衍生工具试题Questions

银行考试金融衍生工具问题

银行考试金融衍生工具问题

例:1.决定期权价格的因素有( )。

A.合同金额

B.执行价格

C.期权期限

D.无风险市场利率

E.期权代表资产的风险度

【答案】BCDE。

中公解析:期权价格包含内在价格和时间价格。

内在价格取决于执行价格和市场价格之间的关系。

时间价格主要取决于以下三个因素:标的资产波动性(资产的风险度)、期权合约期限以及无风险市场利率的高低。

该题难度较高,不同于以往简单考察金融衍生工具的定义,考察了金融衍生工具期权的定价。

例:买卖双方分别承诺在将来某一特定时间按照事先确定的价格,购买和提供某种商品,这种金融衍生工具是( )。

A.远期合约

B.期权合约

C.票据发行便利

D.互换交易

【答案】A。

中公解析:远期的含义。

期权主要是赋予期权购买者未来买卖某种资产的权利。

票据发行便利是指银行同客户签订一项具有法律约束力的承诺,期限一般为5-7年,银行保证客户以自己的名义发行短期票据,银行则负责包销或提供没有销售出部分的等额贷款。

是贷款承诺的一种。

互换是一种约定两个或两个以上的当事人按照协议条件及在约定的时间内交换一系列现金流的衍生工具。

该题相对简单,考察几种常见的金融衍生工具的概念。

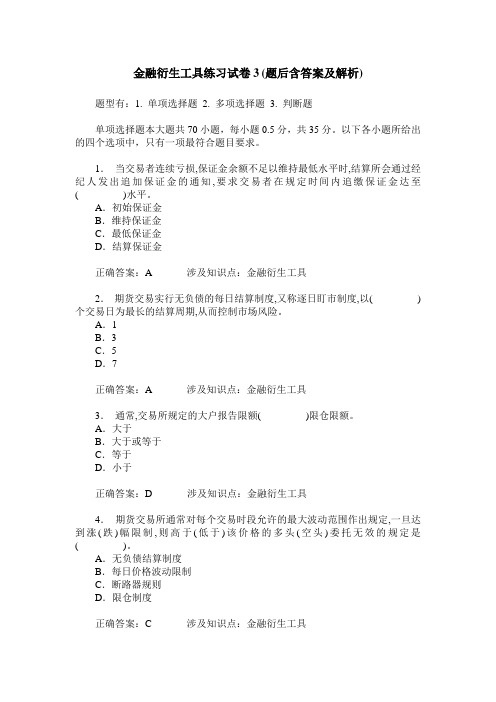

金融衍生工具练习试卷3(题后含答案及解析)

金融衍生工具练习试卷3(题后含答案及解析) 题型有:1. 单项选择题 2. 多项选择题 3. 判断题单项选择题本大题共70小题,每小题0.5分,共35分。

以下各小题所给出的四个选项中,只有一项最符合题目要求。

1.当交易者连续亏损,保证金余额不足以维持最低水平时,结算所会通过经纪人发出追加保证金的通知,要求交易者在规定时间内追缴保证金达至( )水平。

A.初始保证金B.维持保证金C.最低保证金D.结算保证金正确答案:A 涉及知识点:金融衍生工具2.期货交易实行无负债的每日结算制度,又称逐日盯市制度,以( )个交易日为最长的结算周期,从而控制市场风险。

A.1B.3C.5D.7正确答案:A 涉及知识点:金融衍生工具3.通常,交易所规定的大户报告限额( )限仓限额。

A.大于B.大于或等于C.等于D.小于正确答案:D 涉及知识点:金融衍生工具4.期货交易所通常对每个交易时段允许的最大波动范围作出规定,一旦达到涨(跌)幅限制,则高于(低于)该价格的多头(空头)委托无效的规定是( )。

A.无负债结算制度B.每日价格波动限制C.断路器规则D.限仓制度正确答案:C 涉及知识点:金融衍生工具5.外汇期货是以外汇为基础工具的期货合约,主要作用是( )。

A.增加投资品种B.规避外汇风险C.增加金融衍生工具品种D.进行外汇投资正确答案:B 涉及知识点:金融衍生工具6.( )主要是指人们在国际贸易中因汇率变动而遭受损失的可能性,是外汇风险中最常见且最重要的风险。

A.商业性汇率风险B.债权债务风险C.储备风险D.结算风险正确答案:A 涉及知识点:金融衍生工具7.利率期货的基础资产主要是( )。

A.即期利率B.远期利率C.固定收益金融工具D.利率指数正确答案:C 涉及知识点:金融衍生工具8.1975年10月,利率期货产生于( )。

A.美国证券交易所B.堪萨斯农产品交易所C.纽约证券交易所D.芝加哥期货交易所正确答案:D 涉及知识点:金融衍生工具多项选择题本大题共60小题,每小题0.5分,共30分。

金融衍生工具测试题(11)

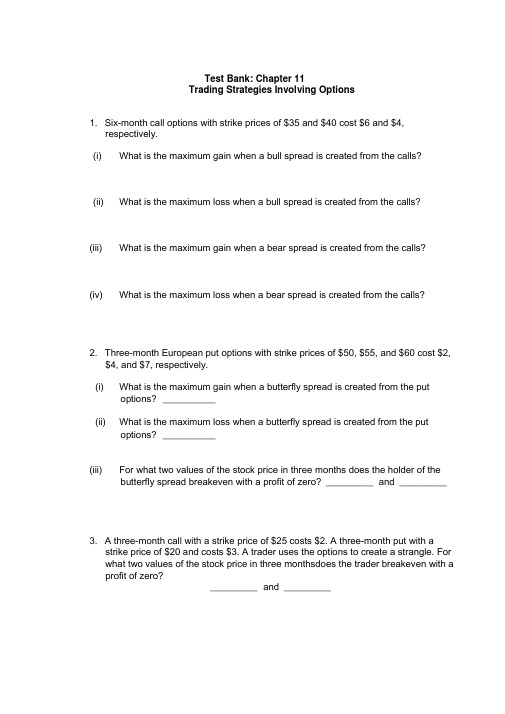

Test Bank: Chapter 11Trading Strategies Involving Options1. Six-month call options with strike prices of $35 and $40 cost $6 and $4,respectively.(i) What is the maximum gain when a bull spread is created from the calls?(ii) What is the maximum loss when a bull spread is created from the calls?(iii) What is the maximum gain when a bear spread is created from the calls? (iv) What is the maximum loss when a bear spread is created from the calls?2. Three-month European put options with strike prices of $50, $55, and $60 cost $2,$4, and $7, respectively.(i) What is the maximum gain when a butterfly spread is created from the putoptions? __________(ii) What is the maximum loss when a butterfly spread is created from the put options? __________(iii) For what two values of the stock price in three months does the holder of the butterfly spread breakeven with a profit of zero? _________ and _________ 3. A three-month call with a strike price of $25 costs $2. A three-month put with astrike price of $20 and costs $3. A trader uses the options to create a strangle. For what two values of the stock price in three monthsdoes the trader breakeven with a profit of zero?_________ and _________。

基金从业资格考试衍生工具练习题

第九章衍生工具一、单项选择题1、衍生工具是由另一种()构成或衍生而来的交易合约。

A、基础资产B、有形资产C、无形资产D、不动产2、关于衍生工具的组成要素,下列表述错误的是()。

A、衍生工具是在合约标的资产基础上创造出来的B、交割价格通常取决于合约标的资产的价格C、所有的衍生工具都会规定一个合约到期日D、衍生工具的结算可以按合约规定在到期日或者在到期日之前结算3、衍生资产价格与()的价格具有联动性。

A、商品市场B、外汇市场C、股票市场D、标的资产4、无论是哪一种衍生工具,都会影响交易者在未来某一时间的现金流,这体现了衍生工具的()特征。

A、不确定性或高风险性B、杠杆性C、跨期性D、联动性5、交易双方约定在未来的某一确定的时间,按约定的价格买入或卖出一定数量的某种合约标的资产的合约称为()。

A、期货合约B、期权合约C、互换合约D、远期合约6、按照衍生工具的产品形态分类,衍生工具可以分为独立衍生工具和()。

A、货币衍生工具B、结构化金融衍生工具C、嵌入式衍生工具D、商品衍生工具7、下列关于衍生工具的说法,错误的是()。

A、按产品形态可以分为独立衍生工具、嵌入式衍生工具B、按合约特点可以分为远期合约、期货合约、期权合约、互换合约和结构化金融衍生工具C、独立衍生工具指期权合约、期货合约或者互换合约D、远期合约、期货合约、期权合约、结构化金融衍生工具常被称为基础性衍生模块8、商品衍生工具指以商品为合约标的资产的金融衍生工具,主要包括()。

A、各种大宗商品的互换合约B、各种大宗商品的远期合约C、各种大宗商品的期权合约D、各种大宗商品的期货合约9、在金融衍生工具中,远期合约的最大功能是()。

A、方便交易B、增加交易量C、增加收益D、转移风险10、远期价格是远期市场为当前交易的一个远期合约而提供的交割价格,它使得远期合约的当前价值为()。

A、0B、1C、﹣1D、211、关于看涨期权交易双方的潜在盈亏,下列说法正确的是()。

衍生金融工具 习题及答案 期末必看资料

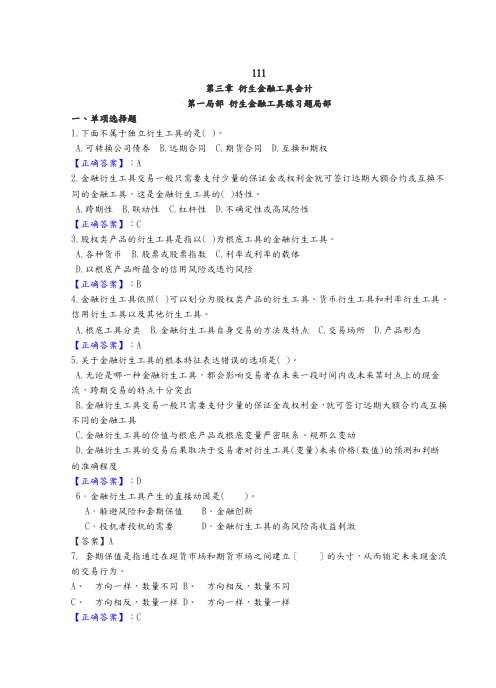

111第三章衍生金融工具会计第一局部衍生金融工具练习题局部一、单项选择题1.下面不属于独立衍生工具的是( )。

A.可转换公司债券B.远期合同C.期货合同D.互换和期权【正确答案】:A2.金融衍生工具交易一般只需要支付少量的保证金或权利金就可签订远期大额合约或互换不同的金融工具,这是金融衍生工具的( )特性。

A.跨期性B.联动性C.杠杆性D.不确定性或高风险性【正确答案】:C3.股权类产品的衍生工具是指以( )为根底工具的金融衍生工具。

A.各种货币B.股票或股票指数C.利率或利率的载体D.以根底产品所蕴含的信用风险或违约风险【正确答案】:B4.金融衍生工具依照( )可以划分为股权类产品的衍生工具、货币衍生工具和利率衍生工具、信用衍生工具以及其他衍生工具。

A.根底工具分类B.金融衍生工具自身交易的方法及特点C.交易场所D.产品形态【正确答案】:A5.关于金融衍生工具的根本特征表达错误的选项是( )。

A.无论是哪一种金融衍生工具,都会影响交易者在未来一段时间内或未来某时点上的现金流,跨期交易的特点十分突出B.金融衍生工具交易一般只需要支付少量的保证金或权利金,就可签订远期大额合约或互换不同的金融工具C.金融衍生工具的价值与根底产品或根底变量严密联系、规那么变动D.金融衍生工具的交易后果取决于交易者对衍生工具(变量)未来价格(数值)的预测和判断的准确程度【正确答案】:D6.金融衍生工具产生的直接动因是( )。

A.躲避风险和套期保值 B.金融创新C.投机者投机的需要 D.金融衍生工具的高风险高收益刺激【答案】A7. 套期保值是指通过在现货市场和期货市场之间建立〔〕的头寸,从而锁定未来现金流的交易行为。

A、方向一样,数量不同B、方向相反,数量不同C、方向相反,数量一样D、方向一样,数量一样【正确答案】:C8. 20世纪80年代以来的金融自由化内容不包括( )。

A.取消对存款利率的最高限额,逐步实现利率自由化B.打破金融机构经营范围的地域和业务种类限制,允许各金融机构业务穿插、互相自由渗透,鼓励银行综合化开展C.放松存款准备金率的控制D.开放各类金融市场,放宽对资本流动的限制【正确答案】:C9. 两个或两个以上的当事人按共同商定的条件,在约定的时间内定期交换现金流的金融交易是( )。

金融衍生工具测试题 (5)

Test Bank: Chapter 5The Determinants of Forward and Futures Prices1.An investor shorts 100 shares when the share price is $50 and closes out the positionsix months later when the share price is $43. The shares pay a dividend of $3 per share during the six months. How much does the investor gain? _ _ _ _ _ _2.The spot price of an investment asset that provides no income is $30 and the risk-freerate for all maturities (with continuous compounding) is 10%. What, to the nearest cent, is the three-year forward price? _ _ _ _ _ _3.Repeat question 2 on the assumption that the asset provides an income of $2 at theend of the first year and at the end of the second year. _ _ _ _ _ _4.In question 2 what is the value to the nearest cent of a three-year forward contractwith a delivery price of $30? _ _ _ _ _ _5.An exchange rate is 0.7000 and the six-month domestic and foreign risk-free interestrates are 5% and 7% (both expressed with continuous compounding). What is the six-month forward rate? Give four decimal places _ _ _ _ _ _6. A short forward contract that was negotiated some time ago will expire in threemonths and has a delivery price of $40. The current forward price for three-month forward contract is $42. The three month risk-free interest rate (with continuous compounding) is 8%. What to the nearest cent is the value of the short forward contract? _ _ _ _ _ _7.The spot price of an asset is positively correlated with the market. Which of thefollowing would you expect to be true (circle one)(a)The forward price equals the expected future spot price.(b)The forward price is greater than the expected future spot price.(c)The forward price is less than the expected future spot price.(d)The forward price is sometimes greater and sometimes less than the expectedfuture spot price.8.The one-year Canadian dollar forward exchange rate is quoted as 1.0500. What thecorresponding futures quote? Give four decimal places _ _ _ _ _ _9.Which of the following is a consumption asset (circle one)(a)The S&P 500 index(b)The Canadian dollar(c)Copper(d)IBM shares10.Which of the following is true (circle one)(a)The convenience yield is always positive or zero.(b)The convenience yield is always positive for an investment asset.(c)The convenience yield is always negative for a consumption asset.(d)The convenience yield measures the average return earned by holding futurescontracts.。

金融衍生工具考试题

金融衍生工具考试题一、单选题(每题1分,共10题)1、金融衍生工具是一种金融合约,其价值取决于()A、利率B、汇率C、基础资产价格D、商品价格2、(),又称柜台市场,是指银行与客户、金融机构之间关于利率、外汇、股票及其指数方面为了套期保值、规避风险或投机而进行的衍生产品交易。

A、场外市场B、场内市场C、中间市场D、银行间市场3、两个或两个以上的参与者之间,或直接、或通过中介机构签订协议,互相或交叉支付一系列本金、或利息、或本金和利息的交易行为,是指()A、远期B、期货C、期权D、互换4、如果一年期的即期利率为10%,二年期的即期利率为10.5%,那么一年到两年的远期利率为()A、11%B、10.5%C、12%D、10%5、客户未在期货公司要求的时间内及时追加保证金或者自行平仓的,期货公司会将该客户的合约强行平仓,强行平仓的相关费用和发生的损失由()承担。

A、期货公司B、期货交易所C、客户D、以上三者按一定比例分担6、下列公式正确的是()A、交易的现货价格=商定的期货价格 + 预先商定的基差B、交易的现货价格=市场的期货价格 + 预先商定的基差C、交易的现货价格=商定的期货价格—预先商定的基差D、交易的现货价格=市场的期货价格—预先商定的基差7、以下属于利率互换的特点是()A、交换利息差额,不交换本金B、既交换利息差额,又交换本金C、既不交换利息差额,又不交换本金D、以上都不是8、按买卖的方向,权证可以分为()A、认购权证和认沽权证B、欧式权证和美式权证C、股本型权证和备兑型权证D、实值权证和虚值权证9、假定某投资者预计3个月后有一笔现金流入可用来购买股票,为避免股市走高使3个月后投资成本增大的风险,则可以先买入股票指数()A、欧式期权B、看跌期权C、看涨期权D、美式期权10、利率低实际上可以看作是一系列()的组合A、浮动利率欧式看涨期权B、浮动利率欧式看跌期权C、浮动利率美式看涨期权D、浮动利率美式看跌期权11、按照基础资产分类,衍生金融工具可以分为:股权式衍生工具、货币衍生工具、()和商品衍生工具。

金融衍生工具测试题(5)

Test Bank: Chapter 5The Determinants of Forward and Futures Prices1. An investor shorts 100 shares when the share price is $50 and closes out the positionsix months later when the share price is $43. The shares pay a dividend of $3 per share during the six months. How much does the investor gain? _______2. The spot price of an investment asset that provides no income is $30 and the risk-freerate for all maturities (with continuous compounding) is 10%. What, to the nearest cent, is the three-year forward price? ________3. Repeat question 2 on the assumption that the asset provides an income of $2 at theend of the first year and at the end of the second year. _______4. In question 2 what is the value to the nearest cent of a three-year forward contract witha delivery price of $30? _____________5. An exchange rate is 0.7000 and the six-month domestic and foreign risk-free interestrates are 5% and 7% (both expressedwith continuous compounding). What is the six-month forward rate? Give four decimal places ___________6. A short forward contract that was negotiated some time ago will expire in three monthsand has a delivery price of $40. The current forward price for three-month forward contract is $42. The three month risk-free interest rate (with continuous compounding) is 8%. What to the nearest cent is the value of the short forward contract?7. The spot price of an asset is positively correlated with the market. Which of thefollowing would you expect to be true (circle one)(a) The forward price equals the expected future spot price.(b) The forward price is greater than the expected future spot price.(c) The forward price is less than the expected future spot price.(d) The forward price is sometimes greater and sometimes less than the expectedfuture spot price.8. The one-year Canadian dollar forward exchange rate is quoted as 1.0500. What thecorresponding futures quote? Give four decimal places _______9. Which of the following is a consumption asset (circle one)(a) The S&P 500 index(b) The Canadian dollar(c) Copper(d) IBM shares10. Which of the following is true (circle one)(a) The convenience yield is always positive or zero.(b) The convenience yield is always positive for an investment asset.(c) The convenience yield is always negative for a consumption asset.(d) The convenience yield measures the average return earned by holding futurescontracts.。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

FINA 0301/2322:DerivativesReview questions,Fall,20131.Which of the positions can result in the following profit diagram?ProfitStock priced d d d d d d d d d d(a)Buy one low strike call,sell two high-strike calls.(b)Buy one high strike call,sell two low strike calls.(c)Buy two strike call,sell three 1050-strike calls.(d)Buy three strike call,sell five 1050-strike calls.Answer:A2.Which of the following phrases is used to describe an option where the strike price is approximately equal to the asset price?(a)At-the-money(b)In-the-money(c)Over-the-money(d)Out-of-the-moneyAnswer:A3.Assume that you purchase 100shares of Jiffy,mon stock at the bid-ask prices of $32.00-$32.50.When you sell the bid-ask prices are $32.50-$33.00.If you pay a commission rate of 0.5%,what is your profit or loss?(a)$0(b)$16.25loss(c)$32.50gain(d)$32.50lossAnswer:D(32.50−32.50)×100+(32.50+32.50)×100×0.5%=32.504.A put option was purchased1year ago.The Exercise price on the underlying asset is$40.If thecurrent price of the asset is$36.45and the future value of the original option premium is$1.62, what is the put profit,if any today?(a)$1.62(b)$1.93(c)$3.55(d)$5.17Answer:B(40−36.45)−1.62=1.935.A strategy consists of buying a market index product at the spot price of$830and longing a puton the index with a strike of$830.If the put premium is$18.00and interest rates are0.5%per month,what is the profit or loss from the long index position by itself at expiration(in6months) if the market index is$810.(a)$45.21loss(b)$21.22loss(c)$18.00gain(d)$24.25gainAnswer:A810−830×1.0056=−45.216.At the6-month point,what is the breakeven index price for a strategy of longing the market indexat a price of830?Effective interest rates are0.5%per month.(a)$802.12(b)$830.00(c)$855.21(d)$866.32Answer:C,you break even when your cost equals your payoff830×1.0056=855.217.The$830strike put premium is$18.00and the call premium is$42.47.The$850strike putpremium is$25.45and the$850strike call is selling for$30.51.What is the maximum profit that an investor can obtain from a strategy employing a long830call and a short850call over6 months?Interest rates are0.5%per month.(c)$6.10(d)$12.32Answer:B,think about the diagram of the bull spread–you achieve maximum profit when the price goes up,and they buyer of the high strike call exercises.Of course you exercise your low strick call as well.Therefore,figure out your payoff,subtract your cost for the options(850−830)−(42.47−30.51)×1.0056=7.688.What is the break even point that an investor can obtain from a6-month strategy employing along830call and a short850call?Interest rates are0.5%per month.(a)$832.82(b)$842.32(c)$852.22(d)$862.92Answer:B,to break even,you must receive some money by exercising the830-call to cover the cost for the options.Figure out your payoffS T−E,then subtract your cost for the options.Set S T=x,(x−830)−(42.47−30.51)×1.0056=0x=842.329.A strategy consists of longing a put on the market index with a strike of850and shorting a calloption on the market index with a strike price of850.The put premium is$25.45and the call premium is$30.51.Interest rates are0.5%per month.What is the breakeven price of the market index for this strategy at expiration(in6months)?(a)$802.12(b)$830.00(c)$855.21(d)$866.32Answer:C,the payoffto the same strike price long put is Max[E−S T,0],and short call is–Max[0, S T−E].Combined,it is just E−S T.This is your payoff.To breakeven,set S T=x,and let payoffequal your cost for the options,850−x−(25.45−30.51)×1.0056=0x=855.2110.Farmer Jayne bought a$1.70strike put option for$0.11and sold a$1.75strike call option fora premium of$0.14.Her total costs are$1.65per bushel and interest rates are4.0%over thisperiod.What is thefloor in her strategy assuming a20,000-bushel crop?(c)$2,624(d)$3,624Answer:B,if the selling price goes down,you can always exercise your put option.Figure out your payoff,then subtract your cost for the options(1.70−1.65)×20,000−(0.11−0.14)×20,000×1.04=1,62411.The annualized dividend yield on the S&P500Index is1.40%.The continuously compoundedinterest rate is6.4%.If the9-month forward price is$925.28and the index is priced at$950.46, what is the profit/loss from a cash-and-carry strategy?(a)$25.18loss(b)$25.18gain(c)$61.50loss(d)$61.50gainAnswer:C925.28−950.46×e(0.064−0.014)×.75=−61.5012.Consider an investment infive S&P500Index futures contracts at a price of$924.80.Theinitial margin requirement is15.0%and the maintenance margin is10.0%.If the continuously compounded interest rate is5.0%what will the futures price need to be for a margin call to occur 2weeks from now?Assume no settlement within the2weeks(52weeks for a year).(a)$852.64(b)$872.79(c)$878.29(d)$905.25Answer:C15%×924.80×e0.05/26+(F1,T−924.80)<924.80×10%F1,T<878.2913.Continuously compounding interest rates on the U.S.dollar are6.5%and euro rates are5.5%.The dollar per euro spot rate is0.950.What is the arbitrage profit on a required$1million Euro contract if the forward rate is0.980dollars per Euro and the exchange occurs in one year?(a)$10,000(b)$21,600(c)$28,000Answer:B,you can quicklyfind out which outcome is better1,000,000×0.980×e0.055−0.950×e0.065=21,600The question is only about profit.Ask yourself,the complete description of the strategy should be,borrow what currency,lend what else currency today,andfinally,long or short a forward contract?14.The annual risk free interest rate is4.0%.Today’s the spot price for corn is212cents/bushel,in12months the forward price is203cents/bushel.What is the approximate annualized lease rate on the12-month corn forward contract?(a)0.00%(b)2.25%(c)4.50%(d)8.34%Answer:Dδ=0.04−ln(203/212)15.What phrase might be used to describe the initial transaction a short seller initiates when shortingan equity security?(a)Buy(b)Sell(c)Borrow(d)CoveringAnswer:C16.A currency dealer has good credit and can borrow either$1,000,000or e800,000for one year.The one-year continuously compounding interest rate in the U.S.is i$=1.98%and in the euro zone the one-year continuously compounding interest rate is i e=5.83%.The one-year forward exchange rate is$1.20=e1.00.What must be the spot rate to eliminate arbitrage opportunities?(a)$1.2471=e1.00(b)$1.20=e1.00(c)$1.1547=e1.00(d)none of the aboveAnswer:A,e0.0198=1.02;e0.0583=1.061.2x0×1.06=1.02x0=1.21.02×1.06=1.247117.Corn call options with a$1.75strike price per bushel are trading for a$0.14premium.FarmerJayne decides to hedge her20,000bushels of corn by selling short call options.Six-month interest rates are4.0%and she plans to close her position in6months.What is the total premium she will earn on her short position in6months?(a)$2,800(b)$2,912(c)$800(d)$1,600Answer:B20000×0.14×1.04=291218.Suppose that the annual interest rate is4.88percent in the United States and3.44percent inGermany,and that the spot exchange rate is$1.12/e and the forward exchange rate,with one-year maturity,is$1.16/e.Assume that an arbitrager can borrow up to$1,000,000.If an astute traderfinds an arbitrage,what is the dollar profit in one year?(a)$10,690(b)$15,000(c)$46,207(d)$21,964.29Answer:De0.0488=1.05;e0.0344=1.035$21,964.29=−$1,000,000×(1.05)+$1,000,000×1.161.12×(1.035)19.Assume now U.S.dollar denominated interest rate is3.0%,and Yen denominated interest rate is4.0%.Today’s spot rate is1Yen equals0.01U.S.dollar.If you want to conduct carry trade,youshould borrow,lend today,and in the future.(a)Yen;U.S.dollar;short Yen(b)Yen;U.S.dollar;long Yen(c)U.S.dollar;Yen;short Yen(d)U.S.dollar;Yen;long YenAnswer:C20.When interest rate parity does not hold we should take(a)cash in advance(b)covered interest arbitrage(c)quasi arbitrage(d)fixed income arbitrageAnswer:B。