管理会计作业

管理会计形考作业

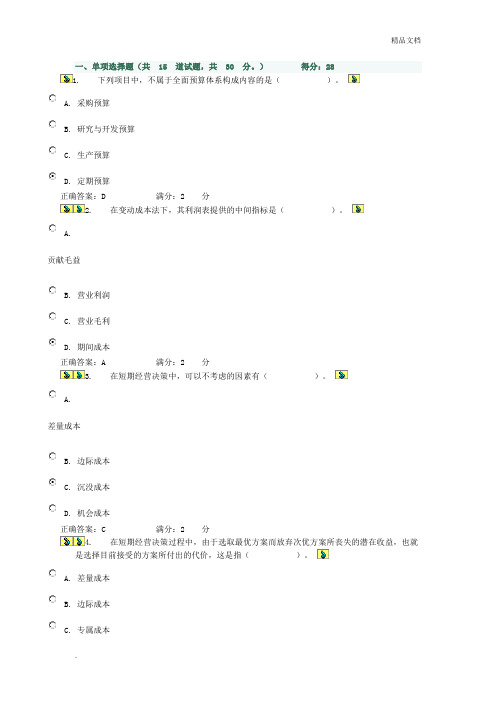

一、单项选择题(共15 道试题,共30 分。

)得分:281. 下列项目中,不属于全面预算体系构成内容的是()。

A. 采购预算B. 研究与开发预算C. 生产预算D. 定期预算正确答案:D 满分:2 分2. 在变动成本法下,其利润表提供的中间指标是()。

A.贡献毛益B. 营业利润C. 营业毛利D. 期间成本正确答案:A 满分:2 分3. 在短期经营决策中,可以不考虑的因素有()。

A.差量成本B. 边际成本C. 沉没成本D. 机会成本正确答案:C 满分:2 分4. 在短期经营决策过程中,由于选取最优方案而放弃次优方案所丧失的潜在收益,也就是选择目前接受的方案所付出的代价,这是指()。

A. 差量成本B. 边际成本C. 专属成本D. 机会成本正确答案:D 满分:2 分5. 广告费属于()。

A. 约束性固定成本B. 酌量性固定成本C. 技术性变动成本D. 酌量性变动成本正确答案:B 满分:2 分6. 通过成本性态分析,把企业全部成本最终分为()。

A. 变动成本和销售成本B. 固定成本和生产成本C. 变动成本和固定成本D. 销售成本和生产成本正确答案:C 满分:2 分7. ()是指由于存货供应中断而造成的损失,包括停工待料损失、商品存货不足而失去的创利额与企业信誉以及紧急订货增加的成本等。

A. 缺货成本B. 订货成本C. 储存成本D. 购置成本正确答案:A 满分:2 分8.“管理会计”被正式命名的年份是()。

A. 1922年B. 1952年C. 1966年D. 1982年正确答案:B 满分:2 分9. 在销售量不变的情况下,保本点越高,能实现的利润()。

A. 越多B. 越少C. 不变D. 不确定正确答案:B 满分:2 分10. 在变动成本法下,标准成本卡不包括()。

A. 直接材料B. 直接人工C. 变动制造费用D.固定制造费用正确答案:D 满分:2 分11. 生产多品种产品企业测算综合保本销售额=固定成本总额÷()。

管理会计学作业题目

一、判断:1. 因为管理会计只为企业内部管理服务,因此与对外服务的财务会计有本质的区别。

()2. 管理会计的职能是客观的,但它所起到作用的大小却收到人的主观能动性的影响。

()3. 管理会计也称为内部会计,财务会计称为外部会计。

()4. 管理会计和财务会计是会计的两个毫无联系的体系。

()二、简答1. 管理会计的职能有哪些?2. 管理会计与财务会计的主要区别是什么?作业二一、判断1. 固定成本的水平通常以其总额来表示,而变动成本的水平则以其单位额来表示。

()2. 无论哪一种混合成本,实际上都可以将其分解为固定成本和变动成本。

()3. 无论是固定成本还是变动成本,只有在其相关范围内才能保留其特征。

()4. 成本性态是指在一定条件下成本总额与业务量之间的依存关系。

()二、计算分析题1. 已知:某企业的甲产品1-8月份的产量和总成本资料如下表所示:(1)采用高低点法进行成本形态分析。

(2)采用线性回归法进行成本性态分析。

一、判断题1. 在变动成本法下,固定性制造费用应当列作期间成本。

()2. 变动成本法下产品成本的具体项目有直接材料预算、直接人工和变动性制造费用。

()3. 在变动成本法下,固定生产成本与全部非生产成本都属于期间成本。

()4. 由于对固定性制造费用的处理不同,导致变动成本法确定的产品成本总额和单位产品成本比完全成本法的相应数值要低,而期间成本则相反。

()5. 无论在哪一种成本计算法下,非生产成本都被作为期间成本处理,必须在发生的当期全额计入利润表,所不同的只是计入利润表的位置或补偿的顺序上有差别。

()6. 当存货量不为零时,按变动成本法确定的存货成本必然小于完全成本法下的存货成本。

()二、计算分析题1. 已知:某企业本期有关成本资料如下:单位直接材料成本为10元,单位直接人工成本为5元,单位变动性制造费用为7元,固定性制造费用总额为4000元,单位变动性销售管理费用为4元,固定性销售管理费用为1000元。

《管理会计》作业试题

对外经贸大学继续教育学院夜大教育部2011---2012学年第一学期2010级会计专本《管理会计》作业二年级_______ 专业__________ 班级__________ 姓名__________ 学号______________一、单项选择题(1×15=15分)1.(D)是指一切成本都可以按其性态划分为固定成本和变动成本。

A.货币时间价值假设B.成本性态可分假设C.会计实体假设D.会计分期假设2.在相关范围内,不随产量变化而变化的成本是(A)A.固定成本B.单位固定成本C.半变动成本D.混合成本3.下列各种混合成本可以用模型y=a+bx表示的是(C)。

A.半固定成本B.延伸变动成本C.半变动成本D.阶梯式变动成本4.某企业只生产一种产品,单位售价6元,单位变动生产成本4元,单位变动销售和变动管理成本0.5元,销量500件,则其产品贡献边际为(B)元。

A.650B.750C.850D.9505.某产品的固定成本总额35000元,变动生产成本15元,变动非生产成本3元,产品的单位变动成本率30%,则该产品的保本量是(B)台。

A.50000B.834C.1000D.7786.下列各种销售预测方法中,没有考虑远近期销售业务量对未来销售状况会产生不同影响的方法是(B)。

A.移动平均法B.算术平均法C.加权平均法D.指数平滑法7.两个可供选择的方案之间预期成本的差异即是(C)。

A.边际成本B.变动成本C.差量成本D.机会成本8.某企业2008年生产某亏损产品的边际贡献总额为3000元,固定成本是1000元,假定2009年其他条件不变,但生产该产品的设备可对外出租,一年的增加收入为(B)元时,应停产该种产品。

A.2001B.3000C.1999D.29009.由于存货数量不能及时满足生产和销售的需要而给企业带来的损失称为(B)。

A.储存成本B.缺货成本C.采购成本D.订货成本10.计算一个项目的投资回收期,应考虑的因素有(C)。

管理会计作业1

管理会计作业1一、单项选择题1.下列选项中,( D )不是在管理会计初级阶段产生的。

A.变动成本法 B.经济增加值 C.本量利分析 D.预算控制2.管理会计的基本内容不包括( D )。

A.成本控制 B.经营预测 C.预算管理 D.成本核算3.现代企业会计的两大分支:除了财务会计还有( C )。

A.财务管理 B.预算会计 C.管理会计 D.成本会计4.管理会计的会计主体不包括( B )。

A.责任人 B.个别产品 C.总经理 D.个别部门5.下列哪个选项中不属于管理会计和财务会计的区别内容( D )。

A.会计主体不同 B.核算依据不同 C.法律效力不同 D.最终目标不同6.管理成本是对企业为了特殊管理目的而引入或建立的各类成本概念的总称。

管理成本的内容不包括( B )。

A.决策成本 B.预测成本 C.控制成本 D.责任成本7.通过成本性态的分析,把企业全部成本最终分为( B )。

A.变动成本和销售成本 B.变动成本和固定成本 C.固定成本和生产成本 D.销售成本和生产成本8.租赁费属于( A )。

A.酌量性固定成本 B.约束性固定成本 C.技术性固定成本 D.酌量性变动成本9.低坡式混合成本又称( A )。

A.半变动成本 B.半固定成本 C.延期变动成本 D.曲线式混合成本10.历史资料分析法是根据企业若干期成本与业务量的相关历史资料,运用数学方法进行数据处理,以完成成本习性分析任务的一种定量分析方法。

历史资料分析法不包括( A )。

A.直接分析法 B.高低点法 C.散布图法 D.回归直线法11.变动生产成本不包括以下哪个选项。

( C )A.直接人工 B.直接材料 C.制造费用 D.变动性制造费用12.在完全成本法下,其利润表所提供的中间指标是( B )。

A.贡献毛益 B.销售毛利 C.营业利润 D.期间成本13.如果某期按变动成本法计算的营业利润为8000元,该期产量为4000件,销售量为2000件。

《管理会计》各章节练习作业答案

《管理会计》各章节练习作业答案第一章练习题及答案二、多项选择题1、管理会计属于()。

A.现代企业会计B.经营型会计C.外部会计D.报账型会计E.内部会计2、管理会计的职能包括( )。

A.参与经济决策B.控制经济过程C.规划经营目标D.预测经济前景E.考核评价经营业绩3、( )属于现代管理会计的基本内容。

A.预测决策会计B.责任会计C.预算会计D.规划控制会计E.以上都是4、( )的出现标志管理会计的原始雏形的形成。

A.标准成本计算制度B.变动成本法C.预算控制D.责任考评E.以上都是5、下列项目中,属于在现代管理会计阶段产生和发展起来的有( )。

A.规划控制会计B.管理会计师职业C.责任会计D.管理会计专业团体E.预测决策会计6、下列项目中,可以作为管理会计主体的有( )。

A.企业整体B.分厂C.车间D.班组E.个人7、管理会计是( )。

A.活帐B.呆帐C.报账型会计D.外部会计E.经营型会计8、下列关于管理会计的叙述,正确的有( )。

A.工作程序性较差B.可以提供未来信息C.以责任单位为主体D.必须严格遵循公认会计原则E.重视管理过程和职工的作用9、可以将现代管理会计的发展趋势简单地概括为()A.系统化B.规范化C.职业化D.社会化E.国际化10、西方管理会计师职业团体主要从事的工作包括()A.组织纯学术研究B.组织专业资格考试C.安排后续教育D.制定规范和标准E.推广管理会计方法ABE、ABCDE、ABD、AC、BCDE、ABCDE、ADE、ABCE、ABCDE、BCDE第二章练习题及答案二、多项选择题1、成本按其核算的目标分类为( )。

A.质量成本B.未来成本C.责任成本D.业务成本E.历史成本2、固定成本具有的特征是( )。

A.固定成本总额的不变性B.单位固定成本的反比例变动性C.固定成本总额的正比例变动性D.单位固定成本的不变性E.固定成本总额变动性3、变动成本具有的特征是( )。

A.变动成本总额的不变性B.单位变动成本的反比例变动性C.变动成本总额的不变性D.变动成本总额的正比例变动性E.单位变动成本的不变性4、下列成本项目中,( )是酌量性固定成本。

管理会计作业

管理会计作业班级:1003401 小组成员:张丹刘照张铭王玉李倩齐莹一 单项选择1、某产品预计单位售价20元,单位变动成本12元,固定成本费用200万元,企业要实现600万元的目标利润,则企业完成的销售量至少应为( )万件。

A 、100 B 、75 C 、25 D 、40 2、下列说法正确的是( )A 、安全边际越小,企业发生亏损的可能性也越小B 、变动成本法所确定的成本数据符合通用会计报表编制的要求C 、平均报酬率是使投资项目的净现值等于零的贴现率D 、在终值与计息期一定的情况下,贴现率越高,则确定的现值越小 3、 根据产品的价值公式 CFV,下列哪种情况可能会导致产品的价值不发生改变( ) A 、成本提高 功能不变 B 、成本提高 功能提高C 、成本降低 功能提高D 、成本不变 功能降低4、管理者的业绩评价目标中不包括以下的哪项 ( ) A 、管理者的能力 B 、管理者的水平C 、管理者为公司创造的价值D 、管理者为实现企业目标所作的贡献5、下列各种销售预测方法中,没有考虑远近期销售业务量对未来销售状况会产生不同影响的方法是( )A 、移动平均法B 、算术平均法C 、加权平均法D 、指数平滑法 6、管理会计的服务侧重于( )A 、股东B 、外部集团C 、债权人D 、企业内部的经营管理 7、如果期末产品存货增加,采用变动成本法计算的税前净利润与采用完全成本法计算的税前净利润的关系是( )A 、两者相等B 、前者大于后者C 、前者小于后者D 、两者没有关系 8、下列决策方法中,能够直接揭示中选的方案比放弃的方案多获得的利润或少发生损失的方法是( )A 、单位资源贡献边际分析法B 、贡献边际总额分析法C 、差别损益分析法D 、相关损益分析法9、某投资项目,若使用10%作为贴现率,其净现值为250,用12%作为贴现率,其净现值为-120,该项目的内部报酬率为 ( )A 、8.65%B 、13.85%C 、11.35%D 、12.35%10、战略管理会计对投资方案的评价除了定量分析模型外,还应用了大量的( )方法。

管理会计第三章作业(有答案)

〔一〕单项选择题1. 采用变动本钱法计算产品本钱时,不包括以下〔D〕A. 直接材料B. 直接人工C. 制造费用D. 固定性制造费用2. 变动本钱法的根本原那么是将期间本钱全部作为当期费用来处理。

其主要依据在于〔D〕A. 期间本钱是不可控的,不应分配计入特定产品的本钱B. 期间本钱一般数量不大,假设将其计入产品本钱,会得不偿失C. 期间本钱的分配是主观,会导致错误的管理决策D. 无论是否生产,期间本钱都会发生,所以将其分配计入产品本钱,将当期经营活动的本钱递延是不适宜的3. 完全本钱法与变动本钱法下,产品本钱都包括〔D〕A. 直接材料、直接人工和直接费用B. 直接材料、直接人工和制造费用C. 固定性生产本钱D. 变动性生产本钱4. 某厂生产乙产品,当月生产6000件,每件直接材料20元,直接工资14元,变动性制造费用12元,全月发生的固定性制造费用12000元。

用完全本钱法计算的乙产品单位产品本钱为〔A〕元元元元5.以下说法正确的选项是〔B〕A.完全本钱法的存货计价必然高于变动本钱法的存货计价B.变动本钱法下,本期生产并销售的产品本钱中不包含固定性制造费用,但本期生产未销售的产品本钱中那么负担了一局部制造费用C.由于完全本钱法和变动本钱法定义的产品本钱不同,因此,两种方法计算的销售本钱必然不同,从而两种方法计算的税前利润必然是不同的D.变动本钱法下,当期扣除的固定性制造费用与产品销售量有关6.在下面哪种情况下,按完全本钱法所确定的净收益大于按变动本钱所确定的净收益?〔B〕A.本期生产量小于销售量B.本期生产量大于销售量C. 本期生产量等于销售量D.期末存货量小于期初存货量7.以下有关变动本钱法的说法不正确的选项是〔D〕A.能够提供各种产品盈利能力的资料,有利于管理人员的决策分析B.便于分清各部门的经济责任,有利于本钱控制C.便于正确进行不同期间的业绩评价D.大大增加了本钱核算的复杂程度和工作量8.如果完全本钱法的期末存货本钱比期初存货本钱多20000元,而变动本钱法的期末存货本钱比期初存货本钱多8000元,那么可断定两种本钱法的广义营业利润之差为〔B〕。

管理会计形成性考核册作业(一)参考答案

《管理会计形成性考核册》作业(一)参考答案一、名词解释(每个2分,计10分)1.1.成本性态,是指在一定条件下成本总额与特定业务量之间的依存关系,又称成本性态,是指在一定条件下成本总额与特定业务量之间的依存关系,又称为成本习性。

它有三个特点:⑴成本性态的相对性;⑵成本性态的暂时性;⑶成本性态的可能转化性。

性态的可能转化性。

2.2.相关范围,是指不会改变固定成本、变动成本性态的有关期间和业务量的特相关范围,是指不会改变固定成本、变动成本性态的有关期间和业务量的特定变动范围。

定变动范围。

3.3.固定成本,是指在一定相关范围内,其总额不随业务量发生任何数额变化的固定成本,是指在一定相关范围内,其总额不随业务量发生任何数额变化的那部分成本。

它有两个特点:⑴固定成本总额的不变性;⑵单位固定成本的反比例变动性。

变动性。

4.4.变动成本,在一定相关范围内,成本总额随业务量成正比例变化的成本。

它变动成本,在一定相关范围内,成本总额随业务量成正比例变化的成本。

它有两个特点:⑴变动成本总额的正比例变动性;⑵单位变动成本的不变性。

5.5.变动成本法,是指在组织成本计算过程中,以成本性态分析为前提条件,只变动成本法,是指在组织成本计算过程中,以成本性态分析为前提条件,只把变动生产成本作为产品成本的构成内容,而把固定生产成本和非生产成本作为期间成本,并按贡献式损益确定程序计量损益的一种成本计算模式。

二、单项选择题(每题2分,计20分)1A 2B 3C 4C 5B 6B 7A 8C 9C 10A三、多项选择题三、多项选择题((每题2分,计20分)1ABCDE 2ABD 3AB 4AB 5DE 6ADE 7AB 8ABC 9AD 10ABC四、简答题(每题2分,计6分)1、答:管理会计作为企业会计的内部会计系统,其工作的侧重点主要为企业内部管理服务,所以管理会计称为企业内部经营管理会计。

2、答:成本性态分析与成本按性态分类是管理会计两个既有联系又有区别的范畴。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

PROCESS COSTINGTRUE/FALSE1. Examples of industries that would use process costing include thepharmaceutical and semiconductor industry.Answer: True Difficulty: 1 Objective: 1 Terms to Learn: process-costing system2. The principal difference between process costing and job costing is that in jobcosting an averaging process is used to compute the unit costs of products orservices.Answer: False Difficulty: 2 Objective: 1 Terms to Learn: process-costing systemThe averaging process is used to calculate unit costs in process costing.3. Process-costing systems separate costs into cost categories according to thetiming of when costs are introduced into the process.Answer: True Difficulty: 2 Objective: 1 Terms to Learn: process-costing system4. Estimating the degree of completion for the calculation of equivalent units isusually easier for conversion costs than it is for direct materials.Answer: False Difficulty: 2 Objective: 1 Terms to Learn: equivalent unitsEstimating the degree of completion is easier for the calculation of directmaterials since direct materials can be measured more easily than conversioncosts.5. Process costing would be most likely used by a firm that producesheterogeneous products.Answer: False Difficulty: 1 Objective: 1 Terms to Learn: process costingProcess costing would be most likely used by a firm that produces homogeneous products.6. The last step in a process-costing system is to determine the equivalent units forthe period.Answer: False Difficulty: 2 Objective: 2 Terms to Learn: process costingThe last step in a process-costing system is to assign the costs incurred tocompleted units and to units in ending work in process.7. Equivalent units are calculated separately for each input.Answer: True Difficulty: 2 Objective: 3 Terms to Learn: equivalent units8. In a process-costing system, there is always a separate Work-in-Process accountfor each different process.Answer: True Difficulty: 2 Objective: 3 Terms to Learn: process costing9. Process-costing journal entries and job-costing journal entries are similar withrespect to direct materials and conversion costs.Answer: True Difficulty: 2 Objective: 4 Terms to Learn: process-costing system10. The accounting (for a bakery) entry to record the transfer of rolls from themixing department to the baking department is:Work in Process-Mixing DepartmentWork in Process-Baking DepartmentAnswer: False Difficulty: 2 Objective: 4 Terms to Learn: process-costing systemThe correct accounting entry is the opposite of the entry shown here.11. The weighted-average process costing method does not distinguish betweenunits started in the previous period but completed during the current period and units started and completed during the current period.Answer: True Difficulty: 2 Objective: 5 Terms to Learn: weighted-average process-costing method12. Equivalent units in beginning work in process + equivalent units of work donein the current period equals equivalent units completed and transferred out in the current period minus equivalent units in ending work in process.Answer: False Difficulty: 2 Objective: 5 Terms to Learn: equivalent unitsThe second part of the equation should be: equivalent units completed andtransferred out in the current period PLUS equivalent units in ending work inprocess.13. In the weighted-average costing method, the costs of direct materials inbeginning inventory are not included in the cost per unit calculation since direct materials are almost always added at the start of the production process.Answer: False Difficulty: 2 Objective: 5 Terms to Learn: weighted-average process-costing methodThe costs of the direct materials are included in the cost per unit calculation. 14. The weighted-average cost is the total of all costs entering the Work-in-Processaccount (whether they are from beginning work-in-process or from work started during the current period) divided by total equivalent units of work done to date.Answer: True Difficulty: 2 Objective: 5 Terms to Learn: weighted-average process-costing method15. The equivalent units are not needed in a weighted-average system, because allcosts are just averaged.Answer: False Difficulty: 2 Objective: 5 Terms to Learn: equivalent units, weighted-average process-costing method The equivalent units are needed in a weighted-average system, even though all costs are averaged.16. The cost of units completed can differ materially between the weighted averageand the FIFO methods of process costing.Answer: True Difficulty: 2 Objective: 5, 6 Terms to Learn: weighted-average process-costing method, first-in, first-out (FIFO) process-costing method17. The first-in, first-out (FIFO) process costing method assigns the cost of thepr evious accounting period’s equivalent units in beginning work-in-processinventory to the first units completed and transferred out of the process.Answer: True Difficulty: 2 Objective: 6 Terms to Learn: first-in, first-out (FIFO) process-costing method18. A distinctive feature of the FIFO process costing method is that the work doneon beginning inventory before the current period is averaged with work done in the current period.Answer: False Difficulty: 2 Objective: 6 Terms to Learn: first-in, first-out (FIFO) process-costing methodA distinctive feature of the FIFO process costing method is that the work doneon beginning inventory before the current period is kept separate from workdone in the current period.19. The FIFO process costing method merges the work and the costs of thebeginning inventory with the work and the costs done during the current period.Answer: False Difficulty: 2 Objective: 6 Terms to Learn: first-in, first-out (FIFO) process-costing methodFIFO only includes the work done during the current period.20. The first-in, first-out process-costing method assumes that units in beginninginventory are completed during the current accounting period.Answer: True Difficulty: 2 Objective: 6 Terms to Learn: first-in, first-out (FIFO) process-costing method MULTIPLE CHOICE21. Costing systems that are used for the costing of like or similar units of productsin mass production are called:a. inventory-costing systemsb. job-costing systemsc. process-costing systemsd. weighted-average costing systemsAnswer: c Difficulty: 1 Objective: 1 Terms to Learn: process-costing system22. Which of the following manufactured products would not use process costing?a. 767 jet aircraftb. 19-inch television setsc. Custom built housesd. Both a and c are correct.Answer: d Difficulty: 2 Objective: 1Terms to Learn: process-costing system23. Process costing should be used to assign costs to products when the:a. units produced are similarb. units produced are dissimilarc. calculation of unit costs requires the averaging of unit costs over all unitsproducedd. Either a or c are correct.Answer: d Difficulty: 2 Objective: 1 Terms to Learn: process-costing system24. Which one of the following statements is true?a. In a job-costing system, individual jobs use different quantities ofproduction resources.b. In a process-costing system each unit uses approximately the same amountof resources.c. An averaging process is used to calculate unit costs in a job-costingsystem.d. Both a and b are correct.Answer: d Difficulty: 2 Objective: 1 Terms to Learn: process-costing system25. Conversion costs:a. include all the factors of productionb. include direct materialsc. in process costing are usually considered to be added evenly throughoutthe production processd. Both b and c are correct.Answer: c Difficulty: 2 Objective: 1 Terms to Learn: process-costing system26. An example of a business which would have no beginning or ending inventorybut which could use process costing to compute unit costs would be a:a. clothing manufacturerb. corporation whose sole business activity is processing the customerdeposits of several banksc. manufacturer of custom housesd. manufacturer of large TVsAnswer: b Difficulty: 2 Objective: 1 Terms to Learn: process-costing system27. Which of the following statement(s) concerning conversion costs is correct?a. Estimating the degree of completion of direct materials in a partiallycompleted unit is usually easier to calculate than estimating the degree ofcompletion for conversion costs.b. The calculation of equivalent units is relatively easy for the textile industry.c. Estimates are usually not considered acceptable.d. Both (b) and (c) are correct.Answer: a Difficulty: 2 Objective: 1 Terms to Learn: process-costing system, equivalent units28. The purpose of the equivalent-unit computation is to:a. convert completed units into the amount of partially completed outputunits that could be made with that quantity of input.b. assist the business in determining ending inventory.c. convert partially completed units into the amount of completed outputunits that could be made with that quantity of input.d. Both b and c are correct.Answer: c Difficulty: 2 Objective: 3 Terms to Learn: equivalent units29. In a process-costing system, the calculation of equivalent units is used for calculating:a. the dollar amount of ending inventoryb. the dollar amount of the cost of goods sold for the accounting periodc. the dollar cost of a particular jobd. Both a and b are correct.Answer: d Difficulty: 1 Objective: 3 Terms to Learn: equivalent units30. When a bakery transfers goods from the Baking Department to the DecoratingDepartment, the accounting entry isa. Work in Process — Baking DepartmentWork in Process — Decorating Departmentb. Work in Process — Decorating DepartmentAccounts Payablec. Work in Process — Decorating DepartmentWork in Process — Baking Departmentd. Work in Process — Baking DepartmentAccounts PayableAnswer: c Difficulty: 2 Objective: 4 Terms to Learn: process-costing systemEXERCISES AND PROBLEMS31. There are basically two distinct methods of calculating product costs.Required:Compare and contrast the two methods.Answer:In job costing the job or product is a distinctly identifiable product or service.Each job requires (or can require) vastly different amounts of input. Job costing is usually associated with products that are unique or heterogeneous. Thus, each job requires different amounts of input, and they can require vastly differentamount of costs to finish. Job-costed products tend to be high cost per unit. Thus the costs of each (unique) job are important for planning, pricing, andprofitability.In process costing, the jobs or products are similar (or homogeneous). Each job usually requires the same inputs, and results in approximately the same costs per unit. The cost of a product or service is obtained by assigning total costs tomany identical or similar units. We assume each unit receives the same amount of direct material costs, direct manufacturing labor costs, and indirectmanufacturing costs. Unit costs are then computed by dividing total costs by the number of units.The principal difference between process costing and job costing is the extent of averaging used to compute unit costs. As noted above in job costing, individual jobs use different quantities of production resources; whereas in process costing, we assume that each job uses approximately the same amount of resources.Difficulty: 2 Objective: 1Terms to Learn: process-costing system32. Why do we need to accumulate and calculate unit costs in process costing (and also job costing)?Answer:We need to accumulate unit costs to:1. Budget (planning)2. Price3. Account for the costs1. Budgeting—To operate a successful business, we should prepare budgets,review the results, and make decisions as to how well our business is doing.Our business has formulated plans for the future. The resources we needfor the future (materials, conversion costs, facilities, etc.) will depend onour estimate of the resources we need to accomplish these goals. Animportant part of these estimates is the unit costs of the products we planto produce. These unit costs will tell us how many dollars we must acquireto accomplish our plans.2. Price— In order to be a profitable business, we must sell our product at aprice in excess of what it costs us to produce the product. Essential for thepricing decision is the cost per unit. We will also learn whether we can sella product at a profit.3. Accounting— During the course of the accounting period, we will beaccumulating costs. At the end of the accounting period, we must allocatethis pool of costs between the units that were transferred out and the goodsin ending inventory. Unit costs are essential for this purpose.Difficulty: 1 Objective: 1Terms to Learn: process-costing system33. The Zygon Corporation was recently formed to produce a semiconductor chipthat forms an essential part of the personal computer manufactured by a major corporation. The direct materials are added at the start of the production process while conversion costs are added uniformly throughout the production process.June is Zygon's first month of operations, and therefore, there was no beginning inventory. Direct materials cost for the month totaled $895,000, whileconversion costs equaled $4,225,000. Accounting records indicate that 475,000 chips were started in June and 425,000 chips were completed.Ending inventory was 50% complete as to conversion costs.Required:a. What is the total manufacturing cost per chip for June?b. Allocate the total costs between the completed chips and the chips inending inventory.Answer:a.Equivalent unit for conversion costs =425,000 completed + (50,000 x 0.5 completed) =425,000 + 25,000 = 450,000b. Completed units = $11.27 x 425,000 = $4,789,750Ending work in process = Direct materials = 50,000 x $1.88 = $ 94,000Conversion costs = 25,000 x $9.39 = 234,750 Total $328,750 Difficulty: 2 Objective: 2Terms to Learn: process-costing system, equivalent units34. Cedar Rapids Chemical placed 220,000 liters of direct materials into the mixingprocess. At the end of the month, 10,000 liters were still in process, 30%converted as to labor and factory overhead. All direct materials are placed inmixing at the beginning of the process and conversion costs occur evenly during the process. Cedar Rapids Chemical uses weighted-average costing.Required:a. Determine the equivalent units in process for direct materials andconversion costs, assuming there was no beginning inventory.b. Determine the equivalent units in process for direct materials andconversion costs, assuming that 12,000 liters of chemicals were 40%complete prior to the addition of the 220,000 liters.Answer:a. Direct materials:Beginning inventory 0 litersUnits started 220,000 litersEquivalent units 220,000 liters Conversion costs:Beginning inventory 0 litersUnits started 220,000 litersTo account for 220,000 litersUnits transferred out 210,000 litersEnding inventory 10,000 litersUnits transferred out 210,000 litersEnding inventory, 30% complete 3,000 litersEquivalent units 213,000 litersb. Direct materials:Completed and transferred out (210,000 + 12,000) 222,000 litersEnding inventory, 100% complete 10,000 litersEquivalent units 232,000 liters Conversion costs:Completed and transferred out 222,000 litersEnding inventory, 30% complete 3,000 litersEquivalent units 225,000 liters Difficulty: 2 Objective: 5Terms to Learn: weighted-average process-costing method, equivalent units共享知识分享快乐。