成熟,汽车市场进入成熟期。

当年,汽车销量达到766.8万辆,同比增长32.0%。

进口汽车销量达到61.99万辆,同比增长53.5%。

8. 2007年:2007年,全球金融危机爆发,给我国汽车市场带来严峻挑战。

当年,汽车销售额为792.5万辆,同比增长3.2%。

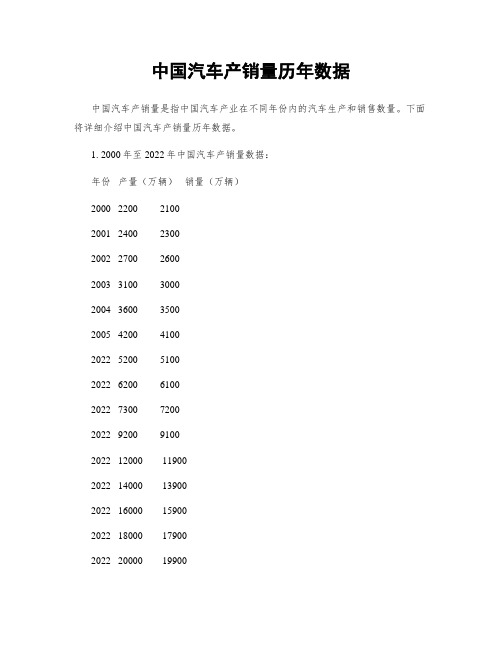

中国汽车产销量历年数据

中国汽车产销量历年数据中国汽车产销量是指中国汽车产业在不同年份内的汽车生产和销售数量。

下面将详细介绍中国汽车产销量历年数据。

1. 2000年至2022年中国汽车产销量数据:年份产量(万辆)销量(万辆)2000 2200 21002001 2400 23002002 2700 26002003 3100 30002004 3600 35002005 4200 41002022 5200 51002022 6200 61002022 7300 72002022 9200 91002022 12000 119002022 14000 139002022 16000 159002022 18000 179002022 20000 199002022 23000 229002022 25000 249002022 28000 279002022 31000 309002022 33000 329002022 35000 349002. 中国汽车产销量历年趋势分析:从上述数据可以看出,中国汽车产销量在2000年至2022年期间呈现了持续增长的趋势。

特殊是自2022年以后,中国汽车产销量增速明显加快,年均增长率超过10%。

这主要得益于中国经济的快速发展和人民生活水平的提高,促使了汽车需求的持续增长。

3. 中国汽车产销量历年数据分析:3.1 产量与销量对照分析:从数据可以看出,中国汽车产量与销量基本保持一致,差距较小。

这表明中国汽车市场的供需状况相对平衡,汽车生产能够满足市场需求。

3.2 年度产销量变化分析:- 2000年至2022年,中国汽车产销量呈现较为平稳的增长态势,年均增长率约为7%摆布。

- 2022年至2022年,中国汽车产销量增速明显加快,年均增长率超过15%。

这一时期,中国政府实施了一系列汽车消费刺激政策,如提供购车补贴和减税优惠等,促使汽车销量大幅增长。

- 2022年至2022年,中国汽车产销量增速有所放缓,年均增长率约为5%摆布。

中国汽车产销量历年数据

中国汽车产销量历年数据中国汽车产销量是指中国汽车工业生产的汽车数量和销售的汽车数量。

这一数据可以反映中国汽车行业的发展情况和市场需求。

下面是中国汽车产销量历年数据的详细介绍:1. 2000年至2022年的中国汽车产销量数据:- 2000年:中国汽车产量约为100万辆,销量约为90万辆。

- 2001年:中国汽车产量约为120万辆,销量约为110万辆。

- 2002年:中国汽车产量约为150万辆,销量约为140万辆。

- 2003年:中国汽车产量约为180万辆,销量约为170万辆。

- 2004年:中国汽车产量约为220万辆,销量约为210万辆。

- 2005年:中国汽车产量约为260万辆,销量约为250万辆。

- 2022年:中国汽车产量约为320万辆,销量约为310万辆。

- 2022年:中国汽车产量约为370万辆,销量约为360万辆。

- 2022年:中国汽车产量约为440万辆,销量约为430万辆。

- 2022年:中国汽车产量约为500万辆,销量约为490万辆。

- 2022年:中国汽车产量约为580万辆,销量约为570万辆。

2. 2022年至2022年的中国汽车产销量数据:- 2022年:中国汽车产量约为660万辆,销量约为650万辆。

- 2022年:中国汽车产量约为770万辆,销量约为760万辆。

- 2022年:中国汽车产量约为810万辆,销量约为800万辆。

- 2022年:中国汽车产量约为870万辆,销量约为860万辆。

- 2022年:中国汽车产量约为900万辆,销量约为890万辆。

- 2022年:中国汽车产量约为950万辆,销量约为940万辆。

- 2022年:中国汽车产量约为980万辆,销量约为970万辆。

- 2022年:中国汽车产量约为990万辆,销量约为980万辆。

- 2022年:中国汽车产量约为980万辆,销量约为970万辆。

- 2022年:中国汽车产量约为1020万辆,销量约为1010万辆。

3. 产销量增长趋势分析:- 从2000年至2022年的20年间,中国汽车产销量呈现出持续增长的趋势。

中国汽车工业发展历史

汽车工业50年发展与回顾1953年7月15日第一汽车制造厂(今中国第一汽车集团公司,以下称一汽)在长春动工兴建,开中国汽车工业之先河。

2003年7月15日恰逢中国汽车工业建设50周年,回顾50年的发展历程,顺遂与曲折并存,急起和徘徊同在,汽车工业在不断学习、创新中前进、成长。

一、汽车产品发展我国的汽车产品发展大体可分两个大阶段。

(一)前30年(1953~1982年)这30年是汽车产品以载货汽车且以中型(载质量4~5t)载货汽车为主的年代。

(二)后20年(1983~2002年)以1982年5月中国汽车工业公司成立为契机,提出汽车产品结构改革方针,包括:实施老产品换型;调整产品结构,改变“缺重少轻”,轿车几乎空白的历史;加大客车、农用车、专用车、柴油车的生产比例;发展系列化多品种生产,结束单一品种生产的历史。

1 1983~1992年1983~1992年,我国汽车产量从20万辆增长到100万辆(106.2万辆),汽车老产品实现全面换型,引进了一大批商用车新产品,增加了微型客货车品种,轿车工业已经起步,明显改变了汽车产品结构,为以后汽车产品结构的更大改变奠定了良好基础。

这一时期开发引进的产品已步入系列化、多品种的轨道。

3)发展微型商用车1980年,国内开始试制日本产品技术的微型商用车,先从微型载货车入手,后逐步扩大到微型厢式载货车,再到厢式客车,经引进技术及建设,陆续投产的品牌有:①吉林牌:吉林汽车工业总公司采用日本铃木技术,1983年投产。

②五菱牌:柳州微型汽车厂(今上汽通用五菱汽车股份有限公司,以下称柳微、五菱)采用日本三菱技术,1984年投产。

③松花江牌:哈尔滨飞机制造厂(今哈飞汽车股份有限公司,以下称哈飞)引进日本铃木技术,1984年投产。

④长安牌:长安机器制造厂(今长安汽车(集团)有限责任公司,以下称长安)引进日本铃木技术,1985年投产。

⑤昌河牌:昌河飞机制造厂(昌河飞机工业(集团)有限责任公司,以下称昌河)引进日本铃木技术,1985年投产。

民营汽车工业发展史

民营汽车工业发展史一、前言民营汽车工业是指由私人或私营企业经营的汽车制造和销售行业。

这个行业在中国的发展历史可以追溯到上世纪80年代,当时的国有企业主导了整个汽车市场。

随着改革开放的深入,中国的民营经济逐渐壮大,民营汽车工业也开始蓬勃发展。

二、80年代至90年代初期:起步阶段1984年,广州本田汽车有限公司成立,成为中国第一家外资合资企业。

此后,一批外资合资企业相继进入中国市场,包括通用、福特、大众等知名品牌。

这些外资企业在技术、管理等方面带来了先进经验和理念,并推动了中国汽车工业的发展。

同时,在国内,一些私人企业也开始尝试涉足汽车制造领域。

1988年,浙江吉利控股集团有限公司成立,并开始生产小型轿车。

此后不久,江淮、奇瑞等一批民营企业也开始尝试自主研发和生产汽车。

然而,在起步阶段,由于技术水平和管理经验相对不足,民营汽车企业面临着许多困难和挑战。

产品质量、技术水平等方面存在较大差距,市场占有率也较低。

三、90年代中期至2000年代初期:快速发展阶段1994年,中国国家经济贸易委员会发布《汽车工业调整方案》,明确提出了“鼓励发展非国有经济参与汽车制造和销售”的政策。

此后,民营汽车企业得到了更多的政策支持和市场机会。

在这一时期,民营汽车企业开始加强技术研发、提高产品质量,并逐渐树立了自己的品牌形象。

例如,吉利控股集团推出了“海豚”等自主品牌,并在国内市场上取得了不错的成绩。

同时,由于外资合资企业的技术转移和管理经验的积累,中国汽车工业整体水平也有了较大提升。

2002年,中国成为全球最大的汽车生产和销售国家之一。

四、2000年代中期至今:多元化发展阶段进入21世纪以来,中国民营汽车工业进入了一个多元化发展的阶段。

一方面,民营汽车企业继续加强技术研发和品牌建设,推出了更多自主品牌,并在国内市场上不断拓展业务。

例如,奇瑞、比亚迪等企业推出了多款自主品牌汽车,并在海外市场上取得了不俗的成绩。

另一方面,民营汽车企业也开始涉足新能源汽车领域,积极响应国家的环保政策。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

中国汽车产业发展趋势一、(全球角度)汽车产业全球化的趋势及汽车需求增长的国际格局汽车产业的全球化集中体现在特征上:一是汽车产业链,包括投资、生产、采购、销售及售后服务、研发等主要环节的日益全球性配置。

例如,过去跨国公司在本国建立、保持研发机构,对于目标国市场采取复制产品的方式进行投资,而现在则采取将各个功能活动和能力分配给全球市场的方式。

由此导致了新的专业化分工协作模式的出现,特别是整车装配与零部件企业之间呈现分离趋势,零部件的跨国公司越来越多,零部件企业与整车装配企业之间以合同为纽带的网络型组织结构日趋明显。

整车制造企业零部件的全球采购以及零部件工业的国际化,模糊了汽车产品的“国家特征”,使其成为了典型的全球化产品。

二是巨型汽车企业之间的大规模重组,形成了“6+3”的格局,9大汽车集团的产量已占世界汽车产量80%以上。

汽车企业在全球的大规模重组实质性地改变了传统的资源配置方式、产业竞争模式和产业组织结构,并使各国特别是发展中国家以往的汽车产业发展战略和相关政策面临严峻挑战。

从汽车产销量的地理分布看,欧美发达国家,普遍出现了严重的市场疲软,而发展中国家,特别是亚洲国家的形势看好。

在亚洲,韩国、泰国和中国等以其良好的成长性和巨大的潜力,继续成为世界汽车市场的亮点。

据预测,从2002年到2010年,全球汽车产量将增加1100万辆,亚太地区将新增7百万辆以上,占到65%,而其中将有一半来自中国。

二、近年来中国汽车产业规模和市场结构变化中国汽车工业经过40多年的发展,已经成为国民经济的重要产业。

随着经济发展水平的不断提高和轿车开始进入家庭,中国已经成为世界上增长最为迅速的市场,对全球汽车产业产生的巨大影响力。

2002年全年累计生产汽车325辆,比2001年同期增长38.49%,销售汽车324.8万辆,比2001年同期增涨37.1%,完成工业增加值1515亿元,同比增长60.94%。

汽车消费成为拉动2002年经济增长的主要力量。

具有法人地位的汽车生产厂有120余家。

2002年一汽、东风、上汽等3大汽车集团生产集中度为57%,比2001年提高了8个百分点;中国轿车由于企业进入和竞争激烈,销量前3位的上海大众、一汽大众和上海通用占总销量的53.4%,比2001年前3名的市场份额下降了6.8个百分点;其他各类汽车的生产集中度总体来讲较之2001年也有一定程度的下降。

就单个企业规模而言,中国汽车工业的前4名一汽、东风、上汽、长安等4大集团汽车生产能力在30万--60万辆之间,规模经济效益开始显现。

尽管如此,与世界级的汽车生产企业相比较,中国汽车工业企业的规模仍然偏小。

市场激烈竞争带来的直接影响,一是促使汽车价格持续下降,最终达到合理价位;二是竞争领域不断扩展,不仅包括产品价格、质量、性能,而且涉及市场营销、售后服务、市场应变能力等各个方面;三是技术进步、产品研发将成为竞争焦点。

通过充分而有效的竞争推进企业优胜劣汰,势不可挡,并将成为推动整个产业健康发展的主导力量。

三、中国汽车工业市场空间、投资机会与盈利前景预测未来时期随着影响中国汽车需求市场的价格、居民收入和消费结构、汽车信贷、消费环境的改善,特别是跨国公司主导下的汽车合资企业不断在全球同步推出适应市场需求的新产品,将对未来市场起到巨大的推动作用。

预计今后10年—15年中国将成长成为全球最大汽车市场,年销量达到1700万辆,汽车保有量超过1亿辆。

近年来,跨国公司加快了进军中国市场的步伐,推动了国内汽车业新一轮的兼并重组热潮。

预计今后跨国公司在中国的角逐将更加激烈,国内几大汽车集团依托跨国公司迅速扩张,将进一步加速各类整车和零部件生产企业,特别是中小企业的兼并重组,市场格局剧烈变化,投资并购机会将不断涌现。

目前,我国汽车行业的整体利润率高于国际水平,随着产品价格的下降,这极可能降低行业利润率,但在价格下降的同时,成本、费用也有较大下降空间,利润总额等总量指标可能保持,甚至有可能提高。

国家进一步降低一些税费,将为行业内大部分企业提供降价空间,如果产销规模能随降价得到有效扩大,规模效应将发挥出来,会使行业效益保持在较好水平。

同时,零部件进口关税的下降,将使一些厂家进口成本有所下降,对采用进口部件较多的中高档产品影响更加明显。

我国汽车行业中的轿车工业发展最为迅速,不仅产量的增长高于整个汽车行业产品产量的增长,技术进步的步伐也大大加快。

从全行业来看,轿车、汽车零部件及配件企业的盈利能力处于行业领先水平,具有更高的投资回报率。

四、中国汽车产业的发展趋势和产业政策取向1.中国汽车产业的发展趋势(1)预计今后10到15年中国将成为世界最大的汽车消费国。

国际经验表明,人均收入水平与汽车普及率存在显著的相关关系。

中国2002年的人均GDP是7972元,按官方汇率计算折合910多美元,而按世界银行测算的购买力平价方法则接近4000美元。

在一些发达城市、东南沿海相当多的地区,人均GDP按官方汇率计算也达到四五千美元,呈现明显的即将进入汽车社会的特征。

预计中国将在未来10年--15年成长成为年销量达到1700万辆的全球最大汽车市场。

(2)汽车的生产和消费将在未来相当长时期成为拉动中国经济增长的重要力量。

汽车产业是波及范围最广和波及效果最大的产业。

对钢铁、有色金属、橡胶、塑料、玻璃、涂料等原材料工业,铸、锻、热、焊、冲压、机加工、油漆、电镀、试验、检测等设备制造业,机械、电子、电器、化工、建材、轻工、纺织等配套产品和零部件,公路建设、能源工业、交通运输业和服务业等,都会产生巨大需求,从而推动这些产业的发展。

预计今后10年每年GDP增量,有1/7至1/6由汽车产业提供。

(3)中国有望成为世界汽车的制造中心。

中国已初步形成相对齐全的汽车工业生产体系。

这是中国汽车产业新发展的起点。

此外,中国发展汽车产业还有如下优势:一是大国的市场优势;二是劳动力成本优势;三是具有较强的制造业配套能力。

预计在今后10到15年,中国有望成为世界重要的汽车制造基地之一。

2.中国今后发展汽车产业的政策取向(1)创造积极而充分的、有利于提高汽车产业国际竞争力的国内竞争环境。

应鼓励各种类型企业特别是民营企业的进入,积极吸引外商直接投资特别是跨国公司直接投资,给予不同性质的企业以平等的市场竞争机会,通过优胜劣汰的市场竞争过程,形成强有力的市场竞争结构,带动我国汽车产业和企业国际竞争力的根本提高。

(2)改制、重组是新时期我国汽车产业组织的基本政策取向。

在开放、竞争的基础上,推动中国汽车企业的改制与重组。

在改制过程中,要采取多种方式解决普遍存在的企业办社会、人员过多、债务负担重、社会保障体系不健全等历史遗留问题,推进企业产权的多元化,建立有效的公司治理机制。

企业重组可以在以下方面重点推进:一是整合汽车资源,以增量盘活存量,提高汽车工业资产利用率;二是进一步加强与汽车跨国公司的多方面合作;三是推动国有企业与非国有企业之间的合作;四是对不同类型的汽车产品采取不同的重组战略;五是在强调放松进入限制的同时,要大力排除退出障碍;六是积极利用资本市场推动产业重组。

(3)有所为、有所不为。

在开放中逐步融入全球汽车制造分工体系。

改变汽车产业链配置主要依赖国内市场和国内资源的思路,分阶段地逐步融入汽车产业的全球采购、制造、销售、研发体系,并逐步向高段领域挺进。

在整车上有进有出,集中力量发展具有市场和资源优势的部分产品;要充分利用中国市场的多层次性以生产中低级别的轿车作为未来时期汽车产业的战略重点,逐步实现规模优势和成本优势,在满足国内市场的同时占领周边发展中国家;同时要利用现有的劳动力优势,扶植国内有条件的零部件厂商要尽快向全球供应商的角色转变。

China's auto industry development trendA, automobile industry globalization trend and automobile demand growth international patternAuto industry globalization embodied in characteristics: one is the auto industry chain, including investment, production, procurement, sales and after-sales service, research and development and other main link increasingly global configuration. For example, the multinational companies in their establishment, keep r&d institution, to the target market take copy product approach to investing, and now are taking will each functional activities and ability to global market distribution way. This has led to new specialization, especially the emergence of cooperative mode between enterprises with parts of vehicle assembly, parts of separation trend appears more and more multinational enterprise and vehicle assembly components in the contract as a link between enterprises of network organizational structure has become increasingly evident. The vehicle manufacturing enterprise parts of the global sourcing and the internationalization of spare parts industry, which blurs automotive products "national characteristics," has to typical globalization products. Two giant car between enterprise's large-scale restructuring, and formed a "6 + 3" pattern, 9 automobile group automobile production of world output has more than 80%. Car companies in the world of large-scale restructuring substantially changed the traditional resource allocation methods, industrial competitive mode and industrial organization structure, and allows countries, especially developing countries before the auto industry development strategy and relevantpolicy is facing serious challenges.The geographical distribution of car output from view, euramerican developed country, generally there was a serious weakness in the market and developing countries, especially the situation in Asia countries. In Asia, South Korea, Thailand and China with its good growth and the huge potential, continue to be the highlight of the world automobile market. According to the forecast, from 2002 to 2010, global auto output will increase 11 million vehicles, the region will add more than 7 million cars, or 65 percent, and which will have half from China.Second, in recent years China's automobile industry scale and market structure changesChina's auto industry after 40 years of development, has become an important industry of the national economy. With the development of economic levels rising and cars began to move into homes, China has become the world's most rapidly growing market, global car industry produce to the great influence. Annual accumulative total production car in 2002 than in 2001 vehicles, 325 38.49% growth from selling auto 324.8 million vehicles, than the same period in 2001, pool 37.1%, complete industrial added value, year-on-year growth of his pupils about 1515 billion yuan 60.94%. Automobile consumption has become pull 2002 the main force of economic growth.The legal person status of more than 120 auto manufacturers. In 2002, faw, dongfeng, saic wait for three major automotive group (57%) production concentration than in 2001, up 8 percentage points; Chinese car because enterprise enters and competition is intense, sales of the top 3 places in Shanghai Volkswagen, faw Volkswagen and Shanghai gm of total sales than 2001 years ago single-month three market share fell 6.8 percentage points; Other kinds of car general production concentration than 2001 also have certain degree of decline. Just a single enterprise scale, China's automotive industry's top four faw, dongfeng, saic, changan automobile production on four big group in 30 million -- ability between 60 million vehicles, scale economic benefit began to appear. Nonetheless, the automobile production enterprise with world-class compared, China's automotive industry enterprise's remained small.Fierce market competition, a direct result of the price of cars is to make continued to decline, and finally achieve reasonable price; 2 it is competitive field, including not only expanded product price, quality, performance, but also related to marketing, after-sale service, market strain capacity, etc; Three is technological progress and productresearch and development will be the focus of competition. Through the full and effective competition of enterprises, unstoppable, and generally will be pushing the healthy growth of the industry's leading power.Third, China's automotive industry market space, investment opportunities and profit outlookFuture period with the influence of Chinese auto demand market price and income and consumption structure, auto loan, the improvement in consumption environment, especially transnational company leading the car under joint venture unceasingly in the global synchronous launch of new products to meet market demand for future market, will greatly push forward. The following 10 years - 15 years China will become the world's largest car market, the annual sales of $17 million vehicles, more than 1 million cars auto possession.In recent years, multinational companies to speed up the pace of the foray into China market, promote the domestic auto industry a new round of m&a boom. Multinational companies in China in the future is expected to take place more intense, the domestic several big automotive group relying on multinational company is rapid and outspread, will further accelerate all kinds of vehicle and parts production enterprises, especially smes, market structure of m&a drastic change, investment opportunities will emerge. MergerAt present, China's auto industry's overall profitability higher than international level, as the price of a product, which is likely to reduce down in price, but industry profit rate dropping, costs, expenses also have larger space, total profit dropped gross index such as likely to maintain, there might even improve. Countries further reduce some taxes, will provide for the majority of enterprises within the industry production and price space, if price is effectively with size can expand, scale effect will play out, can make the industry maintain a good level of efficiency. Meanwhile, parts of the import tariffs dropped, will make some manufacturers to import costs declined, imported parts more upscale product effect more apparent. The car industry in China's automobile industry most rapid development, not only output growth above the whole car industry product output growth, technology progress also greatly accelerated. Judging from the industry, cars, auto parts and accessories enterprise profitability in industry leading level, and has a higher return on investment.Fourth, the development trend of China's auto industry and the industrial policy orientation1. The development trend of China's automobile industry(1) is expected in the next 10 to 15 years, China will become the world's largest car shoppers. International experience shows that per capita income level and automobile penetration rate significantly correlated. China's per capita GDP in 2002, according to official 7972 yuan is the exchange rates more than $910 converted according to the world bank, and the PPP methods measuring is close to $4,000. In some developed city, southeast coastal quite a number of areas, according to the official exchange rate per capita GDP also reached four or five thousand dollars, calculated the obvious characteristics of going into the car society. Expect China will in the next 10 years -- 15 years in annual sales growth to 17m become the world's largest car market bus.(2) of automobile production and consumption in the future will be pulled very long period of China's economic growth important strength. The car industry is the most widely affected the scope of the biggest industry and spread effect. For steel, nonferrous metal, rubber, plastic, glass, coating and other raw materials industry, casting, forging, hot, welding, stamping, machining, paint, electroplating, test and inspection equipment manufacturing industry, machinery, electronics, electrical appliances, chemical industry, building materials, light industry, textile and other supporting products and components, highway construction, energy industry, transportation industry and service industry and so on, can produce huge demand, so as to promote the development of the industry. Each year are expected to the next 10 years, have 1 / GDP increment by seven to 1/6 provide auto industry.(3) China is expected to become the world automobile manufacturing center. China has initially formed relatively complete automobile industrial production system. This is the new development of China's automobile industry begins. In addition, the development of the car industry in China and the following advantages: one is the power market advantages; 2 it is labor cost advantage; Three is strong manufacturing supporting ability. Expected over the next 10 to 15 years, China is expected to become the world's important auto manufacturing one of base.2. The future development of China automobile industry policy orientation(1) create positive and full, to improve the international competitiveness of the automotive industry domestic competition environment. Should encourage various type enterprise especially private enterprise's into, and actively attract foreign direct investment,especially transnational corporations, direct investment, given the different natures of the enterprise with equal opportunity, through market competition market competition of the survival of the fittest, forming process the powerful market competition structure, leading enterprises and auto industry in our country the fundamental improve the international competitiveness.(2) restructuring, reorganization is a new period of China's automobile industry organization basic policy orientation. In the open, competitive, and on the basis of Chinese auto enterprise restructuring push with restructuring. In the restructuring, to adopt various ways to solve widespread enterprise do social, personnel overmuch, debt burden, social security system and the imperfect problems left over by history, promote enterprise property of diversification, the establishment of effective corporate governance mechanism. Corporate restructuring can focus on in the following respects: one is the integration with incremental automotive resources, deposit quantity and improve automobile industrial assets utilization; Second, further strengthen and automobile multinationals all-round cooperation; Three is to promote state-owned enterprise and the cooperation between non-state-owned enterprises; The fourth is to different types of automotive products adopt different restructuring strategy; Five is in emphasizing relax into the limit at the same time, want to eliminate exit barrier; Six is actively use capital market promotion industrial restructuring.(3) something to do, it. In the opening process gradually into the global automotive manufacturing division of labor system. Change the car industry chain configuration basically rely on domestic market and domestic resources by stages, the idea to gradually into the global auto industry procurement, manufacturing, marketing, research and development system, and gradually to high segment field advance. There are in the vehicle into a and concentrate on developing a market and resource advantage part products; To make full use of the Chinese market with more than ZhongDiJi other car production liang.2006.stages future period auto industry as a strategic emphasis, gradually realize scale advantages and cost advantages, and to meet the domestic market and capture peripheral developing countries; Simultaneously must use existing labor advantage, foster domestic conditional parts manufacturers will soon to change of the role of suppliers around the world.。