Chapter1-Introduction to Accounting

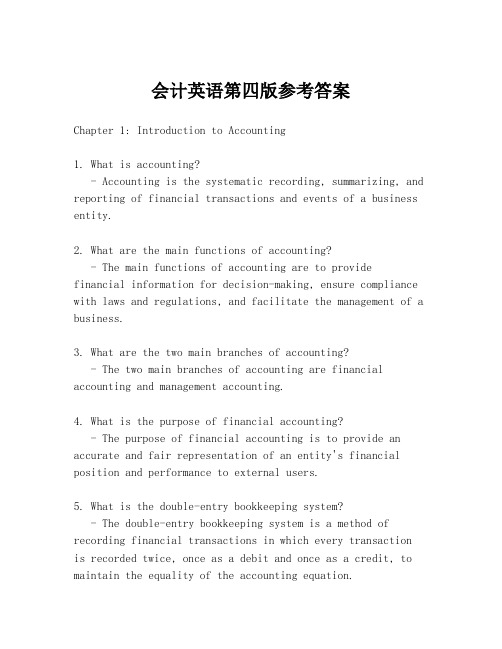

会计英语第四版参考答案

会计英语第四版参考答案Chapter 1: Introduction to Accounting1. What is accounting?- Accounting is the systematic recording, summarizing, and reporting of financial transactions and events of a business entity.2. What are the main functions of accounting?- The main functions of accounting are to providefinancial information for decision-making, ensure compliance with laws and regulations, and facilitate the management of a business.3. What are the two main branches of accounting?- The two main branches of accounting are financial accounting and management accounting.4. What is the purpose of financial accounting?- The purpose of financial accounting is to provide an accurate and fair representation of an entity's financial position and performance to external users.5. What is the double-entry bookkeeping system?- The double-entry bookkeeping system is a method of recording financial transactions in which every transactionis recorded twice, once as a debit and once as a credit, to maintain the equality of the accounting equation.Chapter 2: Accounting Concepts and Principles1. What are the fundamental accounting concepts?- The fundamental accounting concepts include the accrual basis of accounting, going concern, consistency, and materiality.2. What is the accrual basis of accounting?- The accrual basis of accounting records transactions when they occur, regardless of when cash is received or paid.3. What is the going concern assumption?- The going concern assumption is the premise that a business will continue to operate for the foreseeable future.4. What is the principle of consistency?- The principle of consistency requires that an entity should apply accounting policies consistently over time.5. What is the principle of materiality?- The principle of materiality states that only items that could potentially affect the decisions of users of financial statements are included in the financial statements.Chapter 3: The Accounting Equation and Financial Statements1. What is the accounting equation?- The accounting equation is Assets = Liabilities +Owner's Equity.2. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, statement of changes in equity, and cashflow statement.3. What is the purpose of the balance sheet?- The balance sheet provides a snapshot of an entity's financial position at a specific point in time.4. What is the purpose of the income statement?- The income statement reports the revenues, expenses, and net income of an entity over a period of time.5. What is the purpose of the cash flow statement?- The cash flow statement reports the cash inflows and outflows of an entity over a period of time.Chapter 4: Recording Transactions1. What is a journal entry?- A journal entry is the initial recording of atransaction in the general journal.2. What are the steps in the accounting cycle?- The steps in the accounting cycle are analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries.3. What is the difference between a debit and a credit?- A debit is an increase in assets or a decrease inliabilities or equity, while a credit is an increase in liabilities or equity or a decrease in assets.4. What are adjusting entries?- Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are recorded in the correct period.5. What is the purpose of closing entries?- Closing entries are made to transfer the balances of temporary accounts to the owner's equity account and to prepare the accounts for the next accounting period.Chapter 5: Accounting for Merchandising Businesses1. What is a merchandise inventory?- A merchandise inventory is the stock of goods held by a business for sale to customers.2. What is the cost of goods sold?- The cost of goods sold is the direct cost of producing the merchandise sold during an accounting period.3. What is the gross profit?- The gross profit is the difference between the sales revenue and the cost of goods sold.4. What is the difference between a perpetual and a periodic inventory system?- A perpetual inventory system updates inventory records in real-time with each sale or purchase, while a periodicinventory system updates inventory records at specific intervals, such as at the end of an accounting period.5. What is the retail method of inventory pricing?- The retail method of inventory pricing is a method of estimating the cost of ending inventory by applying a cost-to-retail ratio to the retail value of the inventory.Chapter 6: Accounting for Service Businesses1. What are the main differences in accounting for service businesses compared to merchandise businesses?- Service businesses do not have inventory and their primary expenses are typically labor and overhead costs.2. What is the main source of revenue for service businesses? - The main source of revenue for service businesses is the fees charged for the services provided.3. What are the typical expenses。

Unit 1 Introduction of accounting_PPT课件

Classifying and summarizing(分类汇总 )

classifying in order to be most useful to the entity to be summarized for interested parties' use.

Definition of accounting 会计的概念

Definition of accounting 会计的概念

Recording (记录)

up-to-date information, record as transactions occur not only cash in or out, but also goods in or out, and

Analyzing and interpreting (分析解析) analysing data, prepare financial

statement to examine and evaluate all information to make key decision.

Other functions: forecasting and planning for future operation of the business —— "budget".

Accounting equation 会计等式

Asset = liability + owner’s equity 资产=负债+所有者权益

Assets – Liabilities = Net assets 资产 – 负债 = 净资产

Pg.35 Statement of financial position (Balance Sheet) 资产负债表

Introduction to Financial Accounting Chapter 1

Operating activities

Involves transactions in primary operations of business

1-5

Basic Accounting Equation

Company’s resources

Claims to those resources

Investors and Creditors would like to know about

Operating cash flows

Investing cash flows

Financing cash flows

1-16

Statement of Cash Flows for Eagle Golf Academy

EAGLE GOLF ACADEMY Statement of Cash Flows For the month ended January 31 Cash Flows from Operating Activities Cash inflows: From customers $4,200 Cash outflows: For salaries (2800) For rent (6000) Net cash flows from operating activities Cash Flows from Investing Activities Purchase equipment (24000) Net cash flows from investing activities Cash Flows from Financing Activities Issue common stock 25,000 Borrow from bank 10,000 Pay dividends (200) Net cash flows from financing activities Net increase in cash Cash at the beginning of the month Cash at the end of the month

chap01Introduction to Accounting

Accounting defined

Accounting is an information system that identifies, measures, records and communicates relevant, reliable, consistent and comparable information about an organization‟s economic activities.

财会专业英语

CH01 Introduction to Accounting

CH01 Introduction to Accounting

1. Bookkeeping and accounting

2. The field of professional accounting

3. Accounting concepts and principles

Economic Decisions

Various factors must be considered when making economic decisions:

financial aspects

personal taste

social factors

environmental factors

Financial and Management Accounting

Accounting‟s role of assisting decision makers by measuring, processing, and communicating financial information is usually divided into the categories of management accounting and financial accounting. Although the functions of management accounting and financial accounting overlap部分重叠 , the two can be distinguished by the principal users of the information they provide.

《会计专业英语》Chapter 1 Introduction to Accounting

▪ 1.1 What is accounting ▪ 1.2 Forms of business entities ▪ 1.3 Business activities ▪ 1.4 Users of accounting information ▪ 1.5 Types of accounting ▪ 1.6 Careers in accounting

12

Internal users

➢ Internal users are employees of an enterprise and are directly involved in managing and operating the business.

➢ From basic labor categories to chief executive officers, all employees are paid, and their paychecks are generated by the accounting information system.

➢ Resources owned by a business are called capital assets. ➢ Assets have different types and names. Various, non-current,

and tangible assets are called property, plant, and equipment (PPE).

9

Investing activity

➢ Investing activities involve the purchase of the resources a company needs in order to operate.

会计英语 翻译chapter1

Chapter one Introduction to Accounting 1.1 Bookkeeping and AccountingAccounting is an information system that identifies,measures,records and communicates relevant,reliable,consistent,and comparable information about an organization’s economic activity. Its objective is to help people make better decisions.An understanding of the principles of bookkeeping and accounting is essential for anyone who is interested in a successful career in business. The purpose of bookkeeping and accounting is to provide information concerning the financial affairs of a business. Owners, managers, creditors, and governmental agencies need this information.An individual who earns living by recording the financial activities of business is known as a bookkeeper, while the process of classifying and summarizing business transactions and interpreting their effects is accomplished by an accountant. Accountant is the individual who understands the accounting principles, theoretical and practical application, and can manage, analyze, and interpret the accounting records. The bookkeeper is concerned with techniques involving the recording of transactions, and the accountant’s objective is the use of data for interpretation.第一章['tʃæptə]会计导论[.intrə'dʌkʃən]1.1 簿记与会计会计是一个信息系统,[ai'dentəfai]辨别、['meʒəz]测量、记录和交流相关的['reləvənt]、可靠的[ri'laiəbl]、持续的[kən'sistənt]和可比的['kɔmpərəbl]一个组织经济活动的信息。

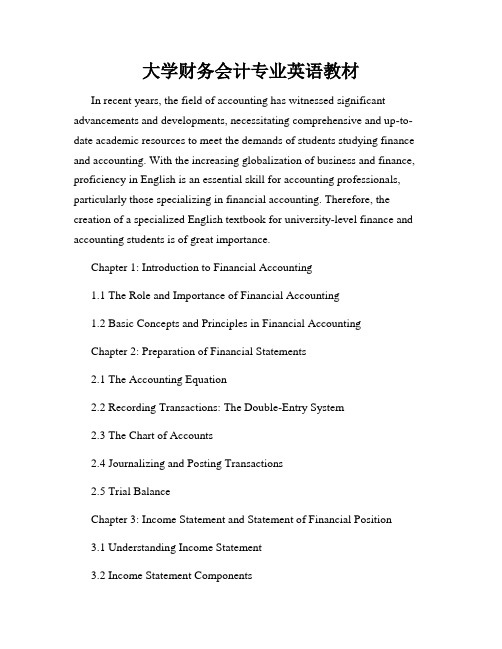

大学财务会计专业英语教材

大学财务会计专业英语教材In recent years, the field of accounting has witnessed significant advancements and developments, necessitating comprehensive and up-to-date academic resources to meet the demands of students studying finance and accounting. With the increasing globalization of business and finance, proficiency in English is an essential skill for accounting professionals, particularly those specializing in financial accounting. Therefore, the creation of a specialized English textbook for university-level finance and accounting students is of great importance.Chapter 1: Introduction to Financial Accounting1.1 The Role and Importance of Financial Accounting1.2 Basic Concepts and Principles in Financial AccountingChapter 2: Preparation of Financial Statements2.1 The Accounting Equation2.2 Recording Transactions: The Double-Entry System2.3 The Chart of Accounts2.4 Journalizing and Posting Transactions2.5 Trial BalanceChapter 3: Income Statement and Statement of Financial Position3.1 Understanding Income Statement3.2 Income Statement Components3.3 Statement of Financial Position: Assets, Liabilities, and EquityChapter 4: Revenue Recognition and Measurement4.1 Revenue Recognition Principles4.2 Measurement of Revenue: Sales, Services, and Other IncomeChapter 5: Expense Recognition and Measurement5.1 Expense Recognition Principles5.2 Measurement of Expenses: Cost of Goods Sold, Operating Expenses, and OthersChapter 6: Cash Flow Statements6.1 Importance and Purpose of Cash Flow Statements6.2 Operating, Investing, and Financing Activities6.3 Preparing a Cash Flow StatementChapter 7: Analysis and Interpretation of Financial Statements7.1 Financial Ratios and Metrics7.2 Horizontal and Vertical Analysis7.3 Limitations and Adjustments in Financial StatementsChapter 8: International Financial Reporting Standards (IFRS)8.1 Overview of IFRS8.2 IFRS Framework and Key Concepts8.3 Differences between IFRS and Generally Accepted Accounting Principles (GAAP)Chapter 9: Corporate Financial Reporting9.1 Financial Reporting for Corporations9.2 Disclosure Requirements and Auditors’ Opinions9.3 Regulatory Framework for Corporate Financial ReportingChapter 10: Accounting for Business Combinations10.1 Mergers and Acquisitions10.2 Consolidation Methods and Procedures10.3 Accounting for Non-controlling InterestsChapter 11: Financial Statement Analysis and Valuation11.1 Valuation of Assets and Liabilities11.2 Valuation Techniques: Cost Approach, Market Approach, and Income Approach11.3 Interpreting Financial Statement Analysis for Investment and Decision MakingBy providing a systematic overview of the principles, concepts, and techniques in financial accounting, this specialized English textbook addresses the needs of university students studying finance and accounting. It equips them with the necessary knowledge and skills to understand and apply financial accounting practices in an international context. With itscomprehensive content and clear explanations, this textbook serves as an indispensable resource for students pursuing a career in finance and accounting.。

1.2_introduction to accounting会计入门ppt课件

ChapterБайду номын сангаас1 第一章

An introduction to accounting 会计入门

ppt课件

1

Learning Objectives / Outcomes 学习目 标/成果

1. Define accounting, describe the accounting process and define the diverse roles of accountants 定义会计 学,描述会计过程并定义会计师的不同角色

6. Describe the financial reporting environment 描述财 务报表环境

7. Explain the accounting concepts, principles, qualitative characteristics and constraints underlying financial statements 说明会计概念,原理, 质量特征和财务报表的潜在约束条件

transactions 分

考虑所有影响

析、记录、分

营业单位的业

类并总结业务

务 Commonly referred to as

‘bookkeeping’ 通常称ppt为课件记账

Communication 交流

Preparing accounting

reports, analysing and interpreting准 备会计报表, 分析并说明

• Economic activities/transactions

e.g. - sale of item to customer 物品出售给客户 - purchase of office stationery from supplier 从供应商购买办公文具

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

CHAPTER 1 INTRODUCTION TO ACCOUNTING

1 WHAT IS ACCOUNTING?

◎Recording the transactions of a business to provide information for day-to day management ◎Summarizing the transactions of a period to provide information about business’s performance and position to interested parties. ◎Two important summary statements are prodeced.

5 THE INCOME STATEMENT

Definition: a summary of income and expenditure over a period time. -If income exceeds expenditure there is a profit. -If expenditure exceeds income there is a loss. Function: to show the amount of profit or loss made in an accounting period, i.e.a period time

Function: to record the assets owned by the enterprise and the liabilities owed by the business at a particular point in time. It satisfies the stewardship needs of users rather than their decision-making needs. For example, if they are creditors, the balance sheet shows the assets which are available to pay off their debts. There are other financial statement ,e.g. cash flow statement. A cash flow statement provides information about cash receipts and cash payments during accounting period.

-

2 BUSINESS ENTITIES Sole trader -the businesses owned and operated

by one person with or without employees. The sole trade is fully liable for the business’sdebts to the full extent of his or her personal as well as business assets.

-

The income statement shows the profit or loss made by the business in a period. This is called the profit and loss account in some countries. The balance sheet shows the position of the business at the end of the period covered by the income statement.It shows all the assets and liabilities of the business.

3 USERS OF FINANCIAL STATEMENTS

The purpose of accounting is to provide information to users of financial statements. Users of accounts Information needs Managers analyzed revenues and express, to provide information for when plans are formulated and decisions made;actual figure,to be compared wih what was budgeted;cost consequences of a particular course of action,to aid decisionmaking

Partnership –several people jointly own and run the business.Again there is no seperation between the assets and liabilities of the business and thosnts Information needs Shareholders and how managements have used their funds potential how the enterprise is likely to perform in shareholders the future,to help decide how they should vote on proposals or whether to disinvest. Financial analysts complex information on the company so as to advise investors such as insurance companies, pension funds,unit trusts and investment rusts, and a company contemplating a take-over bid Employees and how the enterprise(as a whole and in its Their trade union parts)is performing and will how secure representatives jobs are and at what rate they should be paid

The public

4 THE BALANCE SHEET Definition: a statement of assets and liabilities, and the company’s capital, at a point in time (the balance sheet date). --Assets are any tangible or intangible possession which has value. --Liabilities are the financial obligations of an enterprise, e.g. to suppliers, and, in the case of a bank loan or overdraft, to a bank --The capital of a business entity is a special liability of the business. It is the amount that the business owners back to the over of the business.

Users of accounts Lenders (including bankers with overdrafts and suppliers on credit) Government agencies Customers and competitors

Information needs How secure a loan is , in terms of both interest payments and ultimate repayment of the capital

6 FINANCIAL ACCOUNTING, MANAGEMENT ACCOUNTING AND FINANCIAL MANAGEMENT Financial accounting is mainly concerned with accounting to users outside the enterprise for the way in which the business’s funds have been used. This is done by pressing a balance sheet and income at least once every year. Management accounting is an integral part of management activity inside the enterprise, concerned with identifying. pressing and interpreting detailed information used for: ----Formulation of strategy ----Planning and controlling activities ----Decision taking ----Optimizing the use of resources.

Company –shareholders or members put in a

share of the total money needed to operate the business. They often do not participate in the management, but appoint directors to run the company on their behalf. In limited companies the shareholders' possible liability for the company debts is limited to the amount paid for their shares, as the company is a completely separate legal entity. The money put up by the individual, the partners or the shareholders is the business capital. Financial statements of sole traders and partnerships are private. Financial statements of companies are sent to shareholders and may also be publicly viewed.