提升上市公司获利能力

上市公司盈利能力分析外文文献

The path-to-profitability of Internet IPO firms ☆Bharat A.Jain a,1,Narayanan Jayaraman b,2,Omesh Kini c,⁎aCollege of Business and Economics,Towson University,Towson,MD 21044,United States b College of Management,Georgia Institute of Technology,Atlanta,GA 30332,United Statesc Robinson College of Business,Georgia State University,Atlanta,GA 30303,United StatesReceived 1October 2006;received in revised form 1December 2006;accepted 1February 2007AbstractExtant empirical evidence indicates that the proportion of firms going public prior to achieving profitability has been increasing over time.This phenomenon is largely driven by an increase in the proportion of technology firms going public.Since there is considerable uncertainty regarding the long-term economic viability of these firms at the time of going public,identifying factors that influence their ability to attain key post-IPO milestones such as achieving profitability represents an important area of research.We employ a theoretical framework built around agency and signaling considerations to identify factors that influence the probability and timing of post-IPO profitability of Internet IPO firms.We estimate Cox Proportional Hazards models to test whether factors identified by our theoretical framework significantly impact the probability of post-IPO profitability as a function of time.We find that the probability of post-IPO profitability increases with pre-IPO investor demand and change in ownership at the IPO of the top officers and directors.On the other hand,the probability of post-IPO profitability decreases with the venture capital participation,proportion of outsiders on the board,and pre-market valuation uncertainty.©2007Published by Elsevier Inc.Keywords:Initial public offerings;Internet firms;Path-to-profitability;Hazard models;SurvivalJournal of Business Venturing xx (2007)xxx –xxxMODEL 1AJBV-05413;No of Pages 30☆We would like to thank Kalpana Narayanan,Raghavendra Rau,Sankaran Venkataraman (Editor),Phil Phan (Associate Editor),two anonymous referees,and participants at the 2002Financial Management Association Meetings in San Antonio for helpful comments.We thank Paul Gilson and Sandy Lai for excellent research assistance.The usual disclaimer applies.⁎Corresponding author.Tel.:+14046512656;fax:+14046522630.E-mail addresses:bjain@ (B.A.Jain),narayanan.jayaraman@ (N.Jayaraman),okini@ (O.Kini).1Tel.:+14107043542;fax:+14107043454.2Tel.:+14048944389;fax:+14048946030.0883-9026/$-see front matter ©2007Published by Elsevier Inc.doi:10.1016/j.jbusvent.2007.02.004Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Business2 B.A.Jain et al./Journal of Business Venturing xx(2007)xxx–xxx1.Executive summaryThere has been an increasing tendency for firms to go public on the basis of a promise of profitability rather than actual profitability.Further,this phenomenon is largely driven by the increase in the proportion of technology firms going public.The risk of post-IPO failure is particularly high for unprofitable firms as shifts in investor sentiment leading to negative market perceptions regarding their prospects or unfavorable financing environments could lead to a shutdown of external financing sources thereby imperiling firm survival. Therefore,the actual accomplishment of post-IPO profitability represents an important milestone in the company's evolution since it signals the long-term economic viability of the firm.While the extant research in entrepreneurship has focused on factors influencing the ability of entrepreneurial firms to attain important milestones prior to or at the time of going public,relatively little is known regarding the timing or ability of firms to achieve critical post-IPO milestones.In this study,we construct a theoretical framework anchored on agency and signaling theories to understand the impact of pre-IPO factors such as governance and ownership structure,management quality,institutional investor demand,and third party certification on firms'post-IPO path-to-profitability.We attempt to validate the testable implications arising from our theoretical framework using the Internet industry as our setting.Achieving post-issue profitability in a timely manner is of particular interest for Internet IPO firms since they are predominantly unprofitable at the time of going public and are typically characterized by high cash burn rates thereby raising questions regarding their long-term economic viability.Since there is a repeated tendency for high technology firms in various emerging sectors of the economy to go public in waves amid investor optimism followed by disappointing performance,insights gained from a study of factors that influence the path-to-profitability of Internet IPO firms will help increase our understanding of the development path and long-term economic viability of entrepreneurial firms in emerging, high technology industries.Using a sample of160Internet IPO firms that went public during the period1996–2000, we estimate Cox Proportional Hazards(CPH)models to analyze the economic significance of factors that influence the post-IPO path-to-profitability.Consistent with agency explanations,we find that a higher proportion of inside directors on the board and the change in pre-to-post-IPO ownership of top management are both significantly positively related to the probability of attaining post-IPO profitability.These results support arguments in the governance literature pointing to the beneficial impact of the presence of more insiders on the boards of high technology companies as well as the signaling value of the ownership stake of top management in the post-IPO firm.Additionally,we find evidence to indicate that higher institutional investor demand serves as an effective signal of the ability of Internet firms to attain post-IPO profitability,while greater pre-IPO valuation uncertainty reflects higher divergence of opinion about the future prospects of the IPO firm, and serves as a negative signal of the ability to achieve post-IPO profitability.Finally,we find that while underwriter prestige is unrelated to the probability of post-IPO profitability, VC participation decreases the probability of post-IPO profitability.Our results regarding the impact of VC participation on the probability of post-IPO profitability support arguments in the literature that VCs during the Internet boom period had incentives to grandstand by Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Businesstaking their companies public prematurely and that their monitoring role in the post-IPO period was rather limited since they cashed out earlier due to shorter lock-up periods.Our study makes several contributions.First,we construct a theoretical framework based on agency and signaling theories to identify factors that may influence the path-to-profitability of IPO firms.Second,we provide empirical evidence on the economic viability (path-to-profitability and firm survival)of newly public Internet firms.Third,our study adds to the theoretical and empirical literature that has focused on factors influencing the ability of entrepreneurial firms to achieve critical milestones during the transition from private to public ownership.While previous studies have focused on milestones during the private phase of firm development such as receipt of VC funding and completion of a public offering,our study extends this literature by focusing on a post-issue milestone such as attaining profitability.2.IntroductionThe past few decades have witnessed the formation and development of several vitally important technologically oriented emerging industries such as disk drive,biotechnology,and most recently the Internet industry.Entrepreneurial firms in such knowledge intensive industries are increasingly going public earlier in their life cycle while there is still a great deal of uncertainty and information asymmetry regarding their future prospects (Janey and Folta,2006).A natural consequence of the rapid transition from founding stage firms to public corporations is an increasing tendency for firms to go public on the basis of a promise of profitability rather than actual profitability.3Although sustained profitability is no longer a requirement for firms in order to go public,actual accomplishment of post-IPO profitability represents an important milestone in the firm's evolution since it reduces uncertainty regarding the long-term economic viability of the firm.In this paper,we focus on identifying observable factors at the time of going public that have the ability to influence the likelihood and timing of attaining post-IPO profitability by Internet firms.We restrict our study to the Internet industry since it represents a natural setting to study the long-term economic viability of an emerging industry where firms tend to go public when they are predominantly unprofitable and where there is considerably uncertainty and information asymmetry regarding their future prospects.4The attainment of post-IPO profitability assumes significance since the IPO event does not provide the same level of legitimizing differentiation that it did in the past as sustained profitability is no longer a prerequisite to go public particularly in periods where the market is favorably inclined towards investments rather than demonstration of profitability (Stuart et al.,1999;Janey and Folta,2006).During the Internet boom,investors readily accepted the mantra of “growth at all costs ”and enthusiastically bid up the post-IPO offering prices to irrational levels (Lange et al.,2001).In fact,investor focus on the promise of growth rather than profitability resulted in Internet start-ups being viewed differently from typical 3For example,Ritter and Welch (2002)report that the percentage of unprofitable firms going public rose form 19%in the 1980s to 37%during 1995–1998.4Schultz and Zaman (2001)report that only 8.72%of the Internet firms that went public during January 1999to March 2000were profitable in the quarter prior to the IPO.3B.A.Jain et al./Journal of Business Venturing xx (2007)xxx –xxx Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Business4 B.A.Jain et al./Journal of Business Venturing xx(2007)xxx–xxxnew ventures in that they were able to marshal substantial resources virtually independent of performance benchmarks(Mudambi and Treichel,2005).Since the Internet bubble burst in April2000,venture capital funds dried up and many firms that had successful IPOs went bankrupt or faced severe liquidity problems(Chang, 2004).Consequently,investors'attention shifted from their previously singular focus on growth prospects to the question of profitability with their new mantra being“path-to-profitability.”As such,market participants focused on not just whether the IPO firm would be able to achieve profitability but also“when”or“how soon.”IPO firms unable to credibly demonstrate a clear path-to-profitability were swiftly punished with steeply lower valuations and consequently faced significantly higher financing constraints.Since cash flow negative firms are not yet self sufficient and,therefore,dependent on external financing to continue to operate,the inability to raise additional capital results in a vicious cycle of events that can quickly lead to delisting and even bankruptcy.5Therefore,the actual attainment of post-IPO profitability represents an important milestone in the evolution of an IPO firm providing it with legitimacy and signaling its ability to remain economically viable through the ups and downs associated with changing capital market conditions.The theoretical framework supporting our analysis draws from signaling and agency theories as they relate to IPO firms.In our study,signaling theory provides the theoretical basis to evaluate the signaling impact of factors such as management quality,third party certification,institutional investor demand,and pre-IPO valuation uncertainty on the path-to-profitability.Similarly,agency theory provides the theoretical foundations to allow us to examine the impact of governance structure and change in top management ownership at the time of going public on the probability of achieving the post-IPO profitability milestone.Our empirical analysis is based on the hazard analysis methodology to identify the determinants of the probability of becoming profitable as a function of time for a sample of160Internet IPOs issued during the period1996–2000.Our study makes several contributions.First,we construct a theoretical framework based on agency and signaling theories to identify factors that may influence the path-to-profitability of IPO firms.Second,we provide empirical evidence on the economic viability of newly public firms(path-to-profitability and firm survival)in the Internet industry.Third, we add to the theoretical and empirical entrepreneurship literature that has focused on factors influencing the ability of entrepreneurial firms to achieve critical milestones during the transition from private to public ownership.While previous studies have focused on milestones during the private phase of firm development such as receipt of VC funding and successful completion of a public offering(Chang,2004;Dimov and Shepherd,2005; Beckman et al.,2007),our study extends this literature by focusing on post-IPO milestones. Finally,extant empirical evidence indicates that the phenomenon of young,early stage 5The case of E-Toys an Internet based toy retailer best illustrates this cyclical process.E-Toys was successful in developing an extensive customer base and a strong brand.However,the huge investment in technology, advertising,and promotion to sustain their activities as well as increased competition from both new entrants and old economy firms adopting the Internet to sell toys resulted in depressed profit margins and a longer than expected post-IPO time-to-profitability.Investors discouraged by the firm not reaching profitability within the expected time frame reacted negatively,leading to a steep drop in stock prices and consequently drying up of additional sources of external financing.As a result,the firm was forced to file for bankruptcy within a short period of time after its highly successful IPO.Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Businessfirms belonging to relatively new industries being taken public amid a wave of investor optimism fueled by the promise of growth rather than profitability tends to repeat itself over time.6However,profitability tends to remain elusive and takes much longer than anticipated which results in investor disillusionment and consequently high failure rate among firms in such sectors.7Therefore,our study is likely to provide useful lessons to investors when applying valuations to IPO firms when this phenomenon starts to repeat itself.This articles proceeds as follows.First,using agency and signaling theories,we develop our hypotheses.Second,we describe our sample selection procedures and present descriptive statistics.Third,we describe our research methods and present our results.Finally,we discuss our results and end the article with our concluding remarks.3.Theory and hypothesesSignaling models and agency theory have been extensively applied in the financial economics,management,and strategy literatures to analyze a wide range of economic phenomena that revolve around problems associated with information asymmetry,moral hazard,and adverse selection.Signaling theory in particular has been widely applied in the IPO market as a framework to analyze mechanisms that are potentially effective in resolving the adverse selection problem that arises as a result of information asymmetry between various market participants (Baron,1982;Rock,1986;Welch,1989).In this study,signaling theory provides the framework to evaluate the impact of pre-IPO factors such as management quality,third party certification,and institutional investor demand on the path-to-profitability of Internet IPO firms.The IPO market provides a particularly fertile setting to explore the consequences of separation of ownership and control and potential remedies for the resulting agency problems since the interests of pre-IPO and post-IPO shareholders can diverge.In the context of the IPO market,agency and signaling effects are also related to the extent that insider actions such as increasing the percentage of the firm sold at the IPO,percentage of management stock holdings liquidated at the IPO,or percentage of VC holdings liquidated at the IPO can accentuate agency problems with outside investors and,as a consequence,signal poor performance (Mudambi and Treichel,2005).We,therefore,apply agency theory to evaluate the impact of board structure and the change in pre-to-post IPO ownership of top management on the path-to-profitability of Internet IPO firms.ernance structureIn the context of IPO firms,there are at least two different agency problems (Mudambi and Treichel,2005).The first problem arises as a result of opportunistic behavior of agents to 6Interestingly,just a few years after the bust,technology companies have again started going public while they are still unprofitable (Lashinsky,2006).7For instance,in the biotechnology industry where the first company went public a quarter century ago,public companies have taken in close to $100billion dollars from stock market investors but have delivered cumulative losses of more than $40billion (Hamilton,2004).Similarly,the disk drive industry in the early 1980s passed through phases similar to the Internet industry in terms of high firm founding rates,explosive growth,overoptimistic investors,IPO clusters,and high post-IPO failure rate (Lerner,1995).5B.A.Jain et al./Journal of Business Venturing xx (2007)xxx –xxx Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Business6 B.A.Jain et al./Journal of Business Venturing xx(2007)xxx–xxxincrease their share of the wealth at the expense of principals.The introduction of effective monitoring and control systems can help mitigate or eliminate this type of behavior and its negative impact on post-issue performance.The extant corporate governance literature has argued that the effectiveness of monitoring and control functions depends to a large extent on the composition of the board of directors.We,therefore,examine the relationship between board composition and the likelihood and timing of post-IPO profitability.The second type of agency problem that arises in the IPO market is due to uncertainty regarding whether insiders seek to use the IPO as an exit mechanism to cash out or whether they use the IPO to raise capital to invest in positive NPV projects.The extent of insider selling their shares at the time of the IPO can provide an effective signal regarding which of the above two motivations is the likely reason for the IPO.We,therefore,examine the impact of the change in ownership of officers and directors around the IPO on the likelihood and timing of attaining post-issue profitability.3.1.1.Board compositionThe corporate governance literature has generally argued that a greater proportion of outside directors on the board increases board independence and results in better monitoring of management and thereby lowers agency costs(Fama,1980;Fama and Jensen,1983; Williamson,1984).Therefore,a greater proportion of outside directors on the board of Internet IPO firms is likely to lead to a more effective monitoring and control environment, thus ensuring that managers pursue shareholder value maximizing strategies.In addition, due to their short operating history,management of Internet IPO firms are unlikely to have developed the necessary links with customers,suppliers,bankers,and other important stakeholders of the firm.Outside directors can be instrumental in facilitating the establishment of such links,thereby allowing these firms to better compete in the product market as well as capital market.On the basis of the above discussion,we would expect Internet IPO firms with more independent boards to be on a faster path-to-profitability. Hypothesis1:The proportion of outsiders on the board of Internet IPO firms is positively related to the probability of profitability and negatively related to time-to-profitability during the post-IPO period.The extant empirical evidence on the positive relation between board composition and performance,however,has been mixed,both for IPO firms as well as more seasoned corporations(Dalton et al.,1998;Baker and Gompers,2003).The ambiguous results can be partly attributed to the tradeoff between the benefits from the presence of outside directors such as more effective monitoring and control,greater objectivity,and assistance in resource acquisitions versus the benefits provided by inside directors such as detailed knowledge of the firm's operations,customer requirements,and technology that in turn can help the strategic planning process.Viewed through the innovation and technology prism, high technology Internet IPO firms may actually benefit more from in-depth technological knowledge,expertise,commitment,and innovative thinking that insiders bring to the board,rather than from the monitoring and control benefits provided by outside directors.In support of this argument,Zahra(1996)points out that boards comprised of a higher proportion of insiders may be more innovative and better positioned to serve management Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Businessas knowledgeable sounding boards in the formulation of strategy.Further,since high technology Internet firms are unlikely to generate substantial free cash flows in the period immediately after the IPO,the potential for wasteful expenditure is lower,and therefore,the benefits of monitoring and control provided by outsiders is less likely to be substantive.If there is a greater need for creative thinking and decision-making in high technology knowledge-based industries that only insiders are uniquely qualified to provide,we expect a negative relation between the proportion of outsiders on the board and the probability of profitability and a positive relation with time-to-profitability.Hypothesis 1A:The proportion of outsiders on the board of Internet firms is negatively related to the probability of profitability and positively related to time-to-profitability during the post-IPO period.3.1.2.Ownership of officers and directorsCorporate governance studies have also focused extensively on corporate ownership and its impact on performance,both in isolation and in conjunction with board composition.Both agency and signaling theories provide similar predictions regarding the relationship between the extent of insider ownership and post-issue performance.Agency theory suggests that high insider ownership reduces agency conflicts and enhances organizational performance,while signaling theory argues that higher insider ownership is a credible signal of insider's confidence regarding the future prospects of the firm.The change in the ownership of the top managers and directors around the offering can be viewed as an important signal of the issuing firm's future prospects (Leland and Pyle,1977).In the context of the IPO market,a large post-IPO decline in top management ownership can be interpreted as a signal of their lack of confidence in the ability of the firm to generate sufficient cash flows to reach the profitability milestone.Additionally,any decline in the ownership stakes of owners/managers is likely to adversely affect post-IPO performance due to higher agency costs (Jensen and Meckling,1976).While the extent of the change in ownership of insiders around the IPO is an informative signal for all types of IPO firms,it is particularly relevant in the context of Internet firms that go public while predominantly unprofitable and where the informational and incentive problems are particularly acute.For instance,Mudambi and Treichel (2005)find that a substantial reduction in equity holdings of the top management of Internet firms signals an impending cash crisis.We,therefore,argue that the greater the decline in the pre-to-post IPO ownership of top managers and directors,the lower the probability of attaining profitability,and consequently the longer the time-to-profitability.Hypothesis 2:The decline in ownership of officers and directors from pre-to-post-IPO is negatively related to the probability of attaining profitability and positively related to time-to-profitability after the IPO.3.2.Management qualityAn extensive body of research has examined the impact of top management team (TMT)characteristics on firm outcomes for established firms as well as for new ventures by drawing from human capital and demography theories (Eisenhardt and Schoonhoven,7B.A.Jain et al./Journal of Business Venturing xx (2007)xxx –xxx Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Business8 B.A.Jain et al./Journal of Business Venturing xx(2007)xxx–xxx1990;Finkelstein and Hambrick,1990;Wiersema and Bantel,1992;Hambrick et al.,1996; Beckman et al.,2007).For instance,researchers drawing from human capital theories study the impact of characteristics such as type and amount of experience of TMTs on performance(Cooper et al.,1994;Gimeno et al.,1997;Burton et al.,2002;Baum and Silverman,2004).Additionally,Beckman et al.(2007)argue that demographic arguments are distinct from human capital arguments in that they examine team composition and diversity in addition to experience.The authors consequently examine the impact of characteristics such as background affiliation,composition,and turnover of TMT members on the likelihood of firms completing an IPO.Overall,researchers have generally found evidence to support arguments that human capital and demographic characteristics of TMT members influence firm outcomes.Drawing from signaling theory,we argue that the quality of the TMTof IPO firms can serve as a signal of the ability of a firm to attain post-IPO profitability.Since management quality is costly to acquire,signaling theory implies that by hiring higher quality management,high value firms can signal their superior prospects and separate themselves from low value firms with less capable managers.The beneficial impact of management quality in the IPO market includes the ability to attract more prestigious investment bankers,generate stronger institutional investor demand,raise capital more effectively,lower underwriting expenses, attract stronger analyst following,make better investment and financing decisions,and consequently influence the short and long-run post-IPO operating and stock performance (Chemmanur and Paeglis,2005).Thus,agency theory,in turn,would argue that higher quality management is more likely to earn their marginal productivity of labor and thus have a lower incentive to shirk,thereby also leading to more favorable post-IPO outcomes.8 We focus our analyses on the signaling impact of CEO and CFO quality on post-IPO performance.We focus on these two members of the TMT of IPO firms since they are particularly influential in establishing beneficial networks,providing legitimacy to the organization,and are instrumental in designing,communicating,and implementing the various strategic choices and standard operating procedures that are likely to influence post-IPO performance.3.2.1.CEO characteristicsCEOs play a major role in designing and implementing strategic choices and policies for their firms.Their actions can have long-term significance since they typically define long-term policies of the firm(Parrino,1997).While the role and influence of CEOs on strategic choices,incentive mechanisms,accountability issues,and consequently performance is vital for all types of organizations,their impact is especially relevant for newly public firms that face significant competitive,product market,and financing challenges during the post-IPO phase.The role and impact of CEOs can be even more critical for the subset of technology related IPO firms since they may require fundamentally different skill sets and competencies from CEOs compared to those required to run companies in more traditional industries.We assess CEO quality by focusing on variables that capture the extent of general and specific human capital developed by them through their prior work experience and their risk propensity and decision-making behavior.In distinguishing between general and specific8We thank the Associate Editor,Phil Phan for suggesting this explanation.Please cite this article as:Jain,B.A.et al.The path-to-profitability of Internet IPO firms.Journal of Business。

上市公司盈利参考文献

上市公司盈利参考文献1、急求经济类参考文献1] 简东平湖北财经高等专科学校学报 ,2001,(05) 上市公司盈利能力分析评价探讨[J] [3] 王富强,徐静珍财会月刊 ,2004,(23) 上市公司盈利能力分析研究[J] [5] 张涛黑龙江财会 ,2002,(03) 试析股份制企业盈利能力指标[J] [7] 李萍,肖惠民广东金融学院学报 ,2003,(05) 浅谈企业盈利能力的分析[J] [9] 王彤中国工程咨询 ,2003,(05) 影响企业盈利能力的因素分析[J]: Evidence on the Relationship between Construction and Profitability in Banking ,Journal of Money, Credit and Banking,vol[2] Prowse S: The structure of corporate ownership in Japan, Journal of Finance,1992 (3), 1121–1140 , Market structure And Performance in Spanish Banking Using a Direct Measure of Efficiency, Applied Financial Economics, 199 Slade: Competing models of firm profitability, International Journal ofIndustrial Organization,2004(22)[6]管军、李文华石家庄经济学院学报上市公司业绩评价体系初探[J]2002(13)[] 李晓荣,王宪良.因子分析在上市公司盈利能力分析中的应用[J].财经科学.2002年增刊[9]张晓明,何滢.我国旅行社绩效评价方法探索[J].西北大学学报(哲学社会科学版.2003(1)[10] 汤青.中国上市公司盈利能力影响因素实证分析[J].山东财政学院学报[J].2005(2)[11] 王燕.企业盈利能力的评价.中国优秀硕士学位论文全文数据库,2006[12] 张庆昌,傅再育.中国上市公司盈利能力模型分析[J].贵州财经学院学报.2006(1)[13]张瑞龙,陈艳艳.基于Excel 的企业盈利能力分析模型设计[J].中国管理息化.2007(1)[14] 莫生红,李明伟.上市公司盈利能力综合评价模型的构建[J].2007(1)本回答被网友采纳2、最近要写毕业论文商业银行的盈利能力分析不知道哪个银行的比较好写 ~ 还有去哪里比较好找数据。

种业上市公司财务绩效提升路径分析

波又一 波 的行情 , 与其 他 板 块 上 市公 司跌 幅 高 达 8% ~ 0

9% ̄ 比 , o N 农业上 市公 司尤其 以种业 上 市公 司为代 表 的股 价

迭创新高, 显示出较好的市场人气。究其原因可能是, 民以

食为 天 , 别 是伴 随着 可能 出现 全球 性通 货 膨胀 的大 背景 ; 特 此外 , 政策性支 持 、 国际农产 品价格 大涨 、 激励 和并购 等 股权

安徽农业科学 。ora o u A r e.08 3 (6 :5 3 Ju l f mhi gi i20 ,6 3 ) 185—186 n P .S 53

责任编辑

李玮

责任校对

吴晓燕

种 业 上市公 司 财务 绩效 提 升 路 径 分析

写仁林 (阴 范 院 济 理 ,苏 安23 ) 各 淮 师 学 经 管 系 江 淮 20 30

子 、 的培育 、 广和 销售 , 种苗 推 研究 水 平处 于 世界 前 列 , 牢 并 牢 掌握着核心 技术 。公 司在 杂 交水 稻 研究 及利 用 方 面处 于 世 界领 先地 位 , 系全 国最大 的杂 交水 稻种 子供 应基 地 , 水稻 种子 的市场 占有 率超 过 了 1% , 7 稳居 全 国首 位 , 并且 市 场 占 有率 有望上升 到 3%。另外 , 司同时还是亚 洲最大 的蔬菜 3 公

摘要 通 过对种 业上市公 司的偿债 能力 、 获利 能力和发展 能 力财务分析 , 发现种 业上 市公 司的基 本面较历 史 虽有较 大改观 , 还存 在偿 但 债风 险较 高、 获利 能力欠佳 等 I, 种 业上 市公 司要提 升公 司价值 必 须要将 公 司主 营与公 司战 略结 合 , 高技 术研 发优 势 , 强产 品 的 ' N, - - I ”“ 号 、春优 5” 8品种生 产经 营权 。“ 丰 两优香一号 ”“ 、丰两优 三 号” “ 和 丰两 优 四 号” 自有 知 识 产 等 权的新品种选 育成 功 , 司新 增 水稻 新 品种 5 、 公 个 玉米 品种 组 合 1 多个 , 别进入不 同生态 区域 的相关 省 份或 国家 , 0 分 进

浅析上市公司盈利能力分析指标

( 盈利能力的影响因素 一)

盈利 能力 反 映 的是 公 司获 取 利润 的 能力 , 于上 市 对

( ) 公 司盈利 能力 指标 的构 成 - A市 盈利能 力指 标可 以分 为相对 指标 和 绝对指 标 。而在 实践 中 , 财务 分析 往往 侧 重 于相 对指 标 的 分析 而 忽略 绝 对指标 在分 析运 用 中的决定 性作 用 。在相 对指 标分 析时

指标 , 对其他指标以及整个指标体系起着关键性作用。

映了公司管理者运营资产获取利润的能力和效率,反映 了所有资本( 债务资本和权益资本) 的回报情况, 而不受资 本构成的影响。该指标越高 , 表明资产利用的效率越高,

通 可 等) 分析外 , 还要借助一些与公 司股票价格或市场价值相 投资 盈利能力 越强 。 过对该 指标 的深 入分析 , 以了解 关 的指标 分 析 , : 东 权 益 报 酬率 ; 如 股 每股 收益 ; 股 股 公 司获利 能力 与投入 产 出状况 的关 系 ,增 强各方 面对企 每

影 响 因素 可 以概 括 为 : 司 营 销 能力 、 本 费 用 管理 水 公 成

二、 上市公 司盈利能 力指标 的分析与评价

( 以净 利 润为基 础 的盈利 能力 指标 一) 以净 利 润 为指 数 的指 标 是 评 价 盈 利 能力 最 基 础 的

平、 资产管理水平 、 风险管理水平。

司 的财 务状 况 。

(- -) _ A市公 司盈 利能 力指 标确 立 的一般 原则

盈利能力分析的内涵与目的

二、企业获利能力分析的内涵及目的(一)企业获利能力的内涵企业的获利能力又称为企业的盈利能力,是指企业在一定时期内赚取利润的能力。

这是个相对概念,即是相对于一定的投入和收入而言的。

利润率越高,盈利能力则越强;反之,亦然。

无论是企业的经理人员,债权人,还是股东,都十分关心企业的盈利能力,并重视对利润率及其变动趋势的预测与分析。

这只要是因为,盈利能力能够直接反应经营业绩的好坏。

(二)企业获利能力分析的目的企业从事经营活动,最直接的目的就是最大限度的获取利润以保证企业持续稳定的发展与经营;而企业持续稳定的发展与经营又是获取利润的基础。

由此可见,两者息息相关,互相联系。

因此,企业只有在不断获取利润的基础上,才有可能更好的发展;可见,盈利能力强的企业比盈利能力弱的企业具有更大的发展潜力和更好的发展前景。

对企业经理而言,进行企业盈利能力分析的目的具体表现在以下两个方面:⑴利用盈利能力的有关指标反映和衡量企业经营业绩。

企业经理的根本任务,是通过自己的努力使企业获取更多的利润。

各项指标间接反映着经理人员工作业绩的大小,因此,用已达到的获利能力标准与基期,同行平均水平的比较,则能够衡量经理的工作业绩。

⑵经营管理中存在的问题可以通过盈利能力的分析来找到。

盈利能力反映企业的各个经营环节,因此,企业的好坏与经营活动密切相关。

所以,管理者习惯通过根据对经营活动的分析结果来发现经营管理中所存在的问题,进而及时采取补救措施。

对债权人而言,利润指标是衡量债券的重要标准,特别是长期债。

盈利能力的水平会直接作用于的偿债能力:企业欠债过度时,债权人应该重点检查企业的偿债能力。

所以可见,从债权人的利益出发,对企业盈利能力的分析是必然的,也是尤为关键的。

对股东投资人而言,企业盈利能力的高低更是十分重要的。

在市场经济下,股东往往认为企业盈利能力的地位高于经营水平,财务情况。

获取更多更大的利润一直是股东极力追求的,这是因为,在同等水平的一些企业中,人们习惯于投资那些易获得利润,利润大风险小的企业;股东们的股息与企业的盈利能力是紧密相关的,因此,他们格外关心企业赚取利润能力即具体数量并重视利润率的分析结果;并且,股票的价格也会受到企业盈利能力的影响,企业获利能力的增强则会推动企业股价的上涨,由此,股东可以赚取资本收益。

上市公司几个重要指标的分析

上市公司是指公司股票在证券交易所公开流通的股份制企业。

由于上市公司的盈利能力对公司股价有重要影响,因此对上市公司盈利能力分析有一些特殊指标,主要包括:每股收益、每股红利、每股净资产、市盈率和市净率。

下面一一加以详细分析。

(1)每股收益。

每股收益是综合反映上市公司获利能力的重要指标,可以用来判断和评价管理部门的经营业绩。

每股收益所涵盖的信息,有助于对公司未来的股利政策和股价走势做出预测,从而做出“买——卖——持有”的决策。

因此,每股收益具有预测价值和决策有用性。

人们一般视其为公司能否成功地达到其利润目标的计量标志,也可以认为它是一家公司管理效率、盈利能力和股利分配来源的显示器。

对股东说来,利润是一个综合性的盈利概念,它反映了由债权人、优先股和普通股股东投入资源所形成的公司资产上的投资收益。

然而,债权人和除普通股以外的投资者在这块盈利中可以享有的部分只能是一笔固定的金额。

根据他们与公司的契约关系,公司债券与优先股股票通常都规定了利息率和股利率,而这些固定的投资收益正是投资这些有价证券的投资者所期望得到的。

但是,就普通股而言,剩余权益往往意味着盈利下降时,普通股首先会遭受损失,而当盈利上升时,则只能获得剩余收益。

因此,如果债权人和优先股的投资收益首先能够确定的话,每股收益便能比较恰当地说明收益的增长或减少。

因此该指标实际上是一种对普通股收益的描述,我们应当把所有优先证券如公司债券和优先股股票等所产生的投资收益,在公司的盈利中加以扣除,以便得到属于普通股股东的投资收益。

其中,债券持有者的利息早就作为一项费用在确定利润时扣除,所以,接着需要调整的是,将属于优先股的股利从税后利润中减去,以便确定属于普通股股东的盈余部分。

由此,每股收益的计算公式确切表示为:每股收益=(税后利润-优先股股利)/发行在外的普通股股数在分析每股收益指标时,应注意公司利用回购库存股的方式减少发行在外的普通股股数,使每股收益简单增加。

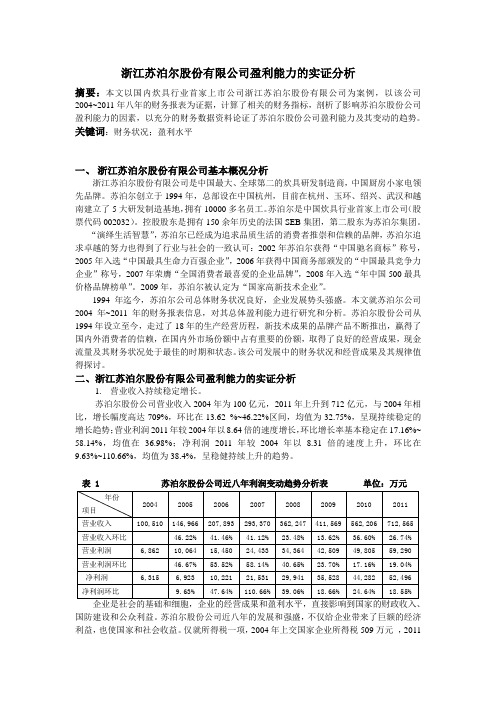

浙江苏泊尔股份有限公司盈利能力的实证分析

浙江苏泊尔股份有限公司盈利能力的实证分析摘要:本文以国内炊具行业首家上市公司浙江苏泊尔股份有限公司为案例,以该公司2004~2011年八年的财务报表为证据,计算了相关的财务指标,剖析了影响苏泊尔股份公司盈利能力的因素,以充分的财务数据资料论证了苏泊尔股份公司盈利能力及其变动的趋势。

关键词:财务状况;盈利水平一、浙江苏泊尔股份有限公司基本概况分析浙江苏泊尔股份有限公司是中国最大、全球第二的炊具研发制造商,中国厨房小家电领先品牌。

苏泊尔创立于1994年,总部设在中国杭州,目前在杭州、玉环、绍兴、武汉和越南建立了5大研发制造基地,拥有10000多名员工。

苏泊尔是中国炊具行业首家上市公司(股票代码002032)。

控股股东是拥有150余年历史的法国SEB集团,第二股东为苏泊尔集团。

“演绎生活智慧”,苏泊尔已经成为追求品质生活的消费者推崇和信赖的品牌,苏泊尔追求卓越的努力也得到了行业与社会的一致认可:2002年苏泊尔获得“中国驰名商标”称号,2005年入选“中国最具生命力百强企业”,2006年获得中国商务部颁发的“中国最具竞争力企业”称号,2007年荣膺“全国消费者最喜爱的企业品牌”,2008年入选“年中国500最具价格品牌榜单”。

2009年,苏泊尔被认定为“国家高新技术企业”。

1994年迄今,苏泊尔公司总体财务状况良好,企业发展势头强盛。

本文就苏泊尔公司2004年~2011年的财务报表信息,对其总体盈利能力进行研究和分析。

苏泊尔股份公司从1994年设立至今,走过了18年的生产经营历程,新技术成果的品牌产品不断推出,赢得了国内外消费者的信赖,在国内外市场份额中占有重要的份额,取得了良好的经营成果,现金流量及其财务状况处于最佳的时期和状态。

该公司发展中的财务状况和经营成果及其规律值得探讨。

二、浙江苏泊尔股份有限公司盈利能力的实证分析1.营业收入持续稳定增长。

苏泊尔股份公司营业收入2004年为100亿元,2011年上升到712亿元,与2004年相比,增长幅度高达709%,环比在13.62 %~46.22%区间,均值为32.75%,呈现持续稳定的增长趋势;营业利润2011年较2004年以8.64倍的速度增长,环比增长率基本稳定在17.16%~ 58.14%,均值在36.98%;净利润2011年较2004年以8.31倍的速度上升,环比在9.63%~110.66%,均值为38.4%,呈稳健持续上升的趋势。

盈利获利能力分析

2010年 2009年

利润总额

115.1272.47Fra bibliotek利息支出

6.54

2.3

平均资产

846.89

667.81

总资产报酬率 14.37%

11.20%

第四节 投资盈利(获利)能力分析

• 投资盈利(获利)能力分析的主要指标 包括:净资产收益率、资本保值增值率;

• 每股收益、市盈率、每股净资产、市净 率、股利支付率等。

单位:百万元 项目

净利润 营业收入 销售净利率(%)

顺络电子销售净利率计算表

2010年 95.84

449.15 21.34

2009年 61.45

326.01 18.85

2、销售净利率的影响因素及评价方法

影响因素:

◆ 营业收入和净利润 营业成本、营业税金及附加、三项期 间费用、资产减值损失、公允价值变动 损益、投资收益及所得税。

二、资本保值增值率

期末所有者权益总额 • 资本保值增值率=期初所有者权益总额 ×100%

项目 期末所有者权益

期初所有者权益

资本保值增值率

项目 期末所有者权

益 期初所有者权

益 资本保值增值

率

2010 410.23 343.43 119.45%

2009 343.43 313.48 109.55%

2010 637.71 524.13 121.67%

与同行业比较,如果公司的毛利率显著高于 同业水平,说明公司产品附加值高,产品定价高, 或与同行比较公司存在成本上的优势,有竞争力。

与历史数值比较,如果公司的毛利率显著提 高,则可能是公司所在行业处于复苏时期,产品价 格大幅上升,在这种情况下分析者需考虑这种价格 的上升是否能持续,公司将来的盈利能力是否有保 证。相反,如果公司毛利率显著降低,则可能是公 司所在行业竞争激烈。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

提升上市公司获利能力

提要企业获利能力是指企业利用各种经济资源赚取利润的能力。

上市公司获利能力是反映上市公司价值的一个重要方面。

提升上市公司获利能力与股东报酬的高低、债权人的安全程度以及公司的健康发展密切相关。

本文从提升上市公司获利能力的现状出发,揭示存在的问题,最后通过提出有效措施来进一步提高上市公司获利能力。

一、上市公司获利能力现状

近年来,上市公司获利能力虽有了一定的提高,但是仍然存在一些问题。

主要问题有:

(一)内部会计控制制度不完善

1、资金管理混乱。

在当今市场经济条件下,上市公司资金流量在一定程度上决定一个企业的生存和发展,如果上市公司资金流量不足、周转不通,将会影响企业的生存和发展,进而影响企业的盈利能力。

在我国,由于商业信用大量存在,而且商业信用欠佳已成为普遍现象。

如,有的企业获利能力很好,由于存在大量不能收回的应收账款,致使现金已经严重紧缺,影响公司正常周转,甚至出现破产现象。

2、主营业务收入所占比重日益降低。

近年来,有些上市公司盈利能力是靠营业外收入、补贴收入来维持的,主营业务收入反而占很少比例。

营业外收入是公司在正常经营活动之外形成的收入,其发生带有偶然性,它与赢利能力无关,如果比重过高,势必影响上市公司的获利能力质量。

3、成本管理制度不健全。

4、费用开支过大。

(二)法人治理机构不完善。

上市公司法人治理结构存在的主要问题为:

1、法人治理结构中角色的责、权、利严重不对称。

决策机构与经营管理机构之间,甚至经营管理机构与执行机构之间,部门重叠、职能混淆、职责不清,导致企业内部目标不明确、分工不协作,企业难以有效运转,同时部门间监督不力,权力制衡机制难以形成。

2、企业管理机制不健全。

对公司经营者缺乏有效的激励机制,难以保障公

司经营者与企业利益的一致性,当企业经营者利益与企业不一致时,难以保证公司利益的最大化。

(三)管理人员、财务人员等相关人员素质不高。

一些上市公司获利能力不高,在很大程度上是因为一些管理人员、财务人员不顾公司实际情况,目光短浅,为了短期利益而牺牲长期利益,结果致使公司利益受到损害。

二、提升上市公司获利能力的措施

(一)加强内部控制制度

1、加强资金管理。

①资金的预算管理。

在新一年开始时,财务部门应编制资金的预算。

通过编制企业年度资金预算计划,能够明确企业年度资金运作的重点,便于公司日常的资金控制,把握资金周转情况,节约公司融资成本,避免盲目贷款和不合理存款等情况的发生。

②资金的风险管理。

公司资金风险主要有使用风险、在途风险和或有风险。

资金的使用风险主要表现为企业的投资风险,它是一种事先可控制的风险,所以对这类风险应加强事先控制。

加强对投资项目的可行性调查论证,项目评审做到科学化、专业化,尽量把预计风险发生的概率控制在最低程度。

资金的或有风险主要是公司为其他企业提供担保而形成的或有负债,每个董事都应慎重对待和严格控制对外担保产生的债务风险,并对违规或失当的对外担保产生的损失依法承担连带责任。

③资金的日常管理。

资金的日常管理主要指资金使用过程中的审批管理、报表管理和跟踪管理。

企业资金审批程序制定应遵循“便捷、高效、控制”的原则,预先设定相应的资金审批程序和权限。

一般上市公司的重大投资、大额银行贷款应由董事会审批;一般固定资产、低值易耗购置、小额贷款等应由总经理审批;大额的合同履约和货款支付应由总经理审批;一般资金使用由财务总监审批。

企业应定期、不定期地对资金使用情况进行检查,既通过日常的报表了解全面情况,又通过专项检查发现资金预算执行过程中的深层次问题,特别是应收账款、预付账款、其他应收款等往来账目应逐笔实行跟踪管理。

2、加强收入管理。

公司的收入主要有主营业务收入、其他业务收入、投资收益、营业外收入及补贴收入五项,管理的重点应该是前三项,特别是主营业务收入。

在日益竞争激烈的市场中,上市公司要提高主营业务收入必须具有不断创新的能力。

3、加强成本管理。

①实行实际成本核算。

直接采用市场价格进行成本核算,改变传统的以内部计划价格加成本差异为依据的核算制度,实现企业内部与动态价值相对应的价值转移。

②对目标成本加以控制。

以整体效益最优化为原则建立目标成本控制体系,一切经济活动的开展以达到目标为目的,并且制定科学的目标计划。

③加强责任成本管理。

根据责任量化、责任相关、责任可控、指标优化、

专业管理与群众管理相结合的原则,贯彻“以人为本”的管理思想,建立一个由成本责任组织体系、指标体系、考核体系和信息反馈体系构成的有机整体,把目标成本指标层层分解落实。

④推行成本差异化管理理念,实施品牌战略。

依据市场和公司发展的需要,全面实施品牌战略,充分发挥技术创新的优势,跳出低成本、低档次产品激烈竞争的圈子,实现成本差异化和投入产出最大化,不断开发技术含量高的产品,最大限度地提高企业竞争力和经济效益。

4、控制费用开支。

公司的经营费用、管理费用、财务费用三项开支在成本中占有一定的比例,控制这部分费用管理,能提高效益,提高竞争力。

①对公司费用实行预算管理。

在制定预算时,必须分清不变费用和可变费用。

预算一经制定,便不可随意修改。

如果经营量没有较大变化,费用预算一般不宜调整。

并将预算按部门、按月、按季进行分解,做到按月检查,按季考核,节约的奖励,超额的处罚。

②在费用控制上,必须实行一个人审批。

③在费用开支上,尽量实行收支两条线管理。

(二)健全法人治理结构

1、实行内部共同治理和外部适当监督相结合的管理体制。

公司作为营利性组织,其目标既要追求公司利益最大化,也要追求股东利益最大化,还要为利益相关者着想。

所以,在设计公司治理结构时,董事会和监事会中要有股东以外的利益相关者代表,如债权银行代表、私人股东等作为企业经营者的监督人,增强股东对公司和公司机构的监督力度,克服企业监督失灵的问题;可以根据公司法的规定增设外部董事,以弥补内部董事和监事专业知识、监督立场上的局限,提高董事会和监事会的管理水平,提高经理层的管理水平。

2、不断完善激励机制。

上市公司的目标考核为动态目标,所以激励机制也应该从短期激励转向长期激励。

通过股权激励机制可以与股东的利益结合起来,建立有效的管理层激励约束机制,从而降低代理成本。

此外,还可以通过EV A (经济增加值)红利银行把公司每期赚取的EV A的一定比例作为红利奖励给管理人员,但这部分红利首先应存入红利银行。

当EV A为正时,它会增加红利银行的账面余额;EV A为负时,抵减以前所取得的红利。

通过这种激励机制实现了所有者和经营者两者的利益一致性。

(三)提高管理人员、财务人员等相关人员素质。

能否提升上市公司获利能力,管理人员、财务人员等相关人员起着关键的作用,除了对其本身必须具备良好的思想品德和职业道德外,还必须有较高的分析能力和业务素质以及专业技能、较广博的知识水平。

此外,还必须有团队精神,能和各个部门人员进行沟通,及时发现公司可能出现的问题,并采取适当的措施解决问题,从而避免公司出现不必要的损失,以达到提升上市公司获利能力的目的。