普华永道--财务管理最佳实践之应付管理

{财务管理内部控制}工薪与人事循环内部控制了解和测试工作底稿讲解

中国注册会计师协会财务报表审计工作底稿培训班

二、工薪与人事循环内部控制了解 1. 了解和评价控制的设计-审计程序(7)

▪ 识别和了解相关控制(续)

为提高审计效率,如存在可以同时达到多个控制目 标的控制活动,可以考虑优先测试该控制活动。

如果某一项控制目标没有相关的控制活动或控制活 动设计不合理,应考虑被审计单位控制的有效性以及 其对拟采取的审计策略的影响

4. 影响的认定

▪ 受影响的相关交易和账户余额

▪ 受影响的认定

与交易相关的认定:

发生、完整性、准确性、截止、分类

与账户余额相关的认定

存在、权利和义务、完整性、计价和分摊

10

中国注册会计师协会财务报表审计工作底稿培训班

二、工薪与人事循环内部控制了解

1. 了解和评价控制的设计

2. 确定控制是否得以执行,包括穿行测 试

5

中国注册会计师协会财务报表审计工作底稿培训班

一、工薪与人事循环内部控制

3. 控制目标的确定与关键控制活动(2)

▪ 工作时间由管理层核准

6

中国注册会计师协会财务报表审计工作底稿培训班

一、工薪与人事循环内部控制

3. 控制目标的确定与关键控制活动(3)

17

中国注册会计师协会财务报表审计工作底稿培训班

二、工薪与人事循环内部控制了解 1. 了解和评价控制的设计-审计程序(6)

▪ 识别和了解相关控制(续)

针对同一控制目标可能存在多项控制活动,只需了

解并记录能够确保该控制目标实现的其中一项关键控 制活动。

应关注被审计单位采取的控制活动是否能够完全达 到相关的控制目标。在某些情况下,某些控制活动单 独执行时,并不能完全达到控制目标,这时需要识别 与该特定目标相关的额外的控制活动,并对其进行测 18

普华永道的财务预算管理内部资料精品文档

普华永道

2008.10

2.2 预算管理在企业管理中的重要性

预算管理的重要性表现于以下几个方面:

a 细化了公司整体战略发展目标和年度经营计划 长期的战略发展目标,需要细化为年度计划,年度计划需要分解至 各部门、各月份及各种经营活动

预算是关于企业在一定的时期内(一般为一年或一个既定的期间内)经营、财 务等方面的总体预测。包括:

业务方面的预算(如收入预算、采购预算、费用预算等) 财务方面的预算(如资本预算、资金预算、利润预算、现金流量

表预算、资产负债表预算等); 预算的编制与执行涉及各个部门的各项业务和经营活动。

预算的编制、执行与调整涉及企业所有部门及主要人员

准备预算的速度 准确度 编制预算的成本 关键评估指标

人员

业务知识 计划技巧 沟通能力 自我挑战

信息系统和基础数据

网上录入数据 避免数据重复录入 系统整合 合理的数据细致程度 统一的数据模型和会

计科目表

普华永道

2008.10 Slide 16

目录 2. 预算管理基本概念

全面预算管理是企业内部管理控制的一种方法。这一方法自从上个世纪20年代在美 国的通用电气、杜邦、通用汽车公司产生之后,很快就成了大型工商企业的标准作 业程序。从最初的计划、协调,发展到现在的兼具控制、激励、评价等功能为一体 的一种综合贯彻企业经营战略的管理机制,全面预算管理已处于企业内部控制的核 心地位。

表一般是根据营业预算、资本预算和现金预算的数据调整编制出来。

普华永道

2008.10 Slide 9

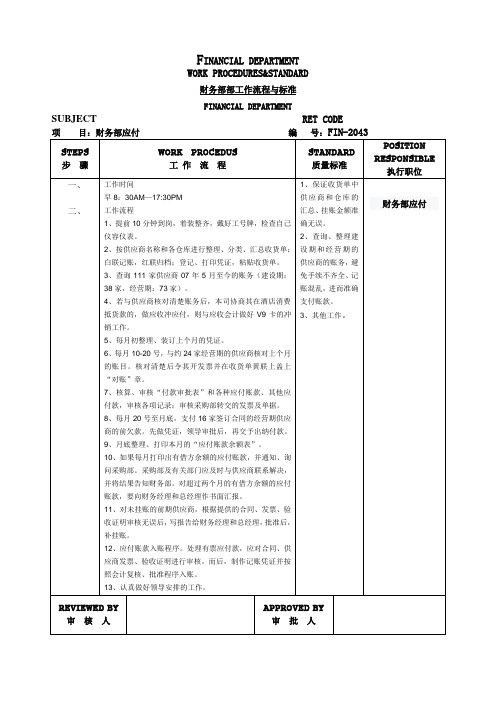

应付工作流程与标准

F INANCIAL DEPARTMENTWORK PROCEDURES&STANDARD财务部部工作流程与标准FINANCIAL DEPARTMENT SUBJECT RET CODE备注:请各部门根据本部门的实际运营情况,制定本部门的人员编制。

并根据部门人员编制岗位,详细写明所有岗位的工作流程与标准(上附样例仅供参考)应付账款管理制度财务管理制度-应付账款管理1、目的为规范财务操作,加强对应付账款的管理,保证应付账款的准确性和有序支付,特制定本制度。

2、范围本制度适用于公司有合同约束的长期或短期配套户,零时配套户的应付账款管理参照“财务管理制度-采购控制管理”3、职责部门配套科负责合同的签订、配套户的分类以及采购发票的签收,配套库负责配套户的结算,财务处负责配套户发票的挂账、付款计划的编制和货款的支付。

4、程序配套科在签订合同时需要明确标明付款时间与付款方式,并且根据配套户的实际情况对配套户进行分类,主要可分为A、B和C三类,A类和B类各限定六户,其余全部划归C类管理,配套科收到配套户所开发票后,需由科室指定专人签字后及时交财务处。

配套库每月根据本公司客户的出账数为配套户结算,填开《入库单》并标明所属月份及时交财务处。

财务处必须严格按照合同的规定对应付账款进行管理,配套户的发票必须在每月最后一天前送达本公司财务才可挂账,财务处接收发票时需仔细核对采购合同和《入库单》,价格或数量不符时,财务人员有权拒收;每月10日前(节假日顺延)财务处根据配套户发票的挂账情况以及采购合同和《入库单》编制当月付款计划,经总经理审批后,财务处据此付款,财务处在付款时需统筹兼顾,在任何情况下必须保留本公司自身的日常开支,在资金紧张的情况下,财务处根据配套科对配套户的分类顺序安排资金,资金充足的情况下集中时间统一办理。

5、维护为保证应付账款的准确性,财务处需定期(至少一个季度)查询公司技术质量处的质量扣款情况,并与配套户进行对账。

普华永道_富大集团SAP实施项目_004蓝图设计_财务管理FI_Scenario-FI-4 Petty Cash备用金管理流程

富大集团备用金管理流程页数.: 1 of 13模块 : FI作者: 林颐张良日期 : 08/07/20业务蓝图确认签署该文件定义了未来富大如何利用SAP R/3系统实现本业务操作。

项目小组富大集团普华永道关键用户顾问签署: __________________ ____________________ 流程确认富大集团签署: ___________________________________________________项目管理富大集团普华永道项目经理项目经理签署: __________________ ____________________富大集团备用金管理流程页数.: 2 of 13模块 : FI作者: 林颐张良日期 : 08/07/20流程说明:本流程主要描述如何在SAP系统里进行备用金管理,具体包括二方面的内容:一、公司备用金管理1.公司备用金申请流程;2.公司备用金弥补流程;二、工厂备用金管理1.工厂备用金申请流程;2.工厂备用金工厂报销流程;3.工厂备用金弥补流程对目前组织架构的改变:无改进要点:一、备用金使用范围:1、公司备用金是指经批准给予省级以上公司出纳的现金周转金,用于公司日常的费用报销及员工借款。

2、工厂备用金是指经批准给予分公司(属于二级法人的饲料工厂)出纳的现金周转金,用于分公司日常的费用报销。

分公司出纳定期向公司级以上财会部申报备用金使用情况表,并提交有关报销凭证由财会部审核和相关批准后付款弥补备用金。

富大集团备用金管理流程页数.: 3 of 13模块 : FI作者: 林颐张良日期 : 08/07/20二、备用金管理流程的操作建议:1.应制定富大集团的备用金管理制度,具体规定各省级公司及下属的饲料工厂备用金的额度和相关人员的批准权限,以及备用金的保管、报销规定等相关内容。

2.工厂备用金在SAP系统上的业务运作时,应注意备用金在工厂报销时,工厂会计只能先预制记帐凭证,当时不能直接过帐;而应在弥补备用金时,由公司财会部会计对已经批准的备用金支出进行预制凭证的过帐。

普华永道财务管理最佳实践之固定资产管理

Determine asset categories for internal and statutory purposes

Monitor asset maintenance charges

Apply insurance valuation to key assets

Ensure asset responsibility at BU level

Controls

Asset verification Asset valuation Acquisition and

disposal authorities

Measures

Number of assets maintained

Cost of department

Elapsed time to record asset

PwC175

3

Fixed Assets - Best Practice Features

Maintain fixed asset register

Control acquisitions and disposals

Manage periodic asset depreciation

Verify and value asset base

Variable asset valuation mechanisms eg historic, current replacement

Forecast asset depreciation for budget purposes

Variable depreciation rules for classes of assets

technical assumptions (most

212普华永道--财务管理最佳实践之应付管理

Optimisation of early payment discounts

Payment runs properly authorised

Consolidated periodic invoicing for high frequency suppliers

3

Period end processing and reporting

6

To

Integrated systems Electronic payment On-line matching Shared Service Centres or

outsourced services

PwC175b(1)

7

Accounts Payable - Critical Success Factors These are a summary of the key business requirements, which must be met to achieve the objectives.

Single supplier database Staff trained in AP process and have clear roles and responsibilities Payment terms defined and agreed with supplier Effective communication and feedback mechanisms in place to handle queries Establish and maintain good supplier relations Process in place for monitoring the status of invoices and payment schedules AP calendar in place and communicated to staff Authorisation levels and payment terms held on the system Automated workflow to route documents to relevant personnel when problems need to be

探索财务管理真经促进企业价值成长——记全国先进会计工作者韦秀长

探索财务管理真经促进企业价值成长——记全国先进会计工作者韦秀长追求卓越是他不变的信念和行动。

他矢志不移地追求卓越,11年为公司节约或挽回的损失超过18亿元,他在财务管理方面的研究和创新实践使他成为财会行业系统中的全国领军人物。

他就是——韦秀长,管理学博士,高级会计师,注册会计师,人事与社会保障部“新世纪百千万人才工程”国家级人选,财政部企业类全国会计领军(后备)人才,财政部会计领军(后备)人才(大赛班) 导师,财政部企业内部控制标准委员会咨询专家,中国会计学会资深会员、内部控制专业委员会委员,广西企业会计准则咨询专家,广西青年联合会常委。

现任中国联合网络通信有限公司广西分公司副总经理、党委委员,分管财务工作;2006年—2008年任中国联合通信有限公司广西分公司总会计师、党委委员。

作为33岁即走上特大型中央企业省级公司领导岗位的管理人员,韦秀长拥有多年的电信行业从业经历和丰富的财务管理经验,凭借其扎实的财务专业知识和丰富的市场管理经验,在公司风险控制、成本管控、辅助经营决策、创建良好的外部经营环境等工作中做出了重要贡献。

同时,作为行业领军人才,他参与了一系列财务领域的重要工作,在推动国家财务事业建设和行业人才建设方面也做出了一定的贡献;再者,作为单位主管财务的领导,在繁忙的工作之余,他紧密结合实际开展学术研究,取得了较大成就,其多项研究成果获国家级、省(部)级表彰。

在广西联通,韦秀长被誉为“企业的一个宝,一个财务好当家”。

他身上体现出的“诚实守信的品格、客观公正的意识、开放广阔的胸襟和进取创新的追求”正是对中国会计精神内涵的精彩诠释。

一、赴桂帮扶施展财智,助力企业脱困步入“快车道”多年来,韦秀长在各个阶段都取得了骄人的成绩。

早在大学时代,韦秀长就表现出全面发展的才能。

1996年被共青团中央、全国学联纳入“跨世纪人才”进行培养,并荣获首届“中国大学生跨世纪发展基金—建昊奖学金”奖励。

1997年被国家教委、共青团中央授予第三届全国“优秀学生干部”标兵,并获第二届“胡楚南优秀大学生”最佳奖。

普华永道财务管理最佳实践之应收管理

➢ Automatic reconciliation facilities between integrated SOP AR and GL systems

➢ Integrated systems to facilitate customer query handling

➢ Forecast cash receipts available for treasury purposes

➢ System provides on-line customer payment history and terms

➢ Use of workflow software to monitor process and help resolve queries

➢ Standard credit control reports

➢ Establish credit levels ➢ Issue sales order ➢ Issue invoice ➢ Monitor credit ➢ Collect cash

Accounts Receivable

Objectives

➢ To ensure customer payments are received efficiently and effectively for goods/services delivered, within the agreed terms and conditions

Accounts Receivable - Trends

From

➢ Separate AR module ➢ Payment by cheque ➢ Complex/variable trading terms ➢ Manual matching ➢ Performed by Finance department

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Single supplier database Staff trained in AP process and have clear roles and responsibilities Payment terms defined and agreed with supplier

PwC175b(1)

3

Accounts Payable - Best practice features

Maintain supplier details Process vouchers Process payments Period end processing and reporting

Process Features

Optimisation of early payment discounts

All transactions completed before period closed

Payment runs properly authorised

Segregation of duties between supplier set up, voucher processing and payment processing

PwC175b(1)

8

Accounts Payable - Appendix 1 : IDEF Process Flow

The diagram below provides a key to the process diagrams used in this document.

Controls (i.e. Procedures Standards Requirements for rework) Input (i.e. Information Material) Process / activity Output (i.e. Information Material)

Best Practice Financial Processes: Accounts Payable

2

Accounts Payable - Best Practice Objectives

Organisation People

Centralised processing Outsourcing potential

Automatic matching of invoice to order and goods received note (GRN) Interface with General Ledger, Purchasing, Fixed Assets and Project Accounting Use of workflow software to resolve queries and monitor process

Cost per purchase invoice processed £6

Invoice processing time in days 6 days 16 days 49 days

10 percentile

Median

90 percentile

Number of invoices received per month Number of suppliers Number of different terms and conditions Complexity of authorisation process Proportion of invoices automatically matched with PO's Number of supplier queries Proportion of invoices received electronically Proportion of payments made electronically

Accounts Payable Objectives

Supplier relations Creditor control

Processes

Maintaining supplier details Process vouchers Process payments Period end processing and reporting

Integration with General Ledger minimises reconciliation adjustments Transaction processing prevented for closed periods

Audit trail of changes to supplier payment details

PwC175b(1)

5

Accounts Payable - Measures/Cost drivers

Number of purchase invoices per FTE per annum 15,000 7,000 3,000 or less £2 £17 10 percentile 90 percentile Median 10 percentile 90 percentile Median Cost drivers

PwC175b(1)

4

Accounts Payable - Best practice features

Maintain supplier details Process vouchers Process payments Period end processing and reporting

Effective communication and feedback mechanisms in place to handle queries

Establish and maintain good supplier relations Process in place for monitoring the status of invoices and payment schedules AP calendar in place and communicated to staff Authorisation levels and payment terms held on the system Automated workflow to route documents to relevant personnel when problems need to be resolved Forward payment schedule to cashflow management Flexible matching criteria

Information Systems

Interface between Accounts Payable and other related processes Shared employee and supplier details System validation and approval checks

To maximise processing efficiency To ensure invoices are processed to agreed terms To ensure payments made only when due and payable To ensure liabilities are fully recorded and distributed correctly To achieve effective balance between extending credit and maintaining good relations with suppliers To take full advantage of opportunities to recover VAT

Reconciliation of Accounts Payable activity and reconciliation with General Ledger control account

Management reports run once period is finally closed

Electronic payments Default payment terms held on supplier file with manual override at P.O. and invoice Production of forward payment entry schedules to aid cash flow management Interface with General Ledger, Fixed Assets, Project Accounting and Cash Management Facility to suspend payments

Authorise and set up new suppliers payment details Maintain supplier payment details

Accounts payable process vouchers: invoices, expense claims, credit notes, debit memos and prepayment requests Suppliers required to use PO number on all documents and three way match wherever possible Consolidated periodic invoicing for high frequency suppliers