Safeguard-Policy-Statement-June2009

亚洲开发银行保障政策声明

外部专家。 那些不参与项目日常执行或监督工作的专家。

高度复杂和敏感的项目。那些亚行认为具有高风险,或存在较大争议,或可能涉及多方 面利益,从而会产生潜在的重大社会和环境影响的项目。

有效协商。这一过程具有以下特征:(1)项目准备阶段就已启动,并贯穿整个项目周 期;(2)以适当的方式,及时而充分地向受影响的人群发布项目的相关信息;(3)协 商必须在不受到威胁和强迫的条件下进行;(4)不存在性别歧视,充分考虑弱势群体的 需求;(5)决策时考虑了所有受影响的人群和其他利益相关方的意见,如项目设计、减 缓措施、共享发展成果和机会,以及执行中的问题。

4.经亚行董事会批准,《保障政策声明》及其对借款人/客户的要求将取代当前的三项保 障政策。新的《业务手册》将取代现有《业务手册》的 F1、F2 和 F3 部分。亚行将修订 其《移民安置手册》2和 《环境评价导则》(2003),并制定《原住民手册》,为相关活 动提供详细的技术指导和建议。

5.《保障政策声明》的征求意见稿已于 2007 年 10 月发布在亚行的官方网站上,以征求 外部意见。在征求意见期间(2007 年 10 月—2008 年 4 月),亚行邀请各利益相关方, 在亚太地区和其他地区举行了 14 次研讨会,广泛听取意见和具体建议。亚行还通过书面 形式、主题讨论会、非正式会议和电话会议等形式,收集了众多反馈意见。所有的意见在 咨询结束以前都发布在亚行的网页上。作为对来自各方的意见的回应,亚行管理层决定在 这些意见和建议的基础上发布《保障政策声明》第二稿,并在马尼拉再举行一次研讨会, 以便利益相关方对第二稿进行评估。

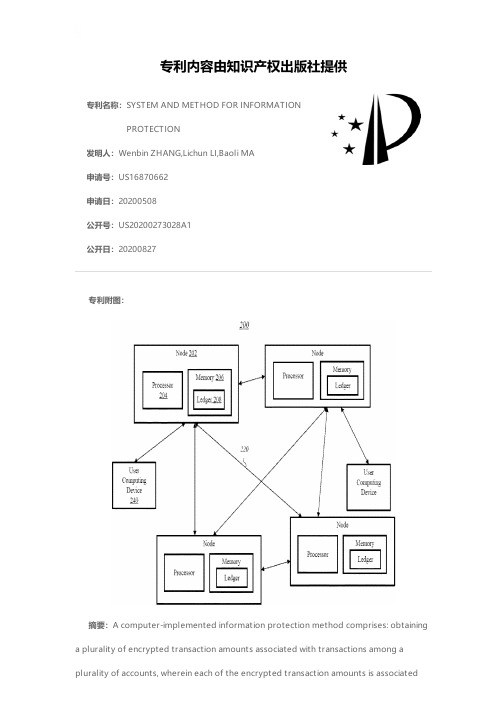

SYSTEM AND METHOD FOR INFORMATION PROTECTION

专利名称:SYSTEM AND METHOD FOR INFORMATIONPROTECTION发明人:Wenbin ZHANG,Lichun LI,Baoli MA申请号:US16870662申请日:20200508公开号:US20200273028A1公开日:20200827专利内容由知识产权出版社提供专利附图:摘要:A computer-implemented information protection method comprises: obtaining a plurality of encrypted transaction amounts associated with transactions among a plurality of accounts, wherein each of the encrypted transaction amounts is associatedwith one of the accounts that sends or receives one of the transaction amounts, and the encryption of each of the transaction amounts at least conceals whether the one account sends or receives the one of the transaction amounts; generating a sum proof based on the obtained encrypted transaction amounts, the sum proof at least indicating that the transaction amounts are balanced; and transmitting the encrypted transaction amounts and the sum proof to one or more nodes on a blockchain network for the nodes to verify the transactions.申请人:ALIBABA GROUP HOLDING LIMITED地址:Grand Cayman KY国籍:KY更多信息请下载全文后查看。

IFRS9原文

November 2009IFRS 9 Financial InstrumentsInternational Financial Reporting Standard 9 Financial InstrumentsIFRS 9 Financial Instr uments is issued by the International Accounting Standards Board (IASB), 30 Cannon Street, London EC4M 6XH, United Kingdom.Tel: +44 (0)20 7246 6410Fax: +44 (0)20 7246 6411Email: iasb@Web: The I ASB, the I nternational Accounting Standards Committee Foundation (IASCF), the authors and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this publication, whether such loss is caused by negligence or otherwise.ISBN for this part: 978-1-907026-47-8ISBN for complete publication (three parts): 978-1-907026-46-1Copyright © 2009 IASCF®International Financial Reporting Standards (including International Accounting Standards and SI C and I FRI C I nterpretations), Exposure Drafts, and other I ASB publications are copyright of the I ASCF. The approved text of I nternational Financial Reporting Standards and other IASB publications is that published by the IASB in the English language. Copies may be obtained from the IASCF. Please address publications and copyright matters to:IASC Foundation Publications Department,1st Floor, 30 Cannon Street, London EC4M 6XH, United Kingdom.Tel: +44 (0)20 7332 2730 Fax: +44 (0)20 7332 2749Email: publications@ Web: All rights reserved. No part of this publication may be translated, reprinted or reproduced or utilised in any form either in whole or in part or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any information storage and retrieval system, without prior permission in writing from the IASCF.The IASB logo/the IASCF logo/‘Hexagon Device’, the IASC Foundation Education logo, ‘IASC Foundation’, ‘e IFRS’, ‘IAS’, ‘IASB’, ‘IASC’, ‘IASCF’, ‘IASs’, ‘IFRIC’, ‘IFRS’,‘IFRSs’, ‘International Accounting Standards’, ‘International Financial Reporting Standards’ and ‘SIC’ are Trade Marks of the IASCF.IFRS 9 F INANCIAL I NSTRUMENTSC ONTENTSparagraphsINTRODUCTIONINTERNATIONAL FINANCIAL REPORTING STANDARD 9 FINANCIAL INSTRUMENTSCHAPTERS1 OBJECTIVE 1.12 SCOPE 2.13 RECOGNITION AND DERECOGNITION 3.1.1–3.1.24 CLASSIFICATION 4.1–4.95 MEASUREMENT 5.1.1–5.4.56 HEDGE ACCOUNTING NOT USED7 DISCLOSURES NOT USED8 EFFECTIVE DATE AND TRANSITION8.1.1–8.2.13 APPENDICESA Defined termsB Application guidanceC Amendments to other IFRSs (see separate booklet)APPROVAL BY THE BOARD OF IFRS 9 FINANCIAL INSTRUMENTSISSUED IN NOVEMBER 2009AMENDMENTS TO THE GUIDANCE ON OTHER IFRSs (see separate booklet) BASIS FOR CONCLUSIONS(see separate booklet)APPENDIXAmendments to the Basis for Conclusions on other IFRSs3© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 2009 International Financial Reporting Standard 9 Financial Instruments (IFRS 9) is set out in paragraphs 1.1–8.2.13 and Appendices A–C. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the I FRS. Definitions of other terms are given in the Glossary for International Financial Reporting Standards. IFRS 9 should be read in the context of its objective and the Basis for Conclusions, the Preface to International Financial Reporting Standards and the Framework for the Preparation and Presentation of Financial Statements. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.© Copyright IASCF4IFRS 9 F INANCIAL I NSTRUMENTSIntroductionReasons for issuing the IFRSN1AS 39 Financial Instr uments: Recognition and Measur ement sets out the requirements for recognising and measuring financial assets, financialliabilities and some contracts to buy or sell non-financial items.The I nternational Accounting Standards Board (I ASB) inherited I AS 39from its predecessor body, the nternational Accounting StandardsCommittee.IN2Many users of financial statements and other interested parties have told the Board that the requirements in I AS 39 are difficult to understand,apply and interpret. They have urged the Board to develop a newstandard for financial reporting for financial instruments that isprinciple-based and less complex. Although the Board has amendedIAS39 several times to clarify requirements, add guidance and eliminateinternal inconsistencies, it has not previously undertaken a fundamentalreconsideration of reporting for financial instruments.IN3Since 2005, the IASB and the US Financial Accounting Standards Board (FASB) have had a long-term objective to improve and simplify the reporting for financial instruments. This work resulted in thepublication of a discussion paper, Reducing Complexity in Reporting Financial Instruments, in March 2008. Focusing on the measurement of financial instruments and hedge accounting, the paper identified several possibleapproaches for improving and simplifying the accounting for financialinstruments. The responses to the paper indicated support for asignificant change in the requirements for reporting financialinstruments. In November 2008 the IASB added this project to its activeagenda, and in December 2008 the FASB also added the project to itsagenda.IN4In April 2009, in response to the input received on its work responding to the financial crisis, and following the conclusions of the G20 leaders andthe recommendations of international bodies such as the Financial Stability Board, the I ASB announced an accelerated timetable forreplacing IAS 39. As a result, in July 2009 the IASB published an exposuredraft Financial Instruments: Classification and Measurement, followed by IFRS 9Financial Instruments in November 2009.5© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 2009IN5In developing IFRS 9 the Board considered input obtained in response to its discussion paper, the report from the Financial Crisis Advisory Grouppublished in July 2009, the responses to the exposure draft and otherdiscussions with interested parties, including three public round tablesheld to discuss the proposals in that exposure draft. The IASB staff alsoobtained additional feedback from users of financial statements andothers through an extensive outreach programme.The Board’s approach to replacing IAS 39IN6The Board intends that IFRS 9 will ultimately replace IAS 39 in its entirety.However, in response to requests from interested parties that theaccounting for financial instruments should be improved quickly, theBoard divided its project to replace IAS 39 into three main phases. As theBoard completes each phase, as well as its separate project on thederecognition of financial instruments, it will delete the relevantportions of AS 39 and create chapters in FRS 9 that replace therequirements in IAS 39. The Board aims to replace IAS 39 in its entiretyby the end of 2010.IN7The Board included proposals for the classification and measurement of financial liabilities in the exposure draft that preceded IFRS 9. In thatexposure draft the Board also drew attention to the discussion paperCr edit Risk in Liability Measur ement published in June 2009. n theirresponses to the exposure draft and discussion paper, many expressedconcern about recognising changes in an entity’s own credit risk in theremeasurement of liabilities. During its redeliberations on theclassification and measurement of financial liabilities, the Board decidednot to finalise the requirements for financial liabilities beforeconsidering those issues further and analysing possible approaches toaddress the concerns raised by respondents.I N8Accordingly, in November 2009 the Board issued the chapters of I FRS 9relating to the classification and measurement of financial assets.The Board addressed those matters first because they form the foundationof a standard on reporting financial instruments. Moreover, many of theconcerns expressed during the financial crisis arose from the classificationand measurement requirements for financial assets in IAS 39.© Copyright IASCF6IFRS 9 F INANCIAL I NSTRUMENTSIN9The Board sees this first instalment on classification and measurement of financial assets as a stepping stone to future improvements in thefinancial reporting of financial instruments and is committed tocompleting its work on classification and measurement of financial instruments expeditiously.Main features of the IFRSI N10Chapters 4 and 5 of I FRS 9 specify how an entity should classify andmeasure financial assets, including some hybrid contracts. They requireall financial assets to be:(a)classified on the basis of the entity’s business model for managingthe financial assets and the contractual cash flow characteristics ofthe financial asset.(b)initially measured at fair value plus, in the case of a financial assetnot at fair value through profit or loss, particular transaction costs.(c)subsequently measured at amortised cost or fair value.IN11These requirements improve and simplify the approach for classification and measurement of financial assets compared with the requirements ofIAS 39. They apply a consistent approach to classifying financial assetsand replace the numerous categories of financial assets in IAS 39, each ofwhich had its own classification criteria. They also result in oneimpairment method, replacing the numerous impairment methods inIAS 39 that arise from the different classification categories.Next stepsIN12IFRS 9 is the first part of Phase 1 of the Board’s project to replace IAS 39.The main phases are:(a)Phase 1: Classification and measurement. The exposure draftFinancial Instruments: Classification and Measurement, published in July2009, contained proposals for both assets and liabilities within thescope of IAS 39. The Board is committed to completing its work onfinancial liabilities expeditiously and will include requirements forfinancial liabilities in IFRS 9 in due course.(b)Phase 2: I mpairment methodology. On 25 June 2009 the Boardpublished a Request for nformation on the feasibility of anexpected loss model for the impairment of financial assets. This7© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 2009formed the basis of an exposure draft, Financial Inst r uments:Amor tised Cost and Impair ment, published in November 2009 with acomment deadline of 30 June 2010. The Board is also setting up anexpert advisory panel to address the operational issues arisingfrom an expected cash flow approach.(c)Phase 3: Hedge accounting. The Board has started to consider howto improve and simplify the hedge accounting requirements ofIAS39 and expects to publish proposals shortly.IN13In addition to those three phases, the Board published in March 2009 an exposure draft Derecognition (proposed amendments to IAS 39 and IFRS 7).Redeliberations are under way and the Board expects to complete thisproject in the second half of 2010.IN14As stated above, the Board aims to have replaced IAS 39 in its entirety by the end of 2010.IN15The IASB and the FASB are committed to achieving by the end of 2010 a comprehensive and improved solution that provides comparabilityinternationally in the accounting for financial instruments. However,those efforts have been complicated by the differing project timetablesestablished to respond to the respective stakeholder groups. The IASB andFASB have developed strategies and plans to achieve a comprehensive andimproved solution that provides comparability internationally. As part ofthose plans, they reached agreement at their joint meeting in October2009 on a set of core principles designed to achieve comparability andtransparency in reporting, consistency in accounting for creditimpairments, and reduced complexity of financial instrumentaccounting.© Copyright IASCF8IFRS 9 F INANCIAL I NSTRUMENTS9© Copyright IASCF International Financial Reporting Standard 9 Financial InstrumentsChapter 1 Objective1.1The objective of this I FRS is to establish principles for the financialreporting of financial assets that will present relevant and useful information to users of financial statements for their assessment of the amounts, timing and uncertainty of the entity’s future cash flows.Chapter 2 Scope2.1An entity shall apply this I FRS to all assets within the scope of I AS 39Financial Instruments: Recognition and Measurement .Chapter 3 Recognition and derecognition3.1 Initial recognition of financial assets3.1.1An entity shall recognise a financial asset in its statement of financialposition when, and only when, the entity becomes party to the contractual provisions of the instrument (see paragraphs AG34 and AG35 of IAS 39).When an entity first recognises a financial asset, it shall classify it in accordance with paragraphs 4.1–4.5 and measure it in accordance with paragraph 5.1.1.3.1.2 A regular way purchase or sale of a financial asset shall be recognised andderecognised in accordance with paragraphs 38 and AG53–AG56 of IAS 39.Chapter 4 Classification4.1U nless paragraph 4.5 applies, an entity shall classify financial assets assubsequently measured at either amortised cost or fair value on the basis of both:(a)the entity’s business model for managing the financial assets; and (b)the contractual cash flow characteristics of the financial asset.I NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 20094.2 A financial asset shall be measured at amortised cost if both of thefollowing conditions are met:(a)the asset is held within a business model whose objective is to holdassets in order to collect contractual cash flows.(b)the contractual terms of the financial asset give rise on specifieddates to cash flows that are solely payments of principal and intereston the principal amount outstanding.Paragraphs B4.1–B4.26 provide guidance on how to apply these conditions.4.3For the purpose of this IFRS, interest is consideration for the time value ofmoney and for the credit risk associated with the principal amountoutstanding during a particular period of time.4.4 A financial asset shall be measured at fair value unless it is measured atamortised cost in accordance with paragraph 4.2.Option to designate a financial asset at fair valuethrough profit or loss4.5Notwithstanding paragraphs 4.1–4.4, an entity may, at initial recognition,designate a financial asset as measured at fair value through profit or lossif doing so eliminates or significantly reduces a measurement orrecognition inconsistency (sometimes referred to as an ‘accountingmismatch’) that would otherwise arise from measuring assets or liabilitiesor recognising the gains and losses on them on different bases(see paragraphs AG4D–AG4G of IAS 39).Embedded derivatives4.6An embedded derivative is a component of a hybrid contract that alsoincludes a non-derivative host—with the effect that some of the cash flowsof the combined instrument vary in a way similar to a stand-alonederivative. An embedded derivative causes some or all of the cash flowsthat otherwise would be required by the contract to be modifiedaccording to a specified interest rate, financial instrument price,commodity price, foreign exchange rate, index of prices or rates, creditrating or credit index, or other variable, provided in the case of anon-financial variable that the variable is not specific to a party to thecontract. A derivative that is attached to a financial instr ument but iscontractually transferable independently of that instrument, or has adifferent counterparty, is not an embedded derivative, but a separatefinancial instrument.© Copyright IASCF10IFRS 9 F INANCIAL I NSTRUMENTS4.7If a hybrid contract contains a host that is within the scope of this IFRS, anentity shall apply the requirements in paragraphs 4.1–4.5 to the entire hybrid contract.4.8If a hybrid contract contains a host that is not within the scope of this IFRS,an entity shall apply the requirements in paragraphs 11–13 and AG27–AG33B of IAS 39 to determine whether it must separate the embeddedderivative from the host. If the embedded derivative must be separatedfrom the host, the entity shall:(a)classify the derivative in accordance with either paragraphs 4.1–4.4for derivative assets or paragraph 9 of IAS 39 for all other derivatives;and(b)account for the host in accordance with other IFRSs.Reclassification4.9When, and only when, an entity changes its business model for managingfinancial assets it shall reclassify all affected financial assets in accordancewith paragraphs 4.1–4.4.Chapter 5 Measurement5.1 Initial measurement of financial assets5.1.1At initial recognition, an entity shall measure a financial asset at its fairvalue (see paragraphs 48, 48A and AG69–AG82 of IAS 39) plus, in the case ofa financial asset not at fair value through profit or loss, transaction costs thatare directly attributable to the acquisition of the financial asset.5.2 Subsequent measurement of financial assets5.2.1After initial recognition, an entity shall measure a financial asset inaccordance with paragraphs 4.1–4.5 at fair value (see paragraphs 48, 48A andAG69–AG82 of IAS 39) or amortised cost.5.2.2An entity shall apply the impairment requirements in paragraphs 58–65and AG84–AG93 of IAS 39 to financial assets measured at amortised cost.5.2.3An entity shall apply the hedge accounting requirements in paragraphs89–102 of IAS 39 to a financial asset that is designated as a hedged item(see paragraphs 78–84 and AG98–AG101 of IAS 39).11© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 20095.3 Reclassification5.3.1If an entity reclassifies financial assets in accordance with paragraph 4.9, itshall apply the reclassification prospectively from the reclassification date.The entity shall not restate any previously recognised gains, losses orinterest.5.3.2If, in accordance with paragraph 4.9, an entity reclassifies a financial assetso that it is measured at fair value, its fair value is determined at thereclassification date. Any gain or loss arising from a difference between theprevious carrying amount and fair value is recognised in profit or loss.5.3.3If, in accordance with paragraph 4.9, an entity reclassifies a financial assetso that it is measured at amortised cost, its fair value at the reclassificationdate becomes its new carrying amount.5.4 Gains and losses5.4.1 A gain or loss on a financial asset that is measured at fair value and is notpart of a hedging relationship (see paragraphs 89–102 of IAS 39) shall berecognised in profit or loss unless the financial asset is an investment in anequity instrument and the entity has elected to present gains and losses onthat investment in other comprehensive income in accordance withparagraph 5.4.4.5.4.2 A gain or loss on a financial asset that is measured at amortised cost and isnot part of a hedging relationship (see paragraphs 89–102 of IAS 39) shall berecognised in profit or loss when the financial asset is derecognised,impaired or reclassified in accordance with paragraph 5.3.2, and throughthe amortisation process.5.4.3 A gain or loss on financial assets that are(a)hedged items (see paragraphs 78–84 and AG98–AG101 of IAS 39) shallbe recognised in accordance with paragraphs 89–102 of IAS 39.(b)accounted for using settlement date accounting shall be recognisedin accordance with paragraph 57 of IAS 39.Investments in equity instruments5.4.4At initial recognition, an entity may make an irrevocable election to presentin other comprehensive income subsequent changes in the fair value of aninvestment in an equity instrument within the scope of this IFRS that is notheld for trading.© Copyright IASCF12IFRS 9 F INANCIAL I NSTRUMENTS5.4.5If an entity makes the election in paragraph 5.4.4, it shall recognise inprofit or loss dividends from that investment when the entity’s right toreceive payment of the dividend is established in accordance with IAS 18 Revenue.Chapter 6 Hedge accounting – not usedChapter 7 Disclosures – not usedChapter 8 Effective date and transition8.1 Effective date8.1.1An entity shall apply this IFRS for annual periods beginning on or after1January 2013. Earlier application is permitted. If an entity applies thisIFRS in its financial statements for a period beginning before 1 January2013, it shall disclose that fact and at the same time apply theamendments in Appendix C.8.2 Transition8.2.1An entity shall apply this IFRS retrospectively, in accordance with IAS 8Accounting Policies, Changes in Accounting Estimates and Er or s, except as specified in paragraphs 8.2.4–8.2.13. This I FRS shall not be applied tofinancial assets that have already been derecognised at the date of initialapplication.8.2.2For the purposes of the transition provisions in paragraphs 8.2.3–8.2.13,the date of initial application is the date when an entity first applies the requirements of this IFRS. The date of initial application may be:(a)any date between the issue of this IFRS and 31 December 2010, forentities initially applying this IFRS before 1 January 2011; or(b)the beginning of the first reporting period in which the entityadopts this IFRS, for entities initially applying this IFRS on or after1 January 2011.8.2.3I f the date of initial application is not at the beginning of a reportingperiod, the entity shall disclose that fact and the reasons for using thatdate of initial application.13© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 20098.2.4At the date of initial application, an entity shall assess whether a financialasset meets the condition in paragraph 4.2(a) on the basis of the facts andcircumstances that exist at the date of initial application. The resultingclassification shall be applied retrospectively irrespective of the entity’sbusiness model in prior reporting periods.8.2.5If an entity measures a hybrid contract at fair value in accordance withparagraph 4.4 or paragraph 4.5 but the fair value of the hybrid contracthad not been determined in comparative reporting periods, the fair valueof the hybrid contract in the comparative reporting periods shall be thesum of the fair values of the components (ie the non-derivative host andthe embedded derivative) at the end of each comparative reportingperiod.8.2.6At the date of initial application, an entity shall recognise any differencebetween the fair value of the entire hybrid contract at the date of initialapplication and the sum of the fair values of the components of thehybrid contract at the date of initial application:(a)in the opening retained earnings of the reporting period of initialapplication if the entity initially applies this IFRS at the beginningof a reporting period; or(b)in profit or loss if the entity initially applies this I FRS during areporting period.8.2.7At the date of initial application, an entity may designate:(a) a financial asset as measured at fair value through profit or loss inaccordance with paragraph 4.5; or(b)an investment in an equity instrument as at fair value throughother comprehensive income in accordance with paragraph 5.4.4.Such designation shall be made on the basis of the facts andcircumstances that exist at the date of initial application. Thatclassification shall be applied retrospectively.8.2.8At the date of initial application, an entity:(a)shall revoke its previous designation of a financial asset asmeasured at fair value through profit or loss if that financial assetdoes not meet the condition in paragraph 4.5.(b)may revoke its previous designation of a financial asset asmeasured at fair value through profit or loss if that financial assetmeets the condition in paragraph 4.5.© Copyright IASCF14IFRS 9 F INANCIAL I NSTRUMENTSSuch revocation shall be made on the basis of the facts and circumstancesthat exist at the date of initial application. That classification shall beapplied retrospectively.8.2.9At the date of initial application, an entity shall apply paragraph 103M ofIAS 39 to determine when it:(a)may designate a financial liability as measured at fair value throughprofit or loss; and(b)shall or may revoke its previous designation of a financial liabilityas measured at fair value through profit or loss.Such revocation shall be made on the basis of the facts and circumstancesthat exist at the date of initial application. That classification shall beapplied retrospectively.8.2.10 f it is impracticable (as defined in AS 8) for an entity to applyretrospectively the effective interest method or the impairment requirementsin paragraphs 58–65 and AG84–AG93 of IAS 39, the entity shall treat thefair value of the financial asset at the end of each comparative period asits amortised cost. In those circumstances, the fair value of the financial asset at the date of initial application shall be treated as the newamortised cost of that financial asset at the date of initial application ofthis IFRS.8.2.11If an entity previously accounted for an investment in an unquotedequity instrument (or a derivative that is linked to and must be settled bydelivery of such an unquoted equity instrument) at cost in accordancewith IAS 39, it shall measure that instrument at fair value at the date ofinitial application. Any difference between the previous carrying amountand fair value shall be recognised in the opening retained earnings of thereporting period that includes the date of initial application.8.2.12Notwithstanding the requirement in paragraph 8.2.1, an entity thatadopts this IFRS for reporting periods beginning before 1 January 2012need not restate prior periods. If an entity does not restate prior periods,the entity shall recognise any difference between the previous carryingamount and the carrying amount at the beginning of the annual reporting period that includes the date of initial application in theopening retained earnings (or other component of equity, as appropriate)of the reporting period that includes the date of initial application.15© Copyright IASCFI NTERNATIONAL F INANCIAL R EPORTING S TANDARD N OVEMBER 20098.2.13If an entity prepares interim financial reports in accordance with IAS 34Interim Financial Reporting the entity need not apply the requirements inthis IFRS to interim periods prior to the date of initial application if it isimpracticable (as defined in IAS 8).© Copyright IASCF16IFRS 9 F INANCIAL I NSTRUMENTSAppendix ADefined termsThis appendix is an integral part of the IFRS.reclassification date The first day of the first reporting period following thechange in business model that results in an entityreclassifying financial assets.The following terms are defined in paragraph 11 of IAS 32 or paragraph 9 of IAS39 and are used in this IFRS with the meanings specified in IAS 32 or IAS 39:(a)amortised cost of a financial asset or financial liability(b)derivative(c)effective interest method(d)equity instrument(e)fair value(f)financial asset(g)financial instrument(h)financial liability(i)hedged item(j)hedging instrument(k)held for trading(l)regular way purchase or sale(m)transaction costs.17© Copyright IASCF。

中华人民共和国商务部公告 2016年 第78号

中华人民共和国商务部公告 2016年第78号佚名【期刊名称】《《中国对外经济贸易文告》》【年(卷),期】2017(000)001【摘要】2005年1月1日,商务部发布2004年第96号公告,决定对原产于美国、日本和韩国的进口非色散位移单模光纤征收反倾销税,实施期限为5年。

2008年6月23日,商务部发布2008年第19号公告,决定将株式会社OPTOMAGIC(OPTOMAGIC CO.,LTD)的反倾销税率调整为2.3%,自2008年4月15日起执行。

2009年5月26日,商务部发布2009年第36号公告,决定由LS电线株式会社(LS Cable Ltd)【总页数】15页(P22-36)【正文语种】中文【中图分类】F752.02【相关文献】1.中华人民共和国国家发展和改革委员会中华人民共和国商务部中华人民共和国海关总署中华人民共和国国家工商行政总局中华人民共和国国家质量监督检验检疫总局公告 [J],2.中华人民共和国国家发展和改革委员会中华人民共和国科学技术部中华人民共和国工业和信息化部中华人民共和国国土资源部中华人民共和国住房和城乡建设部中华人民共和国商务部公告 [J],3.中华人民共和国新闻出版总署中华人民共和国商务部中华人民共和国海关总署公告 2008年第1号关于音像制品进口及市场管理有关问题的公告 [J], ;;;4.中华人民共和国国家发展和改革委员会中华人民共和国科学技术部中华人民共和国国土资源部中华人民共和国住房和城乡建设部中华人民共和国商务部中华人民共和国海关总署公告 2018年第4号 [J], 中华人民共和国国家发展和改革委员会;中华人民共和国科学技术部;中华人民共和国国土资源部;中华人民共和国住房和城乡建设部;中华人民共和国商务部;中华人民共和国海关总署;5.中华人民共和国环境保护部中华人民共和国商务部中华人民共和国国家发展和改革委员会中华人民共和国海关总署国家质量监督检验检疫总局公告 2017年第3号 [J],因版权原因,仅展示原文概要,查看原文内容请购买。

全球历年保障措施案件统计GSGD-WTO

V_NUMBER S G_CTY_NAME CASE_ID Q4_2011Argentina ARG-SG-1 Q4_2011Argentina ARG-SG-2 Q4_2011Argentina ARG-SG-3 Q4_2011Argentina ARG-SG-4 Q4_2011Argentina ARG-SG-5 Q4_2011Argentina ARG-SG-6 Q4_2011Argentina ARG-SG-7 Q4_2011Australia AUS-SG-1 Q4_2011Australia AUS-SG-2 Q4_2011Brazil BRA-SG-1 Q4_2011Brazil BRA-SG-2 Q4_2011Brazil BRA-SG-3 Q4_2011Brazil BRA-SG-4 Q4_2011Bulgaria BGR-SG-1 Q4_2011Bulgaria BGR-SG-2 Q4_2011Bulgaria BGR-SG-3 Q4_2011Bulgaria BGR-SG-4 Q4_2011Bulgaria BGR-SG-5 Q4_2011Bulgaria BGR-SG-6 Q4_2011Canada CAN-SG-1 Q4_2011Canada CAN-SG-2 Q4_2011Canada CAN-SG-3 Q4_2011Chile CHL-SG-1 Q4_2011Chile CHL-SG-2 Q4_2011Chile CHL-SG-3 Q4_2011Chile CHL-SG-4 Q4_2011Chile CHL-SG-5 Q4_2011Chile CHL-SG-6 Q4_2011Chile CHL-SG-7 Q4_2011Chile CHL-SG-8 Q4_2011Chile CHL-SG-9 Q4_2011Chile CHL-SG-10 Q4_2011Chile CHL-SG-11 Q4_2011Chile CHL-SG-12 Q4_2011Chile CHL-SG-13 Q4_2011China CHN-SG-1 Q4_2011Colombia COL-SG-1 Q4_2011Colombia COL-SG-2 Q4_2011Colombia COL-SG-3 Q4_2011Colombia COL-SG-4 Q4_2011Costa Rica CRI-SG-1 Q4_2011Croatia HRV-SG-1 Q4_2011Czech Republic CZE-SG-1 Q4_2011Czech Republic CZE-SG-2 Q4_2011Czech Republic CZE-SG-3 Q4_2011Czech Republic CZE-SG-4 Q4_2011Czech Republic CZE-SG-5 Q4_2011Czech Republic CZE-SG-6 Q4_2011Czech Republic CZE-SG-7 Q4_2011Czech Republic CZE-SG-8Q4_2011Czech Republic CZE-SG-9 Q4_2011Dominican Republic DOM-SG-1 Q4_2011Dominican Republic DOM-SG-2 Q4_2011Dominican Republic DOM-SG-3 Q4_2011Dominican Republic DOM-SG-4 Q4_2011Dominican Republic DOM-SG-5 Q4_2011Ecuador ECU-SG-1 Q4_2011Ecuador ECU-SG-2 Q4_2011Ecuador ECU-SG-3 Q4_2011Ecuador ECU-SG-4 Q4_2011Ecuador ECU-SG-5 Q4_2011Ecuador ECU-SG-6 Q4_2011Ecuador ECU-SG-7 Q4_2011Ecuador ECU-SG-8 Q4_2011Egypt EGY-SG-1 Q4_2011Egypt EGY-SG-2 Q4_2011Egypt EGY-SG-3 Q4_2011Egypt EGY-SG-4 Q4_2011Egypt EGY-SG-5 Q4_2011Egypt EGY-SG-6 Q4_2011El Salvador SLV-SG-1 Q4_2011El Salvador SLV-SG-2 Q4_2011El Salvador SLV-SG-3 Q4_2011Estonia EST-SG-1 Q4_2011European Union EUN-SG-1 Q4_2011European Union EUN-SG-2 Q4_2011European Union EUN-SG-3 Q4_2011European Union EUN-SG-4 Q4_2011European Union EUN-SG-5GCC-SG-1 Q4_2011Gulf Cooperation CouncGCC-SG-2 Q4_2011Gulf Cooperation CouncQ4_2011Hungary HUN-SG-1 Q4_2011Hungary HUN-SG-2 Q4_2011Hungary HUN-SG-3 Q4_2011India IND-SG-1 Q4_2011India IND-SG-2 Q4_2011India IND-SG-3 Q4_2011India IND-SG-4 Q4_2011India IND-SG-5 Q4_2011India IND-SG-6 Q4_2011India IND-SG-7 Q4_2011India IND-SG-8 Q4_2011India IND-SG-9 Q4_2011India IND-SG-10 Q4_2011India IND-SG-11 Q4_2011India IND-SG-12 Q4_2011India IND-SG-13 Q4_2011India IND-SG-14 Q4_2011India IND-SG-15 Q4_2011India IND-SG-16 Q4_2011India IND-SG-17Q4_2011India IND-SG-19 Q4_2011India IND-SG-18 Q4_2011India IND-SG-20 Q4_2011India IND-SG-21 Q4_2011India IND-SG-22 Q4_2011India IND-SG-23 Q4_2011India IND-SG-24 Q4_2011India IND-SG-25 Q4_2011India IND-SG-26 Q4_2011India IND-SG-27 Q4_2011India IND-SG-28 Q4_2011Indonesia IDN-SG-1 Q4_2011Indonesia IDN-SG-2 Q4_2011Indonesia IDN-SG-3 Q4_2011Indonesia IDN-SG-4 Q4_2011Indonesia IDN-SG-5 Q4_2011Indonesia IDN-SG-6 Q4_2011Indonesia IDN-SG-7 Q4_2011Indonesia IDN-SG-8 Q4_2011Indonesia IDN-SG-9 Q4_2011Indonesia IDN-SG-10 Q4_2011Indonesia IDN-SG-11 Q4_2011Indonesia IDN-SG-12 Q4_2011Indonesia IDN-SG-13 Q4_2011Indonesia IDN-SG-14 Q4_2011Indonesia IDN-SG-15 Q4_2011Indonesia IDN-SG-16 Q4_2011Indonesia IDN-SG-17 Q4_2011Indonesia IDN-SG-18 Q4_2011Israel ISR-SG-1 Q4_2011Israel ISR-SG-2 Q4_2011Jamaica JAM-SG-1 Q4_2011Japan JPN-SG-1 Q4_2011Japan JPN-SG-2 Q4_2011Japan JPN-SG-3 Q4_2011Jordan JOR-SG-1 Q4_2011Jordan JOR-SG-2 Q4_2011Jordan JOR-SG-3 Q4_2011Jordan JOR-SG-4 Q4_2011Jordan JOR-SG-5 Q4_2011Jordan JOR-SG-6 Q4_2011Jordan JOR-SG-7 Q4_2011Jordan JOR-SG-8 Q4_2011Jordan JOR-SG-9 Q4_2011Jordan JOR-SG-10 Q4_2011Jordan JOR-SG-11 Q4_2011Jordan JOR-SG-12 Q4_2011Jordan JOR-SG-13 Q4_2011Jordan JOR-SG-14 Q4_2011Jordan JOR-SG-15 Q4_2011Jordan JOR-SG-16Q4_2011Korea KOR-SG-1 Q4_2011Korea KOR-SG-2 Q4_2011Korea KOR-SG-3 Q4_2011Korea KOR-SG-4 Q4_2011Kyrgyz Republic KGZ-SG-1 Q4_2011Kyrgyz Republic KGZ-SG-2 Q4_2011Kyrgyz Republic KGZ-SG-3 Q4_2011Latvia LVA-SG-1 Q4_2011Latvia LVA-SG-2 Q4_2011Lithuania LTU-SG-1 Q4_2011Malaysia MYS-SG-1 Q4_2011Mexico MEX-SG-1 Q4_2011Mexico MEX-SG-2 Q4_2011Moldova MDA-SG-1 Q4_2011Moldova MDA-SG-2 Q4_2011Morocco MAR-SG-1 Q4_2011Morocco MAR-SG-2 Q4_2011Morocco MAR-SG-3 Q4_2011Morocco MAR-SG-4 Q4_2011Morocco MAR-SG-5 Q4_2011Pakistan PAK-SG-1 Q4_2011Panama PAN-SG-1 Q4_2011Peru PER-SG-1 Q4_2011Peru PER-SG-2 Q4_2011Philippines PHL-SG-1 Q4_2011Philippines PHL-SG-2 Q4_2011Philippines PHL-SG-3 Q4_2011Philippines PHL-SG-4 Q4_2011Philippines PHL-SG-5 Q4_2011Philippines PHL-SG-6 Q4_2011Philippines PHL-SG-7 Q4_2011Philippines PHL-SG-8 Q4_2011Philippines PHL-SG-9 Q4_2011Poland POL-SG-1 Q4_2011Poland POL-SG-2 Q4_2011Poland POL-SG-3 Q4_2011Poland POL-SG-4 Q4_2011Poland POL-SG-5 Q4_2011Slovak Republic SVK-SG-1 Q4_2011Slovak Republic SVK-SG-2 Q4_2011Slovak Republic SVK-SG-3 Q4_2011Slovenia SVN-SG-1 Q4_2011South Africa ZAF-SG-1 Q4_2011Thailand THA-SG-1 Q4_2011Tunisia TUN-SG-1 Q4_2011Tunisia TUN-SG-2 Q4_2011Turkey TUR-SG-1 Q4_2011Turkey TUR-SG-2 Q4_2011Turkey TUR-SG-3 Q4_2011Turkey TUR-SG-4 Q4_2011Turkey TUR-SG-5Q4_2011Turkey TUR-SG-6 Q4_2011Turkey TUR-SG-7 Q4_2011Turkey TUR-SG-8 Q4_2011Turkey TUR-SG-9 Q4_2011Turkey TUR-SG-10 Q4_2011Turkey TUR-SG-11 Q4_2011Turkey TUR-SG-12 Q4_2011Turkey TUR-SG-13 Q4_2011Turkey TUR-SG-14 Q4_2011Turkey TUR-SG-15 Q4_2011Turkey TUR-SG-16 Q4_2011Ukraine UKR-SG-1 Q4_2011Ukraine UKR-SG-2 Q4_2011Ukraine UKR-SG-3 Q4_2011Ukraine UKR-SG-4 Q4_2011Ukraine UKR-SG-5 Q4_2011Ukraine UKR-SG-6 Q4_2011Ukraine UKR-SG-7 Q4_2011Ukraine UKR-SG-8 Q4_2011Ukraine UKR-SG-9 Q4_2011USA USA-SG-1 Q4_2011USA USA-SG-2 Q4_2011USA USA-SG-3 Q4_2011USA USA-SG-4 Q4_2011USA USA-SG-5 Q4_2011USA USA-SG-6 Q4_2011USA USA-SG-7 Q4_2011USA USA-SG-8 Q4_2011USA USA-SG-9 Q4_2011USA USA-SG-10 Q4_2011Venezuela VEN-SG-1 Q4_2011Venezuela VEN-SG-2 Q4_2011Venezuela VEN-SG-3 Q4_2011Venezuela VEN-SG-5 Q4_2011Venezuela VEN-SG-6 Q4_2011Venezuela VEN-SG-7 Q4_2011Venezuela VEN-SG-8 Q4_2011Venezuela VEN-SG-9 Q4_2011Venezuela VEN-SG-4 Q4_2011Vietnam VNM-SG-1PRODUCT PET_DATE Footwear10-25-1996 Toys09-22-1997 Footwear MI Motorcycles MI Peaches MI Coloured Television Sets MI Compact Discs Recordable (CD-R)MISwine Meat MISwine Meat MIToys04/26/1996 Coconuts MICD-R and DVD-R12-21-2007 Fine or Table Wine07-01-2011 Non-Aqueous Ammonium Nitrate MICrown Corks10-25-2001 Ammonium Nitrate MISteel07-08-2002 Urea05-14-2002 Iron and Steel MISteel MI Bicycles01-11-2005 Unmanufactured Bright Virginia Flue-Cured Tobacco10-17-2005 Tyres MIWheat/Wheat Flour/Cane or Beet Sugar/Edible Vegetable Oils MISocks (Synthetic and Cotton)MILiquid & Powdered Milk MIMixed Oils12/06/2000 Lighters08/10/2001 Steel12/17/2001 Steel03/26/2002 Fructose/Glucose05/20/2002 Wheat Flour10/05/2004 Powdered Milk/Liquid Milk and Gouda Cheese08-10-2006 Powdered Milk and Gouda Cheese08-10-2009 Maize otherwise worked MISteel MITaxis MI Domestic Blenders12/11/2003 Electric Smoothing Irons12/11/2003 Sodium Bicarbonate07-08-2009 Rice MISemi-hard Cheese and Cheese Substitutes MICane/Beet Sugar MI Footwear MI Isoglucose MICocoa Powder MICitric Acid MIWire/Ropes and Cables MITubes and Pipes MI Ammonium Nitrate MISteel MI Bottles/Flasks and Other Glass Containers MIToilet Paper08-10-2009 Polypropylene Bags and Tubular Fabric MIToilet Paper MI Certain Sports and Other Socks MI Sandals MI Matches MI Fibreboard11-06-2002 Smooth Ceramics05/27/2003 Ceramics and Porcelains05/17/2003 Paper and Paperboard06/05/2003 Pneumatic Tyres of Rubber08/04/2003 Windshields02-24-2010 Safety Matches MI Common Fluorescent Lamps MI Powdered Milk MI Blankets MI Cotton Yarn MI Cotton Textile and Mixed Cotton Textile MIPork MIRice MI Fertilizers MISwine Meat MISteel MI Mandarins MI Salmon MI Strawberries MI Wireless Wide Area Networking06-11-2010 Uncoated Paper and Paper Board MI Angles/Channels/Beams MISteel05-16-2002 Ammonium Nitrate MI Certain Sugar Products MI Acetylene Black MI Styrene Butadiene Rubber MI Carbon Black MI Slabstock Polyol MI Propylene Glycol MI Hardboard MI Phenol MI Acetone MIWhite/Yellow Phosphorus MI Gamma Ferric Oxide/Magnetic Iron Oxide MI Methylene Chloride二氯甲烷MI Epichlorohydrin (ECH)环氧氯丙烷MI Vegetable Oil植物油MI Bisphenol A双酚A MI Starch/Modified Starches and Manioc Based Sago变性淀粉和木薯MI Phthalic Anhydride邻苯二甲酸酐MI Linear Alkyl Benzene直链烷基苯MIOxo Alcohols羰基合成醇MI Dimethoate Technical有机磷杀虫剂MI Acrylic Fibre丙烯酸纤维MIHot Rolled Coils/Sheets/Strips热轧板卷材MI Coated Paper and Paper Board铜版纸和纸板MI Uncoated Paper and Copy Paper未涂布纸和复写纸MIPlain Particle Board普通刨花板MI Unwrought Aluminium/Aluminium Waste/Aluminium Scraps未锻轧铝铝废碎料MI Sodium Hydroxide (also known as Caustic Soda)苛性钠MIN1/3-dimethyl butyl-N Phenyl paraphenylenediamine (also known as PX-13 or 6-PPD)防老剂6ppd MI Phthalic Anhydride邻苯二甲酸酐MI Ceramic Tableware MI Lighters MICast Glass and Rolled Glass MI Dextrose Monohydrate MIWire Nail/Wire of Iron/Non-Alloy Steel (Not Plated)MI Aluminium Foil Food Container and Aluminium Tray and Plain Lid MIWire of Iron/Non-Alloy Steel (not plated/coated)01-14-2010 Wire of Iron/Non-Alloy Steel (plated with zinc)11-18-2009 Stranded Wire/Ropes and Cables for Locked Coil/Flattened Strands and Non-Rotating Wire Ropes01-27-2010 Stranded Wire/Ropes and Cables (excluding Locked Coil/Flattened Strands and Non-Rotating Wire Ropes04-16-2010 Cotton Yarn other than Sewing Thread06-22-2010 Woven Fabrics of Cotton06-22-2010 Tarpaulins/Awnings and Sunblinds of Synthetic Fibres03-16-2011 Polypropylene in Granule Form MI Articles of Iron or Steel Wire08-02-2011 Conveyor Belts or Belting reinforced only with metal of a width exceeding 20 cm10-10-2011 Articles of Finished Casing and Tubing 11-30-2011 Mackerel MISteel Rebars03-23-2009 Glass Wool and Rock Wool11-28-2010 Cement MI Tatami-Omote MI Welsh Onions MI Shitake Mushrooms MI Biscuits/Chocolates MI Magnetic Tapes MIPasta MI Ceramic Sinks/Sanitary Ware Products MI Ceramic Tiles MI Cooking Appliances MI Electric Accumulators MI Cooking Appliances MI Aerated Water MI Insecticides MI Footwear MI Ceramic Tiles MIWhite Cement (whether or not artificially coloured)MI Ceramic Tiles MI Clinker MIBars and Rods of Iron and Steel MISoybean Oil MIDairy Products MI Bicycles and Parts MIGarlic MIWhite Sugar MI Wheat Flour MI Poultry Eggs MISwine Meat05-18-1999 Live Pigs and Pork05-31-2002 Pastry Yeast MIHot-Rolled Coils MI Plywood Panels01-01-2002 Steel Tubes04-06-2010 Sugar MI Cosmetic and Perfume Products MI Bananas MI Rubber Plates and Sheets MI Ceramic Tiles MI Polyvinyl Chloride (PVC)MI Machine-made Carpets MI Footwear05-10-2005 Printed Film in Rolls08-11-2006 Certain Textiles06-23-2004 Cotton Yarn01-19-2009 Grey Portland Cement MI Ceramic Tiles MI Tomato Paste MI Figured Glass MIGlass Mirrors MIFloat Glass MI Sodium Tripolyphosphates MISteel Angle Bars MI Testliner Board MI Potassium Nitrate MI Calcium Carbide MI Matches MIWater Heaters MISteel MISwine Meat MISugar MI Ammonium Nitrate MISwine Meat MI Lysine04-05-2007 Glass Block09-29-2010 Bottles and other Containers of Glass and Glassware of a kind used for Table and Kitchen Purposes MITaps/Cocks and Valves/Locks and Fittings and Mountings Suitable for Furniture and for Buildings MI Thermometers MI Activated Earth and Clays MI Certain Glasswares MI Unframed Glass Mirrors MI Certain Voltmeters and Ammeters MIFootwear MISalt MI Vacuum Cleaners MI Steam Smoothing Irons MI Motorcycles MI Frames and Mountings for Spectacles MI Travel Goods/Handbags and Similar Containers MI Certain Electrical Appliances MI Cotton Yarn MI Matches MI Polyethylene Terephthalate MI Casing and Pump-Compressor Seamless Steel Pipes MI Matches MILiquid Chroline MISheet Glass Thermally Polished (float glass) Unreinforced/Transparent/Colorless and with thickness more MIMI Mineral Fertilisers (containing nitrogen/phosphorus and potassium with a nitrogen content exceeding 10 peFerro-manganese containing by weight more than 2 per cent of carbon (except in ferro-manganese granule MI Cooling and Refrigerating Equipment MI Certain Products of Crude Oil Processing MIMotor Cars MI Tomatoes MI Brooms MI Tomatoes and Peppers MI Wheat Gluten MILamb Meat10-07-1998 Steel Wire Rod MILine Pipe06-30-1999 Crabmeat03-02-2000 Extruded Rubber Thread MISteel MICold-Rolled Steel MIHot-Rolled Steel MITyres MI Turkey Meat MIPaper MIIron/Steel U-Sections MI Clothing Items MI Footwear09-23-2002 Disposable Syringes MIFloat Glass MIF_INJ_DATE F_INJ_DEC WTO_INIT_DATE P_DATE P_INJ_DEC P_DEC P_SG_DATE P_SG_MEA02-25-199702-25-1997A A02-25-1997SD06-12-1997A02-03-199809-29-1998N T....07-21-2000.....07-21-2000A07-22-200005-10-2000A A..06-22-2001A01-12-200101-12-2001A A01-12-2001SD07-17-2001A07-16-200407-05-2004A A07-20-2004AVD01-20-2005A06-06-2006.B B..02-02-2007A06-26-1998.B B..11-12-1998A10-17-2007.B B..12-14-2007N06-18-199606-18-1996A A07-04-1996AVD11-14-1996A08-10-2001.B B..08-05-2002A09-05-2008.B B..10-23-2009N03-15-2012MI MI MI MI MI MI MI11-10-200011-27-2000A A11-28-2000AVD..11-19-2001.B B..02-11-2002A01-16-200207-01-2002A A07-01-2002AVD12-20-2002A09-09-2002.B B..07-14-2003A09-10-2002.B B..01-08-2003A04-30-2003.B B..01-28-2004N03-25-2002.B B..07-04-2002A02-10-2005.B B..09-01-2005P12-29-2005.......08-30-1999.B B..12-24-1999N09-30-199911-26-1999A A11-01-1999AVD01-18-2000A02-09-200007-01-2000P P07-01-2000AVD11-07-2000P06-21-200007-13-2000A A07-13-2000AVD12-06-2000A12-19-200012-22-2000A A01-13-2001AVD..08-31-2001.B B..MI MI12-28-2001.......04-05-2002.B B..07-16-2002P06-08-200207-05-2002OTH OTH07-01-2002AVD08-30-2002OTH12-10-200412-15-2004A A MI AVD02-10-2005A09-08-200610-06-2006A A10-13-2006AVD MI A09-04-200910-02-2009A A10-10-2009AVD01-13-2010N04-27-201204-27-2012A A04-27-2012AVD MI MI05-20-200205-21-2002A A05-24-2002TRQ11-01-2002A06-28-1999.B B..02-29-2000N01-26-2004.B B..MI MI01-26-2004.B B..08-17-2004N09-12-2009MI MI MI MI MI MI MI03-04-200203-07-2002A A03-12-2002AVD12-15-2004N08-28-2009MI P P06-23-2009SD MI P03-03-199903-03-1999A A03-12-1999MI09-15-1999A11-01-2000.B B..07-25-2001N12-20-200001-08-2001A A01-10-2001AVD07-26-2001P11-15-200111-27-2001A A11-30-2001MI06-11-2002A01-30-2002.B B..10-16-2002N02-27-2002.B B..02-19-2003N03-06-2002.B B..02-24-2003P08-14-200202-06-2003A A02-10-2003DPU08-28-2003A08-28-2002.B B..04-29-2003N 04-15-2009.B B..02-02-2010A 10-12-2009.B B.... 12-17-200903-16-2010A A04-01-2010AVD10-05-2010A 01-14-2010.B B.... 03-02-2010MI A A05-20-2010AVD10-25-2010A 01-12-1999MI OTH..... 10-28-199911-14-2000A A12-01-2000AVD10-17-2001A 12-05-200202-20-2003A A01-09-2003AVD07-25-2003A 07-03-200308-20-2003A A09-02-2003AVD01-27-2004A 08-13-2003MI OTH..... 10-31-2003....... 10-31-2003.B B..01-27-2004N 04-19-201005-27-2010N N..09-23-2010A 08-05-199808-08-1998A A08-08-1998AVD02-01-1999A 09-19-1999.B B..02-25-2000A 09-25-200009-25-2000A A09-26-2000AVD03-30-2001A 02-10-200802-10-2008A A02-12-2008SD08-20-2008A 11-24-201112-29-2011A A12-29-2011SD MI MI 02-23-201202-29-2012A A02-29-2012AVD MI MI 01-19-2000MI MI MI MI MI.. 06-21-2000MI MI MI MI MI05-31-2001N 11-08-2000.B B..10-19-2001N 04-10-2003MI MI MI MI MI MI MI 03-28-200203-28-2002A A03-29-2002TRQ09-02-2002A 07-11-200311-06-2003A A11-09-2003TRQ/SD03-12-2004A 03-06-200408-13-2004A A08-15-2004TRQ/SD01-06-2005A 07-06-2005....... 06-30-2010.B B.... 11-07-2009.B B.... 11-07-2009.B B.... 05-22-200205-22-2002A A06-03-2002TRQ12-23-2002P 01-02-200302-03-2003P P02-01-2003SD06-18-2003P 07-21-200307-18-2003A A07-23-2003TRQ/AVD11-27-2003A 11-28-1997.B B..07-15-1998A 01-19-1998.B B.... 02-05-1998.B B..07-15-1998A 02-26-1998.B B..09-17-1998A 02-26-1998.B B..09-11-1998A 05-24-1998.B B..11-12-1998A 02-02-1999.B B..06-11-1999A 06-16-1999.B B..10-07-1999A 09-15-1999.B B..01-17-2000A 07-06-2000.B B..12-20-2000A 07-17-2000.B B..12-15-2000A 03-14-2002.B B..07-05-2002A 05-27-2002.B B..01-23-2003N 03-06-2003.B B..10-27-2003A 07-04-2004.B B..02-16-2005P 11-28-200801-01-2009A A01-29-2009AVD05-28-2009A 12-19-200801-30-2009A N....01-16-2009.B B..05-27-2009A 01-21-200902-02-2009A A03-23-2009AVD05-14-2009A 04-09-200904-15-2009A N..09-30-2009T 04-09-200904-23-2009A T.... 04-20-200904-24-2009A N.... 04-20-200904-24-2009A N.... 04-22-200905-04-2009A T.... 05-22-200905-28-2009A N..11-04-2009W 08-20-200910-15-2009A A12-04-2009AVD04-09-2010A 12-27-2010.B B..06-06-2011A 08-10-201109-23-2011A A01-17-2012AVD03-29-2012A 10-19-2004.B B..05-10-2005A 07-28-2005.B B..01-19-2006N 01-02-2006.B B..09-07-2006N 05-14-2008.B B..08-24-2009A 11-05-2008.B B..09-24-2009A 01-19-201006-14-2010N T.... 01-19-2010.B B..MI A 01-21-2010.B B..MI A 02-05-2010.B B..MI A 04-30-2010.B B..MI A 06-25-2010.B B..01-17-2011A 06-25-2010.B B..MI A 03-22-2011.B B..MI A 04-26-201106-16-2011N T.... 08-19-2011.B B..01-23-2012A 11-03-2011.B B..02-05-2012A 01-20-2012MI MI MI MI MI MI MI 01-27-2012.B B..03-01-2012A 03-26-200906-17-2009A A06-23-2009SD MI MI 01-11-2011.B B..MI A 10-16-200302-16-2004A A02-16-2004AVD04-20-2004A 12-22-200004-20-2001A A04-23-2001SD12-21-2001N 12-22-200004-20-2001A A04-23-2001SD12-21-2001N 12-22-200004-20-2001A A04-23-2001SD12-21-2001N 12-10-2000.B B..08-21-2001P 01-24-200201-24-2002A A02-01-2002SD05-01-2002A 05-18-2002.B B..01-07-2003A 05-27-2002.B B..01-07-2003A 05-29-2002.B B..10-23-2002N 05-29-2002.B B..10-23-2002N 05-29-2002.B B..10-23-2002N 05-29-2002.B B..10-23-2002N 09-17-2002.B B..04-24-2003N 01-16-2005.B B..08-29-2005A 08-01-2006.B B..01-10-2007A 01-31-2007....... 11-16-2008.B B..05-19-2009N 11-23-2008.B B..07-20-2009A 09-16-2010....... 04-04-2012MI MI MI MI MI MI MI08-30-1995......A 05-28-1996.B B..12-02-1996A 08-27-1996.B B..01-21-1997A 10-16-199911-08-1999P P11-13-1999AVD02-02-2000A 02-17-2009MI MI MI MI MI MI MI 04-28-200905-22-2009A A06-11-2009SD11-05-2009A 10-15-2010MI MI MI MI MI MI MI 05-20-199905-20-1999A A06-01-1999SD12-14-1999A 07-01-2002.B B..03-17-2003A 01-13-2001MI MI MI MI MI02-11-2002A 05-09-201108-22-2011N T.... 08-15-200207-02-2005W..... 07-03-2010.B B..03-28-2012N 05-21-2003.B B..09-24-2003A 06-18-200312-23-2004P P MI AVD MI T 06-26-200008-10-2000A A08-10-2000AVD01-26-2001A 12-05-2000.....06-27-2001N 01-24-2005.B B..09-02-2005A 08-10-2009.B B.... 07-19-2010.B B..11-30-2010N 06-17-2005.....08-15-2005T 09-11-200602-13-2007A A04-12-2007AVD05-21-2007A 08-21-200410-12-2004A A10-14-2004MI.. 03-13-200908-17-2009MI T.... 05-28-200111-07-2001A A12-10-2001SD06-25-2003A 05-28-200111-26-2001A A01-09-2002SD03-27-2002A 11-26-2001.....12-26-2001N 04-16-200310-13-2003A A10-13-2003SD03-30-2004A 04-16-200309-23-2003A A10-13-2003TRQ/SD03-30-2004A 05-21-200309-23-2003A A10-13-2003TRQ/SD03-30-2004A 03-08-200607-06-2006A A07-13-2006SD.. 08-11-200801-12-2009A A03-10-2009SD MI A 11-16-2009MI A A05-26-2010SD11-24-2010A 12-22-2000MI MI MI MI MI MI MI 02-18-2002.B B..06-05-2003A 05-07-2002.B B..10-15-2003A 05-28-2002.B B..06-05-2003A 06-08-200208-14-2002P P08-19-2002TRQ/AVD03-07-2003P 05-05-19995/28/1999A A05-21-1999AVD11-19-1999N 10-20-2000.B B..04-25-2001A 10-14-2002.B B..04-08-2003A 10-15-199811-20-1998A A11-21-1998SD.. 05-11-200705-11-2007A A05-11-2007AVD09-25-2007A 12-16-201001-14-2011A A01-15-2011AVD MI A 06-16-2006MI MI MI MI MI MI MI 06-16-2006MI MI MI MI MI MI MI 07-17-2004.....03-04-2005N 07-17-2004.....06-08-2005A 07-17-2004....... 07-17-2004.....05-03-2005N 07-17-2004.....07-13-2005P01-05-2006.B B..07-11-2006A 01-05-2006.B B..07-11-2006A 01-05-2006.B B..07-11-2006A 01-05-2006.B B..07-11-2006A 08-15-200608-15-2006A A08-15-2006SD02-02-2007A 02-11-2007.B B..01-30-2008A 06-05-2007.B B..03-07-2008A 12-19-2007.B B..08-10-2008P05-23-200805-23-2008A A05-23-2008SD08-11-2008P05-02-200905-02-2009A A06-06-2009SD12-06-2009A 02-28-2011.B B..MI A 09-01-2007.B B..07-23-2008A 11-26-2008.B B..MI A 03-17-2009.B B..MI MI 08-27-2009MI A A11-13-2009AVD MI MI 02-03-2010.B B..12-28-2010N 02-17-201012-25-2010MI T....05-06-201004-06-2011MI T....01-29-201112-28-2011N T....07-02-2011MI MI MI MI MI MI MI 03-29-1995.B B..08-12-1996N 03-04-1996.B B..07-02-1996P03-11-1996.B B..08-12-1996N 10-01-1997.B B..01-15-1998A 10-07-1998.B B..02-09-1999A 01-12-1999.B B..05-25-1999OTH 07-29-1999.B B..10-28-1999A 03-15-2000.B B..07-11-2000N 06-15-2000.B B..10-03-2000N 06-28-2001.B B..10-22-2001P01-28-2000.......01-28-2000.......03-08-2000.B B..12-20-2000A 08-24-2001MI N N....10-16-200109-23-2002A MI MI MI07-31-2003A 11-01-200109-03-2002A A10-01-2002AVD MI MI 09-10-2002MI MI MI MI MI MI MI 09-23-2002MI MI MI MI MI MI MI ..OTH OTH....07-01-200910-30-2009A MI MI MI02-08-2010AF_DATE F_DEC F_SG_DATE F_SG_M T ERM_DATE D1_DATE D2_DATE D3_DATE 07-25-1997A09-13-1997SD.11-30-199902-25-2000. ........07-21-2000A07-22-2000TRQ/SD.07-22-200107-22-200207-21-2003 06-22-2001A06-22-2001SD.06-22-200206-22-200306-22-2004 07-17-2001A08-08-2001SD.01-18-200201-18-200301-18-2004 02-09-2005P02-09-2005QR.12-31-200512-31-2006.05-29-2007A05-30-2007SD.05-30-200805-30-2009.01-22-1999N......04-04-2008N......12-19-1996A01-10-1997AVD.12-31-199712-31-199812-31-1999 08-05-2002A09-01-2002QR.08-31-200308-31-200408-31-2005 ....10-23-2009...MI MI MI MI MI MI MI MI ....03-06-2001...12-27-2002A11-19-2002SD.MI MI.12-20-2002A12-28-2002TRQ/SD.12-28-200312-28-200406-30-2005 07-14-2003N......01-08-2003N......01-28-2004N......10-14-2003N......06-06-2006N......02-16-2006W......12-24-1999T......01-18-2000P01-22-2000AVD.MI MI MI11-07-2000P11-07-2000AVD.04-30-200110-31-2001.12-06-2000A01-10-2001AVD.... ....04-25-2001...01-09-2002N......03-26-2002T......MI P07-16-2002AVD.MI MI MI08-30-2002OTH08-30-2002AVD07-05-200207-30-2003..02-10-2005A Feb/Mar 2005AVD.12-10-2005..12-14-2006A12-14-2006AVD.... ....01-13-2010...MI MI MI MI MI MI MI MI.05-23-200305-23-200405-23-2005 11-01-2002A11-20-2002TRQ/AVD02-29-2000N......08-17-2004N......08-17-2004T..08-17-2004...MI MI MI MI MI MI MI MI12-15-2004N......MI P11-09-2009SD....09-15-1999A09-20-1999TRQ.MI MI MI07-25-2001N......07-26-2001P07-26-2001TRQ MI MI MI MI06-11-2002A06-14-2002TRQ/SD.01-01-200301-01-200401-01-2005 10-16-2002N......02-19-2003N......02-24-2003P03-01-2003TRQ.12-31-200312-31-2004.08-28-2003A08-22-2003DPU.04-30-2004..04-29-2003N......02-02-2010N..02-19-2010...11-26-2009T..11-26-2009...10-06-2010A10-18-2010AVD.04-19-201110-20-2011.04-26-2010W..05-04-2010...10-26-2010A12-06-2010AVD.12-07-201112-08-2012. ........A A10-24-2001AVD.MI MI MI07-25-2003A07-16-2003QR.MI MI MI01-27-2004A02-14-2004SD.06-30-200410-31-200403-01-2005 ........02-11-2004T......01-27-2004N......10-11-2010A11-01-2010SD.11-01-201111-01-201205-01-2013 02-01-1999A02-19-1999AVD.02-18-200002-18-200108-04-2001 02-25-2000A02-27-2000MI.02-28-2001..03-30-2001A04-12-2001AVD.04-11-200204-11-200309-24-2003 08-20-2008A08-20-2008SD.02-12-200902-12-2010.MI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MI02-05-2001W......05-31-2001N......10-19-2001N......MI MI MI MI MI MI MI MI09-02-2002A09-29-2002TRQ.09-28-200309-28-200403-28-2005 03-12-2004A04-11-2004TRQ/SD.04-10-200604-10-200704-10-2007 01-06-2005A02-06-2005TRQ/SD.08-13-200508-13-200608-13-2007 12-23-2005W......10-29-2010W..01-26-2011...May 2010T..May 2010...May 2010T..May 2010...12-23-2002P04-02-2003TRQ.10-03-200304-03-200410-03-2004 06-18-2003P06-23-2003SD.07-01-2004...04-30-2004..11-27-2003A11-21-2003TRQ/AVD12-10-1998A12-10-1998SD.12-10-199912-10-2000.05-01-1998T......02-05-1999A02-28-1999AVD.MI MI.12-24-1998A12-24-1998TRQ/AVD.12-24-199906-24-2000..12-24-199906-24-2000.12-24-1998A12-24-1998TRQ/AVD11-12-1998N......06-30-1999A06-30-1999AVD.02-29-200006-29-2001.01-27-2000A01-27-2000AVD/SD.01-26-200101-26-200207-26-2002 01-17-2000N......01-24-2001A01-24-2001AVD.01-23-200201-23-200307-23-2003 MI N......10-30-2002A10-30-2002AVD.10-30-2003..01-23-2003N......MI N......02-16-2005P05-02-2005AVD.05-02-200605-02-2007.05-28-2009A07-01-2009AVD.... ....11-18-2009...05-27-2009N..MI...05-14-2009A08-27-2009AVD.03-23-2010.. ........ ....08-26-2009... ....11-13-2009... ....11-05-2009... ....11-24-2009...11-06-2009T..11-06-2009...MI MI MI MI MI MI MI MI06-06-2011A08-30-2011AVD.08-31-2012..MI MI MI MI MI MI MI MI02-06-2006A01-04-2006SD.MI MI MI01-19-2006N......09-07-2006N......08-24-2009A08-24-2009SD.08-24-201008-24-2011.09-24-2009A10-01-2009AVD.10-01-201010-01-2011. ....06-14-2010...03-23-2011A03-23-2011SD.03-23-201203-23-2013.03-23-2011A03-23-2011SD.03-23-201203-23-2013.03-23-2011A03-23-2011SD.03-23-201203-23-2013.03-23-2011A03-23-2011SD.03-23-201203-23-2013.01-20-2011A06-06-2011SD.06-06-201206-06-2013.03-23-2011A03-23-2011SD.03-23-201203-23-2013.11-17-2011A11-17-2011SD.11-17-201211-17-2013. ....06-16-2011...MI MI MI MI MI MI MI MI04-13-2012N..04-13-2012...MI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MI08-17-2009T..08-17-2009...MI MI MI MI MI MI MI MI08-09-2004N......12-21-2001N......12-21-2001N......12-21-2001N......08-21-2001P09-01-2001SD06-26-200108-31-200208-31-200308-31-2004 05-01-2002A05-01-2002SD.04-30-200304-30-200404-30-2005 02-07-2003A02-25-2003SD.02-24-200402-24-200502-24-2006 02-07-2003A02-25-2003SD.02-24-200402-24-200502-24-2006 10-23-2002N......10-23-2002N......10-23-2002N......10-23-2002N......04-24-2003N......10-12-2005A10-16-2005SD.10-16-200610-16-200710-16-2008 02-20-2007A02-19-2007SD.02-19-200802-19-2009.07-25-2007W......05-19-2009T......MI A03-09-2010SD.03-09-201103-09-2012.10-05-2010T..10-05-2010...MI MI MI MI MI MI MI MI03-12-1996N......01-21-1997A03-01-1997QR.02-28-199802-28-199902-28-2000 03-24-1997N......05-30-2000A06-01-2000AVD/SD.05-31-200105-31-200205-31-2003 MI MI MI MI MI MI MI MI11-05-2009A11-10-2009SD....MI MI MI MI MI MI MI MI12-14-1999A12-18-1999DPU.12-18-200012-17-2001.06-18-2003OTH07-04-2003TRQ/SD.12-31-200312-31-200412-31-2005 02-11-2002A03-01-2002AVD.12-31-200212-31-2003. ....08-22-2011... ........ ....03-28-2012...09-24-2003A01-01-2004AVD.MI MI MI ........02-21-2001A09-01-2001AVD.MI MI MI06-27-2001N......09-02-2005A01-26-2006TRQ/SD.11-30-200611-30-200711-30-2008 08-06-2010W..08-06-2010...12-10-2010T..12-10-2010...08-15-2005T......10-08-2007A10-08-2007AVD.... ....05-04-2005... ....08-17-2009...06-25-2003A12-10-2001SD.MI MI MI04-11-2002A04-11-2002SD.MI MI MI12-26-2001N......03-30-2004A10-13-2003TRQ/SD.MI MI MI03-30-2004A10-13-2003TRQ/SD.MI MI MI03-30-2004A10-13-2003TRQ/SD.MI MI MI02-06-2007T..02-06-2007...07-27-2009A07-27-2009SD.03-11-201003-11-2011.01-03-2011A07-22-2011SD.07-23-201207-23-2013.MI MI MI MI MI MI MI MI.12-31-200304-30-2004.06-05-2003A08-13-2003TRQ/AVD.04-30-2004..11-28-2003A11-28-2003TRQ/AVD.12-31-200304-30-2004.06-05-2003A08-13-2003TRQ/AVD.03-07-200403-07-2005.03-07-2003P03-08-2003TRQ/AVD11-19-1999T..11-19-1999...04-25-2001A05-01-2001QR.MI MI MI04-08-2003A04-20-2003QR.04-19-200404-19-200504-19-2006 ....01-14-1999...09-25-2007A12-14-2007AVD.05-11-200805-11-2009.08-17-2011A08-18-2011AVD/SD.01-15-201201-15-2013.MI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MI03-04-2005N......QR.MI MI MI06-08-2005A07/08/2005 (propose01-18-2005W......05-03-2005N......QR.MI MI MI07-13-2005P08/12/2005 (propose07-11-2006A08-10-2006SD.08-10-200708-10-2008.07-11-2006A08-10-2006DPU.08-10-200708-10-2008.07-11-2006A08-10-2006DPU.08-10-200708-10-2008.07-11-2006A08-10-2006SD.08-10-200708-10-2008.02-02-2007A03-02-2007DPU/SD.08-15-200708-15-2008.01-30-2008A01-30-2008SD.01-30-200901-30-2010.03-07-2008A03-07-2008SD.03-07-200903-07-2010.08-10-2008P08-10-2008DPU/SD.08-10-200908-10-2010.08-11-2008P08-11-2008AVD.05-23-200905-23-2010.12-11-2009A12-23-2009DPU/SD.06-06-201006-06-2011.MI A06-11-2011AVD.06-12-201206-12-2013.07-23-2008A10-01-2008QR.10-01-200910-01-2010.MI A11-06-2009AVD.MI MI.12-16-2009N..12-16-2009...MI MI MI MI MI MI MI MI ....12-28-2010... ....12-25-2010... ....04-06-2011... ....12-28-2011...MI MI MI MI MI MI MI MI08-12-1996N......07-24-1996P11-28-1996AVD.11-27-199711-27-199811-27-1999 08-12-1996N......06-04-1998A06-01-1998QR.05-31-199905-31-200006-01-2001.07-22-200007-22-200107-22-2002 07-09-1999A07-22-1999TRQ/AVD.02-28-200102-28-200203-01-2003 02-17-2000A03-01-2000TRQ/AVD.MI MI03-01-2003 02-22-2000A03-01-2000TRQ/AVD07-11-2000N......10-03-2000N.......03-19-200303-19-200403-20-2005 P03-20-2002TRQ/AVD10/22/2001 and 11/005-12-2000W......05-12-2000W......MI MI MI MI MI MI MI MI ........MI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MIMI MI MI MI MI MI MI MI ........02-23-2010T..02-23-2010...。

数据安全管理制度英文

I. IntroductionThe Data Security Management System (DSMS) is a comprehensive set of policies, procedures, and guidelines designed to protect the confidentiality, integrity, and availability of the organization's data. This system is crucial for ensuring that sensitive information is safeguarded against unauthorized access, use, disclosure, disruption, modification, or destruction. The following document outlines the key components of our DSMS, which are intended to provide a robust framework for data security within our organization.II. ScopeThe DSMS applies to all data owned, created, or maintained by our organization, including but not limited to electronic, physical, and paper-based information. This system also encompasses data stored on internal and external systems, as well as data shared with third parties. All employees, contractors, and third-party vendors are required to adhere to this system.III. ObjectivesThe primary objectives of our DSMS are as follows:1. To ensure the confidentiality, integrity, and availability of data.2. To comply with relevant laws, regulations, and industry standards.3. To minimize the risk of data breaches and unauthorized access.4. To establish a culture of security awareness among employees.5. To facilitate the efficient management of data security incidents.IV. Policies and ProceduresA. Access Control1. User authentication: All users must have unique login credentials,and access levels will be determined based on job function and need-to-know basis.2. User authorization: Access to sensitive data will be granted only to authorized individuals.3. Regular access reviews: Access rights will be reviewed and updated periodically to ensure they remain appropriate.B. Data Classification1. Data will be classified into four categories: Public, Internal, Confidential, and Highly Confidential.2. The classification of data will be determined by its sensitivity, value, and legal requirements.C. Data Encryption1. Sensitive data will be encrypted both in transit and at rest.2. Encryption standards will comply with industry best practices.D. Incident Response1. An incident response plan will be developed and maintained to address data breaches and security incidents.2. All incidents will be reported to the appropriate authorities and documented for analysis and improvement.E. Security Awareness and Training1. Regular security awareness training will be provided to all employees.2. Training will cover topics such as password management, social engineering, and safe internet practices.V. Compliance and AuditingA. Regular audits will be conducted to ensure compliance with the DSMS.B. Any non-compliance issues will be addressed promptly and appropriate corrective actions will be taken.C. Compliance reports will be generated and reviewed by management to monitor the effectiveness of the DSMS.VI. Roles and ResponsibilitiesA. Data Owners: Responsible for the classification, protection, and maintenance of their data.B. Data Custodians: Responsible for implementing the DSMS, including access control, encryption, and incident response.C. Data Users: Responsible for adhering to the DSMS and following security best practices.D. Security Team: Responsible for developing, implementing, and maintaining the DSMS, as well as providing support and guidance to other departments.VII. ConclusionThe Data Security Management System is a critical component of our organization's data protection strategy. By adhering to this system, we aim to create a secure environment for our data, ensuring that it remains confidential, intact, and accessible when needed. It is the collective responsibility of all employees, contractors, and third-party vendors to uphold the principles outlined in this system and contribute to our ongoing commitment to data security.。

产品管理-信息安全产品强制性认证实施规则网络安全隔离卡与线路选择器产品

编号:CNCA-11C-076:2009信息安全产品强制性认证实施规则网络安全隔离卡与线路选择器产品2009-04-29发布 2009-05-01实施 中国国家认证认可监督管理委员会发布目 录1.适用范围 (1)2.认证模式 (1)3.认证的基本环节 (1)3.1认证申请及受理 (1)3.2型式试验委托及实施 (1)3.3初始工厂检查 (1)3.4认证结果评价与批准 (1)3.5获证后监督 (1)4.认证实施 (1)4.1认证程序 (1)4.2认证申请及受理 (2)4.3型式试验委托及实施 (3)4.4初始工厂检查 (4)4.5认证结果评价与批准 (5)4.6获证后监督 (6)5.认证证书 (7)5.1认证证书的保持 (7)5.2认证证书覆盖产品的扩展 (7)5.3认证证书的暂停、注销和撤消 (8)6.强制性产品认证标志的使用 (8)6.1准许使用的标志样式 (8)6.2变形认证标志的使用 (8)6.3加施方式 (8)6.4标志位置 (8)7.收费 (9)附件1: (11)附件2: (12)附件3: (14)附件4: (16)附件5: (17)1.适用范围本规则所指的网络安全隔离卡是指安装在计算机内部,能够使连接该计算机的多个独立的网络之间仍然保持物理隔离的设备。

安全隔离线路选择器是与配套的安全隔离卡一起使用,适用于单网布线环境下,使同一计算机能够访问多个独立的网络,并且各网络仍然保持物理隔离的设备。

本规则适用的产品范围为:(1)安全隔离计算机;(2)安全隔离卡;(3)安全隔离线路选择器。

说明:安全隔离计算机是指以安装网络安全隔离卡实现安全隔离的计算机。

拟用于涉密信息系统的上述产品,按照国家有关保密规定和标准执行,不适用本规则。

2.认证模式型式试验 + 初始工厂检查 + 获证后监督3.认证的基本环节3.1认证申请及受理3.2型式试验委托及实施3.3初始工厂检查3.4认证结果评价与批准3.5获证后监督4.认证实施4.1认证程序申请方可选择集中受理或分段受理两种方式中任意一种进行认证证书申请,两种方式下获得的证书是等效的。

国际金融组织现行主要政策文件目录及网址

国际金融组织现行主要政策文件目录及链接网址一、世界银行1. 世行政策操作手册(Operational Manual)/WBSITE/EXTERNAL/PROJECTS/EXTP OLICIES/EXTOPMANUAL/0,,menuPK:64142516~pagePK:641416 81~piPK:64141745~theSitePK:502184,00.html(概述部分英文版)该手册的目录及内容:/WBSITE/EXTERNAL/PROJECTS/EXTP OLICIES/EXTOPMANUAL/0,,menuPK:64701637~pagePK:516285 25~piPK:64857279~theSitePK:502184,00.html(英文版)/WBSITE/EXTERNAL/PROJECTS/EXTP OLICIES/EXTOPMANUAL/0,,LANG:Chinese~menuPK:51454694 ~pagePK:64724619~piPK:64724753~theSitePK:502184~title:Transl ations%20for%20Chinese,00.html(中译文版)《安全保障政策》(已含在世行操作手册内)。

2. 世行采购政策及程序(Procurement Policies and Procedures) /WBSITE/EXTERNAL/PROJECTS/PROCUREMENT/0,,contentMDK:50002392~pagePK:84269~piPK:600015 58~theSitePK:84266,00.html(英文版)包括:(1)《采购指南》/WBSITE/EXTERNAL/PROJECTS/PROC UREMENT/0,,contentMDK:20060840~menuPK:93977~pagePK:842 69~piPK:60001558~theSitePK:84266~isCURL:Y,00.html(英文版)(2)《咨询服务指南》/WBSITE/EXTERNAL/PROJECTS/PROC UREMENT/0,,contentMDK:20060656~menuPK:93977~pagePK:842 69~piPK:60001558~theSitePK:84266~isCURL:Y,00.html(英文版)3. 世行贷款支付指南及手册(Disbursement Guidelines for Projects)/WBSITE/EXTERNAL/EXTCHINESEHO ME/PROJECTSCHI/0,,contentMDK:21465469~pagePK:41367~piP K:279616~theSitePK:3535340,00.html(中译文版)4. 世行反腐败指南(Governance and Anticorruption Strategy)/WBSITE/EXTERNAL/PROJECTS/0,,cont entMDK:21254834~pagePK:41367~piPK:51533~theSitePK:40941,0 0.html(英文和中译文版)5. 世行债务服务手册(Debt Servicing Handbook)/WBSITE/EXTERNAL/PROJECTS/0,,cont entMDK:20120765~menuPK:276160~pagePK:41367~piPK:51533~t heSitePK:40941,00.html(英文和中译文版)6. 世行贷款通则(General Conditions)/INTTOPGENCON/Resources/IBR D_GC_05_Feb08.pdf(英文版)/INTTOPGENCON/Resources/IBR DGC-Chinese-05-Amd08.pdf(中译文版)二、亚洲开发银行1. 亚行贷款支付手册(Loan Disbursement Handbook)/Documents/Handbooks/Loan_Disbursement/loa n-disbursement-final.pdf(英文版)/Documents/Translations/Chinese/Loan-Disburse ment-Handbook2007-cn.pdf (中译文版)2. 亚行贷款采购指南(Procurement Guidelines)/Documents/Guidelines/Procurement/Guidelines-Procurement.pdf(英文版)/Documents/Translations/Chinese/Guidelines-Pro curement-CN.pdf (中译文2006版)3. 亚行及其借款人使用咨询顾问指南(Guidelines on the Use of Consultants by ADB and Its Borrowers)/Documents/Guidelines/Consulting/Guidelines-C onsultants.pdf(英文版)/Documents/Translations/Chinese/guidelines-con sultants2007-cn.pdf(中译文2006版)4. 亚行贷款财务治理与管理手册(Handbook for Borrowers on the Financial Management and Analysis of Projects)/Documents/Handbooks/Borrowers_Fin_Gov_M gt_Investment/borrowers_financial.pdf(英文版)/Documents/Translations/Chinese/Borrowers-Fin -Gov-Mgt-Investment-CN.pdf(中译文2003版)5. 亚行保障政策声明(Safeguard Policy Statement)/Documents/Policies/Safeguards/Safeguard-Polic y-Statement-June2009.pdf(英文版)/Documents/Translations/Chinese/Safeguard-Poli cy-Statement-cn.pdf (中译文)6. 亚行贷款项目设计与监测框架指南(Guidelines for Preparinga Design and Monitoring Framework)/documents/guidelines/guidelines-preparing-dmf/ guidelines-preparing-dmf.pdf(英文版)/sites/default/files/PPMS-DMF-GuidelinesFeb07-c n.pdf(中译文2006年版)7. 亚行公共信息交流政策(The Public Communications Policy of ADB)/Documents/Policies/PCP/PCP-R-Paper.pdf(英文版)/Documents/Translations/Chinese/PCP-CN.pdf(中译文版)三、国际农发基金1.国际农发基金成立协定(Agreement Establishing IFAD)/pub/basic/agree/e/!01agree.pdf(英文版)2. 国际农发基金贷款政策及标准(Lending Policies and Criteria)/pub/basic/lending/e/02polcri.pdf(英文版)3. 国际农发基金项目审计指南(IFAD Guidelines on Project Audits)/pub/basic/audit/borrower_e.pdf(英文版)4. 国际农发基金财务准则(Financial Regulations of IFAD)/pub/basic/fin/e/!03finre.pdf(英文版)5. 农业发展融资通则(General Conditions for Agricultural Development Financing)/pub/basic/general/e/gencone.pdf(英文版)6. 国际农发基金采购指南(Procurement Guidelines)/pub/basic/procure/e/proceng.pdf(英文版)四、欧洲投资银行1.欧投行2011-2013运营计划(Operational plan 2011-2013)/attachments/strategies/cop_2011_en.pdf(英文版)2. 欧投行服务、产品和工程采购指南(Guide for procurement of services, supplies and works by the EIB for its own account)/attachments/thematic/guide_procurement_service s_en.pdf(英文版)3.欧投行信息披露政策(EIB Transparency Policy)/attachments/strategies/transparency_policy_en.pd f(英文版)4.环境与社会保障原则及标准(Environmental and Social Principle sand Standards)/attachments/strategies/eib_statement_esps_en.pdf (英文版)5.环境与社会实践手册(Environmental and Social Practices Handbook)/attachments/environmental_and_social_practices_ handbook.pdf(英文版)五、全球环境基金1. 全球环境基金建立重组后通则(Instrument for the Establishment of the Restructured)/gef/sites//files/publication/GEF_Instr ument_March08.pdf(英文版)/gef/sites//files/publication/Instrumen t-March08-Chinese.pdf(中译文版)2. 全球环境基金项目运行政策和程序(GEF Policies and procedures for the GEF Project Cycle)/gef/sites//files/documents/GEF%20P olicies%20and%20Procedures%20for%20GEF%20Project%20Cycle. pdf(英文版)3. 资金透明分配体系(System for Transparent Allocation ofResources)/gef/sites//files/documents/document/ GEF.P.3.2010-1.pdf(英文版)4. 增量成本原则适用操作指南(Operational Guidelines for the Application of the Incremental Cost Principle)/gef/sites//files/documents/document/ OPERATIONAL.GUIDELINES.FOR_.THE_.APPLICATION.OF_. THE_.INCREMENTAL.COST_.PRINCIPLE.pdf(英文版)5. 全球环境基金5期重点业务领域战略(GEF-5 Focal Area Strategies)/gef/sites//files/publication/GEF-5%2 0FOCAL%20AREA.pdf(英文版)6. 全球环境基金监测与评价政策(the GEF Monitoring and Evaluation Policy)/gef/sites//files/documents/ME_Polic y_2010.pdf(英文版)。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。