阿里优酷2014财报对比分析

阿里巴巴并购优酷财务整合绩效评价

三、财务整合绩效评价

2、成本降低:通过整合采购、生产、销售等环节,阿里巴巴降低了成本。例 如,优酷土豆的视频内容采购成本得到了有效控制,同时阿里巴巴还通过优化物 流和仓储等环节降低了运营成本。

二、并购背景介绍

二、并购背景介绍

2015年10月,阿里巴巴宣布以每股6.6美元的价格收购优酷土豆。这次并购 使得阿里巴巴能够进一步扩大其在数字媒体领域的市场份额,并加强其在在线视 频领域的地位。优酷土豆作为中国最大的视频分享网站之一,拥有庞大的用户群 体和丰富的视频资源。

三、财务整合绩效评价

三、财务整合绩效评价

4、实现资源共享

4、实现资源共享

在并购优酷土豆后,阿里巴巴可以借助优酷土豆的内容资源和用户群体,进 一步扩大自身的业务范围。同时,优酷土豆也可以借助阿里巴巴的电商资源和大 数据技术,提高自身的运营效率和市场竞争力。这种资源共享可以实现双方的互 利共赢,推动中国互联网行业的发展。

4、实现资源共享

2、提升市场竞争力

通过并购优酷土豆,阿里巴巴在视频领域的市场份额大幅增加,进一步巩固 了其在互联网行业的领导地位。优酷土豆拥有大量的优质内容资源,能够为阿里 巴巴提供更多元化的内容支持。这使得阿里巴巴在与竞争对手的竞争中具备了更 强的竞争优势。

3、提高盈利能力

3、提高盈利能力

阿里巴巴通过并购优酷土豆,能够通过在线视频广告、会员付费等多种方式 进行盈利。同时,优酷土豆的广告平台和数据管理技术能力,可以为阿里巴巴的 广告业务提供更好的支持,进一步提高广告收入。

2014年度视频网站年终总结-4页word资料

2014年度视频网站年终总结视频网站的内容来源无外乎两种模式,一是从外部获取,二是自力更生。

但如今高质量的综艺节目、电视剧、电影等的网络版权费用基本都为天价――以网络独播剧为例,从2009年到2014年,版权价格从2万元一集涨到200万元,5年间涨了100倍。

而与此同时,电视平台也越来越不满足于仅靠版权费用赚“外快”――相较于视频网站对电视观众的分流和对广告主的攫取,版权“外快”显得微不足道。

于是,央视和湖南卫视率先宣布“独播不分销”战略,其他电视平台也都陆续收回了对众多热播内容的播放权,独播战略大行其道。

再者,广电总局对海外节目版权的引进实行紧缩政策,加强监管,导致内容引进模式式微。

“外援”缩紧,视频网站只能克服对原有内容来源的强依赖性,选择自力更生。

为了避开版权壁垒,各家视频网站便都押宝在了“自制”上。

搜狐CEO张朝阳在《?潘磕惺?4》开机发布会上将2014年定义为视频网站的“大自制元年”,将自制作为年度战略来抓。

实则,各大视频网站在自制方面也都铆足了劲,投入不断攀高:2014年搜狐针对自制的投入是2013年的2倍;优酷土豆在2014年投入3亿元做自制;乐视网对自制剧的预算投入占到每年10亿元内容投资的10%-15%,2015年增加到1/3左右。

一方面,这一年各大网站的网络自制剧突破了50部达到1200集的体量,自制节目突破100档大关;另一方面,巨额的成本投入、专业化的制作团队、明星导演和演员的加入,让网络自制内容彻底改头换面,摘掉了“低品质、粗制滥造”的标签。

可以说,“大自制元年”,实至名归。

优酷土豆2014年4月,优酷土豆集团与阿里巴巴集团宣布建立战略投资与合作伙伴关系;6月,根据CNNIC发布的《中国网民网络视频应用研究报告》显示,优酷土豆集团稳居中国视频行业第一;11月,优酷土豆集团在上海宣布与小米公司达成资本和业务方面的战略合作。

优酷土豆自合并成立之初就确立了第一的地位,在顺利度过合并期和优化期后,优酷土豆整合PC、移动端的数据,2014年其多屏月独立访问用户数和移动端日均视频播放量双双突破5亿,以70.4%的用户规模遥遥领先行业。

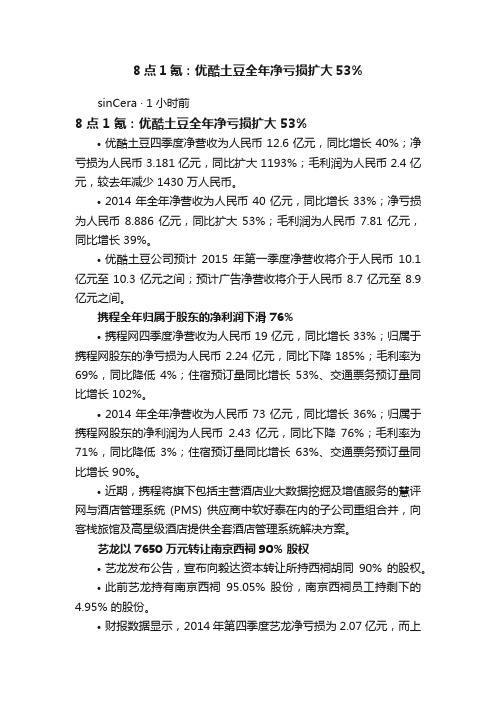

8点1氪:优酷土豆全年净亏损扩大53%

8点1氪:优酷土豆全年净亏损扩大53%sinCera · 1小时前8 点 1 氪:优酷土豆全年净亏损扩大 53%•优酷土豆四季度净营收为人民币 12.6 亿元,同比增长 40%;净亏损为人民币 3.181 亿元,同比扩大 1193%;毛利润为人民币 2.4 亿元,较去年减少 1430 万人民币。

•2014 年全年净营收为人民币 40 亿元,同比增长 33%;净亏损为人民币 8.886 亿元,同比扩大 53%;毛利润为人民币 7.81 亿元,同比增长 39%。

•优酷土豆公司预计2015 年第一季度净营收将介于人民币10.1 亿元至 10.3 亿元之间;预计广告净营收将介于人民币 8.7 亿元至 8.9 亿元之间。

携程全年归属于股东的净利润下滑 76%•携程网四季度净营收为人民币 19 亿元,同比增长 33%;归属于携程网股东的净亏损为人民币 2.24 亿元,同比下降 185%;毛利率为69%,同比降低4%;住宿预订量同比增长53%、交通票务预订量同比增长 102%。

•2014 年全年净营收为人民币 73 亿元,同比增长 36%;归属于携程网股东的净利润为人民币2.43 亿元,同比下降76%;毛利率为71%,同比降低3%;住宿预订量同比增长63%、交通票务预订量同比增长 90%。

•近期,携程将旗下包括主营酒店业大数据挖掘及增值服务的慧评网与酒店管理系统(PMS) 供应商中软好泰在内的子公司重组合并,向客栈旅馆及高星级酒店提供全套酒店管理系统解决方案。

艺龙以 7650 万元转让南京西祠 90% 股权•艺龙发布公告,宣布向毅达资本转让所持西祠胡同90% 的股权。

•此前艺龙持有南京西祠95.05% 股份,南京西祠员工持剩下的4.95% 的股份。

•财报数据显示,2014 年第四季度艺龙净亏损为 2.07 亿元,而上一年同期净亏损为 0.44 亿元。

Google 发布 Android Auto 应用•Android Auto 最早亮相于去年六月。

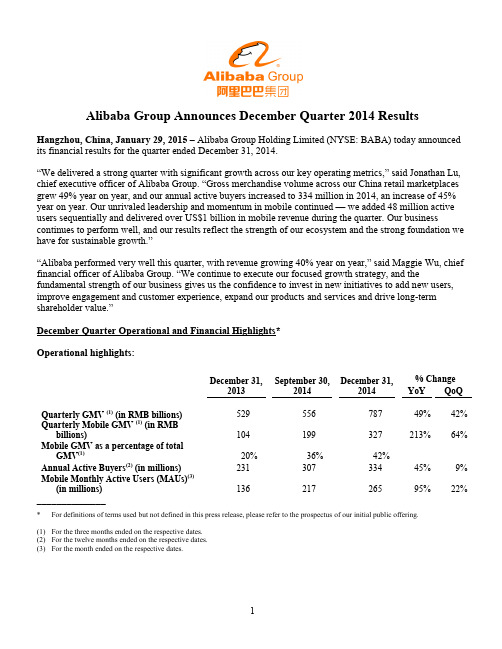

阿里巴巴2014年第四季度财务报表

Alibaba Group Announces December Quarter 2014 Results Hangzhou, China, January 29, 2015– Alibaba Group Holding Limited (NYSE: BABA) today announced its financial results for the quarter ended December 31, 2014.“We delivered a strong quarter with significant growth across our key operating metrics,” said Jonathan Lu, chief executive officer of Alibaba Group. “Gross merchandise volume across our China re tail marketplaces grew 49% year on year, and our annual active buyers increased to 334 million in 2014, an increase of 45% year on year. Our unrivaled leadership and momentum in mobile continued — we added 48 million active users sequentially and delivered over US$1 billion in mobile revenue during the quarter. Our business continues to perform well, and our results reflect the strength of our ecosystem and the strong foundation we have for sustainable growth.”“Alibaba performed very well this quarter, with revenue growing 40% year on year,” said Maggie Wu, chief financial officer of Alibaba Group. “We continue to execute our focused growth strategy, and the fundamental strength of our business gives us the confidence to invest in new initiatives to add new users, improve engagement and customer experience, expand our products and services and drive long-term shareholder value.”December Quarter Operational and Financial Highlights*Operational highlights:December 31,2013 September 30,2014December 31,2014% ChangeYoY QoQQuarterly GMV (1) (in RMB billions)529 556 787 49% 42% Quarterly Mobile GMV (1) (in RMBbillions)104 199 327 213% 64% Mobile GMV as a percentage of totalGMV(1)20% 36% 42%Annual Active Buyers(2) (in millions)231 307 334 45% 9% Mobile Monthly Active Users (MAUs)(3)(in millions) 136 217 265 95% 22% ______________* For definitions of terms used but not defined in this press release, please refer to the prospectus of our initial public offering.(1)For the three months ended on the respective dates.(2)For the twelve months ended on the respective dates.(3)For the month ended on the respective dates.Financial highlights:Three months ended December 31,2013 2014RMB RMB US$⑤YoY % Change(in millions, except percentages and per shareamounts)Revenue18,745 26,179 4,219 40% Mobile Revenue 1,171 6,420 1,035 448% Income from Operations 8,801 9,347 1,506 6%Non-GAAP EBITDA⑤⑤11,246 15,103 2,434 34%Non-GAAP EBITDA Margin⑤⑤60% 58% 58%Net Income 8,357 5,983 964 (28%)⑤⑤⑤Non-GAAP Net Income⑤⑤10,463 13,115 2,114 25% Diluted Earnings per Share/ADS(EPS) 3.55 2.29 0.37 (35%)⑤⑤⑤Non-GAAP Diluted EPS⑤⑤ 4.45 5.05 0.81 13%_______________⑤This release contains translation of certain Renminbi (“RMB”) amounts into U.S. dollars (“US$”) for the convenience of the reader, unlessotherwise stated, all translations of RMB into US$ were made at RMB6.2046 to US$1.00, the exchange rate set forth in the H.10 statistical release of the Federal Reserve Board on December 31, 2014. The percentages stated in this release are calculated based on the RMB amounts.⑤⑤See the sections entitled “Non-GAAP Financial Measures” and “Reconciliati on of Non-GAAP Measures to the Nearest Comparable GAAPMeasures” for more information about the non-GAAP measures referred to within this release.⑤⑤⑤D ecrease primarily due to an increase in share-based compensation expense, a one-time charge for financing-related fees and an increase inincome tax expenses in the quarter ended December 31, 2014, as discussed in detail below.GMV –GMV transacted on our China retail marketplaces in the quarter ended December 31, 2014 wasRMB787 billion (US$127 billion), an increase of 49% compared to the same quarter of 2013, and compared to RMB556 billion in the quarter ended September 30, 2014, representing a net addition of RMB231 billion GMV in three months. GMV transacted on Taobao Marketplace in the quarter ended December 31, 2014 was RMB494 billion (US$80 billion), an increase of 43% compared to the same quarter of 2013. GMV transacted on Tmall in the quarter ended December 31, 2014 was RMB293 billion (US$47 billion), an increase of 60% compared to the same quarter of 2013. The GMV growth was primarily driven by an increase in the number of active buyers and also partially attributable to category expansion, for example, auction transactions. On November 11, 2014, our Singles Day promotion generated GMV settled through Alipay of RMB57 billion (US$9.2 billion) on our China and international retail marketplaces within a 24-hour period, an increase of 58% compared to the Singles Day in 2013.Mobile GMV –Mobile GMV in the quarter ended December 31, 2014 was RMB327 billion (US$53 billion), an increase of 213% compared to the same quarter of 2013. Mobile GMV accounted for 42% of total GMV transacted on our China retail marketplaces in this quarter, compared to 36% in the quarter ended September 30, 2014 and 20% in the same quarter of 2013. The growth was primarily driven by an increase in the monthly active users accessing our platforms through mobile devices and an increase in the level of their spending.Annual active buyers–Our China retail marketplaces had 334 million annual active buyers in the twelve months ended December 31, 2014, compared to 307 million in the twelve months ended September 30, 2014 and 231 million in the twelve months ended December 31, 2013, representing an increase of 45% compared to the same period in 2013. The growth in annual active buyers was driven by an increase in active buyers throughout China, with substantially faster growth from lower tier cities.Mobile MAUs–Mobile MAUs grew to 265 million in the month ended December 31, 2014, compared to 217 million in the month ended September 30, 2014, representing a record high net addition of 48 million MAUs in three months, and a 95% increase from 136 million in the month ended December 31, 2013. According to iResearch, our Mobile Taobao App continues to be the No. 1 e-commerce app in China, demonstrating our ability to attract mobile users with strong purchasing intent on a large scale.Revenue–Revenue increased by 40% to RMB26,179 million (US$4,219 million) in the quarter ended December 31, 2014, compared to RMB18,745 million in the same quarter of 2013. Revenue from the China commerce retail business increased by 32% to RMB21,275 million (US$3,429 million), compared toRMB16,149 million in the same quarter of 2013, mainly driven by the growth in commission revenue and online marketing services revenue. Mobile revenue from the China commerce retail business increased by 448% to RMB6,420 million (US$1,035 million) in the quarter ended December 31, 2014, compared to RMB1,171 million in the same quarter of 2013, primarily due to a greater proportion of GMV generated on mobile devices and an increase in the mobile monetization rate.Income from operations – Income from operations in the quarter ended December 31, 2014 was RMB9,347 million (US$1,506 million), an increase of 6% compared to RMB8,801 million in the same quarter of 2013. Operating income growth was lower than revenue growth primarily due to an increase in share-based compensation expense (as discussed in “Share-based compensation expense” below).Non-GAAP EBITDA–Non-GAAP EBITDA increased by 34% to RMB15,103 million (US$2,434 million) in the quarter ended December 31, 2014, compared to RMB11,246 million in the same quarter of 2013. Non-GAAP EBITDA margin was 58% in the quarter ended December 31, 2014, compared to 60% in the December quarter of 2013. The year-on-year decrease in non-GAAP EBITDA margin was primarily due to the consolidation of newly acquired businesses, mainly UCWeb Inc., or UCWeb, and AutoNavi Holding Limited, or AutoNavi, and investments in new business initiatives, such as our mobile operating system, local services and digital entertainment. The quarter-on-quarter increase in non-GAAP EBITDA margin from 51% in the quarter ended September 30, 2014 was primarily due to operating leverage in this seasonally strong quarter.Net income –Our net income in the quarter ended December 31, 2014 was RMB5,983 million (US$964 million), a decrease of 28% compared to RMB8,357 million in the same quarter of 2013. The decrease was primarily due to (i) an increase in share-based compensation expense (including the effect of “mark-to-market” accounting of share-based awards in an amount of RMB1,494 million (US$241 million)) (as discussed in “Share-based compensation expense” below), (ii) an RMB830 million (US$134 million) one-time charge for financing-related fees as a result of the early repayment of our US$8 billion bank borrowings (as discussed in “Interest expense” below), and (iii) an increase in income tax expenses, primarily due to the expiration of an enterprise income tax (“EIT”) exemption period for one of our major subsidiaries (as discussed in “Income tax expenses” below).Non-GAAP net income–Non-GAAP net income increased by 25% to RMB13,115 million (US$2,114 million) in the quarter ended December 31, 2014, compared to RMB10,463 million in the same quarter of 2013.Diluted EPS and non-GAAP diluted EPS –Diluted EPS in the quarter ended December 31, 2014 was RMB2.29 (US$0.37) on 2,588 million diluted shares outstanding, a decrease of 35% compared to RMB3.55 on 2,343 million diluted shares outstanding in the same quarter of 2013. Non-GAAP diluted EPS in the quarter ended December 31, 2014 was RMB5.05 (US$0.81) on 2,588 million diluted shares outstanding, an increase of 13% compared to RMB4.45 on 2,343 million diluted shares outstanding in the same quarter of 2013. The lower non-GAAP diluted EPS growth rate relative to non-GAAP net income growth rate was due to an increase in number of diluted shares outstanding in the quarter ended December 31, 2014 following the completion of our initial public offering in September 2014.December Quarter Financial ResultsRevenue –Revenue for the quarter ended December 31, 2014 was RMB26,179 million (US$4,219 million), an increase of 40% compared to RMB18,745 million in the same quarter of 2013. The increase was mainly driven by the continuing rapid growth of our China commerce retail business. The following table sets forth a breakdown of our revenue for the periods indicated.Three months ended December 31,2013 2014RMB% ofRevenue RMB US$% ofRevenueYoYChange (in millions, except percentages)China commerceRetail 16,149 86% 21,275 3,429 82% 32% Wholesale 612 3% 860 139 3% 41% Total China commerce 16,761 89% 22,135 3,568 85% 32% International commerceRetail 264 2% 554 89 2% 110% Wholesale 1,000 5% 1,209 195 5% 21% Total international commerce 1,264 7% 1,763 284 7% 39% Cloud computing and Internetinfrastructure 196 1% 362 58 1% 85% Others 524 3% 1,919 309 7% 266% Total 18,745 100% 26,179 4,219 100% 40% China commerce retail business –Revenue from our China commerce retail business in the quarter ended December 31, 2014 was RMB21,275 million (US$3,429 million), or 82% of total revenue, an increase of 32% compared to RMB16,149 million in the same quarter of 2013. The increase was mainly driven by the growth in commission revenue and online marketing services revenue. Commissionrevenue accounted for 37% of China commerce retail revenue in the quarter ended December 31, 2014, compared to 30% in the same quarter of 2013. Revenue growth during this period occurred in the context of and reflected an increase of 49% in GMV transacted on our China retail marketplaces, which was primarily driven by a 45% increase in the number of active buyers.The lower revenue growth relative to GMV growth was mainly a result of (i) the higher percentage of total GMV contributed by mobile GMV, which has a lower monetization rate compared to the non-mobile monetization rate, and (ii) lower pay-for-performance (“P4P”) monetization on the personal computer (“PC”) interface compared to the same quarter of 2013. The lower P4P monetization on PC was primarily caused by our continued efforts to improve user experience, which adversely affected cost per click. Our strong momentum in mobile and commitment to improving user experience may slow the growth rate of our online marketing services revenue in the near term, but we believe they will create significant value for both our users and our business in the longer term.Mobile revenue from the China commerce retail business in the quarter ended December 31, 2014 was RMB6,420 million (US$1,035 million), an increase of 448% compared to RMB1,171 million in the same quarter of 2013, representing 30% of our China commerce retail business revenue, compared to 29% in the quarter ended September 30, 2014 and 7% in the same quarter of 2013. The increase in mobilerevenue from the China commerce retail business was primarily due to a greater proportion of GMV generated on mobile devices and an increase in the mobile monetization rate.∙China commerce wholesale business –Revenue from our China commerce wholesale business in the quarter ended December 31, 2014 was RMB860 million (US$139 million), an increase of 41% compared to RMB612 million in the same quarter of 2013. The increase was due to an increase in average revenue from paying members and an increase in paying members.∙International commerce retail business –Revenue from our international commerce retail business in the quarter ended December 31, 2014 was RMB554 million (US$89 million), an increase of 110%compared to RMB264 million in the same quarter of 2013. The increase was primarily due to an increase in GMV transacted on AliExpress, partially attributable to AliExpress’ participation in our Singles Day promotion campaign on November 11, 2014 for the first time.∙International commerce wholesale business –Revenue from our international commerce wholesale business in the quarter ended December 31, 2014 was RMB1,209 million (US$195 million), an increase of 21% compared to RMB1,000 million in the same quarter of 2013. The main reason for this increase was an increase in the number of paying members and an increase in average revenue from payingmembers.∙Others –Other revenue in the quarter ended December 31, 2014 was RMB1,919 million (US$309 million), an increase of 266% compared to RMB524 million in the same quarter of 2013. This increase was primarily due to the consolidation of revenue from acquired business (mainly UCWeb and AutoNavi) and an increase in interest income generated by our SME loan business. When the restructuring of our relationship with Ant Financial closes, which we expect in the March 2015 quarter, we will no longer consolidate revenue generated by the SME loan business in our financial results.Cost of revenue –Cost of revenue in the quarter ended December 31, 2014 was RMB7,520 million(US$1,212 million), or 29% of revenue, compared to RMB4,171 million, or 22% of revenue, in the same quarter of 2013. The increase was primarily due to an increase in share-based compensation expense (as discussed in “Share-based compensation expense” below), an increase in costs associated with our new businesses initiatives, and an increase in payment processing fees resulting from an increase in GMV transacted on our retail marketplaces.Product development expenses – Product development expenses in the quarter ended December 31, 2014 were RMB3,083 million (US$497 million), or 12% of revenue, compared to RMB1,707 million, or 9% of revenue in the same quarter of 2013. The increase was primarily due to an increase in share-based compensation expense (as discussed in “Share-based compensation expense” below). The increase was partially offset by the decrease in royalty fees paid to Yahoo which terminated upon completion of our initial public offering in September 2014.Sales and marketing expenses –Sales and marketing expenses in the quarter ended December 31, 2014 were RMB3,021 million (US$487 million), or 12% of revenue, compared to RMB1,897 million, or 10% of revenue in the same quarter of 2013. The increase was primarily due to an increase in share-based compensation expense (as discussed in “Share-based compensation expense” below). The increase was alsodue to the consolidation of marketing expenses of acquired business (mainly UCWeb and AutoNavi), an increase in advertising and promotional spending mainly to strengthen marketing of our Taobao and Tmall brands, especially in lower tier cities, as well as to promote our new businesses initiatives (e.g., local services) during this quarter.General and administrative expenses – General and administrative expenses in the quarter ended December 31, 2014 were RMB2,419 million (US$390 million), or 9 % of revenue, compared to RMB2,046 million, or 11% of revenue in the same quarter of 2013. The decrease in general and administrative expenses as a percentage of revenue was primarily due to a one-time equity-settled donation expense of RMB1,269 million made in the quarter ended December 31, 2013 relating to the grant of options to purchase 50,000,000 of our ordinary shares to a non-profit organization, which was partially offset by an increase in share-based compensation expense in the quarter ended December 31, 2014 (as discussed in “Share-based compensation expense” below).Share-based compensation expense – Share-based compensation expense included in respective cost or expense items above in the quarter ended December 31, 2014 was RMB4,313 million (US$695 million), or 16% of revenue, an increase of 554% compared to RMB659 million, or 4% of revenue, in the same quarterof 2013. The increase was primarily caused by (1) performance-based and retention grants of share-based awards granted prior to our initial public offering in 2014, with vesting periods of four years for our employees and six years for senior management, (2) the “mark-to-market” accounting of (i) share-based awards we granted to the employees of Zhejiang Ant Small and Micro Financial Services Company Ltd., or Ant Financial, and (ii) Ant Financial’s share-based awards granted by a major shareholding entity of Ant Financial controlled by Jack Ma, our executive chairman, to our employees. The expense arising from such Ant Financial share-based awards granted to our employees represents a non-cash accounting charge to us that will not result in any equity dilution to our shareholders. Without the effect of such “mark-to-market” accounting, our share-based compensation expense would have been RMB2,819 million (US$454 million) in the quarter ended December 31, 2014, compared to RMB2,233 million in the quarter ended September 30, 2014. Pursuant to generally accepted accounting principles in the United States, we are required to perform such re-measurement at each period end. Accordingly, we expect that our share-based compensation expense will continue to be affected by changes in the fair value of our share-based awards as well as the fair value of Ant Financial’s share-based awards granted to our employees.Amortization of intangible assets – Amortization of intangible assets in the quarter ended December 31, 2014 was RMB614 million (US$99 million), a significant increase from RMB123 million in the same quarter of 2013. This increase was due to an increase in intangibles assets primarily as a result of our strategic acquisitions, mainly UCWeb and AutoNavi.Income from operations – Income from operations in the quarter ended December 31, 2014 was RMB9,347 million (US$1,506 million), an increase of 6% compared to RMB8,801 million in the same quarter of 2013. The lower growth of operating income relative to revenue growth in this quarter and the decrease in operating margin to 36% in the quarter ended December 31, 2014 from 47% in the same quarter of 2013 were primarily due to an increase in share-based compensation expense (as discussed in “Share-based compensation expense” above).Non-GAAP EBITDA – Non-GAAP EBITDA increased by 34% to RMB15,103 million (US$2,434 million) in the quarter ended December 31, 2014, compared to RMB11,246 million in the same quarter of 2013.Non-GAAP EBITDA margin was 58% in the quarter ended December 31, 2014, compared to 60% in the December quarter of 2013. The year-on-year decrease in non-GAAP EBITDA margin was primarily due to the consolidation of newly acquired businesses, mainly UCWeb and AutoNavi, and investments in new business initiatives, such as our mobile operating system, local services and digital entertainment. Thequarter-on-quarter increase in non-GAAP EBITDA margin from 51% in the quarter ended September 30, 2014 was primarily due to operating leverage in this seasonally strong quarter. A reconciliation of operating income to non-GAAP EBITDA is included at the end of this release.Interest and investment income, net – Interest and investment income, net in the quarter ended December 31, 2014 was RMB313 million (US$51 million), an increase of 6% compared to RMB296 million in the same quarter of 2013. The increase was primarily due to an increase in interest income as a result of higher cash balance during the period, which in turn was primarily due to the proceeds from our initial public offering in September 2014 and an increase in operating cash flow. This increase was partially offset by an increase in impairment charge of cost-method investments and losses recognized with respect to the periodic revaluation of convertible bonds we held in connection with our strategic investments in publicly traded entities.Interest expense –Interest expense in the quarter ended December 31, 2014 was RMB1,344 million(US$216 million), an increase of 247% compared to RMB387 million in the same quarter of 2013. The increase was primarily due to an RMB830 million (US$134 million) one-time charge for financing-related fees as a result of the early repayment of our US$8 billion bank borrowings with proceeds from our issuance of US$8 billion senior unsecured notes in this quarter.Other income, net –Other income, net in the quarter ended December 31, 2014 was RMB901 million (US$145 million), an increase of 64% compared to RMB548 million in the same quarter of 2013. The increase was primarily due to an increase of RMB101 million (US$16 million) in royalty fees and software technology service fees received from Ant Financial to RMB344 million (US$55 million) in the quarter ended December 31, 2014 from RMB243 million in the same quarter of 2013 as a result of an increase in pre-tax income of Ant Financial, as well as an increase in government grants received from central and local governments in connection with our contribution to technology development and investments in local business districts.Income tax expenses – Income tax expenses in the quarter ended December 31, 2014 were RMB2,429 million (US$392 million), an increase of 228% compared to RMB741 million in the same quarter of 2013. The increase was primarily due to the increase in taxable income from our operations in China. Our effective tax rate increased to 26% in the quarter ended December 31, 2014 from 8% in the same quarter of 2013. Excluding share-based compensation expense, impairment of goodwill, intangible assets and investments, and unrealized gain/loss on investments which are not deductible or assessable for income tax purposes, our effective tax rate would have been 17% in the quarter ended December 31, 2014, compared to 7% in the same quarter of 2013. The increase was primarily due to the expiration of an EIT exemption period for one of our major subsidiaries, upon which the subsidiary became subject to an EIT rate of 12.5% (or 50% of the statutory EIT rate) in calendar year 2014.Net income and non-GAAP net income –As a result of the foregoing, our net income in the quarter ended December 31, 2014 was RMB5,983 million (US$964 million), a decrease of 28% compared to RMB8,357 million in the same quarter of 2013. Excluding the effects of share-based compensation expense, impairment of goodwill and investment in equity investees, the one-time charge for financing-related fees, amortization of intangible assets and certain other items, non-GAAP net income in the quarter ended December 31, 2014 was RMB13,115 million (US$2,114 million), an increase of 25% compared to RMB10,463 million in the same quarter of 2013. A reconciliation of net income to non-GAAP net income is included at the end of this release.Net income attributable to ordinary shareholders – Net income attributable to ordinary shareholders in the quarter ended December 31, 2014 was RMB5,936 million (US$957million), a decrease of 28% compared to RMB8,266 million in the same quarter of 2013.Diluted EPS and non-GAAP diluted EPS –Diluted EPS in the quarter ended December 31, 2014 was RMB2.29 (US$0.37) on 2,588 million diluted shares outstanding, a decrease of 35% compared to RMB3.55 on 2,343 million diluted shares outstanding in the same quarter of 2013. Excluding the effects of share-based compensation expense, impairment of goodwill and investment in equity investees, the one-time charge for financing-related fees, amortization of intangible assets and certain other items, non-GAAP diluted EPS in the quarter ended December 31, 2014 was RMB5.05 (US$0.81), an increase of 13% compared to RMB4.45 in the same quarter of 2013. The lower non-GAAP diluted EPS relative to non-GAAP net income growth rate was due to an increase in the number of diluted shares outstanding in the quarter ended December 31, 2014 following the completion of our initial public offering. A reconciliation of diluted EPS to the non-GAAP diluted EPS is included at the end of this release.Cash –As of December 31, 2014, cash, cash equivalents and short-term investments were RMB130,741 million (US$21,071 million), compared to RMB43,632 million as of March 31, 2014.Cash flow from operating activities and free cash flow – Net cash provided by operating activities in the quarter ended December 31, 2014 was RMB19,408 million (US$3,128 million), an increase of 30% compared to RMB14,922 million in the same quarter of 2013. Capital expenditures in the quarter ended December 31, 2014 were RMB1,513 million (US$244 million), compared to RMB1,601 million in the same quarter of 2013. Capital expenditures in the quarter ended December 31, 2014 included cash outflow for acquisition of land use rights and construction in progress of RMB291 million (US$47 million). Free cash flow, a non-GAAP measurement of liquidity, in the quarter ended December 31, 2014 was RMB22,924 million (US$3,695 million), an increase of 34% compared to RMB17,163 million in the same quarter of 2013. A reconciliation of net cash provided by operating activities to free cash flow, a non-GAAP measure of liquidity, is included at the end of this release.Net cash used in investing activities – During the quarter ended December 31, 2014, net cash used in investing activities of RMB4,817 million (US$776 million) mainly included disbursements for short-term investments of RMB1,944 million (US$313 million), capital expenditure of RMB1,513 million (US$244 million) as well as investment and acquisition activities of RMB2,657 million (US$428 million) primarily in mobile and logistics related businesses.Employee number – As of December 31, 2014, we had a total of 34,081 employees, compared to 33,239 as of September 30, 2014 and 20,884 as of December 31, 2013.Webcast and Conference Call InformationA live webcast of the earnings conference call, which will be held shortly following the release of this announcement, can be accessed at /en/ir/earnings. An archived webcast will be available through the same link following the call. A replay of the conference call will be available for one week (dial-in number: +1 646-254-3697; conference ID: 65377381).Please visit Alibaba Group’s Investor Relations website at /en/ir/home on January 29, 2015 to view the earnings release and accompanying slides prior to the conference call.About Alibaba Group。

三大运营商2014年财报

三大运营商2014年财报近日,三大运营商分别公布了2014年财报。

三张成绩单并不靓丽,甚至有些惨淡。

过去一年中,通信行业外受OTT跨界竞争,内受营改增、网间结算调整的拖累,光景并不好。

内忧外患之下,运营商的营收和利润都受到严重抑制。

如何扭转颓势?运营商必须抓住流量这根救命稻草。

电信联通微增,移动下滑总览三大运营商的财报,2014年,中国移动营收6414亿元,同比增长1.8%,其中,通信服务收入5818亿元,同比下降1.5%。

净利润1093亿元,同比下降10.2%。

中国电信营收3244亿元,同比增长0.9%,通信服务收入2874亿元,同比增长3.1%,其中,移动业务收入1516亿元,同比增长0.3%,固网业务收入1728亿元,同比增长1.4%。

净利润177亿元,同比增长0.8%。

中国联通营收2847亿元,同比下降3.5%,通信服务收入2449亿元,同比增长2.6%,其中,移动业务收入1551亿元,同比增长2.6%;固网业务收入885亿元,同比增长2.3%。

净利润121亿元,同比增长15.8%。

仅从财务数字上看,2014年,运营商营收增长明显放缓,中国移动甚至出现负增长。

在利润方面,中国移动连续两年下滑,中国电信只微增长,中国联通的增长幅度也快速下滑。

语音收入锐减,数据难填平如此惨淡的财务表现,真的让人为通信行业捏把汗。

究其原因,运营商的业绩与通信行业大环境有关。

2014年,通信行业已经进入新常态:一方面,三大运营商的主要收入由语音转向数据。

运营商的数据业务受到OTT的激烈竞争,逐渐被管道化。

财报显示,2014年,中国移动语音业务收入3090亿元,减少467亿元,数据业务收入2531亿元,增加462亿元。

数据业务的增长未能填平语音业务的亏欠,这是中国移动营收减少的重要原因。

显然,在OTT的冲击下,中国移动没能给数据卖个好价钱。

与中国移动一样,其他两家运营商也面临语音业务下滑的状况。

中国电信固网语音业务收入336亿元,减少50亿元,移动语音业务收入547亿元,减少35亿元;中国联通的固定电话用户也由8764万户下降到8206万户,损失558万户。

2014年互联网视频分析报告

2014年互联网视频分

析报告

2014年7月

目录

一、网络视频前景广阔 (3)

1、网络视频行业总体市场规模保持上升,增速放缓 (3)

2、“宽带中国”战略提升互联网普及率 (4)

3、网络视频用户持续增长,使用率回升 (5)

4、网络视频行业收入构成 (6)

(1)广告 (7)

(2)版权分销 (9)

(3)付费 (10)

5、智能电视 (11)

二、行业成长驱动力:外延并购增厚业绩 (13)

1、并购对传媒企业的成长贡献度较高 (13)

2、电影与娱乐、广告营销子行业并购最为活跃 (15)

三、投资主线 (16)

1、网络视频行业盈利增长预期带来的投资机会 (16)

2、并购成为传媒行业业绩与股价增长的主要驱动力 (16)

四、重点公司简况 (17)

1、乐视网 (17)

2、华策影视 (18)

一、网络视频前景广阔

1、网络视频行业总体市场规模保持上升,增速放缓

随着互联网的普及与发展,网络在线视频因其内容的丰富、点播观看的便捷性被越来越多的人们所接受,从2009 年以来,市场规模不断上升,至2011 年规模增长率达到100%,2012 年起增速回落至47%左右,预计今后几年将保持40%左右的增速稳健发展,行业总体市场规模不断上升。

从季度增长来看,2014 年Q1,中国网络视频行业市场规模达36.8 亿元,同比增长67.3%,环比增长-17.5%,虽然在每年的第一季度规模均有所下降,但总体仍然保持平稳上升的态势。

2014年双十一电子商务数据分析

双十一全网品牌排行

美的成功的分析

也许正是看到了毫无底线的价格战背后存在着 隐忧,美的生活电器自进入电商领域以来,一 直在努力提倡回归商业和产品的价值本质,合 理运用价格调控手段,以此来构建更健康的电 商市场环境。 为此,美的生活电器在“美的品牌周”等众多电 商促销活动中,都没有用低价格作为噱头,而 是回归产品价值、服务价值,用高品质、高性 价比的产品,以及完善的配套服务和物流体系 ,提升消费者网购体验。这种“价值战”模式为 它在电商取得成功奠定了基础。 其实,在今年双十一前提出“五好小家电”政策 ,就是美的生活电器电商价值战思潮的一种体 现。因为,价格好、品质好、服务好、物流好 、体验好这五大方面,几乎涵盖了网购全流程 ,不但可以全面升级消费者网购体验,还可以 加强消费者对品牌的记忆深度,从而提升品牌 口碑和市场影响力,这些是价值战带来的比销 售业绩更有价值的财富。

其他电商

1号店

截至上午10点,1号店全站成交额周环比增长8倍;截至11点,全站成 交额周环比增长9倍。 1号店全站销售环比增长6倍,和去年同期相比销售额翻番;双11当天, 1号店全站流量突破2188万。 1号店移动端销售额是去年同期的9倍,浏览量和订单占比是去年同期 的7倍。

当当:

双十一天猫销售额变化表

时间 00:00:75 00:02:53 00:14:02 00:38:28 0:50 1:00 1:34 7:17 7:36 9:44 10:51 12:00 12:33 12:59 13:20 13:31 15:29 19:25 21:12 23:12 24:00:00 销售额(亿元) 手机成交占比 10 50 100 113 122 145 200 207 260 300 327 340 350 358 362 400 463 500 550 571 手机成交额 (亿元) 1

细数2014视频行业“一波三折”

细数2014视频行业“一波三折”回顾2013年年底的那段时光,各大视频网站的内容争夺战不断,《好声音》、《爸爸去哪儿》等成功综艺新一季讲花落谁家成了行业讨论的热点,版权独播费纪录被不断刷新,几大关键词也从各大营销会上频频出现,力求有所创新的未来战略中还是免不了围绕内容为中心而攻城略地。

在内容之争上,各大网站依旧热情高涨,2014年发生了这许多的变故与风波让身为局外人的笔者都不得不感叹这一年视频行业发展的确是一波三折。

一波:挥泪辞旧迎新,行业整合末班车长江后浪推前浪,一代新人胜旧人。

2014年在视频网站中,不得不提及令人扼腕的快播,这个曾经的屌丝福利集中营最终还是走下了神坛,终究是败给了版权,尽管此前也曾努力洗白,却也回天无力了。

如果说2013年年底的那次服务器查扣是前戏,那么随着王欣的被抓就彻底宣告着快播真的已经离开了我们,而留给竞争者更多的则是对内容的敬畏。

除了快播以外,版权的余威也波及了国内的字幕网站,国内最早创立、影响最大的字幕组人人影视以及中文字幕交流平台射手网也都相继上演着曲尽人散的戏码。

对比关站后的门可罗雀,“卖身”或许还更体面些,还有可能可以重振旗鼓重获转机,但这只是可能。

4年前,人人网8000万美元收购56网,而4年后的今天,56网被作价1290万美元卖给搜狐视频,这是继优酷并购土豆,爱奇艺并购PPS之后的行业内并购的又一个里程碑。

人人网的业绩单上可以看出,对于养活56网,人人网的社交红利还是实力不够。

犹记得年初的时候搜狐视频掌门人张朝阳还曾对媒体称,“搜狐视频没有并购计划,会专注媒体娱乐的发展。

”面对现实与企业发展的需要,打脸有时也是必要的。

就连以“逐梦者”自称的盛大也将酷6 41%股份卖了,由语音视频文字聊天工具iSpeak的创始人许旭东接盘,交易完成后盛大占股约30%。

对于东家变化,酷6又将迎来新一轮人事变动。

被卖身的消息一经公开,酷6的命运就更添了几分多舛。

一直以来,视频行业都是个让企业爱恨交织的领域,至今盈利者寥寥无几,即便是素有行业老大之称的优土虽年初称今年将实现盈利,却也被现实打了脸。