个人贷款英文资料

(完整版)贷款合同英文版

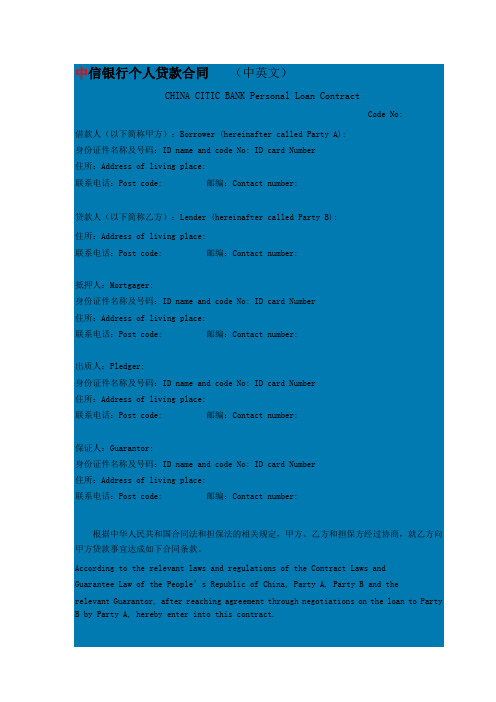

中信银行个人贷款合同(中英文)CHINA CITIC BANK Personal Loan ContractCode No:借款人(以下简称甲方):Borrower (hereinafter called Party A):身份证件名称及号码:ID name and code No: ID card Number住所:Address of living place:联系电话:Post code: 邮编:Contact number:贷款人(以下简称乙方):Lender (hereinafter called Party B):住所:Address of living place:联系电话:Post code: 邮编:Contact number:抵押人:Mortgager:身份证件名称及号码:ID name and code No: ID card Number住所:Address of living place:联系电话:Post code: 邮编:Contact number:出质人:Pledger:身份证件名称及号码:ID name and code No: ID card Number住所:Address of living place:联系电话:Post code: 邮编:Contact number:保证人:Guarantor:身份证件名称及号码:ID name and code No: ID card Number住所:Address of living place:联系电话:Post code: 邮编:Contact number:根据中华人民共和国合同法和担保法的相关规定,甲方、乙方和担保方经过协商,就乙方向甲方贷款事宜达成如下合同条款。

According to the relevant laws and regulations of the Contract Laws andGuarantee Law of the People’s Republic of China, Party A, Party B and therelevant Guarantor, after reaching agreement through negotiations on the loan to Party B by Party A, hereby enter into this contract.第一条借款金额Article 1 Amount of Loan详见本合同第十四条第一款。

个人借款合同英文范本

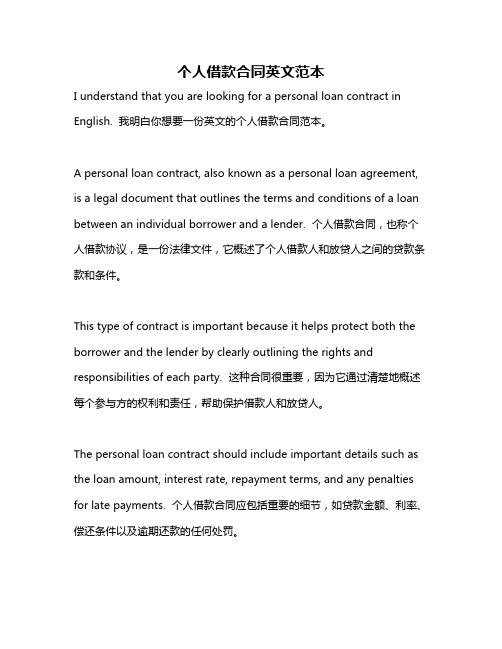

个人借款合同英文范本I understand that you are looking for a personal loan contract in English. 我明白你想要一份英文的个人借款合同范本。

A personal loan contract, also known as a personal loan agreement, is a legal document that outlines the terms and conditions of a loan between an individual borrower and a lender. 个人借款合同,也称个人借款协议,是一份法律文件,它概述了个人借款人和放贷人之间的贷款条款和条件。

This type of contract is important because it helps protect both the borrower and the lender by clearly outlining the rights and responsibilities of each party. 这种合同很重要,因为它通过清楚地概述每个参与方的权利和责任,帮助保护借款人和放贷人。

The personal loan contract should include important details such as the loan amount, interest rate, repayment terms, and any penalties for late payments. 个人借款合同应包括重要的细节,如贷款金额、利率、偿还条件以及逾期还款的任何处罚。

In addition, it should also cover other important aspects such as the loan disbursement process, conditions for early repayment, and what happens in the event of default. 另外,它也应涵盖其他重要方面,如贷款发放流程、提前偿还的条件以及在违约情况下的处理。

全版个人贷款担保合同英文版

全版个人贷款担保合同英文版Full Version Personal Loan Guarantee ContractThis document serves as a legal agreement between the lender and the guarantor in relation to a personal loan. The guarantor agrees to guarantee the repayment of the loan by the borrower in the event of default. The terms and conditions outlined in this contract are binding and enforceable by law.1. Parties Involved:- Lender: [Name of Lender]- Borrower: [Name of Borrower]- Guarantor: [Name of Guarantor]2. Loan Details:- Amount of Loan: [Insert Loan Amount]- Interest Rate: [Insert Interest Rate]- Repayment Schedule: [Insert Repayment Schedule]3. Guarantor's Obligations:- The guarantor agrees to guarantee the repayment of the loan by the borrower.- In the event of default by the borrower, the guarantor will be responsible for the outstanding amount.4. Term of Guarantee:- The guarantee provided by the guarantor will remain in effect until the loan is fully repaid or until otherwise terminated by mutual agreement.5. Release of Guarantor:- The guarantor may be released from their obligations under this contract upon written agreement between the lender, borrower, and guarantor.6. Governing Law:- This contract shall be governed by the laws of [Insert Jurisdiction].7. Dispute Resolution:- Any disputes arising from this contract shall be resolved through arbitration in accordance with the rules of [Insert Arbitration Institution].8. Severability:- If any provision of this contract is found to be invalid or unenforceable, the remaining provisions shall remain in full force and effect.9. Entire Agreement:- This contract constitutes the entire agreement between the parties and supersedes any prior agreements or understandings.10. Signatures:- Lender: [Signature]- Borrower: [Signature]- Guarantor: [Signature]By signing below, the parties acknowledge that they have read and understood the terms and conditions of this contract and agree to be bound by them.[Date of Contract]。

贷款英文合同范本

贷款英文合同范本This Loan Agreement (the "Agreement") is made and entered into as of [date] and between:The Lender:Name: [Lender's Name]Address: [Lender's Address]And the Borrower:Name: [Borrower's Name]Address: [Borrower's Address]WHEREAS, the Lender agrees to lend to the Borrower, and the Borrower agrees to borrow from the Lender, the principal amount of [amount of loan] (the "Loan").NOW, THEREFORE, in consideration of the mutual covenants and agreements hereinafter set forth, the parties hereto agree as follows:1. The Loan. The Lender shall lend to the Borrower the principal amount of the Loan, and the Borrower shall repay the Loan in accordance with the terms and conditions of this Agreement.2. Repayment. The Borrower agrees to repay the Loan in installments or in a lump sum as specified in this Agreement. The repayment schedule shall be [detl the repayment schedule].3. Interest. The Loan shall bear interest at the rate of [interest rate] per annum. Interest shall be calculated and payable as provided in this Agreement.4. Default. In the event that the Borrower fls to make any payment when due or otherwise defaults under this Agreement, the Lender shall have the right to take such actions as are provided for in this Agreement or as may be avlable law.5. Governing Law. This Agreement shall be governed and construed in accordance with the laws of [applicable law].6. Notices. All notices and other munications required or permitted underthis Agreement shall be in writing and shall be delivered to the parties at theaddresses set forth above or such other addresses as may be designated the parties in writing.IN WITNESS WHEREOF, the parties have caused this Agreement to be signed their respective authorized representatives as of the date first above written.The Lender:[Lender's Signature]The Borrower:[Borrower's Signature]Please note that this is just a basic template and should be customized and reviewed legal professionals to meet the specific needs and circumstances of the loan transaction.。

写一封关于贷款的信英文作文

写一封关于贷款的信英文作文英文回答:Dear Sir/Madam,。

I am writing to inquire about the possibility of obtaining a loan from your esteemed institution. I am in need of financial assistance for a personal project and believe that your bank may be able to provide the necessary funds.Firstly, I would like to provide you with some background information about myself. I am a hardworking individual with a stable income and a good credit history.I have been a loyal customer of your bank for several years now and have always been satisfied with the services provided.I have carefully considered my options and have decided that a loan would be the most suitable solution for mycurrent financial needs. I require a loan amount of $10,000 to cover the expenses associated with my project. I am confident that with the loan, I will be able to successfully complete the project and achieve the desired results.In terms of repayment, I am willing to negotiate a repayment plan that is both reasonable and manageable. I understand the importance of meeting my financial obligations and assure you that I will make every effort to repay the loan on time.I believe that I am a trustworthy and responsible borrower, and I hope that you will consider my loan application favorably. I am confident that with your assistance, I will be able to achieve my goals and contribute to the growth and development of our community.Thank you for considering my request. I look forward to hearing from you soon.Sincerely,。

关于loan的英文作文

关于loan的英文作文英文:When it comes to loans, there are many things to consider. Firstly, it's important to understand the different types of loans available, such as personal loans, student loans, and business loans. Each type of loan hasits own terms and conditions, so it's important to do your research and choose the one that best suits your needs.One important factor to consider when taking out a loan is the interest rate. This is the amount of money that the lender charges you for borrowing their money. A high interest rate can make it difficult to repay the loan, soit's important to find a loan with a low interest rate.Another important factor to consider is the repayment period. This is the amount of time you have to repay the loan. A longer repayment period may mean lower monthly payments, but it also means you'll be paying more ininterest over time.It's also important to consider the fees associated with the loan, such as origination fees or prepayment penalties. These fees can add up quickly, so it's important to factor them into your overall cost of borrowing.When taking out a loan, it's important to borrow only what you need and can afford to repay. Taking out too much money can lead to financial difficulties down the road.Overall, taking out a loan can be a useful tool for achieving your financial goals, but it's important to do your research and choose the right loan for your needs.中文:谈到贷款,有很多事情需要考虑。

北京银行个人贷款合同英文模板

北京银行个人贷款合同的英文模板1This is a template of the personal loan contract of Bank of Beijing.The loan amount is clearly stated as [Specific Amount]. The interest rate is determined as [Specific Rate] per annum. The repayment method shall be [Detailed Repayment Method], which could be monthly installments or others as agreed. The loan term is fixed for [Specific Period], starting from [Starting Date] and ending on [Ending Date].In case of default or failure to meet the repayment obligations on time, the borrower shall bear the corresponding liability for breach of contract. Penalties and additional charges will be imposed as per the regulations. If the borrower fails to repay the loan within the agreed period, the lender has the right to take legal actions to recover the outstanding amount and any associated costs.The borrower undertakes to provide true and accurate information during the loan application process. Any false or misleading information provided may lead to the termination of the loan contract and legal consequences.This contract is subject to the laws and regulations of the People's Republic of China and the relevant rules and policies of Bank of Beijing. Any disputes arising from this contract shall be resolved through amicablenegotiation or legal proceedings.2This is a template of the personal loan contract of Bank of Beijing.The borrower (hereinafter referred to as Party A) agrees to borrow a certain amount of money from Bank of Beijing (hereinafter referred to as Party B). Party A shall repay the loan in accordance with the agreed repayment schedule and method. The repayment shall include both the principal and the accrued interest.Party B has the right to supervise the use of the loan funds by Party A to ensure that they are used for the agreed purposes. In case of default by Party A, Party B reserves the right to take legal measures to recover the loan and impose penalties as stipulated.Party A undertakes to provide true and valid information during the loan application process. Any false information provided may lead to the termination of the loan contract and legal consequences.The interest rate of the loan shall be determined in accordance with the relevant regulations and policies of the People's Bank of China and Bank of Beijing. Changes in the interest rate shall be notified to Party A in a timely manner.This contract is subject to the laws and regulations of the People's Republic of China. Any disputes arising from this contract shall be resolved through friendly negotiation. If negotiation fails, either party may resort tolegal means for settlement.The terms and conditions of this contract are binding on both parties. Any amendment or supplementation to this contract shall be made in writing and signed by both parties.3This is a template of the personal loan contract of Bank of Beijing.The contract shall come into effect upon the signature of both the borrower and the lender. The borrower is obligated to provide true and valid information and to repay the loan in accordance with the agreed terms and schedules.In case of any disputes arising from this contract, both parties shall first attempt to resolve the issue through friendly negotiation. If the negotiation fails, either party may file a lawsuit in the court having jurisdiction as stipulated by law.Confidentiality is a crucial aspect of this contract. Both the borrower and the lender shall keep all information related to the loan transaction strictly confidential and shall not disclose it to any third party without the prior written consent of the other party.The borrower shall use the loan funds for the specified purpose and shall not divert them for any other purposes. Any violation of this provision shall be regarded as a breach of contract.The lender reserves the right to monitor the use of the loan funds andto take necessary measures in case of any suspected irregularities.This contract constitutes the entire agreement between the borrower and the lender regarding the loan transaction and supersedes all previous oral or written agreements.4This is a template of the personal loan contract for Bank of Beijing.The borrower agrees to use the loan funds for specific purposes as approved by the bank and shall not use the funds for any illegal or unauthorized activities. The loan purposes are strictly limited and any deviation may result in consequences.Regarding early repayment, the borrower has the right to make early repayments. However, a certain notice period should be provided and there might be associated fees or penalties depending on the timing and amount of the early repayment.In case of overdue repayments, the borrower shall be liable for additional charges and interest. The bank reserves the right to take legal actions to recover the outstanding amount and may report the default to relevant credit agencies, which could adversely affect the borrower's credit record.The borrower is obligated to provide accurate and up-to-date information throughout the loan period. Any false or misleading information may lead to the termination of the loan contract and legalconsequences.This contract is subject to the laws and regulations of the People's Republic of China and any disputes shall be resolved through legal channels.The terms and conditions of this loan contract are binding on both the borrower and the bank, and both parties shall abide by them.5This is a sample personal loan contract of Bank of Beijing.Party A (the Lender): Bank of BeijingParty B (the Borrower): [Full Name]Loan Amount: The loan amount provided by Party A to Party B is [Specific Amount].Loan Term: The loan term commences on [Start Date] and ends on [End Date].Interest Rate: The interest rate is determined as [Rate] per annum.Repayment: Party B shall repay the loan in accordance with the agreed repayment schedule.Guarantee Clause: In order to secure the loan, Party B shall provide [Type of Guarantee] as guarantee.Notification Obligation: Party B shall promptly notify Party A of any significant changes in personal circumstances or financial status.Applicable Law: This contract shall be governed by the laws of thePeople's Republic of China.In the event of default by Party B, Party A has the right to take legal measures to recover the loan and associated interests and penalties.This contract constitutes the entire agreement between the parties and supersedes all prior negotiations and understandings. Any amendments or supplements to this contract must be made in writing and signed by both parties.。

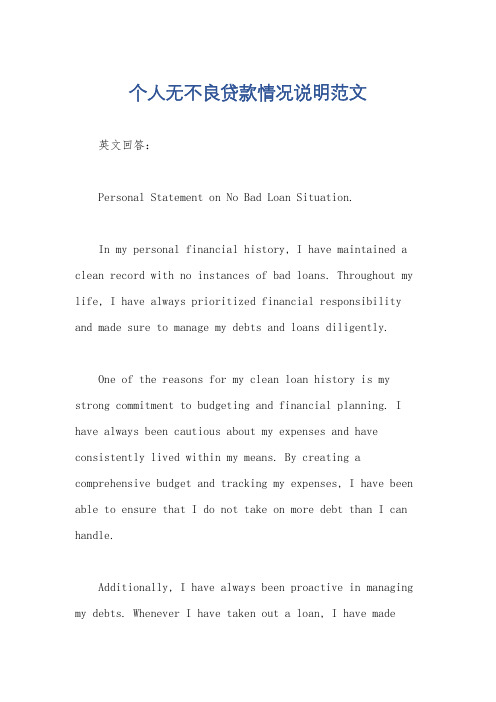

个人无不良贷款情况说明范文

个人无不良贷款情况说明范文英文回答:Personal Statement on No Bad Loan Situation.In my personal financial history, I have maintained a clean record with no instances of bad loans. Throughout my life, I have always prioritized financial responsibility and made sure to manage my debts and loans diligently.One of the reasons for my clean loan history is my strong commitment to budgeting and financial planning. I have always been cautious about my expenses and have consistently lived within my means. By creating a comprehensive budget and tracking my expenses, I have been able to ensure that I do not take on more debt than I can handle.Additionally, I have always been proactive in managing my debts. Whenever I have taken out a loan, I have madesure to carefully consider the terms and conditions,interest rates, and repayment plans. I have always chosen reputable lenders and have thoroughly reviewed all the necessary documentation before signing any loan agreement.Furthermore, I have a stable source of income, whichhas allowed me to comfortably meet my financial obligations.I prioritize making timely payments on all my debts, including credit cards, student loans, and mortgages. This has helped me build a strong credit history and maintain a good credit score.In summary, my personal financial history reflects my commitment to financial responsibility and prudent debt management. Through budgeting, proactive debt management, and a stable source of income, I have successfully maintained a clean record with no instances of bad loans.中文回答:个人无不良贷款情况说明。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Material Source: Hitotsubashi University Author: lichiro uesugiRole of collateral and personal guarantees in relationship lending: evidence fromJapan's SME loan market1 IntroductionA key issue of interest in the recent literature on financial intermediation has been the role of relationship lending. Relationship lending is particularly common in the case of small business lending, because small businesses typically rely on bank loans for a substantial part of their financing needs but also tend to be informationally opaque. An important issue in this context is the use of collateral, which is a common feature of loan contracts between small firms and banks around the world, and a number of theoretical and empirical studies have examined why it is so widespread and how it relates to the incentives for borrowers and lenders and the borrower-lender relationship. For instance, it has been argued that in the presence of information asymmetries between creditors and borrowers, collateral may mitigate the problem of adverse selection (Bester, 1985; 1987) and/or the problem of moral hazard (Bester, 1994; Boot, Thakor, and Udell, 1991). Collateral also affects the incentives of creditors, who will use it either as a substitute for (Manove, Padilla, and Pagano, 2001) or complement to (Rajan and Winton, 1995; Boot 2000; Longhofer and Santos, 2000) screening and monitoring efforts. Another aspect of collateral that studies have concentrated on is that its presence may depend on the length and intimacy of the relationship between creditors and borrowers (Boot, 2000; Boot and Thakor, 1994; Sharpe, 1990). Existing empirical research has yet to reach decisive conclusions about the nature of these relationships.This paper seeks to contribute to the existing literature on collateral using a unique firm-level data set of the small and medium sized enterprise (SME) loan market in Japan. Explicitly differentiating physical collateral (such as real estate) and personal guarantees by business representatives, we investigate how the use of collateral and personal guarantees affects the incentives of borrowers, lenders, and the relationship between them. More specifically, we examine the following three issues. First, we examine whether riskier borrowers are more likely to be required to provide collateral or personal guarantees. Second, we investigate how collateral and personal guarantees affect banks’ monitoring of borrowers. Third, we examine the correlation between the use of collateral and personal guarantees on the one hand and the closeness of borrower-lender relationships on the other.The data set we employ is based mainly on the “Survey of the Financial Environment” (SFE) conducted by the Small and Medium Enterprise Agency of Japan in October 2002. In order to focus on firms that mostly depend on bank loans for their financing, we limit the sample to firms satisfying the legal definition of an SME in Japan. We then combine the SFE data for each SME with information on their main bank obtained from the bank’s financial statements in order to control for lender characteristics as well. Furthermore, to control for the effect of government credit guarantees on collateral and personal guarantees, in the main analysis of this paper we exclude from the sample all firms that enjoyed any form of government credit guarantee.As a result of this screening process, we end up with a sample of 1,702 firms. Our main findings can be summarized as follows. We find that firms’ riskiness does not have a significant effect on the likelihood that collateral is used. Thus, we cannot find firm evidence that the use of collateral mitigates moral hazard. We find, however, that banks whose claims are collateralized monitor borrowers more intensively, and that borrowers who have a long-term relationship with their main bank are more likely to pledge collateral. These findings suggest that collateral is complementary to relationship lending. In contrast, the complementarity between relationship lending and personal guarantees is weaker.As far as we know, this is the first empirical study that systematically examines the role of collateral and personal guarantees in Japan’s SME loan market. The two main contributions of the paper are as follows. First, given that Japan is generally considered to have a relationship-based financial system in which the relationship-lender, the main bank, plays a central role in corporate financing (Rajan and Zingales, 2003), the study helps to improve our understanding of the role of collateral in relationship lending and complements existing studies that focus on the United States and Europe. Second, and more importantly, by distinguishing collateral and personal guarantees, the study detects an important role of collateral in relationship lending that has not been remarked on much before. As we argue below, although a typical SME in Japan has a long-term relationship with its main bank, it actually engages in transactions with several banks, which is not common in other countries. A possible corollary of this is that because of the informational free-rider problem it creates, this practice may reduce the main bank’s incentive to screen and monitor borrowers. Since collateral defines the order of seniority amongcreditors, using collateral may mitigate the free-rider problem and enhance the main bank’s screening and monitoring. This incentive effect for the main bank becomes tenuous for personal guarantees, because personal guarantees do not define the seniority among creditors. Thus, our work provides empirical evidence on how collateral affects relationship lenders’ incentives, and complements previous studies that focus on the problem of borrower incentives (moral hazard and adverse selection).The remainder of the paper is organized as follows. Section 2 develops our empirical hypotheses which are based on previous theoretical models and empirical research. Section 3 describes the data and variables that are used in the paper, and explains our empirical model.Section 4 presents the results of our empirical analysis, and Section 5 concludes.2 Empirical hypotheses2.1 Borrower riskinessMuch of the empirical literature in this field examines theoretical predictions of asymmetric information models on the relationship between risk and collateral. If the bank cannot discern borrowers’ riskiness (hidden information), then collateral may serve as a screening device to distinguish between borrowers and to mitigate the adverse selection problem (Bester, 1985). This follows from the observation that a lower-risk borrower has a greater incentive to pledge collateral than a risky borrower, because of his lower probability of failure and loss of collateral. Hence, the lower-risk borrower will choose the contract with collateral.On the other hand, if the lender can observe the ex-ante risk, but there are information asymmetries with regard to actions taken by the borrower after the loan is extended, collateral potentially provides an incentive to mitigate moral hazard. Thus, opposite to models focusing on hidden information, those concentrating on hidden action suggest that it is observably riskier borrowers that will pledge collateral, because collateral induces more effort by the borrower (Boot, Thakor, and Udell, 1991), or reduces the incentives of strategic default (Bester, 1994).Because our data base only contains measures of firms’ observed riskiness (namely, credit scores), we couch our first empirical hypothesis as follows: Hypothesis 1 (H1): The use of collateral is higher among observably higher-risk (low credit score) borrowers if the lender requires collateral in order to mitigate the extent of moral hazard.Alternatively, if borrowers pledge collateral as a signal of their unobserved high credit quality, then there is negative or no relationship between the use of collateral and the credit score.Consistent with the theory of moral hazard, most existing empirical studies, including Berger and Udell (1990; 1995), have found a positive relationship between collateral and borrowers’ ex-ante risk. Jiménez, Salas and Saurina (2006) directly test the adverse selection and moral hazard hypotheses by separating ex-ante and ex-post measures of borrower riskiness, namely defaults prior to and after the loan origination. Their results suggest that although observed riskiness increases the likelihood that collateral is used, there is also a negative association between collateral and default after the loan has been granted, which is consistent with the adverse selection argument.It should be noted that theories of collateral as a solution to moral hazard and/or adverse selection problems assume collateral is external to the firm.Unfortunately, our measure of the incidence of collateral does not distinguish between firm (inside) collateral and personal (outside) collateral. Hence, throughout our analysis, we will assume that collateral is mostly inside, but allow for the fact that there may also be some outside collateral. As for personal guarantees, they clearly represent outside collateral.2.2 Screening and monitoring by the lenderRecent research on collateral also discusses how collateral affects lenders’ incentives with regard to information production, that is, the screening of borrowers’quality and the monitoring of their performance. These theories of the effect of collateral on lenders’ incentives apply to both inside and outside collateral. Manove, Padilla, and Pagano (2001), for instance, argue that, from banks’ point of view, collateral can be considered as a substitute for the evaluation of the actual risk of a borrower. Thus, banks that are highly protected by collateral may perform less screening of the projects they finance than is socially optimal.However, several theoretical studies argue that collateral may complement lenders’ screening and monitoring activities. In the presence of other claimants, lenders’ incentive to monitor borrowers is reduced due to the informational free-rider problem. In order to enhance lenders’ incentive to monitor, loan contracts must be structured in a way that makes lenders’ payoff sensitive to borrowers’ financial health. Rajan and Winton (1995) argue that collateral may serve as acontractual device to increase lenders’ monitoring incent ive, because collateral is likely to be effective only if its value can be monitored. Moreover, the use of collateral as an incentive will be more extensive when the value of such collateral (as in the case of accounts receivable and inventories, for example) depreciates rapidly if business conditions deteriorate, than when the value of collateral is relatively stable (as in the case of, e.g., real estate). Longhofer and Santos (2000) argue that collateral serves as an incentive for information production by the principal lender in the presence of several creditors, because taking collateral is effective in making its loan senior to other creditors’ claims. Thus, the bank that provides collateralized loan is able to reap the benefits of screening and monitoring activities. Note that this argument does not straightforwardly apply to personal guarantees, because, in general, personal guarantees do not define seniority among several creditors.As we have a proxy variable for the intensity of monitoring by the principal lender, our second hypothesis for the empirical analysis is as follows:Hypothesis 2 (H2): The use of collateral decreases with the intensity of monitoring by the principal lender if collateral reduces lenders’ incentive to exert effort in loan management. Alternatively, if collateral serves as an incentive device to induce monitoring efforts by the principal lender in the presence of other claimants, then we expect a positive relationship between the use of collateral and monitoring intensity.To our knowledge, there are only two existing studies that empirically assess whether the use of collateral and personal guarantees substitute for or complement screening and monitoring by the lender. Examining Spanish loan data, Jiménez, Salas and Saurina (2006) found that banks with a lower level of expertise (smaller banks and savings banks) in small business lending use collateral more intensively. This is consistent with the theory that collateral is used as a substitute for the evaluation of credit risk. The present study complements these works investigating the relationship between collateral and screening by focusing on the relationship between collateral and monitoring using Japanese firm data. Our proxy variable for monitoring intensity is the frequency of document submissions to the main bank.2.3 Relationship between the borrower and the lenderThe existing literature on relationship lending provides conflicting predictions on how the strength of the relationship between borrower and lender affects the likelihood of collateral being pledged. By establishing a solid relationship with theborrower, the lender learns about the hidden attributes and actions of the borrower, thus reducing information asymmetries. Hence, the terms of loan contracts may become more favorable to the borrower if the firm has transactions with a specific relationship lender over a long period of time and thus establishes trust, resulting in a lower likelihood of collateral being pledged (Boot and Thakor, 1994). However, a solid relationship may become detrimental to the borrower if the bank exerts its information monopoly by charging higher interest rates or requiring more collateral (Sharpe, 1990). If such a hold-up problem is indeed common, then there is likely to be a positive correlation between the strength of a relationship and the use of collateral. It should be noted that these theories assume that the collateral is outside collateral. In addition, collateral can also be used as an incentive device in mitigating the soft-budget constraint problem in relationship lending (Boot, 2000). For example, consider the case where a borrower in difficulty asks the bank for more credit and reduced interest obligations in order to avoid default. Although a transaction-based lender would not lend to such a borrower, a relationship lender that has already made loans might accept the borrower’s request in the hope of recovering a previous loan. However, once the borrower realizes he can renegotiate the loan contract relatively easily, he has an incentive to misbehave ex ante (the soft budget problem). In such cases, collateral will increase the ex-post bargaining power of the lender and hence reduce the extent of the soft-budget constraint problem, because collateral makes the value of the lender’s claim less sensitive to the borrower’s total net worth. These theoretical considerations apply to inside collateral as well as outside collateral and lead to the following hypothesis:Hypothesis 3 (H3): Borrowers that establish a solid relationship with their principal lender are less likely to use collateral if the relationship reduces information asymmetries and enhances mutual trust between the borrower and the lender. Alternatively, borrowers with a strong relationship with their principal lender are more likely to use collateral if the effects of the hold-up problem or the mitigation of the soft-budget constraint problem dominate.。