金融衍生品(习题)

金融衍生工具_课程习题答案(2)

资料范本本资料为word版本,可以直接编辑和打印,感谢您的下载金融衍生工具_课程习题答案(2)地点:__________________时间:__________________说明:本资料适用于约定双方经过谈判,协商而共同承认,共同遵守的责任与义务,仅供参考,文档可直接下载或修改,不需要的部分可直接删除,使用时请详细阅读内容第一章1、衍生工具包含几个重要类型?他们之间有何共性和差异?2、请详细解释对冲、投机和套利交易之间的区别,并举例说明。

3、衍生工具市场的主要经济功能是什么?4、“期货和期权是零和游戏。

”你如何理解这句话?习题答案1、期货合约::也是指交易双方按约定价格在未来某一期间完成特定资产交易行为的一种方式。

期货合同是标准化的在交易所交易,远期一般是OTC市场非标准化合同,且合同中也不注明保证金。

主要区别是场内和场外;保证金交易。

二者的定价原理和公式也有所不同。

交易所充当中间人角色,即买入和卖出的人都是和交易所做交易。

特点:T+0交易;标准化合约;保证金制度(杠杆效应);每日无负债结算制度;可卖空;强行平仓制度。

1)确定了标准化的数量和数量单位、2)制定标准化的商品质量等级、(3)规定标准化的交割地点、4)规定标准化的交割月份互换合约:是指交易双方约定在合约有效期内,以事先确定的名义本金额为依据,按约定的支付率(利率、股票指数收益率)相互交换支付的约定。

例如,债务人根据国际资本市场利率走势,将其自身的浮动利率债务转换成固定利率债务,或将固定利率债务转换成浮动利率债务的操作。

这又称为利率互换。

互换在场外交易、几乎没有政府监管、互换合约不容易达成、互换合约流动性差、互换合约存在较大的信用风险期权合约:指期权的买方有权在约定的时间或时期内,按照约定的价格买进或卖出一定数量的相关资产,也可以根据需要放弃行使这一权利。

为了取得这一权利,期权合约的买方必须向卖方支付一定数额的费用,即期权费。

期权主要有如下几个构成因素①执行价格(又称履约价格,敲定价格〕。

金融衍生品学习题解答合集

金融衍生品学习题解答合集1. 简介金融衍生品是一种金融工具,其价值来源于基础资产,如股票、商品、利率等。

它们的交易形式包括期权、期货、互换合约等。

本文将提供一些金融衍生品学习题的解答,并对每个问题给出详细的分析和解释。

2. 期权问题解答2.1. 请解释什么是认购期权和认沽期权。

认购期权是一种购买权,给予持有人在未来某个时间以特定价格购买标的资产的权利。

认购期权通常用于投机或套利的目的,因为当标的资产价格上涨时,认购期权的价值就会增加,持有人可以以低于市场价格购买。

认沽期权是一种出售权,给予持有人在未来某个时间以特定价格出售标的资产的权利。

认沽期权通常用于对冲或保护的目的,因为当标的资产价格下跌时,认沽期权的价值就会增加,持有人可以以高于市场价格出售。

2.2. 什么是期权的行权价?行权价是期权合约规定的购买或出售标的资产的价格。

对于认购期权,行权价是持有人行使购买权的价格;对于认沽期权,行权价是持有人行使出售权的价格。

行权价的确定通常基于市场需求、预期价格和风险偏好等因素。

2.3. 如何计算期权的收益?期权的收益取决于两个因素:标的资产的价格变化和期权合约的类型(认购或认沽)。

对于认购期权,当市场价格高于行权价时,持有人可以选择行使期权,并以行权价购买标的资产,然后以市场价格出售获得利润。

如果市场价格低于行权价,持有人可以选择不行使期权,只损失购买期权的费用。

对于认沽期权,当市场价格低于行权价时,持有人可以选择行使期权,并以行权价出售标的资产,然后从市场价格下跌中获得利润。

如果市场价格高于行权价,持有人可以选择不行使期权,只损失购买期权的费用。

3. 期货问题解答3.1. 什么是期货合约?期货合约是一种约定,以特定价格在将来的某个时间点交付标的资产。

期货合约通常用于投机、套利和对冲的目的。

持有期货合约的一方被称为多头,另一方被称为空头。

3.2. 如何计算期货的盈亏?期货的盈亏计算基于开仓价格和平仓价格之间的差异。

金融衍生工具课后习题答案

金融衍生工具课后习题答案金融衍生工具课后习题答案金融衍生工具是指那些通过与金融资产或金融指标相关联的合约或协议,用于管理金融风险或进行投资的工具。

这些工具包括期权、期货、互换和其他衍生品。

在金融市场中,衍生工具起到了非常重要的作用,它们可以帮助投资者进行风险管理,实现投资组合的多样化,并提供一种有效的投机机会。

在学习金融衍生工具的过程中,习题是非常重要的一部分。

通过解答习题,我们可以更好地理解和掌握相关的概念和技巧。

下面是一些金融衍生工具课后习题的答案,希望对你的学习有所帮助。

1. 期权是一种金融衍生工具,它给予持有者在未来某个时间以特定价格购买或出售某种资产的权利。

期权分为两种类型:认购期权和认沽期权。

认购期权赋予持有者以特定价格购买资产的权利,而认沽期权赋予持有者以特定价格出售资产的权利。

2. 期货是一种标准化合约,约定在未来某个时间以特定价格交割一定数量的某种标的资产。

期货合约可以用于投机和套期保值。

投机者通过买入或卖出期货合约来获取价格波动的利润,而套期保值者则通过买入或卖出期货合约来对冲其在现货市场上的风险。

3. 互换是一种金融合约,约定在未来某个时间交换一定数量的资产或现金流。

互换合约可以用于对冲风险、降低成本或进行投机。

最常见的互换类型是利率互换和货币互换。

4. 衍生品的价格受到多种因素的影响,包括标的资产价格、市场波动性、利率水平和时间价值等。

标的资产价格是影响期权和期货价格的最主要因素,市场波动性则是影响期权价格的重要因素。

利率水平对互换价格有着直接的影响,而时间价值则是期权价格中的一个重要组成部分。

5. 在期权定价中,有两个重要的概念:内在价值和时间价值。

内在价值是期权的实际价值,即期权行权时的立即收益。

时间价值则是期权的额外价值,它取决于期权的剩余时间和市场波动性。

时间价值随着期权到期日的临近而逐渐减少。

6. 黑-斯科尔斯期权定价模型是一种用于计算欧式期权价格的数学模型。

它基于一些假设,如市场无摩擦、无交易成本和无套利机会等。

金融衍生工具练习题及答案(英文版)

金融衍生工具DerivativesExercises AnswersQuestion 1The basis strengthens unexpectedly. Which of the following is true (circle one)(a) A short hedger's position improves.(b) A short hedger's position worsens.(c) A short hedger's position sometimes worsens and sometimes improves.(d) A short hedger's position stays the same.Short Hedge•Suppose thatF1: Initial Futures PriceF2: Final Futures PriceS2: Final Asset Price•You hedge the future sale of an asset by entering into a short futures contract•Price Realized=S2+(F1 –F2)= F1+Basis3Question 2On March 1 the spot price of a commodity is $20 and the July futures price is $19. On June 1 the spot price is $24 and the July futures price is $23.50. A company entered into a futures contract on March 1 to hedge the purchase of the commodity on June 1. It closed out its position on June 1. What is the effective price paid by the company for the commodity?Long Hedge•Suppose thatF1: Initial Futures PriceF2: Final Futures PriceS2: Final Asset Price•You hedge the future purchase of an asset by entering into a long futures contract•Cost of Asset=S2–(F2–F1)= F1+ Basis =19+(24-23.5)=19.55Question 3The following futures prices were observed for gold at the end of five consecutive trading days:$900, $903, $912.5, $898, and $890.Mr Smith short one gold futures (contract size 100 oz.) at the end of Day 1. Suppose the initial margin requirement is $4,000 and the maintenance margin at the 75% level.1.Is Mr Smith bullish or bearish on gold?pute his cash flows and margin levels.3.At what price of gold will Mr Smith get a margin call?4.How much of a variation margin will Mr Smith have to secure?5.How much in total during the five days has Mr Smith earned?Margins and Marking-to-Market, in DollarsDATE FUTURESPRICE CASHFLOWBEGINNINGMARGINCASHWITHDRAWALENDINGMARGINDay 1900004,0004,000 Day 2903-3003,70003,700 Day 3912.5-9502,7501,2504,000 Day 489814505,450-1,4504,000 Day 58908004,800-8004,000•Since he sold gold futures, he is bearish.•The beginning margin is the margin level at the end of the trading day. •The ending margin is the after-cash flow adjustment based on the margin call or removal of excess margin.–There is no margin call until the margin reaches 75% of $4,000, or $3,000.Then, it has to be restored to the initial margin level of $4,000.–If the profit exceeds the initial margin level, this excess margin can be removed (as on Days 4 and 5).•Mr Smith will get a margin call when the account value falls to $3,000 or loses 4,000 –3,000 = $1,000. As Mr Smith loses $100 for each $1increase in gold price, he will lose $1,000 if gold increases by $10.•He will have to secure $1,000 in cash.•His profit during the five days is: 1450 + 800 –1250 = $1000Question 4•Suppose that a March put option to sell a share for $40 costs $3.5 and is held until March.a. Draw a diagram illustrating how the profit from a shortposition in the option depends on the stock price atmaturity of the option.b. Under what circumstances will the option beexercised? If the option is exercised, will the seller ofthe option make profit? What is the maximum loss the seller may suffer?Question 5•The current £/$US spot exchange rate is 0.680. If you invested one UK pound for 90 days in the domesticriskless asset you would earn £1.05, and if you invested one US dollar for 90 days in the US riskless asset you would earn 1.01 dollars (assume continuouscompounding). A broker offers you a 90-day forwardcontract to buy or sell one million US dollars at theexchange rate of 0.60 pounds/dollar.•Can you make an arbitrage profit? If so, explain.Answer:Yes, there is arbitrage profit.90 days Present value Present value basedon spot rate$USD 1 million 1/1.01=0.9901 million 0.9901 * 0.68= UKP 0.6733 M£Worth:0.6733*1.05 = UKP0.7070 M USD 1.1783 M UKP 0.6733 MUKP 0.6733 M1.Borrow USD 0.9901M, change to UKP 0.6733 M2.Hold for 90 days, 0.6733*1.05 =UKP0.7070 M3.Change to USD, 0.7070M/0.60 = USD 1.17834.Repayment of the loan. Profit = 1.1783 –1 = USD 0.1783 millions.Question 6Prove the result F2= F1e r(t2 –t1)where F2and F1are two forward prices on the same commodity with maturity dates t1and t2(t1< t2), and r is the risk-free interest rate.Answer:F(t,T) = S(t)e r(T –t)where S is today’s spot, S1is spot at time t1and S2is spot at time t2,F1= Se rt1=> S = F1e–rt1and F2= Se rt2=> S = F2e–rt2Equate the two results to get F1e–rt1= F2e–rt2Multiplying both sides by e rt2gives the result.Question 7This is February. Forward prices for April and June forward contracts for gold are $900 and $915 per ounce, respectively, and the riskless yearly rate is 5%. Can you make arbitrage profits? Explain. Assume that the time differencebetween the maturity of the two contracts is 60 days.Question 8The current value of the Dow Jones Industrial Average is 11,200.The dividend yield is 3.00 per annum, assuming continuouscompounding and a 365-day year.a) What is the 60-day Dow Jones Industrial Average futures price?The interest rate is 10%.b) The Dow slides down and a week later ends at 10,500. What isthe 53-day forward price? What is the value of the forwardcontract to the long? Assume that the forward contract’s payoffs are determined by multiplying the above results by $10.a)R=10%, the continuous compounded interest rate:e r= 1+10%r = ln(1.10) = 9.53%The 60-day forward price:F0= S0e(r–q )T= 11,200e(0.0953 –0.03)(60/365)= 11,321b) The 60-day forward price:F0= S0e(r–q )T= 10,500 e(0.0953 –0.03)(53/365)= 10,600the value of the forward contract to long:= (10,600–11,321) e-0.0953 *(53/365)= –711.1If the forward’s payoffs are determined by multiplying the payoff by $10, then the long has lost $7,111Question 9•Show that a newly written forward contract is equivalent to a portfolio consisting of one purchased European call option on the underlying asset and one written European put option on the underlying asset, both with a common expiration date equal to the delivery date, and both with a common striking price equal to the forward price, F.Question 10A company has a $36 million portfolio with a beta of 1.2. The S&P index is currently standing at 900. Futures contracts on $250 times the index can be traded. What trade is necessary to achieve the following. (Indicate the number of contracts that should be traded and whether the position is long or short.)•Eliminate all systematic risk in the portfolio •Reduce the beta to 0.9•Increase beta to 1.8Question 11•What is the lower bound for the price of a four-month call option on a non-dividend paying stock when thestock price is $28, the strike price is $25, and therisk-free interest rate is 8% per annum?•What is the lower bound for the price of a one-month European put option on a non-dividend paying stockwhen the stock price is $12, the strike price is $15,and the risk-free interest rate is 6% per annum?i) 66.32528)12/4(08.00=−=−−−eKeS rTii)93.215)12/1(06.00==−−−eS KerTQuestion 12An investor is looking at the options market, where the following prices are being quoted for American options (stock price = $30).MONTH & STRIKE CALL PRICE PUT PRICEMay 2542May 3013June 3012a) The investor is exploring the ways to make some arbitrage profits. Explain the different ways to make arbitrage profits based on the above information.b) Draw the payoff diagrams with options. In particular,i) a straddle (long call and long put with May 25)ii) a bull spread (long May 25 call and short May 30 call)Question 13The following prices are given for European options on a particular stock expiring in December.Dec 50 call = $7Dec 55 call = $3Dec 50 put = $4Dec 55 put = $8Draw the profit and loss diagram on the expiration date from the following positions:(a) A bull spread (long Dec 50 call and short Dec 55 call).(b) A straddle (long Dec 55 call and long Dec 55 put).(c) A strangle (long Dec 50 put and long Dec 55 call)Question 14A non-dividend paying stock sells for $7.59. What is the theoretical value of a European style, $8 call with 1 year until expiration, assuming interest rates of 12% (with continuous compounding) and annual volatility of 30%?)1( 0D Kec S p rT++=+−724.16.06.06.0)12/7(12.0)12/4(12.0)12/2(12.0=++=−−−e e e D The put-call parity relationship with dividends becomes:where D denotes the present value (PV) of dividend payments. We expect three dividend payments of $0.60 in 2, 4 and 7 months. Therefore:956.5724.1363)12/8(12.000=⇒++=−++=⇒++=+−−−p e S D Ke c p D Ke c S p rT rT Now we have everything we need in equation (1) to compute the value of the put option:Question 16Use the put-call parity relationship to derive, for a non-dividend-paying stock, the relationship between:•The delta of a European call and the delta of a European put.•The gamma of a European call and the gamma of a European put.•The vega of a European call and the vega of a European put.•The theta of a European call and the theta of a European put.Question 17• A non-dividend paying stock sells for $10/share. In three months it will be either $12/share or $8/share. The risk free interest rate is 5% per annum (with continuouscompounding).(a) What is the value of a put option if the strike price is $10using no-arbitrage valuation?(b) What is the call price with the same strike and maturity?(c) Suppose that the market value of the put option is $2.Explain whether you can make arbitrage profits.The riskless portfolio is: long 0.5 shares and long 1 put option. The value of the portfolio in 3 months is 12*0.5 = 6.The value of the portfolio today is 6*e – 0.05*0.25 = 5.92.The value of the put option = 5.92 – 10*0.5 = $0.92– r t- 0.05*0.25b) c = p + S0 - K e = 0.92 + 10 - 10 e = $1.04c)Sell the traded put for $2buy a synthetic put for $0.92 (short sell 0.5 stocks and lend $(0.5*10 + 0.92) = 5.92 at the interest rate of 5% per annum).Today: Net cash flow is 2 + 0.5*10 - 5.92 = + $1.08.At maturity:(i) If the stock price is 12,cash flow from the traded put is 0,cash flow from the synthetic put is –0.5*12 + 5.92 e 0.05*0.25 = 0. (ii) If the stock price is 8,cash flow from the traded put is –(10 – 8) = –2,cash flow from the synthetic put is –0.5*8 + 5.92 e 0.05*0.25 = 2.Net cash inflow is –2 + 2 = 0.Thus $1.08 is the arbitrage profit you can make today.Question 18Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months.a)Calculate u, d, and p for a two-step tree.b)Value the option using a two-step tree.Question 19The volatility of a stock price is 30% per annum. What is the standard deviation of the percentage price change in one trading day?Question 20Explain the principle of risk-neutral valuation.。

金融衍生工具的课后习题

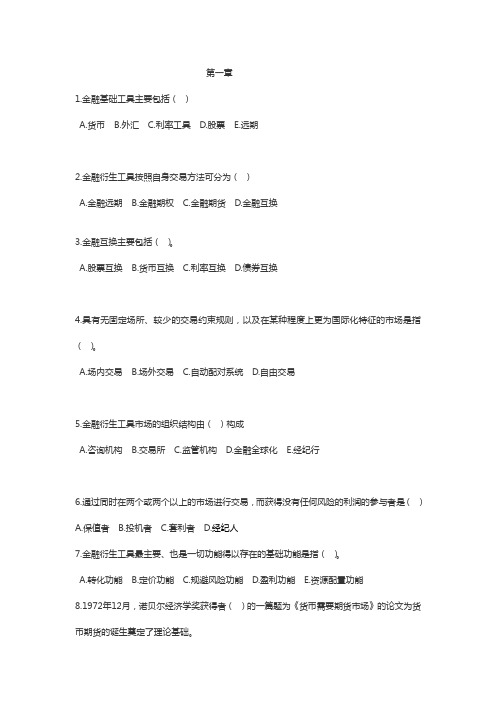

第一章1.金融基础工具主要包括()A.货币B.外汇C.利率工具D.股票E.远期2.金融衍生工具按照自身交易方法可分为()A.金融远期B.金融期权C.金融期货D.金融互换3.金融互换主要包括()。

A.股票互换B.货币互换C.利率互换D.债券互换4.具有无固定场所、较少的交易约束规则,以及在某种程度上更为国际化特征的市场是指()。

A.场内交易B.场外交易C.自动配对系统D.自由交易5.金融衍生工具市场的组织结构由()构成A.咨询机构B.交易所C.监管机构D.金融全球化E.经纪行6.通过同时在两个或两个以上的市场进行交易,而获得没有任何风险的利润的参与者是()A.保值者B.投机者C.套利者D.经纪人7.金融衍生工具最主要、也是一切功能得以存在的基础功能是指()。

A.转化功能B.定价功能C.规避风险功能D.盈利功能E.资源配置功能8.1972年12月,诺贝尔经济学奖获得者()的一篇题为《货币需要期货市场》的论文为货币期货的诞生奠定了理论基础。

A.米尔顿弗里德曼(Milton Friedman)B.费雪和布莱克(Fisher and Black)C.默顿和斯克尔斯(Myron and Scholes)D.约翰纳什(John Nash)9.()是20世纪80年代以来国际资本市场的最主要特征之一。

A.金融市场资本化B.金融市场国际化C.金融市场创新化D.金融市场证券化10.下面选项中属于金融衍生工具新产品的有()A.巨灾再保险期货B.巨灾期权合约C.气候衍生品D. 信用衍生产品二、思考题1.如何定义金融衍生工具?怎样理解金融衍生工具的含义?2.与基础工具相比,金融衍生工具有哪些特点?3.金融衍生工具的功能有哪些?4.金融衍生工具市场的参与者有哪些?5.请简述金融衍生工具对金融业的正、负两方面影响。

6.请根据下述各种情况,指出分别运用了哪种金融衍生工具,并简要说明如何操作。

情况一:9月初,你决定购买一辆新汽车。

《衍生金融工具》(第二版)习题及答案第11章

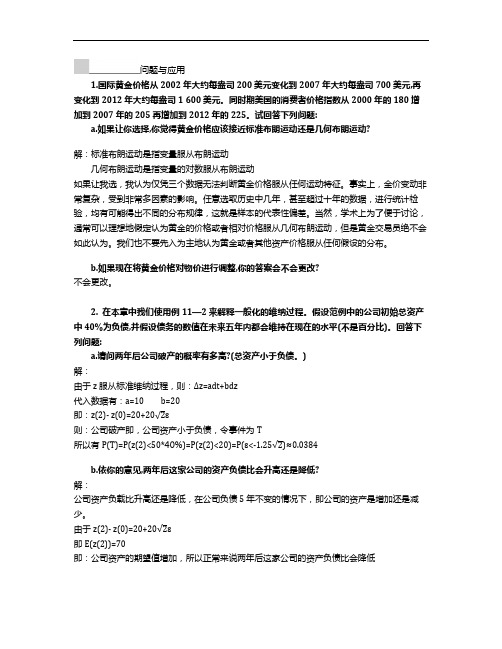

问题与应用1.国际黄金价格从2002年大约每盎司200美元变化到2007年大约每盎司700美元,再变化到2012年大约每盎司1600美元。

同时期美国的消费者价格指数从2000年的180增加到2007年的205再增加到2012年的225。

试回答下列问题:a.如果让你选择,你觉得黄金价格应该接近标准布朗运动还是几何布朗运动?解:标准布朗运动是指变量服从布朗运动几何布朗运动是指变量的对数服从布朗运动如果让我选,我认为仅凭三个数据无法判断黄金价格服从任何运动特征。

事实上,金价变动非常复杂,受到非常多因素的影响。

任意选取历史中几年,甚至超过十年的数据,进行统计检验,均有可能得出不同的分布规律,这就是样本的代表性偏差。

当然,学术上为了便于讨论,通常可以理想地假定认为黄金的价格或者相对价格服从几何布朗运动,但是黄金交易员绝不会如此认为。

我们也不要先入为主地认为黄金或者其他资产价格服从任何假设的分布。

b.如果现在将黄金价格对物价进行调整,你的答案会不会更改?不会更改。

2.在本章中我们使用例11—2来解释一般化的维纳过程。

假设范例中的公司初始总资产中40%为负债,并假设债务的数值在未来五年内都会维持在现在的水平(不是百分比)。

回答下列问题:a.请问两年后公司破产的概率有多高?(总资产小于负债。

)解:由于z服从标准维纳过程,则:∆z=adt+bdz代入数据有:a=10 b=20即:z(2)- z(0)=20+20√2ɛ则:公司破产即,公司资产小于负债,令事件为T所以有P(T)=P(z(2)<50*40%)=P(z(2)<20)=P(ɛ<-1.25√2)≈0.0384b.依你的意见,两年后这家公司的资产负债比会升高还是降低?解:公司资产负载比升高还是降低,在公司负债5年不变的情况下,即公司的资产是增加还是减少。

由于z(2)- z(0)=20+20√2ɛ即E(z(2))=70即:公司资产的期望值增加,所以正常来说两年后这家公司的资产负债比会降低c.假设这家公司在外发行了1 000万股。

cfa衍生品题目

cfa衍生品题目

以下是一个关于CFA衍生品的样题:

1. (单选)下列哪项措施可以限制衍生品的使用?

A. 假设市场提供套利机会

B. 对衍生品的预期收益进行风险贴现

C. 对衍生品的预期收益和风险加收风险溢价

2. (多选)以下哪些是CFA一级考试中衍生品相关内容的考点?

A. 衍生品的基本概念和种类

B. 衍生品市场的交易机制和参与者

C. 衍生品定价和风险管理的原理和方法

D. 衍生品市场的监管和法规

3. (简答)请简述衍生品对金融市场的主要影响,并指出应当如何规范衍生品市场的交易活动。

4. (论述)请论述在投资组合管理中,如何利用衍生品进行风险管理和资产配置。

以上题目旨在测试考生对CFA衍生品相关内容的理解和应用能力。

考生需

要掌握衍生品的基本概念、种类、交易机制和市场参与者,理解衍生品定价和风险管理的原理和方法,以及衍生品市场监管和法规的要求。

同时,考生还需要了解衍生品对金融市场的主要影响,以及如何规范衍生品市场的交易活动。

最后,考生需要掌握如何利用衍生品进行风险管理和资产配置的方法。

(完整版)金融衍生品第一章至十一章课后习题答案

金融衍生品课后思考与习题第一章期货市场基本原理(书P29)1、结合期货市场产生历程,谈谈期货市场产生的规律是什么?答:从芝加哥期货交易所的产生历程可以看到,期货市场的形成经历了从现货交易到远期交易最后到期货交易的复杂演变过程,它是人们在贸易过程中不断追求交易效率、降低交易成本与风险的结果,期货市场是现货市场发展的产物,两者相辅相成、互相补充、共同发展。

2、讨论茶叶和烟草是否能作为期货品种?答:我认为茶叶和烟草不能作为期货品种。

理由如下:并不是所有现货市场的商品都适合进行期货交易,一般而言,能够成为期货品种必须具备以下条件:商品同质性;价格波动大且频繁;现货规模大;适宜储藏。

3、期货合约主要条款有哪些?答:一、合约名称;二、交易单位;三、报价单位;四、最小变动价位;五、每日价格最大波动限制;六、合约交割月份;七、交易时间;八、最后交易日;九、交割日期;十、交割等级;十一、交割地点;十二、交易手续费;十三、交割方式。

4、期货市场的功能有哪些?答:一、价格发现,合理配置资源:1、优化资源配置功能;2、信息功能;3、定价功能二、风险管理,化解国民经济系统性风险5、期货交易的基本特征是什么?答:交易集中化、合约标准化、交易的远期性质、保证金制度与杠杆机制、每日无负债结算制度、交易所具有担保履约职责、双向交易和对冲机制。

第二章期货市场构成(书P58)1、期货交易者是如何分类的?期货交易者可以分为两大类:套期保值者和投资者,后者包括投机交易者和套利交易者2、我国期货中介机构有哪些分类?中国香港的期货中介机构有两种类型:一是经纪商,二是期货商;我国大陆期货中介机构目前包括期货公司、介绍经纪人、和居间人三类。

3、期货交易所的主要职能是什么?主要职能:(1)提供交易的场所、设施和服务。

(2)设计合约,安排合约上市。

(3)、制定期货交易规则,组织并监督交易。

(4)、监控市场风险。

(5)、发布市场信息。

4、会员制与公司制期货交易所各自的特征是什么?会员制的特征:(1)、它是由全体会员共同出资组建,缴纳一定的会员资格费,作为注册资本;(2)、会员在进行交易或代理客户交易之前必须取得会员资格;(3)、会员制期货交易所实行自律管理。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

课本习题:

1、 P42-2.15在某天结束时,一位交易所成员持有100份多头合约,结算价格为每份合约

50000美元,每份合约的初始保证金为2000美元,第二天该成员又已51000美元的价格签订了20份多头合约,这天结算价为50200美元,这位成员须向交易所补交多少保证金?

2、P43-2.25假设不存在玉米储存费用,一年期借款利率为5%,2004年2月4日当天,2004

年3月玉米期货结算价格为每蒲式耳270.25每分,2004年5分期货价格结算价为275.25美分,如何在2004年2月4日通过交易2004年3月份和5月份的合约赚取利润?

3、P96例5-3考虑一份6个月期的远期合约,其标的资产在6个月中的期望收益率为2%,

按连续复利计的无风险年利率为10%。

资产价格为25美元,求按半年计复利4%年的收益率等价的连续复利计的年利率为多少?远期价格为多少?

4、P104例5-7如表,加拿大元的期货价格随着合约到期时间的增加而以每年1%的速度减

少(2004年9月合约收盘价格0.7449,约比2004年3月的收盘价格0.7485低了0.5%)。

这一关系表明在2004年2月4日澳大利亚的短期利率比美国的短期利率大约高出1%。

5、P105例5-8考虑一份1年期黄金期货合约,我们假设储藏黄金没有收入,仅有每年2美

元/盎司的成本,支付在年末进行。

假设现货价格为450美元,对于所有期限而言无风险利率均为年7%。

求合约有效期内扣除收入后总储藏成本的现值及期货价格。

并分析套利机会。

6、P114 5-24一家银行给其公司客户两个选择:一是以11%的年利率借入现金,二是以每

年2%的利率借入黄金。

(如果借入的是黄金,那么利息也必须以黄金支付。

这样现在借入100盎司黄金一年后要以102盎司归还。

)无风险利率是年9.25%,储藏成本为年0.5%。

讨论黄金贷款的利率相对于现金贷款而言是高还是低。

(两笔贷款利率均按照均为按年计复利。

无风险利率和储藏成本是按连续复利计算)

7、P175例8-2考虑一份以15美元/股的价格卖出100股股票的看跌期权,假设公司宣告25%

的股票股利,相当于5对4的股票拆分,期权合约的条款将变更为持有者有权以12美元/股的价格卖出125股股票。

8、P180例8-4一名美国投资者决定用保证金购买200股某股票,并出售2份基于该股的看

涨期权合约。

股价为63美元,执行价格为60美元,期权价格为7美元。

保证金账户允许投资者借入股票价格的50%,即6300美元。

投资者可以用收取期权费(7*200=1400美元)作为购买股票的部分资金。

购买股票需要63*200=12600美元,求该投资者进行这些交易需要的最低初始现金额?

9、P187 8.11描述下面投资组合的终值:一份刚签订的远期合约多头头寸和一份同一标的的

资产、同一到期日的欧式看跌期权多头头寸,期权的执行价格与构建组合时资产的远期价格相等。

证明欧式看跌期权的价格与具有相同执行价格和到期日的欧式看涨期权相同。

10、P187 8.12 一名交易商买入一个执行价格为45美元的看涨期权以及一个执行价格

为40美元的看跌期权。

两期权具有相同到期日。

看涨期权价格为3美元,看跌期权价格为4美元。

用图说明交易商的利润是怎样随资产价格变化而变化。

11、一名美国投资者出售了5份无保护看涨期权合约,期权价格为3.5美元,执行价格

为60美元,股票价格为57美元。

要求初始保证金是多少?

12、P195 例9-1考虑一个不支付股利的欧式股票看涨期权,此时股票价格为51美元,

执行价格为50美元,距到期日还有6个月,无风险利率为每年12%。

求期权的价格下限。

13、P206 9.22一只股票的欧式看涨期权和欧式看跌期权的执行价格均为20美元,且都

在3个月后到期,期权价格均为3美元,无风险利率为每年10%,股票现价19美元,预期一个月后股利为1美元。

对于交易商而言存在何种套利机会?

14、P206 9.25假设你是一家杠杆比例很高的公司的经理和唯一的所有者,所有的债务

在1年后到期,如果到时公司价值高于债务面值,你就可以偿还债务;如果到时公司价值小于债务面值,你就必须破产,让债务人拥有公司。

a、将公司价值作为期权标的物,描述你的头寸情况

b、按照以公司价值为标的物的期权的形式,描述债务人的头寸情况

c、你应当如何提高你头寸的价值?。