布兰查德《宏观经济学》章节课后习题详解(货币政策:一个总结)【圣才出品】

布兰查德《宏观经济学》章节课后习题详解(预期:基本工具)【圣才出品】

第14章预期:基本工具一、概念题1.名义利率(nominal interest rates)答:名义利率又称“货币利率”,是包含了对通货膨胀风险补偿的利率。

与“实际利率”相对而言,是包括了物价变动的利息率,表现为银行挂牌执行的存款、贷款的利率。

现实的经济生活中物价水平具有不稳定性,并且物价水平的上涨是一种普遍的趋势。

划分名义利率和实际利率的理论意义在于其提供了分析通货膨胀条件下利率变动的工具。

在经济管理中,能操作的是名义利率,但对经济关系产生实质影响的是实际利率。

名义利率近似值的计算公式为:i=π+r。

其中,i为名义利率,r为实际利率,π为借贷期内物价的变动率(通货膨胀率)。

由于通货膨胀还会使利息部分贬值,名义利率还应作向上的调整。

这样,名义利率的计算公式可以写成:i=(1+π)(1+P)-1。

名义利率随通货膨胀的变化而变化并非同步的。

由于人们对价格变化的预期往往滞后于通货膨胀的变化,所以相对于通货膨胀率的变化,名义利率的变化也往往有滞后的特点,但也不是绝对的。

2.实际利率(real interest rates)答:实际利率,与“名义利率”相对而言,是指名义利率扣除通货膨胀因素后的利率。

实际利率为正值时,有利于吸收储蓄、降低通货膨胀率;实际利率为负值时,则会减少储蓄、刺激金融投机、恶化通货膨胀。

其计算公式为:1-=+名义利率通货膨胀率实际利率通货膨胀率当通货膨胀率很低时,可近似记为:实际利率=名义利率-通货膨胀率。

3.通货紧缩陷阱(deflation trap )答:通货紧缩陷阱是指较低的经济活动水平使经济陷入通货紧缩后,由于与产出下降,实际利率升高将导致投资和消费下降,从而导致产出进一步下降,经济陷入通货紧缩的恶性循环之中的现象。

4.自然利率(natural interest rate )答:自然利率是指假设所有价格具有充分弹性,令总需求与总供给永远相等时的利率水平,即与产出的自然水平相对应的利率值。

布兰查德《宏观经济学》课后习题及详解(汇率制度)【圣才出品】

第21章汇率制度一、概念题1.金本位(gold standard)答:金本位是“国际金本位制”的简称,是指以黄金作为本位货币的一种货币制度。

金本位制包括“金币本位制”、“金块本位制”、“金汇兑本位制”,其中金币本位制是金本位制中较为典型的一种形式,因此通常金本位制就是金币本位制,即法律确定金铸币为本位币。

其主要特征在于:金币可以自由铸造;银行券可以自由兑换金币或黄金;黄金对外可以自由输入输出。

金本位制是一种相对稳定的货币制度,其相对稳定性表现为两方面:①国内流通中通货的币值对金币不发生贬值的现象;②在国外则是外汇行市的相对稳定。

1816年英国最早实行金本位制,其后西方其他国家也相继采用这一货币制度。

金本位制促进了各国商品生产与流通的快速发展,也促进了国际贸易与信用业的发展。

第一次世界大战后,金本位制的稳定性因素遭到破坏。

其原因在于:①金币自由铸造与自由流通的基础已受到削弱;②银行券自由兑换黄金的可能性也已受削弱;③黄金在国际上自由输出输入受到限制。

这就导致许多国家先后放弃了作为典型金本位制的金币本位制。

在1924~1928年的战后相对稳定时期内,英国、法国、比利时、荷兰等经济实力较强的国家开始转而实行金块本位制,德国、意大利、奥地利等国则和一些殖民地、半殖民地国家改行金汇兑本位制。

直至1929~1933年世界性经济危机期间和以后,西方各国相继放弃各种金本位制,开始实施不兑现的信用货币制度。

2.最优货币区域(optimal currency area)答:最优货币区又称“最佳货币区”,指各有关国家通过实现国际贸易和生产要素流动的一体化而组成的最适合于相互间实行固定汇率的地区。

每一个实现了经济一体化的地区都可以成为一个最优货币区。

比如欧洲联盟各国经济一体化程度较高,适合于组成一个最优货币区。

最优货币区理论是有关固定汇率最适合于那些通过国际贸易和生产要素流动而实现一体化的地区的理论。

该理论由诺贝尔经济学奖获得者、美国经济学家蒙代尔于20世纪60年代初提出。

布兰查德《宏观经济学》课后习题及详解(预期、产出和政策)【圣才出品】

第17章 预期、产出和政策一、概念题1.总私人支出(aggregate private spending ,or private spending ) 答:总私人支出包括消费和投资两部分,表示为:。

总私人支出是收入的递增函数:收入越高,消费和投资越高;它是税收的递减函数:高税收使得消费下降;它是实际利率的递减函数:高实际利率使得投资下降。

2.动物精神(animal spirits )答:动物精神又称为“血气冲动”、“本能冲动”、“动物本能”、“创业冲动”,是指用来说明企业家作出投资决策时的心理状态,以及这种心理状态对投资的影响。

凯恩斯认为,企业家是否进行一项投资,并不是十分理性地进行冷静周密的计算后作出决定,而是一时“动物本能”的结果。

因此,投资是一种动物本能影响的活动。

私人投资不仅取决于企业家对未来投资收益的估算,而且还受到企业家一时一地的心理状态和情绪的影响。

以后,英国经济学家J.罗宾逊在分析投资问题时,也运用了动物本能这一概念。

3.适应性预期(adaptive expectations )答:适应性预期是一种预期形成理论,指对某一经济变量,不仅依据其现期的实际值,而且依据其现期实际值与在上一期对其做出的本期的估计值之间的误差,进行相应调整,得()()(),,,A Y T r C Y T I Y r ≡-+Y T r出对其未来估计值的预期。

适应性预期产生于20世纪50年代,是由菲利普·卡甘在一篇讨论恶性通货膨胀的文章中提出来的,很快在宏观经济学中得到广泛的应用。

适应性预期假定经济人根据以前的预期误差来修正以后的预期。

适应性预期模型的要点是预期变量依赖于该变量的历史信息。

某个时期的适应性预期价格等于上一时期预期的价格加上常数与上期价格误差(上个时期实际价格与预期价格之差)之和。

即预期价格是过去所有实际价格的加权平均数,权数是常数的函数。

适应性预期在物价较为稳定的时期能较好地反映经济现实。

布兰查德《宏观经济学》章节课后习题详解(财政政策:一个总结)【圣才出品】

第23章财政政策:一个总结一、概念题1.通货膨胀调整的赤字(inflation-adjusted deficit)答:赤字的正确度量结果有时称作经通货膨胀调整的赤字,是指用实际利息支付度量利息支付——实际利率乘以现有负债,而非事实上的利息支付——名义利率乘以现有负债。

官方用事实上的(名义)利息支付来度量赤字,是不正确的。

当通货膨胀很高时,官方的度量有很大的误导性。

2.周期调整的赤字(cyclically adjusted deficit)答:周期调整的赤字又称充分就业赤字、中周期赤字、标准就业赤字、结构性赤字,是指在现有的税收和支出规则下,如果产出处于自然率水平,赤字应该是多少。

这一方法提供了可以判断财政政策方向的简单基准:如果实际赤字很大,但周期调整的赤字等于零,那么随着时间的推移,当前的财政政策不会导致债务的系统性增加。

只要产出低于自然率水平,债务就会增加。

但是随着产出增加到自然率水平,赤字将会消失,债务将稳定。

3.政府预算约束(government budget constraint)答:政府预算约束可以简单表述为,第t年内政府债务的变化等于第t年的赤字。

B t-B t-1=赤字t。

上式中,B表示政府债务。

如果政府处于赤字状态,政府债务增加;如果政府处于盈余状态,政府债务减少。

4.自动稳定器(automatic stabilizer)答:自动稳定器指经济活动对赤字的影响,衰退自然导致赤字增加,而赤字增加本身有发挥财政扩张的作用,这将会部分地抵消衰退。

一些财政支出和税收制度就具有某种自动调整经济的灵活性,可以自动配合需求管理,减缓总需求的波动性,从而有助于经济的稳定。

在社会经济生活中,通常具有内在稳定器作用的因素主要包括:个人和公司所得税、失业补助和其他福利转移支付、农产品维持价格以及公司储蓄和家庭储蓄等。

例如,在萧条时期,个人收入和公司利润减少,政府所得税收入自动减少,从而相应增加了消费和投资。

布兰查德《宏观经济学》章节课后习题详解(金融市场和预期)【圣才出品】

第15章 金融市场和预期一、概念题1.收益,到期收益,或者n 年期债券的利率(yield to maturity or n-year interest rate ) 答:到期收益即到期收益率,是指投资者在二级市场上买入已经发行的债券并在持有到期满为止的期限内的年平均收益率。

以息票债券为例,假定某债券当前价格为P ,每年获得的利息支付为D ,债券第T 年到期时的面值为FV ,则到期收益率i 满足:()()()211111n nD D DFV P i i i i -=++++++++即到期收益率是使债券收益的贴现值等于债券价格时的利率。

n 年期债券的利率可以用到期收益率来衡量或表示。

2.违约风险(default risk )答:违约风险又称为信用风险,是指证券发行人在证券到期时无法还本付息而使投资者遭到损失的风险。

违约风险受发行人的经营能力、盈利水平、规模大小等因素影响。

违约风险对股票、债券均有影响,但对债券影响更大,因为债券是一种需要按约定时间还本付息的证券。

债券的违约风险从低到高依次为政府债券、地方政府债券、金融债券、公司债券。

3.期限(maturity )答:期限是债券期限的简称,指从债券发行一直到债券到期的时间间隔。

企业通常根据资金需求的期限、未来市场利率走势、流通市场的发达程度、债券市场上的其他债券的期限情况、投资者的偏好等多种因素来确定发行债券的期限结构。

各种债券有不同的偿还期限,短则几个月,长则几十年,根据偿还期限的不同,债券可分为长期债券、短期债券和中期债券。

一般来说,偿还期限在10年以上的为长期债券;偿还期限在1年以下的为短期债券;期限在1年或1年以上、10年以下(包括10年)的为中期债券;10年以上的为长期债券。

当资金需求量较大,债券流通较发达,利率有上升趋势时,可发行长期债券,否则,应发行短期债券。

4.收益曲线(yield curve)答:收益曲线是指反映债券收益与债券到期时间之间函数关系的曲线,是进行货币金融分析的有力工具。

布兰查德《宏观经济学》课后习题及详解(开放经济中的物品市场)【圣才出品】

第19章 开放经济中的物品市场一、概念题1.国内产品的需求(demand for domestic goods )答:在开放经济中,对国内产品的需求可表示为:其中,前面的三项——消费()、投资()和政府支出()——构成了产品的国内需求;是实际汇率,即用国内产品形式表示的国外产品的价格,因此就是用国内产品表示的进口价值;是出口价值。

部分为对国内产品的国内需求,X 是对国内产品的国外需求,两者相加即表示对国内产品的总需求。

2.产品的国内需求(domestic demand for goods )答:假定消费与可支配收入()正相关;投资与产出()正相关,与实际利率()负相关;政府支出()是给定的,暂时不考虑预期对影响支出的作用。

则产品的国内需求可以表示为:3.协调,七国集团(coordination ,G7)答:协调是指为了减少国际间的经济波动或金融动荡,政府间所进行的一系列谈判、合/Z C I G IM X ε≡++-+C I G ε/IM εX /C I G IM ε++-Y T -Y r G ()()()(),国内需求 C I G C I GY T Y r =++=++-++-,作、妥协的过程。

从实际情况看,由于各国间的利益冲突,国家间的宏观协调非常有限。

这可能有以下原因:①协调就意味着一些国家可能比其他国家贡献得更多,但它们可能并不愿意这样做。

②假定只有一些国家处于衰退中,那些并没有处于衰退之中的国家可能就不愿意提高它们自己的需求;但是如果它们不这么做,那些扩张的国家相对于不扩张的国家就可能会出现贸易赤字。

③假定一些国家已经有巨大的贸易赤字。

这些国家可能就不愿意削减税收或者进一步提高支出,因为这样会更加提高它们的贸易赤字。

它们会要求其他国家作出更多的调整,然而其他的国家可能并不愿意这么做。

④各个国家都会承诺协调,然后并不实现其诺言。

一旦所有的国家都同意提高支出,那么,每一个国家都会有不实行的动机,以从其他国家的需求提高中获益,从而改善其贸易状况。

《宏观经济学》课后答案(布兰查德版)

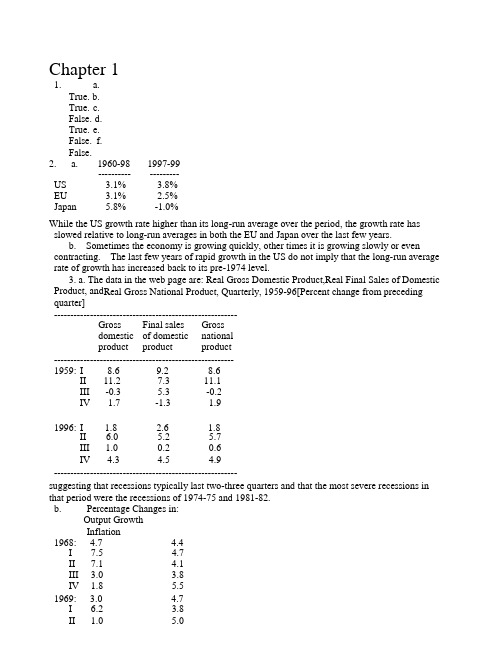

Chapter 11. a.True. b.True. c.False. d.True. e.False. f.False.2. a. 1960-98 1997-99-------------------US 3.1% 3.8%EU 3.1% 2.5%Japan 5.8%-1.0%While the US growth rate higher than its long-run average over the period, the growth rate has slowed relative to long-run averages in both the EU and Japan over the last few years.b. Sometimes the economy is growing quickly, other times it is growing slowly or even contracting. The last few years of rapid growth in the US do not imply that the long-run average rate of growth has increased back to its pre-1974 level.3. a. The data in the web page are: Real Gross Domestic Product,Real Final Sales of Domestic Product, and Real Gross National Product, Quarterly, 1959-96[Percent change from preceding quarter]--------------------------------------------------------Gross Final sales Grossdomestic of domestic nationalproduct product product-------------------------------------------------------1959: I 8.6 9.2 8.6II11.27.311.1III-0.3 5.3-0.2IV 1.7-1.3 1.91996: I 1.8 2.6 1.8II 6.0 5.2 5.7III 1.00.20.6IV 4.3 4.5 4.9--------------------------------------------------------suggesting that recessions typically last two-three quarters and that the most severe recessions in that period were the recessions of 1974-75 and 1981-82.b. Percentage Changes in:Output GrowthInflation1968: 4.7 4.4I7.5 4.7II7.1 4.1III 3.0 3.8IV 1.8 5.51969: 3.0 4.7I 6.2 3.8II 1.0 5.0III 2.3 5.8IV-2.0 5.11970: 0.1 5.3I-0.7 6.0II0.6 5.7III 3.7 3.4IV-3.9 5.41971: 3.3 5.2I11.3 6.4II 2.3 5.5III 2.6 4.4IV 1.1 3.3If history simply repeats itself, the United States might have a short recession (lasting perhaps oneyear) accompanied by an acceleration in the rate of inflation by about one percentage point.4. a. Banking services, business services.b. Not only has the relative demand for skilled workers increased but the industries wherethis effect is the strongest are making up a greater fraction of the economy.5. 1. Low unemployment might lead to an increase in inflation.2. Although measurement error certainly contributes to the measured slowdown ingrowth, there are other issues to consider as well, including the productivity of newresearch and accumulation of new capital.3. Although labor market rigidities may be important, it is also important to consider thatthese rigidities may not be excessive, and that high unemployment may arise from flawed macroeconomic policies.4. Although there were serious problems with regard to the management of Asian financial systems, it is important to consider the possibility that the flight of foreign capital from thesecountries worsened the situation by causing a severe stock market crash and exchange rate depreciation.5. Although the Euro will remove obstacles to free trade between European countries,each country will be forced to give up its own monetary policy.* 6. a. From Chapter 1: US output 1997=$8b; Ch ina output 1996=$.84b. Note that China’s outputin 1997 is $(.84)*(1.09) b. Equating output for some time t in the future:8*(1.03)t=(.84*1.09)*(1.09)t8/(.84*1.09)=(1.09/1.03)t8.737=(1.058)tt =ln(8.737)/ln(1.058) H38yrsb. From Chapter 1: US output/worker in 1997=$29,800; China output/per worker in1996=$70029.8*(1.03)t=(.7*1.09)*(1.09)tt H65 yearsChapter 21. a. False.b. Uncertain: real or nominalGDP. c. True.d. True.e. False. The level of the CPI means nothing. Its rate of change tells us about inflation.f. Uncertain. Which index is better depends on what we are trying to measure—inflationfacedby consumers or by the economy as a whole.2. a. +$100; Personal ConsumptionExpenditures b. nochange:intermediategoodc. +$200 million; Gross PrivateDomesticFixedInvestmentd. +$200 million; Net Exportse. no change: the jet was already counted when it was produced, i.e., presumably whenDelta(or some other airline) bought it new as an investment.*3. a. Measured GDP increases by $10+$12=$22.b. True GDP should increase by much less than $22 because by working for an extra hour,you are no longer producing the work of cooking within the house. Since cooking within the house is a final service, it should count as part of GDP. Unfortunately, it is hard to measure the value of work within the home, which is why measured GDP does not include it.4. a. $1,000,000 the value of the silver necklaces.b. 1st Stage:$300,000.2ndStage:$1,000,00-$300,000=$700,000.GDP: $300,000+$700,000=$1,000,000.c. Wages: $200,000 + $250,000=$450,000.Profits: ($300,000-$200,000)+($1,000,000-$250,000-300,000)=$100,000+$450,000=$550,000.GDP:$450,000+$550,000=$1,000,000.5. a. 1998 GDP: 10*$2,000+4*$1,000+1000*$1=$25,0001999 GDP: 12*$3,000+6*$500+1000*$1=$40,000Nominal GDP has increased by 60%.b. 1998 real (1998) GDP: $25,0001999 real (1998) GDP: 12*$2,000+6*$1,000+1000*$1=$31,000Real (1998) GDP has increased by 24%.c. 1998 real (1999) GDP: 10*$3,000+4*$500+1,000*$1=$33,0001999 real (1999) GDP: $40,000.Real (1999) GDP has increased by 21.2%.d. True.6. a. 1998 base year:Deflator(1998)=1; Deflator(1999)=$40,000/$31,000=1.29Inflation=29%b. 1999 base year:Deflator(1998)=$25,000/$33,000=0.76; Deflator(1999)=1Inflation=(1-0.76)/0.76=.32=32% c. Yes7. a. 1998 real GDP = 10*$2,500 + 4*$750 + 1000*$1 = $29,0001999 real GDP = 12*$2,500 + 6*$750 + 1000*$1 = $35,500b. (35,500-29,000)/29,000 = .224 = 22.4%c. Deflator in 1998=$25,000/$29,000=.86Deflator in 1999=$40,000/$35,500=1.13Inflation = (1.13 -.86)/.86 = .314 = 31.4%.8. a. The quality of a routine checkup improves over time. Checkups now may includeEKGs, for example. Medical services are particularly affected by this problem due toconstant improvements in medical technology.b. You need to know how the market values pregnancy checkups with and withoutultra-sounds in that year.c. This information is not available since all doctors adopted the new technologysimultaneously. Still, you can tell that the quality adjusted increase will be lower than20%.*9. a. approximately 2.5% b. 1992 real GDP growth: 2.7%;unemployment rate Jan 92: 7.3%; unemployment rate Jan 93: 7.3%Supports Okun's law because the unemployment rate does not change when the growth rate of real GDP is near 2.5% c. -2 percentage points change in the unemployment rate; 5percent GDP growth d. The growth rate of GDP must increase by 2.5 percentage points.Chapter 31. a. True.b. False. Government spending was 18% if GDP without transfers.c. False. The propensity to consume must be less than one for our model to be welldefined.d.True.false.f. False. The increase in output is one times the multiplier.2. a. Y=160+0.6*(Y-100)+150+150 0.4Y=460-60 Y=1000b. Y D=Y-T=1000-100=900c. C=160+0.6*(900)=7003. a. No. The goods market is not in equilibrium. Frompart 2a, Demand=1000=C+I+G=700+150+150b. Yes. The goods market is in equilibrium.c. No. Private saving=Y-C-T=200. Public saving =T-G=-50. National saving (or inshort, saving) equals private plus public saving, or 150. National saving equalsinvestment.4. a. Roughly consistent. C/Y=700/1000=70%; I/Y=G/Y=150/1000=15%.b. Approximately -2%.c. Y needs to fall by 2%, or from 1000 to 980. The parameter c0needs to fall by20/multiplier,or by 20*(.4)=8. So c0needs to fall from 160 to 152.d. The change in c0(-8) is less than the change in GDP (-20) due to the multiplier.5. a. Y increases by 1/(1-c1) b. Y decreases by c1/(1- c1)c. The answers differ because spending affects demand directly, but taxes affectdemand through consumption, and the propensity to consume is less than one.d. The change in Y equals 1/(1-c1) - c1/(1- c1) = 1. Balanced budget changes in G and Tare not macroeconomically neutral.e. The propensity to consume has no effect because the balanced budget tax increase abortsthe multiplier process. Y and T both increase by on unit, so disposable income, and hence consumption, do not change.*6. a. The tax rate ilessthanone.b.Y=c0+c1Y D+I+G impliesY=[1/(1-c1+c1t1)]*[c0-c1t0+I+G]c. The multiplier = 1/(1-c1+c1t1) <1/(1- c1), so the economy responds less to changes inautonomous spending when t1is positive.d. Because of the automatic effect of taxes on the economy, the economy responds less tochanges in autonomous spending than in the case where taxes are independent of income. So output tends to vary less, and fiscal policy is called an automatic stabilizer.*7. a. Y=[1/(1-c1+c1t1)]*[c0-c1t0+I+G] b. T = c1t0+ t1*[1/(1-c1+c1t1)]*[c0-c1t0+I+G]c. Both Y and T decrease.d. If G is cut, Y decreases even more.Chapter 41.a.True.b.Fals.c.True.d.True.e.False.f.False.g.True.2. a. i=0.05: Money demand = $18,000; Bond demand = $32,000i=.1: Money demand = $15,000; Bond demand = $35,000b. Money demand decreases when the interest rate increases; bond demand increases. Thisis consistent with the text.c. The demand for money falls by 50%. d. The demand formoney falls by 50%.e. A 1% increase (decrease) in income leads to a 1% increase (decrease) in money demand.This effect is independent of the interest rate.3. a. i=100/$P B–1; i=33%; 18%; 5% when $P B=$75; $85; $95.b. Negative.c. $P B=100/(1.08) $934. a. $20=M D=$100*(.25-i) i=5%b. M=$100*(.25-.15)M=$105. a. B D= 50,000 - 60,000 (.35-i)An increase in the interest rate of 10% increases bond demand $6,000.b. An increase in wealth increases bond demand, but has no effect on money demand.c. An increase in income increases money demand, but decreases bond demand.d. When people earn more income, this does not change their wealth right away. Thus,they increase their demand for money and decrease their demand for bonds.6. a. Demand for high-powered money=0.1*$Y*(.8-4i)b. $100 b = 0.1*$5,000b*(.8-4i) i=15%c. M=(1/.1)*$100 b=$1,000 b M= M d at the interest derived in part b.6. d. If H increases to $300, falls to 5%.e. M=(1/.1)*$300 b=$3,000 b7. a. $16 is withdrawn on each trip to the bank.Money holdings—day one: $16; day two: $12; day three: $8; day four: $4.b. Average money holdings are $10.c. $8 dollar withdrawals; money holdings of $8; $4; $8; $4.d. Average money holdings are $6.e. $16 dollar withdrawals; money holdings of $0; $0; $0; $16.f. Average money holdings are $4.g. Based on these answers, ATMs and credit cards have reduced money demand.8. a. velocity=1/(M/$Y)=1/L(i)b. Velocity roughly doubled between the mid 1960s and the mid 1990s.c. ATMS and credit cards reduced L(i) so velocity increased.Chapter 51.a.Trub.Truc.Fal.d. False. The balanced budget multiplier is positive (it equals one), so the IS curve shiftsright.e. False.f. Uncertain. An increase in G leads to an increase in Y (which tends to increaseinvestment), but an increase in the interest rate (which tends to reduce investment).g. True.*2. Firms deciding how to use their own funds will compare the return on bonds to the return on investment. When the interest rate on bonds increases, they become more attractive, and firms are more likely to use their funds to purchase bonds, rather than to finance investment projects.a.Y=[1/(1-c1)]*[c0-c1T+I+G]The multiplier is 1/(1-c1).b. Y=[1/(1-c1-b1)]*[c0-c1T+ b0-b2i +G]The multiplier is 1/(1-c1-b1). Since the multiplier is larger than the multiplier in part a, the effect of a change in autonomous spending is bigger than in part a.c. Substituting for the interest rate in the answer to partb: Y=[1/(1-c1-b1+ b2d1/d2)]*[c0-c1T+ b0+(b2*M/P)/d2+G]The multiplier is 1/(1-c1-b1+ b2d1/d2).d. The multiplier is greater (less) than the multiplier in part a if (b1- b2d1/d2) is greater (less)than zero. The multiplier is big if b1is big, b2is small, d1is small, and/or d2is big, i.e., if investment is very sensitive to Y, investment is not very sensitive to i, money demand is not very sensitive to Y, money demand is very sensitive to i.4. a. The IS curve shifts left. Output and the interest rate fall. The effect on investmentis ambiguous because the output and interest rate effects work in opposite directions: the fall in output tends to reduce investment, but the fall in the interest rate tends to increase it.b. From 3c: Y=[1/(1-c1-b1)]*[c0-c1T+ b0-b2i +G]c. From the LM relation: i= Y*d1/d2–(M/P)/d2To obtain the equilibrium interest rate, substitute for Y from part b.d. I= b0+ b1Y- b2i= b0+ b1Y- b2Y* d1/d2+ b2(M/P)/d2To obtain equilibrium investment, substitute for Y from part b.e. Holding M/P constant, I increases with equilibrium output when b1>b2d1/d2.Since a decrease in G reduces output, the condition under which a decrease in G increases investment is b1<b2d1/d2.f. The interpretation of the condition in part e is that the effect on I from Y has to be lessthan the effect from i after controlling for the endogenous response of i and Y, determined by the slope of the LM curve, d1/d2.5. a. Y=C+I+G=200+.25*(Y-200)+150+.25Y-1000i+250Y=1100-2000ib.M/P=1600=2Y-8000i i=Y/4000-1/5c. Substituting b into a: Y=1000d. Substituting c into b: i=1/20=5%e. C=400; I=350; G=250; C+I+G=1000f. Y=1040; i=3%; C=410; I=380. A monetary expansion reduces the interest rate andincreases output. The increase in output increases consumption. The increase in output and the fall in the interest rate increase investment.g. Y=1200; i=10%; C=450; I=350. A fiscal expansion increases output and the interestrate. The increase in output increases consumption.h. The condition from problem 3 is satisfied with equality (.25=1000*(2/8000)), socontractionary fiscal policy will have no effect on investment. When G=100: i=0%;Y=800; I=350; and C=350.*6. a. The LM curve is flatb. Japan was experiencing a liquidity trap. c. Fiscal policy is more effective.7. a. Increase G (or reduce T) and increase M.b. Reduce G (or increase T) and increase M. The interest rate falls. Investment increases,since the interest rate falls while output remains constant.CHAPTER 61.a.Fals.b.Fals.c.Falsd.False.Truf.Falsg.Uncertaih.True.i. False.2. a. (Monthly hires+monthly separations)/monthly employment =6/93.8=6.4%b. 1.6/6.5=25%c. 2.4/6.5=37%. Duration is 1/.37 or 2.7 months.d. 4.9/57.3=9%.e. new workers: .35/4.9=7%; retirees: .2/4.9=4%.3. a and b. Answers will depend on when the page is accessed.c. The decline in unemployment does not equal the increase in employment, because thelabor force is not constant. It has increased over the period.4. a. 66%; 66%*66%*66%= 29%; (66%)6= 8%b. (66%)6= 8%c. (for 1998): 875/6210= .145. a. Answers will vary.b and c. Most likely, the job you will have ten years later will pay a lot more thanyour reservation wage at the time (relative to your typical first job).d. The later job is more likely to require training and will probably be a much harderjob to monitor. So, as efficiency wage theory suggests, your employer will be willing to pay a lot more than your reservation wage for the later job, to ensure low turnover and low shirking.6. a. The computer network administrator has more bargaining power. She is muchharder to replace.6. b. The rate of unemployment is a key statistic. For example, when there are manyunemployed workers it becomes easier for firms to find replacements. This reduces the bargaining power of workers.7. a. W/P=1/(1+ )=1/1.05=.95 b. Price setting: u=1-W/P=5%c. W/P=1/1.1=.91; u=1-.91=9%. The increase in the markup lowers the real wage.From the wage-setting equation, the unemployment rate must rise for the real wage to fall.So the natural rate increases.CHAPTER 71.a.Trub.Trc.Falsd.Fale.Truf.Falg.Fal2. a. IS right, AD right, AS up, LM up, Y same, i up, P upb. IS left, AD left, AS down, LM down, Y same, i down, P down3. a.WS PS AS AD LM IS Y i PShort run:up same up same up same down up upMedium run:up same up same up same down up upb.WS PS AS AD LM IS Y i PShort run:same up down same down same up down downMedium run:same up down same down same up down down4. a. After an increase in the level of the money supply, output and the interest-rate eventually return to the same level. However, monetary policy is useful, because it can accelerate the return to the natural level of output.b. In the medium run, investment and the interest rate both change with fiscal policy.c. False. Labor market policies, such as unemployment insurance, can affect the naturallevel of output.*5. a. Open answer. Firms may be so pessimistic about sales that they do not want to borrow at any interest rate.b. The IS curve is vertical; the interest rate does not affect equilibrium output.c. No change.d. The AD curve is vertical; the price level does not affect equilibrium output.e. The increase in z reduces the natural level of output and shifts the AS curve up. SincetheAD curve is vertical, output does not change, but prices increase. Note that output is above its natural level.f. The AS curve shifts up forever, and prices keep increasing forever. Output does notchange, and remains above its natural level forever.6. a. The natural level of output is Y n. Assuming that output starts at is naturallevel, P0= M0- (1/c)*Y nb. Assuming that P e=P0: Y = 2cM0-cP=2cM0-cP0-cdY+cdY nRecalling that Y n=c(M0-P0): Y= Y n+ (c/(1+c d))*M0c. Investment goes up because output is higher and the interest rate is lower.d. In the medium run, Y = Y ne. In the medium run, investment returns to its previous level, because output and the interestrate return to their previous levels.CHAPTER 81.a.Trb.Fac.Fad.Tre.Faf.Tr2. a. No. In the 1970s, we experienced high inflation and high unemployment. The expectations- augmented Phillips curve is a relationship between inflation and unemployment conditional on the natural rate and inflation expectations. Given inflation expectations,increases in the natural rate (which result from adverse shocks to labor market institutions—increases in z—or from increases in the markup—which encompass oil shocks) lead to an increase in both theunemployment rate and the inflation rate. In addition, increases in inflation expectations imply higher inflation for any level of unemployment and tend to increase the unemployment rate inthe short run (think of an increase in the expected price level, given last period’s price,in the AD-AS framework). In the 1970s, both the natural rate and expected inflation increased, so both unemployment and inflation were relatively high.b. No. The expectations-augmented Phillips curve implies that maintaining a rate ofunemployment below the natural rate requires increasing (not simply high) inflation. This is because inflation expectations continue to adjust to actual inflation.3. a. u n=0.1/2 =5%b. t=0.1-2*.03 = 4% every year beginning with year t.c. e= 0 and =4% forever. Inflation expectations will be forever wrong. This isunlikely.t td. ⎝ might increase because pe ople’s inflation expectations adapt to persistently positiveinflation. The increase in ⎝ has no effect on u n.e. 5= 4+.1-.06=4%+4%=8%For t>5, repeated substitution implies, t= 5+(t-5)*4%.So, 10=28%; 15=48%.f. Inflation expectations will again be forever wrong. This is unlikely.4. a. t= t-1+ 0.1 - 2u t= t-1+ 2%t=2%; t+1=4%; t+2=6%; t+3=8%.b. t=0.5 t+ 0.5 t-1+ 0.1 - 2u tor, t= t-1+ 4%4. c. t=4%; t+1=8%; t+2=12%; t+3=16%d. As indexation increases, low unemployment leads to a larger increase in inflation overtime.5. a. A higher cost of production means a higher markup.b. u n=(0.08+0.1⎧)/2; Thus, the natural rate of unemployment increases from 5% to 6% as⎧increases from 20% to 40%.6. a. Yes. The average rate of unemployment is down. In addition, the unemploymentrate is at a historical low and inflation has not risen.b. The natural rate of unemployment has probably decreased.7. An equation that seems to fit well is: t- t-1=6-u t, which implies a natural rate of approximately 6%.8. The relationships imply a lower natural rate in the more recent period. CHAPTER 91. F TT F FT TT2. a. The unemployment rate will increase by 1% per year when g=0.5%. Unemploymentwill increase unless the growth rate exceeds the sum of productivity growth and labor force growth.b. We need growth of 4.25% per year for each of the next four years.c. Okun’s law is likely to beco me: u t-u t-1=-0.4*(g yt-5%)3. a. u n= 5%b. g yt= 3%; g mt=g yt+ t= 11%c. u g yt g mtt-1:8%5%3%11%t:4%9%-7%-3%t+1:4%5%13%17%t+2:4%5%3%7%4. a. t- t-1= -(u t-.05)u t- u t-1= -.4*(g mt- t-.03)b. t=6.3%; u t=8.7%t+1=1%; u t+1=10.3%c. u=5%; g y=3%; =-3%;5. a. See text for full answer. Gradualism reduces need for large policy swings, with effectsthat are difficult to predict, but immediate reduction may be more credible and encourage rapid, favorable changes in inflation expectations. On the other hand, the staggering ofwagedecisions suggests that, if the policy is credible, a gradual disinflation is the optionconsistent with no change in the unemployment rate.b. Not clear, probably fast disinflation, depending on the features inc.5. c. Some important features: the degree of indexation, the nature of the wage-settingprocess, and the initial rate of inflation.*6. a. u n=K/2; sacrifice ratio=.5 b. t=10%; t+1=8%; t+2=6%; t+3=4%; t+4=2%c. 5 years; sacrifice ratio=(5 point years of excess unemployment)/(10 percentage pointreduction in inflation)=.5d. t=7.5%; t+1=4.125%; t+2=1.594%; 3 years of higher unemployment for a reduction of10%: sacrifice ratio=0.3 e. t+1f. Take measures to enhance credibility.7. a. Inflation will start increasing.b.It should let unemployment increase to its new, higher, natural rate.Chapter 101. TTTFFFTU2. a. Example: France: (1.042)48*5.150=$37.1 k.Germany: $43.4 k; Japan: $76.5 k; UK: $22.5 k; U.S.:$31.7k b. 2.4c. yes.3. a. $5,000b. 2,500 pesos c. $500d. $1,000e. Mexican standard of living relative to the U.S.—exchange rate method:1/10; PPP method: 1/54. a. Y=63b. Y doubles. c. Yes.d. Y/N=(K/N)1/2e. K/N=4 implies Y/N=2. K/N=8 implies Y/N=2.83. Output less than doubles.f. No.g. No. In part f, we are looking at what happens to output when we increasecapital only, not capital and labor in equal proportion. There are decreasing returns tocapital.h. Yes.5. The United States was making the most important technical advances. However, theother countries were able to make up much of their technological gap by importing thetechnologies developed in the United States, and hence, have higher technological progress.6.Convergence for the France, Belgium, and Italy; no convergence for the second set ofcountriesChapter 111. a. Uncertain. True if saving includes public and private saving. False if saving onlyincludes private saving.b. False.c.Uncert UTFFd2. a. No. (1) The Japanese rate of growth is not so high anymore. (2) If the Japanesesaving rate has always been high, then this cannot explain the difference between the rate of growth inJapan and the US in the last 40 or 50 years. (3) If the Japanese saving rate has been higher thanit used to be, then this can explain some of the high Japanese growth. The contribution of high saving to growth in Japan should, however, come to an end.3. After a decade: higher growth rate. After five decades: growth rate back to normal, higher level of output per worker.4. a. Higher saving. Higher output per workerb. Same output per worker. Higher output per capita.5.*YYYd. Y/N = (K/N)1/3e. In steady state, sf(K/N) = ™K/N, which, given the production function in part d,implies: K/N=(s/™)3/2f. Y/N =(s/™)1/2g. Y/N = 2h. Y/N = 21/26.* a. 1b. 1c. K/N=.35; Y/N=.71d. Using equation (11.3), the evolution of K/N is: 0.9, 0.82, 0.757. a. K/N=(s/(2™))2; Y/N=s/(4™) b. C/N=s(1-s)/(4™)c-e. Y/N increases with s; C/N increases until s=.5, then decreases. CHAPTER 121.TFTFTFTUF2. a. Lower growth in poorer countries. Higher growth in rich countries.b. Increase in R&D and in output growth.c. A decrease in the fertility of applied research; a (small) decrease in growth.d. A decrease in the appropriability of drug research. A drop in the development of newdrugs. Lower technological progress and lower growth.3. See discussion in section 12.2.4. Examples will vary. Weakening patent protection would accelerate diffusion, but mightalso discourage R&D.5. a. Year 1: 3000; Year 2: 3960b. Real GDP: 3300; output growth: 10%c. 20%d. Real GDP/Worker=30 in both years; productivity growth is zero.e. RealGDP:3990;outputgrowth:33%.f. -0.8%g. Proper measurement implies real gdp/worker=36.3 in year 2. With improper measurement, productivity growth would be 21 percentage points lower and inflation 21% points higher.6. a. Both lead to an initial decrease in growthb. Only the first leads to a permanent decrease in growth7. a. (K/(AN))*=(s/(™+g A+g N))2=1; (Y/(AN))*=(1)1/2; g Y/(AN)=0; g Y/N=4%; g Y=6%b. (K/(AN))=(4/5)2; (Y/(AN))*=(4/5); g Y/(AN)=0; g Y/N=8%; g Y=10%c. (K/(AN))=(4/5)2; (Y/(AN))*=(4/5); g Y/(AN)=0; g Y/N=4%; g Y=10%People are better off in case a. Given any set of initial values, the level of technology is the same in cases a and c, but the level of capital per effective worker is higher atevery point in time in case a. Thus, since Y/N=A*(Y/(AN))=A*(K/(AN))1/2, output per worker is always higher in case a.8. There is a slowdown in growth and the rate of technological progress in the modernperiod. Japan’s growth rate of technological progress is higher because it is catching upto the U.S. level of technology. Not all of the difference in growth rates of output per worker is attributable to the difference in rates of technological progress. A big part is attributable to the difference in rates of growth of capital per worker.9.* a. ProbablyaffectsA.Thinkofclimate.b.Affects H.c. Affects A. Strong protection tends to encourage more R&D but also to limit diffusion of technology.d. May affect A through diffusion.e. May affect K, H, and A. Lower tax rates increase the after-tax return on investment,and thus tend to lead to more accumulation of K and H and more R&D spending.f. If we interpret K as private capital, than infrastructure affects A—e.g., bettertransportation networks may make the economy more productive by reducing congestion time.g. Assuming no technological progress, lower population growth implies highersteady-state level of output per worker. Lower population growth leads to higher capital per worker. Ifthere is technological progress, there is no steady-state level of output per worker. In this case, however, lower population growth implies that output per worker will be higher at every point in time, for any given path of technology. See the answer to problem 7c.Chapter 131.FFTTTTTTF2. a. u=1-(1/(1+⎧))(A/A e)b. u=1-(1/(1+⎧))=4.8%c. No. Since wages adjust to expected productivity, an increase in productivityeventuallyleads to equiproportional increases in the real wage implied by wage setting and price setting, at the original natural rate of unemployment. So equilibrium can bemaintained without any change in the natural rate of unemployment.3.* a. P=P e(1+⎧)(A e/A)(Y/L)(1/A)b. AS shifts down. Given A e/A=1, an increase in A implies a fall in P, given Y. Thisoccurs because for a given level of Y, unemployment is higher, so wages are lower and so, in turn, is the price level.c. There is now an additional effect, a fall in A e/A. In effect, workers do not receive asmuchof an increase in wages as warranted by the increase in productivity. Compared to part b, nominal wages are lower, leading to a lower value of P given Y.4. Discussion question.5. a. Reduce the gap, if this leads to an increase in the relative supply of skilled workers.b. Reduce the gap, since it leads to a decrease in the relative supply of unskilled workers.c. Reduce the gap, since it leads to an increase in the relative supply of skilled workers.d. Increase the gap, if U.S. firms hire unskilled workers in Central America, since itreduces the relative demand for U.S. unskilled workers.6. a. Textiles production is moving to low wage countries.b. Possibly demographic changes, increased availability of child care outside the home,decline in labor supply for these positions.c. Technological progress.7. Discussion question.CHAPTER 14。

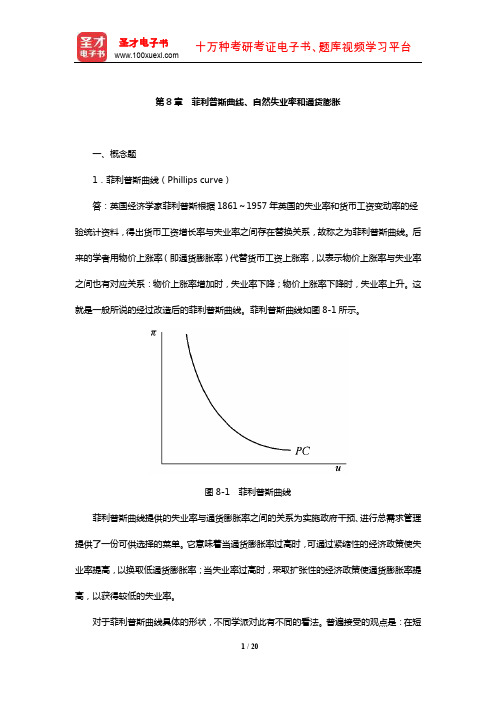

布兰查德《宏观经济学》章节课后习题详解(菲利普斯曲线、自然失业率和通货膨胀)【圣才出品】

第8章菲利普斯曲线、自然失业率和通货膨胀一、概念题1.菲利普斯曲线(Phillips curve)答:英国经济学家菲利普斯根据1861~1957年英国的失业率和货币工资变动率的经验统计资料,得出货币工资增长率与失业率之间存在替换关系,故称之为菲利普斯曲线。

后来的学者用物价上涨率(即通货膨胀率)代替货币工资上涨率,以表示物价上涨率与失业率之间也有对应关系:物价上涨率增加时,失业率下降;物价上涨率下降时,失业率上升。

这就是一般所说的经过改造后的菲利普斯曲线。

菲利普斯曲线如图8-1所示。

图8-1 菲利普斯曲线菲利普斯曲线提供的失业率与通货膨胀率之间的关系为实施政府干预、进行总需求管理提供了一份可供选择的菜单。

它意味着当通货膨胀率过高时,可通过紧缩性的经济政策使失业率提高,以换取低通货膨胀率;当失业率过高时,采取扩张性的经济政策使通货膨胀率提高,以获得较低的失业率。

对于菲利普斯曲线具体的形状,不同学派对此有不同的看法。

普遍接受的观点是:在短期内,菲利普斯曲线向右下方倾斜,而长期菲利普斯曲线是一条垂直线,表明在长期失业率与通货膨胀率之间不存在替换关系。

2.工资-价格螺旋(wage-price spiral)答:工资—价格螺旋又称为“工资—物价螺旋式上升”,是一种关于工资与物价相互促进而引起持续通货膨胀的理论。

给定预期价格,工人认为就是去年的价格,更低的失业导致更高的名义工资,更高的名义工资导致更高的价格,更高的价格导致更高的通货膨胀。

这一机制被称为工资—价格螺旋。

其作用机制为:(1)低失业引起更高的名义工资。

(2)作为对更高工资的反应,企业提高它们的价格,价格就升高了。

(3)作为对更高价格的反应,工人要求更高的名义工资。

(4)更高的名义工资致使企业进一步提高价格,最终价格进一步提升。

(5)作为对价格进一步提升的反应,在他们再次制定工资的时候,工人进一步要求更高的名义工资。

价格和工资之间的这种竞赛,导致持续的工资和价格膨胀。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第24章 货币政策:一个总结一、概念题1.通胀目标制(inflation targeting )答:通胀目标制指在许多国家,中央银行把他们的基本目标定为在短期和中期获得低通胀率。

它基于两个原则:第一个原则是货币政策的首要目标是保持通货膨胀稳定且较低。

第二个原则是达到这一目标的最好途径是遵循一个利率规则,这一规则保证被央行直接控制的利率能够对通胀和经济活动的变化做出反应。

2.利率规则(interest rate rule )答:利率规则指由于通胀不在中央银行的直接控制之下,而中央银行通过利率影响支出,为了实现通货膨胀目标制,中央银行应考虑直接选择利率而不是选择名义货币增长率。

泰勒提出了一个中央银行应该遵守的规则:**()()t t t n i i a b u u p p =+---上式中,πt 表示通胀率,以π*表示目标通胀率;i 表示名义利率,i*表示目标名义利率;以u t 表示失业率,u n 表示自然失业率。

如果通胀率等于目标通胀率(πt =π*),失业率等于自然失业率(u t -u n ),那么中央银行应该设定名义利率i 等于目标值i*。

这样,经济可以处于同一个轨道:通胀等于目标值,失业也等于自然率。

如果通胀高于目标值(πt >π*),中央银行应该将名义利率i t 增加到i*之上。

这一更高的利率将增加失业,失业的增加将导致通胀的降低。

3.大缓和(Great Moderation)答:大缓和指在2008年危机来临前,在采取通胀目标制的国家中,大部分国家的通货膨胀降低,保持较低和稳定的水平,产出波动振幅减小的时期。

大部分经济学家认为较好的货币政策是这“大缓和”的一个主要原因。

4.皮鞋成本(shoe-leather cost)答:皮鞋成本指在中期,较高的通胀率会导致较高的名义利率,从而使得持有货币的机会成本更高。

结果是人们更频繁地光顾银行去取钱所造成的成本。

如果通胀很低,人们就不会频繁光顾银行,而是做点别的事情,如更努力工作或享受更多的闲暇。

发生恶性通胀时,皮鞋成本可能变得非常大。

但是在通胀适中时,皮鞋成本的重要性会很有限。

如果现有的通胀率导致人们每月多光顾银行一次,或者在货币市场基金和可开支票存款账户间多进行一次交易,这几乎不能算是一个很大的成本。

5.税级攀升(bracket creep)答:税级攀升是指名义收入(而不是实际收入)增加了,人们就被推到更高的纳税等级。

尽管实际的资本收益率等于实际利率,不是名义利率,但应税所得却是名义利息收入,而不是实际利息收入。

与各种所得税率相对应的收入等级并没有随着通胀自动增加。

结果随着时间的推移,名义收入增加了,人们就被推到更高的纳税等级。

6.货币总量(monetary aggregates)答:货币总量指不仅包括货币还包括其他一些流动性资产的总和,其名字为M2、M3等。

在美国,M2——有时也称为广义货币——等于M1(货币和可开支票的存款)加上货币市场共同基金份额、货币市场储蓄存款(与货币市场基金份额相同,但是由银行发行而非由货币市场基金发行)、定期存款(这种存款的期限为几个月至几年,且提前取款要收罚金)之和。

7.广义货币(M 2)[(broad money (M 2))]答:M 2指不仅包括货币还包括其他一些流动性资产的总和。

在美国,广义货币(M 2)等于M 1(货币和可开支票的存款)加上货币市场共同基金份额、货币市场储蓄存款(与货币市场基金份额相同,但是由银行发行而非由货币市场基金发行)、定期存款(这种存款的期限为几个月至几年,且提前取款要收罚金)之和。

8.泰勒规则(Taylor rule )答:泰勒规则指为了实现通货膨胀目标制,中央银行应考虑直接选择利率而不是选择名义货币增长率,泰勒提出了一个中央银行应该遵守的规则:**()()t t t n i i a b u u p p =+---上式中,πt 表示通胀率,以π*表示目标通胀率;i 表示名义利率,i*表示目标名义利率;以u t 表示失业率,u n 表示自然失业率。

如果通胀率等于目标通胀率(πt =π*),失业率等于自然失业率(u t -u n ),那么中央银行应该设定名义利率i 等于目标值i*。

这样,经济可以处于同一个轨道:通胀等于目标值,失业也等于自然率。

如果通胀高于目标值(πt >π*),中央银行应该将名义利率i t 增加到i*之上。

这一更高的利率将增加失业,失业的增加将导致通胀的降低。

9.宏观审慎工具(Macro prudential tools )答:宏观审慎工具指根据情况的不同直接针对借款者、贷款者或银行及其他金融机构制定的规则。

在处理泡沫、信贷繁荣或金融系统的危险行为时,利率并不是一个恰当的政策工具。

利率是一个过于迟钝的工具,它能影响整个经济却不能立即解决手头的问题,正确的工具应该是宏观审慎工具。

10.贷款与房价比率[(loan-to-value ratio(LTV ratio))]答:贷款与房价比率指针对所购房屋的价值设定一个贷款上限,规定借款者所能借到款项的最大额度,这一贷款上限被称作最大贷款与房价比率,或最大LTV。

降低最大贷款和房价比率可能会减少需求,从而放缓房价增速。

11.巴塞尔新资本协议II、巴塞尔新资本协议III(Basel II,Basel III)答:《巴塞尔新资本协议II》指为了克服《巴塞尔协议》的局限性,巴塞尔银行监管委员会就新的资本协议发布了征求意见稿,这通常被称为《巴塞尔协议II》,它建立在三个支柱之上:①旨在将大型国际活跃银行的资本金要求与其实际风险更为密切地联系起来;②着重强调监管过程;③着重通过增加银行披露其风险敞口、准备金和资本金规模、控制银行的管理层、内部评级体系的有效性等信息的程度,强化市场纪律。

《巴塞尔新资本协议III》是1999年6月,该委员会提出的草案;2001年1月,公布了该草案第二稿;2003年4月,公布了第三次征求意见稿。

新协议草案以资本充足率、监管部门监督检查、市场纪律为三大要素,体现了银行业监管的发展趋势和方向,进一步强化了监管的标准和手段。

《巴塞尔新资本协议II》和《巴塞尔新资本协议III》规定了资本占所有资产比率的最小值,或资本占风险加权资产比率的最小值;其中,更高风险的资产具有更高的权重。

很多国家同意强制他们的银行执行相同的最小比率。

12.资本管制(capital controls)答:资本管制是国家政府机关等权力机构用来掌控资本从国家资本账户等的流进和流出,以及定向投资金额从国家或货币中的进出的一种货币政策工具。

资本管制从克林顿政府祈求通过国际社会的努力创建世界贸易组织(WTO)起变得越来越突出,最初是因为全球化已经提升了区域强势货币的加快速度,换句话说,给一些货币超出其自然地理界限的效用。

13.外商直接投资(foreign direct investment)答:外商直接投资是指以控制经营管理权为核心,以获取利润为目的,是与国际间接投资相对应的一种国际投资基本形式。

在我国外商直接投资指外国企业和经济组织或个人(包括华侨、港澳台胞以及我国在境外注册的企业)按我国有关政策、法规,用现汇、实物、技术等在我国境内开办外商独资企业、与我国境内的企业或经济组织共同举办中外合资经营企业、合作经营企业或合作开发资源的投资(包括外商投资收益的再投资),以及经政府有关部门批准的项目投资总额内企业从境外借入的资金。

二、计算与分析题1.运用本章学到的知识,判断以下陈述属于“正确”、“错误”和“不确定”中的哪一种情况?并解释。

a.支持OECD国家通胀率为正的最重要观点是铸币税。

b.因为M2的变动与通货膨胀非常密切,所以美联储应该以M2的增长为目标。

c.抵制通胀应该成为美联储的唯一目标。

d.因为大多数人都能够毫不费力地区分名义和实际价值,所以通货膨胀不会扭曲决策。

e.美联储在2012年初宣布了2%的通胀目标。

f.通胀率越高,有效的资本收益税率也越高。

g.泰勒规则描述了在萧条时期和繁荣时期央行是如何调整货币增速的。

h.央行唯一可使用的货币工具是利率和货币存量。

答:a.错误。

通货膨胀的好处还在于对宏观经济政策而言可以选择负的实际利率以及利用货币幻觉和通货膨胀的相互作用方便地调整实际工资。

在正常情况下,铸币税对于一国的财政收入是微乎其微的。

因此,铸币税不应该成为通胀为正的最重要证据。

b.错误。

首先,M2的增长和通胀之间的关系比M1的增长和通胀之间的关系要紧密,但是也不是非常的紧密。

其次,尽管联邦储备银行可以控制M1,但无法控制M2。

c.错误。

宏观经济政策的主要目标有四个:经济增长、充分就业(低失业)、物价稳定(低通货膨胀)和国际收支平衡。

联储利用货币政策改变实际利率会影响投资;短期内,可以影响产出、降低失业率;长期内,会影响经济的资本存量,因而影响经济的长期增长。

况且,《汉弗莱·霍金斯法案》(Humphrey-Hawkins Act)中规定要求联邦储备银行:保持货币和信用总量的长期增长与经济中产出增加的长期潜力相配合,以有效地促进就业最大化、价格稳定和适度长期利率的目标。

因此,美联储的目标有多个。

d.错误。

有足够的证据表明人们具有货币幻觉,这就意味着通胀会扭曲人们的决策。

e.正确。

美联储采用通货膨胀目标制,在2012年初,美联储宣布了2%通货膨胀目标。

f.正确。

因为资本收益税率并没有对通货膨胀指数化。

g.错误。

斯坦福大学的约翰·泰勒认为:由于中央银行通过利率影响支出,中央银行应。