最新《会计学》第七版 孙茂竹 课后习题答案

会计学第七版试题分析及答案

会计学第七版试题分析及答案一、单选题1. 会计的基本职能是什么?A. 记录、核算、监督B. 预测、决策、控制C. 计划、组织、领导D. 协调、沟通、监督答案:A2. 下列哪项不是会计核算的基本原则?A. 客观性原则B. 相关性原则C. 可比性原则D. 历史成本原则答案:B3. 会计要素中的资产和负债,其关系是?A. 资产=负债+所有者权益B. 资产=负债-所有者权益C. 资产+负债=所有者权益D. 资产-负债=所有者权益答案:A二、多选题4. 会计信息的质量要求包括以下哪些方面?A. 可靠性B. 及时性C. 可理解性D. 重要性答案:A, B, C, D5. 会计核算的基本程序包括哪些步骤?A. 确认B. 计量C. 记录D. 报告答案:A, B, C, D三、判断题6. 会计准则是会计核算和监督的法律依据。

()答案:正确7. 会计信息的使用者只包括企业内部的管理者。

()答案:错误四、简答题8. 简述会计的基本假设。

答案:会计的基本假设包括会计主体假设、持续经营假设、货币计量假设和会计分期假设。

会计主体假设指会计核算应当以独立的法人或其他组织为单位进行;持续经营假设假设企业将无限期地持续经营下去;货币计量假设指会计核算以货币作为计量单位;会计分期假设将企业的经营活动划分为若干个相等的会计期间。

9. 会计信息对企业决策有哪些作用?答案:会计信息对企业决策具有重要作用,包括提供决策依据、评价经营成果、监控财务状况、预测未来趋势等。

通过会计信息,管理者可以了解企业的财务状况、经营成果和现金流量,从而做出合理的经营决策和财务规划。

五、计算题10. 某企业2023年1月1日的资产负债表如下所示:资产:流动资产 200,000元,固定资产 300,000元。

负债:流动负债 100,000元。

所有者权益:实收资本 400,000元。

假设该企业2023年1月31日的净利润为50,000元,请计算其1月31日的资产负债表。

会计学基础课后答案 (5)

会计学基础课后答案题目1问题:什么是会计学?它的主要目标是什么?答案:会计学是一门研究财务信息系统的科学,它涉及记录、分类、汇总和报告经济实体的财务信息。

会计学的主要目标是提供有关经济实体财务状况、经营成果和变动的相关信息,以便供内部管理决策和外部决策者使用。

题目2问题:什么是会计基本假设?列举并解释会计基本假设的四个主要要素。

答案:会计基本假设是在进行会计记录和报告时所依赖的基本前提。

以下是会计基本假设的四个主要要素:1.实体假设:会计活动应该与经济实体进行分开。

经济活动中涉及的人、事、业务都应当被视为是独立且独立于该实体的。

2.会计期间假设:会计记录应当在特定的时间段内进行,这个时间段通常为一个会计年度。

这个假设是基于需要有一个固定的时间段来进行财务信息的汇总和报告。

3.货币单位假设:会计记录和报告中的数额应当以货币单位表示。

这意味着所有的财务信息都应当以通用货币来进行计量,并且货币单位应当保持稳定不变。

4.会计会计期间假设:会计记录和报告中的信息应当衡量、记录和报告为一个会计时期(通常为12个月)内发生的经济事项和交易。

这个假设是为了方便财务信息的比较和分析。

题目3问题:什么是会计主体?与会计主体有关联的实体有哪些?答案:会计主体是指进行会计记录和报告的特定组织、个人或法人实体。

与会计主体有关联的实体包括以下几种:1.所有者:所有者是指对会计主体的资金和资源具有法定或经济上的所有权的个人或组织。

所有者对会计主体的投资和收益有决策权和经济利益。

2.债权人:债权人是指借给会计主体资金或提供其他经济资源的个人或组织。

债权人对会计主体拥有的债务有经济利益和风险。

3.政府:政府是指与会计主体相关的各级政府机构,包括中央政府和地方政府。

政府通过税收和其他形式的收入征收来管理和监督会计主体。

4.员工:员工是指为会计主体工作并从中获取报酬的人员。

员工对会计主体的财务状况和经营结果有直接的影响。

题目4问题:什么是会计核算?它有哪些基本要素?答案:会计核算是将经济活动转化为财务信息的过程,通常通过记录和汇总交易和事件来完成。

会计学第七版复试题及答案

会计学第七版复试题及答案一、选择题1. 会计的基本职能是什么?A. 记录、分析、报告B. 预测、决策、控制C. 计划、组织、领导D. 协调、监督、评价答案:A2. 会计信息的质量要求中,哪个要求强调信息的准确性和可靠性?A. 及时性B. 相关性C. 可靠性D. 可比性答案:C3. 以下哪项不是会计要素?A. 资产B. 负债C. 所有者权益D. 利润答案:D二、判断题1. 会计准则是会计工作的法律依据。

()答案:正确2. 会计核算的基本原则是历史成本原则。

()答案:错误(会计核算的基本原则包括历史成本原则,但不是唯一原则)3. 会计报表只包括资产负债表和利润表。

()答案:错误(会计报表还包括现金流量表等)三、简答题1. 简述会计的四个基本假设。

答案:会计的四个基本假设包括:会计主体假设,持续经营假设,货币计量假设,会计分期假设。

2. 什么是权责发生制?它与收付实现制有何不同?答案:权责发生制是指收入和费用的确认以权责发生的时间为准,即收入在实现时确认,费用在发生时确认。

与收付实现制不同,收付实现制是以现金的收付为标准来确认收入和费用。

四、计算题1. 某公司2023年1月1日的资产总额为500万元,负债总额为200万元,所有者权益为300万元。

2023年12月31日,该公司的资产总额增加到600万元,负债总额增加到250万元。

请计算该公司2023年的净利润。

答案:根据会计公式,净利润 = 资产总额 - 负债总额。

2023年初所有者权益为300万元,年末所有者权益 = 年末资产总额 - 年末负债总额 = 600 - 250 = 350万元。

净利润 = 年末所有者权益 - 年初所有者权益 = 350 - 300 = 50万元。

五、案例分析题1. 某公司在2023年12月31日收到一笔应收账款,金额为10万元,但该款项直到2024年1月5日才实际收到。

根据权责发生制原则,这笔收入应该在哪个会计年度确认?答案:根据权责发生制原则,收入应在实现时确认。

会计学基础试题及答案第七版

会计学基础试题及答案第七版1、按现行企业会计准则规定,短期借款发生的利息一般应借记的会计科目是()。

[单选题] *A.短期借款B.应付利息C.财务费用(正确答案)D.银行存款2、无形资产是指企业拥有或控制的没有实物形态的可辨认的()。

[单选题] *A.资产B.非流动性资产C.货币性资产D.非货币性资产(正确答案)3、企业生产经营期间发生的长期借款利息应计入()科目。

[单选题] *A.在建工程B.财务费用(正确答案)C.开办费D.长期待摊费用4、企业因解除与职工的劳动关系给予职工补偿而发生的职工薪酬,应借记的会计科目是()。

[单选题] *A.管理费用(正确答案)B.计入存货成本或劳务成本C.营业外支出D.计入销售费用5、下列各项,不影响企业营业利润的项目是()。

[单选题] *A.主营业务收入B.其他收益C.资产处置损益D.营业外收入(正确答案)6、.(年浙江省第二次联考)会计人员的职业道德规范不包括()[单选题] *A操守为重、不做假账(正确答案)B爱岗敬业、诚实守信C、廉洁自律、客观公正D坚持准则、提高技能7、企业对账面原值为15万元的固定资产进行清理,累计折旧为10万元,已计提减值准备1万元,清理时发生清理费用5万元,清理收入6万元,不考虑增值税,该固定资产的清理净收益为()万元。

[单选题] *A.5B.6C.5(正确答案)D.58、当法定盈余公积达到注册资本的()时,可以不再提取。

[单选题] *A.10%B.20%C.50%(正确答案)D.30%9、.(年浙江省高职考)根据我国会计法律规范体系的构成和层次,《会计职称条例》的归属范畴是()[单选题] *A、宪法B会计法规(正确答案)C会计规章D会计法律10、下列项目中,应计入营业外收入的有()。

[单选题] *A.处置交易性金融资产的收益B.固定资产盘盈C.接受捐赠(正确答案)D.无法收到的应收账款11、用盈余公积弥补亏损时,应借记“盈余公积”,贷记()。

第七版成本会计学课后练习题答案

第七版成本会计学课后练习题答案第3章费用在各种产品以及期间费用之间的归集和分配四、教材练习题答案1.按定额消耗量比例分配原材料费用甲、乙两种产品的原材料定额消耗量。

A材料:甲产品定额消耗量=100×10=1000乙产品定额消耗量=200×=800合计1800B材料:甲产品定额消耗量=100×5=00乙产品定额消耗量=200×6=1200合计1700计算原材料消耗量分配率。

A材料消耗量分配率=B材料消耗量分配率==0.9=1.01计算甲、乙两种产品应分配的原材料实际消耗量。

甲产品应分配的A材料实际数量=1000×0.99=990乙产品应分配的A材料实际数量=800×0.99=792甲产品应分配的B材料实际数量=500×1.01=505乙产品应分配的B材料实际数量=1200×1.01=1212计算甲、乙两种产品应分配的原材料计划价格费用。

甲产品应分配的A材料计划价格费用=990×2=1980甲产品应分配的B材料计划价格费用=505×3=1515合计3495乙产品应分配的A材料计划价格费用=92×2=1584乙产品应分配的B材料计划价格费用=1212×3=3636合计220计算甲、乙两种产品应负担的原材料成本差异。

甲产品应负担的原材料成本差异=3495×=-69.9乙产品应负担的原材料成本差异=5220×=-104.4计算甲、乙两种产品的实际原材料费用。

甲产品实际原材料费用=3495-69.9=3425.1乙产品实际原材料费用=5220-104.4=5115.6根据以上计算结果可编制原材料费用分配表。

根据原材料费用分配表,编制会计分录如下:1)借:基本生产成本——甲产品3495——乙产品5220贷:原材料7152)借:材料成本差异174.3贷:基本生产成本——甲产品69.9——乙产品 104.42.采用交互分配法分配辅助生产费用交互分配。

(完整版)会计学课后习题答案

第一章总论【思考题】1.说明财务会计与管理会计的区别与联系。

答:财务会计与管理会计的区别可概括为;(1)财务会计以计量和传送信息为主要目标财务会计不同于管理会计的特点之一,是财务会计的目标主要是向企业的投资者、债权人、政府部门,以及社会公众提供会计信息。

从信息的性质看,主要是反映企业整体情况,并着重历史信息。

从信息的使用者看,主要是外部使用者,包括投资人、债权人、社会公众和政府部门等。

从信息的用途看,主要是利用信息了解企业的财务状况和经营成果。

而管理会计的目标则侧重于规划未来,对企业的重大经营活动进行预测和决策,以及加强事中控制。

(2)财务会计以会计报告为工作核心财务会计作为一个会计信息系统,是以会计报表作为最终成果。

会计信息最终是通过会计报表反映出来。

因此,财务报告是会计工作的核心。

现代财务会计所编制的会计报表是以公认会计原则为指导而编制的通用会计报表,并把会计报表的编制放在最突出的地位。

而管理会计并不把编制会计报表当做它的主要目标,只是为企业的经营决策提供有选择的或特定的管理信息,其业绩报告也不对外公开发表。

(3)财务会计仍然以传统会计模式作为数据处理和信息加工的基本方法为了提供通用的会计报表,财务会计还要运用较为成熟的传统会计模式作为处理和加工信息的方法。

传统会计模式也是历史成本模式,它依据复式簿记系统,以权责发生制为基础,采用历史成本原则。

(4)财务会计以公认会计原则和行业会计制度为指导公认会计原则是指导财务会计工作的基本原理和准则,是组织会计活动、处理会计业务的规范。

公认会计原则由基本会计准则和具体会计准则所组成。

这都是我国财务会计必须遵循的规范。

而管理会计则不必严格遵守公认的会计原则。

2.试举五个会计信息使用者,并说明他们怎样使用会计信息。

答:股东。

他们需要评价过去和预测未来。

有关年度财务报告是满足这些需要的最重要的手段,季度财务报告、半年度报告也是管理部门向股东报告的重要形式。

向股东提供这些报告是会计信息系统的传统职责,股东借助于财务报告反映的常规信息,获得有关股票交易和股利支付的情况,从而做出投资决策。

财务管理学第七版课后习题答案全

财务管理学第七版课后习题答案全在学习财务管理学这门课程时,课后习题是巩固知识、检验学习效果的重要手段。

以下为您提供财务管理学第七版的课后习题答案全,希望能对您的学习有所帮助。

一、单项选择题1、企业财务管理的目标是()A 利润最大化B 股东财富最大化C 企业价值最大化D 相关者利益最大化答案:C解析:企业价值最大化考虑了货币的时间价值和风险因素,能克服企业在追求利润上的短期行为,也较好地兼顾了各利益主体的利益,所以是较为合理的财务管理目标。

2、下列各项中,不属于财务管理经济环境构成要素的是()A 经济周期B 通货膨胀水平C 宏观经济政策D 公司治理结构答案:D解析:经济环境包括经济体制、经济周期、经济发展水平、宏观经济政策及社会通货膨胀水平等。

公司治理结构属于法律环境的范畴。

3、某企业于年初存入银行 10000 元,假定年利率为 12%,每年复利两次。

已知(F/P,6%,5)=13382,(F/P,6%,10)=17908,(F/P,12%,5)=17623,(F/P,12%,10)=31058,则第 5 年末的本利和为()元。

A 13382B 17623C 17908D 31058答案:C解析:每年复利两次,年利率为 12%,则实际利率为(1 + 12%/2)^2 1 = 1236%,第 5 年末的本利和= 10000×(F/P,1236%,5)= 10000×17908 = 17908(元)二、多项选择题1、下列各项中,属于财务管理风险对策的有()A 规避风险B 减少风险C 转移风险D 接受风险答案:ABCD解析:财务管理风险对策包括规避风险、减少风险、转移风险和接受风险。

2、下列各项中,属于年金形式的有()A 定期定额支付的养老金B 偿债基金C 零存整取储蓄存款的零存额D 年资本回收额答案:ABCD解析:年金是指一定时期内每次等额收付的系列款项,包括普通年金(后付年金)、即付年金(先付年金)、递延年金和永续年金。

《会计学》(第7版)习题答案 hh_acct7_sm_ch21_appx

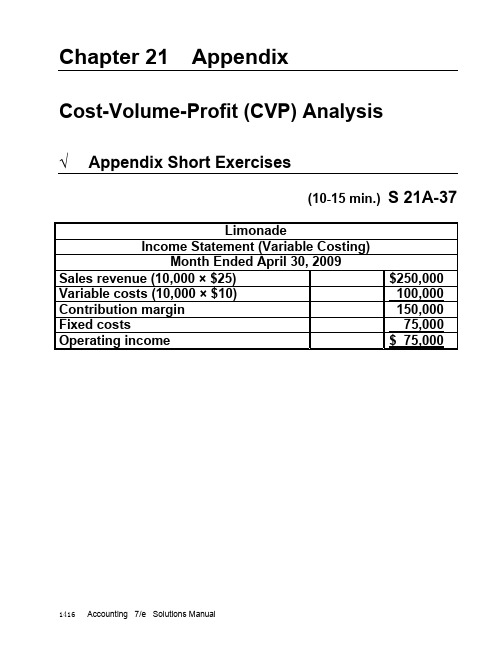

Chapter 21 AppendixCost-Volume-Profit (CVP) Analysis√Appendix Short Exercises(10-15 min.) S 21A-37LimonadeIncome Statement (Variable Costing)Month Ended April 30, 2009Sales revenue (10,000 × $25) $250,000 Variable costs (10,000 × $10) 100,000 Contribution margin 150,000 Fixed costs 75,000 Operating income $ 75,000(15 min.) S 21A-38 Req. 1LimonadeIncome Statement (Absorption Costing)Month Ended April 30, 2009Sales revenue (10,000 × $25) $250,000 Cost of goods sold[10,000 × ($8 var. + $5 fixed*)] 130,000 Gross Profit 120,000 Selling and administrative cost[(10,000 × $2) + $20,000] 40,000 Operating income $ 80,000 *$55,000 / 11,000 = $5 per unitReq. 2The difference in incomes of $5,000 is the 1,000 units in ending inventory × $5 fixed cost per unit that will be expensed when goods are sold next month.√Appendix Exercises(15-20 min.) E 21A-39 Req. 1Seams CompanyConventional (Absorption Costing) Income StatementYear Ended December 31, 2008Sales revenue (185,000 × $35) $6,475,000 Less: Cost of goods sold (185,000 × $25*) 4,625,000 Gross profit 1,850,000 Operating costs [(185,000 × $5) + $300,000] 1,225,000 Operating income $ 625,000 __________*Variable manufacturing cost per unit of $15 plus $10 fixedmanufacturing cost per unit ($2,000,000 fixed manufacturing overhead / 200,000 units produced).Seams CompanyContribution Margin (Variable Costing) Income StatementYear Ended December 31, 2008Sales revenue (185,000 × $35) $6,475,000 Variable costs:Variable cost of goods sold (185,000 × $15manufacturing) $2,775,000 Variable sales commission (185,000 × $5) 925,000 3,700,000 Contribution margin 2,775,000 Fixed costs:Manufacturing overhead $2,000,000 Operating costs 300,000 2,300,000 Operating income $ 475,000(continued) E 21A-39 Req. 2Absorption costing operating income is higher than variable costing operating income. This is because absorption costing defers 15,000 goggles × $10 fixed manufacturing overhead per goggle = $150,000 of 2008 fixed manufacturing overhead as an asset in ending inventory. In contrast, variable costing expenses all the 2008 fixed manufacturing overhead during 2008. Variable costing expenses $150,000 more costs during 2008, so variable costing operating income is $150,000 less than absorption costing income in 2008 ($625,000 − $475,000). Req. 3Seams’ managers can use the contribution margin income statement format to evaluate the sales promotion.Increase in contribution margin (15,000 × $15)*... $225,000Increase in fixed costs……………………………… (150,000)Increase in operating income……………………… $ 75,000Seams should go ahead with the promotion.*Contribution margin per unit:Sale price………………………………………... $35 Variable manufacturing cost………………… $15 Variable operating cost……………………….. 5 (20)Contribution margin per unit………………… $15√ Appendix Problems(10-15 min.) P 21A-40Req. 1January, 2007 Absorption Variable Costing CostingVariable manufacturing costs………… $4.00 $4.00Fixed manufacturing costs……………. .50a — Total………………………………………...$4.50 $4.00a Fixed overhead Fixed manufacturing overheadper meal= Number of meals producedIn January:$700 = 1,400= $0.50 per mealReq. 2aGia’s FoodsIncome Statement (Absorption Costing)Month Ended January 31, 2007Sales revenue (1,000 × $8) $ 8,000 Deduct: Cost of goods sold (1,000 × $4.50) (4,500) Gross profit 3,500 Deduct: Operating costs:Marketing and administrative costs[(1,000 × $1) + $600] (1,600) Operating income $ 1,900 UnitsBeginning inventory 0Units produced…………………… 1,400Units available…………………….1,400Units sold…………………………. (1,000)Ending inventory (400)Req. 2bGia’s FoodsIncome Statement (Variable Costing)Month Ended January 31, 2007Sales revenue (1,000 × $8) $ 8,000 Deduct: Variable costs:Variable cost of goods sold (1,000 × $4) $4,000Sales commission cost (1,000 × $1) 1,000Total variable costs (5,000) Contribution margin 3,000 Deduct: Fixed costs:Fixed manufacturing overhead 700 Fixed marketing and administrative costs 600Total fixed costs (1,300) Operating income $ 1,700Req. 3In January, absorption costing operating income exceeds variable costing income. This is because production exceeds sales. Absorption costing defers some of January’s fixed manufacturing overhead costs in the 400 units of ending inventory. These costs will not be expensed until those units are sold. Deferring some of January’s fixed manufacturing overhead costs to the future increases January’s absorption costing income.Absorption costing assigns $0.50 of fixed manufacturing overhead to each unit. There are 400 units in ending inventory, so absorption costing defers 400 × $0.50 = $200 of January fixed overhead costs. Thus, absorption costing income is $200 higher than variable costing income in January.Req. 1OctoberVariable AbsorptionCosting CostingVariable manufacturing costs………… $15 $15Fixed manufacturing costs……………. 4 — Total………………………………………...$19 $15Req. 2aVideo KingIncome Statement (Absorption Costing)Month Ended November 30, 2008Sales revenue (3,000 × $40) $120,000 Deduct: Cost of goods sold (3,000 × $19) (57,000) Gross profit 63,000 Deduct: Operating costs:Marketing and administrative costs[(3,000 × $8) + $9,000] (33,000) Operating income $ 30,000 UnitsBeginning inventory (500)Units produced…………………… 2,500Units available…………………….3,000Units sold…………………………. (3,000)Ending inventory 0Req. 2bVideo KingIncome Statement (Variable Costing)Month Ended November 30, 2008Sales revenue (3,000 × $40) $120,000 Deduct: Variable costs:Variable cost of goods sold (3,000 × $15) $45,000Sales commission cost (3,000 × $8) 24,000Total variable costs (69,000) Contribution margin 51,000 Deduct: Fixed costs:Fixed manufacturing overhead 10,000Fixed marketing and administrative costs 9,000Total fixed costs (19,000) Operating income $ 32,000Req. 3In November, variable costing operating income exceeds absorption costing income. This is because sales exceed production. Absorption costing deferred some of October’s fixed manufacturing overhead costs in the 500 units of beginning inventory for November. These costs were expensed when those units were sold in November. Deferring some of October’s fixed manufacturing overhead costs to the future increased October’s absorption costing income and decreased November’s absorption costing income.Absorption costing assigns $4.00 of fixed manufacturing overhead to each unit. There are 500 units in October’s ending inventory, so absorption costing deferred 500 × $4 = $2,000 of October fixed overhead costs until November, when the 500 units were sold. Thus, absorption costing income is $2,000 lower than variable costing income in November.√Team Project(60-70 minutes, most of which is advance preparation)This challenging role play works best with groups of 4 to 6 students. Each group will form two subgroups—one for each role.Kevin McDaniel:Req. 1FASTPACK ManufacturingIncome Statement (Absorption Costing)Year Ended December 31, 2007(In millions)Sales revenue (15 × $3) $45.00 Less: Cost of goods sold:Beginning finished goods inventory $ 0Cost of goods manufactured (15 × $2.56)a38.4Cost of goods available for sale 38.4Ending finished goods inventory 0Cost of goods sold 38.4 Gross profit 6.6 Less: Operating costs:Marketing and administrative costs[(15 × $0.50) + $1.1] (8.6) Operating loss $ (2.0) a[$2 variable manufacturing cost per roll + ($8.4 million / 15million) fixed manufacturing overhead per roll = $2.56 per roll]Req. 2FASTPACK should adopt the advertising campaign.DATE: __________TO: Board of Directors, FASTPACK Manufacturing FROM: Kevin McDanielSUBJECT: Advertising campaignI have authorized our ad agency to go ahead with the advertising campaign. Although this campaign will cost us $2.3 million, I expect it to increase our operating income by $2.2 million, as shown below.In millions Increased revenue from higher sales (9 million more rolls sold × $3)…..... $27.0(22.5) Increase in variable costs (9 million more rolls sold × $2.50b)….………..... Increase in contribution margin from higher sales…………………………... 4.5 Increase in fixed costs from advertising campaign………………………….. (2.3) Increase in operating income from advertising campaign………………….. $ 2.2b$2 Variable manufacturing costs + $0.50 variablemarketing and administrative costs per roll.Req. 3McDaniel’s bonus is based on absorption costing operating income. Absorption costing defers part of current period fixed manufacturing overhead in ending inventory. Therefore, increasing ending inventory increases current period absorption costing income. If McDaniel wants to maximize his bonus, he will direct FASTPACK to produce at capacity, 30 million rolls.If McDaniel is more concerned about FASTPACK than about himself or his bonus, he will direct FASTPACK to produce the 24 million rolls that he expects will be sold in 2008.Req. 4If FASTPACK produces 30 million rolls:FASTPACK ManufacturingIncome Statement (Absorption Costing)Year Ended December 31, 2008(In millions)Sales revenue (24 × $3) $ 72.00 Less: Cost of goods sold:Beginning finished goods inventory $ 0.00Cost of goods manufactured (30 × $2.28)c68.40Cost of goods available for sale 68.40Ending finished goods inventory (6 × $2.28) (13.68) Cost of goods sold 54.72 Gross profit 17.28 Less: Operating costs:Marketing and administrative costs[(24 × $0.50) + $3.4]d(15.40) Operating income $ 1.88c$2 variable manufacturing cost per roll + ($8.4 million / 30million) fixed manufacturing overhead per roll = $2.28 per roll. d$1.1 million + $2.3 million = $3.4 million.Kevin McDaniel’s bonus is 10% of absorption costing income: 10% × $1,880,000 = $188,000Req. 4 (continued)If FASTPACK produces only 24 million rolls:FASTPACK ManufacturingIncome Statement (Absorption Costing)Year Ended December 31, 2008(In millions)Sales revenue (24 × $3) $ 72.0 Less: Cost of goods sold:Beginning finished goods inventory $ 0Cost of goods manufactured (24 × $2.35)e56.4Cost of goods available for sale 56.4Ending finished goods inventory 0Cost of goods sold (56.4) Gross profit 15.6 Less: Operating costs:Marketing and administrative costs[(24 × $0.50) + $3.4]f 15.4 Operating income $ 0.2 e$2.00 variable manufacturing cost per roll + ($8.4 million / 24 million) fixed manufacturing overhead per roll = $2.35 per roll.f$1.1 million + $2.3 million = $3.4 million.If FASTPACK produces only 24 million rolls, absorption costing operating income is $200,000, so Kevin McDaniel’s bonus is only $20,000.Req. 5Assuming McDaniel ordered FASTPACK to produce 30 million rolls, McDaniel is building up inventory because FASTPACK can only sell 24 million rolls per year. Under absorption costing, this defers part of current year fixed manufacturing costs to the future. This increases current period absorption costing income.The maximum FASTPACK can sell in the near future is 24 million rolls. If McDaniel continues to produce 30 million rolls per year, but FASTPACK sells only 24 million, FASTPACK will soon run out of room to store the inventory. Eventually, FASTPACK will have to reduce production and use up inventory. When inventory declines, absorption costing expenses prior period costs stored in the inventory. This will reduce absorption costing income in years when inventory declines. In turn, this would reduce McDaniel’s bonus.If he must reduce inventory, McDaniel is unlikely to continue his employment at FASTPACK under a contract that bases his bonus on absorption costing income. Consequently, McDaniel may well take the job at the new company. He can increase his bonus by building up its inventories.If McDaniel produced only 24 million rolls, operating income would be $200,000, and he would receive a small bonus. In this case, he is likely to leave FASTPACK and take the other company’s offer.Board of Directors:Req. 1See income statement in Req. 1 of McDaniel’s role.Req. 2FASTPACK should adopt the advertising campaign, because the campaign will increase operating income by 2.2 million.In millions Increased revenue from higher sales (9 million more rolls sold × $3).…… $27.0(22.5) Increase in variable costs (9 million more rolls sold × $2.50)*……….......... Increase in contribution margin from higher sales…………………….…….. 4.5 Increase in fixed costs from advertising campaign………………………….. (2.3) Increase in operating income from advertising campaign………………….. $ 2.2*$2.00 variable manufacturing costs + $0.50 variablemarketing and administrative costs per roll.Req. 3FASTPACK can only sell 24 million rolls of tape. Therefore, it should produce only 24 million rolls of tape.Req. 4The evaluation of McDaniel will depend upon his decisions:•McDaniel should receive a more favorable evaluation if he adopts the advertising campaign.•McDaniel should receive a more favorable evaluation if he produces only 24 million rolls. McDaniel’s bonus is basedon absorption costing income. This gives him the incentive to produce at capacity (30 million rolls). Buildinginventory defers part of current period fixed costs to the future. This inflates current year absorption costing income, and McDaniel’s bonus. If he resists this temptation, the Board should take this into considerationin his evaluation.•McDaniel’s evaluation also should depend upon FASTPACK’s performance. The Board can assess FASTPACK’s performance using a variable costing incomestatement. The following income statement assumes that FASTPACK produces 30 million rolls, but variable costingincome would be the same regardless of the number of rolls produced.FASTPACK ManufacturingIncome Statement (Variable Costing)Year Ended December 31, 2008(In millions)Sales revenue (24 × $3) $72.0 Less: Variable costs:Beginning finished goods inventory $ 0.0Cost of goods manufactured (30 × $2) 60.0Cost of goods available for sale 60.0Ending finished goods inventory (6 × $2) (12.0)Variable cost of goods sold 48.0Variable marketing and administrativecosts (24 × $0.50) 12.0 Total variable costs (60.0) Contribution margin 12.0 Less: Fixed costs:Fixed manufacturing overhead 8.4 Fixed marketing and administrative costs($1.1 + $2.3) 3.4 Total fixed costs (11.8) Operating income $ 0.2 Variable costing shows that FASTPACK has made a profit of $200,000 in 2008. While this is better than the $2.0 million loss in 2007, the present level of performance probably is not good enough to ensure FASTPACK’s long-run survival.1436Accounting 7/e Solutions ManualReq. 5The bonus provision should be revised. Basing the bonus on absorption costing operating income gives the president an incentive to build up inventory. This inflates absorption costing income by deferring current period fixed manufacturing costs to the future. While it is a good idea to tie the president’s bonus to FASTPACK’s income, it would be better to use variable costing income, which does not give an incentive to build inventory.If the Board wants to keep the absorption costing income provision, then it should adopt a policy preventing inventory buildup.Chapter 21 Cost-Volume-Profit (CVP) Analysis 1437Meeting between the Board and McDaniel:The content and outcome of this meeting will depend upon the decisions McDaniel has made, and whether the Board believes he has made enough progress in improving FASTPACK’s performance. If the Board wants to keep McDaniel, it should base the bonus on variable costing income (or at least implement a provision against building up inventory). However, the Board may be inclined to let McDaniel go, given FASTPACK’s lackluster performance. This is especially true if the Board believes McDaniel has taken advantage of FASTPACK by building up inventory, or if McDaniel made a mistake by not adopting the advertising campaign.Even if the Board offers McDaniel a new contract, it is not clear whether he will stay with FASTPACK or accept the other company’s offer. If he must start reducing inventory, McDaniel is unlikely to continue at FASTPACK if his bonus is based on absorption costing income. There is not enough information to determine whether McDaniel would be better off staying with FASTPACK under a contract that granted a bonus based on variable costing income or whether he would be better off accepting the position with the new company.1438Accounting 7/e Solutions Manual。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第一章教材习题解析一、思考题1.从管理会计定义的历史研究中你有哪些思考和想法?答:对管理会计的定义从狭义的管理会计阶段发展到广义的管理会计阶段,我们可以看出,这一过程是一个广泛引入和应用相邻学科的新的方法从而不断丰富学科本身内容的过程,是一个伴随着社会经济环境变化和经济管理理论等多学科理论的发展而发展的过程。

管理会计是适应企业管理发展的要求而产生和不断完善、发展的。

新的管理理论的产生及推广运用总是源于企业实践的需要,并随着实践的发展而发展。

相应地,管理会计的理论与技术方法也会随着管理理论的发展而发展,必然推动着管理会计定义不断丰富、清晰、完整,促进管理会计基本理论框架的建立与完善。

所以,从管理会计定义的历史研究来看,结合管理会计各个阶段的变化和发展,我们觉得可以更好地预测未来管理会计工作的变动趋势和管理会计以后研究的演变,除了了解过往、以史为鉴,更重要的是寻找管理会计发展的动因和规律,并能够把握未来的发展方向。

2.从管理会计人员的职业道德和管理会计学科课程体系的内容设计看,你认为管理会计人员在企业管理中处于何种地位?答:从管理会计人员的职业道德和管理会计学科课程体系的内容设计看,管理会计人员只有具有良好的职业道德,才能成功进行以使用价值管理为基础的价值管理,实现管理会计的目标,履行管理会计人员职能和重要工作,在企业管理中发挥提供客观的信息、有效参与决策的重要作用。

特别是,当信息也成为企业的竞争力之一时,管理会计人员的作用也就逐渐从辅助性决策支持者转为积极的商业伙伴,通过发现企业持续改进的机会和评价稀缺资源的最佳使用方案而促进企业各种变革的展开。

由于管理会计人员在单位中的地位和独立程度不同,导致会计职业道德有不同程度的欠缺。

单位负责人的道德水准较高,单位的人事政策对管理会计人员的任用和选拔比较重视,管理会计人员在单位中的地位较高,其独立性较强,就有利于管理会计人员职业道德水平的提高,也有利于其在企业管理中发挥重要作用。

如果管理会计人员的独立性受到很大制约,就不利于管理会计人员职业道德水平的提高。

因为管理会计人员的工作完全在单位负责人的领导、管理之下,具有天然的从属性,单位负责人享有独立的人事分配权和劳动用工权,管理会计人员对于“老板”是不具有监督职能的,充其量只具有建议功能。

这种情况,严格地讲,虽也表现出管理会计人员职业道德上的缺欠,但主要不是管理会计人员自身职业道德缺欠,而主要是比管理会计人员握有更大权力的单位负责人道德缺欠造成的。

这会导致管理会计人员在企业管理中处于两难的尴尬地位。

3.经济理论对管理会计的产生和发展有哪些重要影响?你从中得到了什么启示?答:古典组织理论特别是科学管理理论的出现促使现代会计分化为财务会计和管理会计,现代会计的管理职能得以表现出来。

该阶段,管理会计以成本控制为基本特征,以提高企业的生产效率和工作效率为目的,其主要内容包括标准成本、预算控制和差异分析。

为适应企业管理重心由提高生产和工作效率转到提高经济效益的需要,西方管理理论出现了行为科学、系统理论、决策理论,使得管理会计的理论体系逐渐完善,内容更加丰富,逐步形成了预测、决策、预算、控制、考核、评价的管理会计体系。

随着市场竞争的日趋激烈,战略管理的理论有了长足发展,重视环境对企业经营的影响是企业战略管理的基本点。

因而,战略管理会计运用灵活多样的方法,收集、加工、整理与战略管理相关的各种信息,并据此协助企业管理层确立战略目标、进行战略规划、评价管理业绩。

从中得到的启示:管理会计的历史证明,管理会计的形成和发展受社会实践及经济理论的双重影响:一方面,社会经济的发展要求加强企业管理;另一方面,经济理论的形成又使这种要求得以实现。

管理会计在其形成和发展的各个阶段,无不体现着这两方面的影响。

一方面,管理会计的理论和技术方法会随着管理理论的发展而发展;另一方面,只有新的管理会计的理论和技术方法发展了,才能满足新的管理理论实践的需要。

在经济理论与管理会计演化的历史长河中,经济理论历来揭示经济的本质及运行目标,而管理会计则为体现这种本质并为其顺利运行提供理论和技术方法上的保障。

4.科学管理理论对现代管理会计有哪些重要影响?这些影响在管理会计的不同发展阶段是如何表现的?答:现代管理科学的形成与发展对管理会计的形成与发展在理论上起着奠基和指导作用,在方法上赋予它现代化的方法与技术,从而使它能够突破传统会计框架的局限,在会计领域孕育出一个崭新的体系,以适应并服务于当代社会经济高速发展的需要。

在以成本控制为基本特征的管理会计阶段,古典组织理论特别是科学管理理论的出现促使现代会计分化为财务会计和管理会计,现代会计的管理职能得以表现出来。

该阶段,管理会计以成本控制为基本特征,以提高企业的生产效率和工作效率为目的,其主要内容包括标准成本、预算控制、差异分析。

在以预测、决策为基本特征的管理会计阶段,以标准成本制度为主要内容的管理控制继续得到了强化并有了新的发展。

责任会计将行为科学的理论与管理控制的理论结合起来,不仅进一步加强了对企业经营的全面控制(不仅仅是成本控制),而且将责任者的责、权、利结合起来,考核、评价责任者的工作业绩,从而极大地激发了经营者的积极性和主动性。

现代管理科学的形成和发展对决策性管理会计的形成和发展在理论上起着奠基和指导的作用,其中,赫伯特·西蒙(HerbertASimon)的管理决策理论对决策性管理会计的发展起到了举足轻重的作用。

为了进行科学的决策分析,必须采用不同于对外报告所使用的方法来收集和计算成本数据,以供内部管理使用,于是,变动成本法应运而生,并成为现代管理会计中规划和控制经济活动的重要工具。

在重视环境适应性为基本特征的战略管理会计阶段,随着高新技术的发展和国际化市场竞争的日趋激烈,战略管理重视环境对企业经营的影响,从战略的角度综合利用企业内外部信息进行管理活动;而会计信息系统是一个不可或缺的决策支持系统。

因此,战略管理的形成导致了对战略管理会计的需要。

战略管理会计运用灵活多样的方法,收集、加工、整理与战略管理相关的各种信息,并据此协助企业管理层确立战略目标、进行战略规划、评价管理业绩。

5.战略选择和战术安排如何才能在管理会计中有效结合?答:战略管理会计是在知识经济和网络革命的宏观背景下,为适应企业战略管理的迫切需要而产生的。

它承袭了战略管理的主要思想,突破了战术管理会计的局限性,拓宽了战术管理会计的活动空间,无论在管理观念上,还是在管理方法和管理内容上都有新的突破。

尽管如此,战略管理会计并不会完全取代战术管理会计,只会进一步促进管理会计的完善和发展,因为战略管理会计是站在全球高度,从战略角度寻求企业整体竞争优势,致力于“知彼”,而战术管理会计则注重企业内部管理,致力于“知己”;一个是战略,一个是战术,两者相辅相成,缺一不可,共同服务于企业管理,进一步促进管理会计的发展和完善。

战略选择和战术安排必须在管理会计中有效结合,原因在于现代企业内部管理和战略管理会计本身都需要战术管理会计及其提供的信息资源。

管理会计作为决策支持系统的性质并未发生改变,信息支持和控制仍是其两大基本职能。

企业的战略决策仍要由企业管理层综合各方面信息做出。

当然,这种职能并不是传统意义上的简单重复,而是一次重大的功能扩展。

从范围上看,它跳出了单一企业这一狭小的空间范围,将视角更多地投向了影响企业的外部环境,密切关注整个市场和竞争对手的动向,运用战略管理会计的方法时要结合竞争对手的情况来进行,比如预测时要充分考虑各种影响未来趋势的因素,系统全面地对市场需求做出预测,充分认识潜在市场机会和各种竞争状况的变化,对企业风险进行充分估计。

从时间上看,它超越了单一期间的界限,着重从多期竞争地位的变化中把握企业未来的发展方向,注重企业持久竞争优势的取得和保持,着眼于企业长期发展,有时甚至会牺牲一些短期利益。

战术管理会计将管理会计方法引向工业界、商业界和学术界,而战略管理会计又将工业界、商业界和学术界带入信息社会和知识经济这一崭新的时代。

6.如何理解管理会计对象的复合性?复合性表现在哪些管理会计内容和方法上?请举例说明。

答:从实践角度看,管理会计的对象具有复合性的特点。

一方面,管理会计致力于使用价值生产和交换过程的优化,强调加强作业管理,其目的在于提高生产和工作效率。

作业管理必然强调有用作业和无用作业的区分,并致力于消除无用作业。

为此,必须按生产经营的内在联系,设计作业环节和作业链,为作业管理和管理会计的实施奠定基础。

可以说,作业管理使管理会计的重新构架成为可能。

另一方面,在价值形成和价值增值过程中,管理会计强调加强价值管理,其目的在于提高经济效益,实现价值的最大增值。

因此,价值管理必然强调价值转移、价值增值与价值损耗之间的关系:价值转移是价值增值的前提,减少价值损耗是价值增值的手段。

为此,必须按照价值转移和增值的环节,设计价值环节和价值链。

可以说,价值管理使管理会计的重新构架成为现实。

正是因为管理会计对象具有的复合性,才使得作业管理和价值管理得以统一,构成完整的管理会计对象,并得以与其他学科区别开来。

一方面,价值环节和价值链与作业环节和作业链密切联系,基本形成一一对应的关系;另一方面,价值的增值取决于作业环节的减少和无用作业的消除(当然,整个纵向价值链的优化也是价值增值的重要方面),因为作业环节的减少和无用作业的消除将减少资源的耗费,在整个纵向价值链的价值增值额不变的情况下,必然会增加企业的价值增值额。

可以说,作业管理和价值管理是管理会计的两个轮子。

7.当准确性和及时性发生矛盾时,你将如何决策?答:准确性是指管理会计所提供的信息在相关范围内必须正确地反映客观事实。

信息总是越精确越好,但要考虑到及时性及获取高精度信息所需的处理成本,因而在管理会计中,信息的准确性以决策的正确性为标准。

由于企业管理中的决策问题千差万别,对管理会计信息的准确性也就难以有一个统一的普遍适用的标准。

“不影响决策的正确性”就是管理会计信息的“有效使用范围”。

正是基于这一特性,管理会计可以采用近似的方法来获取所需信息的近似值或估计值,以此来简化信息的处理程序,提高信息的处理效率,降低信息的处理成本。

及时性是指管理会计必须为管理者决策提供最为及时、迅速的信息。

管理会计中,有些信息是常规需要的,可设定必要的精度,在信息成本—效益平衡性原则约束下,通过程序化方式予以提供。

对于大量的非常规需要的信息,为了及时提供,往往采用近似的获取估计值或近似值。

管理会计信息的及时性以满足管理的需要为标准,没有固定的时间标准和精确性标准。

及时信息有利于正确的决策;相反,过时的信息则会导致决策的失误。

在准确性和及时性之间,管理会计会更加重视及时性,甚至愿意牺牲部分准确性以换取信息的及时性。