会计学原理第三章答案

会计学原理--教材第三章复式记账答案

习题一数据依次为:1920; 6300; 6740;15100 ;11000; 9860;13200;43000习题二(1) AH(2) IB(3)AF(4)I B (假设本月工资已经支付)(5)AD(6)AD(7)I B (文具用品当时就被领用)(8)CB(9)AB(10)AD习题三(1)借:主营业务成本28000贷:银行存款28000 (2)借:银行存款100000贷:短期借款100000 (3)借:银行存款200000贷:实收资本200000 (4)借:固定资产370000贷:应付账款370000 (5)借:应付账款58000贷:银行存款58000 (6)借:库存现金96750贷:银行存款96750 借:主营业务成本96750贷:应付职工薪酬96750借:应付职工薪酬96750贷:库存现金96750 (7)借:原材料66700贷:银行存款66700 (8)借:银行存款294560贷:主营业务收入294560 (9)借:主营业务成本89600贷:银行存款89600(10)借:主营业务成本73200贷:原材料72300习题四(1)借:财务费用26600贷:银行存款26600 (2)借:固定资产54800贷:应付账款54800(3)借: 银行存款 54000贷:应收账款54000(4)借::原材料 47000贷:银行存款 47000(5)借: :银行存款350000贷:主营业务收入350000(6) 借:主营业务成本 10780贷:银行存款 10780 (假设本月工资本月支付)(7)借: 主营业务成本75800贷:银行存款75800(8) 借:主营业务成本 128900贷:原材料1289002.借方 银行存款 贷方期初余额 45600(3) 54000(1) 26600 (5) 350000(4)47000(6) 10780(7)75800本期发生额404000 期末余额:289420本期发生额160180借方应收账款 贷方(6)10780(7)75800(8)128900期末余额:215480借方财务费用贷方(1) 26600期末余额:26600至善公司8月份账户本期发生额对照表75000 7500027000 2700015000 15000 500005000050000 50000 128000 62000 190000习题五1①借:银行存款贷:实收资本投资者投入资本750000。

会计学原理Financial-Accounting-by-Robert-Libby第八版-第三章-答案

会计学原理Financial-Accounting-by-Rob ert-Libby第八版-第三章-答案Chapter 3Operating Decisions andthe Accounting SystemANSWERS TO QUESTIONS1. A typical business operating cycle for a manufacturer would be as follows:inventory is purchased, cash is paid to suppliers, the product is manufactured and sold on credit, and the cash is collected from the customer.2. The time period assumption means that the financial condition andperformance of a business can be reported periodically, usually every month, quarter, or year, even though the life of the business is much longer.3. Net Income = Revenues + Gains - Expenses - Losses.Each element is defined as follows:Revenues -- increases in assets or settlements of liabilities from ongoing operations.Gains -- increases in assets or settlements of liabilities from peripheral transactions.Expenses -- decreases in assets or increases in liabilities from ongoingoperations.Losses -- decreases in assets or increases in liabilities from peripheraltransactions.4. Both revenues and gains are inflows of net assets. However, revenuesoccur in the normal course of operations, whereas gains occur from transactions peripheral to the central activities of the company. An example is selling land at a price above cost (at a gain) for companies not in the business of selling land.Both expenses and losses are outflows of net assets. However, expenses occur in the normal course of operations, whereas losses occur from transactions peripheral to the central activities of the company. An example is a loss suffered from fire damage.5. Accrual accounting requires recording revenues when earned andrecording expenses when incurred, regardless of the timing of cash receipts or payments. Cash basis accounting is recording revenues when cash is received and expenses when cash is paid.Financial Accounting, 8/e 3-2 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Financial Accounting, 8/e3-3© 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.6. The four criteria that must be met for revenue to be recognized under theaccrual basis of accounting are (1) delivery has occurred or services have been rendered, (2) there is persuasive evidence of an arrangement for customer payment, (3) the price is fixed or determinable, and (4) collection is reasonably assured.7. The expense matching principle requires that expenses be recorded whenincurred in earning revenue. For example, the cost of inventory sold during a period is recorded in the same period as the sale, not when the goods are produced and held for sale.8. Net income equals revenues minus expenses. Thus revenues increase netincome and expenses decrease net income. Because net income increases stockholders’ equity, revenues increase stockholders’ equity and expenses decrease it.9. Reve nues increase stockholders’ equity and expenses decreasestockholders’ equity. To increase stockholders’ equity, an account must be credited; to decrease stockholders’ equity, an account must be debited. Thus revenues are recorded as credits and expenses as debits. 10.11.12.13. Total net profit margin ratio is calculated as Net Income Net Sales (orOperating Revenues). The net profit margin ratio measures how much of every sales dollar is profit. An increasing ratio suggests that the company is managing its sales and expenses effectively.ANSWERS TO MULTIPLE CHOICE1. c2. a3. b4. b5. c6. c7. d8. b9. a10. bFinancial Accounting, 8/e 3-4 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Authors' Recommended Solution Time(Time in minutes)* Due to the nature of this project, it is very difficult to estimate the amount of time students will need to complete the assignment. As with any open-ended project, it is possible for students to devote a large amount of time to these assignments. While students often benefit from the extra effort, we find that some become frustrated by the perceived difficulty of the task. You can reduce student frustration and anxiety by making your expectations clear. For example, when our goal is to sharpen research skills, we devote class time discussing research strategies. When we want the students to focus on a real accounting issue, we offer suggestions about possible companies or industries.Financial Accounting, 8/e 3-5 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Financial Accounting, 8/e 3-6© 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.MINI-EXERCISESM3–1.TERMG (1) LossesC (2) Expense matching principle F (3) RevenuesE (4) Time period assumption B(5) Operating cycleM3–2.Cash Basis Income StatementAccrual Basis Income StatementRevenues: Cash sales Customer deposits$8,000 5,000 Revenues: Sales to customers$18,000 Expenses:Inventory purchases Wages paid 1,000 900 Expenses: Cost of sales Wages expense Utilities expense 9,000 900 300Net Income$11,100Net Income $7,800Revenue Account Affected Amount of Revenue Earned in JulyM3–4.Expense Account Affected Amount of Expense Incurred in JulyFinancial Accounting, 8/e 3-7 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.a. Cash (+A) ............................................................................ 15,000Games Revenue (+R, +SE) .......................................... 15,000 b. Cash (+A) ............................................................................ 3,000Accounts Receivable (+A) ................................................ 5,000 Sales Revenue (+R, +SE) ............................................. 8,000 c. Cash (+A) ............................................................................ 4,000Accounts Receivable (-A) ........................................... 4,000 d. Cash (+A) ............................................................................ 2,500Unearned Revenue (+L) ............................................... 2,500 M3–6.e. Cost of Goods Sold (+E, -SE)........................................... 6,800Inventory (-A) ............................................................... 6,800 f. Accounts Payable (–L) (800)Cash (-A) (800)g. Wages Expense (+E, -SE) ................................................. 3,500Cash (-A) ...................................................................... 3,500 h. Insurance Expense (+E, -SE) . (500)Prepaid Expenses (+A) ...................................................... 1,00 Cash (-A) ...................................................................... 1,500 i. Repairs Expense (+E, -SE) .. (700)Cash (-A) (700)j. Utilities Expense (+E, -SE) (900)Accounts Payable (+L) (900)Financial Accounting, 8/e 3-8 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Transaction (c) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.M3–8.Transaction (h) results in an increase in an asset (prepaid expenses) and a decrease in an asset (cash). Therefore, the net effect on assets is 500.Financial Accounting, 8/e 3-9 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.Craig’s Bowling, Inc.Income StatementFor the Month of July 2014Revenues:Games revenue $15,000Sales revenue 8,000Total revenues 23,000Expenses:Cost of goods sold 6,800Utilities expense 900Wages expense 3,500Insurance expense 500Repairs expense 700Total expenses 12,400Net income $ 10,600M3–10.Financial Accounting, 8/e 3-10 © 2014 by McGraw-Hill Global Education Holdings, LLC. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.M3–11.These results suggest that Jen’s Jewelry Company earned approximately $0.31 for every dollar of revenue in 2015, and over time, the ratio has improved. Jen’s has become more effective at managing sales and expenses.As additional analysis:Between 2013 to 2014 and 2014 to 2015, sales have increased at a lower percentage than net income. This suggests that the company has been more effective at controlling expenses than generating revenues.EXERCISESE3–1.TERMK (1) ExpensesE (2) GainsG (3) Revenue realization principleI (4) Cash basis accountingM (5) Unearned revenueC (6) Operating cycleD (7) Accrual basis accountingF (8) Prepaid expensesJ (9) Revenues - Expenses = Net IncomeL (10) Ending Retained Earnings =Beginning Retained Earnings + Net Income - Dividends DeclaredE3–2.Req. 1Cash Basis Income StatementAccrual Basis Income StatementRevenues:Cash sales Customer deposits $500,00070,000Revenues:Sales tocustomers$750,000Expenses:Inventory purchases Wages paidUtilities paid90,000180,30017,200Expenses:Cost of salesWages expenseUtilities expense485,000184,00019,130Net Income $282,500 Net Income $61,870Req. 2Accrual basis financial statements provide more useful information to external users. Financial statements created under cash basis accounting normally postpone (e.g., $250,000 credit sales) or accelerate (e.g., $70,000 customer deposits) recognition of revenues and expenses long before or after goods andservices are produced and delivered (until cash is received or paid). They also do not necessarily reflect all assets or liabilities of a company on a particular date.Activity Revenue AccountAmount of RevenueActivity Expense AccountAmount of ExpenseE3–5.Transaction (k) results in an increase in an asset (cash) and a decrease in an asset (accounts receivable). Therefore, there is no net effect on assets.* A loss affects net income negatively, as do expenses.E3–6.Transaction (f) results in an increase in an asset (property, plant, and equipment) and a decrease in an asset (cash). Therefore, there is no net effect on assets.E3–7.(in thousands)a. Plant and equipment (+A) (636)Cash ( A) (636)Debits equal credits. Assets increase and decrease by the same amount.b. Cash (+A) (181)Short-term notes payable (+L) (181)Debits equal credits. Assets and liabilities increase by the same amount.c. Cash (+A) ..........................................................................Accounts receivable (+A) ................................................ 10,765 28,558Service revenue (+R, +SE) ........................................ 39,323 Debits equal credits. Revenue increases retained earnings (part of stockholders' equity). Stockholders' equity and assets increase by the same amount.E3–7. (continued)d. Accounts payable (-L) ..................................................... 32,074Cash (-A) ................................................................... 32,074 Debits equal credits. Assets and liabilities decrease by the same amount.e. Inventory (+A) ................................................................... 32,305Accounts payable (+L) .............................................. 32,305 Debits equal credits. Assets and liabilities increase by the same amount.f. Wages expense (+E, -SE) ............................................... 3,500Cash (-A) ................................................................... 3,500 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.g. Cash (+A) .......................................................................... 39,043Accounts receivable (-A) ....................................... 39,043 Debits equal credits. Assets increase and decrease by the same amount.h. Fuel expense (+E, -SE) (750)Cash (-A) (750)Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.i. Retained earnings (-SE) (597)Cash (-A) (597)Debits equal credits. Assets and stock holders’ equity decrease by thesame amount.j. Utilities expense (+E, -SE) (68)Cash (-A) ................................................................... Accounts payable (+L) .............................................. 55 13Debits equal credits. Expenses decrease retained earnings (part of stockholders' equity). Together, stockholders' equity and liabilities decrease by the same amount as assets.E3–8.Req. 1a.Cash (+A) ................................................................... 2,300,000Short-term note payable (+L) ........................ 2,300,000 Debits equal credits. Assets and liabilities increase by the same amount.b.Equipment (+A) ......................................................... 98,000Cash (-A) ........................................................ 98,000 Debits equal credits. Assets increase and decrease by the same amount.c.Merchandise inventory (+A) .................................... 35,000Accounts payable (+L) .................................. 35,000 Debits equal credits. Assets and liabilities increase by the same amount.d.Repairs (or maintenance) expense (+E, -SE) ......... 62,000Cash (-A) ........................................................ 62,000 Debits equal credits. Expenses decrease retained earnings (part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.e.Cash (+A) ................................................................... 390,000Unearned pass revenue (+L) ......................... 390,000 Debits equal credits. Since the season passes are sold before Vail Resorts provides service, revenue is deferred until it is earned. Assets andliabilities increase by the same amount.f.Two transactions occur:(1) Accounts receivable (+A) (800)Ski shop sales revenue (+R, +SE) (800)Debits equal credits. Revenue increases retained earnings (a part ofstockholders' equity). Stockholders' equity and assets increase by thesame amount.(2) Cost of goods sold (+E, -SE) (500)Merchandise inventory (-A) (500)Debits equal credits. Expenses decrease retained earnings (a part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.E3–8. (continued)g.Cash (+A) ................................................................... 320,000Lift revenue (+R, +SE) .................................... 320,000 Debits equal credits. Revenue increases retained earnings (a part ofstockholders' equity). Stockholders' equity and assets increase by thesame amount.h.Cash (+A) ................................................................... 3,500Unearned rent revenue (+L) .......................... 3,500 Debits equal credits. Since the rent is received before the townhouse isused, revenue is deferred until it is earned. Assets and liabilities increase by the same amount.i. Accounts payable (-L) ............................................. 17,500Cash (-A) ........................................................ 17,500 Debits equal credits. Assets and liabilities decrease by the same amount. j.Cash (+A) . (400)Accounts receivable (-A) (400)Debits equal credits. Assets increase and decrease by the same amount. k.Wages expense (+E, -SE) ........................................ 245,000Cash (-A) ........................................................ 245,000 Debits equal credits. Expenses decrease retained earnings (a part ofstockholders' equity). Stockholders' equity and assets decrease by thesame amount.Req. 22/1 Rent expense (+E, -SE) (275)Cash (-A) (275)2/2 Fuel expense (+E, -SE) (490)Accounts payable (+L) (490)2/4 Cash (+A) (820)Unearned revenue (+L) (820)2/7 Cash (+A) (910)Transport revenue (+R, +SE) (910)2/10 Advertising expense (+E, -SE) (175)Cash (-A) (175)2/14 Wages payable (-L) ......................................................... 2,300Cash (-A) ......................................................... 2,3002/18 Cash (+A) ..........................................................................Accounts receivable (+A) ................................................ 1,600 2,200Transport revenue (+R, +SE) ......................... 3,800 2/25 Parts supplies (+A) .......................................................... 2,550Accounts payable (+L) ................................... 2,550 2/27 Retained earnings (-SE) .. (200)Dividends payable (+L) (200)Req. 1 and 2Accounts Unearned Fee NoteAdditional Paid-inRebuilding Fees RentItem (f) is not a transaction; there has been no exchange.E3–10. (continued)Req. 3Net income using the accrual basis of accounting:Revenues $19,850 ($19,000 + $850)– Expenses 16,900 ($16,500 + $400)Net Income $ 2,950Assets = Liabilities + Stockholders’ Equity$12,090 $ 7,700 $ 1,70024,800 4,440 7,8202,460 48,500 9,36010,420 2,950 netincome7,40025,300$82,470 $60,640 $21,830Req. 4Net income using the cash basis of accounting:Cash receipts $27,650 (transactions a through d)–Cash disbursements 19,760 (transactions g, i, and k)Net Income $ 7,890Cash basis net income ($7,890) is higher than accrual basis net income ($2,950) because of the differences in the timing of recording revenues versus receipts and expenses versus disbursements between the two methods. The $7,800 higher amount in cash receipts over revenues includes cash received prior to being earned (from (b), $600) and cash received after being earned (in (d), $7,200). The $2,860 higher amount in cash disbursements over expenses includes cash paid after being incurred in the prior period (in (g), $2,300), plus cash paid for supplies to be used and expensed in the future (in (k), $960), less an expense incurred in January to be paid in February (in (e), $400).STACEY’S PIANO REBUILDING COMPANYIncome Statement (unadjusted)For the Month Ended January 31, 2014 Operating Revenues:Rebuilding fees revenue $ 19,000 Total operating revenues 19,000 Operating Expenses:Wages expense 16,500 Utilities expense 400 Total operating expenses 16,900 Operating Income 2,100 Other Item:Rent revenue 850 Net Income $ 2,950Req. 1 and 2Common Additional RetainedFood Sales Revenue Catering Sales RevenueE3–14.Req. 1TRAVELING GOURMET, INC.Income Statement (unadjusted)For the Month Ended March 31, 2014 Revenues:Food sales revenueCatering sales revenueTotal revenues Expenses:Supplies expenseUtilities expenseWages expenseFuel expenseTotal costs and expenses $ 11,9004,20016,10010,8304206,28036317,893Net Loss $ (1,793) Req. 2Transaction O, I, or F Activity (or No Effect) on Statement ofDirection and AmountReq. 3The company generated a small loss of 1,793 during its first month of operations, before making any adjusting entries. The adjusting entries for use of the building and equipment and interest expense on the borrowing will increase the loss. Cash flows from operating activities were also negative at $2,973 (= + 11,900 + 2,600 –10,830 –363 –6,280) . So far the company does not appear to be successful, but it is only in its first month of operating a retail store. If sales can be increased without inflating fixed costs (particularly salaries expense), the company may soon turn a profit. It is not unusual for small businesses to report a loss or have negative cash flows from operations as they start up operations.E3–15.Req. 1Transaction Brief Explanationa Issued 10,000 shares of common stock to shareholders for $82,000cash.b Purchased store fixtures for $15,400 cash.c Purchased $24,800 of inventory, paying $6,200 cash and thebalance on account.d Sold $14,000 of goods or services to customers, receiving $9,820cash and the balance on account. The cost of the goods sold was$7,000.e Used $1,480 of utilities during the month, not yet paid.f Paid $1,300 in wages to employees.g Paid $2,480 in cash for rent, $620 related to the current month and$1,860 related to future months.h Received $3,960 cash from customers, $1,450 related to currentsales and $2,510 related to goods or services to be provided in thefuture.Req. 2Kate’s Kite CompanyIncome StatementFor the Month Ended April 30, 2014Sales Revenue Expenses:Cost of salesWages expenseRent expenseUtilities expenseTotal expenses $ 15,4507,0001,3006201,48010,400Net Income $ 5,050Kate’s Kite CompanyBalance SheetAt April 30, 2014Assets Liabilities and Shareholders’ Equity Current Assets: Current Liabilities:Cash $70,400 Accounts payable $20,080 Accounts receivable 4,180 Unearned revenue 2,510 Inventory 17,800 Total current liabilities 22,590 Prepaid expenses 1,860 Shareholders’ Equity:Total current assets 94,240 Common stock 10,000 Store fixtures 15,400 Additional paid-in capital 72,000Retained earnings 5,050Total shareholders’equity87,050Total Assets $109,640 Total Liabilities &Shareholders’ Equity$109,640E3–16.Req. 1Assets = Liabilities + Stockholders’ Equity $ 3,200 $ 2,400 $ 800 8,000 5,600 4,0006,400 1,600 3,200 $17,600 $9,600 $ 8,000Req. 2Accounts Long-TermAccounts Unearned Long-TermAdditionalConsulting Fee InvestmentRent ExpenseE3–16. (continued)Req. 3Revenues $58,400 ($58,000 from sales + $400 on investments)– Expenses 56,400 ($36,000 + $12,000 + $800 + $7,600)Net Income $ 2,000Assets = Liabilities + Stockholders’ Equity$ 1,120 $ 1,600 $ 80012,400 7,200 4,0006,400 1,600 2,7202,000 net income $19,920 $10,400 $ 9,520 Req. 4Net Profit Margin = Net Income = $2,000 = 0.0345Ratio Sales (Operating) Revenues $58,000* or 3.45% * The $400 of investment income is not an operating revenue and is not included in the computation.The increasing trend in the net profit margin ratio (from 2.5% in 2013 to 2.9% in 2014 and then to 3.45% in 2015) suggests that the company is managing its sales and expenses more effectively over time.E3–17.Req. 1Accounts receivable increases with customer sales on account and decreases with cash payments received from customers.Prepaid expenses increase with cash payments of expenses related to future periods and decrease as these expenses are incurred over time.Unearned subscriptions increase with cash payments received from customers for goods or services to be provided in the future and decreases when those goods or services are provided.Req. 2Trade Accounts ReceivablePrepaidExpensesUnearnedSubscriptionsComputations:Beginning + “+”-“-”= EndingTrade accounts receivable 717 + 5,240 -??==6935,264Prepaid expenses 95 + 203 -??==107191Unearned subscriptions 224 + 2,690 -??==2312,683E3–18.ITEM LOCATION1. Description of a company’sprimary business(es). Letter to shareholders;Management’s Discussion and Analysis; Summary of significant accounting policies note2. Income taxes paid. Notes; Statement of cash flows3. Accounts receivable. Balance sheet4. Cash flow from operatingactivities.Statement of cash flows5. Description of a company’srevenue recognition policy. Summary of significant accounting policies note6. The inventory sold during theyear.Income statement (Cost of Goods Sold)7. The data needed to compute thenet profit margin ratio.Income statementPROBLEMSP3-1.Transactions Debit Credita. Example: Purchased equipment for use in the business;5 1, 8paid one-third cash and signed a note payable for thebalance.b. Paid cash for salaries and wages earned by employees thisperiod.15 1 c. Paid cash on accounts payable for expensesincurred last period.7 1d. Purchased supplies to be used later; paid cash. 3 1e. Performed services this period on credit. 2 14f. Collected cash on accounts receivable for servicesperformed last period. 1 2g. Issued stock to new investors. 1 11, 12h. Paid operating expenses incurred this period.15 1i. Incurred operating expenses this period to be paidnext period.15 7 j. Purchased a patent (an intangible asset); paid cash. 6 1 k. Collected cash for services performed this period. 1 14 l. Used some of the supplies on hand for operations.15 3 m. Paid three-fourths of the income tax expense for the year;the balance will be paid next year.16 1, 10 n. Made a payment on the equipment note in (a); the paymentwas part principal and part interest expense.8, 17 1 o. On the last day of the current period, paid cash for aninsurance policy covering the next two years. 4 1a. Cash (+A) ........................................................................... 40,000Common stock (+SE) (20)Additional paid-in capital (+SE) ................................ 39,980 b. Cash (+A) ........................................................................... 60,000Note payable (long-term) (+L) ..................................... 60,000 c. Rent expense (+E, -SE) .................................................... 1,500Prepaid rent (+A) ............................................................... 1,500 Cash (-A) ...................................................................... 3,000 d. Prepaid insurance (+A) ..................................................... 2,400Cash (-A) ..................................................................... 2,400 e. Furniture and fixtures (or Equipment) (+A) ..................... 15,000Accounts payable (+L) ............................................... 12,000Cash (-A) ..................................................................... 3,000 f. Inventory (+A) .................................................................... 2,800Cash (-A) ..................................................................... 2,800 g. Advertising expense (+E, -SE) .. (350)Cash (-A) (350)h. Cash (+A) (850)Accounts receivable (+A) (850)Sales revenue (+R, +SE) ............................................ 1,700 Cost of goods sold (+E, -SE) . (900)Inventory (-A) (900)i. Accounts payable (-L) ...................................................... 12,000Cash (-A) ..................................................................... 12,000 j. Cash (+A) (210)Accounts receivable (-A) (210)。

会计学原理3业务核算及分类选择判断题答案

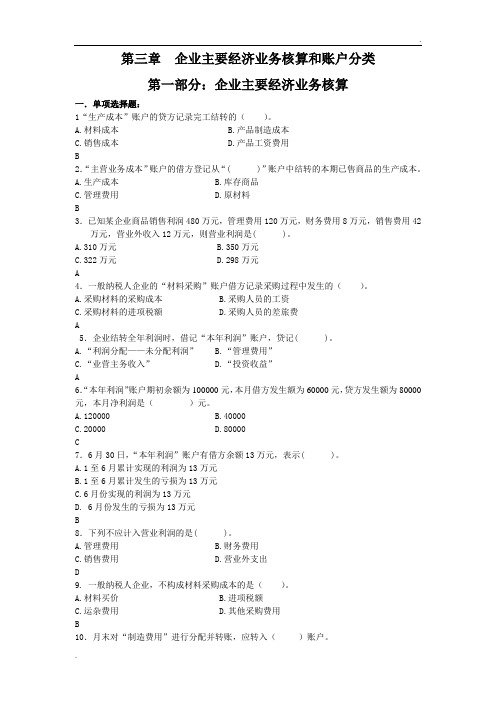

第三章企业主要经济业务核算和账户分类第一部分:企业主要经济业务核算一.单项选择题:1“生产成本”账户的贷方记录完工结转的()。

A.材料成本B.产品制造成本C.销售成本D.产品工资费用B2.“主营业务成本”账户的借方登记从“( )”账户中结转的本期已售商品的生产成本。

A.生产成本B.库存商品C.管理费用D.原材料B3.已知某企业商品销售利润480万元,管理费用120万元,财务费用8万元,销售费用42万元,营业外收入12万元,则营业利润是( )。

A.310万元B.350万元C.322万元D.298万元A4.一般纳税人企业的“材料采购”账户借方记录采购过程中发生的()。

A.采购材料的采购成本B.采购人员的工资C.采购材料的进项税额D.采购人员的差旅费A5.企业结转全年利润时,借记“本年利润”账户,贷记( )。

A.“利润分配——未分配利润”B.“管理费用”C.“业营主务收入”D.“投资收益”A6.“本年利润”账户期初余额为100000元,本月借方发生额为60000元,贷方发生额为80000元,本月净利润是()元。

A.120000B.40000C.20000D.80000C7.6月30日,“本年利润”账户有借方余额13万元,表示( )。

A.1至6月累计实现的利润为13万元B.1至6月累计发生的亏损为13万元C.6月份实现的利润为13万元D. 6月份发生的亏损为13万元B8.下列不应计入营业利润的是( )。

A.管理费用B.财务费用C.销售费用D.营业外支出D9. 一般纳税人企业,不构成材料采购成本的是()。

A.材料买价B.进项税额C.运杂费用D.其他采购费用B10.月末对“制造费用”进行分配并转账,应转入()账户。

A.生产成本B.管理费用C.主营业务成本D.财务费用A11.购买单位在材料采购业务之前按合同先向供应单位预付购货款时,形成了()。

A.负债 B.债务C.债权D.权益C12.购买单位购进材料时暂不付款,从而形成企业对供应单位的一项()。

会计学原理第三章课后答案

会计学原理第三章课后答案第三章3-1:练习借贷记账法的运用(一)编制会计分录:题号分录题号分录借:库存现金 300 借:银行存款 15,000 1 6 贷:银行存款 300 贷:短期借款15,000借:其他应收款 300 借:应付账款 12,000 2 7 贷:库存现金 300 贷:银行存款12,000借:应交税费 2,000 借:生产成本 16,000 3 8 贷:银行存款 2,000 贷:原材料16,000借:原材料 8,000 借:银行存款 2,900 4 9 贷:应付账款 8,000 贷:应收账款2,900借:固定资产 2,000 借:短期借款 9,000 5 10 贷:银行存款 2,000 贷:银行存款 9,000(二)开设并登记T型账(没有发生额的省略):借库存现金贷借银行存款贷期初余额 100 期初余额 18,0001、 3002、 300 6、 15,000 1、 3009、 2,900 3、 2,0005、 2,0007、 12,00010、 9,000本期发生额 300 本期发生额 300 本期发生额 17,900 本期发生额 25,300 期末余额 100 期末余额 10,600借应收账款贷借其他应收款贷期初余额 2,900 期初余额 1,0009、 2,900 2、 300本期发生额 2,900 本期发生额 300 期末余额 0 期末余额 1,300借原材料贷借生产成本贷期初余额 26,000 8、 16,000 4、 8,000 8、16,000 本期发生额 8,000 本期发生额16,000 本期发生额16,000 期末余额18,000 期末余额 16,000借固定资产贷借短期借款贷期初余额 450,000 期初余额 9,000 5、2,000 10、 9,000 6、 15,000 code certificate, tax registration certificate, legal persons or persons in charge of identity documents, articles of incorporation, verification report, credit card and other information; 2, the business unit financial information, including financial reports, accounting records, bank account statements, or the transaction flow, upstream and本期发生额 2,000 本期发生额 9,000 本期发生额 15,000 期末余额 452,000 期末余额 15,000借应付账款贷借应交税费贷期初余额 4,000 期初余额 2,000 7、 12,000 4、 8,000 3、 2,000本期发生额12,000 本期发生额 8,000 本期发生额 2,000期末余额 0 期末余额 0期初余额本期发生额期末余额账户名称借方贷方借方贷方借方贷方库存现金 100 300 300 100 银行存款 18,000 17,900 25,300 10,600 应收账款2,900 2,900 0 其他应收款 1,000 300 1,300 原材料 26,000 8,000 16,000 18,000 库存商品 10,000 10,000 生产成本 16,000 16,000 固定资产 450,000 2,000 452,000 短期借款 9,000 9,000 15,000 15,000 应付账款 4,000 12,0008,000 应交税费 2,000 2,000 实收资本 450,000 450,000 盈余公积 32,00032,000 本年利润 11,000 11,000合计 508,000 508,000 67,500 67,500 508,000 508,000第五章:练习账户按经济内容和用途结构分类经济内容资产负债所有者成本损益用途结构账户账户权益账户账户账户 1、盘存账户 5、9、20、22 2、结算账户 1、6 2、3、13 3、资本账户 11、16 4、跨期摊配账户 15 10 5、对外投资账户 23 6、集合分配账户 4 7、成本计算账户 18 8、集合配比账户 8、12、14、17 9、财务成果账户 7 10、计价对比账户 11、待处理账户 24 12、调整账户 19 21 code certificate, taxregistration certificate, legal persons or persons in charge of identity documents, articles of incorporation, verification report, credit card and other information; 2, the business unit financial information, including financial reports, accounting records, bank account statements, or the transaction flow, upstream andcode certificate, tax registration certificate, legal persons or persons in charge of identity documents, articles of incorporation, verification report, credit card and other information; 2, the business unit financial information, including financial reports, accounting records, bank account statements, or the transaction flow, upstream and。

李海波《会计学原理》第3章习题答案

1.借:银行存款 35100贷:主营业务收入 30000 应交税费——应交增值税(销项税额) 5100 2. 借:应收账款 52650贷:主营业务收入 45000 应交税费——应交增值税(销项税额) 7650 3.借:主营业务成本 57000贷:库存商品 570004.借:销售费用 1000贷:银行存款 10005.借:销售费用 1140贷:应付职工薪酬 11406.借:银行存款 1200贷:其他业务收入 12007.借:其他业务成本 1000贷:原材料 10001.借:银行存款 58500贷:主营业务收入 50000 应交税费——应交增值税(销项税额) 8500 2. 借:主营业务成本 35000贷:库存商品 350003. 借:销售费用 500贷:库存现金 5004.借:管理费用 300贷:银行存款 3005.借:财务费用 2200贷:银行存款 22006.借:营业外支出 500贷:银行存款 5007.借:其他应付款 300贷:营业外收入 300 %%%%%%%%%%%%%%%%%%%%%%%%1.借:主营业务收入 50000营业外收入 300贷:本年利润 50300借:本年利润 38500贷:主营业务成本 35000销售费用 500管理费用 300财务费用 2200营业外支出 5002.12月份利润总额=50300-38500=11800元12月份应交所得税=11800*25%=2950元借:所得税费用 2950贷:应交税费——应交所得税 2950借:本年利润 2950贷:所得税费用 29503.12月份净利润=11800-2950=8850元借:本年利润 8850贷:利润分配——未分配利润 88504. 8850*10%=885元借:利润分配——提取法定盈余公积 885贷:盈余公积 885 5. 8850*15%=1327.50元借:利润分配——提取任意盈余公积 1327.50 贷:盈余公积 1327.50 6. 8850*10%=885元借:利润分配——应付股利 885贷:应付股利 885P137 习题六1.借:银行存款 400000贷:实收资本 4000002. 借:固定资产 180000贷:实收资本 1800003.借:银行存款 50000贷:短期借款 500004. 借:银行存款 500000贷:长期借款 5000005. 借:短期借款 50000贷:银行存款 500006.借:固定资产清理 120000累计折旧 30000贷:固定资产 150000 借:长期股权投资 130000贷:固定资产清理 120000营业外收入 10000 7. 借:固定资产清理 20000累计折旧 10000贷:固定资产 30000 借:银行存款 20000贷:固定资产清理 200008.借:应付职工薪酬 3000贷:银行存款 3000P138习题七1.借:生产成本——基本生产成本——A——直接材料 21900——B——直接材料 18100 贷:原材料 40000 2.借:制造费用 2000贷:原材料 20003.借:库存现金 30000贷:银行存款 300004.借:应付职工薪酬 24000贷:库存现金 240005.借:材料采购——甲材料 15000应交税费——应交增值税(进项税额)2380贷:银行存款 17380 借:原材料——甲材料 15000贷:材料采购——甲材料 150006. 借:材料采购——乙材料 40000应交税费——应交增值税(进项税额) 6800贷:应付票据 46800 7. 借:材料采购——乙材料 600贷:库存现金 600借:原材料——乙材料 40600贷:材料采购——乙材料 406008.借:银行存款 3000贷:应收账款——新华厂 30009.借:应交税费 1000贷:银行存款 100010.借:生产成本——基本生产成本——A——直接人工 10000——B——直接人工 10000 制造费用 3000管理费用 1000贷:应付职工薪酬 24000 11. 借:生产成本——基本生产成本——A——直接人工 1400——B——直接人工 1400 制造费用 420管理费用 140贷:应付职工薪酬 3360 12.借:制造费用 2380管理费用 780贷:累计折旧 316013.借:制造费用 1400贷:银行存款 140014.制造费用=2000+3000+420+2380+1400=9200元制造费用分配率=9200/(10000+10000)=0.46借:生产成本——基本生产成本——A——制造费用4600——B——制造费用4600 贷:制造费用 9200 15.A完工产品成本=21900+10000+1400+4600=37900元借:库存商品——A 37900贷:生产成本——基本生产成本——A 37900(*A单位产品成本=37900/2000件=18.95元/件)16. 借:应收账款 131040贷:主营业务收入 112000 应交税费——应交增值税(销项税额) 19040 17.借:主营业务成本 80000贷:库存商品 8000018.借:销售费用 1100贷:库存现金 110019.借:财务费用 5000贷:银行存款 500020. 借:管理费用 1200贷:银行存款 120021.借:营业外支出 1120贷:待处理财产损溢 112022.借:其他应付款 300贷:营业外收入 30023.借:银行存款 2340贷:其他业务收入 2000应交税费——应交增值税(销项税额)340 借:其他业务成本 1500贷:原材料 1500(24)“管理费用”借方发生额合计=1000+140+780+1200=3120 “主营业务收入”贷方发生额合计=112000“主营业务成本”借方发生额合计=80000“销售费用”借方发生额合计=1100“财务费用”借方发生额合计=5000“营业外支出”借方发生额合计=1120“营业外收入”贷方发生额合计=300“其他业务收入”贷方发生额合计=2000“其他业务成本”借方发生额合计=1500借:主营业务收入 112000其他业务收入 2000营业外收入 300贷:本年利润 114300借:本年利润 91840贷:管理费用 3120主营业务成本 80000销售费用 1100财务费用 5000营业外支出 1120其他业务成本 1500利润总额=114300-91840=22460元(25)应交所得税=22460*25%=5615元借:所得税费用 5615贷:应交税费——应交所得税 5615借:本年利润 5615贷:所得税费用 5615“本年利润”账户余额=22460-5615=16845元(即净利润)借:本年利润 16845贷:利润分配——未分配利润 16845(26)提取法定盈余公积=16845*10%=1684.50元借:利润分配——提取法定盈余公积 1684.50贷:盈余公积 1684.50。

会计学原理 智慧树知到网课章节测试答案

1、选择题:会计的目标是()。

选项:A:向信息使用者提供可据以作出决策的会计信息B:对经济活动进行核算和控制C:管理生产经营活动D:评价企业的绩效答案: 【向信息使用者提供可据以作出决策的会计信息】2、选择题:会计处基本职能外,还具有()等职能。

选项:A:会计决策B:会计考核C:会计分析D:会计预测E:会计预算答案: 【会计决策,会计考核,会计分析,会计预测,会计预算】3、选择题:会计可以从不同的角度来进行考察与认识,会计可以被认为是()。

选项:A:一种管理的工具B:一个经济信息系统C:一种统计数据D:一种提供信息的技艺E:一种管理活动答案: 【一种管理的工具,一个经济信息系统,一种提供信息的技艺,一种管理活动】4、选择题:会计被认为是一种将预计发生的经济活动加工为会计信息的技艺。

选项:A:对B:错答案: 【错】5、选择题:会计信息的提供者对于所提供的会计信息,特别是对外提供的会计信息负有法律责任。

选项:A:对B:错答案: 【对】1、选择题:资产和负债按照市场参与者在计量日发生的有序交易中,出售一项资产所能收到或者转移一项负债所需支付的金额计量属性是()。

选项:A:现值B:公允价值C:历史成本D:重置成本答案: 【公允价值】2、选择题:下列做法中,有助于提高会计信息可比性的有()。

选项:A:同一企业前后各期采用相同的会计政策B:在财务会计报告中提供以前期间的对比数据C:各企业根据自身的需要灵活选择会计政策D:各企业都遵循会计准则的同一规定E:在财务会计报告中披露企业所采用的中大会计政策答案: 【同一企业前后各期采用相同的会计政策,在财务会计报告中提供以前期间的对比数据,各企业都遵循会计准则的同一规定】3、选择题:关于历史成本的评价,下列说法中正确的有()。

选项:A:数据容易取得,操作方便B:相关性强C:能够被核实和验证D:不同时期的会计信息可能缺少可比性E:资产的账面价值可能会脱离实际价值答案: 【数据容易取得,操作方便,能够被核实和验证,不同时期的会计信息可能缺少可比性,资产的账面价值可能会脱离实际价值】4、选择题:法律主体可以成为会计主体,但会计主体不一定能成为法律主体。

(完整word版)浙江大学远程会计学原理练习题第三章答案

第三章企业主要经济活动的核算一、单项选择题1.在计划成本核算下,用来核算企业购入材料的买价和采购费用,据以确定材料采购成本的账户是(B ),在实际成本核算下,则是(E )。

A.原材料 B.材料采购 C.制造费用 D.主营业务成本 E在途物资2.下列费用项目中,应作为产品生产成本的是(B)。

A.厂部管理耗用的材料费 B.生产车间管理人员工资C.行政管理部门固定资产折旧费用 D.银行借款利息3.实收资本账户属于(C)账户。

A.资产类 B.负债类 C.所有者权益类 D.收入类4“固定资产”账户是反映企业固定资产的( C )。

A。

磨损价值 B。

累计折旧C。

原始价值 D.净值5.已经完成全部生产过程并已验收入库,可供对外销售的产品即为( D )。

A.已销产品 B。

生产成本C。

销售成本 D.库存商品6.下列属于其他业务收入的是( B ),属于营业外收入的是(D)A.利息收入B.出售材料收入C。

投资收益 D。

清理固定资产净收益7.企业8月末负债总额100万元,9月份收回欠款15万元,用银行存款归还借款10万元,用银行存款预付购货款5万元,则9月末负债总额为( C )A。

110万元 B.105万元C.90万元 D。

80万元8。

在权责发生制下,下列货款应列作本期收入的是( A )A. 本月销货款存入银行B. 上个月销货款本月收存银行C. 本月预收下月货款存入银行D。

本月收回上月多付给供应单位的预付款存入银行9.下列费用中,不构成产品成本的有( C )。

----------专业最好文档,专业为你服务,急你所急,供你所需-------------A。

直接材料费 B。

直接人工费C。

期间费用 D.制造费用10.“本年利润”账户年内的贷方余额表示( C )。

A。

利润分配额 B。

未分配利润额C.净利润额 D。

亏损额11。

年末结转后,“利润分配”账户的贷方余额表示( D )。

A。

实现的利润总额 B。

净利润额C。

利润分配总额 D。

江西财经大学会计学原理第三章答案

第三章(账户和复式记账的应用)习题答案习题一:1、借:原材料 15 000应交税费——应交增值税(进项税额) 2 550银行存款 7 450贷:实收资本(或股本) 25 0002、借:无形资产 20 000贷:实收资本 20 0003、借:固定资产 50 000贷:实收资本 50 0004、借:固定资产 50 000贷:实收资本 50 0005、借:银行存款 50 000贷:短期借款 50 0006、借:银行存款 100 000贷:长期借款 100 000习题二:1、不可抵扣借:固定资产 47 000贷:应付账款 47 000可以抵扣借:固定资产 40 200应交税费-应交增值税(进项税额) 6 800贷:应付账款 47 0002、不可抵扣借:在建工程 35 700元贷:银行存款 35 700可以抵扣借:在建工程 30 600应交税费-应交增值税(进项税额) 5 100贷:银行存款 35 7003、不可抵扣(1)借:在建工程 317贷:应交税费—应交增值税(进项税转出) 17 原材料 100库存现金 200可抵扣借:在建工程 300贷:原材料 100库存现金 200(2)不可抵扣借:固定资产 36 017 贷:在建工程 36 017 可以抵扣借:固定资产 30 900贷:在建工程 30 9004、(1)借:在途物资—甲 20 200应交税费—应交增值税(进项税额) 3 400 贷:应付账款 23 400库存现金 200(2)借:原材料—甲 20 200贷:在途物资—甲 20 2005、借:在途物资---乙 10 300应交税费—应交增值税(进项税额) 1 700 贷:银行存款 12 0006、借:原材料—乙 10 300贷:在途物资—乙 10 3007、借:应付账款 23 400贷:银行存款 23 4008、借:预付账款15 000贷:银行存款15 000 9、借:在途物资—丙20 000应交税费—应交增值税(进项税额) 3400 贷:预付账款15 000 银行存款84 00 10、借:原材料—丙20 000贷:在途物资—丙20 000习题三、1、借:在途物资—甲 6 000—-乙 5 000 应交税费—应交增值税(进项税额) 1 870 贷:银行存款12 8702、660(1)分配率=6+4= 66(元/吨)甲材料应负担运费=6╳66=396元乙材料应负担运费=4╳66=264元(2)借:在途物资—甲396—乙 264 贷:库存现金运杂费算进在途物资 6603、借:原材料—甲 6 396—乙 5 264贷:在途物资—甲 6 396—乙 5 264习题四:1、借:生产成本—A 25 000—B 15 000制造费用8 000管理费用 2 000贷:原材料--××材料50 0002、借:生产成本—A 22 800—B 11 400 制造费用 3 420管理费用7 980 贷:应付职工薪酬---工资45 6003、借:其他应收款——张平 1 000贷:银行存款 1 0004、借:制造费用 200管理费用 800贷:银行存款 1 0005、借:制造费用 200管理费用 100贷:银行存款 3006、借:财务费用 500贷:应付利息 5007、借:制造费用 2 000管理费用 1 000贷:累计折旧 3 0008、借:应付利息 1 200短期借款 20 000贷:银行存款 21 2009、借:制造费用 1 180管理费用 620贷:应付账款 1 800习题五:(一)1、(1)本月制造费用=8000元(1)+3420元(2)+200元(4)+200元(5)+2000元(7)+1180元(9)=15000元制造费用分配率=15000/34200(A、B产品工人工资总额)=0. 4386(元)A产品应摊销制造费用=22800 × 0.4386=10000元B产品应摊销制造费用=11400 × 0.4386=5000元制造费用分配表分配对象分配标准分配率分配额A产品22 800 0.438596 10 000B产品11 400 0.438596 5 000合计34 200 0.438596 15 000(2)借:生产成本——A 10 000——B 5 000贷:制造费用 15 0002、A产品完工产品成本=2200+(25000+22800+10000)- 0 =60000元借:库存商品——A 60 000贷:生产成本——A 60 000A产品完工产品成本计算表入库产品数量:1000件成本项目总成本金额单位产品成本直接材料26 200 26.20直接人工23 200 23.20制造费用10 600 10.60合计60 000 60.003、B产品完工产品成本=0+(15000+11400+5000)-0=31400元借:库存商品——B 31 400贷:生产成本——B 31 400B产品完工产品成本计算表入库产品数量:2000件成本项目总成本金额单位产品成本直接材料15000 7.5直接人工11400 5.7制造费用5000 2.5合计31400 15.7(二)制造费用=5 000(1)+10 000(2)+7000(3)+5000(4)=270001、分配率=27 000÷60 000=0.452、A分配额=0.45×40 000=18 000B分配额=0.45×20 000=9 0003、A生产费用=20 000(1)+40 000(2)+18 000(制)=78 000B生产费用=16 000(1)+20 000(2)+9 000(制)=45 000(三)1、总成本=15 000+85 000-0=100 0002、单位产品成本=100 000÷2 000(件)=50元/件3、材料:10 000+56 000-0=66 000单位产品材料成本:66 000÷2 000(件)=33/件人工:3 000+24 000-0=27 000单位产品人工成本:27 000÷2 000(件)=13.50/件制造费用:2 000+5 000-0=7 000单位产品制造费用:7 000÷2 000(件)=3.50/件习题六:1、借:应收账款 23 400贷:主营业务收入 20 000应交税费——应交增值税(销项税额) 3 4002、借:银行存款 46 800贷:主营业务收入 40 000应交税费——应交增值税(销项税额) 6 8003、借:银行存款 20 000贷:预收账款 20 0004、借:预收账款 23 400贷:主营业务收入 20 000应交税费——应交增值税(销项税额) 3 4005、(1)甲产品加权平均成本=(65.5×100+60×1000)/(100+1000)=60.5元甲产品本月销售成本=60.5×800=48 400元(2)借:主营业务成本 48 400贷:库存商品——甲 48 4006、借:销售费用 1 600贷:银行存款 1 6007、(1)借:营业税金及附加 4 000贷:应交税费——应交消费税 4 000 (2)借:应交税费——应交消费税 4 000贷:银行存款 4 000习题七:1、借:银行存款 2340贷:其他业务收入 2000应交税费——应交增值税(销项税额) 3402、借:其他业务成本 1800贷:原材料 18003、借:应付账款 5000贷:营业外收入 50004、借:营业外支出 4 700违约金贷:银行存款 4 700习题八:管理费用=2000(4.1)+7980(4.2) +800(4.4)+100(4.5)+1000(4.7)+620(4.9)=12500财务费用=500(4.6)主营业务收入=20000(6.1)+40000(6.2)+20000(6.4)=80000 主营业务成本=48400(6.5)销售费用=1600(6.6)营业税金及附加=4000(6.7)其他业务收入=2000(7.1)其他业务成本=1800(7.2)营业外收入=5000(7.3)营业外支出=4700(7.4)1、借:主营业务收入 80000其他业务收入 2000营业外收入 5000贷:本年利润 870002、借:本年利润 73500贷:主营业务成本 48400其他业务成本 1800营业税金及附加 4000销售费用 1600管理费用 12500财务费用 500营业外支出 47003、本月利润总额=87000-73500=13500元本月应交所得税=13500×25%=3375元借:所得税费用 3375贷:应交税费——应交所得税 33754、借:本年利润 3375贷:所得税费用 33755、净利润=13500-3375=10125元提取法定盈余公积=10125×10%=1012.5元提取任意盈余公积=10125×5%=506.25元借:利润分配——提取法定盈余公积 1012.5——提取任意盈余公积 506.25 贷:盈余公积----法定盈余公积 1012.5 ----任意盈余公积 506.256、借:利润分配—应付现金股利 3000贷:应付股利 3000习题九1、借:银行存款 200000贷:短期借款 2000002、借:固定资产 120000贷:实收资本(或股本) 1200003、借:财务费用 2500贷:应付利息 25004、借:应付账款 45000贷:银行存款 450005、借:其他应收款——张三 1000预借差旅费贷:库存现金 10006、借:短期借款 40000应付利息 1800贷:银行存款 418007、借:固定资产 36000贷:银行存款 360008、借:预付账款 80000贷:银行存款 800009、借:在途物资——乙材料 100000——丙材料 200000应交税费——应交增值税(进项税额) 51000贷:银行存款 300000 应付账款 5100010、运杂费分配率=6000/(100000+200000)=0.02乙材料分摊:0.02×100000=2000丙材料分摊:0.02×200000=4000借:在途物资——乙材料 2000——丙材料 4000贷:银行存款 600011、借:原材料——乙材料 102000——丙材料 204000贷:在途物资——乙材料 102000——丙材料 204000验收入库后才成为原材料12、借:在途物资——甲材料 102000应交税费——应交增值税(进项税额) 17000贷:预付账款 80000银行存款 3900013、借:库存现金 30000取钱用于发工资贷:银行存款 30000借:应付职工薪酬—工资 30000贷:库存现金 3000014、借:生产成本——A产品 150000——B产品 60000制造费用 20000管理费用 10000贷:原材料——甲材料 150000——乙材料 30000——丙材料 6000015、借:生产成本——A产品 15000——B产品 10000制造费用 3000管理费用 2000贷:应付职工薪酬—工资 3000016、借:制造费用 30000管理费用 20000贷:累计折旧 5000017、借:制造费用 800管理费用 400贷:银行存款 120018、借:制造费用 2700贷:银行存款 270019、借:管理费用 1500差旅费贷:其他应收款——张三 1000库存现金 50020、借:制造费用 1000管理费用 2000贷:库存现金 300021、借:销售费用 10000广告费贷:银行存款 1000022、借:银行存款 500000贷:预收账款 50000023、制造费用合计=20000(14)+3000(15)+30000(16)+800(17)+2700(18)+1000(20)=57500 制造费用分配率=57500/(15000+10000)=2.3A产品分配:15000×2.3=34500B产品分配:10000×2.3=23000借:生产成本——A产品 34500——B产品 23000贷:制造费用 5750024、A产品完工产品成本=10000+(材料150000+工资15000+制造费用34500)-20000=189500(元) B产品完工产品成本= 0 + (材料60000+工资10000+制造费用23000)-4000=89000(元)借:库存商品——A 189500——B 89000验收入库贷:生产成本——A 189500——B 8900025、借:预收账款 702000贷:主营业务收入 600000应交税费——应交增值税(销项税额) 10200026、借:应收票据 351000贷:主营业务收入 300000应交税费——应交增值税(销项税额) 5100027、A产品每件入库成本=189500÷2000件=94.75元A产品销售成本=94.75×1500=142125(元)B产品每件入库成本=89000÷500件=178元B产品销售成本=178×300=53400(元)借:主营业务成本--A 142125--B 53400贷:库存商品——A 142125——B 5340028、借:营业税金及附加 20000贷:应交税费——应交消费税 2000029、借;银行存款 8000贷:营业外收入 800030、借:营业外支出 3000贷:银行存款 300031、借:银行存款 46800贷:其他业务收入 40000应交税费——应交增值税(销项税额) 6800借:其他业务成本 31000贷:原材料 3100032、主营业务收入=600000(25)+300000(26)=900000其他业务收入=40000(31)营业外收入=8000(29)主营业务成本=142125(27)+53400(27)=195525其他业务成本=31000(31)营业税金及附加=20000(28)销售费用=10000(21)管理费用=10000(14)+2000(15)+20000(16)+400(17)+1500(19)+2000(20)=35900 财务费用=2500(3)营业外支出=3000(30)借:主营业务收入 900000其他业务收入 40000营业外收入 8000贷:本年利润 948000借:本年利润 297925贷:主营业务成本 195525其他业务成本 31000营业税金及附加 20000销售费用 10000管理费用 35900财务费用 2500营业外支出 300033、利润总额=948000-297925=650075应交所得税=650075×25%=162518.75借:所得税费用 162518.75贷:应交税费——应交所得税 162518.75 借:本年利润 162518.75贷:所得税费用 162518.7534、净利润=650075-162518.75=487556.25借:利润分配——提取法定盈余公积 48755.63——提取任意盈余公积 24377.81 贷:盈余公积——法定盈余公积 48755.63——任意盈余公积 24377.8135、(1)借:利润分配——应付现金股利 243778.12 贷:应付股利 243778.12 (2)借:应付股利 243778.12贷:银行存款 243778.1236、借:本年利润 487556.25贷:利润分配——未分配利润 487556.2537、借:利润分配——未分配利润 316911.56贷:利润分配——提取法定盈余公积 48755.63——提取任意盈余公积 24377.81——应付现金股利 243778.12 未分配利润=487556.25-316911.56=170644.69。

新编会计学原理(李海波)第三章习答案

本月合计8792

本月合计8792

产品生产成本计算表

单位:元

成本项目

A产品(100件)

B产品(80件)

直接材料3225Leabharlann 32.252580

32.25

直接人工

5700

57

4560

57

制造费用

2065

20.65

1652

20.65

产品生产成本

10990

109.90

8792

109.90

(2)9000

(3)1260

(8)3717

(9)19782

本月合计19782

本月合计19782

借方生产成本——A产品贷方

(1)3225

(2)5000

(3)700

(9)2065

(9)10990

本月合计10990

本月合计10990

借方生产成本——B产品贷方

(1)2580

(2)4000

(3)560

(8)1652

——B产品1652

贷:制造费用3717

9、借:库存商品——A产品10990

——B产品8792

贷:生产成本——A产品10990

——B产品8792

借方制造费用贷方

(2)2000

(3)280

(4)600

(5)200

(6)400

(7)237

(8)3717

本月合计3717

本月合计3717

借方生产成本贷方

(1)5805

第三章习题二答案P133

8、本月制造费用总额:2000+280+600+200+400+237=3717

新编会计学原理第三章课后参考答案

新编会计学原理第三章课后参考答案习题⼀参考答案1、借:其他应收款——**采购员500贷:库存现⾦5002、借:材料采购——甲材料16000——⼄材料12800应交税费——应交增值税(进项税额)6800贷:应付票据33696 3、借:材料采购720贷:银⾏存款480库存现⾦2404、借:原材料——甲材料16480——⼄材料13040贷:材料采购295205、借:应付票据33696贷:银⾏存款336966、借:材料采购——甲材料5500——⼄材料5600应交税费——应交增值税(进项税额)1887贷:应付票据12987 7、借:材料采购720贷:银⾏存款540库存现⾦1808、借:原材料——甲材料5940——⼄材料5880贷:材料采购11820习题⼆参考答案1、借:⽣产成本——A产品3225——B产品2580贷:原材料5805 2、借:⽣产成本——A产品5000——B产品4000制造费⽤2000管理费⽤3000贷:应付职⼯薪酬14000 3、借:⽣产成本——A产品700——B产品560制造费⽤280管理费⽤420贷:应付职⼯薪酬1960 4、借:制造费⽤600管理费⽤300贷:累计折旧900 5、借:制造费⽤200贷:库存现⾦200 6、借:制造费⽤400贷:库存现⾦400 7、借:制造费⽤237库存现⾦63贷:其他应收款300 8、借:⽣产成本——A产品2065——B产品1652贷:制造费⽤3717 9、借:库存商品——A产品10990——B产品8792贷:⽣产成本19782习题三参考答案1、借:银⾏存款35100贷:主营业务收⼊——A产品30000 应缴税费——应交增值税5100 2、借:应收账款52650贷:主营业务收⼊——B产品45000应缴税费——应交增值税7650 3、借:主营业务成本57000贷:库存商品——A产品22500——B产品34500 4、借:销售费⽤1000贷:银⾏存款1000 5、借:销售费⽤1140 贷:应付职⼯薪酬1140 6、借:银⾏存款1404贷:其他业务收⼊1200应缴税费——应交增值税2047、借:其他业务成本1000贷:原材料——甲1000营业利润:75000—57000+1200—1000—1000—1140=16060=营业收⼊-营业成本-税⾦及附加-销售费⽤-管理费⽤-财务费⽤+投资收益营业税⾦及附加?习题四参考答案1、借:制造费⽤5000管理费⽤3000贷:应付职⼯薪酬80002、借:制造费⽤420管理费⽤700贷:应付职⼯薪酬11203、借:制造费⽤800管理费⽤600贷:累计折旧1400 4、借:管理费⽤1200贷:银⾏存款1200 5、借:管理费⽤400贷:库存现⾦400 6、借:管理费⽤300贷:库存现⾦300 7、借:管理费⽤480贷:库存现⾦480 8、借:销售费⽤1500贷:银⾏存款1500 9、借:财务费⽤900贷:银⾏存款900 10、借:销售费⽤700贷:银⾏存款600库存现⾦10011、借:管理费⽤1200贷:库存现⾦1200 12、借:管理费⽤960库存现⾦40贷:其他应收款1000 13、借:制造费⽤1900管理费⽤500贷:银⾏存款2400 14、借:管理费⽤1000 制造费⽤2000贷:银⾏存款3000习题五参考答案1、借:银⾏存款58500贷:主营业务收⼊50000应交税费—应交增值税8500 2、借:主营业务成本35000贷:库存商品35000税⾦及附加借:税⾦及附加5000贷:应交税费5000 3、借:销售费⽤500贷:库存现⾦500 4、借:管理费⽤300贷:银⾏存款300 5、借:财务费⽤2200贷:银⾏存款2200借:财务费⽤1000贷:应付利息1000借:应付利息1000财务费⽤1200贷:银⾏存款22006、借:营业外⽀出500贷:银⾏存款5007、借:其他应付款300贷:营业外收⼊300增值税??12⽉份利润总额=50000-35000-5000-500-300-2200+300-500=6800计算结转和分配利润4-1-①借:主营业务收⼊550000其他业务收⼊6000营业外收⼊4300贷:本年利润5603004-1-②借:本年利润462500贷:主营业务成本410000税⾦及附加5000销售费⽤25500管理费⽤3300财务费⽤4200其他业务成本3500营业外⽀出2000全年12个⽉份利润总额=560300—462500=97800(元)应交所得税:97800×25%=24450(元)4-2-①借:所得税费⽤24450贷:应交税费—应交所得税244504-2-②借:本年利润24450贷:所得税费⽤24450则净利润=97800-24450=73350(元)4-3借:本年利润73350贷:利润分配733504-4借:利润分配—提取法定盈余公积7335贷:盈余公积7335 4-5借:利润分配—提取任意盈余公积11002.5贷:盈余公积11002.5 4-6借:利润分配7335贷:应付股利7335.习题六参考答案1、借:银⾏存款400000贷:实收资本400000 2、借:固定资产150000贷:实收资本150000 3、借:银⾏存款50000贷:短期借款50000 4-1借:银⾏存款500000贷:长期借款5000004-2借:⼯程物资500000贷:银⾏存款500000 5、借:短期借款50000贷:银⾏存款500006-1借:固定资产清理120000累计折旧30000贷:固定资产150000 6-2借:长期股权投资130000贷:固定资产清理120000营业外收⼊10000 7-1借:固定资产清理20000累计折旧10000贷:固定资产30000 7-2借:银⾏存款20000贷:固定资产清理20000 8、借:应付职⼯薪酬3000贷:银⾏存款3000习题七参考答案1、借:⽣产成本——A产品21900——B产品18100贷:原材料40000 2、借:制造费⽤2000贷:原材料2000 3、借:库存现⾦30000贷:银⾏存款30000 4、借:应付职⼯薪酬24000贷:库存现⾦240005-1借:材料采购——甲14000应交税费——应交增值税2380贷:银⾏存款17380 5-2借:原材料14000贷:材料采购——甲14000 6、借:材料采购——⼄40000应交税费——应交增值税6800贷:应付票据46800借:原材料40000贷:材料采购——⼄40000 7-1借:材料采购——⼄600贷:库存现⾦600 7-2借:原材料——⼄40600贷:材料采购——⼄40600 8、借:银⾏存款3000贷:应收账款3000 9、借:应交税费1000贷:银⾏存款1000 10、借:⽣产成本——A产品10000——B产品10000制造费⽤3000管理费⽤1000贷:应付职⼯薪酬24000 11、借:⽣产成本——A产品1400——B产品1400制造费⽤420管理费⽤140贷:应付职⼯薪酬3360 12、借:制造费⽤2380管理费⽤780贷:累计折旧3160 13、借:制造费⽤1400贷:银⾏存款1400 14、借:⽣产成本——A产品4600——B产品4600贷:制造费⽤9200 15、借:库存商品——A产品37900贷:⽣产成本37900 16、借:应收账款——新华⼚131040贷:主营业务收⼊112000应交税费——应交增值税19040 17、借:主营业务成本——A产品36000——B产品44000贷:库存商品——A产品36000——B产品44000 18、借:销售费⽤1100贷:库存现⾦1100 19、借:财务费⽤5000贷:银⾏存款5000 20、借:管理费⽤1200贷:银⾏存款1200 21、借:税⾦附加5600。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

4

借:原材料8,000

贷:应付账款8,000

9

借:银行存款2,900

贷:应收账款2,900

5

借:固定资产2,000

贷:银行存款2,000

10

借:短期借款9,000

贷:银行存款9,000

(二)开设并登记T型账(没有发生额的省略):

借库存现金贷借银行存款贷

期初余额100

期初余额18,000

库存商品

10,000

10,000

生产成本

16,000

16,000

固定资产

450,000

2,000

452,000

短期借款

9,000

9,000

15,000

15,000

应付账款

4,000

12,000

8,000

应交税费

2,000

2,000

实收资本

450,000

450,000

盈余公积

32,000

32,000

本年利润

本期发生额2,000

期末余额0

期末余额0

账户名称

期初余额

本期发生额

期末余额

借方

贷方

借方

贷方

借方

贷方

库存现金

100

300

300

100

银行存款

18,000

17,900

25,300

0

其他应收款

1,000

300

1,300

原材料

26,000

8,000

16,000

18,000

1、300

2、300

6、15,000

9、2,900

1、300

3、2,000

5、2,000

7、12,000

10、9,000

本期发生额300

本期发生额300

本期发生额17,900

本期发生额25,300

期末余额100

期末余额10,600

借应收账款贷借其他应收款贷

期初余额2,900

期初余额1,000

9、2,900

期初余额9,000

5、2,000

10、9,000

6、15,000

本期发生额2,000

本期发生额9,000

本期发生额15,000

期末余额452,000

期末余额15,000

借应付账款贷

借应交税费贷

期初余额4,000

期初余额2,000

7、12,000

4、8,000

3、2,000

本期发生额12,000

本期发生额8,000

11,000

11,000

合计

508,000

508,000

67,500

67,500

508,000

508,000

2、300

本期发生额2,900

本期发生额300

期末余额0

期末余额1,300

借原材料贷

借生产成本贷

期初余额26,000

8、16,000

4、8,000

8、16,000

本期发生额8,000

本期发生额16,000

本期发生额16,000

期末余额18,000

期末余额16,000

借固定资产贷

借短期借款贷

期初余额450,000

第三章3-1:练习借贷记账法的运用

(一)编制会计分录:

题号

分录

题号

分录

1

借:库存现金300

贷:银行存款300

6

借:银行存款15,000

贷:短期借款15,000

2

借:其他应收款300

贷:库存现金300

7

借:应付账款12,000

贷:银行存款12,000

3

借:应交税费2,000

贷:银行存款2,000

8

借:生产成本16,000